United States Ready Meals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

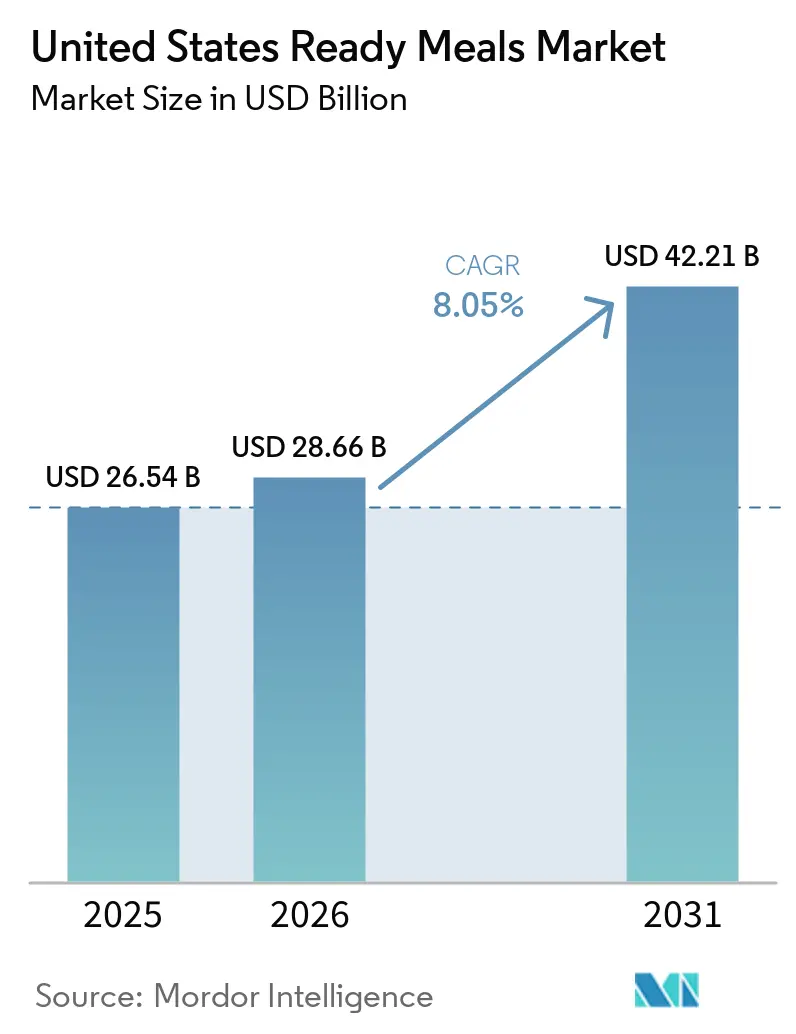

| Base Year Market Size (2025) | USD 26.54 Billion |

| Market Size (2026) | USD 28.66 Billion |

| Market Size (2031) | USD 42.21 Billion |

| Growth Rate (2026 - 2031) | 8.05% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Ready Meals Market Analysis by Mordor Intelligence

The U.S. ready meals market size was valued at USD 26.54 billion in 2025 and is estimated to grow from USD 28.66 billion in 2026 to reach USD 42.21 billion by 2031, at a CAGR of 8.1% during the forecast period (2026-2031). The U.S. ready meals market is moving from occasional convenience use to a more routine role in household meal planning because time pressure, smaller household formats, and stronger retail execution are all reinforcing repeat purchase. Demand is also being supported by a household structure that favors faster meal solutions, with 39.7 million one-person households in the United States in 2025 and 49.1% of married-couple families having both spouses employed in 2025 [1]Source: U.S. Census Bureau, “Fewer Than Half of U.S. Households Are Married-Couple Households,” U.S. Census Bureau, census.gov. The U.S. ready meals market remains moderately fragmented, so large manufacturers still benefit from scale, but focused brands in chilled, organic, and clean-label formats are taking share in higher-growth pockets of demand. Regulatory pressure is also shaping product decisions, especially as the FDA’s Phase II sodium reduction guidance and proposed front-of-package labeling framework raise the cost of standing still for conventional packaged meal portfolios [2]Source: U.S. Food and Drug Administration, “FDA Announces Milestone in Sodium Reduction Efforts, Issues Draft Guidance with Lower Target Levels for Certain Foods,” FDA, fda.gov.

Key Report Takeaways

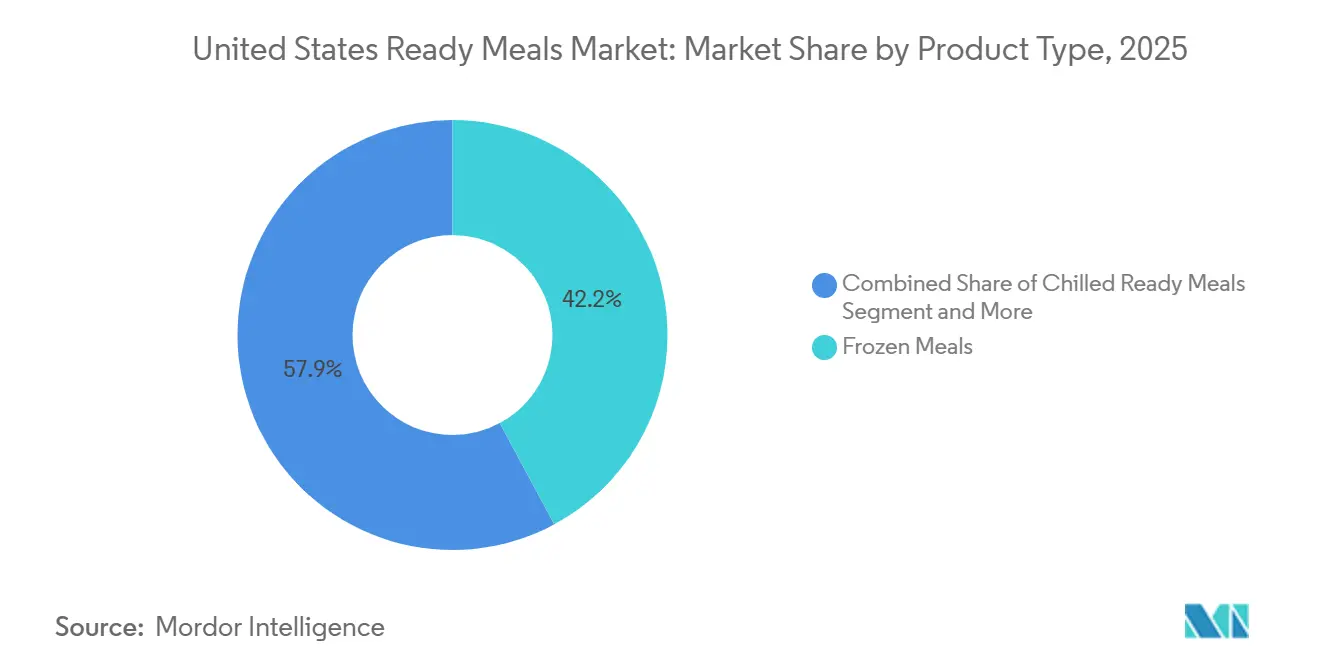

- By product type, frozen ready meals led with 42.15% share in 2025, while chilled ready meals are forecast to expand at an 8.20% CAGR through 2031.

- By ingredient type, non-vegetarian meals held 51.94% share in 2025, while vegetarian meals recorded the highest projected CAGR at 5.12% through 2031.

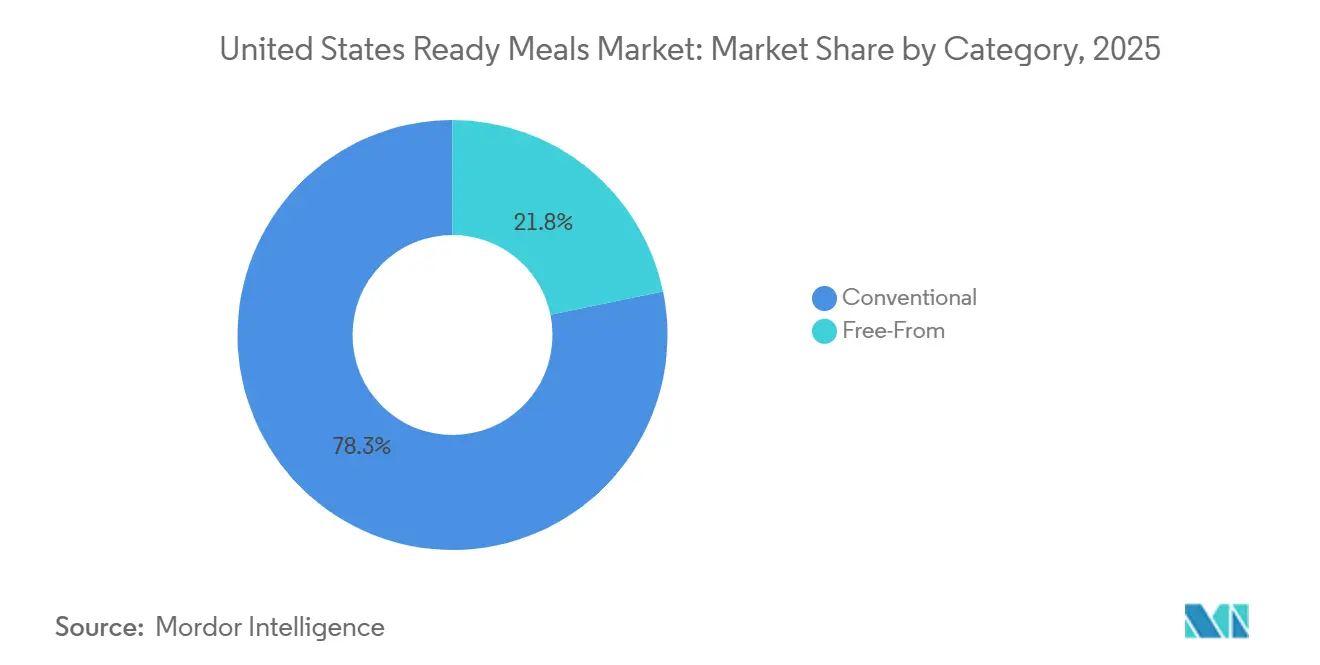

- By category, conventional ready meals accounted for 78.25% share in 2025, while free-from ready meals are advancing at a 6.82% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets held 47.12% share in 2025, while online retail is projected to grow fastest at a 4.20% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Ready Meals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Convenience-Driven Consumption | +2.5% | National, strongest in urban metros such as New York, Los Angeles, and Chicago | Short term (≤ 2 years) |

| Expansion of Dual-Income and Single-Person Households | +1.8% | National, with amplified effect in Northeastern and Western metro areas | Medium term (2-4 years) |

| Growth in Retail Cold Chain and Modern Grocery Infrastructure | +1.2% | National, with Sunbelt and Midwest supply-chain expansion leading | Long term (≥ 4 years) |

| Product Innovation and Premiumization | +1.5% | National, concentrated in higher-income suburban and urban markets | Medium term (2-4 years) |

| Self-Heating Meal Packaging Gains Retail Listings | +0.4% | National, with early adoption in outdoor, convenience, and emergency-preparedness retail | Long term (≥ 4 years) |

| Growing Preference for Ready Plant-Based and Sustainable Meals | +0.6% | West Coast, Northeast, and urban college-adjacent markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Convenience-Driven Consumption

Convenience-driven demand in the U.S. ready meals market is expanding beyond traditionally higher-income consumer segments, as time constraints increasingly affect a broad range of households, employment patterns, and meal occasions. The category also benefits from the scale and established presence of the frozen food aisle, which provides ready meals with strong visibility, distribution reach, and consistent shopper traffic within mainstream grocery retail channels. In parallel, the growth in single-person households is broadening demand for portion-controlled and single-serve meal solutions that reduce preparation effort and food waste. As a result, ready meals are becoming more deeply embedded in everyday meal planning behavior, supporting higher purchase frequency and reinforcing their position as a practical, value-driven convenience offering rather than an occasional backup option. In addition, increasing urbanization and more fragmented daily schedules are reshaping eating habits, with consumers seeking faster, lower-friction meal solutions that fit irregular working hours, commuting patterns, and limited cooking time. This is further accelerating reliance on ready meals as a practical alternative to traditional home cooking. Collectively, these factors are driving greater penetration of ready meals into routine meal planning, elevating them from an occasional convenience fallback to a consistently integrated, value-oriented component of weekly food consumption.

Growth in Retail Cold Chain and Modern Grocery Infrastructure

Cold-chain infrastructure continues to expand the operating capacity and scalability of the U.S. ready meals market, particularly across frozen formats and temperature-sensitive chilled products that require stringent handling and storage compliance. The USDA recorded gross refrigerated warehouse capacity at 3.99 billion cubic feet as of October 1, 2025, with usable freezer space accounting for 79% of total usable refrigerated capacity across 931 warehouses [3]Source: USDA National Agricultural Statistics Service, “Capacity of Refrigerated Warehouses 2025 Summary,” USDA ESMIS, esmis.nal.usda.gov. This established cold-chain backbone ensures broad product availability across both high-density metropolitan areas and secondary markets, reinforcing category penetration and enabling consistent assortment depth at retail. It effectively reduces logistical friction and supports stable in-store execution for ready meals across diverse geographies. Similarly, the addition of new distribution nodes and import-export hubs within key logistics corridors is enhancing national flow-through capacity for refrigerated goods, improving connectivity between supply sources, processing facilities, and retail demand centers.

Product Innovation and Premiumization

Innovation in the U.S. ready meals market is increasingly shifting the category away from a primarily value-oriented proposition toward differentiated positioning anchored in protein density, ingredient quality, and greater alignment with specific consumption occasions. This reflects a broader premiumization trend in which convenience alone is no longer sufficient to drive category growth. Leading meal kit and prepared food players are accelerating product investment cycles, expanding recipe portfolios, upgrading ingredient sourcing standards, and developing targeted meal solutions tailored to evolving consumer needs, including nutrition-forward use cases such as high-protein diets and medically influenced eating patterns. This is strengthening the relevance of ready meals as a more personalized and functional food category. Major food manufacturers are broadening their convenience-focused protein offerings through portable, high-protein formats and expanding into adjacent prepared food subcategories within frozen and deli-style formats. These innovations enhance cross-category penetration and increase relevance across multiple meal occasions, from snacking to full meal replacement. Premium frozen meal providers are also scaling distribution of certified organic and higher-specification product lines through large-format retail channels, reinforcing the role of quality certifications and ingredient transparency as key demand drivers.

Self-Heating Meal Packaging Gains Retail Listings

Self-heating packaging remains a niche but strategically relevant innovation within the U.S. ready meals market, extending category applicability into usage occasions that are not effectively addressed by conventional frozen or chilled formats. These systems function as integrated meal solutions that heat independently of external appliances, making them particularly well-suited to environments with limited or no access to a kitchen. This format meaningfully expands the addressable consumption landscape for ready meals into non-traditional channels and contexts such as travel, field-based occupations, emergency preparedness use cases, convenience retail, and outdoor consumption. In doing so, it decouples meal activation from household infrastructure, enabling consumption in mobility-driven and utility-constrained settings. The commercial viability of the format is illustrated by products such as APack Ready Meals, which are marketed as emergency-preparedness meal solutions. Each case contains multiple meal varieties, providing greater menu diversity in situations where consumer appetite and food preferences may be affected by stress or disruption. The meals can be heated and consumed within minutes through an integrated self-heating mechanism, eliminating the need for external cooking equipment and enhancing operational convenience during emergency or field-use scenarios.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health Perception Concerns Related to High Sodium and Additives | -0.8% | National, amplified in health-conscious West Coast and Northeastern markets | Short term (≤ 2 years) |

| Volatility in Raw Material and Packaging Input Costs | -1.2% | National, with heightened exposure for processors in the Midwest and South | Medium term (2-4 years) |

| Rising Compliance Costs Due to Packaging Sustainability Regulations | -0.5% | California, Colorado, Oregon, and Minnesota, with increasing national applicability | Long term (≥ 4 years) |

| Heightened Competitive Pricing Pressure Compressing Margins | -0.9% | National, most severe in mid-tier branded conventional frozen ready meals | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Health Perception Concerns Related to High Sodium and Additives

Health and nutrition perceptions remain a key growth constraint for the U.S. ready meals market, as concerns surrounding sodium content, preservatives, and other additives continue to influence consumer purchasing decisions. Increasing regulatory scrutiny is amplifying this challenge and raising the importance of product reformulation across the category. In August 2024, the U.S. Food and Drug Administration (FDA) issued Phase II voluntary sodium reduction targets covering 163 food categories, including commercially packaged and prepared meals, as part of its broader strategy to reduce average daily sodium intake among U.S. consumers to 2,750 mg [4]Source: U.S. Food and Drug Administration, “FDA Announces Milestone in Sodium Reduction Efforts, Issues Draft Guidance with Lower Target Levels for Certain Foods,” FDA, fda.gov. In parallel, the FDA proposed a front-of-package Nutrition Info Box that would provide simplified nutrient disclosures by classifying sodium, saturated fat, and added sugar levels as low, medium, or high on most packaged food products. These developments have significant implications for ready meal manufacturers because sodium plays a critical functional role in flavor enhancement, shelf-life management, and product stability, particularly within frozen and shelf-stable formats. As front-of-pack labeling and nutrient transparency become more prominent, products perceived as nutritionally unbalanced may face greater consumer scrutiny at the point of purchase.

Volatility in Raw Material and Packaging Input Costs

Input cost volatility remains a persistent challenge for the U.S. ready meals market, as fluctuations in protein, energy, packaging, and other key production inputs continue to create pressure across the value chain. Although inflationary conditions have moderated relative to peak levels, cost structures have not fully normalized, maintaining an elevated operating environment for manufacturers. According to data from the U.S. Bureau of Labor Statistics (BLS), the producer price index for materials used in food manufacturing remained elevated throughout 2025, fluctuating between 264 and 275 compared with a range of 244 to 262 in 2024. The persistence of higher input cost levels indicates that cost normalization across key food manufacturing materials remained incomplete, sustaining pressure on procurement and production economics across the ready meals value chain. The impact is particularly pronounced within the ready meals category, where pricing flexibility is often constrained by retailer promotional programs, private-label competition, and frequent discount-driven purchasing behavior. As a result, manufacturers may have limited ability to fully pass through rising costs without affecting volume performance or market share.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Chilled Formats Threaten Frozen's Long-Term Primacy

Frozen ready meals held 42.15% of the U.S. ready meals market share in 2025, and the segment remained the broadest distribution anchor for the category. The segment’s market leadership is underpinned by the extensive cold-chain infrastructure available across the United States, with freezer storage representing the majority of national refrigerated warehousing capacity. This logistics advantage supports broad geographic distribution, high product availability, and efficient inventory management across national supermarket chains, club stores, mass retailers, and secondary markets. Beyond everyday meal consumption, frozen and shelf-stable ready meals benefit from diversified demand drivers, including pantry stocking, emergency preparedness, travel, and on-the-go consumption occasions. The emergence of self-heating meal technologies further expands the category’s addressable use cases by enabling consumption independent of conventional kitchen infrastructure.

In contrast, chilled ready meals represent the fastest-growing segment of the U.S. ready meals market and are projected to expand at a CAGR of 8.20% through 2031. Growth is being driven by evolving consumer preferences for products that combine convenience with enhanced quality perceptions, premium ingredients, and more personalized nutritional offerings. The format is increasingly positioned at the intersection of health, freshness, and convenience, enabling brands to differentiate beyond traditional value-oriented propositions. Product innovation within the chilled segment is accelerating this transition, with manufacturers expanding menu variety, improving ingredient quality, and developing targeted meal solutions tailored to specific dietary and wellness needs.

By Ingredient Type: Protein Anchors Non-Vegetarian Leadership as Vegetarian Formats Diversify

Non-vegetarian ready meals accounted for 51.94% of the U.S. ready meals market in 2025, reflecting the continued importance of protein-centric consumption patterns within the category. The segment benefits from strong consumer demand for convenient, high-protein meal solutions and remains a key focus area for product innovation among leading food manufacturers. Major protein brands have expanded their presence in the ready meals space through the introduction of portable, protein-forward offerings and convenient meal formats designed to align with evolving consumer preferences. For instance, Tyson Foods has strengthened its position within the U.S. ready meals market through the launch of protein-focused convenience products, including Tyson Chicken Cups and Hillshire Farm frozen sandwich offerings.

Conversely, vegetarian ready meals are projected to expand at a CAGR of 5.12% through 2031, making them one of the faster-growing ingredient-based segments in the U.S. ready meals market. Growth is being supported by rising consumer interest in plant-forward eating habits, clean-label products, and broader dietary diversification rather than exclusively by the plant-based meat alternative trend. The segment is also benefiting from increasing retail acceptance of organic and certified vegetarian meal offerings, particularly within large-format and club retail channels where established brands have successfully expanded distribution. Product innovation is broadening the category beyond traditional vegetarian meals into formats such as grain bowls, burritos, globally inspired cuisines, and allergen-conscious offerings, enabling manufacturers to address a wider range of consumer preferences and eating occasions.

By Category: Free-From Growth Reshapes the Competitive Agenda Beyond Volume Share

Conventional ready meals represented 78.25% of the U.S. ready meals market in 2025, maintaining their position as the dominant category segment due to their affordability, widespread availability, and strong consumer familiarity. The segment continues to benefit from extensive retail penetration, established merchandising practices, and longstanding integration into mainstream grocery purchasing behavior. Its scale advantages are further reinforced by continued investment from leading manufacturers in large-scale production capabilities, reflecting confidence in the sustained demand for conventional ready meal offerings and the importance of operational efficiency in driving category competitiveness.

Despite the dominance of conventional products, free-from ready meals are emerging as one of the most dynamic segments within the market and are projected to expand at a CAGR of 6.82% through 2031. Growth is being driven by increasing consumer focus on ingredient transparency, allergen management, clean-label formulations, and overall health-conscious purchasing behavior. As consumers become more selective about food ingredients, products positioned around the absence of specific allergens, artificial additives, or other perceived undesirable ingredients are gaining broader market acceptance.

By Distribution Channel: Supermarkets Anchor Volume as Digital Channels Redefine Discovery

Online retail is projected to be the fastest-growing distribution channel in the U.S. ready meals market, expanding at a CAGR of 4.20% through 2031. Its strategic importance extends beyond sales growth, as digital platforms are increasingly shaping product discovery, consumer engagement, and repeat purchasing behavior. The online environment enables consumers to evaluate nutritional attributes, ingredient claims, dietary suitability, portion sizes, and value propositions more efficiently than in traditional retail settings. The channel is particularly advantageous for premium, chilled, health-oriented, and specialized ready meal offerings that may have limited physical shelf space within conventional retail formats. By reducing shelf-space constraints and enhancing product visibility, e-commerce platforms provide emerging and niche brands with a scalable route to market.

Supermarkets and hypermarkets remained the dominant distribution channel, accounting for 47.12% of the U.S. ready meals market in 2025. Their leadership is supported by extensive geographic coverage, established consumer shopping habits, and the ability to offer broad product assortments across frozen, chilled, shelf-stable, and premium meal categories. These retail formats continue to serve as the primary volume driver for the industry and remain critical to brand visibility and market scale.

Specialty retailers also play a significant role in category development, particularly for organic, ethnic, free-from, and premium ready meal products where consumers actively seek differentiated ingredients, dietary attributes, and authentic cuisine experiences. Meanwhile, club stores and convenience channels are gaining relevance as manufacturers expand into bulk-pack, portable, and occasion-specific meal solutions. The successful expansion of premium and organic ready meal brands into club retail formats demonstrates the growing importance of alternative retail channels in broadening category reach.

Geography Analysis

The U.S. ready meals market exhibits nationwide penetration; however, demand dynamics, product preferences, and growth opportunities vary significantly across regions. Regional differences in demographics, income levels, urbanization patterns, retail infrastructure, and consumer lifestyles continue to shape category development and product positioning strategies. The Northeast represents one of the most attractive markets for premium and chilled ready meals, supported by high population density, urban living environments, and consumer willingness to pay for convenience-oriented meal solutions. These characteristics create favorable conditions for premiumization, enabling manufacturers to expand higher-value offerings focused on freshness, nutrition, and specialized dietary needs. In contrast, the Midwest remains a core volume market for conventional frozen ready meals. The region benefits from extensive supermarket penetration, strong household adoption of frozen foods, and value-oriented purchasing behavior, making it a key contributor to category scale. Established cold-chain infrastructure and well-developed frozen merchandising programs further reinforce the region’s importance as a stable demand base for mainstream ready meal products.

The Sunbelt is emerging as a major growth region, driven by population expansion, household diversification, and increasing demand for varied meal options. Continued investments in cold-chain infrastructure are improving product availability and supporting the expansion of frozen and chilled ready meals across these fast-growing markets. The West Coast remains a leading market for premium, organic, and free-from ready meals. Strong consumer interest in clean-label, certified organic, and health-focused products makes the region an important launch market for innovative meal concepts, which are often scaled nationally following successful adoption.

Competitive Landscape

The U.S. ready meals market remains moderately fragmented, creating a competitive environment where scale provides operational advantages but does not guarantee market leadership. Large manufacturers such as Nestlé, Conagra Brands, and Kraft Heinz benefit from extensive manufacturing capabilities, established retail relationships, and nationwide distribution networks. However, specialized players continue to gain traction through differentiated positioning in premium, organic, chilled, and clean-label segments.

Companies such as Amy's Kitchen and HelloFresh have strengthened their market presence by focusing on health-oriented, premium, and convenience-driven offerings, while emerging clean-label brands are capitalizing on increasing consumer demand for dietary-specific and ingredient-transparent products. This dynamic enables niche players to compete effectively despite the scale advantages of established incumbents.

Key growth opportunities remain concentrated in affordable premium chilled meals, clean-label shelf-stable products, and personalized nutrition-oriented meal solutions. At the same time, supply-chain capabilities are becoming an increasingly important source of competitive differentiation. Investments in automation, advanced cold-chain infrastructure, and warehouse technologies are improving throughput, inventory management, and service reliability for temperature-sensitive products. As a result, competitive success in the U.S. ready meals market is increasingly determined by product differentiation, innovation capabilities, and execution excellence rather than market concentration alone, allowing both large-scale manufacturers and focused category specialists to capture growth opportunities.

United States Ready Meals Industry Leaders

Nestlé S.A.

Conagra Brands Inc.

The Kraft Heinz Company

Tyson Foods Inc.

Hormel Foods Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Conagra Brands launched Chef Boyardee Skillet Meals, extending the iconic brand into a new ready meal format designed for convenience-oriented households. The launch marks Conagra's strategy of leveraging established brand equity into new prepared meal category segments, with further innovation under the Chef Boyardee brand expected throughout 2026.

- April 2026: Smithfield launched Meal Ready Cuts, a first-of-its-kind lineup of pre-cut, pre-marinated fresh pork delivering meals in under 20 minutes, available nationwide at Walmart, Kroger, Albertsons, and Meijer. Each variety offers up to 19 grams of protein per serving, targeting convenience-and-protein demand with a fresh rather than frozen ready meal format.

- April 2025: Lineage Inc. announced plans to expand its US cold-storage network through two fully automated next-generation cold storage warehouses with Tyson Foods as anchor customer, incorporating LinOS proprietary warehouse execution technology.

- June 2025: Hormel Foods introduced two new HORMEL MARY KITCHEN Hash Skillet varieties, including a Chorizo Skillet delivering 14 grams of protein per serving, expanding the No. 1 US hash brand's lineup into multi-occasion convenience meal formats.

United States Ready Meals Market Report Scope

Ready meals are pre-prepared food products consisting of multiple ingredients that together form a complete meal and require minimal preparation before consumption, typically through microwave heating, oven cooking, or other convenient reheating methods.

The U.S. ready meals market is segmented by product type, ingredient type, category, and distribution channel. By product type, the market is segmented into frozen ready meals, chilled ready meals, shelf-stable ready meals, and self-heating ready meals. Based on ingredient type, the market includes vegetarian and non-vegetarian ready meals. By category, the market is divided into conventional ready meals and free-from ready meals. By distribution channel, the market is segmented into supermarkets and hypermarkets, convenience stores, specialty stores, online retailers, and other distribution channels. The market size and forecasts have been provided in value terms (USD) and Volume (Tons) for all the above-mentioned segments.

| Frozen Ready Meals |

| Chilled Ready Meals |

| Shelf Stable Ready Meals |

| Freeze-Dried Ready Meals |

| Vegetarian |

| Non-Vegetarian |

| Conventional |

| Free-From |

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channel |

| By Product Type | Frozen Ready Meals |

| Chilled Ready Meals | |

| Shelf Stable Ready Meals | |

| Freeze-Dried Ready Meals | |

| By Ingredient Type | Vegetarian |

| Non-Vegetarian | |

| By Category | Conventional |

| Free-From | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Online Retail Stores | |

| Other Distribution Channel |

Key Questions Answered in the Report

What is the expected value of the U.S. ready meals market by 2031?

The U.S. ready meals market is projected to reach USD 42.21 billion by 2031, up from USD 28.66 billion in 2026.

Which product type currently leads sales in U.S. ready meals?

Frozen ready meals led the category with a 42.15% share in 2025 because of strong cold-chain support, long shelf life, and wide retail distribution.

Which product format is growing fastest in the United States?

Chilled ready meals are forecast to grow fastest, at an 8.20% CAGR through 2031, supported by premium positioning and stronger freshness perception.

Why are ready meals becoming more common in U.S. households?

Growth is being supported by time pressure, a rising number of one-person households, and high dual-income family participation, all of which increase demand for faster meal solutions.

Page last updated on: