Compression Garments And Stockings Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

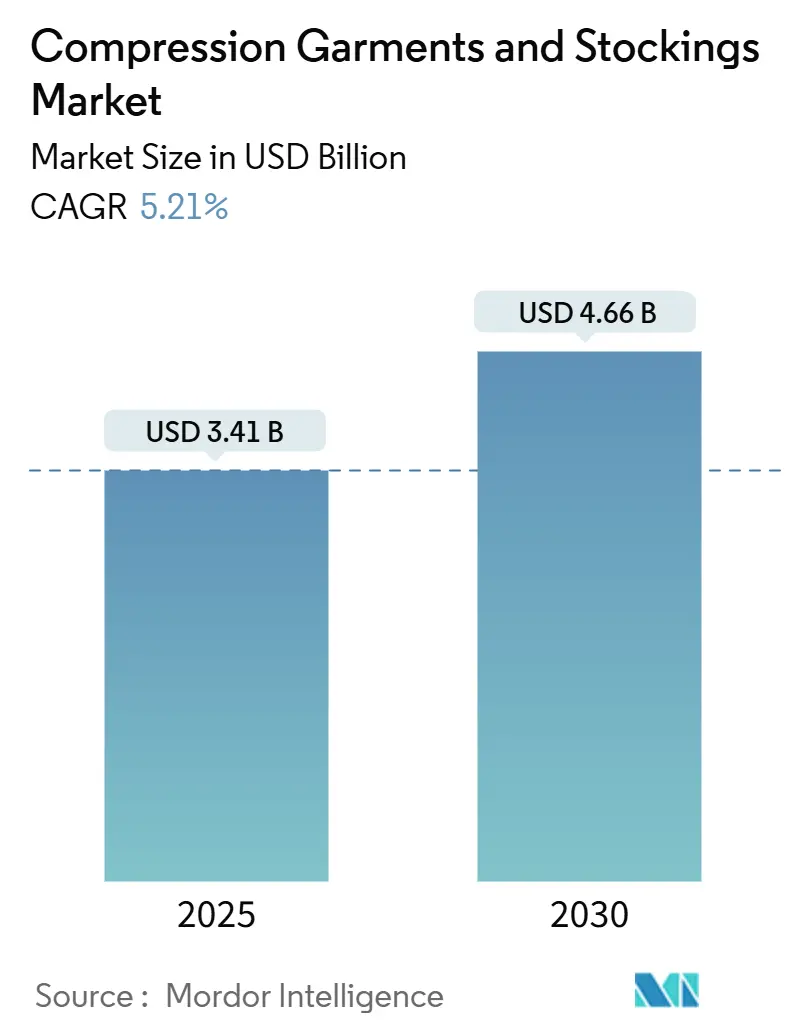

| Market Size (2025) | USD 3.41 Billion |

| Market Size (2030) | USD 4.66 Billion |

| Growth Rate (2025 - 2030) | 5.21% CAGR |

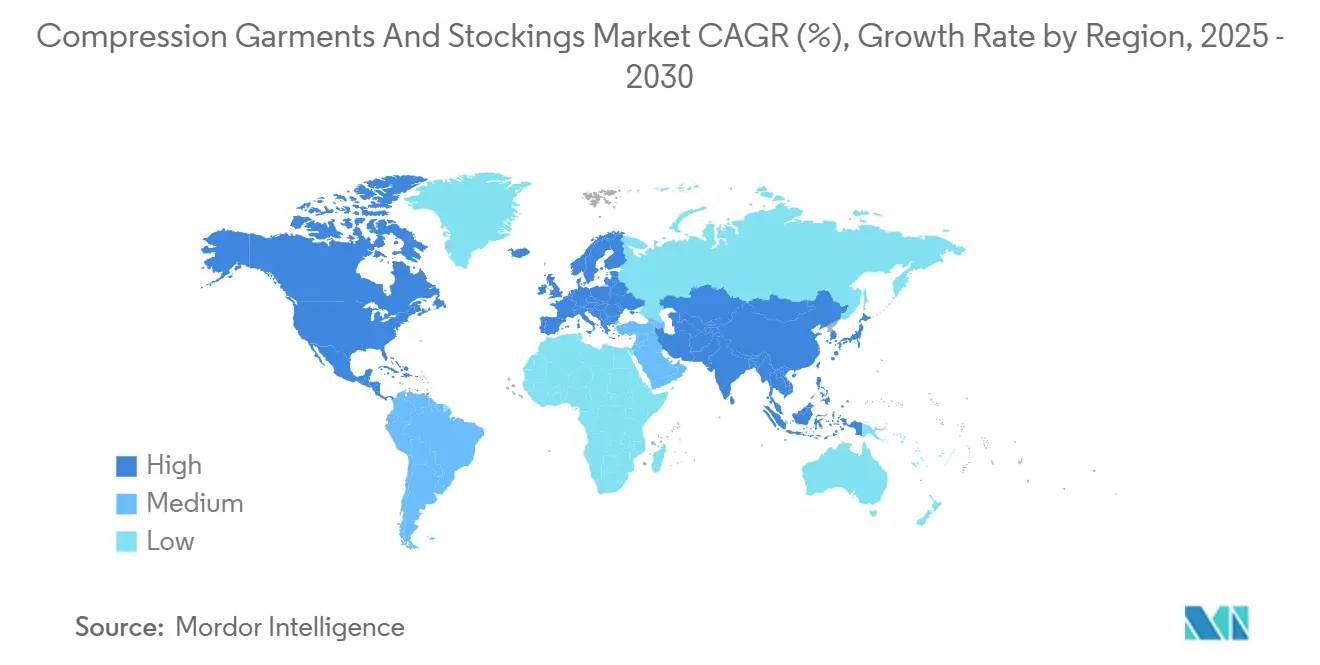

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Compression Garments And Stockings Market Analysis by Mordor Intelligence

The compression garments and stockings market size stands at USD 3.44 billion in 2025 and is forecast to reach USD 4.66 billion by 2030, expanding at a 5.21% CAGR across the period. Steady demand comes from chronic venous disease treatment, preventive wellness adoption, and continual technology upgrades that make compression therapy easier to prescribe, fit, and monitor. Growing surgical volumes, longer life expectancy, and sedentary routines widen the patient pool. Meanwhile, mainstream acceptance of wearable sensors positions intelligent compression as a data-rich pillar of conservative vascular care. Competitive momentum favors brands that can validate therapeutic performance, navigate shifting reimbursement rules, and serve omnichannel shoppers without sacrificing clinical standards.

Key Report Takeaways

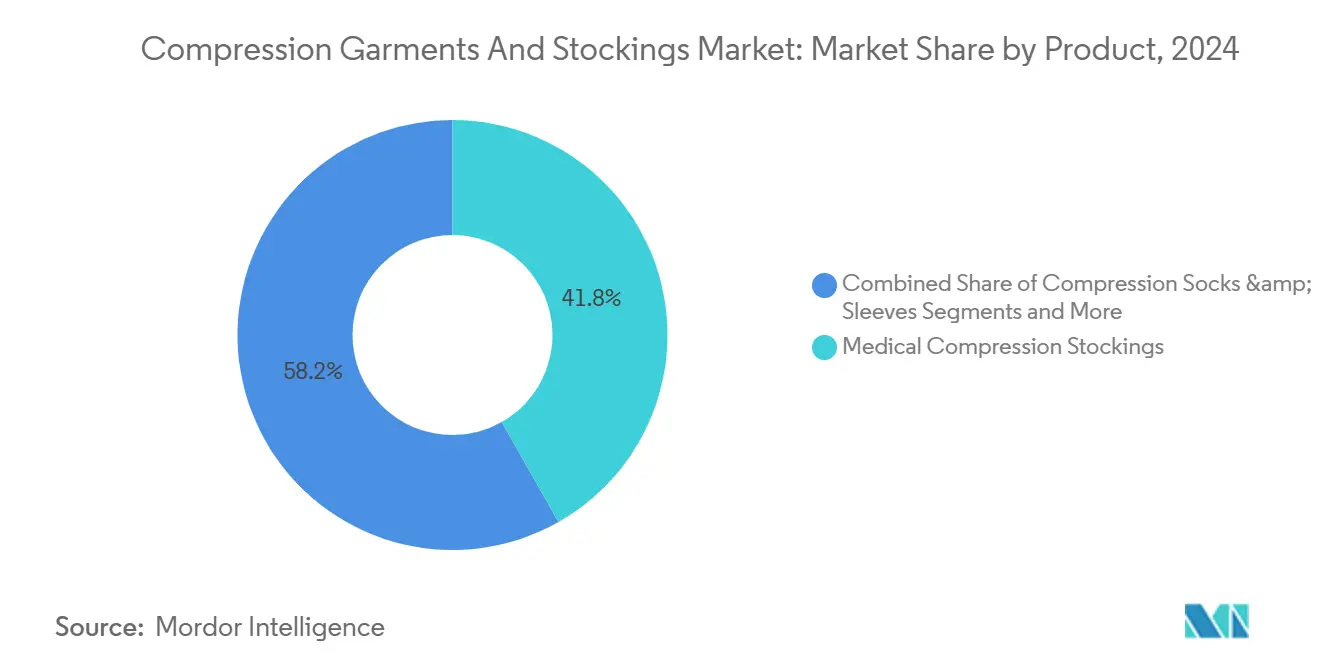

- By product type, medical compression stockings held 41.8% of the compression garments and stockings market share in 2024, whereas post-surgical compression garments are set to record an 8.9% CAGR through 2030.

- By compression class, Class II products accounted for 46.5% share of the compression garments and stockings market size in 2024, while custom and variable compression is projected to expand at 9.7% CAGR over the same horizon.

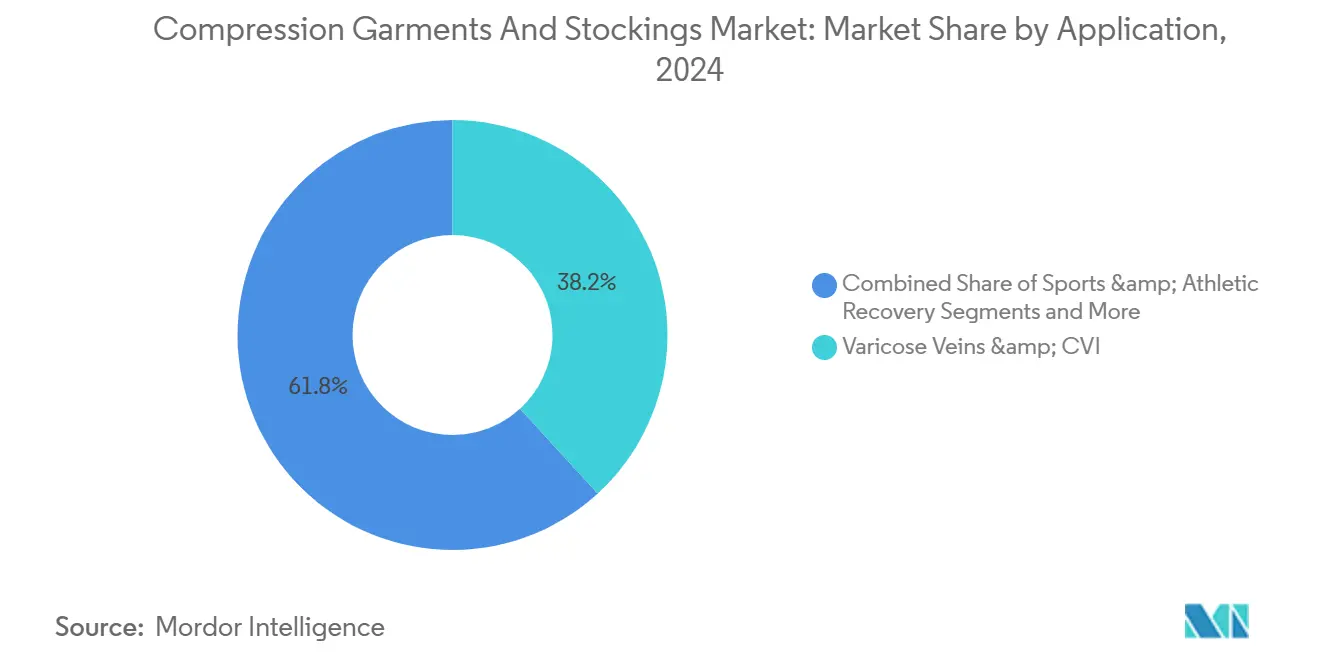

- By application, varicose veins and chronic venous insufficiency dominated with 38.2% revenue share in 2024; sports and athletic recovery is expected to deliver the fastest 8.5% CAGR to 2030.

- By end user, hospitals and surgical centers led with 34.7% share of the compression garments and stockings market size in 2024, although the e-commerce consumer segment is advancing at 9.3% CAGR.

- By geography, North America commanded 37.2% of 2024 revenue, yet Asia Pacific is forecast to post the strongest 6.4% CAGR through 2030.

Global Compression Garments And Stockings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Chronic Venous Disorders & Lymphedema | +1.20% | Global, with higher impact in North America & Europe | Long term (≥ 4 years) |

| Rapid Growth Of E-Commerce & DTC For Medical-Grade Compression Wear | +0.80% | Global, led by North America and the Asia Pacific | Medium term (2-4 years) |

| Aging Population & Sedentary Lifestyles Increasing DVT Risk | +1.00% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Integration Of Smart-Textile Sensors Enabling Compliance Monitoring | +0.60% | North America & EU early adoption, APAC following | Medium term (2-4 years) |

| Post-COVID Surgical Backlog Boosting Demand For Anti-Embolism Stockings | +0.40% | Global, with regional variations in recovery pace | Short term (≤ 2 years) |

| Temperature-Responsive Yarns Unlocking Long-Wear Comfort Benefits | +0.30% | Global, premium market segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Venous Disorders & Lymphedema

Chronic venous insufficiency now affects 25.95% of the global population, with Latin American cohort studies noting prevalence as high as 68.11%. Compression stockings achieve healing rates of 50–75% for venous leg ulcers when appropriately fitted. The 2025 SCAI clinical practice guidelines reinforce compression therapy as first-line care for venous ulcers, further anchoring demand.[1]ScienceDirect Editors, “Prosthetic Venous Valves for Chronic Venous Insufficiency: Advancements and Future Design Directions,” ScienceDirect, sciencedirect.com Lymphedema management is exceptionally durable because garments require replacement every six months; Medicare’s 2024 coverage expansion eliminated a significant economic barrier for U.S. patients. Combined, these epidemiologic and policy factors keep baseline utilization high regardless of economic cycles.

Rapid Growth of E-Commerce & Direct-to-Consumer Models

Online channels shorten the path from manufacturer to patient, raising transparency in price and product details while enabling virtual fitting and subscription replenishment. Digital specialty sites and marketplace storefronts widen global reach, particularly in regions with limited brick-and-mortar medical supply stores. Brands that invest in size-accurate imagery, instructional videos, and responsive tele-consultation convert first-time buyers into repeat subscribers, supporting the 9.3% CAGR projected for the e-commerce consumer segment. The downside is counterfeit proliferation, which can erode therapeutic confidence and push regulators to intensify marketplace policing, adding compliance costs for sellers.

Aging Population & Sedentary Lifestyles Increasing DVT Risk

The global count of peripheral artery disease cases in older adults more than doubled between 1990 and 2021, surpassing 87 million.[2]Chandrasekharan Natarajan-et al., “Trends of Peripheral Artery Disease in the Elderly,” BMC Geriatrics, bmcgeriatr.biomedcentral.com Knee replacement procedures are projected to approach 3 million annually by 2040, each case typically requiring perioperative compression therapy.[3]Juzo Education Team, “Compression Benefits for Knee Replacement Surgery Patients,” Juzo USA, juzousa.com Remote-work habits have extended daily sitting time, spurring preventive use of travel socks and office-friendly sleeves. Because these risk factors stem from demographic structure and lifestyle change, they underpin a stable, long-run growth path that shields the compression garments and stockings market from short-term economic swings.

Integration of Smart-Textile Sensors Enabling Compliance Monitoring

SeamFit garments from Cornell track posture and activity with 93.4% accuracy without external devices, blending conductive threads directly into compression fabric. Tactile Medical’s Nimbl platform links pneumatic sleeves to a mobile app that records session duration, pressure cycles, and symptom scores. Academic labs are pairing organic electrochemical transistors with stretchable yarns to process signals on-fabric, trimming battery bulk, and improving wash durability. Early clinical deployments show higher adherence when patients receive real-time feedback, lowering ulcer recurrence and hospital visits. Cost and wash-cycle lifespan remain hurdles, yet pilot data make a persuasive case for broader payer adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Reimbursement For Off-The-Shelf Garments | -0.70% | Global, varying by healthcare system | Long term (≥ 4 years) |

| Patient Non-Adherence Due To Donning Difficulty | -0.50% | Global, higher impact in elderly populations | Medium term (2-4 years) |

| Fragmented Regulatory Standards Outside US/EU | -0.30% | Emerging markets, developing regions | Long term (≥ 4 years) |

| Counterfeit Products On Online Marketplaces Eroding Brand Trust | -0.40% | Global, concentrated in e-commerce channels | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Reimbursement for Off-the-Shelf Garments

Coverage inconsistency hampers preventive uptake. U.S. private insurers often restrict benefits to physician-prescribed garments, and European payers vary widely in defining medical necessity. Patients without coverage turn to out-of-pocket purchases, which skews demand toward lower-priced, lighter-pressure products that may not achieve clinical goals. Reimbursement gaps also discourage clinicians from standardizing compression therapy for early-stage venous disease. Growing acceptance of health-savings-account reimbursement offers partial relief, yet administrative complexity deters broad utilization.

Patient Non-Adherence Due to Donning Difficulty

Application challenges remain the top cause of therapy discontinuation, especially among seniors and people with limited dexterity. While zippers, slanted cuffs, and glide-on aids improve usability, they can compromise graduated pressure or shorten garment lifespan. Premium adaptive devices address complex cases but carry price tags beyond many insurance caps. These usability barriers translate into missed therapy days, ulcer recurrence, and avoidable hospitalizations, tempering the overall compression garments and stockings market growth potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Medical Stockings Maintain Dominance as Post-Surgical Garments Surge

Medical stockings produced 41.8% of 2024 revenue, underscoring their central role in hospital discharge kits and chronic care regimens. They remain the baseline product for documenting pressure gradients under ISO and FDA Class II rules, giving clinicians high confidence in therapeutic effect. Post-surgical compression garments, although smaller in absolute terms, are pacing the field at an 8.9% CAGR, fueled by outpatient surgery expansion and protocols that prioritize early mobilization. Sleeves and socks attract athletes and travelers seeking light preventive pressures, whereas bandages and wraps retain importance in wound clinics for adjustable compression and edema management.

Product innovation intertwines with material science. Temperature-responsive yarns keep wearers comfortable across climates, and recycled elastane meets hospital sustainability mandates. Smart-sensor integration is penetrating stockings first because the lower limb remains the primary treatment site for chronic venous disease. In parallel, post-surgical lines add targeted panels and easy closures to simplify nurse application. As supply chains stabilize post-pandemic, SKU breadth increases, enabling fit for diverse limb geometries and driving repeat purchase frequency within the compression garments and stockings market.

By Compression Class: Class II Leads, Custom & Variable Compression Gain Traction

Class II (30–40 mmHg) devices controlled 46.5% share of the compression garments and stockings market size in 2024, aligning with guideline-preferred pressure levels for venous ulcers and post-operative DVT prophylaxis. Hospitals standardize around Class II to streamline inventory and staff training. Custom and variable compression offerings, though niche today, are forecast to climb 9.7% CAGR as 3-D knitting and on-demand manufacturing lower cost-per-fit.

Variable models embed pneumatic or shape-memory elements that adjust pressure in response to movement, potentially resolving the trade-off between daytime comfort and therapeutic rigor. Meanwhile, Class I garments cater to moderate swelling and preventive travel needs, and Class III/IV products serve severe lymphedema cases under specialist oversight. European RAL and DIN standards ensure uniform pressure testing, giving prescribers confidence when switching among brands. Overall, class diversification lets manufacturers segment pricing and broaden appeal without diluting clinical integrity.

By Application: Varicose Veins Anchor Demand, Sports Recovery Accelerates

Varicose veins and chronic venous insufficiency treatments generated 38.2% of 2024 sales, reflecting both high prevalence and acceptance of compression as first-line therapy. Wound clinics and dermatology practices drive repeat orders, as ulcer patients require replacement pairs every 4–6 months to maintain compression fidelity. Deep vein thrombosis prophylaxis remains steady, tethered to surgical volume rather than macroeconomics.

Sports and athletic recovery is the bright spot, projected to rise at an 8.5% CAGR. Evidence that sleeves attenuate muscle oscillation and speed lactate clearance has convinced coaches and rehabilitation specialists to include compression in training kits. Lymphedema management, while smaller numerically, delivers high lifetime value; patients often need multiple custom pieces and ancillary accessories. Post-partum compression emerges as an under-tapped niche, particularly in the Asia Pacific, where cultural emphasis on post-natal care dovetails with rising purchasing power.

By End User: Hospitals Retain Procurement Clout; E-Commerce Propels Consumer Reach

Hospitals and surgical centers controlled 34.7% of 2024 revenue, leveraging bundled purchasing contracts and post-acute care protocols that embed stockings in discharge packs. Their volume ensures stable baseline orders and creates clinical endorsement that spills over to retail channels. Ambulatory and specialty clinics complement hospitals by fitting chronic patients and teaching donning techniques, adding ancillary revenue to their service mix.

E-commerce, however, is the fastest-growing venue at 9.3% CAGR, reshaping how patients discover, select, and replenish garments. Platforms integrate video consultations and 3-D size scanners to reduce return rates, a critical margin lever for elastic textiles. Home-care settings benefit from telehealth prescriptions, enabling nurses to monitor leg circumference and skin integrity remotely. Fitness clubs and physiotherapy centers round out the mix, stocking sleeves and tights for members focused on prevention and performance. Channel convergence means manufacturers must synchronize inventory across medical, retail, and online nodes to preserve brand positioning in the compression garments and stockings market.

Geography Analysis

North America generated the largest revenue share at 37.2% in 2024, supported by comprehensive reimbursement for therapeutic stockings, high obesity rates, and robust surgical throughput. U.S. Medicare’s inclusion of lymphedema garments in 2024 materially expanded the addressable base, while Canada’s provincial health plans offer partial subsidies that encourage early adoption. E-commerce penetration is also high, providing manufacturers a direct conduit to rural patients who previously depended on urban medical supply stores.

Europe ranks second but navigates the ongoing transition to the EU Medical Device Regulation. Although MDR compliance costs temper small-entrant activity, the rules raise overall quality, reinforcing clinician trust and enabling export of CE-marked goods to Middle Eastern and African buyers. Classifications under DIN 58133 keep pressure tolerances tight, aiding cross-border standardization. Germany, France, and the Nordic region show mature replacement cycles, whereas Eastern Europe offers growth upside as healthcare spending per capita rises.

Asia Pacific, advancing at a 6.4% CAGR, combines rapid population aging with rising middle-class purchasing power. Japan and South Korea pioneered compression therapy decades ago and now adopt smart-textile variants early. China’s tier-2 cities see growing outpatient surgery centers stocking post-operative garments, and digital platforms handle the bulk of sales to remote provinces. India’s lymphedema burden, tied to filariasis, presents a public-health opportunity once coverage schemes broaden.

Latin America records high venous disease prevalence but lower treatment penetration. Brazil’s private insurers started reimbursing high-pressure stockings for ulcer cases, yet economic volatility slows category upgrades. Meanwhile, the Middle East and Africa remain nascent. Urban centers in the Gulf import premium European brands, while national health systems in sub-Saharan Africa focus resources on infectious diseases, leaving compression therapy primarily in private clinics. Over the forecast window, knowledge transfer from European manufacturers and telehealth initiatives could accelerate adoption, positioning emerging regions as future volume drivers of the compression garments and stockings market.

Competitive Landscape

The market sits at a mid-fragmented equilibrium where the top five manufacturers command significant presence in hospitals yet face nimble challengers online. SIGVARIS, Medi GmbH, and Essity’s BSN Medical sustain leadership by pairing clinical validation with broad SKU depth and global regulatory muscle. They invest in R&D that marries knit precision with recyclable yarns, aligning with hospital sustainability goals. 3M leverages material science to refresh the FUTURO range with softer, four-way-stretch fabrics, broadening appeal to people living with arthritis.

Tactile Medical bridges pneumatic compression and smart connectivity, giving payers outcome data that supports reimbursement renewals. Start-ups concentrate on direct-to-consumer niches, using influencer campaigns and subscription logistics to scale rapidly among travelers and gamers. Partnerships with telehealth platforms surface as a route to capture prescription-linked e-commerce sales. Suppliers of conductive yarns and bio-based elastomers hope to lock in long-term contracts as brands scramble for differentiated components.

Regulatory agility becomes a competitive wedge. Companies with established MDR technical files face lower incremental costs when adding sensor modules than new entrants who must secure complete device certifications. Channel diversification also matters; hospital volume shields revenue during economic downturns, while consumer channels supply faster growth. Overall, rivalry is defined less by price and more by evidence-backed performance, sustainability credentials, and omnichannel execution—factors that will keep churn moderate and margins stable within the compression garments and stockings market.

Compression Garments And Stockings Industry Leaders

3M

Medi GmbH & Co. KG

Sigvaris Group

Essity Medical Solutions

Bauerfeind AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: 3M introduced redesigned FUTURO premium sleeves with ultra-soft four-way stretch fabric for day-long wear.

- February 2025: Tactile Medical expanded Nimbl pneumatic compression to lower-extremity lymphedema, featuring a 68% lighter pump and Bluetooth adherence tracking.

- December 2024: Hyosung debuted CREORA cooling yarns delivering 10% enhanced thermal regulation for medical and sports compression lines.

Global Compression Garments And Stockings Market Report Scope

| Medical Compression Stockings |

| Compression Socks & Sleeves |

| Compression Bandages & Wraps |

| Compression Shorts & Tights |

| Post-surgical Compression Garments |

| Varicose Veins & CVI |

| Deep Vein Thrombosis (DVT) Prophylaxis |

| Lymphedema Management |

| Sports & Athletic Recovery |

| Post-surgical & Post-partum Care |

| Hospitals & Surgical Centers |

| Ambulatory & Specialty Clinics |

| Home-care Settings |

| Health & Fitness Clubs |

| E-commerce Consumers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Medical Compression Stockings | |

| Compression Socks & Sleeves | ||

| Compression Bandages & Wraps | ||

| Compression Shorts & Tights | ||

| Post-surgical Compression Garments | ||

| By Application | Varicose Veins & CVI | |

| Deep Vein Thrombosis (DVT) Prophylaxis | ||

| Lymphedema Management | ||

| Sports & Athletic Recovery | ||

| Post-surgical & Post-partum Care | ||

| By End User | Hospitals & Surgical Centers | |

| Ambulatory & Specialty Clinics | ||

| Home-care Settings | ||

| Health & Fitness Clubs | ||

| E-commerce Consumers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the compression garments and stockings market in 2025?

The compression garments and stockings market size is USD 3.44 billion in 2025.

What is the expected growth rate for compression garments and stockings through 2030?

Aggregate revenue is forecast to rise at a 5.21% CAGR, reaching USD 4.66 billion by 2030.

Which product type currently holds the most significant share?

Medical compression stockings control 41.8% of 2024 sales, reflecting their long-standing role in venous care.

Which channel is growing fastest for compression garments?

E-commerce consumers are projected to expand purchases at a 9.3% CAGR as digital fitting and subscription models gain traction.

Which region is poised for the strongest expansion?

Asia Pacific is forecast to lead growth with a 6.4% CAGR thanks to aging demographics and broader healthcare access.

What technological trend is reshaping the category?

Integration of smart-textile sensors that capture pressure data and adherence metrics is transforming both clinical oversight and consumer engagement.

Page last updated on: