Bulk Food Ingredients Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

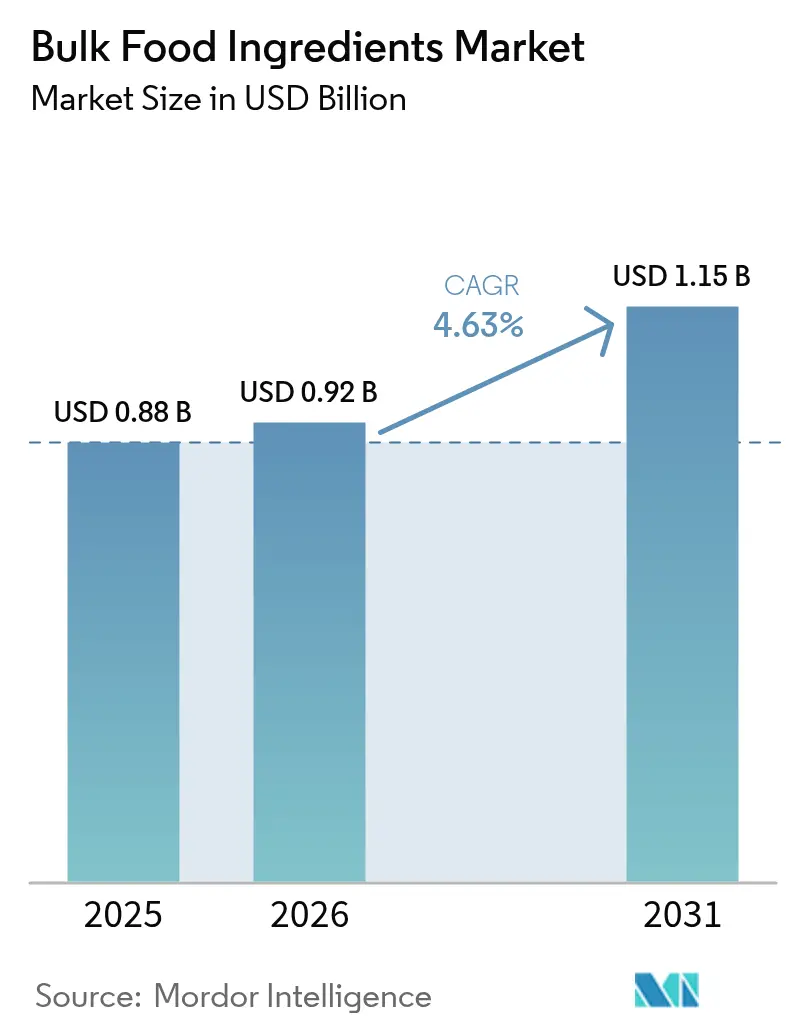

| Market Size (2026) | USD 0.92 Billion |

| Market Size (2031) | USD 1.15 Billion |

| Growth Rate (2026 - 2031) | 4.63% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Bulk Food Ingredients Market Analysis by Mordor Intelligence

Bulk food ingredients market size in 2026 is estimated at USD 0.92 billion, growing from 2025 value of USD 0.88 billion with 2031 projections showing USD 1.15 billion, growing at 4.63% CAGR over 2026-2031. Demand resilience is tied to the push for secure, traceable supply chains and the growing preference for vertically integrated sourcing that lets processors stabilize quality and respond quickly to shifts in orders. Producers of grains, pulses, and oilseeds are reinforcing this model through expanded in-house storage, cleaning, and sorting facilities, which reduces third-party dependencies and strengthens price bargaining power. In tandem, digital traceability platforms built on blockchain are gaining traction among leading players, giving buyers end-to-end visibility into provenance, farm inputs, and shipping conditions. The market also benefits from regulatory momentum favoring safer, naturally derived additives, a trend that is reshaping formulation choices across bakery, snack, and ready-meal lines.

Key Report Takeaways

- By product type, Grains, Pulses, and Cereals accounted for 45.21% market share in 2025, while Herbs and Spices are forecasted to expand at a 6.41% CAGR to 2031

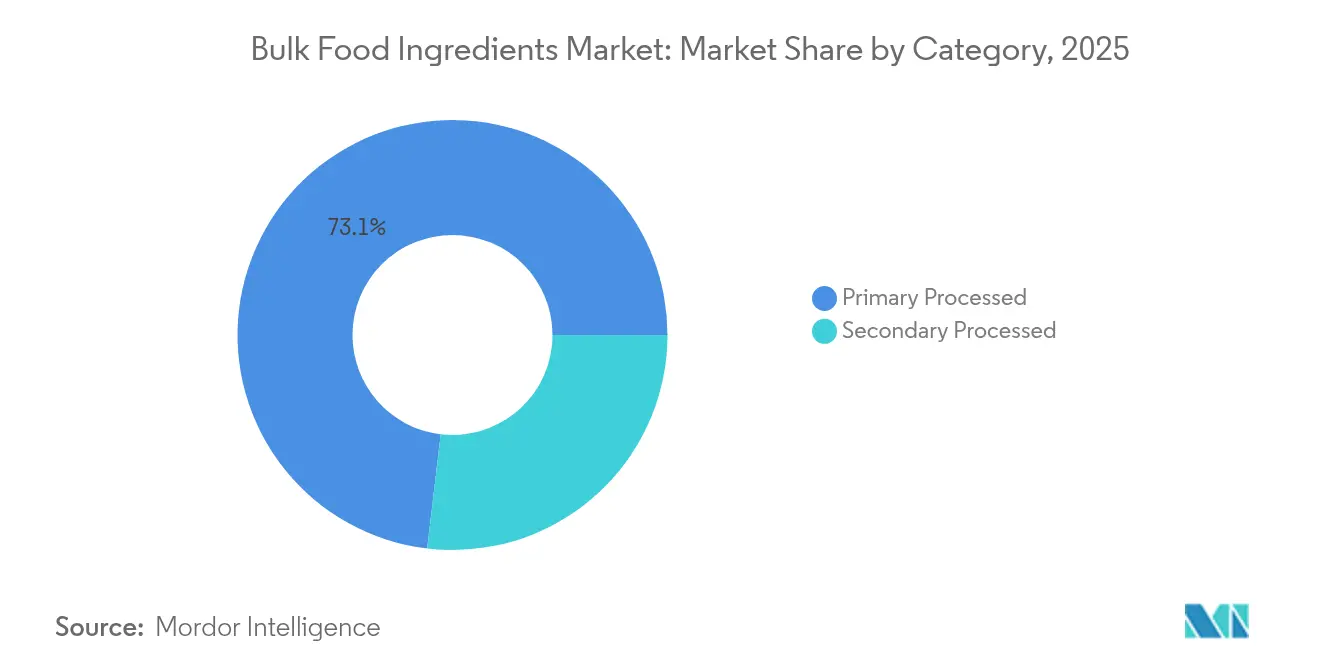

- By category, Primary Processed ingredients led with 73.12% share in 2025, while Secondary Processed is forecast to expand at a 5.85% CAGR to 2031.

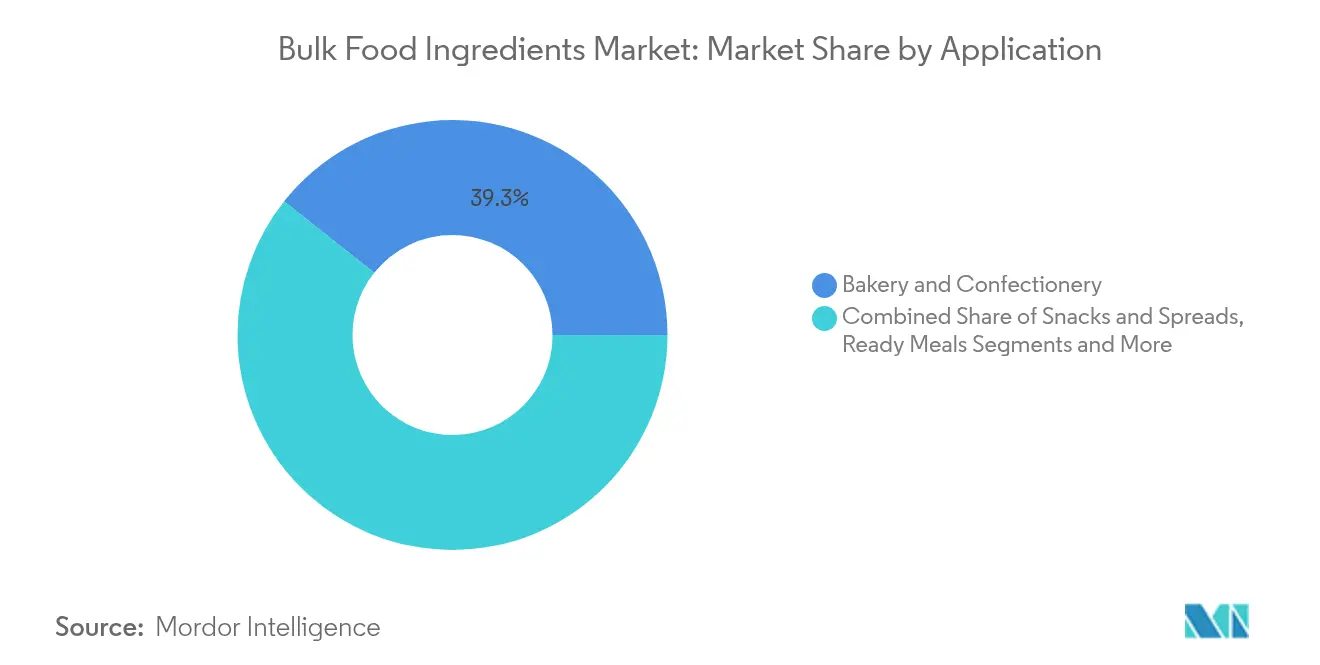

- By application, Bakery and Confectionery accounted for 39.32% share of the bulk food ingredients market size in 2025; Ready Meals is advancing at a 6.22% CAGR through 2031.

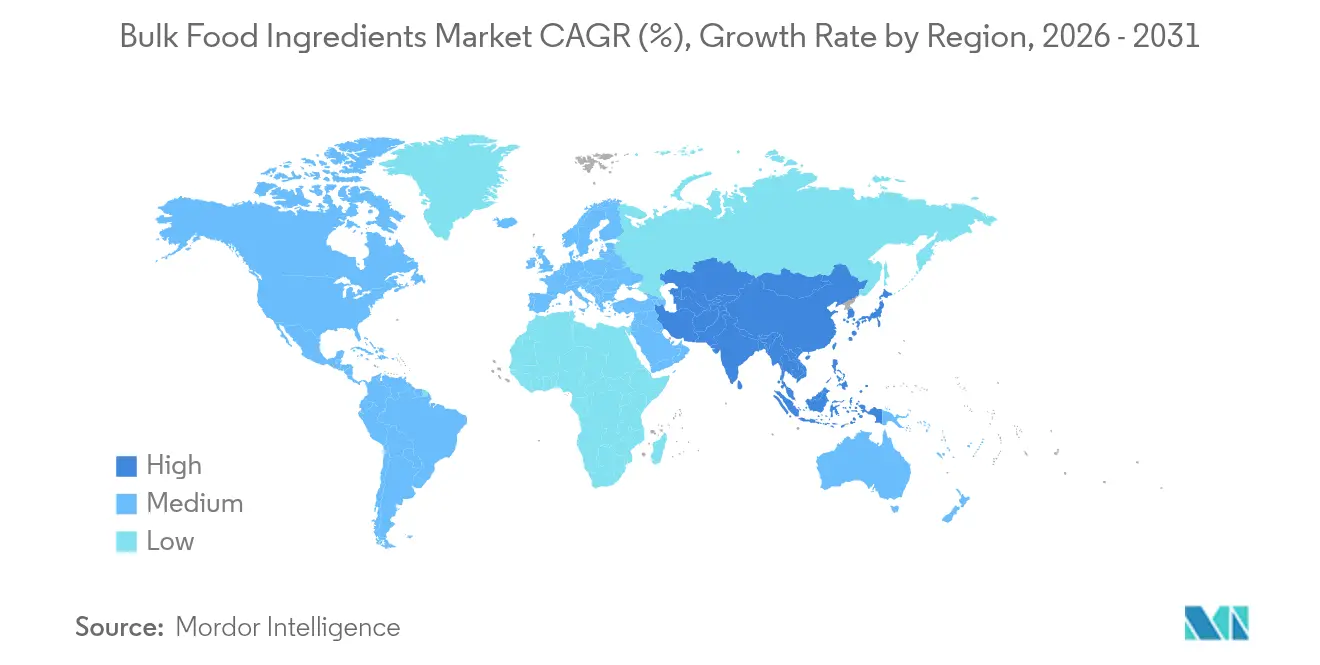

- By geography, Asia-Pacific dominated with 33.42% revenue share in 2025, whereas the Middle East and Africa region is forecast to register a 5.85% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bulk Food Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Processed Food Fuels Bulk Ingredients Usage | +1.2% | Global, with highest impact in Asia-Pacific | Medium term (2-4 years) |

| Growth in Plant-Based Diets Elevates the Market | +0.9% | North America & Europe, spillover to Asia-Pacific | Medium term (2-4 years) |

| Cost Effectiveness of Bulk Ingredients Over Packaged Alternatives | +1.5% | Global, with highest impact in emerging markets | Short term (≤ 2 years) |

| Booming Bakery Industry Spurring Bulk Ingredients Demand | +0.8% | Global, with concentration in Europe and Asia-Pacific | Medium term (2-4 years) |

| Rise in Demand for Clean Label Ingredients | +0.5% | North America & Europe | Long term (≥ 4 years) |

| Globalization of Cuisines Propelling Demand for Ethnic Spices | +0.7% | Global, highest impact in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Processed Food Fuels Bulk Ingredients Usage

The increasing demand for processed food is a significant driver of the global bulk ingredients market. As consumer preferences shift toward convenience and ready-to-eat food products, the need for bulk ingredients, such as starches, sweeteners, preservatives, and other additives, has risen substantially. The global processed food market has witnessed consistent growth, driven by urbanization, rising disposable incomes, and changing dietary habits. The global processed food industry has expanded significantly in recent years, with bulk ingredients playing a pivotal role in meeting production requirements. Furthermore, Food and Agriculture Organization (FAO) highlight the importance of bulk ingredients in enhancing food security and reducing food waste by extending product shelf life. Industry associations, including the Institute of Food Technologists (IFT), also emphasize the critical role of bulk ingredients in ensuring the quality, safety, and consistency of processed food products [1]Source: Institute of Food Technologies, "Food Science and Technology Solutions to Improve Food and Nutrition Security", www.ift.org . This trend is expected to continue driving the bulk ingredients market during the forecast period, as manufacturers increasingly rely on these components to meet evolving consumer demands and regulatory standards.

Growth in Plant-Based Diets Elevates the Market

The growing adoption of plant-based diets is significantly driving the market growth. Consumers are increasingly shifting toward plant-based food products due to rising health consciousness, environmental concerns, and ethical considerations. This trend has led to a surge in demand for bulk ingredients such as plant-based proteins, starches, and oils, which are essential in the production of plant-based food and beverages. The plant-based food market has witnessed substantial growth in recent years, with plant-based alternatives becoming a mainstream choice for consumers. Additionally, organizations like the Plant Based Foods Association (PBFA) report that around 59% of households in United States purchased plant based foods in 2024 [2]Source: Plant-Based Foods Association, "Building the market presence and power of the plant-based foods industry", www.plantbasedfoods.org. As consumers continue to prioritize sustainable and health-focused diets, the demand for bulk ingredients in the plant-based segment is expected to grow further during the forecast period.

Cost Effectiveness of Bulk Ingredients Over Packaged Alternatives

The cost-effectiveness of bulk ingredients compared to packaged alternatives is a significant driver of the global bulk food ingredients market. Bulk ingredients are generally sold in larger quantities, which reduces packaging costs and allows for economies of scale. This cost advantage is particularly appealing to food manufacturers, restaurants, and other businesses in the food industry, as it helps lower production costs and improves profit margins. Additionally, bulk purchasing minimizes waste associated with individual packaging, aligning with the growing consumer preference for sustainable and eco-friendly practices. These factors collectively contribute to the increasing demand for bulk food ingredients, driving growth in the market during the forecast period. Furthermore, the affordability of bulk ingredients enables small and medium-sized enterprises (SMEs) to compete effectively in the market by reducing their operational expenses. The flexibility offered by bulk ingredients also allows businesses to customize their product offerings, catering to diverse consumer preferences and dietary requirements. For instance, bulk spices, grains, and sweeteners can be tailored to meet the needs of organic, gluten-free, or vegan product lines, further enhancing their appeal in niche markets.

Booming Bakery Industry Spurring Bulk Ingredients Demand

The bakery sector is experiencing a renaissance driven by evolving consumer preferences and product innovation, creating sustained demand for specialized bulk ingredients. Key growth drivers include protein-fortified baked goods, regenerative whole grains, and low-sugar formulations that align with health-conscious consumer preferences. This evolution extends beyond traditional categories, with significant growth in culturally inspired bakery items that incorporate diverse flavors and ingredients. The trend is particularly evident in the donut and bagel segments, which are experiencing increased household penetration. Manufacturers are responding with innovations in functional ingredients that deliver specific nutritional benefits while maintaining the sensory experiences consumers expect from baked goods. The integration of prebiotic and probiotic components represents a significant opportunity for differentiation, as does the resurgence of traditional bread products like sourdough that require specialized flour blends and starters. These developments are creating demand for both conventional bulk ingredients and novel specialty components that enable manufacturers to address emerging consumer preferences.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Food Safety Challenges in Bulk Ingredient Storage and Handling | -1.2% | Global, with higher impact in emerging markets | Medium term (2-4 years) |

| Rising Awareness Around Sugar Related Health Risks | -0.7% | North America and Europe, spreading globally | Long term (≥ 4 years) |

| Quality Control Issues in Mass-Scale Processing | -0.9% | Global, pronounced in high-volume export hubs | Short term (≤ 2 years) |

| High Dependency on Seasonal Agricultural Output | -1.1% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Food Safety Challenges in Bulk Ingredient Storage and Handling

The inherent complexities of bulk ingredient management create significant food safety vulnerabilities that can impact market growth. The design limitations of many transport units and inadequate cleaning protocols further compound these risks, potentially leading to cross-contamination events that can affect entire production batches. Recent updates to food safety standards are imposing stricter validation requirements for cleaning procedures, necessitating significant investments in both equipment and processes. The ENFIT Working Group has developed structured cleaning protocols tailored to specific product types, aiming to standardize practices across the supply chain, but implementation remains inconsistent Beyond transportation, storage facilities present additional challenges, with factors like humidity, temperature fluctuations, and pest control requiring sophisticated management systems. These safety considerations are particularly significant for ingredients like grains and pulses, which are vulnerable to mycotoxin contamination if not properly stored and monitored.

Rising Awareness Around Sugar Related Health Risks

Heightened consumer consciousness regarding sugar consumption is reshaping product formulations and ingredient specifications across the food industry. This trend is further accelerated by the growing use of GLP-1 medications for weight management, which are altering taste preferences and consumption patterns among a significant consumer segment. The FDA's proposed front-of-package nutrition labels aim to increase transparency regarding added sugars, potentially accelerating the shift away from high-sugar formulations[3]Source: U.S. Food and Drug Administration, "FDA Proposes Requiring At-a-Glance Nutrition Information on the Front of Packaged Foods", www.fda.gov. Bulk ingredient suppliers face the challenge of crafting cost-effective alternatives to sugar. These alternatives must not only provide sweetness but also replicate sugar's other essential functions, such as texture, preservation, and browning. Achieving this balance is complex, as sugar plays a critical role in the structural and sensory attributes of many products. This need for reformulation presents both challenges and opportunities. Manufacturers are on the lookout for ingredients that can offer the same sensory experiences, such as mouthfeel and flavor enhancement, while cutting down on sugar content.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Category: Primary Processed Dominates While Secondary Accelerates

Primary Processed ingredients account for 73.12% of the bulk food ingredients market share in 2025. Their prevalence stems from universal demand for minimally transformed grains, pulses, and oilseeds that underpin basic calorie intake. Steady global trade flows and familiar handling protocols give buyers confidence in cost forecasts, safeguarding production schedules for bakery, dairy, and snack lines. Climate-driven supply shocks prompt processors to invest in optical sorters and color graders that lift yield and quality, helping preserve margins. The segment’s scale also encourages co-location of cleaning, dehulling, and milling facilities near ports, shortening lead times and strengthening traceability.

Secondary Processed ingredients are growing at a 5.85% CAGR through 2031. Suppliers offer pre-gelatinized starches, instant flours, and roasted pulse powders that shorten cooking cycles and raise functional versatility. Demand from ready-meal plants illustrates the appeal of time-saving intermediates that let formulators skip on-site heat treatment. Enzyme-modified oils and fats improve mouthfeel in dairy alternatives, while spray-dried fruit powders add flavor bursts without refrigeration. As premium niches widen, the bulk food ingredients market size attached to secondary processing commands higher margins, incentivizing investment in specialty extrusion and drum-drying capacity.

By Product Type: Grains Lead While Herbs and Spices Gain Ground

Grains, Pulses and Cereals hold a 45.21% revenue share of the bulk food ingredients market. Wheat, corn, and rice continue to anchor calorie intake, but interest in regenerative and heritage grains raises the profile of millet, sorghum, and teff. Millers deploy stone-ground and low-temperature processes that preserve micronutrients, aligning with clean-label aspirations. Growing acceptance of whole-grain consumption supports demand for debranning systems that retain fiber while delivering lighter flour textures. Exporters in Argentina and Australia emphasize gluten-strength and protein content metrics to win price premiums.

Herbs and Spices are the fastest-rising cluster at a 6.41% CAGR within this segmentation despite a smaller base. Globalization of palates and social-media exposure motivate consumers to cook with complex regional flavorings. Suppliers invest in cryogenic milling to lock in volatile oils and ensure batch-to-batch consistency. Organic certification and fair-trade sourcing differentiate premium offerings, compelling brand owners to disclose farm-gate practices. Although exact growth rates vary by sub-category, the consistent uptick underscores new opportunities for origin-specific turmeric, cumin, and chili lines that feed directly into the bulk food ingredients market.

By Application: Bakery and Confectionery Leads While Ready Meals Rise

Bakery & Confectionery applications represent 39.32% of the bulk food ingredients market size in 2025. Continuous NPD in protein-enriched muffins, reduced-sugar cookies, and mindful indulgence chocolate is stimulating purchases of high-protein wheat gluten, specialty fats, and unrefined cane sugar. Gluten-free baking mixes capitalize on sorghum and buckwheat flours, while cold-pressed cocoa butters raise clean-label credentials. Recipe adjustments responding to front-of-pack labeling rules encourage use of fruit purees and oligosaccharide syrups that supply sweetness and moisture retention.

Ready Meals register the fastest momentum with a 6.22% CAGR to 2031. Multi-layer microwave bowls and frozen entrées require sauces thickened with modified starches, clean-label preservatives, and IQF vegetables that maintain color integrity. High-pressure processing extends chilled shelf life, enabling retailers to stock chef-inspired dishes with fewer additives. Suppliers deliver diced protein concentrates and spice pre-blends in 1-ton totes that feed directly into batching kettles, avoiding unpacking waste and labor costs. As urban consumers split meals across dayparts, the bulk food ingredients market gains incremental throughput from snack-sized, high-protein ready bowls.

Geography Analysis

Asia-Pacific commands 33.42% of bulk food ingredients market revenue, anchored by China and India’s vast processing sectors and expanding urban middle classes. Regional millers leverage port-side silos and automated bagging lines to feed bakery, dairy, and instant-noodle plants at scale. Government investments in cold-chain logistics widen access to perishable produce, stimulating demand for stabilizers and texture agents that extend shelf life under variable temperatures. Spices sourced from Vietnam, Indonesia, and Cambodia supply both domestic and export-oriented processors, reinforcing intra-regional trade flows. Sustainability initiatives in Australia encourage regenerative farming certifications that open premium export channels.

North America follows with mature demand centered on convenience foods, sports nutrition, and plant-forward product design. Processors in the United States integrate blockchain nodes into ERP systems to satisfy retailer mandates for origin transparency. Canadian pulse exporters expand pea-protein fractionation, supported by favorable agronomy and hydroelectric energy pricing that trims carbon footprints. Europe holds a significant position in the global bulk food ingredients market, driven by its robust food and beverage industry and high consumer demand for processed and convenience foods. The region's well-established supply chain infrastructure and stringent food safety regulations further enhance its role as a key player in this market. Countries such as Germany, France, and the United Kingdom are major contributors, owing to their advanced manufacturing capabilities and strong export activities.

The Middle East and Africa is the fastest-growing region, projected to rise at a 5.85% CAGR to 2031. GCC nations import significant volumes of wheat, sugar, and dairy powders for re-export-oriented bakeries and confectioners. UAE processors collaboratively develop risk-mitigation programs that include multi-origin sourcing and strategic grain reserves. In Sub-Saharan Africa, the emergence of organized retail and quick-service restaurants fuels demand for standardized spice blends and batter mixes. Governments invest in local milling and oilseed-crush capacity to capture value addition domestically, broadening the footprint of the bulk food ingredients market.

Competitive Landscape

The bulk food ingredients industry shows moderate concentration. Cargill, Incorporated, Archer Daniels Midland Company, Tate & Lyle PLC, Ingredion Incorporated, and Bunge Limited are among the key players using scale to secure freight, storage, and currency hedging advantages. Their vertical integration spans from seed genetics to crushing, refining, and consumer-branded products, enabling margin capture across multiple nodes. Investments in AI-enabled inspection and predictive maintenance lower downtime in high-throughput terminals, sharpening cost positions further.

Digital collaboration initiatives strengthen the competitive advantages of established companies. The Covantis consortium operates a blockchain-based trade platform that improves document processing, reduces shipping delays, and minimizes fraud risk. Participants benefit from faster contract settlements, which improves their working capital position. Smaller traders face higher costs to join these systems, leading them to focus on niche commodities and domestic markets where operational scale requirements are lower.

Specialist suppliers target high-growth adjacencies such as plant-protein isolates, clean-label powder blends, and origin-specific spice extracts. Firms with agile product-development teams secure contracts with dairy-alternative, gluten-free, and functional beverage brands seeking rapid iteration. Regional players leverage local crop knowledge and shorter delivery radii to provide freshness guarantees unattainable for transocean shipments. As sustainability pledges intensify, even large incumbents pursue acquisitions in fermentation-based sweeteners and precision-fermented fats, broadening their ingredient toolkits without diluting portfolio focus on bulk volumes.

Bulk Food Ingredients Industry Leaders

-

Cargill, Incorporated

-

Archer Daniels Midland Company

-

Tate & Lyle PLC

-

Bunge Limited

-

Ingredion Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Bunge, a global leader in agribusiness, has poured around USD 550 million into a state-of-the-art facility in the U.S. This facility, dedicated to producing soy protein concentrate (SPC) and textured soy protein concentrate (TSPC), is seamlessly integrated with Bunge's soybean crushing plant located in Morristown, Indiana. Once fully operational, the facility is set to process an extra 4.5 million bushels of soybeans.

- April 2025: Nestlé and Olam Food Ingredients (OFI) announced their largest joint agroforestry initiative to date, a partnership aimed at transforming cocoa farming and tackling the dual threats of carbon emissions and deforestation.

- June 2024: CP Kelco and Tate & Lyle have joined forces, forming a dominant entity in the realm of food and beverage product development and customer service solutions. This strategic merger seeks to position the newly formed powerhouse as a frontrunner in specialty food and beverage solutions, leveraging the unique strengths of both companies to seize a more substantial slice of the market.

- April 2024: Glanbia completed the acquisition of Flavor Producers for USD 300 million, expanding its capabilities in the flavor solutions segment and strengthening its position in the nutritional ingredients market, with particular focus on protein solutions and premixes

Global Bulk Food Ingredients Market Report Scope

Bulk food ingredients refer to raw or semi-processed food materials purchased in large quantities from wholesale suppliers. These ingredients are often used in the food processing and manufacturing industry to produce a wide range of food products, including snacks, beverages, baked goods, and more. Some common examples of bulk food ingredients include grains, flour, sugars, spices, oils, nuts, seeds, and dried fruits.

The market for bulk food ingredients has been segmented by category into primary and secondary processed. By product type into grains, pulses, cereals, tea, coffee, cocoa, herbs and spices, oilseeds, sugar and sweeteners, edible oils, and other product types. By application into bakery and confectionery, snacks and spreads, ready meals, and other applications. By geography into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa.

The market sizing has been done in value terms in USD for all the abovementioned segments.

| Grains, Pulses and Cereals |

| Tea, Coffee and Cocoa |

| Herbs and Spices |

| Oilseeds |

| Sugar |

| Others |

| Primary Processed |

| Secondary Processed |

| Bakery and Confectionary |

| Snacks and Spreads |

| Ready Meals |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Grains, Pulses and Cereals | |

| Tea, Coffee and Cocoa | ||

| Herbs and Spices | ||

| Oilseeds | ||

| Sugar | ||

| Others | ||

| By Category | Primary Processed | |

| Secondary Processed | ||

| By Application | Bakery and Confectionary | |

| Snacks and Spreads | ||

| Ready Meals | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current bulk food ingredients market size?

The bulk food ingredients market size stands at USD 0.92 billion in 2026 and is expected to reach USD 1.15 billion by 2031.

Which region holds the largest bulk food ingredients market share?

Asia-Pacific leads the market with 33.42% revenue share in 2025.

Which application segment is growing the fastest?

Ready Meals show the fastest growth, advancing at a 6.22% CAGR through 2031 as consumers look for convenient, premium meal solutions at home.

What role does blockchain play in this industry?

Blockchain platforms, such as those deployed by the Covantis consortium, enable end-to-end ingredient traceability, reduce paperwork, and lower fraud risk.

Page last updated on: