Seafood Extracts Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 10.98 Billion |

| Market Size (2031) | USD 15.13 Billion |

| Growth Rate (2026 - 2031) | 6.62% CAGR |

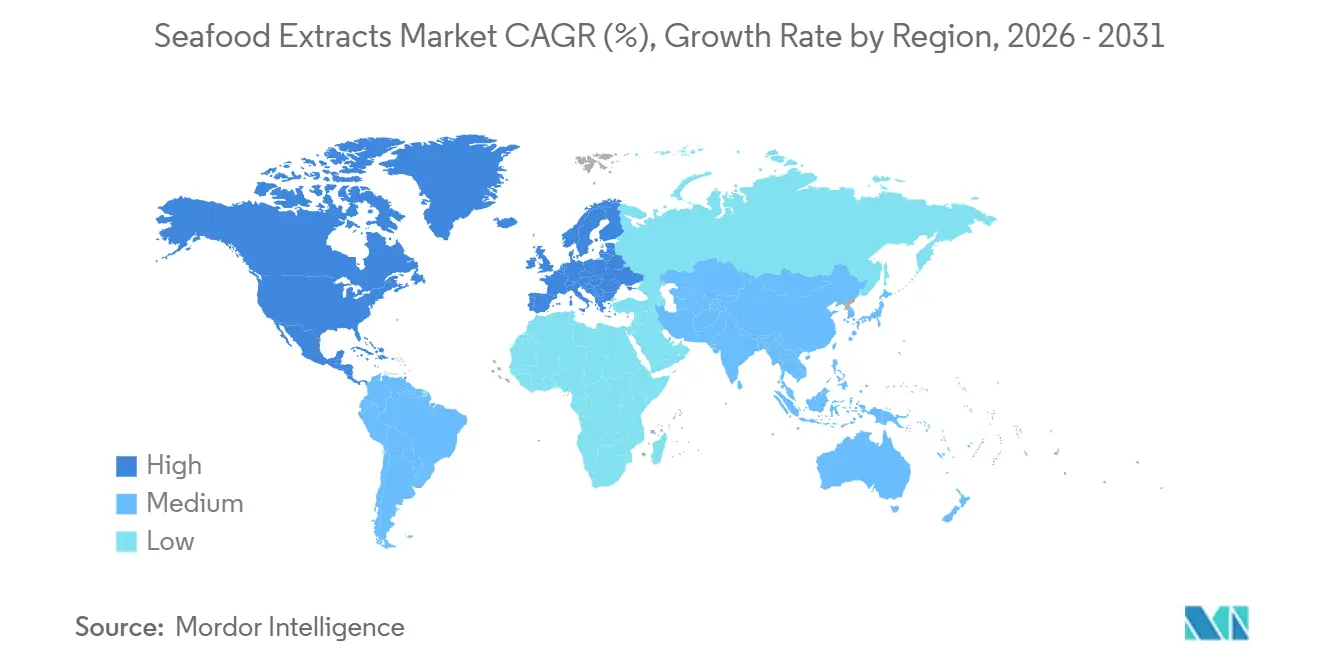

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Seafood Extracts Market Analysis by Mordor Intelligence

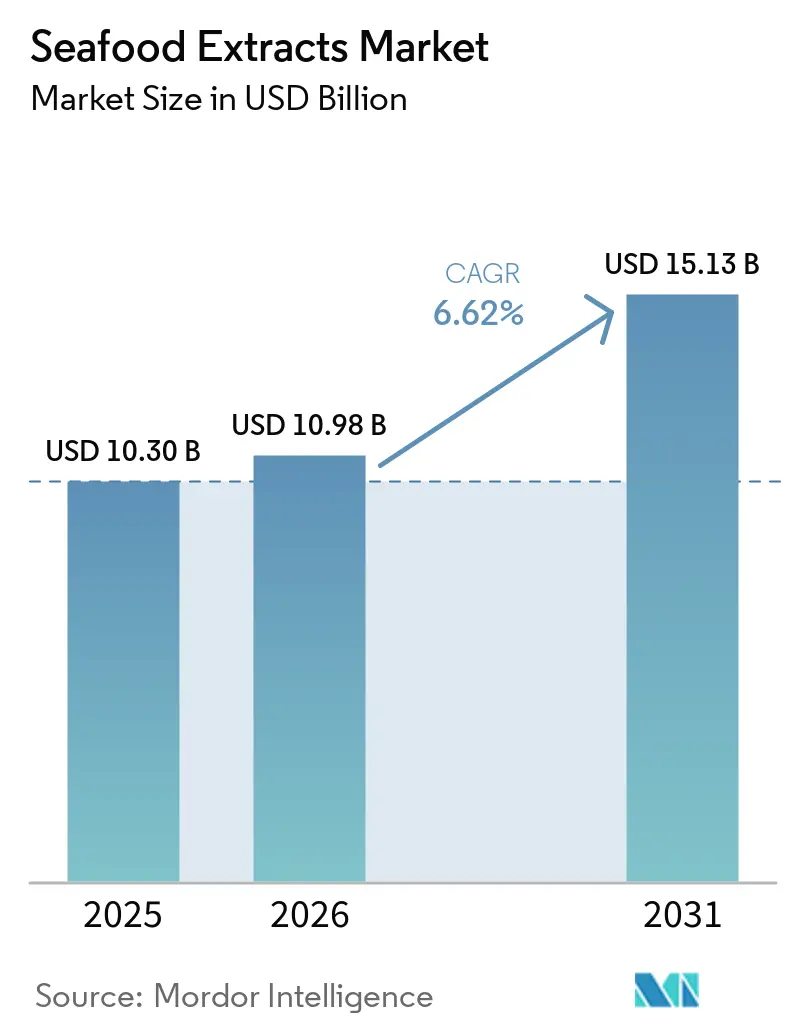

The Seafood Extracts Market size is projected to be USD 10.30 billion in 2025, USD 10.98 billion in 2026, and reach USD 15.13 billion by 2031, growing at a CAGR of 6.62% from 2026 to 2031. Wide adoption of marine-derived bioactives, stricter clean-label preferences, scalable aquaculture systems, and continual progress in supercritical CO₂ and deep eutectic solvent extraction technologies sustain long-run expansion. Consumer trust in recognizable ingredients accelerates the shift away from synthetic additives, while regulatory bodies raise quality benchmarks that favor suppliers able to certify sustainability and traceability. For instance, according to the International Food Information Council, in 2025, approximately 13% of respondents in the United States mentioned that they prefer "clean eating"[1]Source: International Food Information Council, "2025 Food and Health Survey", www.ific.org. Vertical integration by established processors secures raw-material flow and unlocks circular-economy valorization of by-products. At the same time, biotechnology entrants shorten development cycles, intensifying innovation across food, nutraceutical, cosmetic, and feed applications.

Key Report Takeaways

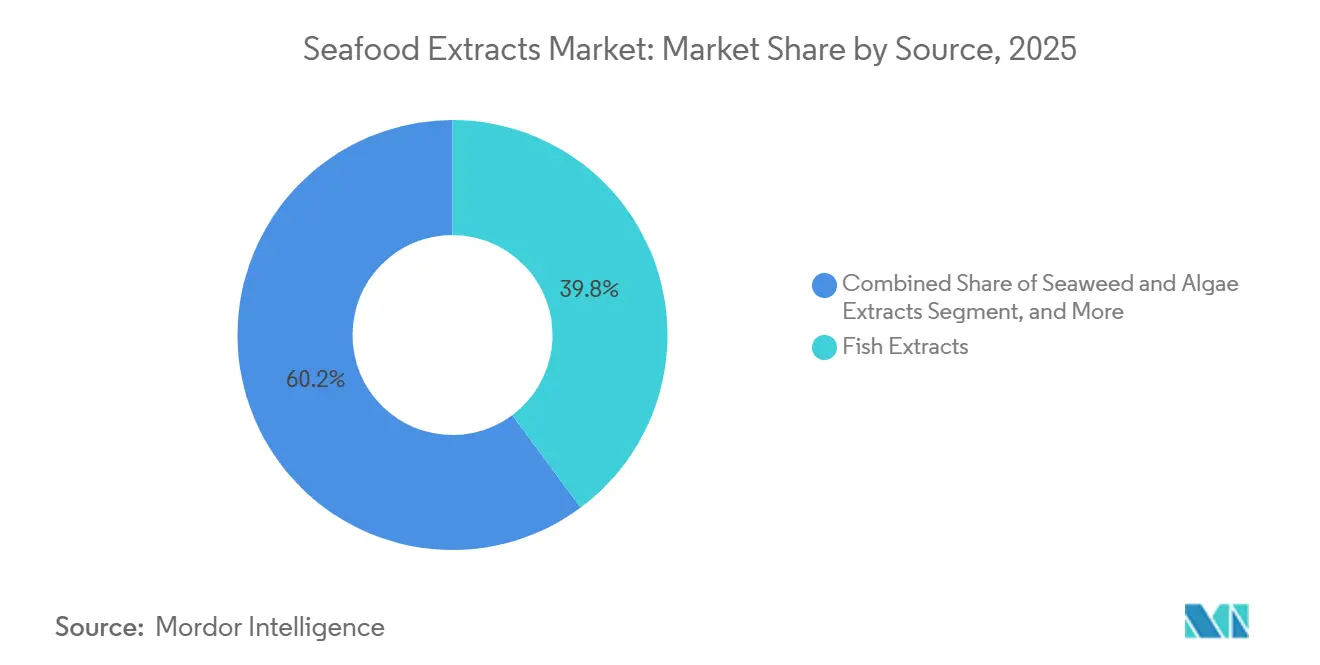

- By source, fish derivatives led with 39.82% of the seafood extracts market share in 2025, and seaweed and algae extracts are projected to expand at a 7.05% CAGR to 2031, the fastest among sources.

- By form, liquid products accounted for 62.98% of 2025 volume, and powder formats are forecast to grow at 6.84% CAGR through 2031.

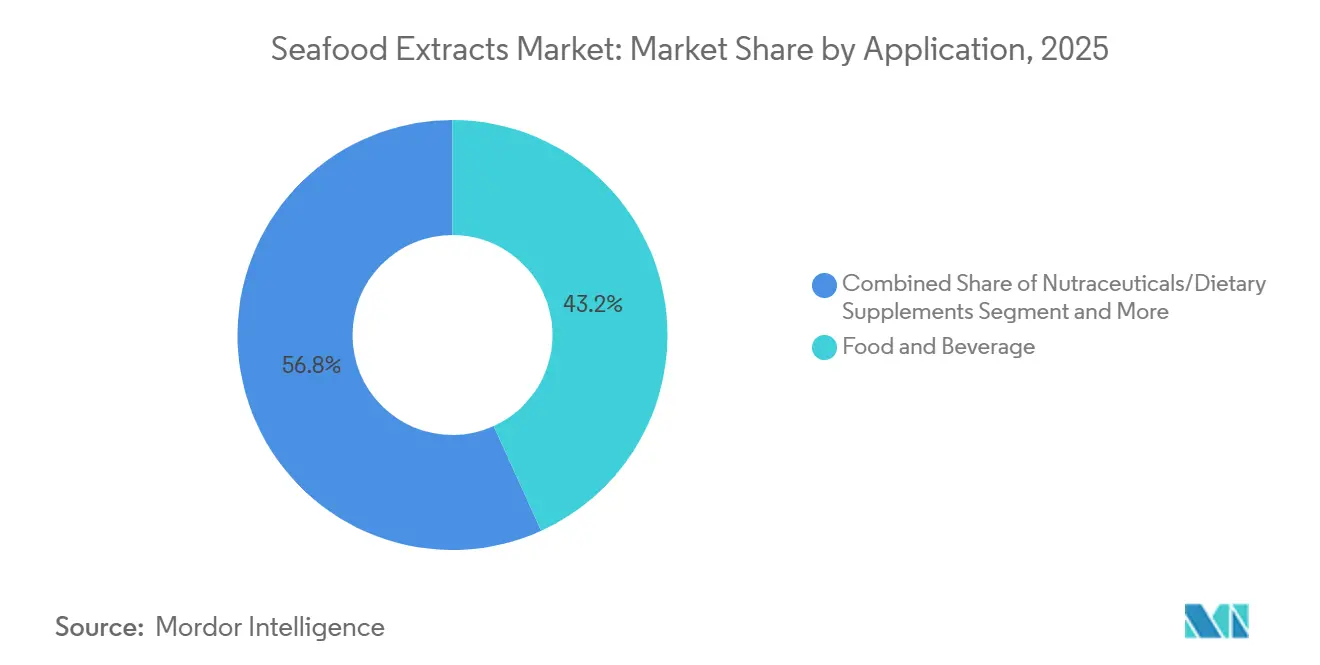

- By application, food and beverages held 43.22% of 2025 revenue, and nutraceuticals are advancing at 7.56% CAGR to 2031, outpacing all other uses.

- By geography, North America captured 32.33% of sales in 2025, and Asia-Pacific is set to post the highest regional CAGR at 8.19% over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Seafood Extracts Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for natural and clean-label ingredients | +1.3% | Global, with strongest pull in North America and Europe | Medium term (2-4 years) |

| Sustainable sourcing certifications like MSC attracting eco-conscious buyers | +0.9% | Global, led by North America, Europe, Australia | Long term (≥ 4 years) |

| Health benefits from omega-3 fatty acids, peptides, and antioxidants for supplements and functional foods | +1.5% | Global, fastest uptake in Asia-Pacific and North America | Short term (≤ 2 years) |

| Expansion in cosmetics for collagen-boosting, anti-aging skincare formulations | +0.8% | Asia-Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| Technological advancements in extraction methods | +0.7% | Global, with R&D hubs in Europe and North America | Long term (≥ 4 years) |

| Growth in ready-to-eat meals and convenience foods requiring authentic seafood taste | +1.0% | Asia-Pacific and North America, emerging in Middle East | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising demand for natural and clean-label ingredients

Retailers in the United Kingdom, United States, and Australia now merchandise over 90% of their chilled and ambient seafood under Marine Stewardship Council (MSC) seals, reflecting a strong consumer demand for sustainably and transparently sourced ingredients. This shift aligns with the growing emphasis on environmental responsibility and traceability in the seafood market. Food manufacturers are increasingly adopting marine extracts as natural alternatives to synthetic flavor enhancers. These extracts not only deliver the desired umami flavor but also comply with front-of-pack labeling requirements, catering to health-conscious consumers. In 2024, Thailand exported 833,000 tonnes of canned seafood, a significant 19.7% year-on-year increase. This growth is driven by the rising demand for all-natural formulations, particularly among European private-label brands[2]Source: Thai Frozen Foods Association, "Thailand Frozen Seafood Exports 2024", thai-frozen.or . The European Food Safety Authority's (EFSA) 2025 guideline, which mandates the disclosure of processing aids, is further accelerating the adoption of enzyme-based clarification methods over chemical solvents. This regulatory push is expected to enhance product transparency and safety standards.

Sustainable sourcing certifications like MSC attracting eco-conscious buyers

Certification schemes have become indispensable for premium-tier extract suppliers. MSC-certified fisheries now account for over 18% of global wild-capture volume. Brands sourcing from these fisheries report 12-15% higher retail velocities in North America and Europe compared to non-certified counterparts. Cargill Aqua Nutrition, in its 2025 Impact Report, disclosed that 90.5% of its marine ingredients originated from MSC-certified sources or fishery-improvement projects. Additionally, its Norwegian mills achieved 100% renewable energy operation in 2024, setting a benchmark that smaller players struggle to match. Asia supplies 30-35% of global fishmeal and fish oil, according to the International Fishmeal and Fish Oil Organisation, but only a small fraction carries third-party sustainability labels. This has created a divided market where certified Peruvian anchovy and Norwegian herring command USD 200-300 per tonne premiums over uncertified Southeast Asian equivalents. Regulatory oversight is tightening. In 2024, the U.S. Seafood Import Monitoring Program expanded its species coverage, while the European Union's due diligence regulation for deforestation-free products is driving scrutiny of marine supply chains. By 2028, traceability is expected to become a standard requirement rather than a differentiator.

Health benefits from omega-3 fatty acids, peptides, and antioxidants for supplements and functional foods

Marine-derived bioactives are gaining traction in nutraceuticals, driven by clinical validation. The Global Organization for EPA and DHA Omega-3s reported 5% annual growth in omega-3 supplement sales, with pet food and infant formula sectors leading as formulators recognize the cognitive and cardiovascular benefits of long-chain polyunsaturated fatty acids. In March 2026, MVS Pharma launched its MVS Omega-3 capsule in Europe, delivering 758 milligrams of EPA and 362 milligrams of DHA in a re-esterified triglyceride form. This formulation achieves over 92% purity and superior bioavailability compared to ethyl-ester variants. Fish collagen peptides are gaining attention in the beauty industry. NOW Foods' Aquatic Beauty+ capsules, containing 1 gram of MoriKol marine collagen tripeptides from tilapia, report clinical results: a 3-fold increase in skin hydration after 6 weeks and a 6-fold improvement in elasticity by week 12. In June 2025, the U.S. Food and Drug Administration approved OMTRYG, a prescription omega-3 ethyl-ester derived from fish. Each capsule contains at least 900 milligrams, including approximately 465 milligrams of EPA and 375 milligrams of DHA, validating therapeutic dosing thresholds now targeted by over-the-counter brands. A Chinese research team revealed in November 2025 that combining fish collagen with probiotics enhances gut-barrier function and systemic antioxidant capacity, driving multi-ingredient supplement launches across the Asia-Pacific region.

Expansion in cosmetics for collagen-boosting, anti-aging skincare formulations

Prestigious skincare brands are increasingly adopting marine collagen over bovine and porcine sources due to Type I collagen's structural similarity to the human dermis and lower immunogenicity. Thai Union Group invested USD 30 million in a marine collagen facility in Thailand, operational since 2025, producing 1,500 tonnes annually under the ThalaCol brand from tuna skins, a previously discarded by-product. The Collagen Co USA introduced a marine collagen powder sourced from Australian wild-caught fish scales, offering 10,000 milligrams per serving with a molecular weight under 2 kilodaltons for optimal transdermal absorption. Youth's CollaGEM nano collagen, derived from tilapia scales, features an ultra-low molecular weight of approximately 417 Daltons, making it ideal for premium beauty supplements with faster systemic distribution. Natural Factors launched Total Body Marine Collagen, featuring Collactive Marine Collagen from wild-caught fish like cod, haddock, and pollock, delivering 1,880 milligrams of collagen and 120 milligrams of elastin per serving to support joint and skin health. The cosmetics segment's 0.8% contribution to overall CAGR reflects its smaller revenue base but rapid growth. Dermatological studies from 2025 show oral marine collagen supplementation increases dermal collagen density by 7-12% in 12 weeks, strengthening brands' efficacy claims.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental concerns and sustainability | -0.8% | Stricter in Europe and North America | Long term (≥ 4 years) |

| Competition from synthetic and alternative | -1.1% | Cost-sensitive markets worldwide | Medium term (2-4 years) |

| High operational and production costs | -0.9% | Regions with limited infrastructure | Short term (≤ 2 years) |

| Stringent regulatory and safety standards | -0.7% | Developed markets with mature regulations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from Synthetic and Alternative Ingredients

In 2024, the F3 (Future of Fish Feed) challenge incentivized startups to develop krill-replacement ingredients using microalgae and yeast fermentation, with several achieving omega-3 profiles within 10% of wild krill oils. Mycoprotein and precision-fermentation platforms attracted significant venture capital, with multiple startups securing Series B funding in 2025 to scale production of heme proteins and long-chain fatty acids. These innovations replicate the umami and mouthfeel of fish extracts without marine feedstocks. Brands targeting vegan and flexitarian consumers increasingly favor these alternatives, with such consumers comprising 23% of U.S. supplement buyers in 2025, up from 18% in 2023. Synthetic astaxanthin and beta-carotene, produced via chemical synthesis or microbial fermentation, are 30-40% cheaper per kilogram than natural marine-derived counterparts, pressuring margins for extract suppliers lacking scale or vertical integration. This restraint's -0.6% drag on CAGR reflects direct substitution in cost-sensitive applications and the strategic risk of regulatory approval for fermentation-derived omega-3 oils disrupting the marine-extract value proposition.

Stringent regulatory compliance and food safety standards

In fiscal 2024, the U.S. Food and Drug Administration (FDA) rejected 1,234 seafood imports, citing issues like undeclared allergens and veterinary-drug residues. In response, extract producers are now adopting real-time PCR testing and blockchain traceability to sidestep such border rejections. Meanwhile, the European Food Safety Authority, in 2025, mandated full disclosure of processing aids in marine ingredients. This push has led suppliers to favor enzyme-based clarification over chemical solvents, ensuring they uphold a clean-label status. In 2024, Japan's Ministry of Health, Labour and Welfare imposed stricter limits on heavy metals in marine supplements. They now require batch-level certificates for lead, cadmium, and mercury, increasing compliance costs for importers by USD 0.15-0.25 per kilogram. The Codex Alimentarius Commission is working on unified standards for marine bioactive ingredients, with a 2027 completion date. These standards will necessitate reformulations for products currently benefiting from national exemptions. However, many smaller extract producers in Southeast Asia face challenges. Lacking the funds for inline metal detectors and HACCP-certified systems, they risk losing market access as multinational buyers streamline their supplier lists to reduce audit fatigue and liability risks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Fish Extracts Lead Despite Seaweed Innovation

In 2025, fish extracts led the market, contributing 39.82% of revenue. This growth was driven by established streams from tuna, anchovy, and whitefish by-products, essential for producing fishmeal, fish oil, and collagen peptides. In March 2026, Maruha Nichiro rebranded its next-generation protein unit to "Umios" and unveiled 45 marine-derived product launches, emphasizing the industry's focus on maximizing value from fish frames, heads, and skins previously used for low-value rendering. Thai Union's USD 30 million marine collagen facility, operational since 2025 with a 1,500-tonne annual capacity, highlights vertical integration to capture margins in high-value bioactive segments. Peru's anchovy biomass reached 10.92 million tonnes in 2025, with a 3-million-tonne fishing quota ensuring stable feedstock for fishmeal and omega-3 concentrate production. Chile's 2024 landings surged 53%, leading to a 2025 quota of 710,000 tonnes, reflecting improved stock management and favorable oceanographic conditions.

Seaweed and algae extracts are projected to grow at a 7.05% CAGR from 2026 to 2031, the fastest among all segments, driven by offshore cultivation that bypasses wild-harvest quotas and ensures consistent quality. Biorefinery techniques unlock multiple revenue streams from a single kelp or spirulina harvest, including protein isolates for food fortification, carrageenan and agar for gelling, phycocyanin for natural coloring, and residual biomass for animal feed or biofuel. In 2024, China's fishmeal imports reached 1.9 million tonnes, with consumption expected to rise 20% in 2025 as aquaculture operators increasingly substitute fishmeal with seaweed-derived proteins to reduce feed costs and improve sustainability metrics. Data from the International Fishmeal and Fish Oil Organisation's Asia Summit revealed Asia supplies 30-35% of global fishmeal and fish oil. However, seaweed cultivation is expanding faster than wild-fish landings, particularly in Indonesia, the Philippines, and South Korea, where government subsidies cover 40-60% of offshore-farm capital costs. Crustacean and mollusc extracts, valued for their high astaxanthin and taurine content, face supply constraints as shrimp and crab by-products are increasingly diverted to chitin and chitosan production for pharmaceutical and cosmetic applications.

By Form: Liquid Dominance Challenged by Powder Innovation

In 2025, liquid extracts accounted for 62.98% of the market volume, favored in ready-to-eat soups, sauces, and marinades for their blending ease and quick flavor release. Thailand's canned seafood exports surged by 19.7% in 2024, reaching 833,000 tonnes and valued at USD 3.8 billion. Liquid seafood extracts played a pivotal role as the flavor backbone for private-label products in European and North American supermarkets. Liquid formats also dominate aquafeed applications, with fish hydrolysates sprayed onto pellets to boost palatability and feed conversion ratios. Highlighting the significance of liquid extracts in the aquaculture value chain, Cargill Aqua Nutrition sold 1.94 million tonnes of aquafeed in 2024, sourcing 90.5% of its marine ingredients from MSC-certified fisheries or fishery-improvement projects.

From 2026 to 2031, powder seafood extracts are projected to grow at a 6.84% CAGR. Their rise is driven by superior shelf stability, reduced freight costs, and adaptability to capsule and sachet formats in nutraceuticals. Advancements in spray-drying and freeze-drying technologies now preserve volatile flavor compounds and bioactive peptides, enabling powder extracts to rival liquid formats in sensory performance while avoiding cold-chain logistics. MVS Pharma launched MVS Omega-3 capsules in March 2026, delivering 758 milligrams of EPA and 362 milligrams of DHA in a re-esterified triglyceride form with over 92% purity. This encapsulation method protects omega-3 from oxidation, extending shelf life to 24 months at room temperature. The Collagen Co USA offers marine collagen powder, derived from Australian wild-caught fish scales, delivering 10,000 milligrams per serving with a molecular weight below 2 kilodaltons. It targets the beauty-from-within market, where consumers prefer single-ingredient powders for blending into smoothies and beverages. Powder formats are also gaining traction in dry seasoning blends and instant-noodle flavor packets, where moisture control prevents caking and microbial growth, and in pet-food toppers, allowing owners to enhance palatability with concentrated marine protein without increasing liquid volume.

By Application: Nutraceuticals Drive Growth Beyond Food Dominance

In 2025, food and beverage applications accounted for 43.22% of the market revenue, encompassing ready meals, soups, sauces, snacks, and functional beverages. These applications harness seafood extracts to enhance umami depth, fortify with minerals, and maintain clean-label declarations. A trade agreement in February 2025 between Thailand and China greenlit the export of 50,000 metric tonnes of white seabass. This move is set to rake in THB 4.9 billion in revenue, with a notable chunk earmarked for extract production. These extracts are poised to cater to China's burgeoning instant-noodle and hot-pot seasoning markets. While liquid seafood extracts lead the charge due to their seamless integration into liquid matrices, powdered forms are carving a niche in dry seasoning blends and bouillon cubes, where moisture management is paramount. In the realms of animal feed and aquafeed, lower-grade fish hydrolysates and fishmeal find a home. Cargill Aqua Nutrition, a major player, moved 1.94 million tonnes of feed in 2024. However, these segments grapple with slimmer per-tonne margins and face competition from emerging alternatives like insect protein and single-cell protein.

From 2026 to 2031, nutraceuticals and dietary supplements are projected to grow at a 7.56% CAGR, the fastest among all application segments. Clinical studies link marine collagen to improved skin hydration and omega-3 ethyl esters to reduced triglyceride levels. NOW Foods' Aquatic Beauty+ capsules, featuring 1 gram of MoriKol marine collagen tripeptides sourced from tilapia, report a 3-fold hydration boost in 6 weeks and a 6-fold elasticity enhancement in 12 weeks, enabling premium pricing. Natural Factors introduced Total Body Marine Collagen, utilizing Collactive Marine Collagen from wild-caught whitefish—cod, pollock, saithe, haddock, and plaice. Each serving delivers 1,880 milligrams of collagen and 120 milligrams of elastin, targeting joint and skin health. The U.S. FDA, in June 2025, approved OMTRYG, a prescription omega-3 ethyl-ester product containing at least 900 milligrams per capsule, including approximately 465 milligrams of EPA and 375 milligrams of DHA, setting therapeutic dosing benchmarks for over-the-counter brands. Pharmaceuticals and cosmetics applications, though smaller, are steadily growing as marine-derived excipients and active ingredients gain recognition for their biocompatibility and regulatory acceptance.

Geography Analysis

North America maintained 32.33% market share in 2025, supported by established nutraceutical distribution networks and stringent quality standards that favor premium marine extract products. The region's regulatory framework, including FDA oversight and NOAA inspection programs, creates barriers to entry while ensuring product quality that commands price premiums in global markets. Consumer willingness to pay for natural and sustainable ingredients drives demand for certified marine extracts, particularly in functional food and dietary supplement applications. The region's technological leadership in extraction methods and bioactive research maintains competitive advantages despite higher production costs compared to Asian alternatives.

Asia-Pacific demonstrates the strongest growth momentum with 8.19% CAGR through 2031, driven by expanding aquaculture infrastructure and rising consumer awareness of marine bioactives' health benefits. China's seafood import surge to 4.6 million metric tons valued at USD 18.8 billion in 2023 reflects growing domestic demand that supports extract production. Japan's IFIA/HFE exhibition in 2024 showcased significant innovation in marine-derived functional ingredients, with 377 exhibitors highlighting the region's technological advancement. The region's cost advantages in seaweed cultivation and fish processing create competitive pricing for bulk marine extracts, while growing domestic consumption reduces export dependency.

Europe, South America, and the Middle East and Africa contribute smaller shares but have distinct growth drivers. In Europe, the European Food Safety Authority's 2025 guidance mandates full disclosure of processing aids in marine-derived ingredients, prompting suppliers to adopt enzyme-based clarification over chemical solvents. Marine Stewardship Council data reveals UK retail sales of MSC-certified seafood reached GBP 1.7 billion in 2024, while Australian sales totaled AUD 400 million, reflecting consumer preference for traceable provenance. South America's growth relies on Peru's anchovy biomass, recorded at 10.92 million tonnes in 2025 with a 3-million-tonne fishing quota, and Chile's 53% rise in 2024 landings, supported by a 710,000-tonne quota for 2025. These factors ensure stable feedstock for fishmeal and omega-3 concentrate production. In the Middle East and Africa, rising disposable incomes and urbanization drive demand for fortified foods and supplements, though infrastructure gaps and limited cold-chain logistics pose near-term challenges.

Competitive Landscape

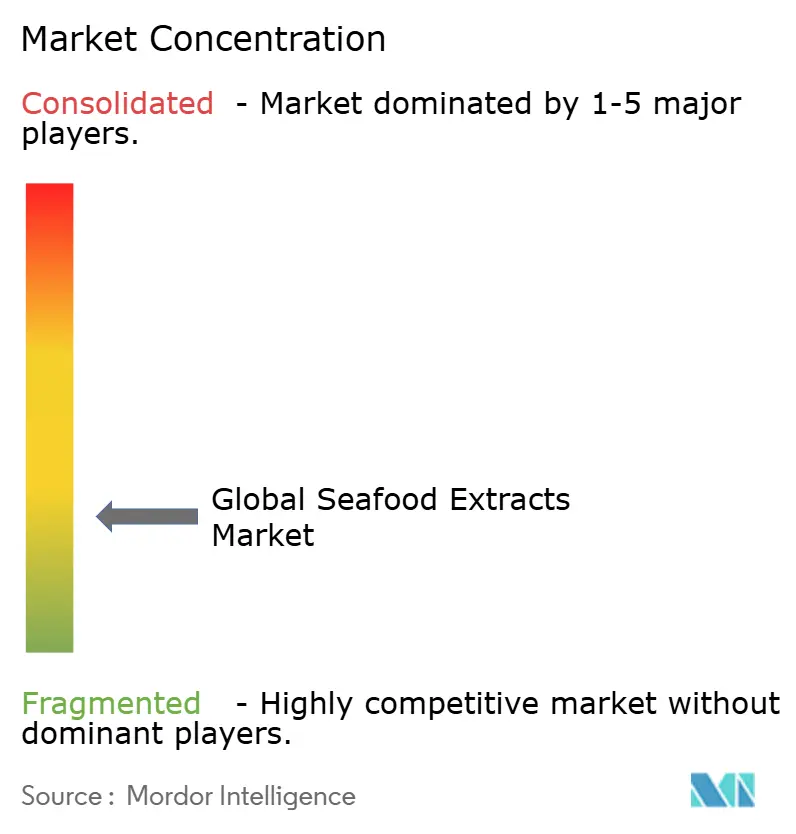

The seafood extracts market is fragmented, with established food giants competing against niche biotechnology firms and emerging aquaculture-based processors. No single player holds over a 15% share, creating opportunities for consolidation and tech-driven differentiation. Traditional players like Thai Union Group and Maruha Nichiro leverage vertical integration to secure raw materials while expanding into high-value bioactive extraction, strengthening their market position.

Specialty ingredient firms such as Symrise and Firmenich focus on premium applications requiring consistent quality and regulatory compliance. Their technical expertise and strong customer relationships enable them to command premium pricing. Technology adoption reveals varied strategies: established players invest in advanced extraction infrastructure, while startups explore innovative bioactive discoveries and sustainable sourcing. For example, Thai Union's USD 30 million marine collagen facility highlights the shift toward high-margin bioactive compounds to boost profitability.

Opportunities are growing in circular economy applications, where waste valorization technologies unlock value from seafood by-products. As regulatory frameworks and consumer preferences favor sustainable sourcing, companies with certifications and robust traceability systems gain a competitive edge. Firms aligning with these trends are well-positioned to meet the rising demand for sustainable and traceable seafood extracts.

Seafood Extracts Industry Leaders

-

Thai Union Group PCL

-

Symrise AG

-

Nikken Foods Co., Ltd.

-

Umios Corporation

-

dsm-firmenich

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Umami Bioworks, a Singaporean cellular agriculture company, has partnered with salmon specialist Nippon Barrier Free. Nippon Barrier Free, which specialises in selling functional materials from salmon, aims to bring cultivated marine cosmetics and supplements to the East Asian country.

- June 2025: BioMara, a seaweed biotech startup, launched Revyntra, a high-purity fucoidan cosmetic active derived from regeneratively farmed seaweed. It supports skin hydration, antioxidant defense, anti-aging, and environmental protection. It is suitable for serums, creams, masks, and hair products, representing a next-generation marine-derived skin and hair care ingredient.

- June 2025: Macro Oceans launched Big Kelp Flex, a seaweed cellulose ingredient designed to replace synthetic materials in skincare. It creates a smooth, hydrating visco-gel structure for superior skin feel and stability without microplastics. This followed the company’s 2024 Big Kelp Hydration launch, both focused on sustainability and high performance in natural skin care products.

- April 2025: Profand Seafood introduced Snackish fish churros made with fish flour from salmon and cod instead of wheat flour. The product is a protein-rich, healthier alternative to traditional churros. Launched at the Seafood Expo Global in Barcelona, it aligns with sustainability goals and includes flavorful sauces like sweet pepper and tartar, targeting health-conscious consumers.

Global Seafood Extracts Market Report Scope

The seafood extracts market comprises concentrated bioactive compounds and flavoring ingredients derived from marine sources such as fish, shrimp, crab, seaweed, and other seafood, used to enhance flavor, nutritional value, and functional properties across industries, including food, nutraceuticals, pharmaceuticals, and cosmetics.

The Seafood Extracts Market Report segments the industry by source into fish extracts, crustacean extracts, mollusc extracts, and seaweed and algae extracts; by form into liquid and powder; by application into food and beverage, nutraceuticals/dietary supplements, animal feed and aquafeed, pharmaceuticals, and cosmetics and personal care; and by geography into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been based on value (USD).

| Fish Extracts |

| Crustacean Extracts |

| Mollusc Extracts |

| Seaweed and Algae Extracts |

| Liquid |

| Powder |

| Food and Beverage |

| Nutraceuticals/Dietary Supplements |

| Animal Feed and Aquafeed |

| Pharmaceuticals |

| Cosmetics and Personal Care |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Source | Fish Extracts | |

| Crustacean Extracts | ||

| Mollusc Extracts | ||

| Seaweed and Algae Extracts | ||

| By Form | Liquid | |

| Powder | ||

| By Application | Food and Beverage | |

| Nutraceuticals/Dietary Supplements | ||

| Animal Feed and Aquafeed | ||

| Pharmaceuticals | ||

| Cosmetics and Personal Care | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big will global demand for seafood extracts be by 2031?

The seafood extracts market is projected to reach USD 15.13 billion by 2031, expanding at a 6.62% CAGR from 2026 to 2031.

Which raw material contributes the most revenue?

Fish by-products such as tuna, anchovy, and whitefish delivered 39.82% of 2025 sales, retaining leadership among all sources.

Which application will outpace others in growth?

Nutraceuticals and dietary supplements are forecast to rise at 7.56% CAGR through 2031 on the back of validated marine collagen and omega-3 benefits.

Why is Asia-Pacific the fastest-growing region?

Government incentives for offshore farming, expanding aquaculture, and rising middle-class supplement use drive an 8.19% regional CAGR.

Page last updated on: