Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.35 Billion |

| Market Size (2031) | USD 2.81 Billion |

| Growth Rate (2026 - 2031) | 15.74% CAGR |

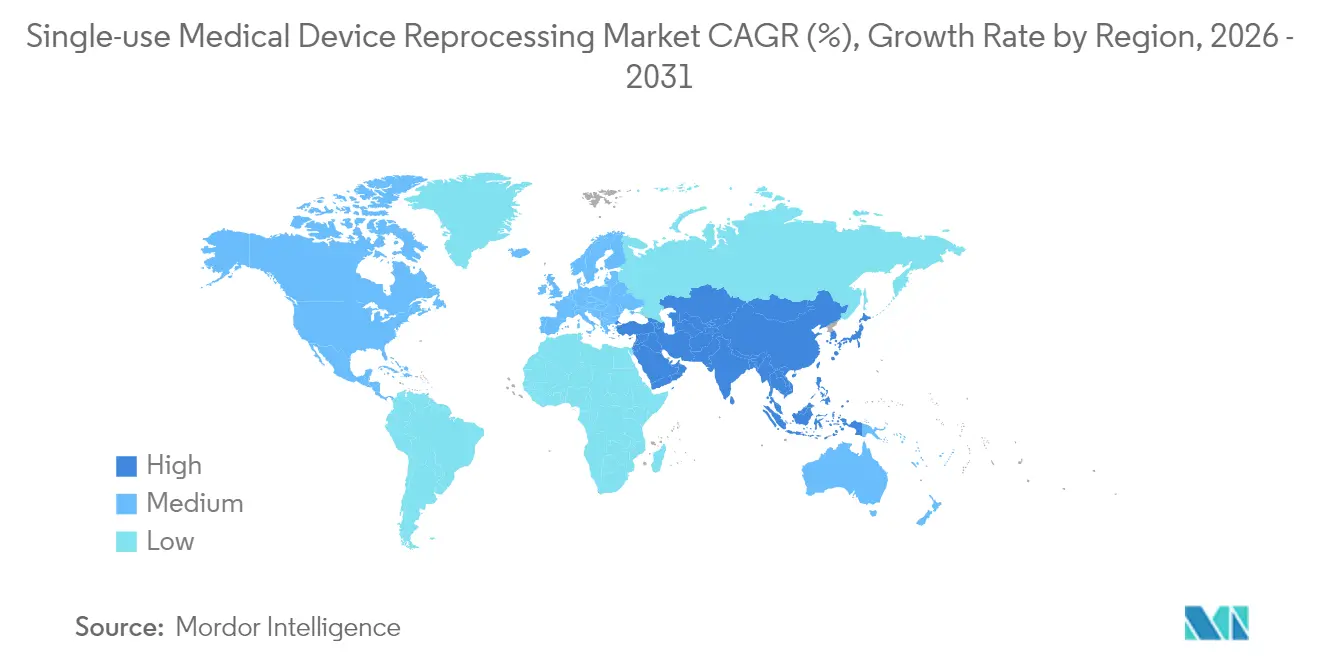

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Single-use Medical Device Reprocessing Market Analysis by Mordor Intelligence

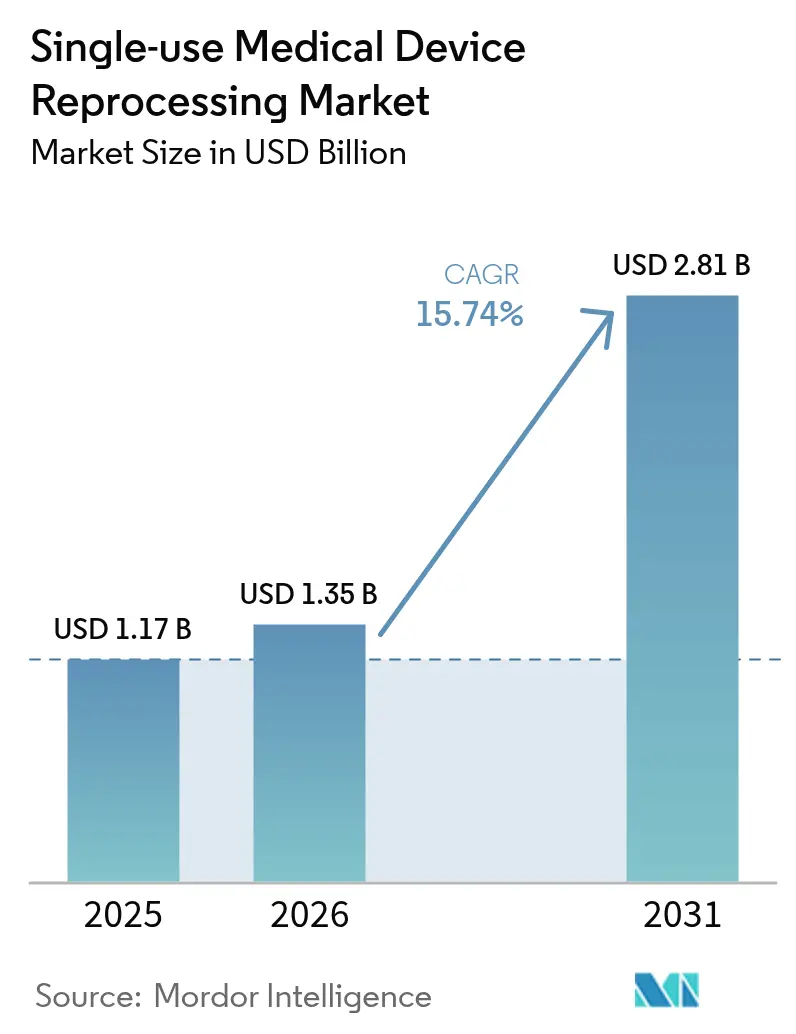

The single-use medical device reprocessing market size is expected to grow from USD 1.17 billion in 2025 to USD 1.35 billion in 2026 and is forecast to reach USD 2.81 billion by 2031 at 15.74% CAGR over 2026-2031. Regulatory clarity from the U.S. FDA’s May 2024 guidance on remanufacturing and growing acceptance of vaporized hydrogen peroxide sterilization have reduced compliance uncertainty and broadened the universe of devices considered safe for reprocessing[1]Source: U.S. Food and Drug Administration, “FDA Issues Final Guidance to Clarify ‘Remanufacturing’ of Devices,” fda.gov . Hospital procurement teams view reprocessing as a line-item lever for margin preservation amid inflation and reimbursement headwinds, especially after documented savings of USD 451 million in 2024 across 17 countries[2]Source: Dan Vukelich, “Earth Day News: Hospitals and Surgical Centers Save USD 451 Million,” amdr.org . Sustainability mandates, Scope-3 carbon accounting and antitrust enforcement against restrictive OEM contracts are accelerating device-level adoption, while AI-enabled traceability platforms and automated sterilizers reinforce patient-safety confidence .

Key Report Takeaways

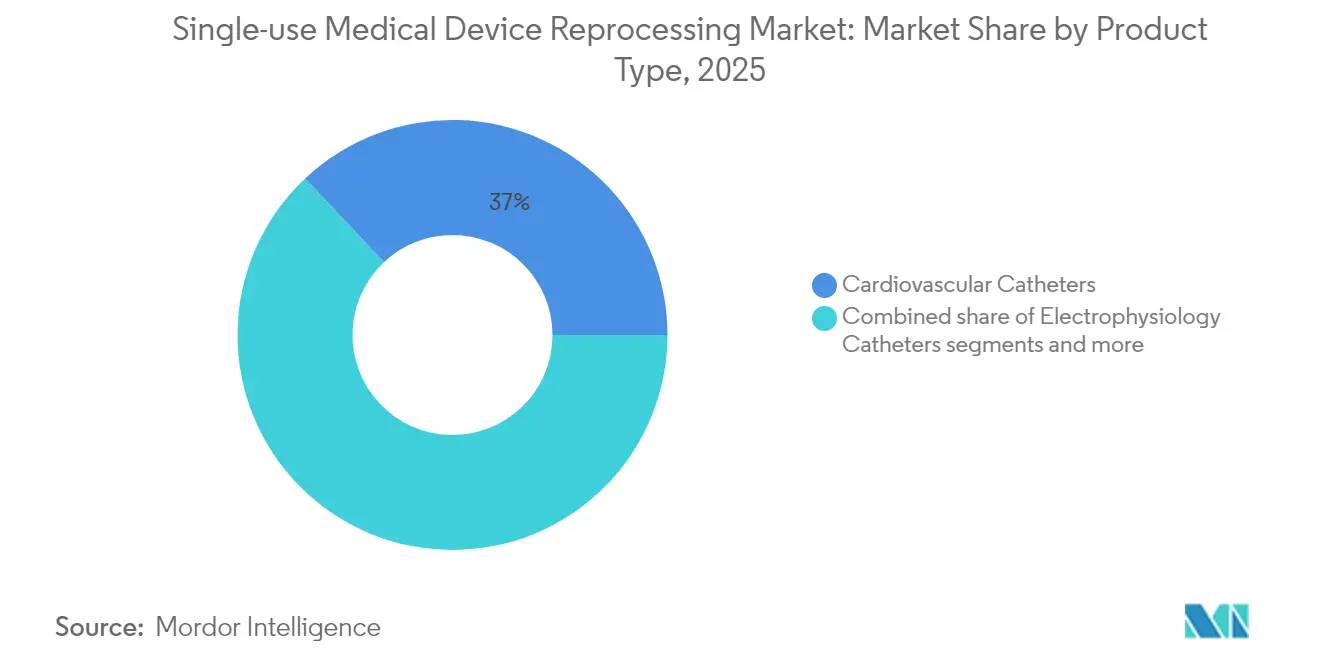

- By product type, cardiovascular catheters led with 37.02% of single-use medical device reprocessing market share in 2025; electrophysiology catheters are projected to register the fastest 15.92% CAGR through 2031 .

- By service provider, third-party commercial reprocessors held 84.12% of the single-use medical device reprocessing market size in 2025, while the segment is poised to expand at a 16.05% CAGR between 2026 and 2031 .

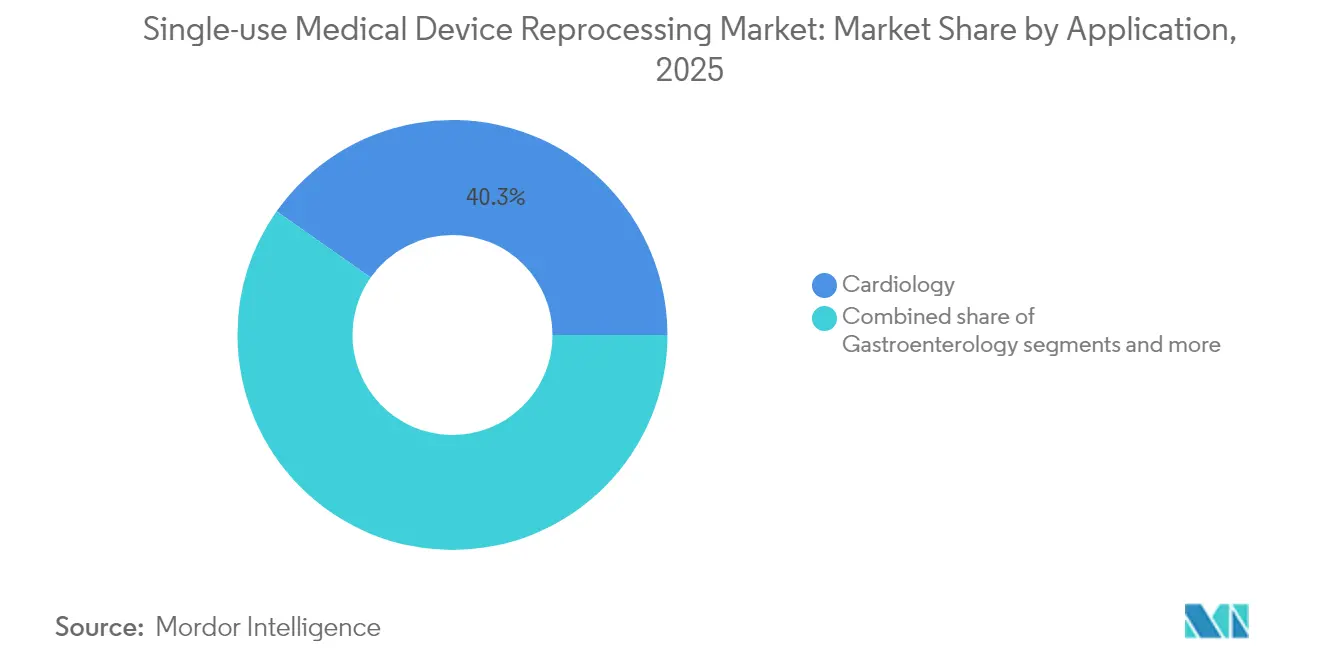

- By application, cardiology accounted for 40.25% share of the single-use medical device reprocessing market size in 2025; gastroenterology applications show the highest 16.28% CAGR outlook to 2031 .

- By end user, hospitals and surgical centers represented 63.75% demand in 2025, whereas ambulatory surgical centers are advancing at a 16.63% CAGR through 2031 .

- By geography, North America commanded 43.10% revenue in 2025, yet Asia-Pacific is forecast to expand the single-use medical device reprocessing market at 16.88% CAGR to 2031 .

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Single-use Medical Device Reprocessing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-containment pressure on hospitals | +4.2% | Global, with acute impact in North America & Europe | Medium term (2-4 years) |

| Regulatory approvals & clearances for reprocessed SUDs | +3.8% | North America & EU primary, expanding to APAC | Long term (≥ 4 years) |

| Sustainability & waste-reduction mandates | +2.9% | EU leading, North America following, APAC emerging | Long term (≥ 4 years) |

| ESG reporting tying Scope-3 emissions to procurement | +2.1% | Global corporate markets, concentrated in developed economies | Medium term (2-4 years) |

| Antitrust rulings curbing OEM restrictive contracts | +1.8% | North America primary, potential EU spillover | Short term (≤ 2 years) |

| Supply-chain resilience post-pandemic PPE shortages | +1.5% | Global, with emphasis on strategic stockpiling regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cost-containment Pressure on Hospitals

Shrinking operating margins have moved reprocessing from optional to essential in hospital supply-chain playbooks, often delivering 40-60% device-level savings versus OEM list prices . Medicare payment reforms and private-payer contracting heightened visibility of disposable device spend, prompting the Veterans Health Administration to revisit its own reprocessing restrictions in 2025 . Chief financial officers increasingly embed reprocessing ROIs in annual capital-allocation models, translating to systematic adoption across multi-hospital networks . The scale of savings is now material to bond-rating agencies evaluating nonprofit health-system liquidity, reinforcing management commitment . As inflation persists, financial stewardship is expected to underpin at least one-third of new account conversions through 2027 .

Regulatory Approvals & Clearances for Reprocessed SUDs

The FDA’s 2024 remanufacturing guidance clarified boundaries between servicing and reprocessing, reducing legal ambiguity for third-party operators . Vaporized hydrogen peroxide earned recognition as an established sterilization modality, diversifying validated methods beyond ethylene oxide . Japan embedded single-use device re-manufacturing into its QMS ordinance with staggered compliance deadlines through 2024, setting a template for other APAC regulators . The FDA’s 2025 approvals of VARIPULSE and Sphere-9 catheter systems, each containing reusable components, signaled growing confidence in mixed-use platforms . These milestones collectively expand the single-use medical device reprocessing market addressable base beyond cardiology into complex electrophysiology segments .

Sustainability & Waste-reduction Mandates

National health systems in the EU and United Kingdom now treat reprocessing as a compliance lever for landfill diversion and carbon-reduction targets rather than a discretionary green initiative . Over 70% of U.S. hospitals reported formal operating-room waste programs in 2024, with reprocessing identified as the single largest contributor to avoided landfill tonnage . The United Kingdom’s plan to eliminate avoidable single-use medical products by 2045 explicitly lists device reprocessing among endorsed strategies . Several EU jurisdictions are evaluating waste taxes indexed to kilogram output, potentially boosting the economic rationale for reprocessing by 2026 . With healthcare estimated to contribute 4.4% of global greenhouse gases, every 40% emission reduction per reprocessed unit tangibly improves providers’ Scope-3 profiles .

ESG Reporting Tying Scope-3 Emissions to Procurement

Rating agencies and investors increasingly scrutinize hospital Scope-3 disclosures, linking supply-chain emissions to cost of capital for large systems . Proprietary carbon calculators from leading reprocessors now quantify per-device CO₂ avoidance, enabling procurement teams to monetize the sustainability premium in vendor scorecards . Large integrated delivery networks bundle carbon metrics with price when awarding multi-year supply contracts, elevating reprocessing from tactical savings tool to strategic ESG differentiator . Health-system CFOs highlight Scope-3 performance in bond-offering documents to tap green-bond investor pools, creating financial upside for aggressive device-level reprocessing adoption . Collectively, these pressures are projected to drive 18–20% of new reprocessing account wins through 2028 .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OEM lobbying & restrictive labelling practices | -2.8% | Global, concentrated in markets with strong OEM presence | Medium term (2-4 years) |

| Device design limits to multiple re-use cycles | -1.9% | Global, technology-dependent rather than geography-specific | Long term (≥ 4 years) |

| EU MDR Article 17 cross-border fragmentation | -1.4% | European Union primary, potential regulatory spillover effects | Long term (≥ 4 years) |

| AI-enabled traceability exposing reprocessing failures | -0.8% | Developed markets with advanced healthcare IT infrastructure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

OEM Lobbying & Restrictive Labeling Practices

Johnson & Johnson’s 2025 antitrust loss, accompanied by a USD 442 million penalty, underscores systemic OEM resistance to reprocessing adoption . Manufacturers continue to leverage “single-use” labels to sow legal uncertainty, particularly in emerging markets with nascent regulatory oversight . Trade associations funded by OEMs lobby against expanded device-eligibility lists, delaying clinical uptake in high-volume categories like laparoscopic instruments . Even where antitrust scrutiny curbs overt contract restrictions, soft barriers such as staff-training withdrawal can still impede provider confidence . The resulting legal environment is expected to shave nearly three percentage points off projected CAGR in the near term .

EU MDR Article 17 Cross-border Fragmentation

European Union's Medical Device Regulation Article 17 creates a complex patchwork of national implementations that fragment the European reprocessing market and increase compliance costs. Individual member states retain authority to restrict or prohibit reprocessing, resulting in regulatory arbitrage that complicates pan-European reprocessing strategies. Germany's Bundesrat consideration of banning CE reprocessing after over 10 years of practice demonstrates regulatory instability that creates investment uncertainty. Cross-border device movement for reprocessing faces varying national interpretations of manufacturer obligations, creating logistical complexity that favors larger reprocessors with multi-jurisdictional compliance capabilities. The European Commission's December 2022 study on Article 17 implementation revealed significant variation in national approaches, suggesting continued fragmentation rather than harmonization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cardiovascular Dominance Drives Market Maturity

The cardiovascular catheter category delivered 37.02% of single-use medical device reprocessing market size in 2025, sustained by well-documented clinical equivalency studies and standardized sterilization workflows . Electrophysiology catheters are pacing the field with a 15.92% CAGR, catalyzed by FDA approvals for VARIPULSE and Sphere-9 systems that incorporate reusable components . Laparoscopic instruments benefit from robotic-surgery scale, yet complex geometries demand automated cleaning tunnels available chiefly at large commercial reprocessors . Gastroenterology device growth hinges on sterilization breakthroughs like ULTRA GI hydrogen-peroxide gas-plasma cycles, which mitigate past infection risks . Orthopedic external-fixation hardware remains niche due to patient-custom configurations and extended wear times, while general-surgery tools provide steady volume but face pricing commoditization pressures .

Technological advances, notably AI-based device-tracking tags and cloud analytics, now allow product-level performance benchmarking across reuse cycles, fostering surgeon trust in reprocessed alternatives . Enhanced inspection optics and non-destructive integrity testing continue to elevate quality assurance, helping cardiovascular and laparoscopic devices maintain near-parity with new OEM units in failure rates . As category life-cycle emissions enter formal ESG scorecards, providers prioritize high-volume disposable categories such as catheters for earliest conversion, reinforcing leadership of cardiovascular subsegments in the single-use medical device reprocessing market .

By Service Provider: Third-party Consolidation Accelerates

Third-party operators accounted for 84.12% of single-use medical device reprocessing market share in 2025, reflecting scale advantages in sterilization, validation and logistics . The sector’s 16.05% CAGR through 2031 is fueled by payer and regulator preference for ISO-certified specialist facilities over resource-strained in-house units . Consolidation continues, exemplified by Medline’s 2024 acquisition of Ecolab’s surgical solutions business, integrating reprocessing into a full-line distribution model that simplifies provider procurement.

Hospitals evaluating internal programs confront capital outlays for sterilizers, traceability software and quality testing that exceed USD 5 million per site, tipping cost-benefit calculations toward outsourcing . Regulatory amendments harmonizing FDA QSR with ISO 13485 in 2026 are expected to heighten documentation burdens, disadvantaging smaller in-house units lacking dedicated regulatory teams . As commercial partners adopt AI vision-inspection and robotic packing lines, throughput efficiencies generate 5–8-point margin advantages, widening the gap versus hospital-run operations. Accordingly, most top-100 U.S. IDNs now operate hybrid models where only very low-volume instruments remain on-site, while high-volume cath-lab and EP devices ship to third-party plants weekly.

By Application: Cardiology Leadership with Gastroenterology Acceleration

Cardiology procedures accounted for 40.25% of single-use medical device reprocessing market size in 2025, built on decades of clinical studies proving reprocessed catheter safety . Ablation volume growth and antitrust rulings that dismantle OEM service-withholding policies should maintain momentum through 2031 . Gastroenterology shows the highest 16.28% CAGR forecast, thanks to newly validated vaporized-hydrogen-peroxide sterilization cycles for duodenoscopes that remove infection-control barriers .

Orthopedics remains limited by low procedure standardization and patient-specific instrumentation, but trauma centers still unlock savings on external-fixation constructs with predictable geometries . Urology applications benefit from increased adoption of disposable ureteroscopes, creating demand for validated secondary reuse cycles once lumen-cleaning robotics reach commercial maturity in 2027. General surgery’s growth parallels operating-room sustainability mandates but faces price ceiling constraints due to commoditized device sets .

By End User: ASC Growth Outpaces Hospital Adoption

Hospitals and integrated delivery networks comprised 63.75% of 2025 demand, yet growth rate trails the overall market as decision hierarchies extend evaluation cycles . In contrast, ambulatory surgical centers will post a 16.63% CAGR through 2031, driven by fee-for-service migration and investor-owned ASC chains prioritizing rapid payback on device expense lines . ASCs leverage reprocessing to sidestep inventory-carrying costs and mitigate vendor-backorder risk, often signing exclusive deals with a single commercial partner to streamline logistics .

Academic medical centers, while early adopters of sustainability programs, face unique research protocol constraints that slow full transition to reprocessed instrumentation . Specialty cath labs capitalize on high device-reuse potential, negotiating volume-based rebates that can exceed USD 2 million annually at top U.S. heart institutes. The combined ASC–clinic segment is expected to capture 38% of incremental single-use medical device reprocessing market revenue over the next five years, reflecting procedure site-of-care shifts accelerated by payer incentives .

Geography Analysis

North America generated 43.10% of 2025 revenue, underpinned by FDA guidance certainty, antitrust enforcement and well-developed third-party networks . The U.S. market also benefits from hospital sustainability charters that align reprocessing with ESG key-performance indicators . Canada’s public-funded health system adopts reprocessing to offset budget caps, while Mexico’s medical-device cluster in Baja California offers near-shore sterilization capacity expansion for cross-border providers .

Asia-Pacific is on track to record a 16.88% CAGR to 2031, led by Japan’s QMS rule harmonization and China’s hospital-modernization programs, which target 70% device-reuse certification in tier-1 cities by 2028 . India’s Ayushman Bharat scheme expands insurance coverage, compelling public hospitals to stretch fixed budgets, thereby elevating reprocessing in procurement tenders starting 2026 . South Korea and Australia, both early electron-beam sterilization adopters, pilot AI-tracked catheter reuse to meet national zero-waste targets by 2035 .

Europe’s outlook is tempered by Article 17 fragmentation that introduces divergent reprocessing rules among member states, inflating compliance costs by up to 25% for cross-border operators . Germany’s potential CE-reprocessing ban could remove USD 90 million in annual revenue if enacted in 2026, although Denmark and the Netherlands have issued guidance enabling reprocessing under strict quality-management oversight . The United Kingdom, outside EU frameworks, formally targets elimination of avoidable single-use medical goods by 2045, positioning reprocessing as a central compliance mechanism . France’s health ministry launched a limited pilot in 2024 to evaluate duodenoscope reprocessing economics, possibly informing national policy in 2027 .

Regulatory Landscape

In the United States, third-party and hospital reprocessors are regulated by the U.S. Food and Drug Administration (FDA) as medical device manufacturers under the Federal Food, Drug, and Cosmetic Act, with premarket submission requirements (510(k) or PMA) tied to device classification and ongoing compliance obligations comparable to original manufacturers. FDA program materials and related guidance, including the May 2024 final guidance clarifying boundaries around remanufacturing, continues to influence how providers and commercial reprocessors structure labeling, quality systems, and documentation to support safety and performance across reuse cycles.

In Europe, Regulation (EU) 2017/745 (EU MDR) governs reprocessing through Article 17, which permits Member States to allow reprocessing of single-use devices only where national law enables it, creating a patchwork of market access requirements across countries. Where permitted, reprocessed single-use devices must meet safety and performance requirements, and reprocessors assume manufacturer-like obligations. This includes conformity assessment supported by notified bodies and applicable common specifications, so cross-border scaling remains sensitive to national implementation choices and enforcement practices.

Value Chain Analysis

The value chain begins with OEM production and original distribution of single-use devices, followed by hospital and ambulatory-site selection of eligible SKUs for collection. Devices are segregated and shipped under chain-of-custody controls to either in-house reprocessing units or, more commonly, third-party commercial reprocessors. These providers run validated workflows covering receipt and sorting, cleaning and decontamination, functional testing and inspection, sterilization (including growing use of vaporized hydrogen peroxide as an alternative pathway where validated), repackaging and labeling, and regulated release back to healthcare facilities. With the FDA treating reprocessors as manufacturers, quality-system requirements, traceability, and post-market surveillance sit at the center of commercial plant operations, placing microbiology testing and documentation teams alongside validation activities.

Downstream, hospitals integrate reprocessed devices into procurement and inventory systems alongside new-device purchasing, often contracting for closed-loop logistics, usage tracking, and reporting of savings and waste diversion. Trade-association data points to expanding network effects, with AMDR reporting 11,458 hospitals and surgical centers in 18 countries using reprocessed devices in 2025. Operational risk management is also part of the chain, as shown when Medline ReNewal completed a voluntary recall in March 2026 for several reprocessed electrophysiology catheters and an electrosurgical product, underscoring how robust lot traceability, rapid notification processes, and corrective-and-preventive-action capability differentiate large-scale reprocessors.

Competitive Landscape

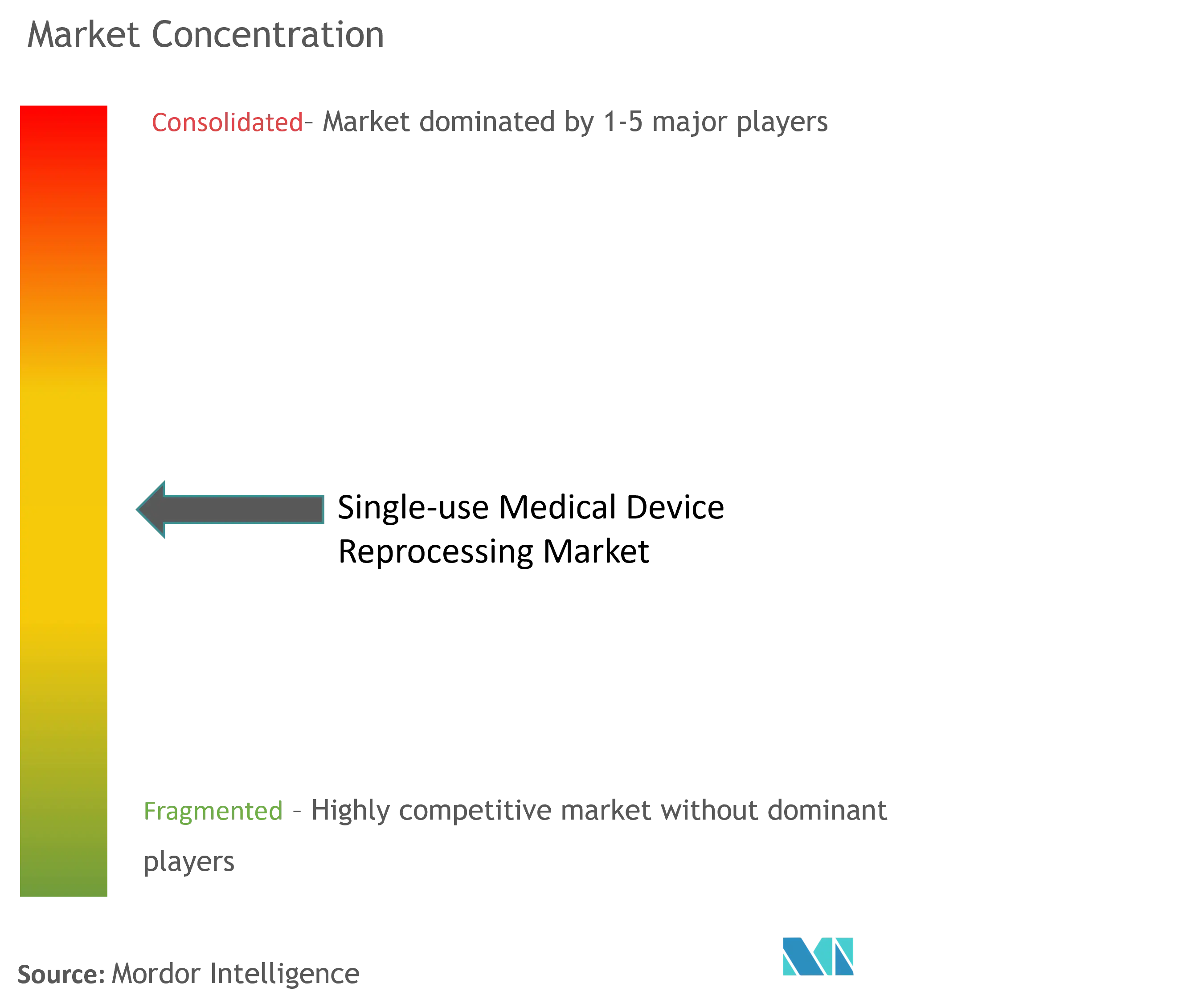

The single-use medical device reprocessing market remains moderately fragmented, yet scale-driven consolidation is accelerating as ISO-quality compliance and advanced sterilization investments raise entry barriers . Stryker’s Sustainability Solutions division served more than 3,000 U.S. hospitals and delivered USD 238 million in customer savings during 2023, leveraging AI-enabled track-and-trace dashboards to differentiate service levels . Medline’s acquisition of Ecolab’s surgical solutions portfolio in 2024 extended end-to-end logistics control from original manufacture through reprocessing, enhancing negotiating power with hospitals seeking bundled sourcing .

Independent specialty players capitalize on electrophysiology and gastroenterology niches where device complexity historically limited reuse; Innovative Health’s successful antitrust verdict against Johnson & Johnson validates the pathway for market access challenges when OEMs withhold support . New entrants featuring cloud-native quality-management systems and modular sterilization pods aim to service rural hospitals lacking volume for traditional hub-and-spoke models .

Looking forward, the 2026 FDA QSR–ISO 13485 alignment should simplify dual-compliance burdens, favoring agile mid-tier firms while maintaining rigorous patient-safety thresholds . Systematic digitization of sterilizer performance metrics and predictive maintenance algorithms will likely underpin next-wave differentiation, enabling real-time client dashboards that tie device-reuse cycles to carbon-savings analytics . Anticipated OEM divestitures of internal reprocessing units could inject additional consolidation targets, potentially elevating top-five market share above the current 55% threshold by 2028 .

Single-use Medical Device Reprocessing Industry Leaders

Stryker Corporation

Medline Industries Inc.

Innovative Health

Johnson & Johnson (Sterilmed Inc.)

Arjo

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space remains in scaling reprocessing penetration beyond mature cath-lab categories into more complex electrophysiology and gastroenterology device families, where validated sterilization and inspection protocols determine how quickly hospitals convert. AMDR provides a near-term proof point: it reports 11,458 hospitals and surgical centers across 18 countries used reprocessed single-use devices in 2025, reflecting an 8.26% increase in sales volume versus 2024 and USD 495.5 million in reported savings for participating health systems. This installed base supports additional opportunity in enterprise contracts that bundle cost savings with measurable waste and carbon reporting, tying procurement more directly to Scope-3 disclosures and operating-room waste programs.

Regulatory evolution also creates additional opportunity, particularly in Europe. The European Commission proposed in February 2026 an amendment to the EU MDR to move toward harmonized rules for single-use device reprocessing across Member States, targeting friction created by national opt-in frameworks. At the same time, policy-enforced pressure on ethylene oxide use, including proposed U.S. EPA standards tightening EtO concentration limits per cycle, increases demand for validated alternatives and for reprocessors that can industrialize modalities such as vaporized hydrogen peroxide with process monitoring. These shifts increase the practical value of investments in automation, AI-enabled track-and-trace, and quality-system digitization, since they make reuse-cycle verification and audit readiness easier for hospitals, payers, and regulators to assess at scale.

Recent Industry Developments

- June 2026: Innovative Health announced the publication of a new single-use device reprocessing workbook developed by the Collaborative for Healthcare Action to Reduce MedTech Emissions (CHARME). The resource formalized practical guidance linking reprocessing to emissions-reduction and procurement accountability, reinforcing sustainability-led adoption alongside traditional cost-containment.

- May 2025: A federal jury returned a unanimous verdict in favor of Innovative Health in its antitrust lawsuit against Johnson & Johnson MedTech (Biosense Webster) related to restrictions affecting reprocessed catheter use. The outcome strengthened legal precedent against OEM practices that constrain third-party reprocessing access and supported wider hospital choice in electrophysiology catheter sourcing.

- June 2024: Innovative Health and US Endovascular announced an agreement to expand access to reprocessed single-use devices in ambulatory surgery centers and office-based labs. The partnership targeted faster-growing outpatient settings where streamlined governance and rapid payback thresholds make reprocessing programs easier to deploy across multi-site networks.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the global revenues generated from reprocessing medical devices that are originally labeled for single use, where the device is collected after use and then cleaned, disinfected or sterilized, tested, and prepared for safe reuse under applicable rules.

Scope exclusions: We exclude general hospital sterilization of reusable instruments and consumables that are not part of a single use device reprocessing workflow.

Segmentation Overview

- By Product Type (Value, USD)

- Cardiovascular Catheters

- Electrophysiology Catheters

- Laparoscopic Instruments

- Gastroenterology Devices

- Orthopedic External Fixation Devices

- General Surgery Instruments

- By Service Provider (Value, USD)

- Third-party /Commercial Reprocessors

- In-house /Hospital Reprocessing Units

- By Application (Value, USD)

- Cardiology

- Gastroenterology

- Orthopedics

- Urology

- General Surgery

- By End User (Value, USD)

- Hospitals & Surgical Centers

- Ambulatory Surgical Centers

- Specialty Clinics & Cath Labs

- Academic & Research Institutes

- By Geography (Value, USD)

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- Saudi Arabia

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by mapping what is legally allowed to be reprocessed, and where adoption is most established, since the market depends heavily on regulatory permissions and hospital procurement norms. We used public sources such as FDA device and reuse guidance, CDC infection prevention references, WHO patient safety and waste guidance, and OECD or World Bank health spending and hospital capacity indicators to anchor the demand setting.

Next, we cross-checked the demand pool using practical hospital activity signals, such as inpatient and surgical procedure volumes, operating room throughput, and the typical mix of high value single use device categories used in procedures. Company filings, investor presentations, credible press, and association websites were used to understand service models and pricing logic. A paid subscription for company financials, news, and patents was also used to validate timelines, facility expansion signals, and technology claims at a high level. These sources are illustrative only, and we also consulted other public and paid references to collect data, validate assumptions, and clarify gaps.

Primary Interviews and Surveys

Primary discussions were run with reprocessing service operators, hospital sterile processing and supply chain teams, and a few quality and regulatory roles, because these groups know what gets reprocessed in practice and what is rejected during inspection. We also spoke with device category specialists across major regions so that adoption, pricing, and compliance assumptions could be stress tested before the final numbers were signed off.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 13% | APAC: 37% |

| Mid tier: 56% | Functional/Unit leaders: 30% | EMEA: 36% |

| Smaller Players: 19% | Managers: 57% | Americas: 27% |

Market-Sizing & Forecasting

Sizing was built using a top-down demand reconstruction. Hospital procedure volumes and reprocessable device utilization rates were used to form the eligible device pool, which is then filtered by reprocessing penetration and typical reprocessing price per device (or per cycle) in each geography. When the model was nearly complete, we used selective bottom-up checks such as sampled hospital program volumes, service provider capacity cues, and average selling price ranges gathered from interviews, which helped adjust totals that looked out of line.

Key inputs treated as the most sensitive were the share of procedures using high-volume eligible categories, the average number of eligible devices per procedure, rejection rates during collection and inspection, the average number of allowable reprocessing cycles, and the price progression over the forecast period as volume scales. For forecasting, we used scenario analysis supported by short regression-style checks on drivers such as elective procedure recovery, cost-containment pressure in hospitals, and policy clarity in major markets. Where country data was thin, proxy indicators like hospital bed counts and surgical rates were used, then corrected through regional expert feedback so the totals stayed realistic.

Data Validation & Update Cycle

Outputs were validated through triangulation across independent signals, and the checks were not limited to growth rates alone. We reviewed year-on-year jumps, region shares, and implied price or volume assumptions, then ran variance checks against procedure trends and known adoption patterns in highly regulated markets.

Before sign-off, a second analyst review was completed, and outliers triggered follow-up calls to confirm whether the issue was scope, pricing, or penetration. The report is refreshed annually, and interim updates are made when material events occur, such as major regulatory changes or sudden shifts in hospital utilization. Right before delivery, a final pass is done so clients receive an updated view based on the latest available public information.

Mordor Intelligence's Global Single Use Medical Device Reprocessing Market Sizing Compared With Other Published Estimates

Published market values for single use device reprocessing can look far apart because the scope line can be drawn differently, and the market itself is still uneven by region. Differences usually come from what is counted as reprocessing revenue, the years chosen as the base, and how quickly adoption is assumed to move beyond the most commonly reprocessed categories.

In this study, the key gap drivers were whether the estimate includes only reprocessing services for eligible single use devices, or whether it also blends in broader reprocessed medical devices, waste management, or general sterilization activities that sit outside the reprocessing loop. The spread also rises when procedure-based demand signals are not used to anchor the eligible pool, or when pricing is escalated aggressively without being checked against contract behavior and rejection rates. To keep the perimeter consistent, we maintained a service-only definition and used procedure-linked demand checks, a modeling choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.35 B (2026) | |

| Global Consultancy A | USD 3.20 B (2024) | Uses an earlier base year and appears to bundle adjacent activities like broader sterilization, infection control, or waste-related services, which expands the revenue perimeter beyond reprocessing service receipts. |

| Industry Publisher B | USD 3.26 B (2024) | Uses a broader RSUD framing and a different forecast window, which can pull in device categories and revenue types that are not strictly tied to eligible single use device reprocessing cycles. |

The table indicates that the biggest swing is usually not the growth math, but what gets counted and which year the estimate starts from. By tying the eligible device pool to procedure activity and validating penetration, rejection, and pricing assumptions with interviews, the final number stays traceable to clear steps that a buyer can replicate and sanity-check.

Key Questions Answered in the Report

What is the projected value of the single-use medical device reprocessing market in 2031?

It is forecast to reach USD 2.81 billion by 2031, up from USD 1.35 billion in 2026 at a 15.74% CAGR.

Which product type currently dominates device reprocessing?

Cardiovascular catheters hold 37.02% revenue share, supported by long-standing clinical validation.

Why are ambulatory surgical centers adopting reprocessing faster than hospitals?

ASCs prioritize margin management and have streamlined governance, enabling a 16.63% CAGR through 2031.

How do environmental regulations influence adoption?

Scope-3 carbon reporting and landfill-reduction mandates position reprocessing as a compliance pathway that also generates device-level savings.

What impact did the 2025 Johnson & Johnson antitrust ruling have?

The USD 442 million penalty curtailed OEM contract restrictions and opened catheter reprocessing opportunities for independent providers.

Page last updated on: