Medical Device Leak Testing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

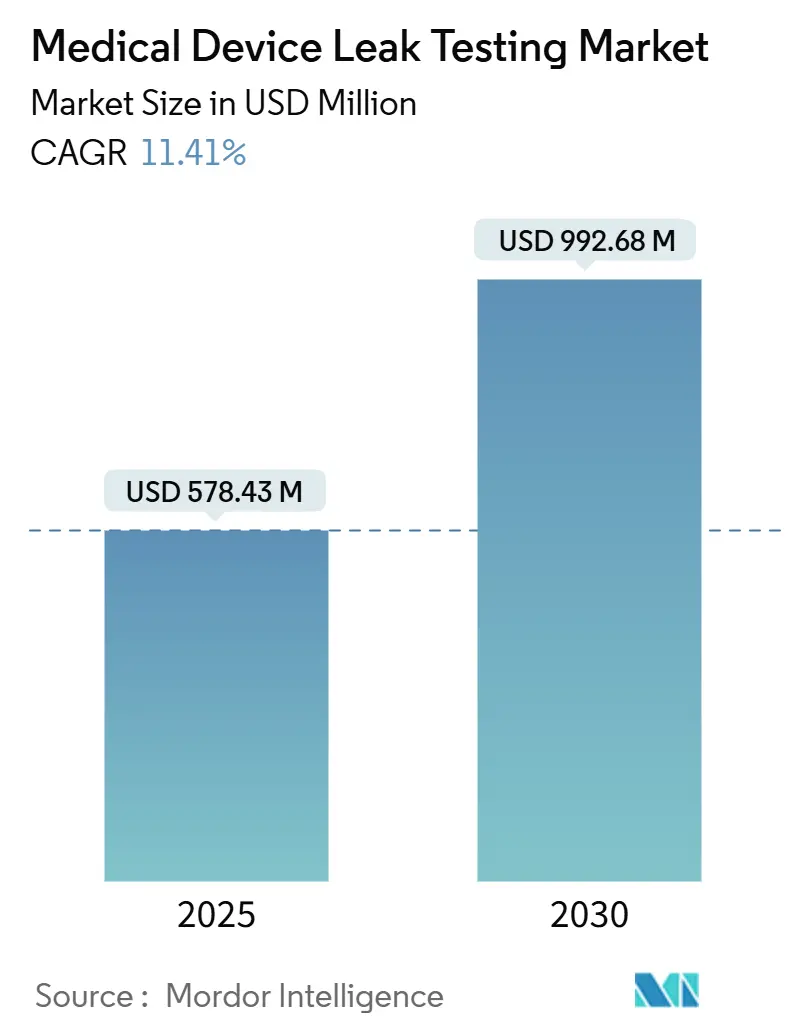

| Market Size (2025) | USD 578.43 Million |

| Market Size (2030) | USD 992.68 Million |

| Growth Rate (2025 - 2030) | 11.41% CAGR |

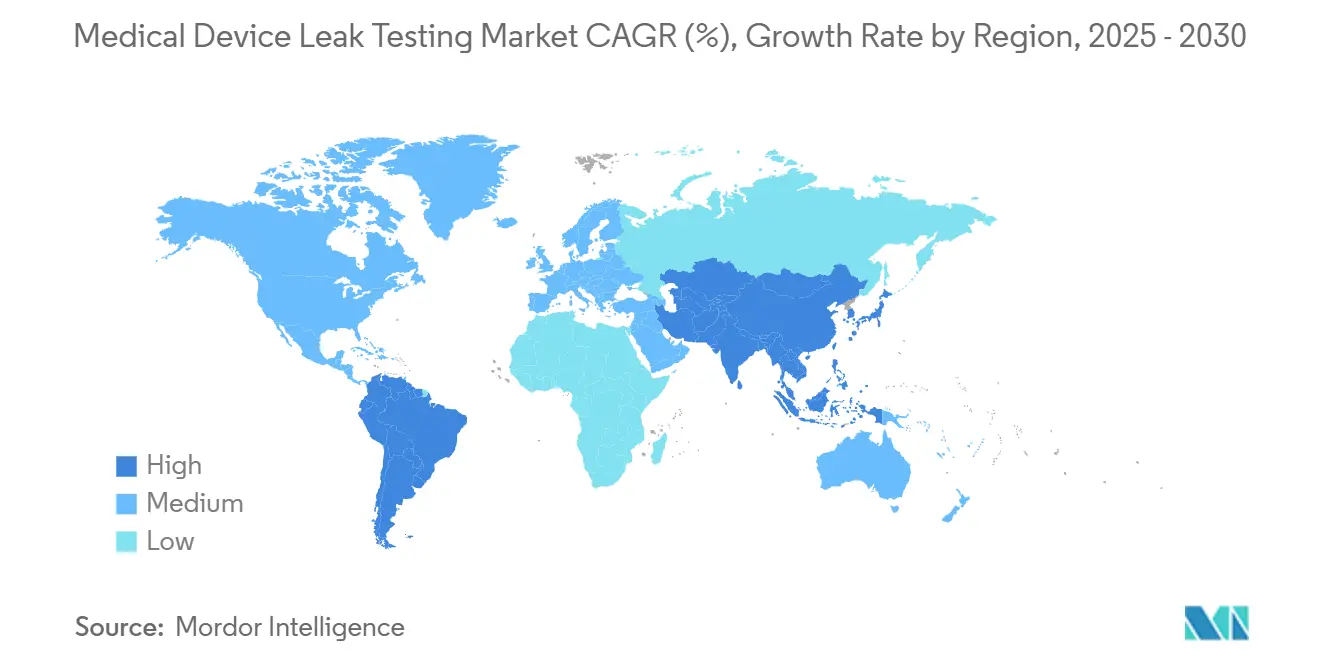

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

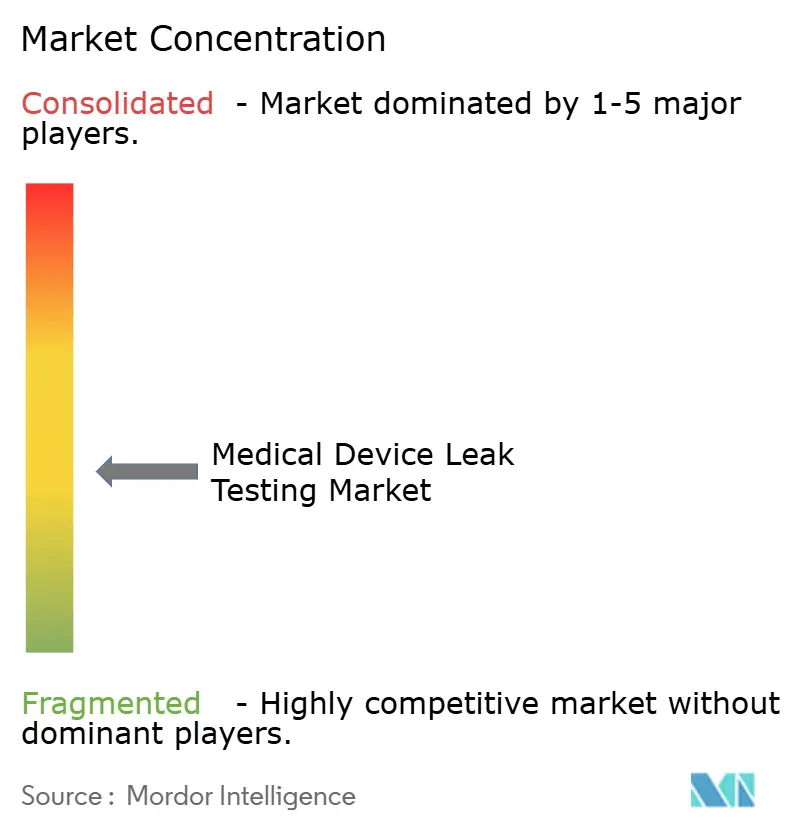

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Device Leak Testing Market Analysis by Mordor Intelligence

The medical device leak testing market reached USD 578.43 million in 2025 and is forecast to reach USD 992.68 million by 2030, reflecting an 11.41% CAGR over the period. This growth trajectory underscores the sector’s reaction to stronger global regulation, an industry-wide pivot toward deterministic Container Closure Integrity Testing (CCIT), and the expanding footprint of minimally invasive devices that demand tighter integrity verification. Heightened enforcement by the U.S. FDA and parallel rule-making in Europe and Asia have accelerated adoption of automated vacuum decay and helium mass-spectrometry systems, while helium scarcity simultaneously pushes laboratories toward cost-efficient hydrogen-nitrogen forming-gas testers. Competitive intensity has risen as equipment suppliers embed artificial-intelligence analytics, shorten cycle times, and bundle services to help manufacturers meet ISO 11607, ISO 10555, and USP 1207 mandates. Regional dynamics remain uneven—North America dominates in revenue, yet Asia-Pacific posts the most rapid gains on the back of localized manufacturing investments and improving regulatory harmonization.

Key Report Takeaways

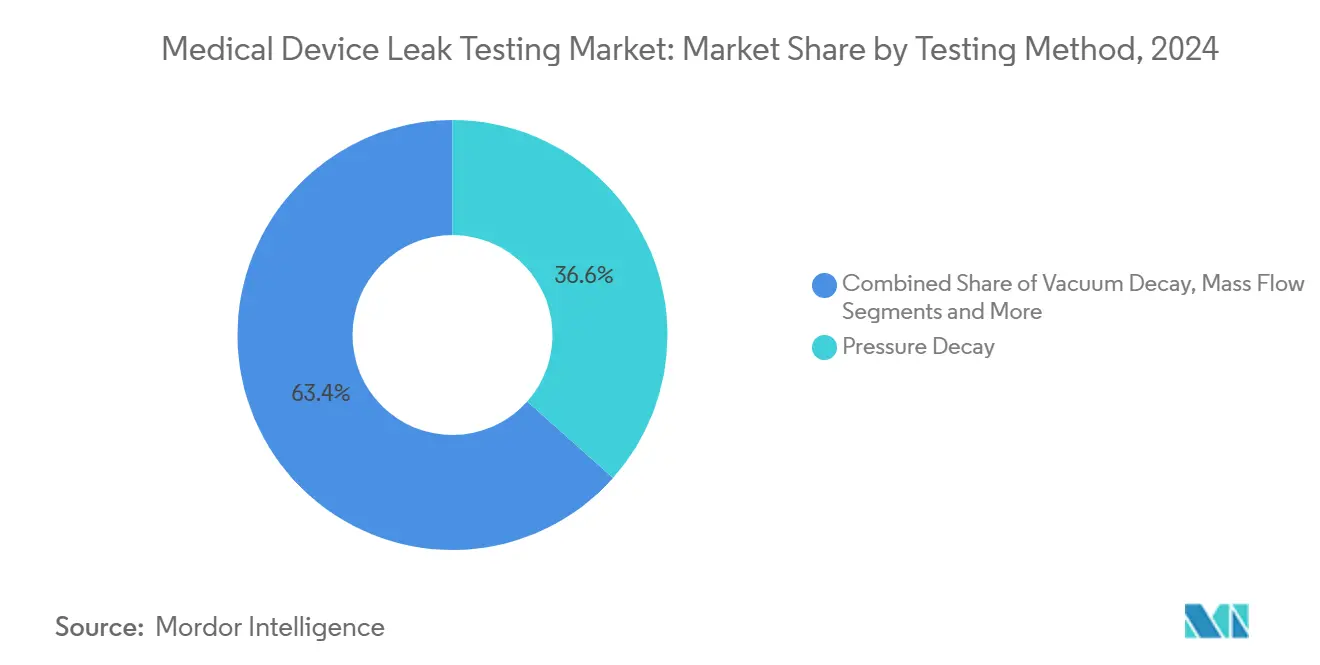

- By testing method, pressure decay captured 36.59% revenue share in 2024, while vacuum decay is on course for a 14.64% CAGR through 2030.

- By component, equipment accounted for 53.44% share of the medical device leak testing market size in 2024 and software & analytics is expanding at a 15.99% CAGR to 2030.

- By application, catheters and cannulas led with 24.58% of the medical device leak testing market size in 2024; packaging & container-closure systems are forecast to climb at a 15.77% CAGR through 2030.

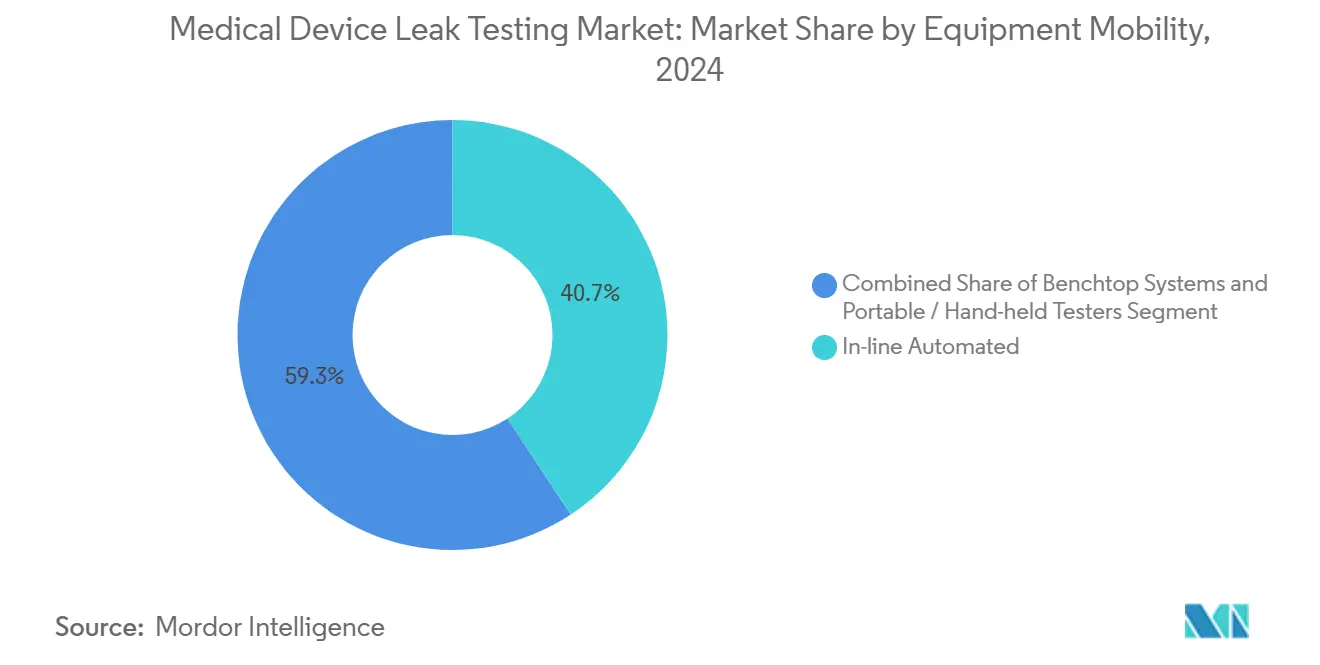

- By equipment mobility, in-line automated systems represented 40.74% of the medical device leak testing market share in 2024 and are expected to grow at a 15.27% CAGR up to 2030.

- By end user, medical device OEMs dominated with 61.57% share in 2024, whereas Testing, Inspection & Certification firms will post the fastest 14.38% CAGR to 2030.

- By geography, North America held 44.38% of the medical device leak testing market share in 2024; Asia-Pacific is projected to advance at a 13.58% CAGR to 2030.

Global Medical Device Leak Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory shift to deterministic CCIT | +2.8% | North America, EU lead; global rollout | Medium term (2-4 years) |

| Rising ISO 11607 & ISO 10555 scrutiny | +2.1% | Mature regulatory markets | Long term (≥ 4 years) |

| Surge in minimally invasive device output | +1.9% | APAC hubs, global OEMs | Medium term (2-4 years) |

| AI/ML-enabled predictive quality analytics | +1.6% | North America, EU trailblazers; APAC catching up | Long term (≥ 4 years) |

| Forming-gas testers offset helium shortage | +1.4% | Global, acute in helium-tight regions | Short term (≤ 2 years) |

| Automated in-line testers cut recalls | +1.3% | High-volume plants in APAC, Mexico, Eastern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Shift to Deterministic CCIT Under USP 1207

USP 1207’s insistence on quantitative, non-destructive leak detection forces manufacturers to retire dye ingress tests in favor of vacuum decay and helium mass-spectrometry. PTI’s VeriPac technology identifies 5-micron defects while preserving sterility, illustrating why deterministic methods now represent best practice for parenteral combination products and drug-device assemblies.[1]PTI Corporate Communications, “Vacuum Decay vs Dye Testing,” PTI-Inspection Systems, pti-ccit.com Adopters gain numeric leak-rate data that supports tighter statistical process control, lowers false-negative risk, and satisfies auditors. Early uptake in the United States and Western Europe sets the pace, but multinational OEMs are standardizing the same protocols across plants in Asia and Latin America, driving uniform capital spending on compliant systems.

Rising Regulatory Scrutiny & ISO 11607 / ISO 10555 Compliance

The 2023 amendments to ISO 11607-1 emphasize risk management in sterile barrier systems, while ISO 10555 revisions endorse non-destructive catheter testing with air-pressure and water-immersion correlation. Uson’s Sprint mD unit aligns with these updates by converting air-to-liquid leak-rate equivalencies in real time.[2]John Smith, “Understanding ISO 10555 Catheter Updates,” Uson, uson.com Global regulators increasingly demand machine-generated data logs, forcing suppliers to integrate Ethernet/IP connectivity and electronic signatures. As a result, procurement specs now mandate multi-parameter analytics, pushing the market beyond single-channel benches toward scalable, networked platforms that secure traceability across long supply chains.

Surge in Minimally Invasive Device Production (Catheters, Stents)

High-growth catheter and stent lines rely on ultra-thin walls, braided reinforcements, and multi-lumen geometries that amplify leak-detection difficulty. TE Connectivity’s expanded catheter component portfolio highlights this complexity and intensifies the need for sub-millibar sensitivity. OEMs migrate from bubble tests to differential-pressure systems able to discern micro-leaks without distorting delicate substrates. Production engineers favor programmable fixtures that accommodate personalized device dimensions, bolstering demand for flexible mass-flow or vacuum-decay solutions that cut cycle times yet uphold ISO 10555 tolerances.

AI/ML-Enabled Predictive Quality Analytics in Leak Testing

ETQ’s Reliance platform, paired with Acerta LinePulse, demonstrates how machine-learning models now parse sensor streams to predict drift, highlight abnormal patterns, and recommend pre-emptive maintenance. In leak-testing cells, algorithms flag rising residual pressures or helium-background noise before failures trigger recalls. Manufacturers gain lower test-piece scrap, reduced gage Repeatability & Reproducibility (R&R) variation, and expedited audit response. Integration momentum grows fastest in North America, but cost-down pressures ensure analogous rollouts in European and Asian satellite plants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of helium & tracer-gas systems | -1.8% | Regions with limited helium supply | Short term (≤ 2 years) |

| Shortage of skilled technicians | -1.2% | Aging workforces in North America & EU | Medium term (2-4 years) |

| Material diversity in micro-fluidic devices | -0.9% | High-tech hubs; microfluidics manufacturers | Long term (≥ 4 years) |

| Sustainability pressure on tracer gases | -0.7% | EU & North America environmental leaders | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Helium & Tracer-Gas Systems

Helium’s price spikes, triggered by the U.S. Federal Helium Reserve wind-down and geopolitical supply shocks, inflate test-cycle costs for micro-leak detection. Cincinnati Test Systems’ recovery rigs reclaim up to 95% of consumed helium, easing OPEX yet adding CAPEX pressure. Smaller firms postpone upgrades or pivot to forming-gas, but that switch necessitates method revalidation and regulatory submission updates, stretching timelines and budgets.

Shortage of Skilled Technicians for Complex Test Methods

Advanced helium-mass-spectrometry and AI-enhanced platforms require multidisciplinary competencies—vacuum physics, data science, and regulatory documentation. Retirements deplete know-how quicker than training pipelines can refill. Cincinnati Test Systems counters with modular e-learning and on-site certification, though ramp-up periods still extend project lead times. Skill scarcity drives OEMs toward outsourced TIC services, yet that shift introduces scheduling bottlenecks during regulatory audits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Testing Method: Vacuum Decay Gains Momentum

Vacuum decay and pressure decay together account for the largest slice of the medical device leak testing market size, with pressure decay leading at 36.59% revenue in 2024. Vacuum decay, however, is poised for the fastest 14.64% CAGR, propelled by its ability to detect smaller micro-defects at shorter cycle times, traits that align with USP 1207 deterministic requirements.

Manufacturers migrating to vacuum systems cite fewer temperature-drift artifacts and stronger repeatability, especially for sealed polymer pouches and IV bags. Helium-mass-spectrometry maintains dominance in ultra-critical applications such as implantable cardiac devices, yet its tracer-gas cost limits broader penetration. Hydrogen tracer and differential-pressure rise methods serve price-sensitive or high-throughput settings where detection limits above 1 sccm remain acceptable, illustrating the heterogeneous mix of solutions within the medical device leak testing market.

By Component: Software Analytics Drives Innovation

In 2024 equipment generated 53.44% of the medical device leak testing market share as OEMs upgraded benches, vacuum chambers, and mass-spectrometers. Software & analytics, although smaller in absolute value, is scaling at a 15.99% CAGR to 2030, underpinned by Industry 4.0 adoption and the infusion of AI dashboards that translate raw leak-rate data into actionable insights.

Cloud-enabled platforms stitch together test-records from multiple lines and geographies, feeding predictive models that pre-empt drift or gage wear. Services follow similar growth arcs as OEMs outsource calibration, validation, and training. Steady demand also persists for consumables—calibration orifices, leak standards, and tracer-gas cartridges—which constitute a resilient aftermarket revenue stream that stabilizes supplier margins within the medical device leak testing industry.

By Application/Device Type: Packaging Emerges as Growth Leader

Catheters and cannulas captured 24.58% of the medical device leak testing market size in 2024, a reflection of brisk minimally invasive procedure volumes and strict ISO 10555 expectations. Packaging and container-closure systems, however, are slated for the steepest 15.77% CAGR as drug-device combinations and parenteral nutrition bags become mainstream.

Regulatory bodies now scrutinize sterile-barrier performance across the product lifecycle, pushing manufacturers to adopt non-destructive vacuum decay in lieu of dye ingress. Implantables and drug-delivery pumps remain important niches, but growth is capped by lower production run rates. Respiratory circuits, endoscopes, and surgical instruments make incremental gains as hospitals demand rigorous reprocessing assurance to avoid hospital-acquired infections, reinforcing the breadth of use cases driving the medical device leak testing market.

By Equipment Mobility: In-Line Automation Dominates Growth

In-line automated platforms controlled 40.74% of the medical device leak testing market share in 2024 and will grow at a 15.27% CAGR, buoyed by throughput imperatives and shrinking takt-time expectations. These systems integrate directly into molding or assembly conveyors, enabling 100% inspection without human intervention.[3]Uson, “Sprint mD Multi-Channel Leak Tester,” Uson, uson.com

Benchtop units remain indispensable in R&D or pilot-line environments where flexibility outweighs speed. Portable testers satisfy field-maintenance of ventilators or dialysis machines, illustrating the niche but essential role of mobility. Still, as factories pivot to dark-plant concepts, in-line assets that funnel real-time leak data to enterprise-quality dashboards will capture expanding wallet share across the medical device leak testing market.

By End User: TIC Firms Capitalize on Outsourcing Trends

Medical device OEMs retained 61.57% control of the medical device leak testing market in 2024, yet they increasingly offload non-core verification tasks to Testing, Inspection & Certification providers, a segment racing ahead at 14.38% CAGR. FDA warnings on fraudulent third-party reports from certain overseas labs convinced many manufacturers to build hybrid strategies that blend internal audit labs with vetted TIC partners.

Contract Manufacturing Organizations serve mid-tier clients lacking capital for dedicated test bays, while research institutions adopt advanced benches for novel material exploration. Hospitals and clinics begin deploying point-of-care leak test carts for reusable endoscopes and ventilators, but the bulk of revenue still funnels through industrial settings tied to the production end of the medical device leak testing market.

Geography Analysis

North America generated the highest revenue, holding 44.38% of the medical device leak testing market share in 2024. Stringent FDA requirements and rapid uptake of deterministic CCIT equipment anchor this regional leadership. Ongoing helium-recovery investments and AI retrofits further reinforce the region’s premium positioning, while incendiary FDA comments on foreign data integrity stimulate reshoring of lab capacity. Canada leverages proximity and mutual-recognition agreements, whereas Mexico packages competitive labor costs with rising in-line automation demand.

Asia-Pacific is expanding fastest at a 13.58% CAGR through 2030 as China, India, and Southeast Asia scale catheter, stent, and infusion-set plants. Regulatory harmonization via ASEAN Medical Device Directive variants and India’s Medical Devices Rules fuels confidence, encouraging capex on pressure-decay rigs and software analytics per global templates. Japanese and South Korean firms adopt helium recovery earliest, and Taiwan’s electronics pedigree dovetails with AI-enabled quality dashboards, collectively lifting regional sophistication.

Europe maintains steady growth, bolstered by sustainability legislation that catalyzes helium-recovery adoption and forming-gas experimentation. Germany’s engineering base dominates high-precision vacuum chambers, the United Kingdom provides regulatory consultancy, and Nordic companies inject circular-economy ethos into procurement. Emerging EU directives on fluorinated gases spur R&D on environmentally benign tracer alternatives, guiding purchasing toward platforms that log carbon metrics alongside leak rates. Collectively, these continental developments cement Europe’s role as a sustainability pace-setter within the medical device leak testing market.

Competitive Landscape

The competitive environment remains moderately fragmented, leaving ample room for mid-tier innovators. ATEQ, Cincinnati Test Systems, and Uson lead in pressure-based technologies, while INFICON and Pfeiffer Vacuum dominate helium-mass-spectrometry. PTI and WILCO excel in vacuum-decay for pharmaceutical packages, and emerging software firms carve niches in AI analytics.

Strategic maps reveal vendors bundling cloud dashboards and training packages to counter hardware commoditization. Cincinnati Test Systems markets helium-recovery add-ons that deliver 2-year payback, while ATEQ promotes forming-gas benches that skirt volatile helium prices. Acquisition activity heats up: late-2024 saw INFICON acquire a European sensor start-up to bolster algorithmic sensitivity, and PTI partnered with a data-analytics firm to accelerate digital-twin simulations.

White-space opportunities concentrate in wearable-sensor housings, biodegradable polymer implants, and 3D-printed micro-fluidics—segments needing bespoke leak-test fixturing. Suppliers racing to embed machine-learning engines position themselves for differentiated margins, while slower rivals risk relegation to commodity status. Overall, the market balance favors agile firms that pair deterministic hardware with predictive-quality software, cementing long-term contracts across the medical device leak testing industry.

Medical Device Leak Testing Industry Leaders

ATEQ

Cincinnati Test Systems

Uson

InterTech Development Company

Cosmo Instruments

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Qaelon Medical and RevMedica announced a non-exclusive data partnership to improve stapler performance and surgical outcomes in gastrointestinal procedures.

- October 2024: ETQ rolled out the Reliance Predictive Quality Analytics suite, integrating AI analytics with Acerta LinePulse for real-time defect prevention.

- July 2024: Uson released guidance on ISO 10555 compliance, detailing air-pressure and water-immersion catheter leak-testing methods.

Global Medical Device Leak Testing Market Report Scope

| Pressure Decay |

| Vacuum Decay |

| Mass Flow |

| Helium/Mass Spectrometry |

| Bubble / Submersion |

| Others (H₂ tracer, differential pressure rise) |

| Equipment |

| Software & Analytics |

| Services (Calibration, Validation, TIC) |

| Consumables & Accessories |

| Catheters & Cannulas |

| Implantable Devices (Pacemakers, Stents) |

| Drug-Delivery & Infusion Systems |

| Respiratory & Ventilator Circuits |

| Endoscopes & Reusable Instruments |

| Packaging & Container-Closure Systems |

| Dialysis & IV Sets |

| Surgical Instruments & Tools |

| Benchtop Systems |

| Portable / Hand-held Testers |

| In-line Automated Systems |

| Medical Device OEMs |

| Contract Manufacturing Organisations (CMOs) |

| Testing, Inspection & Certification (TIC) Firms |

| Hospitals & Clinical Labs |

| Research Institutions |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Testing Method | Pressure Decay | |

| Vacuum Decay | ||

| Mass Flow | ||

| Helium/Mass Spectrometry | ||

| Bubble / Submersion | ||

| Others (H₂ tracer, differential pressure rise) | ||

| By Component | Equipment | |

| Software & Analytics | ||

| Services (Calibration, Validation, TIC) | ||

| Consumables & Accessories | ||

| By Application / Device Type | Catheters & Cannulas | |

| Implantable Devices (Pacemakers, Stents) | ||

| Drug-Delivery & Infusion Systems | ||

| Respiratory & Ventilator Circuits | ||

| Endoscopes & Reusable Instruments | ||

| Packaging & Container-Closure Systems | ||

| Dialysis & IV Sets | ||

| Surgical Instruments & Tools | ||

| By Equipment Mobility | Benchtop Systems | |

| Portable / Hand-held Testers | ||

| In-line Automated Systems | ||

| By End User | Medical Device OEMs | |

| Contract Manufacturing Organisations (CMOs) | ||

| Testing, Inspection & Certification (TIC) Firms | ||

| Hospitals & Clinical Labs | ||

| Research Institutions | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the medical device leak testing market in 2025 and what annual growth is expected through 2030?

Current value stands at USD 578.43 million and it is projected to grow at an 11.41% CAGR, reaching USD 992.68 million by 2030.

Which leak-testing technology is gaining the most momentum among manufacturers?

Vacuum decay systems are expanding fastest with a 14.64% CAGR because they deliver higher sensitivity and shorter cycle times while meeting deterministic CCIT guidelines.

Why are helium-based test methods facing pushback from device makers?

Global helium scarcity has raised operating costs; companies are switching to hydrogen-nitrogen forming-gas blends or installing helium-recovery units that can reclaim up to 95% of tracer gas.

What drives Asia-Pacific to be the fastest-growing region in leak testing?

Accelerated device manufacturing investments, regulatory harmonization, and the need for in-house verification following overseas data-integrity warnings are lifting regional demand by 13.58% CAGR.

How does AI improve leak-testing operations on the plant floor?

Machine-learning dashboards use live sensor streams to spot drift, predict maintenance needs, and cut false rejects, thereby preventing recalls and lowering scrap rates.

Which end-user group is expanding quickest in adopting leak-testing solutions?

Testing, Inspection & Certification firms are rising at a 14.38% CAGR as OEMs outsource specialized verification to manage regulatory complexity and focus on core production.

Page last updated on: