Meat Extract Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

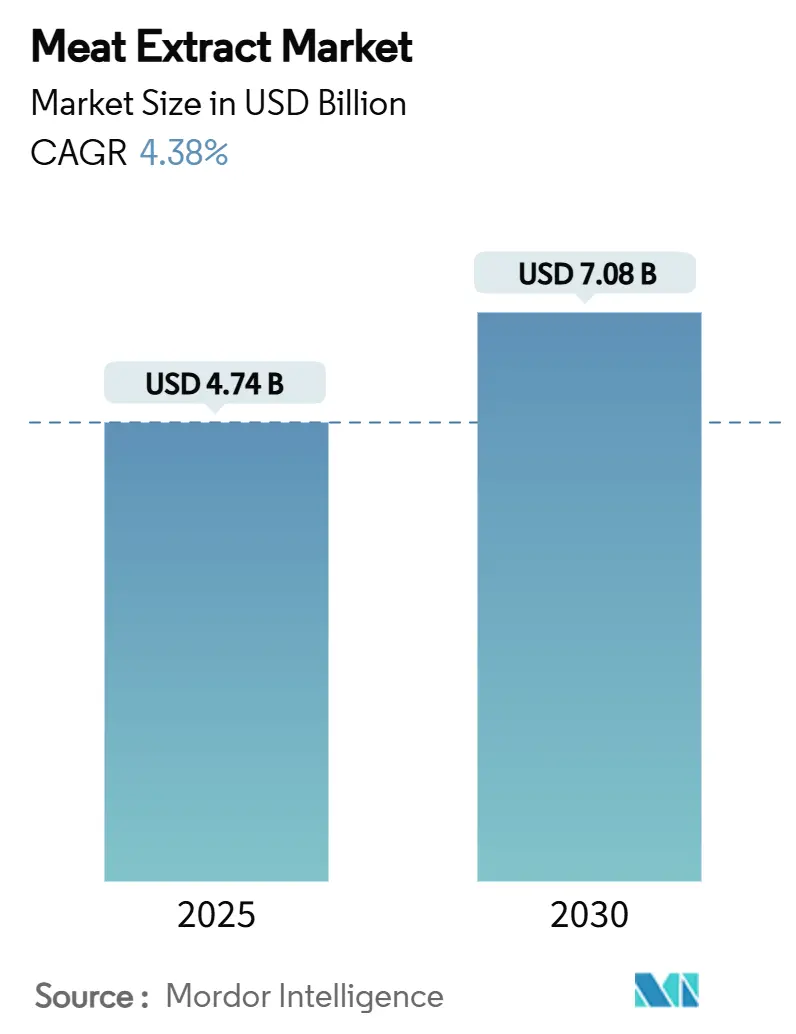

| Market Size (2025) | USD 4.74 Billion |

| Market Size (2030) | USD 7.08 Billion |

| Growth Rate (2025 - 2030) | 4.38% CAGR |

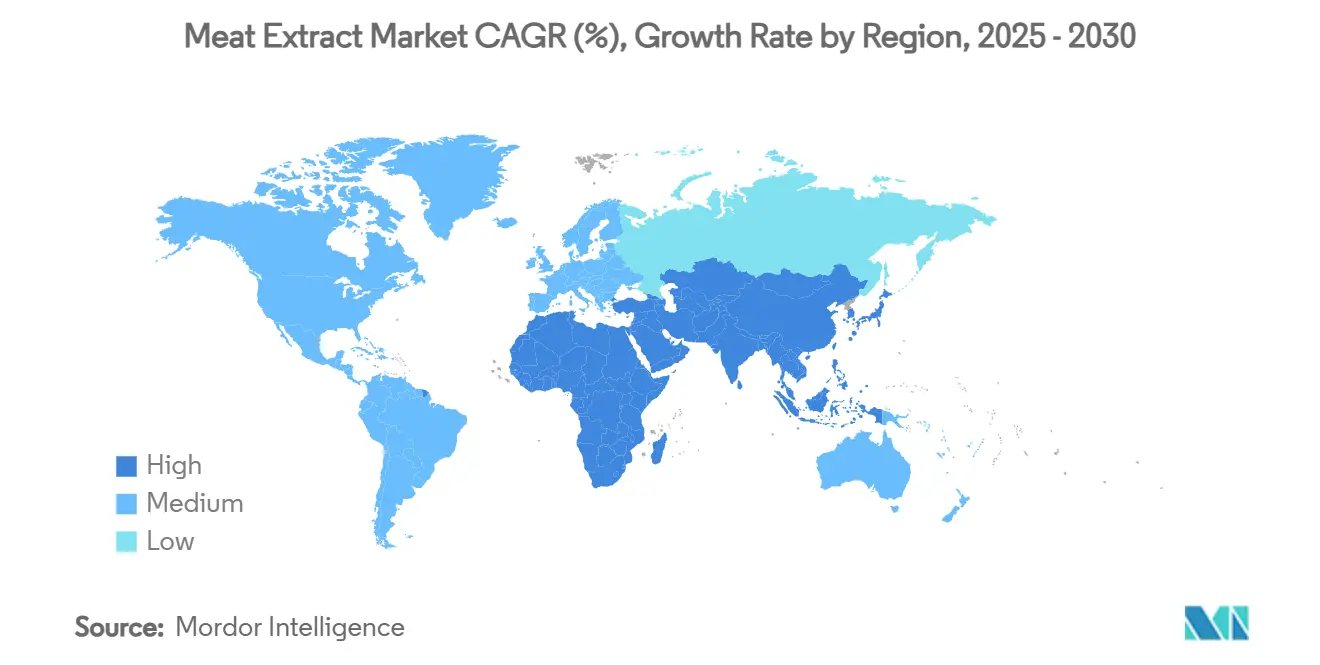

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Meat Extract Market Analysis by Mordor Intelligence

The meat extract market size reached USD 4.74 billion in 2025 and is projected to achieve USD 7.08 billion by 2030, reflecting an 8.38% CAGR through the forecast period. This strong upward trajectory is underpinned by rising demand for protein-rich convenience foods, wider adoption of savoury flavour bases in soups and sauces, and the expanding use of meat extracts in cell-culture media. Powder formats dominate procurement decisions because of superior shelf stability, while liquid concentrates are quickly gaining ground in foodservice kitchens. Technology investments in enzymatic hydrolysis have raised protein density and flavour consistency, allowing manufacturers to respond to clean-label preferences and sustainability expectations. Regional performance skews toward Asia-Pacific, which benefits from urbanisation and higher disposable incomes, whereas the Middle East and Africa is advancing the fastest as young populations adopt modern packaged foods.

Key Report Takeaways

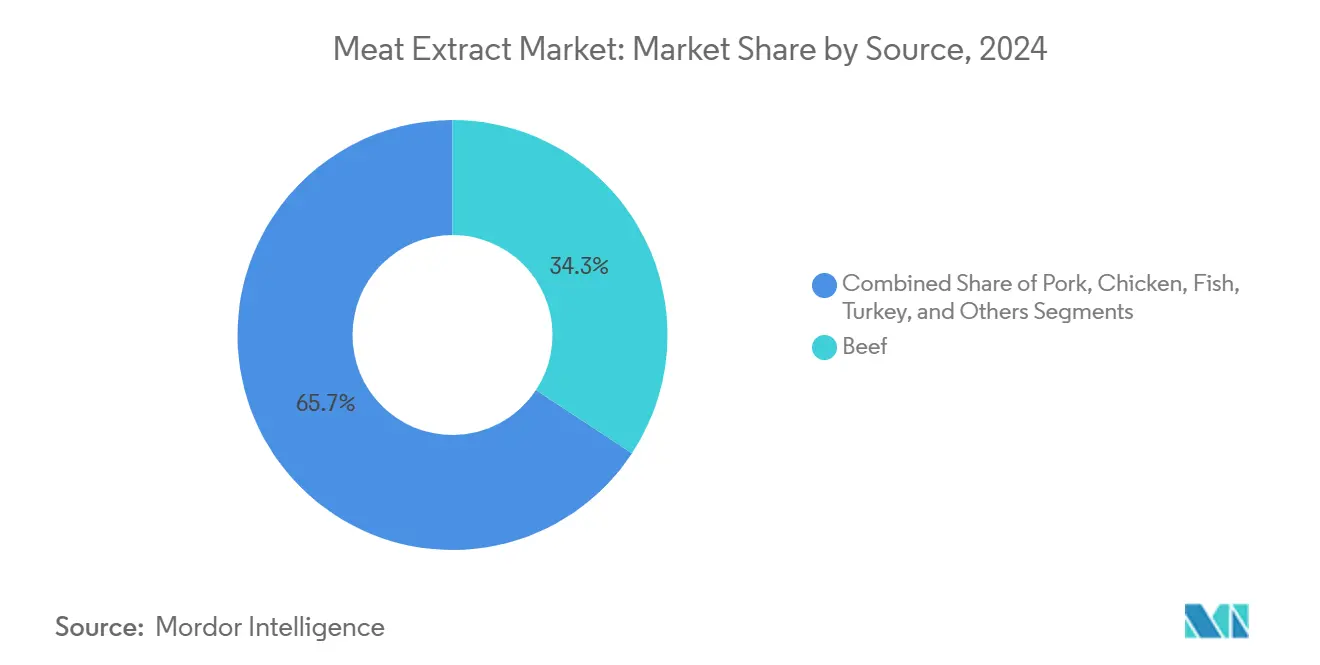

- By source, beef extracts held 34.26% of meat extract market share in 2024 while fish extracts are expanding at an 8.58% CAGR through 2030.

- By form, powder commanded 45.18% share of the meat extract market size in 2024, and liquid concentrates are forecast to grow at 9.17% CAGR to 2030.

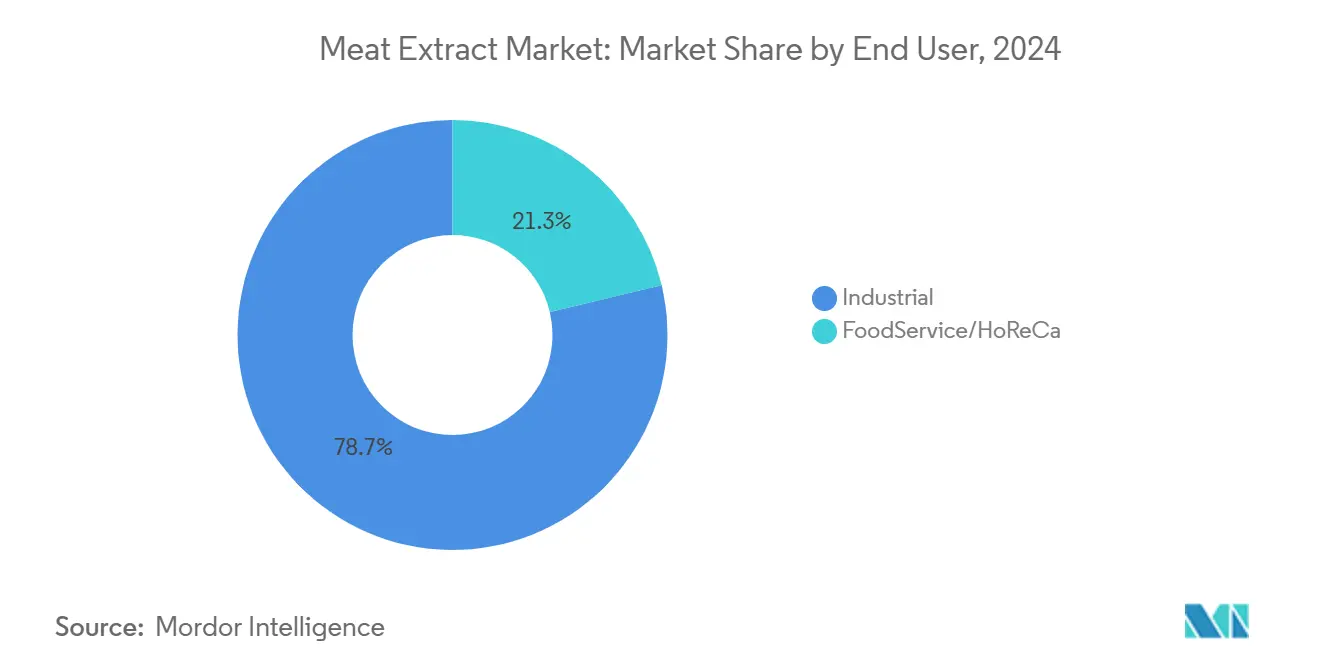

- By end user, industrial applications accounted for 78.57% of meat extract market size in 2024 and foodservice is recording the highest projected CAGR at 9.68% through 2030.

- By geography, Asia-Pacific secured 37.94% revenue share in 2024, while the Middle East and Africa is set to advance at an 8.34% CAGR to 2030.

Global Meat Extract Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for protein-rich convenience foods | +2.1% | North America, Asia-Pacific | Medium term (2-4 years) |

| Growth in savoury flavour applications in soups & sauces | +1.8% | Europe, Asia-Pacific | Short term (≤ 2 years) |

| Clean-label and natural ingredient preference | +1.2% | North America, EU, expanding Asia-Pacific | Long term (≥ 4 years) |

| Expansion of pet-food and animal nutrition uses | +0.9% | North America, Europe | Medium term (2-4 years) |

| Adoption in biopharma & cell-culture media | +0.8% | North America, EU, spill-over Asia-Pacific | Long term (≥ 4 years) |

| Sustainability-driven valorisation of meat co-products | +0.6% | EU, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for protein-rich convenience foods

Time-pressed consumers across demographics are choosing ready-to-heat meals fortified with concentrated protein derived from beef, pork, poultry, and fish extracts. Uniform labelling dates set by the USDA FSIS provide clarity for reformulations, encouraging manufacturers to launch new protein-dense SKUs[1]Food Safety and Inspection Service. "Uniform Compliance Date for Food Labeling Regulations." November 27, 2024. https://www.federalregister.gov/documents/2024/11/27/2024-27864/uniform-compliance-date-for-food-labeling-regulations. Enzymatic hydrolysis has boosted amino acid recovery without compromising taste, letting brands balance nutrition and flavour. Retailers are allocating greater shelf space to high-protein soups, sauces, and snacks, reinforcing downstream demand. Emerging convenience formats in retort pouches and microwavable cups further embed meat extracts into everyday meal routines.

Growth in savoury flavour applications in soups & sauces

Umami-forward culinary trends favour meat extracts as concentrated flavour bases for bouillons, ramen broths, curries, and gravies. Novozymes’ tailored enzyme solutions intensify peptide release and simultaneously cut sodium, satisfying dual mandates for taste and health. Foodservice chains value the reproducible flavour profile that powdered or liquid beef and chicken extracts deliver across multi-unit operations. In Europe, low-salt gravy cubes fortified with meat extract are ramping up supermarket penetration. The result is wider application breadth that lifts volume demand even in relatively mature regions.

Clean-label and natural ingredient preference

Consumers equate shorter ingredient lists with quality, fueling a shift from synthetic flavours toward natural meat extracts. The FDA’s 2024 decision to revoke 52 outdated standards of identity signals agency support for innovation in natural ingredients. Manufacturers now highlight gentle extraction processes and traceable livestock sourcing on packs. Clear-label positioning allows premium pricing that offsets raw-material volatility. EU producers adopting low-temperature vacuum evaporation underscore provenance and animal-welfare messaging, deepening consumer trust.

Expansion of pet-food and animal nutrition uses

Premiumisation has reached the companion-animal aisle, where brand owners formulate with human-grade beef and fish extracts to boost palatability and protein density. Functional treats containing concentrated turkey extract address joint health and senior-pet vitality. Regulatory guidelines for pet-food labelling are tightening, aligning quality expectations with human food norms. Mid-size processors across Latin America are importing powdered meat extracts to accelerate new-product rollout, widening geographic demand coverage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying plant-based alternatives competition | -1.4% | Global, with concentration in North America & EU | Short term (≤ 2 years) |

| Volatility in livestock raw-material costs | -0.7% | Global, with acute impact in emerging markets | Medium term (2-4 years) |

| Stricter carbon-footprint labelling regulations | -0.5% | EU & North America primary, expanding to APAC | Long term (≥ 4 years) |

| Technological advances in non-meat umami substitutes | -0.4% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intensifying plant-based alternatives competition

Enzymatically hydrolysed pea or soy proteins now mimic beefy or chicken-like flavour notes, offering manufacturers allergen-controlled options that lower carbon footprints. Novozymes’ vegetable-protein solutions are already replacing meat extracts in bouillon cubes aimed at flexitarian consumers. Retailers in Western Europe position plant-based gravy bases adjacent to traditional jars, creating direct substitution risk. Corporate climate targets and carbon-labelling schemes reinforce the shift. This rivalry pressures meat extract processors to emphasise traceability, humane sourcing, and improved extraction yields to safeguard share.

Volatility in livestock raw-material costs

Feed price spikes, African Swine Fever outbreaks, and drought-driven herd reductions distort supply of trimmings and bones used in extract production. Spot-market raw-material premiums compress processor margins, especially in cost-sensitive emerging markets with limited hedging. Currency depreciation in Brazil and South Africa amplifies import costs for extraction enzymes and stainless-steel equipment. Makers respond by expanding thermal-hydrolysis capacity that unlocks incremental collagen from the same input tonnage, cushioning supply shocks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Beef Dominance Meets Fish Innovation

Beef extracts generated the largest revenue of 34.26% in 2024, underpinned by omnipresent use in bouillons, gravies, and ramen bases. Robust cold-chain infrastructure in North America and Europe underwrites stable raw-material flows. Clear USDA identity standards facilitate cross-border trade, giving multinational formulators confidence. Fish extracts are scaling rapidly at an 8.58% CAGR as processors valorise salmon heads and tuna frames into omega-3 enriched concentrates. Technological strides in membrane filtration suppress fishy off-notes, expanding adoption in nutraceutical capsules. Pork and chicken extracts fill mid-priced savoury applications in Asia, where cuisine traditions align with pork bone soup and chicken essences.

Powdered beef extract continues to anchor many industrial recipes because of its long ambient shelf life and compatibility with automated dosing systems. Yet liquid fish extract is carving space in premium ramen shops across Japan and South Korea, valued for quick dispersion and clean ingredient declarations. Turkey and mixed-species blends remain niche, used mainly by value-positioned snacks seeking differentiated flavour cues.

By Form: Powder Practicality Versus Liquid Innovation

Powder remains the default format for industrial plants that run high-speed sachet filling lines. Its 45.18% market share derives from low water activity, which delivers two-year shelf life without preservatives. Air-spray drying locks in amino acids and volatile flavour compounds, preserving sensory attributes. Inventory costs stay contained because powders stack efficiently on pallets and tolerate wider temperature swings during transport.

Liquid concentrates are posting a 9.17% CAGR as chefs in QSR chains pursue speed and precision. Bag-in-box packs allow mess-free dispensing directly into stock pots, cutting prep labour. Viscous concentrates integrate smoothly into icy sauces, eliminating grit often associated with reconstituted powders. Pastes cater to European charcuterie and pâté producers that prize rich mouthfeel. Twin-screw extruders create custom paste consistencies, though higher water activity demands chilled storage.

By End User: Industrial Scale Meets Foodservice Growth

Industrial food manufacturers absorb 78.57% of global volume, converting powdered meat extracts into instant noodle seasonings, canned stews, and savoury snack coatings. Long tenure recipes deter dilution by substitutes because reformulation risks brand equity. Continuous kettles and vacuum evaporators installed at scale deliver unit-cost advantages unattainable for smaller rivals, reinforcing volume concentration.

Foodservice and HoReCa is forecast to expand at 9.68% CAGR as restaurant operators outsource stock preparation to control labour costs. Central kitchens for quick-service brands add liquid chicken and beef extracts to base sauces for burgers and rice bowls, ensuring flavour uniformity across franchises. Hotels in Gulf Cooperation Council states deploy fish extract cubes in large banquets catering to diversified palates. The segment benefits from tourism recovery and the growth of cloud-kitchen models that demand shelf-stable yet premium flavour enhancers.

Geography Analysis

Asia-Pacific held 37.94% of global revenue in 2024, propelled by China and India where middle-class households allocate greater spend to packaged soups and frozen dumplings. Urban convenience stores promote microwaveable broth cups containing powdered meat extract, reinforcing volume throughput. Government support for modern slaughtering hubs in Vietnam and Indonesia ensures steady supply of raw materials, lowering production costs. Japan and South Korea favour high-purity fish extracts for ramen and hot-pot restaurants, reflecting a deep culinary heritage that appreciates marine flavours.

The Middle East and Africa region is climbing at an 8.34% CAGR. Gulf states import powdered beef extract for kabsa rice mixes, while South African processors enhance biltong and soup cubes with liquid chicken extract. Infrastructure investments in cold-storage corridors improve raw-material safety, encouraging local extraction plants. Youthful demographics and growing quick-service chains extend penetration beyond affluent consumer groups.

North America exhibits mature but resilient demand, driven by premium snack innovation and clean-label packaged meals. Mexican ready-meal producers integrate pork extract into carnitas sauces, supported by cross-border livestock flows. Europe demonstrates steady uptake, aided by EU guidance on sustainable co-product utilisation. Tight environmental regulations incentivise processors to maximise protein extraction from carcass remnants, turning compliance costs into revenue streams. South America leverages abundant cattle supplies; Brazilian firms export powdered bovine extract to Asian seasoning houses, capitalising on favourable currency exchange.

Competitive Landscape

The meat extract market is moderately concentrated. Global flavour houses such as Givaudan leverage proprietary enzyme systems and worldwide distribution, underpinning double-digit revenue growth in 2024. DSM-Firmenich’s divestiture of its animal-nutrition arm narrows focus onto high-margin speciality ingredients, freeing capital for fermentation technology that could lower extraction costs.

Emerging regional players specialise in niche flavours like halal goat extract or clean-label fish collagen peptides. Their agility enables fast customisation for smaller customers overlooked by multinationals. Strategic alliances between extract makers and rapid-frozen meal brands lock in multi-year supply contracts, reinforcing incumbents’ share.

Vertical integration across slaughtering, rendering, and extraction promotes cost efficiency and traceability. Innovation pipelines include membrane-filtered concentrates for low-sodium snacks and biotech-grade bovine extracts for cultivated-meat media. Competitive advantage increasingly hinges on demonstrating low carbon intensity and full livestock traceability.

Meat Extract Industry Leaders

-

Givaudan SA

-

Kerry Group PLC

-

DSM- Firmenich

-

Essentia Protein Solutions

-

International Dehydrated Foods

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: JBS SA agreed to acquire The Vegetarian Butcher from Unilever, signalling portfolio diversification into plant-based proteins.

- December 2022: Essentia Protein Solutions announces plans to build a new broth manufacturing plans to build a new broth manufacturing plant near Dalton, GA. The greenfield plant processes USDA-inspected, refrigerated raw material to produce food-grade stocks, broths, and fats.

Global Meat Extract Market Report Scope

| Beef |

| Pork |

| Chicken |

| Fish |

| Turkey |

| Other Sources |

| Powder |

| Paste |

| Liquid Concentrate |

| Other Forms |

| Foodservice and HoReCa | |

| Industrial | Soups and Bouillons |

| Sauces and Dressings | |

| Ready Meals and Instant Noodles | |

| Snacks and Seasonings | |

| Nutraceuticals & Dietary Supplements | |

| Baby Food | |

| Pet Food | |

| Biotechnology & Culture Media | |

| Other Industries |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Source | Beef | |

| Pork | ||

| Chicken | ||

| Fish | ||

| Turkey | ||

| Other Sources | ||

| By Form | Powder | |

| Paste | ||

| Liquid Concentrate | ||

| Other Forms | ||

| By End User | Foodservice and HoReCa | |

| Industrial | Soups and Bouillons | |

| Sauces and Dressings | ||

| Ready Meals and Instant Noodles | ||

| Snacks and Seasonings | ||

| Nutraceuticals & Dietary Supplements | ||

| Baby Food | ||

| Pet Food | ||

| Biotechnology & Culture Media | ||

| Other Industries | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the meat extract market?

The meat extract market size reached USD 4.74 billion in 2025 and is forecast to rise to USD 7.08 billion by 2030.

Which source segment leads revenue contribution?

Beef extracts led with 34.26% of meat extract market share in 2024 due to their universal flavour acceptance and established supply chains.

Which region grows fastest through 2030?

The Middle East and Africa is projected to record the fastest regional CAGR at 8.34% as urbanising populations embrace convenience foods.

Why are liquid concentrates gaining popularity?

Liquid meat extract concentrates support quick dispersion and labour savings in foodservice kitchens, driving a 9.17% CAGR in the segment.

Page last updated on: