South Africa Foodservice Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

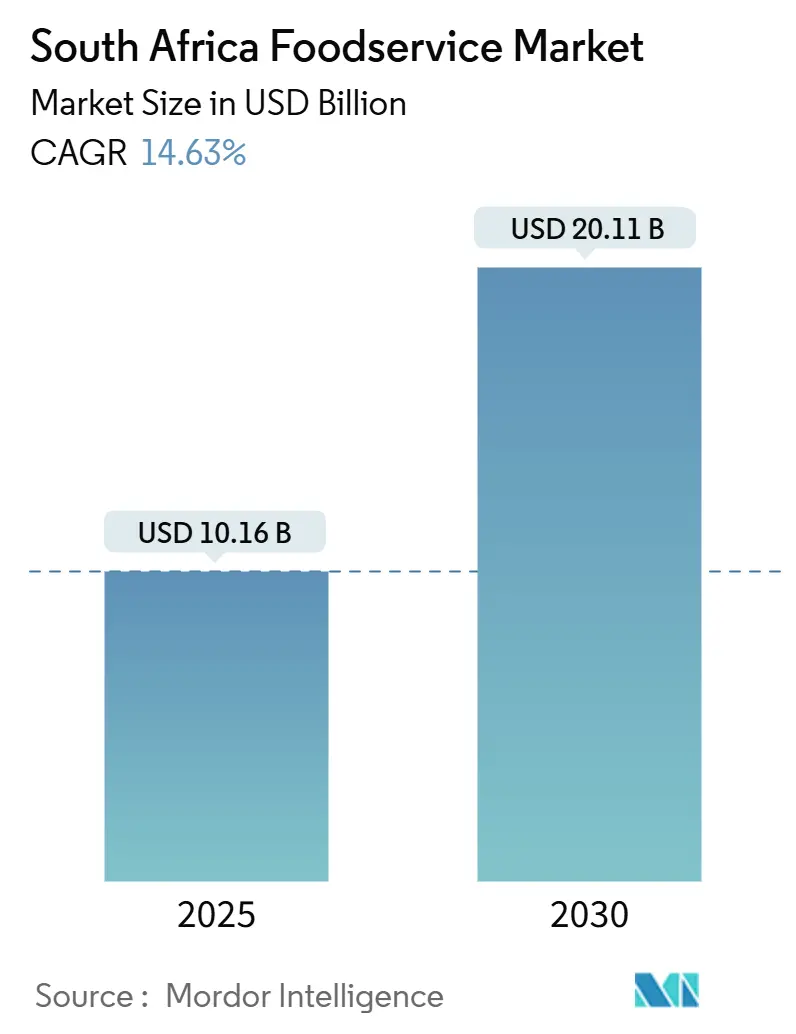

| Market Size (2025) | USD 10.16 Billion |

| Market Size (2030) | USD 20.11 Billion |

| Growth Rate (2025 - 2030) | 14.63% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South Africa Foodservice Market Analysis by Mordor Intelligence

The South African foodservice market was valued at USD 10.16 billion in 2025 and is projected to grow at a CAGR of 14.63%, reaching USD 20.11 billion by 2030. The market's growth is driven by consistent demand for affordable prepared meals, increased adoption of digital ordering, and the recovery of the tourism sector. Quick service restaurants (QSRs) dominate in terms of volume, while cloud kitchens are gaining market share with their low-overhead, delivery-focused models. Major chains are investing in alternative power solutions to mitigate load-shedding costs, while enhancements in cold-chain infrastructure are reducing spoilage risks. Additionally, the shift toward heritage grains, plant-based menu options, and premium experiential dining formats is increasing average ticket sizes and fostering menu innovation.

Key Report Takeaways

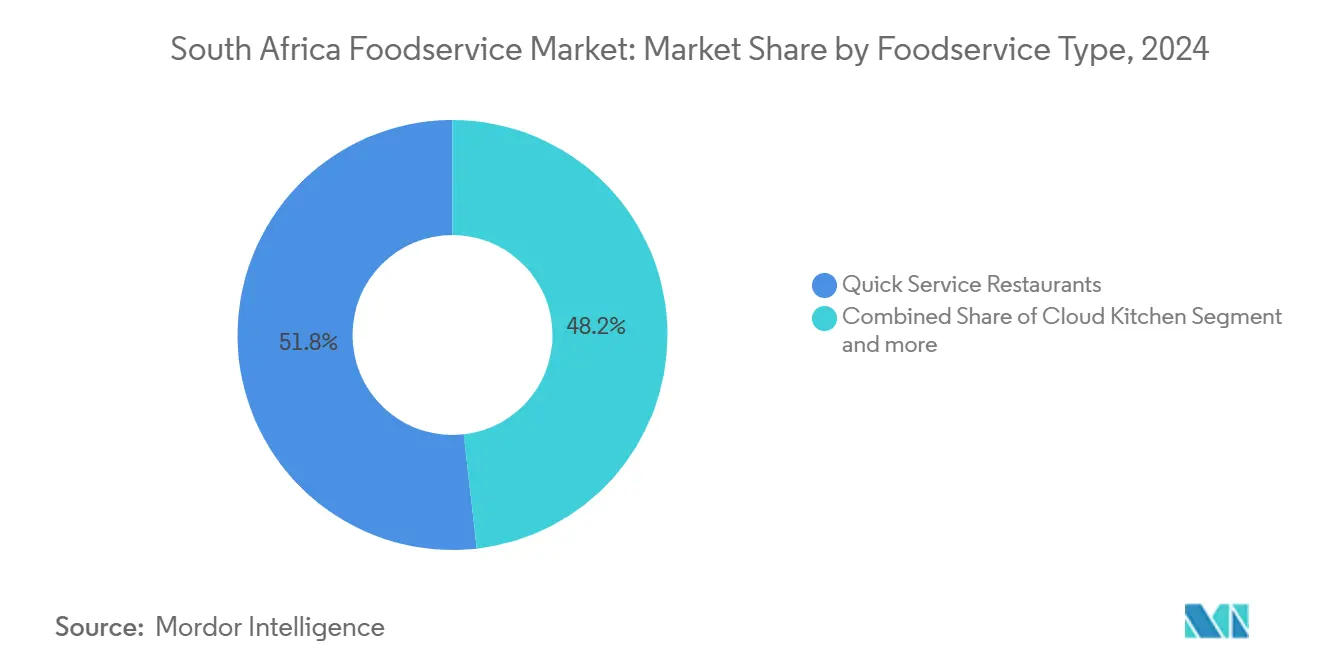

- By foodservice type, QSRs held 48.16% of the South Africa foodservice market share in 2024, and Cloud kitchens are set to log the fastest expansion, advancing at a 17.41% CAGR between 2025 and 2030.

- Independent outlets accounted for 72.02% of the South Africa foodservice market size in 2024, while chained outlets are forecast to capture a 15.32% CAGR.

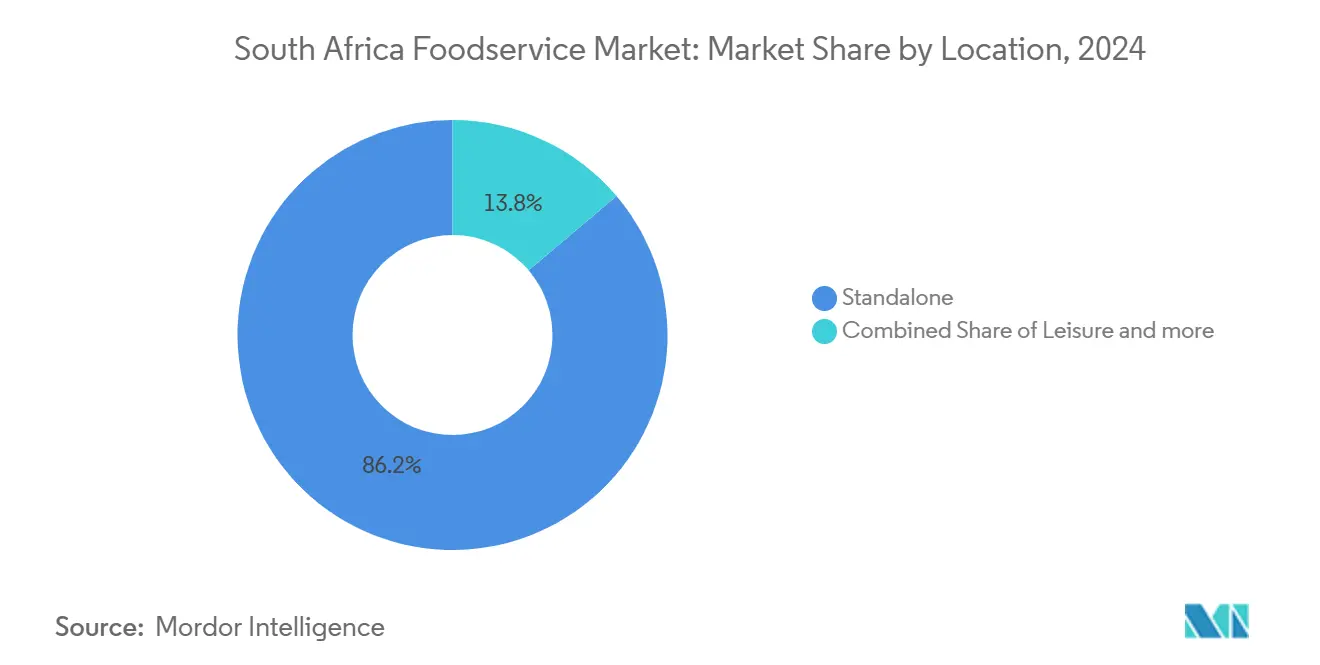

- Standalone locations dominated the market with an 86.23% share in 2024, yet leisure venues are predicted to register a 18.71% CAGR.

- Dine-in service captured 56.45% of the South African foodservice market in 2024, whereas delivery is p a 16.34% CAGR.

Worldwide, activity is shaped by contributions from multiple countries and regions, with South africa representing one among them. The global report on food service market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

South Africa Foodservice Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of quick service restaurants (QSRs) | +3.2% | National, concentrated in Gauteng, Western Cape | Medium term (2-4 years) |

| Tourism and hospitality expansion | +2.8% | Western Cape, KwaZulu-Natal, Gauteng | Medium term (2-4 years) |

| Expansion of delivery and digital ordering platforms | +2.1% | Urban centers, township expansion via partnerships | Short term (≤ 2 years) |

| Consumer demand for ethnic and international cuisines | +1.9% | Major metropolitan areas, emerging in secondary cities | Long term (≥ 4 years) |

| Experience-based dining and premiumization | +1.7% | Cape Town, Johannesburg, Durban leisure districts | Long term (≥ 4 years) |

| Consumer shift towards sustainable, organic, and plant-based menu options | +1.4% | Urban affluent areas, university towns | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth of quick service restaurants (QSRs)

The South African quick-service restaurant (QSR) market witnessed significant growth, driven by affordability pressures, increasing demand for convenience, and operational efficiencies achieved through technology adoption. QSRs demonstrated resilience in challenging economic conditions, as their value-focused offerings attracted price-sensitive consumers while maintaining convenience and quality. Famous Brands illustrated this growth by opening 137 new restaurants in 2024 and achieving 95% alternative power coverage across its network to address the challenges of ongoing load-shedding[1]Source: Famous Brands, " Consumer technology supporting strategy," famousbrands.co.za. Technology integration has become a key component of QSR strategies, improving both operational efficiency and customer engagement. For instance, KFC introduced South Africa’s first WhatsApp ordering system in January 2025, catering to younger consumers through low-data, mobile-friendly platforms[2]Source: KFC, "KFC South Africa: First QSR to launch WhatsApp ordering in SA," kfc.com. Digital ordering systems, app-based delivery services, and integrated point-of-sale solutions have streamlined operations, optimized workforce management, and extended market access beyond traditional urban areas.

Tourism and hospitality expansion

The growth of South Africa’s tourism and hospitality industry has significantly contributed to the expansion of the foodservice market, driving demand across quick-service, casual dining, and fine-dining segments. Rising tourist arrivals and increased hospitality activities have provided opportunities for both local and international foodservice operators to expand their presence, introduce new menu offerings, and adapt to changing consumer preferences. According to the World Travel & Tourism Council (WTTC), South Africa’s travel and tourism sector is expected to achieve a significant milestone in the coming years. Supporting this trend, South Africa Stats reported that approximately 30.8 million travelers visited the country in 2024, indicating consistent growth in domestic and international tourism[3]Source: Stats South Africa, "Fewer Travellers, More Tourists: SA Sees Shift in Visitor Trends," statssa.gov.za. This increase in visitor numbers has led to higher foot traffic in restaurants, hotels, cafés, and quick-service outlets, boosting foodservice revenues and creating opportunities for new concepts aligned with tourists’ expectations.

Expansion of delivery and digital ordering platforms

The rapid advancement of digital technology and evolving consumer preferences have significantly reshaped South Africa's foodservice market, with delivery and digital ordering platforms becoming major growth drivers. Consumers increasingly prioritize convenience, speed, and flexibility, favoring food delivery via apps, websites, and mobile platforms over traditional dine-in options. This shift has been further driven by the widespread use of smartphones, improved internet connectivity, and the introduction of low-data ordering channels tailored to younger, tech-savvy consumers. Foodservice operators have responded to this trend by collaborating with third-party delivery platforms, creating proprietary apps, and adopting advanced point-of-sale (POS) and logistics systems to improve operations and customer satisfaction. The growth of delivery and digital channels enables restaurants to expand their reach into suburban and previously underserved areas, enhance staff efficiency, and increase revenue without requiring significant physical expansion.

Consumer demand for ethnic and international cuisines

Ethnic cuisine demand reflects South Africa's cultural diversity and growing cosmopolitan preferences, particularly in metropolitan areas. The trend toward "Borderless Cuisine" emphasizes thoughtful cross-cultural flavor combinations, with examples including chakalaka ramen, Thai-style bobotie, and peri-peri Gochujang aioli. The "Culinary Roots" trend emphasizes African heritage grains and reimagined Khoisan stews, creating opportunities for foodservice operators to differentiate through authentic local ingredients while appealing to cultural pride and sense of place. International cuisine expansion benefits from improved supply chains, with Tiger Brands' enterprise supplier development program onboarding agricultural suppliers for diverse ingredients including bitter sorghum and specialty grains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High energy costs and load shedding | -2.8% | National, severe in industrial areas | Short term (≤ 2 years) |

| Supply chain and logistics challenges | -2.1% | Rural-urban corridors, port-dependent regions | Medium term (2-4 years) |

| Economic instability and inflation | -1.9% | National, acute in lower-income segments | Medium term (2-4 years) |

| Rising labor and operational costs | -1.6% | Urban centers, skilled labor markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High energy costs and load shedding

South Africa's foodservice industry is facing operational challenges due to high energy costs and frequent load-shedding, which adversely affect profitability, service reliability, and customer experience. Restaurants, cafés, and quick-service outlets rely extensively on electricity for essential functions such as cooking, refrigeration, lighting, and digital operations. Frequent power outages disrupt these activities, increasing dependence on backup generators or alternative energy sources and driving up operational costs. As a result, operators are compelled to adjust pricing or reduce service offerings. The increasing cost of electricity is prompting foodservice operators to invest in energy-efficient equipment, alternative power solutions, and strategies to optimize operations. For instance, chains like Famous Brands have implemented measures to ensure alternative power coverage for over 90% of their locations, helping to mitigate the impact of load-shedding and maintain service continuity. However, smaller operators often face challenges in securing the capital needed for sustainable energy solutions, exposing them to operational risks and potentially leading to market consolidation.

Supply chain and logistics challenges

The South African foodservice market continues to face persistent supply chain and logistics challenges, affecting product availability, cost management, and operational efficiency. Key factors contributing to these issues include infrastructure constraints, transportation delays, reliance on imports, and fluctuating fuel prices. These challenges are especially significant for perishable goods, frozen products, and high-demand imported ingredients, which require stringent cold-chain management to ensure quality and safety. In response, foodservice operators are adopting strategies such as diversifying suppliers, enhancing local sourcing networks, and investing in inventory management and cold-chain technologies to reduce risks. The demand for agility and reliability has also driven the adoption of technology-enabled logistics solutions, including real-time tracking, predictive demand planning, and integrated supplier platforms. However, supply chain volatility continues to impact menu planning, cost control, and pricing strategies, particularly for small- and medium-sized operators with limited bargaining power in supplier negotiations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Foodservice Type: Cloud Kitchens Lead Digital Transformation

Quick Service Restaurants are projected to maintain market dominance with a 48.16% share in 2024, driven by affordability-focused consumer behavior and operational efficiency improvements through technology adoption. Cloud Kitchens are expected to be the fastest-growing segment, with a CAGR of 17.41% during 2025-2030, leveraging the expansion of delivery platforms and reduced operational costs through concepts such as Nevernoteatinggood and Jozi Cloud Kitchens.

Full-service restaurants face challenges from margin pressures but benefit from the recovery in tourism and the growing popularity of experience-driven dining. Premium venues, such as La Colombe, have gained international recognition, ranking #49 in the World's 50 Best Restaurants. The Cafes and Bars segment demonstrates resilience by diversifying into specialty offerings. Brands like Vida e Caffè and Mugg & Bean continue to expand their presence despite economic challenges. This segment also benefits from trends like "Street Food Couture," which elevates everyday dishes, such as gourmet mielies and shisa nyama sosaties, into premium dining contexts while maintaining their authenticity.

By Outlet: Chained Operations Drive Standardization

Independent outlets are projected to hold a 72.02% market share in 2024, highlighting South Africa's fragmented foodservice market and strong entrepreneurial culture. However, chained outlets are expected to grow significantly, with a compound annual growth rate (CAGR) of 15.32% from 2025 to 2030. This growth is attributed to franchisors' ability to utilize technology, implement standardized operations, and optimize supply chains. For instance, Famous Brands plans to open 137 new restaurants in 2024, with 95% of these outlets equipped with alternative power solutions, showcasing how chains enhance operational resilience through strategic infrastructure investments.

Independent operators continue to leverage their local market knowledge and operational flexibility as competitive advantages. However, they face challenges in adopting advanced technologies and optimizing supply chains. Changes in the regulatory framework, such as mandatory spaza shop registration and business licensing requirements, may accelerate formalization trends. These changes are likely to favor chained operations, which already have established systems to ensure regulatory compliance.

By Location: Leisure Venues Capitalize on Experience Economy

Standalone locations are projected to maintain a dominant market share of 86.23% in 2024, reflecting South Africa's urban development trends and consumer preference for dedicated dining establishments. In contrast, leisure venues are expected to be the fastest-growing segment, with a compound annual growth rate (CAGR) of 18.71% during 2025-2030, driven by the recovery of tourism and the increasing demand for experience-oriented consumer activities.

Lodging-integrated foodservice is anticipated to experience steady growth, supported by the recovery of the hospitality sector. These venues are focusing on sourcing local ingredients and incorporating cultural storytelling to enhance guest experiences. The growing trend toward "experiential, bespoke dining" is creating opportunities for smaller, curated venues that emphasize unique and memorable atmospheres over high-volume operations.

By Service Type: Delivery Platforms Transform Access

Dine-in services are projected to retain market leadership with a 56.45% share in 2024, driven by consumer preferences for social dining and experience-oriented behavior. Meanwhile, delivery services are expected to grow at a robust CAGR of 16.34% during 2025-2030, fueled by advancements in platform technology and enhancements in last-mile logistics. For instance, KFC's introduction of a WhatsApp ordering system in January 2025 addresses South Africa's high data costs while leveraging natural language processing to facilitate seamless customer interactions.

Takeaway services are benefiting from consumer demand for convenience and improvements in operational efficiency. Operators such as McDonald's are adopting app-based pickup systems to minimize reliance on third-party platforms and reduce associated commission costs. Additionally, the "Diner Designed" trend highlights the growing importance of customization and personalization, enabled by technology. This trend supports the growth of both delivery and takeaway services by offering streamlined ordering experiences that cater to dietary preferences and promote waste reduction initiatives.

Geography Analysis

Gauteng recorded the highest absolute sales in 2024, with Johannesburg and Pretoria collectively accounting for nearly one-third of all national QSR transactions. The province benefits from dense office hubs that drive weekday lunch demand. Additionally, Gauteng exhibits the highest adoption of loyalty-app rewards, supported by widespread smartphone penetration. The Western Cape leads in premium dining revenue, with La Colombe’s inclusion in the global top-50 restaurant list enhancing international visibility and luxury spending. Wine-estate restaurants in Stellenbosch combine vineyard tours with curated menus, resulting in average ticket sizes exceeding the national average.

Township markets present considerable untapped potential. Initiatives such as SPAR2U's partnerships with local delivery providers are expanding foodservice access to areas like Tembisa, Ivory Park, and Hamanskraal. Regulatory changes requiring spaza shop registration may formalize these markets, creating opportunities for organized foodservice operators to grow through compliant local partnerships. Port infrastructure supports fresh import logistics; however, cold-storage shortages outside eThekwini cause product bottlenecks. The Eastern Cape is experiencing incremental growth as agritourism routes introduce gastro-pubs featuring free-range Karoo lamb.

Formalization rules mandating spaza shop registration could enhance food-safety compliance, enabling bank-financed expansion opportunities. Meanwhile, rural regions face challenges with road conditions that increase freight timelines. However, precision-agriculture platforms are helping smallholder growers connect directly with urban chefs, thereby shortening supply chains.

Mordor Intelligence provides coverage of the food service market across other key regional markets. Detailed country-level analysis extends to Netherlands incorporating local coverage and market participation, as required.

Competitive Landscape

The South Africa foodservice market exhibits moderate consolidation, allowing both established players and new entrants to compete effectively. The market is characterized by a fragmented leadership structure across various segments. Prominent players such as Famous Brands, Yum! Brands (KFC and Pizza Hut), and McDonald's dominate the quick-service restaurant (QSR) category. These companies have achieved their positions through strategies focused on technology-driven expansion and operational resilience, enabling them to adapt to changing consumer preferences and market dynamics effectively.

Emerging opportunities in the market include the growth of cloud kitchen concepts, which offer a cost-effective alternative to traditional restaurant setups. These kitchens operate with reduced overhead costs and focus on delivery services, catering to the increasing demand for convenience among consumers. Additionally, heritage food offerings are gaining traction as consumers show a growing interest in traditional and locally inspired cuisines. This trend provides an avenue for operators to differentiate themselves by incorporating cultural and regional elements into their menus.

Another significant area of opportunity lies in township market penetration, where there is untapped potential for growth. Operators such as Nevernoteatinggood and Spaza Eats are leading the way by implementing scalable business models that integrate reduced overhead costs with delivery platform partnerships. These strategies enable them to reach underserved areas while maintaining operational efficiency. As these trends continue to evolve, they are expected to shape the competitive landscape of the South Africa foodservice market in the coming years.

South Africa Foodservice Industry Leaders

-

Famous Brands Limited

-

McDonald's Corporation

-

Restaurant Brands International Inc.

-

Spur Corporation Limited

-

Yum! Brands Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: A new burger restaurant named ShoSho has opened on Loop Street in Cape Town, founded by entrepreneurs Hanno Pienaar, Werner Neitz, and celebrated rugby stars Cheslin Kolbe and Ox Nché. The concept emphasises South African heritage and flavour, with “ShoSho” referencing local slang that resonates across the country’s diverse linguistic groups.

- October 2025: Global seafood-chef Ángel León launched his first African restaurant, Amura, at the Belmond Mount Nelson Hotel in Cape Town, scheduled to open in December 2025. The concept fuses South African and Mediterranean coastal culinary traditions, emphasising little-known fish species, seaweed, wild herbs, and native spices, all underpinned by a mission of ocean-conscious sourcing and sustainability.

- February 2025: Pret A Manger (UK-based grab-and-go sandwich & coffee brand) has entered the South African market via a licensing deal with Millat Group and opened its first store in Johannesburg. The expansion strategy includes rolling out further outlets in major cities such as Cape Town, Durban, and Pretoria, leveraging a menu that mixes global classics with local flavour adaptations.

South Africa Foodservice Market Report Scope

| Cafes and Bars | By Cuisine | Bars and Pubs |

| Cafes | ||

| Juice/Smoothie/Desserts Bars | ||

| Specialist Coffee and Tea Shops | ||

| Cloud Kitchen | ||

| Full Service Restaurants | By Cuisine | Asian |

| European | ||

| Latin American | ||

| Middle Eastern | ||

| North American | ||

| Other FSR Cuisines | ||

| Quick Service Restaurants | By Cuisine | Bakeries |

| Burger | ||

| Ice Cream | ||

| Meat-based Cuisines | ||

| Pizza | ||

| Other QSR Cuisines |

| Chained Outlets |

| Independent Outlets |

| Leisure |

| Lodging |

| Retail |

| Standalone |

| Travel |

| Dine-In |

| Takeaway |

| Delivery |

| By Foodservice Type | Cafes and Bars | By Cuisine | Bars and Pubs |

| Cafes | |||

| Juice/Smoothie/Desserts Bars | |||

| Specialist Coffee and Tea Shops | |||

| Cloud Kitchen | |||

| Full Service Restaurants | By Cuisine | Asian | |

| European | |||

| Latin American | |||

| Middle Eastern | |||

| North American | |||

| Other FSR Cuisines | |||

| Quick Service Restaurants | By Cuisine | Bakeries | |

| Burger | |||

| Ice Cream | |||

| Meat-based Cuisines | |||

| Pizza | |||

| Other QSR Cuisines | |||

| By Outlet | Chained Outlets | ||

| Independent Outlets | |||

| By Location | Leisure | ||

| Lodging | |||

| Retail | |||

| Standalone | |||

| Travel | |||

| By Service Type | Dine-In | ||

| Takeaway | |||

| Delivery | |||

Key Questions Answered in the Report

What is the current value of the South Africa Foodservice Market

The sector generated USD 10.16 billion in 2025 and is projected to double to USD 20.11 billion by 2030.

Which segment is growing fastest in the sector

Cloud kitchens are forecast to advance at a 17.41% CAGR between 2025 and 2030 as delivery penetration deepens.

How significant is delivery in driving future sales

Delivery sales are on a 16.34% CAGR trajectory thanks to low-data WhatsApp ordering and expanded township logistics.

What share do independent restaurants hold

Independents controlled 72.02% of 2024 revenue, though chains are scaling rapidly through franchise investment.

Page last updated on: