Pharmaceutical Sterility Testing Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

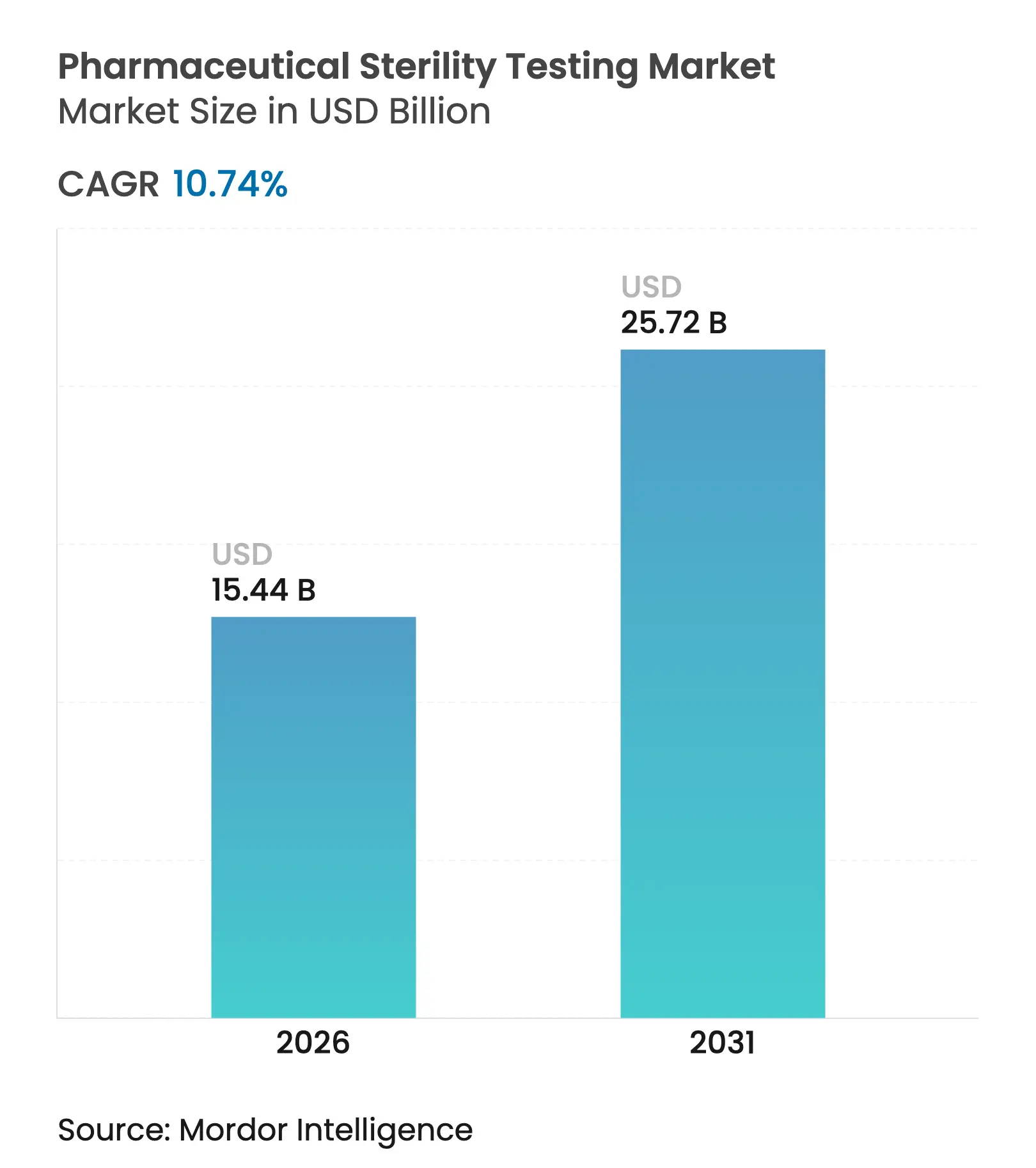

| Market Size (2026) | USD 15.44 Billion |

| Market Size (2031) | USD 25.72 Billion |

| Growth Rate (2026 - 2031) | 10.74 % CAGR |

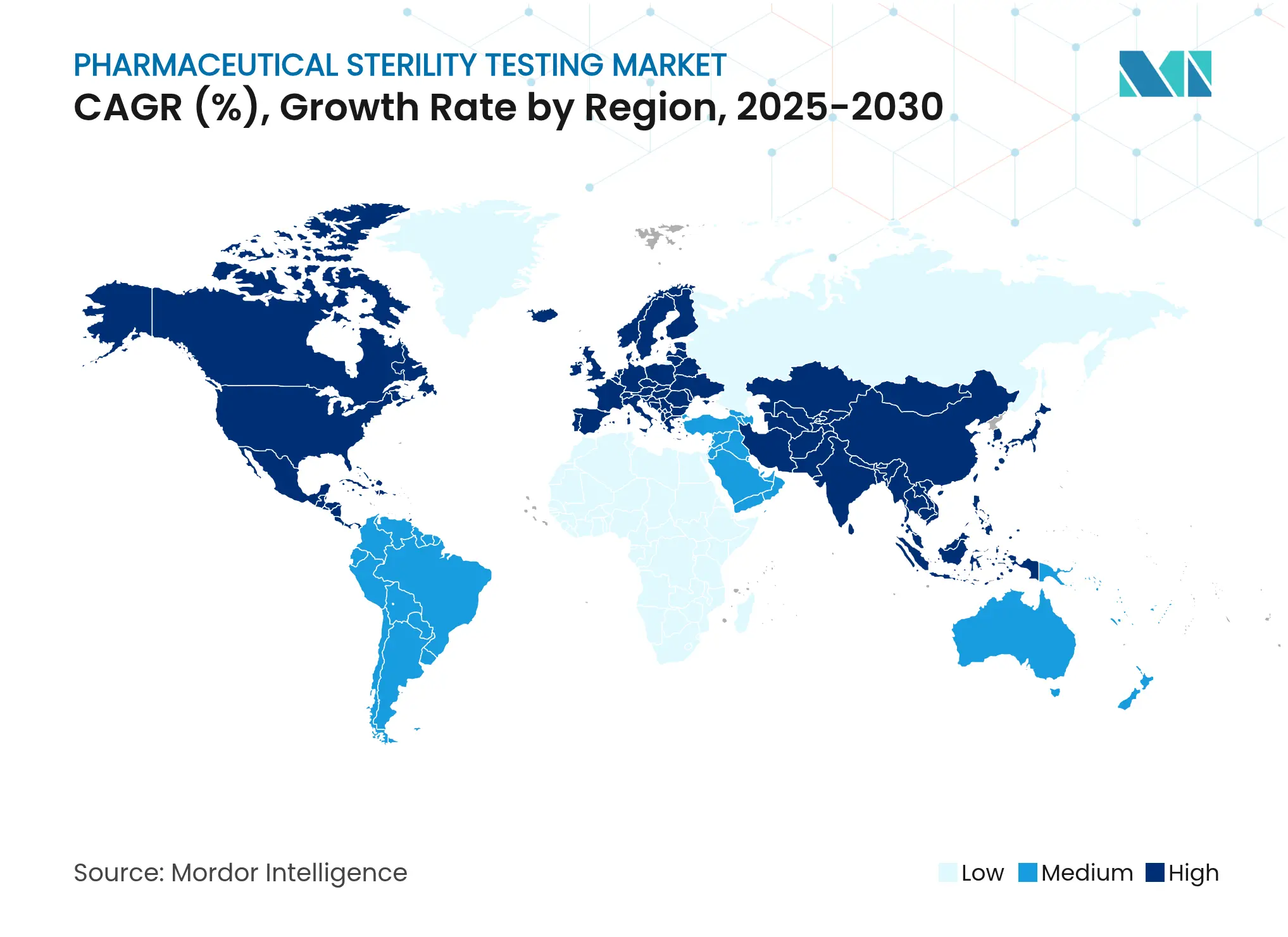

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Pharmaceutical Sterility Testing Market Analysis by Mordor Intelligence

pharmaceutical sterility testing market size in 2026 is estimated at USD 15.44 billion, growing from 2025 value of USD 13.94 billion with 2031 projections showing USD 25.72 billion, growing at 10.74% CAGR over 2026-2031. The growth arises from tighter global regulations, swift biologics adoption, and a strategic move by drug makers toward outsourced quality-control partnerships that lower compliance risk while accelerating product release timelines.[1]Food and Drug Administration, “Inspection of Rapid Microbial Methods,” fda.gov Rapid-microbial-method (RMM) validation initiatives, expanding parenteral pipelines, and record venture funding for automated testing technologies further amplify demand for sterility assurance services across injectable, vaccine, and gene-therapy products. Consequently, the pharmaceutical sterility testing market continues to evolve toward closed-system, data-rich workflows that shorten sterility confirmation cycles from 14 days to fewer than 72 hours.

Key Report Takeaways

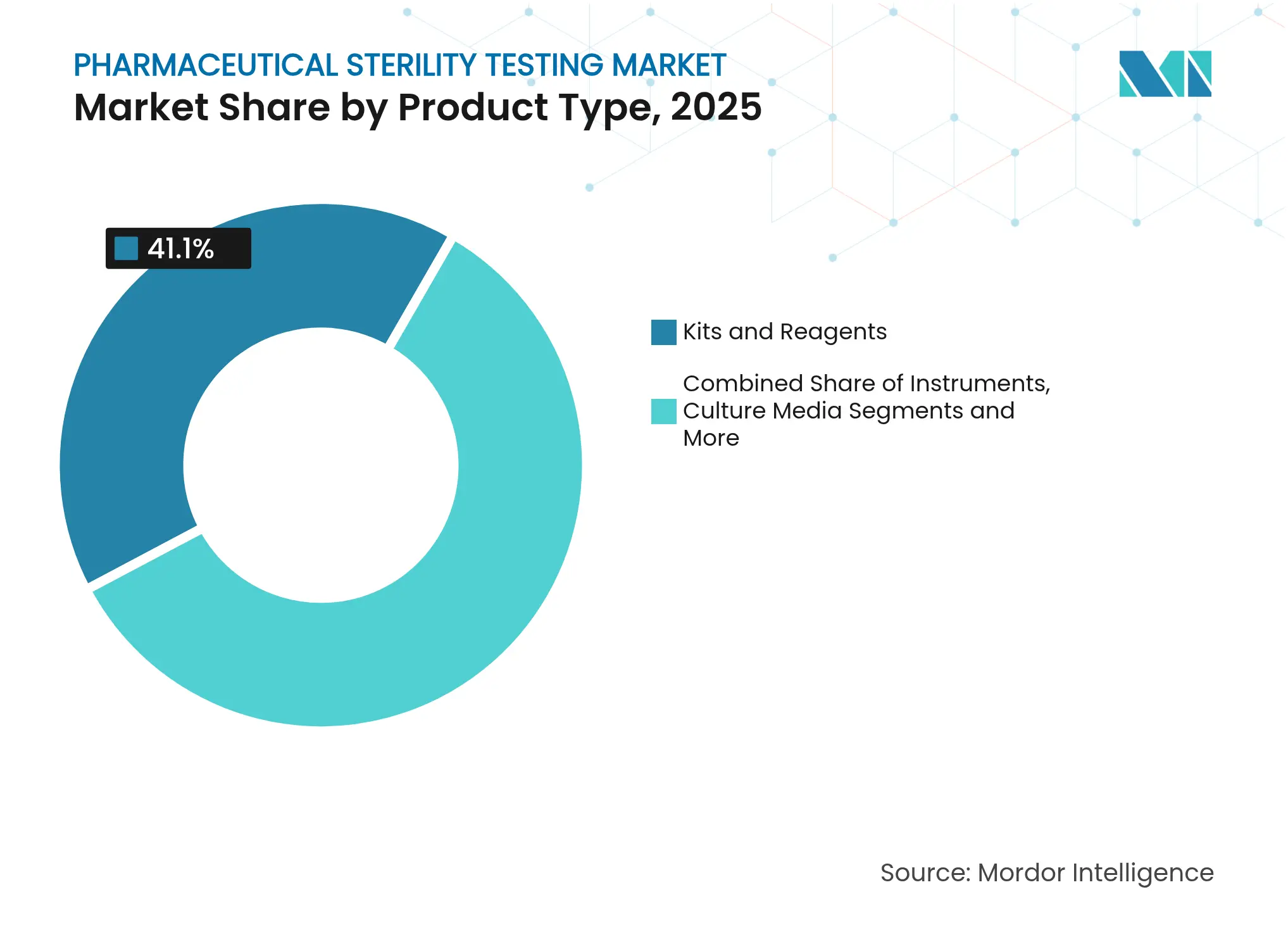

- By product type, kits and reagents led with 41.10% of the pharmaceutical sterility testing market share in 2025; rapid-microbial-method instruments are poised to expand at a 13.95% CAGR through 2031.

- By service model, outsourced testing services accounted for 59.60% of the pharmaceutical sterility testing market size in 2025 and are projected to grow at a 12.36% CAGR to 2031.

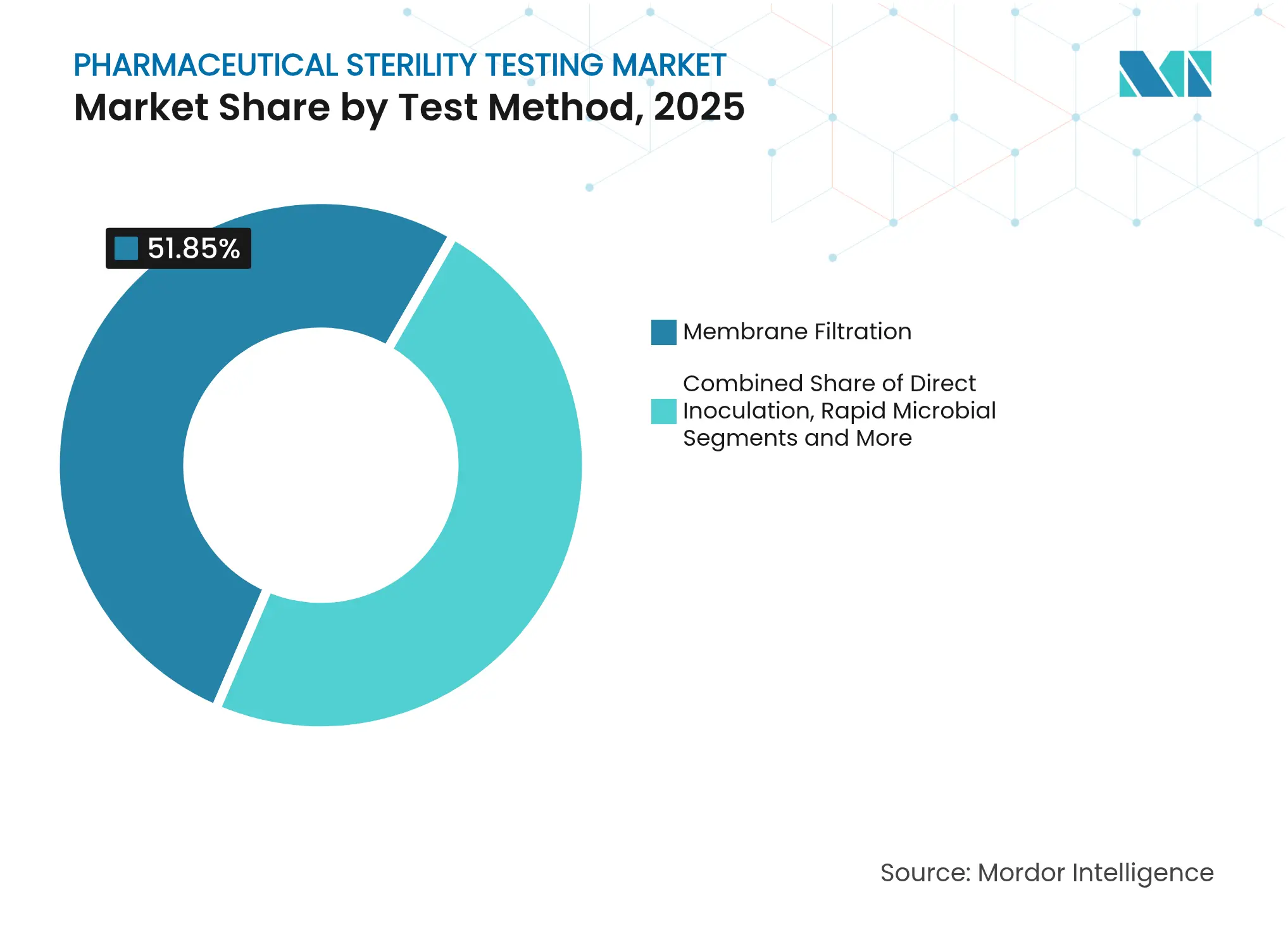

- By test method, membrane filtration captured 51.85% of the pharmaceutical sterility testing market size in 2025, while rapid methods are advancing at a 15.28% CAGR.

- By end user, pharmaceutical and biotechnology firms controlled 59.75% of the pharmaceutical sterility testing market share in 2025, whereas CROs and CDMOs are projected to register a 13.64% CAGR to 2031.

- By geography, North America held a 40.35% revenue share of the pharmaceutical sterility testing market in 2025; Asia-Pacific exhibited the fastest regional CAGR, at 11.88% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pharmaceutical Sterility Testing Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Expanding pipeline of parenteral biologics Expanding pipeline of parenteral biologics | +2.10% | Global, North America & EU | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+2.10% | Geographic Relevance:Global, North America & EU | Impact Timeline:Medium term (2-4 years) |

Surge in outsourced QC to comply with latest GMP Annex 1 Surge in outsourced QC to comply with latest GMP Annex 1 | +1.80% | Global, EU & APAC | Short term (≤ 2 years) | |||

FDA draft guidance encouraging RMM validation FDA draft guidance encouraging RMM validation | +1.40% | North America, global spillover | Medium term (2-4 years) | |||

Accelerated orphan-drug approvals requiring small-batch tests Accelerated orphan-drug approvals requiring small-batch tests | +1.20% | North America & EU, expanding to APAC | Long term (≥ 4 years) | |||

VC funding into automated sterility-testing start-ups VC funding into automated sterility-testing start-ups | +0.90% | North America, early EU adoption | Short term (≤ 2 years) | |||

Growing cell- and gene-therapy manufacturing capacity Growing cell- and gene-therapy manufacturing capacity | +1.60% | Global, North America & EU | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Expanding Pipeline of Parenteral Biologics

Approvals for novel biologics rose 21% year-on-year in 2024, bringing 17 new Biologics License Applications into commercial production and sparking fresh demand for aseptic manufacturing environments that cannot rely on terminal sterilization. Each monoclonal antibody batch now undergoes container-closure-integrity checks, real-time environmental monitoring, and rapid mycoplasma detection before release, raising the total number of sterility tests per product lot. The pharmaceutical sterility testing market consequently benefits from higher consumables turnover and instrument installations, particularly for single-use isolators that mitigate cross-contamination risk. Closed-system filling lines popular in antibody plants require integrated sterility assurance platforms, encouraging vendors to bundle filtration media, process qualification, and in-situ ATP monitoring into unified solutions. Personalized biologics intensify this demand by shrinking batch size and shortening shelf life, pushing test laboratories toward automated readers capable of issuing sterility clearance in under 3 days.

Surge in Outsourced QC to Comply with Latest GMP Annex 1

The EU’s 2023 Annex 1 revision compels drug makers to formalize contamination-control strategies and introduce risk-based environmental monitoring across every aseptic process step.[2]PIC/S, “Annex 1 Revision Implementation,” picscheme.orgSmaller firms lacking capital for isolators or data-integrity software increasingly turn to contract testing labs, fuelling service-provider expansions that underpin 60.2% market dominance for outsourced sterility testing. Eurofins alone operates 45 GMP-compliant sites offering 24/7 rapid sterility testing queues, ensuring global customers meet shrinking lead-time targets for parenteral lots. Outsourcing simultaneously mitigates staffing shortages by giving manufacturers access to microbiology experts who manage method validation and regulatory submissions.

FDA Draft Guidance Encouraging Rapid-Microbial-Method (RMM) Validation

The FDA agency’s 2024 draft guidance clarifies equivalence demonstration pathways for fluorescence, PCR, and ATP bioluminescence technologies, reducing uncertainty around replacing conventional 14-day broth cultures. Early adopters have shown that RMM systems can accelerate lot release for cell therapies with 48-hour shelf lives, cutting working-capital exposure by up to USD 15 million per product line. Manufacturers now embed automated readers directly on filling lines to obtain sterility clearance in real time, while electronic batch-record integration boosts data integrity and audit readiness.

Accelerated Approvals of Orphan Drugs Requiring Small-Batch Sterility Tests

Orphan-drug approvals reached record highs in 2024, many involving micro-volume vials that limit sample-pull volumes necessary for traditional sterility assays. Sponsors, therefore, deploy risk-based environmental monitoring strategies, supplementing minimal end-product testing with continuous particulate monitoring inside restricted-access barrier systems. Contract labs have responded by offering tailored statistical sampling plans and proprietary low-volume membrane-filtration cassettes that preserve scarce drug substance.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High Capital Cost Of Automated Isolators High Capital Cost Of Automated Isolators | -1.30% | Global, particularly impacting smaller manufacturers | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-1.30% | Geographic Relevance:Global, particularly impacting smaller manufacturers | Impact Timeline:Medium term (2-4 years) |

Shortage Of Skilled Microbiologists In High-Income Countries Shortage Of Skilled Microbiologists In High-Income Countries | -0.80% | North America & EU, with spillover effects globally | Long term (≥ 4 years) | |||

Persistent False-Positive Risk With Direct-Inoculation Methods Persistent False-Positive Risk With Direct-Inoculation Methods | -0.70% | Global, with higher impact in cost-sensitive markets | Short term (≤ 2 years) | |||

Fragmented Regulatory Expectations Across Emerging Markets Fragmented Regulatory Expectations Across Emerging Markets | -0.60% | APAC, Latin America, MEA emerging markets | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High Capital Cost of Automated Isolators

Turn-key aseptic isolator lines cost USD 500,000 or more before installation and validation, a sum that can exceed USD 1 million once annual maintenance and decontamination cycles are factored in. This expense constrains capital allocation for emerging biotech firms already balancing facility build-outs with clinical-trial funding. Many thus delay in-house sterility-testing upgrades and lean more heavily on outsourcing, creating longer sample-shipment times that may complicate parallel release strategies. Vendors attempt to mitigate sticker shock through pay-per-use leasing models, yet uptake remains muted among firms with limited cash flow. High-volume generic-injectable producers likewise weigh the isolation-technology benefit against tight pricing margins, slowing widespread adoption despite regulatory encouragement.

Shortage of Skilled Microbiologists in High-Income Countries

Retirement of senior microbiologists, coupled with limited university throughput in pharmaceutical microbiology, has left hundreds of QC positions unfilled across the United States and Western Europe. Remaining staff shoulder heavier validation workloads as RMM adoption advances, elevating burnout risk and turnover. Contract labs extend training academies to close gaps, but demand continues to outstrip supply. Artificial-intelligence colony counters and scripted deviation-analysis tools aim to reduce reliance on scarce expertise, yet regulatory inspections still expect human oversight, sustaining the labor bottleneck.

Segment Analysis

By Product Type: Kits and Reagents Sustain Revenue; Instruments Accelerate Adoption

Kits and reagents held 41.10% of the pharmaceutical sterility testing market share in 2025, reflecting their indispensable, repeat-purchase nature that underpins predictable supplier cash flows. Every membrane-filtration run consumes fresh sterile pads, pre-filled culture broths, and neutralizing agents, translating into steady volume growth as global batch counts rise. Ready-to-use media pouches incorporating bar-coded traceability now ship worldwide to eliminate autoclave cycles, cut technician handling, and strengthen data integrity audit trails. Vendors continue embedding environmental-monitoring plates and disinfectant residues into holistic reagent portfolios to lock in multi-year supply contracts.

Although rapid-microbial-method instruments currently represent a smaller dollar contribution, they recorded a 13.95% CAGR and are redefining the pharmaceutical sterility testing market’s technology mix. The latest image-based incubation chambers accept up to 700 sample bottles simultaneously and employ machine-vision algorithms that flag colony growth within eight hours. Early adopters report 85% labor savings versus manual plate counts and achieve faster product-release clearance, offering a compelling payback in high-throughput biologics plants. Instrument vendors now pair hardware with subscription analytics engines, anchoring recurring revenue as users scale global operations.

Note: Segment shares of all individual segments available upon report purchase

By Service Model: Outsourced QC Services Dominate, In-House Labs Retain Strategic Roles

Outsourced sterility-testing partners handled 59.60% of the overall testing volume in 2025, equal to USD 8.31 billion of the pharmaceutical sterility testing market. Their appeal stems from deep regulatory-affairs bench strength, multi-site redundancy, and the ability to amortize isolator investments across hundreds of clients, producing price points unattainable for single-manufacturer labs. Recent FDA remote-inspection pilots further favor large networks that maintain integrated laboratory-information-management systems capable of streaming real-time audit data to regulators.

In-house laboratories remain integral for blockbuster molecules, where continuous production demands parallel sterility clearance to avoid costly inventory stacking. Firms manufacturing at giga-scale maintain barrier-isolator lines within core fill-finish suites, citing intellectual-property control and shorter sample-transport windows as critical advantages. Hybrid models emerge as top-10 pharma companies outsource low-volume therapy lots but retain high-volume vaccine testing under their own roof, balancing flexibility with cost.

By Test Method: Membrane Filtration Retains Primacy; Rapid Technologies Gain Pace

Membrane filtration delivered 51.85% of the pharmaceutical sterility testing market share, commanding trust for its broad compendial acceptance and high recovery rates for stressed microorganisms. Filtration setups now integrate pre-sterilized single-use manifolds and online pressure monitoring to minimize clamp errors. Suppliers also commercialize low-adsorptive membranes tailored for lipid nanoparticle formulations, gaining popularity in mRNA platforms.

Rapid microbial methods headline growth, achieving a 15.28% CAGR, fueled by FDA encouragement and shrinking lead times in CGT supply chains. ATP bioluminescence readers flag contamination within four hours, while PCR microfluidic chips quantify Mycoplasma in 30 minutes without extensive sample prep. As compendial bodies approve new chapters, manufacturers increasingly deploy dual-method strategies, rapid screens for preliminary clearance followed by confirmatory membrane filtration to blend speed with regulatory familiarity, gradually tilting market preference toward automated modalities.

Note: Segment shares of all individual segments available upon report purchase

By Sample Category: Injectables, Biologics, and Vaccines Command Testing Attention

Injectables continue to anchor demand given direct bloodstream exposure, accounting for nearly half of total testing events in 2024. Prefilled syringes, lyophilized vials, and large-volume parenterals require 100% batch testing, and the rise of high-potency oncology drugs amplifies sterility scrutiny. Biologics and vaccines, comprising proteins, viral vectors, and lipid nanoparticles, must avoid heat sterilization, thus embracing advanced contamination-control envelopes and frequent in-process sterility checks.

Medical-device combinations, such as drug-eluting stents and on-body injectors, extend sterility-testing scope beyond traditional pharma boundaries, driving instrument vendors to develop flexible fixtures for irregular geometries. Ophthalmic solutions, though mature, persist as steady testing contributors thanks to sensitive ocular tissue considerations and the shift toward preservative-free formulations necessitating aseptic fills. As single-use technology replaces stainless-steel lines, sample-category complexity rises, pushing labs to master multiple test matrices under one roof.

By End User: Pharma Majors Lead Volume; CROs and CDMOs Expand Rapidly

Pharmaceutical and biotechnology companies controlled 59.75% of the pharmaceutical sterility testing market share in 2025, performing tests internally when economies of scale and IP protection justify dedicated clean rooms. Their sterility programs now intersect with enterprise-wide digital-quality initiatives aiming to leverage lab data for predictive maintenance and contamination-trend analytics.

Contract research and manufacturing organizations enjoy the swiftest expansion, supported by double-digit biologics outsourcing and a 13.64% CAGR in sterility-testing revenue. Service providers differentiate through 24-hour sample accession, integrated container-closure-integrity assays, and cloud dashboards that alert clients to out-of-spec events in real time. Medical-device manufacturers and hospital compounders represent emerging end-user cohorts seeking pharma-grade sterility validation as regulations tighten around injectable admixtures and implantable devices.

Geography Analysis

North America accounted for 40.35% of the pharmaceutical sterility testing market revenue in 2025, underpinned by FDA leadership on RMM adoption, a broad biologics pipeline, and abundant venture capital for automation start-ups. United States manufacturers embed growth-direct readers and AI-powered colony counters into high-speed syringe lines to trim working capital, while Canadian biotech hubs leverage cross-border contract labs to meet Health Canada and FDA alignment. Mexico’s expanding fill-finish sector turns to third-party test centers in California and Texas, spurring cross-border logistics solutions tailored to maintain sample integrity.

Europe maintains strong demand as GMP Annex 1 revisions fuel investment in barrier-technology upgrades. Germany and Ireland construct greenfield bioprocessing plants configured for closed-system sterility assurance, and the United Kingdom’s “License for Advanced Therapies” pathway accelerates rapid-method validation for CGTs entering hospital-based manufacturing. Regulatory focus on data integrity drives labs to deploy blockchain-anchored e-batch records that stakeholders can audit remotely.

Asia-Pacific is the fastest-growing geography, projected at a 11.88% CAGR through 2031. China elevates sterility standards via National Medical Products Administration harmonization with PIC/S, compelling domestic vaccine makers to import isolator technology from European vendors. South Korea and Singapore strengthen their status as global API and biologics export centers, incorporating automated sterility test suites to achieve under-48-hour release cycles that satisfy just-in-time inventory models for multinational clients. India’s injectable hubs in Hyderabad and Ahmedabad form public-private skill academies to train microbiologists and address talent shortages, while Australia capitalizes on government grants to expand viral-vector manufacturing linked to university-hospital networks.

Competitive Landscape

Market Concentration

The pharmaceutical sterility testing market remains moderately fragmented yet increasingly shaped by strategic consolidation. Thermo Fisher Scientific, Sartorius, and Merck KGaA leverage scale advantages across instruments, reagents, and services, reinforcing customer stickiness through end-to-end solution bundles that simplify validation workflows. Thermo Fisher’s USD 4.1 billion acquisition of Solventum’s purification and filtration business augments its downstream-processing footprint, enabling cross-selling of membrane-filtration kits and isolator consumables within an expanded bioprocess portfolio.

Mid-tier contenders, including STERIS and Nelson Labs, carve out niches via rapid-testing services that guarantee six-day sterility clearance, appealing to CGT manufacturers with ultra-short product shelf lives. Danaher’s merger of Cytiva and Pall creates a USD 7.5 billion bioprocess technology platform that marries filtration hardware with analytics software, promising integrated sterility-assurance packages for single-use production lines. Vendors increasingly embed SaaS dashboards that transform colony counts into predictive-quality insights, differentiating offerings based on data-analytics depth rather than standalone hardware features.

Emerging disruptors focus on AI-guided robotics, cloud-native validation workflows, and miniature benchtop isolators designed for decentralized hospital-based production of autologous therapies. Venture-backed firms such as Persist AI deploy modular robotic labs to automate test-method development, appealing to start-ups lacking internal QC infrastructure yet unwilling to rely solely on third-party providers. Competitive intensity thus revolves around time-to-result, digital traceability, and flexible capacity tailored to heterogeneous therapy pipelines rather than price alone.

Pharmaceutical Sterility Testing Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Thermo Fisher Scientific acquired Solventum’s purification & filtration business for USD 4.1 billion, expanding its bioproduction capabilities and targeting USD 125 million in operating-income synergies by 2030.

- February 2025: STERIS opened a new testing and validation laboratory in Swindon, United Kingdom, broadening European sterility-testing reach.

- February 2025: Jabil acquired Pharmaceutics International Inc., adding 360,000 sq ft of aseptic-filling and high-potency capacity to its CDMO network.

- January 2025: Pace Life Sciences purchased a New Jersey laboratory from Curia, boosting FDA-registered sterility and container-closure-integrity services.

Table of Contents for Pharmaceutical Sterility Testing Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Expanding Pipeline Of Parenteral Biologics

- 4.2.2Surge In Outsourced QC To Comply With Latest GMP Annex 1

- 4.2.3FDA's Draft Guidance Encouraging Rapid-Microbial-Method (RMM) Validation

- 4.2.4Accelerated Approvals Of Orphan Drugs Requiring Small-Batch Sterility Tests

- 4.2.5VC Funding Into Automated Sterility Testing Start-Ups

- 4.2.6Growing Cell And Gene Therapy Manufacturing Capacity

- 4.3Market Restraints

- 4.3.1High Capital Cost Of Automated Isolators

- 4.3.2Shortage Of Skilled Microbiologists In High-Income Countries

- 4.3.3Persistent False-Positive Risk With Direct-Inoculation Methods

- 4.3.4Fragmented Regulatory Expectations Across Emerging Markets

- 4.4Regulatory Landscape

- 4.5Technological Outlook

- 4.6Porter's Five Forces Analysis

- 4.6.1Threat of New Entrants

- 4.6.2Bargaining Power of Buyers

- 4.6.3Bargaining Power of Suppliers

- 4.6.4Threat of Substitutes

- 4.6.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Product Type

- 5.1.1Instruments

- 5.1.2Kits & Reagents

- 5.1.3Culture Media

- 5.1.4Sterility Testing Accessories

- 5.1.5Others

- 5.2By Service Type

- 5.2.1In-house Testing

- 5.2.2Outsourced Sterility Testing Services

- 5.3By Test Method

- 5.3.1Membrane Filtration

- 5.3.2Direct Inoculation

- 5.3.3Rapid Microbial Methods

- 5.3.4Other Methods

- 5.4By End User

- 5.4.1Pharmaceutical & Biotech Companies

- 5.4.2Medical-Device Manufacturers

- 5.4.3CROs & CDMOs

- 5.4.4Compounding Pharmacies

- 5.4.5Others

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4South Korea

- 5.5.3.5Australia

- 5.5.3.6Rest of Asia Pacific

- 5.5.4Middle East & Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East & Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Alcami Corporation

- 6.3.2Almac Group

- 6.3.3Charles River Laboratories

- 6.3.4Merck KGaA

- 6.3.5Sartorius AG

- 6.3.6SGS SA

- 6.3.7Nelson Laboratories

- 6.3.8Rapid Micro Biosystems

- 6.3.9Thermo Fisher Scientific

- 6.3.10Eurofins Scientific

- 6.3.11Wuxi AppTec

- 6.3.12Pacific Biolabs

- 6.3.13Pace Analytical

- 6.3.14Solvias AG

- 6.3.15Labor LS SE & Co. KG

- 6.3.16Microbac Laboratories

- 6.3.17Fujifilm Diosynth Biotechnologies

- 6.3.18Danaher (Pall Corporation)

- 6.3.19STERIS plc

- 6.3.20BA Sciences

- 6.3.21Toxikon

7. Market Opportunities & Future Outlook

- 7.1White-Space & Unmet-Need Assessment

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Segmentation Overview

- By Product Type

- Instruments

- Kits & Reagents

- Culture Media

- Sterility Testing Accessories

- Others

- Instruments

- By Service Type

- In-house Testing

- Outsourced Sterility Testing Services

- In-house Testing

- By Test Method

- Membrane Filtration

- Direct Inoculation

- Rapid Microbial Methods

- Other Methods

- Membrane Filtration

- By End User

- Pharmaceutical & Biotech Companies

- Medical-Device Manufacturers

- CROs & CDMOs

- Compounding Pharmacies

- Others

- Pharmaceutical & Biotech Companies

- By Geography

- North America

- United States

- Canada

- Mexico

- United States

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Germany

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- China

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- GCC

- South America

- Brazil

- Argentina

- Rest of South America

- Brazil

- North America

Detailed Research Methodology and Data Validation

Primary Research

Desk Research

Market-Sizing & Forecasting

Data Validation & Update Cycle

Why Our Pharmaceutical Sterility Testing Baseline Commands Reliability

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 13.94 B (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 1.93 B (2025) | Global Consultancy A | Excludes instrument sales; uses conservative rapid-method uptake | ||

USD 1.80 B (2024) | Trade Journal B | Captures only outsourced service revenues; omits APAC kit consumption | ||

USD 1.54 B (2025) | Industry Association C | Applies uniform ASPs and annual refresh lag of two years |