North America Foodservice Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.13 Trillion |

| Market Size (2026) | USD 1.26 Trillion |

| Market Size (2031) | USD 2.21 Trillion |

| Growth Rate (2026 - 2031) | 11.80% CAGR |

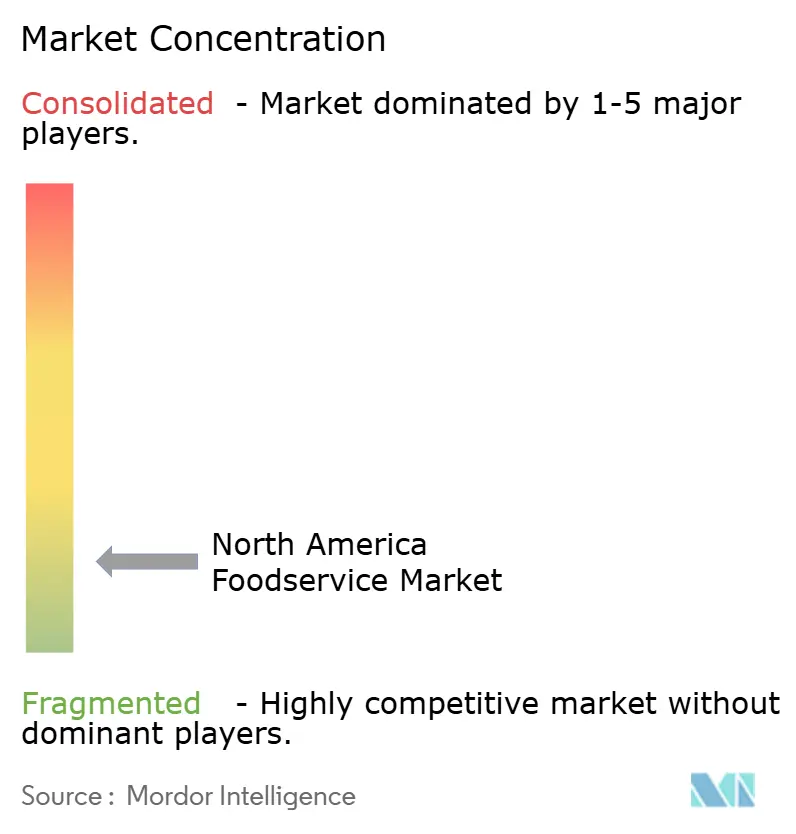

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Foodservice Market Analysis by Mordor Intelligence

The North American foodservice market size was valued at USD 1.13 trillion in 2025 and estimated to grow from USD 1.26 trillion in 2026 to reach USD 2.21 trillion by 2031, at a CAGR of 11.80% during the forecast period (2026-2031). Demand recovery post-pandemic, combined with omnichannel ordering, mobile payments, and digitalization of the supply chain, drives growth. Quick service, delivery-first, and specialty beverage formats capture consumer spending, while operators invest in drive-through lanes, ghost kitchens, and ordering apps to enhance efficiency and ticket values. Technology supports margins by automating back-of-house tasks, allowing labor to focus on customer engagement. Demographic shifts toward diverse, convenience-seeking households are expanding the customer base, ensuring long-term growth in the North American foodservice market. Canada is growing faster than the United States, with a 16.16% CAGR through 2030, driven by favorable licensing and ghost kitchen expansion. The United States, while mature, remains the largest market, while Mexico benefits from rising incomes and urbanization, creating new opportunities for domestic and foreign brands. Advances in order aggregation, delivery routing, smartphone penetration, and digital loyalty programs reinforce convenience and personalization across the region.

Key Report Takeaways

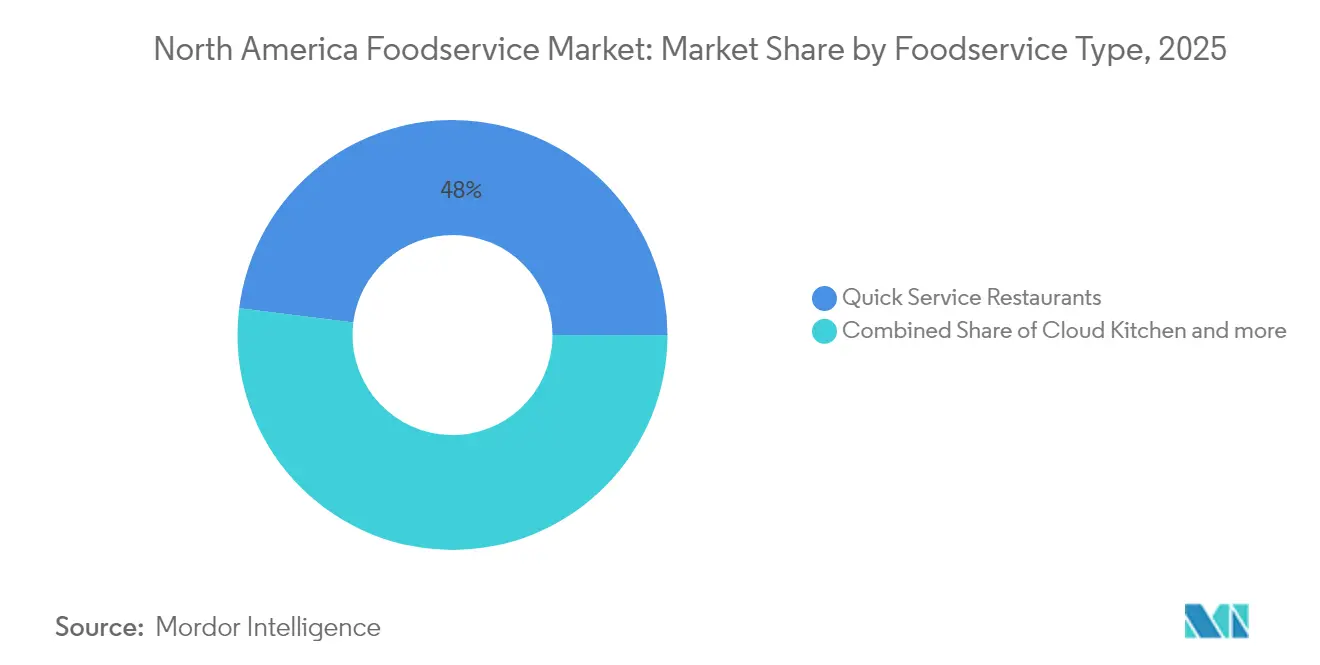

- By foodservice type, quick service restaurants held 48.02% of the North America foodservice market share in 2025, while Cloud Kitchens are projected to record a 14.95% CAGR through 2031.

- By outlet, independent operators accounted for a 54.38% share of the North American foodservice market size in 2025; chained formats are expanding at a 13.10% CAGR through 2031.

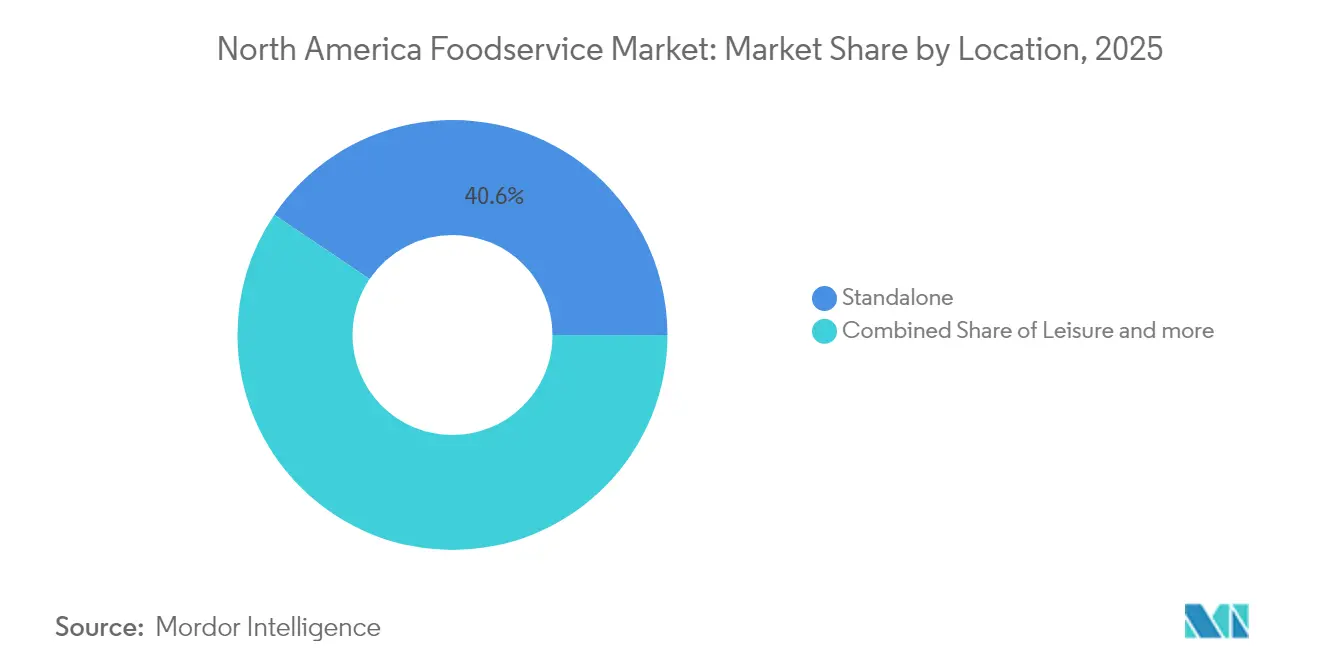

- By location, standalone outlets captured a 40.55% revenue share in 2025, whereas leisure venues are projected to grow at a 14.62% CAGR through 2031.

- By service type, dine-in services earned 51.45% of segment revenue in 2025; delivery services are projected to grow at a 14.66% CAGR between 2026 and 2031.

- Canada leads geographic growth with a 15.85% CAGR, outpacing the broader North American foodservice market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Foodservice Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technological innovation and digital integration | +2.8% | North America-wide, strongest in urban centers | Medium term (2-4 years) |

| Menu innovation and customization | +1.9% | Global, with premium segments leading adoption | Short term (≤ 2 years) |

| Demand for diverse and global cuisines | +1.6% | Urban North America, expanding to suburban markets | Long term (≥ 4 years) |

| Menu innovation and customization (operational efficiency) | +1.4% | Chain operators primarily, spreading to independents | Medium term (2-4 years) |

| Sustainability and ethical practices | +1.2% | North America and European markets, consumer-driven | Long term (≥ 4 years) |

| Expansion of off-premise dining | +2.1% | Global, accelerated in dense urban areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Technological innovation and digital integration

Artificial intelligence, automation, and integrated ordering systems are at the forefront of a digital transformation, reshaping foodservice operations to enhance both customer experience and operational efficiency. McDonald's has rolled out AI-driven voice ordering systems in 13,000 U.S. locations, underscoring the vast scale of this technological shift. Meanwhile, Starbucks employs deep learning algorithms for inventory management, achieving an impressive 15-20% annual reduction in waste. Cloud-based point-of-sale systems are revolutionizing the industry, offering real-time analytics and predictive ordering. This empowers operators to dynamically adjust menu offerings and pricing in response to demand patterns and ingredient costs. Furthermore, the integration of Internet of Things sensors in kitchen equipment is ushering in predictive maintenance capabilities, which not only reduce downtime but also extend the lifecycles of assets. In 2024, a significant 89% of North American consumers embraced mobile payments, solidifying a trend towards contactless transactions that have outlasted their pandemic-era origins.

Menu innovation and customization

Operators leverage personalization technologies to craft bespoke dining experiences, commanding premium prices and fostering customer loyalty through data-driven menu curation and dietary accommodations. In 2024, Chipotle's digital customization platform accounted for 65% of its total revenue, with AI-driven recommendation engines boosting average order values by 18% over traditional methods. Reflecting a shift towards health-conscious and culturally diverse choices, consumers are gravitating towards plant-based protein alternatives and globally-inspired fusion cuisines. Thanks to adaptable supply chain partnerships, operators can rotate seasonal menus, seizing on ingredient cost variations and keeping customers engaged with limited-time offerings. Meanwhile, the adoption of nutritional tracking and allergen management systems not only meets regulatory compliance but also champions consumer health objectives.

Demand for diverse and global cuisines

North America's evolving demographics fuel a growing appetite for genuine international flavors and innovative fusions that marry age-old techniques with local tastes. In 2024, major cities saw Korean, Vietnamese, and Middle Eastern cuisines boost their menu presence by 25-30%, a trend echoing both immigration patterns and the sway of social media in food exploration. Independent operators are tapping into local cultural communities, carving out niche, authentic offerings that stand out against chain rivals. This trend is a boon for ghost kitchen operators, who can now serve a medley of cuisines from a single site, catering to the varied tastes of nearby residents without the usual spatial limitations. Meanwhile, the emergence of food halls and shared kitchen setups is granting smaller ethnic food entrepreneurs access to prime locations, all while allowing them to split operational expenses and leverage cross-marketing strategies.

Expansion of off-premise dining

In 2024, North American delivery sales hit USD 86 billion, with average order values 23% higher than dine-in transactions, driven by convenience premiums and bundling strategies, as reported in DoorDash's SEC 10-K Filing. Third-party delivery platforms and direct-to-consumer ordering systems are not only creating new revenue streams but also reshaping restaurant real estate needs and operational workflows. Urban markets are witnessing a surge in ghost kitchens and virtual restaurant brands, which are lowering capital requirements and facilitating swift geographic expansion and menu experimentation. Enhancements in curbside pickup and drive-through services, such as dedicated mobile order lanes and geofenced arrival notifications, are boosting throughput without compromising service quality. The use of temperature-controlled delivery bags and GPS tracking systems not only addresses food safety concerns but also elevates customer satisfaction. Additionally, the expanding number of foodservice establishments bolsters this market's growth. For example, YUM BRANDS INC, a global restaurant giant, boasts ownership of KFC, Taco Bell, Pizza Hut (including WingStreet), and Habit Burger & Grill, and in 2024, KFC alone had nearly 32,000 outlets, as highlighted by the U.S. Securities and Exchange Commission[1]Source: U.S. Securities and Exchange Commission, "Yum! Brands Form 10-K 2024", sec.gov.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex food safety and health regulations | -1.8% | North America-wide, varying by state/province | Medium term (2-4 years) |

| Food waste management and disposal costs | -1.4% | Urban markets primarily, expanding regulations | Long term (≥ 4 years) |

| Food waste management and disposal costs (operational) | -1.1% | All operators, scale-dependent impact | Short term (≤ 2 years) |

| Supply chain disruptions and rising costs | -2.3% | Global impact, acute in North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Complex food safety and health regulations

Smaller operators, often without dedicated regulatory affairs resources, find themselves disproportionately burdened by evolving food safety standards and health regulations. These regulations not only impose significant compliance costs but also introduce operational complexities. For instance, mid-sized restaurant groups face annual compliance costs averaging between USD 45,000 and 75,000 due to the expanding preventive controls requirements of the FDA Food Safety Modernization Act. Furthermore, state-level mandates such as menu labeling, allergen disclosure, and nutritional information standards add to the administrative load, necessitating system upgrades and staff training. While the rise of artificial intelligence offers advantages in food safety monitoring, the technology demands hefty investments, stretching the budgets of independent operators. Additionally, regulatory fragmentation across provinces and states poses challenges for multi-jurisdictional expansion, especially for emerging chain concepts eyeing rapid geographic growth.

Supply chain disruptions and rising costs

In 2024, food commodity prices rose by 8.2% year-over-year, with protein costs facing heightened inflation driven by feed price fluctuations and constraints in processing capacity. Persistent volatility in supply chains and surging commodity prices are squeezing restaurant margins. These pressures are compelling restaurants to adapt their operations, influencing both menu pricing and ingredient sourcing strategies. Labor shortages in food processing and transportation are causing delivery delays and service disruptions. As a result, operators are compelled to hold larger inventory levels, which not only strains working capital but also heightens the risk of spoilage. Meanwhile, the consolidation of food distribution networks is curtailing competition among suppliers. This shift is amplifying reliance on major distributors and diminishing the negotiating leverage of smaller operators. Additionally, climate-induced disruptions in agricultural production are presenting seasonal availability hurdles, necessitating flexibility in menus and alternative sourcing strategies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Foodservice Type: Cloud Kitchens Disrupt Traditional Models

In 2025, Quick Service Restaurants (QSRs) held a commanding 48.02% market share, skillfully leveraging operational efficiency and brand recognition to appeal to value-conscious consumers amid economic uncertainties. Meanwhile, Cloud Kitchens are emerging as the segment's growth engine, boasting a robust 14.95% CAGR projected through 2031. This growth is not only challenging traditional real estate norms but also facilitating swift market entry for new brands. Full-service restaurants grapple with margin pressures due to escalating labor costs and shifting consumer preferences. In contrast, cafes and bars are reaping the rewards of a trend towards experiential dining and a surge in premium beverage consumption.

As major QSR brands invest in automation and AI-driven operations, the technological divide between chain and independent operators is becoming more pronounced. For instance, McDonald's automated beverage systems and Domino's GPS delivery tracking underscore the competitive edge that technology offers, a feat that smaller operators find hard to match, as highlighted in Domino's Pizza's SEC 10-K Filing. Similarly, as of 2024, Domino's operated 585 stores in Canada, according to the Domino's Pizza SEC 10-K Filing. Cloud kitchen operators, benefiting from reduced overheads and menus tailored for delivery, enjoy profit margins that are 15-20% fatter than their traditional counterparts. Their asset-light model not only allows for swift geographic expansion but also encourages menu experimentation, sidestepping the usual constraints of location and permitting delays. The cloud kitchen market's expansion is further fueled by the entry of major personalities, such as MrBeast with his MrBeast Burger, which has impressively scaled to over 900 locations across the U.S.

By Outlet: Independent Resilience Amid Chain Consolidation

In 2025, independent outlets captured a 54.38% market share and are projected to grow at a 13.10% CAGR through 2031. This growth underscores their resilience against competition from tech-driven chains, largely driven by consumer preference for authentic, locally-sourced dining. Independent operators, with their lower corporate overheads and deep community ties, offer personalized services and customizable menus, allowing them to swiftly adapt to market changes.

Chained outlets, on the other hand, harness economies of scale in purchasing, marketing, and technology. This strategy not only boosts their operational efficiency but also solidifies their brand recognition and standardized service delivery. An expanding store count further bolsters their growth. For example, the U.S. Securities and Exchange Commission reported that in 2024, Burger King boasted 7,082 outlets across the U.S. and Canada, raking in approximately USD 1.45 billion, a notable rise from the prior year's USD 1.3 billion. Meanwhile, the rise of franchise-as-a-service platforms is allowing independent operators to tap into chain-like operational systems, all while retaining local ownership and menu adaptability. Regional chains are carving out a niche, blending operational standardization with insights into local markets and community engagement, an edge over both pure independents and national chains.

By Location: Leisure Venues Lead Experience Economy

In 2025, standalone locations command a 40.55% market share, capitalizing on lower rental costs and greater operational flexibility. Meanwhile, leisure venues are projected to experience a robust 14.62% CAGR through 2031, driven by consumers' growing preference for experiential dining and entertainment. This blending of dining and entertainment not only enhances the customer experience but also opens avenues for increased revenue, as patrons tend to spend more and linger longer. However, retail spots in shopping centers grapple with dwindling foot traffic and evolving consumer shopping habits. As a result, operators are compelled to rethink their service models and how they utilize their spaces.

Travel-centric venues, especially those at airports and along highways, enjoy the advantage of a captive audience. Yet, they navigate distinct challenges, such as stringent security protocols, longer operating hours, and a need for menu adaptability. Foodservice operations within lodgings are pivoting towards collaborations with local cuisine providers and offering grab-and-go selections. These moves cater specifically to the fast-paced nature and dietary needs of business travelers. Furthermore, in high-traffic travel venues, the adoption of mobile ordering and contactless payment systems is paramount, as the speed of service plays a crucial role in ensuring customer satisfaction.

By Service Type: Delivery Transformation Accelerates

In 2025, dine-in services command a 51.45% market share as social dining experiences bounce back post-pandemic. Meanwhile, delivery services surge, boasting a 14.66% CAGR projected through 2031, underscoring a lasting shift towards convenience. Third-party delivery platforms not only open new revenue avenues but also come with commission costs, averaging 15-30% of order values. This dynamic pushes operators to fine-tune menu pricing and boost operational efficiency.

Takeaway services, benefiting from lower labor demands and quicker table turnovers, empower operators to enhance revenue per square foot. This aligns with consumers' growing preference for off-premise dining. While establishing dedicated pickup windows, mobile order-ahead systems, and curbside services demands capital, these investments significantly elevate operational efficiency and customer satisfaction. Ghost kitchen operators shine in delivery-centric setups, crafting menus and packaging tailored for transport, all while sidestepping dine-in costs and spatial constraints.

Geography Analysis

In 2025, the U.S. commands a dominant 48.20% share of North America's foodservice market, buoyed by its established infrastructure and robust consumer spending. Meanwhile, Canada is on a rapid ascent, boasting a 15.85% CAGR through 2031, thanks to aggressive chain expansions and a regulatory landscape that's welcoming to innovative service models. Canadian operators, as highlighted by Statistics Canada Food Services and Drinking Places Survey, enjoy expedited licensing for ghost kitchens and delivery services, allowing them to scale operations faster than their U.S. counterparts. Urban centers in Canada, especially Toronto and Vancouver, are swiftly adopting digital payment systems and contactless services, with AI-driven ordering and inventory management systems leading the charge.

Mexico's foodservice industry is riding the wave of increasing disposable incomes and urbanization. Major cities like Mexico City, Guadalajara, and Monterrey witness a 23% annual surge in international chain penetration, as reported by the Instituto Nacional de Estadística y Geografía. Mexico's pivotal role in North American trade not only offers operators a strategic edge in sourcing ingredients affordably but also opens doors for cross-border expansions. For international brands venturing into Mexico, weaving local cuisine into their offerings is paramount. Successful entrants are those who blend traditional Mexican flavors and cooking techniques into their menus, all while upholding consistent operational standards.

Within the U.S., regional disparities highlight diverse demographic and economic landscapes. Coastal markets are at the forefront of embracing technology and premium dining, whereas interior regions lean towards value-driven concepts and traditional services. High-density urban areas, grappling with soaring real estate costs, are witnessing a surge in food halls and shared kitchen concepts, justifying their collaborative approach. In contrast, rural markets remain steadfast in their support for independent operators, emphasizing community ties and locally-sourced menus.

Competitive Landscape

In North America, the foodservice market is fragmented and fiercely competitive. Major distributors, including Sysco Corporation, Performance Food Group (PFG), and Gordon Food Service, compete for dominance alongside well-known restaurant chains such as McDonald's, Darden Restaurants, and Starbucks. As competition intensifies, these players are adopting innovative strategies to meet evolving consumer demands and overcome operational challenges. Key growth drivers include a surge in consumer spending on fast food, a growing appetite for convenient and ethnic cuisine, and the rising presence of international brands. To bolster their positions in 2024 and 2025, industry giants are making strategic acquisitions, leveraging technology and AI for enhanced efficiency and engagement, and expanding their product lines to cater to health-conscious diners and evolving tastes.

In a bid to fortify its distribution network, Sysco made headlines with its January 2024 acquisition of US Foods. The company is also leveraging AI to streamline logistics, manage inventory, and develop personalized marketing strategies. PFG mirrored this approach, snapping up Cheney Brothers and José Santiago in 2024, a move aimed at broadening its geographic reach and catering to independent foodservice clients. Responding to the growing consumer shift towards plant-based diets, companies are rolling out new offerings. Notably, Starbucks teamed up with Beyond Meat in May 2024, introducing a plant-based protein bowl to its menu. The trend of delivery-only models gained momentum, culminating in the January 2025 merger of Grubhub and Uber Eats, which birthed the entity "Now Delivery." This move underscores a strategic emphasis on optimizing last-mile delivery and broadening service reach.

Restaurant giants are also getting in on the action. McDonald's, for instance, inked a multi-year partnership with DoorDash in March 2024, amplifying its delivery prowess and customer outreach. Yet, amidst these strides, the market grapples with challenges like labor shortages and economic unpredictability. In response, industry players are honing in on operational efficiency and bolstering customer loyalty through enhanced digital experiences and loyalty programs.

North America Foodservice Industry Leaders

-

McDonald’s Corporation

-

Starbucks Corporation

-

Yum! Brands Inc.

-

Inspire Brands Inc.

-

Restaurant Brands International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Flowers Foods, a major U.S. baked goods company known for brands like Dave's Killer Bread and Wonder, acquired Simple Mills, a maker of gluten-free, organic, and plant-based snacks and baking mixes. The acquisition, announced in January 2025 and finalized in the first quarter of 2025, was valued at USD 795 million in cash.

- December 2024: Value Foodservice (VFS), a franchise restaurant operator and portfolio company of private equity firm BlackBern Partners, acquired 11 Kentucky Fried Chicken (KFC) restaurants. The acquisition brought VFS's total number of KFC locations to 59, primarily concentrated in the greater Nashville area.

- May 2024: Starbucks collaborated with Beyond Meat to introduce a new plant-based protein bowl in select U.S. stores. The move was part of Starbucks' strategy to diversify its menu and cater to the growing demand for plant-based and health-conscious food options.

- March 2024: McDonald's and DoorDash entered into a new long-term strategic partnership, expanding their existing collaboration and ending McDonald's previous exclusive arrangement with Uber Eats. The new agreement includes DoorDash powering orders placed through the McDonald's app using its "DoorDash Drive" white-label service.

North America Foodservice Market Report Scope

Cafes & Bars, Cloud Kitchen, Full Service Restaurants, Quick Service Restaurants are covered as segments by Foodservice Type. Chained Outlets, Independent Outlets are covered as segments by Outlet. Leisure, Lodging, Retail, Standalone, Travel are covered as segments by Location. Canada, Mexico, United States are covered as segments by Country.| Cafes and Bars | By Cuisine | Bars and Pubs |

| Cafes | ||

| Juice/Smoothie/Desserts Bars | ||

| Specialist Coffee and Tea Shops | ||

| Cloud Kitchen | ||

| Full Service Restaurants | By Cuisine | Asian |

| European | ||

| Latin American | ||

| Middle Eastern | ||

| North American | ||

| Other FSR Cuisines | ||

| Quick Service Restaurants | By Cuisine | Bakeries |

| Burger | ||

| Ice Cream | ||

| Meat-based Cuisines | ||

| Pizza | ||

| Other QSR Cuisines |

| Chained Outlets |

| Independent Outlets |

| Leisure |

| Lodging |

| Retail |

| Standalone |

| Travel |

| Dine-in |

| Takeaway |

| Delivery |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America |

| Foodservice Type | Cafes and Bars | By Cuisine | Bars and Pubs |

| Cafes | |||

| Juice/Smoothie/Desserts Bars | |||

| Specialist Coffee and Tea Shops | |||

| Cloud Kitchen | |||

| Full Service Restaurants | By Cuisine | Asian | |

| European | |||

| Latin American | |||

| Middle Eastern | |||

| North American | |||

| Other FSR Cuisines | |||

| Quick Service Restaurants | By Cuisine | Bakeries | |

| Burger | |||

| Ice Cream | |||

| Meat-based Cuisines | |||

| Pizza | |||

| Other QSR Cuisines | |||

| Outlet | Chained Outlets | ||

| Independent Outlets | |||

| Location | Leisure | ||

| Lodging | |||

| Retail | |||

| Standalone | |||

| Travel | |||

| Service Type | Dine-in | ||

| Takeaway | |||

| Delivery | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

Market Definition

- FULL-SERVICE RESTAURANTS - A foodservice establishment where customers are seated at a table, give their order to a server and are served food at a table.

- QUICK SERVICE RESTAURANTS - A foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables.

- CAFES & BARS - A type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars.

- CLOUD KITCHEN - A foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers.

| Keyword | Definition |

|---|---|

| Albacore Tuna | It is one of the smallest species of tuna found in the six distinct stocks known globally in the Atlantic, Pacific, and Indian oceans, as well as the Mediterranean Sea. |

| Angus beef | It is beef derived from a specific breed of cattle indigenous to Scotland. It requires certification from the American Angus Association to receive the "Certified Angus Beef" quality mark. |

| Asian cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Chinese, Indian, Korean, Japanese, Bengali, Southeast Asian, etc. |

| Average Order Value | It is the average value of all orders made by the customers at a foodservice establishment. |

| Bacon | It is salted or smoked meat that comes from the back or sides of a pig. |

| Bars & Pubs | It is a drinking establishment that is licensed to serve alcoholic drinks for consumption on the premises. |

| Black Angus | It is beef derived from a black-hided breed of cows that don't have horns. |

| BRC | British Retail Consortium |

| Burger | It is a sandwich consisting of one or more cooked beef patties, placed inside a sliced bread roll or bun roll. |

| Café | It is a foodservice establishment serving various refreshments (mainly coffee) and light meals. |

| Cafes & Bars | It is a type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars. |

| Cappuccino | It is an Italian coffee drink that is traditionally prepared with equal parts double espresso, steamed milk, and steamed milk foam. |

| CFIA | Canadian Food Inspection Agency |

| Chained Outlet | It refers to a foodservice establishment that shares brands, operates in several locations, has central management, and standardized business practices. |

| Chicken Tender | It refers to chicken meat prepared from the pectoralis minor muscles of a chicken bird. |

| Cloud Kitchen | It is a foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers. |

| Cocktail | It is an alcoholic mixed drink made with either a single spirit or a combination of spirits, mixed with other ingredients such as juices, flavored syrups, tonic water, shrubs, and bitters. |

| Edamame | It is a Japanese dish prepared with soybeans (harvested before they ripen or harden) and cooked in its pod. |

| EFSA | European Food Safety Authority |

| ERS | Economic Research Service of the USDA |

| Espresso | It is a concentrated form of coffee, served in shots. |

| European cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Italian, French, German, English, Dutch, Danish, etc. |

| FDA | Food and Drug Administration |

| Fillet Mignon | It is a cut of meat taken from the smaller end of the tenderloin. |

| Flank Steak | It is a cut of beef steak taken from the flank, which lies forward of the rear quarter of a cow. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Franks | Also known as frankfurter or Würstchen, it is a type of highly seasoned smoked sausage popular in Austria and Germany. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Full service restaurant | It refers to a foodservice establishment where customers are seated at a table, give their order to a server, and are served food at a table. |

| Ghost Kitchen | It refers to a cloud kitchen. |

| GLA | Gross Leasable Area |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Grain-fed beef | It is beef derived from cattle that have been fed a diet supplemented with soy and corn and other additives. Grain-fed cows can also be given antibiotics and growth hormones to fatten them up more quickly. |

| Grass-fed beef | It is beef derived from cattle that have only been fed grass as feed. |

| Ham | It refers to the pork meat taken from the leg of a pig. |

| HoReCa | Hotels, Restaurants and Cafes |

| Independent Outlet | It refers to a foodservice establishment that operates with a single outlet or is structured as a small chain with no more than three locations. |

| Juice | It is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| Latin American | It includes full-service offerings in restaurants that serve cuisines from cultures such as Mexican, Brazilian, Argentinian, Colombian, etc. |

| Latte | It is a milk-based coffee that is made up of one or two shots of espresso, steamed milk, and a thin layer of frothed milk. |

| Leisure | It refers to foodservice offered as a part of a recreation business, such as sports arenas, zoos, movie theaters, and museums. |

| Lodging | It refers to foodservice offerings at hotels, motels, guesthouses, holiday homes, etc. |

| Macchiato | It is an espresso coffee drink with a small amount of milk, usually foamed. |

| Meat-based cuisines | This inlcudes food items like fried chicken, steak, ribs, etc. where meat is the primary ingredient for the dish. |

| Middle Eastern cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Arabic, Lebanese, Iranian, Israeli, etc. |

| Mocktail | It is an non-alcoholic mixed drink. |

| Mortadella | It is a large Italian sausage or luncheon meat made of finely hashed or ground heat-cured pork, which incorporates at least 15% small cubes of pork fat. |

| North American | It includes full-service offerings in restaurants that serve cuisines from cultures such as American, Canadian, Caribbean, etc. |

| Pastrami | It refers to a highly seasoned smoked beef, typically served in thin slices. |

| PDO | Protected Designation of Origin: It is the name of a geographical region or specific area that is recognized by official rules to produce certain foods with special characteristics related to location. |

| Pepperoni | It is an American variety of spicy salami made from cured meat. |

| Pizza | It is a dish made typically of flattened bread dough spread with a savory mixture usually including tomatoes and cheese and often other toppings and baked. |

| Primal cuts | It refers to the major sections of the carcass. |

| Quick service restaurant | It refers to a foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables. |

| Retail | It refers to a foodservice outlet inside a mall. shopping complex or a commercial real estate building, where there are other businesses operating as well. |

| Salami | It is a cured sausage consisting of fermented and air-dried meat. |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Scallop | It is an edible shellfish that is a mollusk with a ribbed shell in two parts. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Self-service kiosk | It refers to a self-order point-of-sale (POS) system through which customers place and pay for their own orders at kiosks, enabling totally contactless and frictionless service. |

| Smoothie | It is a beverage made by placing all the ingredients in a container and processing them together, without removing the pulp. |

| Specialty coffee & tea shops | It refers to a foodservice establishment that serves only various types of tea or coffee. |

| Standalone | It refers to a restaurants that have an independent infrastructure setup and not connected to any other business. |

| Sushi | It is a Japanese dish of prepared vinegared rice, usually with some sugar and salt, accompanied by a variety of ingredients, such as seafood—often raw—and vegetables. |

| Travel | It refers to foodservice offerings such as airplane food, dining on long-distance trains, and foodservice on cruise ships. |

| Virtual Kitchen | It refers to a cloud kitchen. |

| Wagyu Beef | It is beef derived from any of four strains of a breed of black or red Japanese cattle that are valued for their highly marbled meat. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for the market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market size estimations for the forecast years are in nominal terms. Inflation is considered for average order value, and it is forecasted as per predicted inflation rates in the countries.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms