U.S. Meal Kit Delivery Services Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

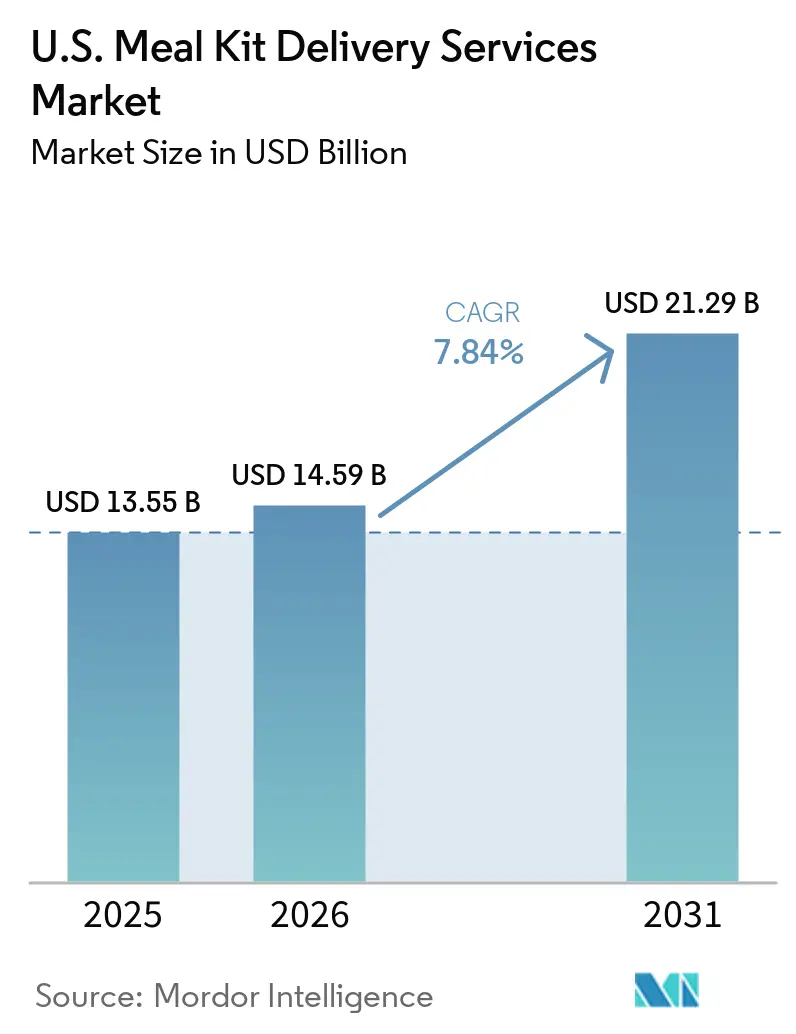

| Base Year Market Size (2025) | USD 13.55 Billion |

| Market Size (2026) | USD 14.59 Billion |

| Market Size (2031) | USD 21.29 Billion |

| Growth Rate (2026 - 2031) | 7.84% CAGR |

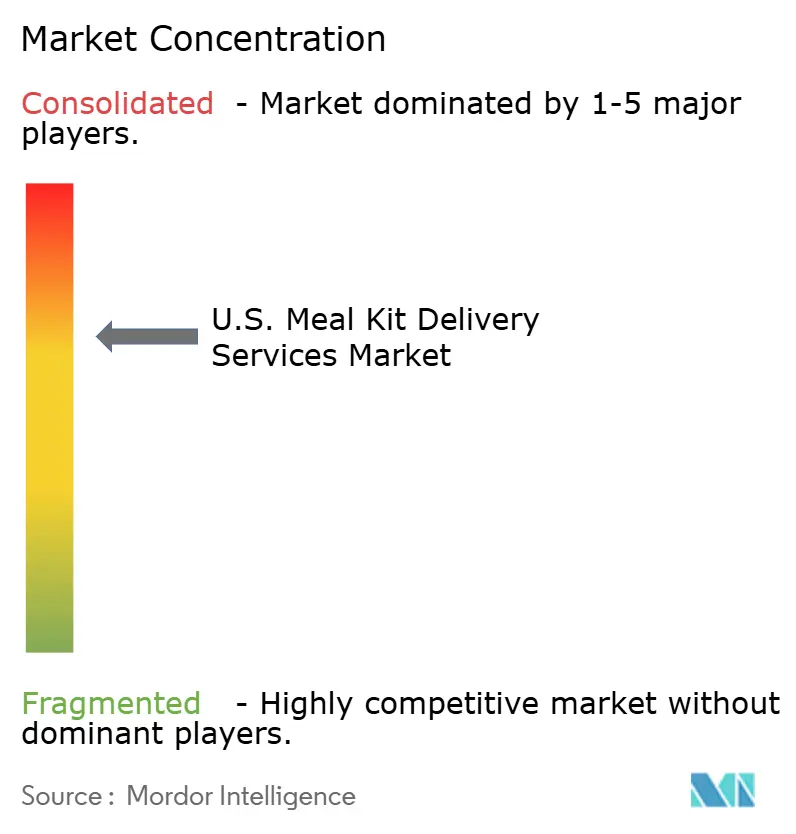

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. Meal Kit Delivery Services Market Analysis by Mordor Intelligence

The U.S. meal kit delivery service market size was valued at USD 13.55 billion in 2025 and estimated to grow from USD 14.59 billion in 2026 to reach USD 21.29 billion by 2031, at a CAGR of 7.84% during the forecast period 2026 to 2031. The U.S. meal kit delivery service market continues to benefit from a clear shift toward home dining, with 60% of U.S. consumers preparing dinner at home at least 5 times per week in 2024 and more than half of shoppers planning to increase home meal preparation. Meal kits are well-suited to that setting because they remove the planning and shopping work while still supporting fresh cooking and ingredient quality. The U.S. meal kit delivery service market is also gaining support from new access channels, including employer and health plan partnerships, as shown by Cigna Healthcare’s 2024 arrangement with HelloFresh that extended discounted access to up to 12 million members. Competition is becoming more selective, with larger operators protecting margins, building personalized menus, and expanding across digital and retail touchpoints, while smaller brands face higher pressure from logistics costs and retention challenges. Subscriber churn remains the main risk, which means the strongest opportunity in the U.S. meal kit delivery service market lies in flexible ordering, better personalization, and benefit-linked access that can hold customers for longer.

Key Report Takeaways

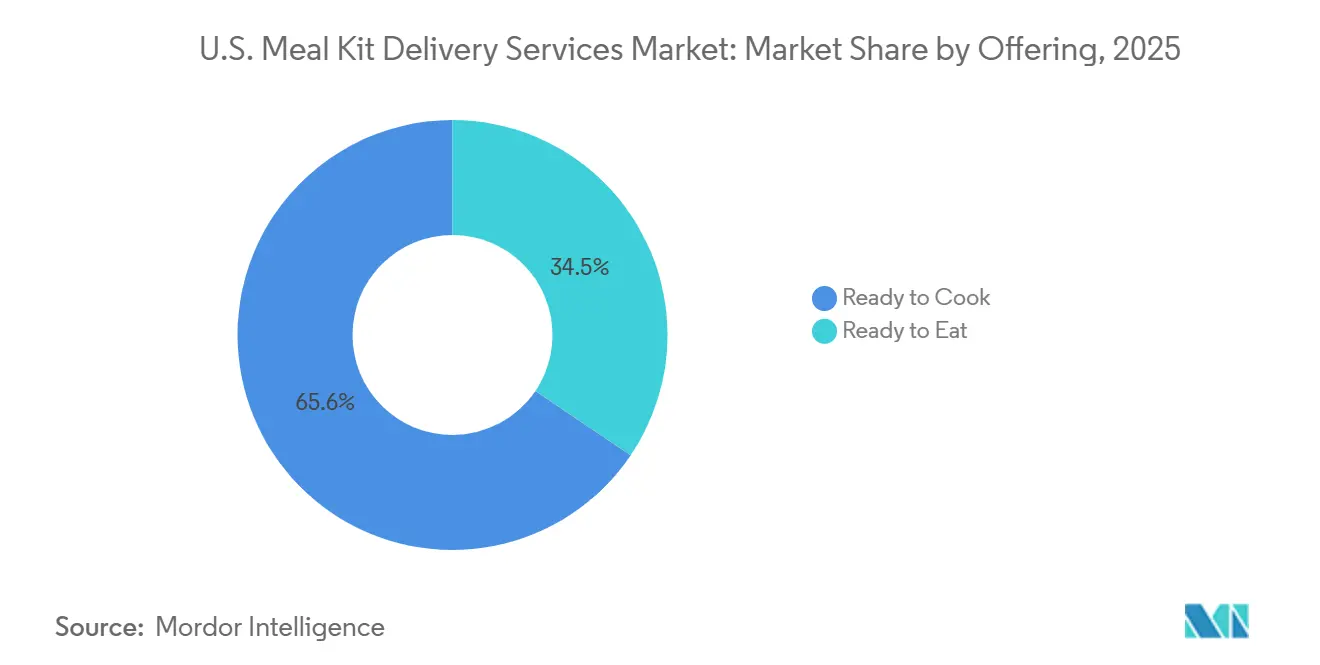

- By offering, Ready to Cook accounted for 65.55% of revenue in 2025, while Ready to Eat is projected to expand at a 8.17% CAGR through 2031.

- By meal type, Non-vegetarian meals accounted for 61.28% of revenue in 2025, while Vegan meals are forecast to grow at 9.29% CAGR through 2031.

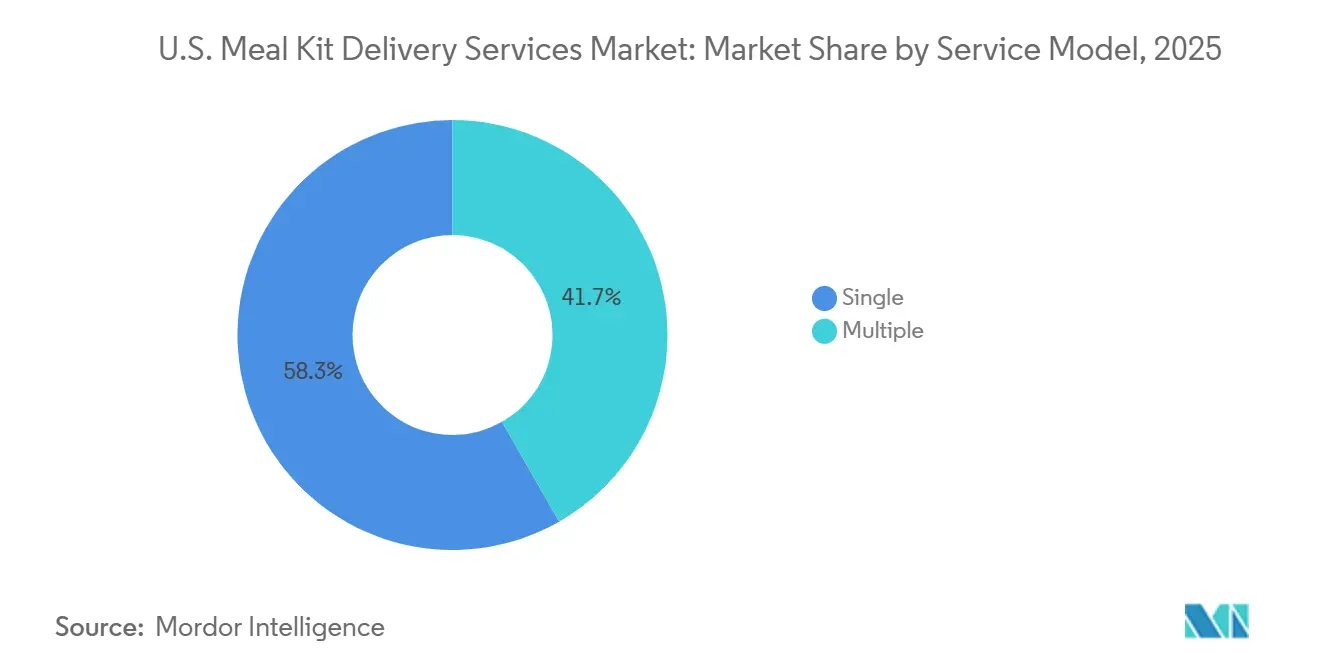

- By service model, Single-service subscriptions held 58.26% of the U.S. meal kit delivery service market share in 2025, while Multiple-service configurations are projected to grow at 8.48% CAGR through 2031.

- By fulfillment channel, Online retail accounted for 64.42% of revenue in 2025, while Offline retail is expected to grow at a 8.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Meal Kit Delivery Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Convenience-Led Home Dining Demand | +2.1% | National, strongest in urban Northeast and West Coast metros | Short term (≤ 2 years) |

| Health-Focused And Portion-Controlled Eating | +1.4% | National, with elevated uptake in coastal and Sun Belt metros | Medium term (2-4 years) |

| Rising Penetration Of Digital Ordering Platforms | +1.2% | National, West South Central and West Coast lead digital adoption | Short term (≤ 2 years) |

| Employer And Payer Meal-Benefit Partnerships | +0.7% | National, with early gains in large employer markets in New York, Texas, and California | Medium term (2-4 years) |

| Advancements In Cold-Chain Logistics | +0.9% | National, highest operational impact in Sun Belt and Mountain West delivery corridors | Medium term (2-4 years) |

| Expansion Of Personalized Meal Options | +1.0% | National, strongest pull in health-conscious Pacific and Middle Atlantic markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Convenience-led home dining demand accelerates meal kit adoption

Structural shifts in how Americans organize their meals continue to underpin steady demand for meal kits. Food Industry Association (FMI) data from 2025 shows that over half of U.S. shoppers plan to prepare more meals at home, and more than one-third eat dinner at home with others every day, reinforcing a durable home-dining orientation. The less-discussed angle is that restaurant recreation is now widespread: 80% of high-income households and 75% of middle-income households actively attempt to recreate restaurant dishes at home, positioning meal kits as a culinary infrastructure rather than a niche premium product, according to the Institute of Food Technologists[1]Source: A. Elizabeth Sloan, “Home-Centric Eating Creates Market Opportunities,” Food Technology Magazine, ift.org. Hybrid meal preparation, combining scratch cooking with semi-prepared components, reached 54% of all home dinners in 2024, up from 51% in 2023, creating a natural entry point for partially prepped meal kits. Gen Z consumers are 2x more likely than older cohorts to seek easy-to-prepare options and meal kits, adding a demographic tailwind to the convenience narrative.

Health-focused and portion-controlled eating reshapes meal kit product design

The convergence of clinical weight-management trends and everyday dietary awareness is materially altering what meal kit providers put in the box. The emergence of GLP-1 medications has created a distinct consumer cohort demanding nutrient-dense, protein-rich, and fiber-forward meals; HelloFresh responded with a dedicated GLP-1 meal collection for the U.S. RTE category in Q1 2025. Green Chef became the only meal kit company to achieve Clean Label Project certification for select recipes in January 2026, backed by a Citrus Labs clinical trial validating that its meals support sustainable weight management and improved gut health. The company followed this with the industry's first Longevity Recipe Collection in March 2026, targeting cellular health and long-term wellness, a positioning that competes directly with functional supplement brands rather than grocery rivals. This shift toward evidence-based health claims is raising the bar for ingredient sourcing standards across the sector. FMI data from 2025 confirms that 47% of U.S. consumers follow a specific eating plan, underpinning a structurally elevated demand for diet-customized meal formats.

Rising penetration of digital ordering platforms drives reach and retention

Digital platform ecosystems are no longer just acquisition channels; they have become infrastructure for customer loyalty, cross-sell, and subscription retention. Blue Apron's transition in 2025 from a rigid weekly subscription model to a flexible à la carte shopping experience, offering 100+ weekly meals, nearly double its prior assortment, with 75% of the menu customizable, represents a direct response to digital consumer behavior that prizes frictionless optionality. Wonder's integration of Blue Apron's meal kit service into its restaurant-ordering app in February 2025 introduced a multi-category ordering model, allowing users to place kit and restaurant orders within a single session, deepening digital stickiness in a way that standalone subscription platforms cannot replicate. Kroger's expanded partnership with Instacart, which now includes an AI-powered "Cart Assistant" for personalized meal planning in Kroger's iOS app, and its new Uber Eats marketplace integration in early 2026, collectively extend Home Chef's digital reach to millions of additional households. HelloFresh's AI embedding across SKU forecasting, menu design, and personalization, cited in its 2025 annual report for managing combinatorial complexity, demonstrates that algorithm-driven personalization is now a core operational advantage rather than a marketing feature. Platform integration at this depth is also suppressing customer acquisition cost, with flexible ordering models forecasting a 25% reduction in CAC according to early operators in the segment.

Employer and payer meal-benefit partnerships unlock new demand channels

The routing of meal kit access through healthcare and employer benefit channels represents one of the least-priced growth vectors in the market. Cigna Healthcare's 2024 partnership with HelloFresh to extend discounted kits to up to 12 million employer plan members was underpinned by hard public health economics: diet-related chronic diseases account for approximately 20% of annual U.S. healthcare costs. InComm Healthcare and Uber Health launched a food delivery benefit program for Medicare Advantage and Medicaid members in January 2025, managing over USD 3.5 billion in supplemental benefit funds and reaching 10 million cardholders across 1,200+ health plans. Misfits Market's partnership with NationsBenefits, launched in March 2025, saw shipments grow by over 250% and revenue increase by over 300% in 2024 through health-plan benefit card integration, demonstrating the scale channel access can unlock[2]Source: Misfits Market Rx, “MM x NationsBenefits – Misfits Market Rx,” Misfits Market Rx, misfitsmarketrx.com. The strategic implication for mid-tier operators is that employer and health plan partnerships effectively convert what was a discretionary household spend into a subsidized, recurring benefit line, meaningfully reducing churn risk. Companies that do not have a healthcare distribution strategy by 2027 may find themselves locked out of this high-retention user segment as plan contract cycles consolidate.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply Chain And Logistics Complexities | -0.9% | National, most acute in Mountain West and rural South delivery corridors | Medium term (2-4 years) |

| High Subscription And Meal Costs | -0.8% | National, disproportionately affecting lower-income quintiles in Midwest and South | Short term (≤ 2 years) |

| Food Waste And Packaging Concerns | -0.5% | National, regulatory influence sharpest in California and Northeast states | Long term (≥ 4 years) |

| Churn And Subscription Fatigue | -1.0% | National, with highest attrition in price-sensitive suburban and rural markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Supply chain and logistics complexities cap margin recovery

Maintaining the cold chain from fulfillment center to doorstep across diverse U.S. geographies remains a structurally expensive challenge. Industry data indicates that meal kit operators face 5-10% refund rates attributable to late deliveries and temperature excursions, with each late delivery costing the equivalent of three to seven future orders in lifetime value. HelloFresh's U.S. RTE operations in Arizona encountered regulatory-driven manufacturing bottlenecks in 2025, necessitating new shelf-life testing protocols and extended reheat times. The FDA's Current Good Manufacturing Practice requirements under 21 CFR Part 117 mandate rigorous preventive controls for RTE foods exposed to the environment prior to packaging, and the FSMA Food Traceability Rule, with a compliance deadline extended to July 20, 2028, places additional record-keeping obligations on operators handling fresh produce, seafood, and cheeses common in meal kits[3]Source: U.S. Food and Drug Administration, “Current Good Manufacturing Practice, Hazard Analysis, and Risk-Based Preventive Controls for Human Food,” Code of Federal Regulations, fda.gov. Smaller regional operators without scale logistics networks absorb these compliance costs at a proportionally higher rate, which constrains their competitive positioning versus vertically integrated national players.

Churn and subscription fatigue limit revenue predictability

Subscriber retention remains the most operationally corrosive challenge in the U.S. meal kit delivery service market. Monthly churn rates of 8-15% produce annualized attrition of 63-85%, and the M3 subscriber survival rate, those still active after 3 months, sits at only 40-55% across the category. The underlying dynamic extends beyond price sensitivity: consumers describe rigid subscription structures as a "chore," and 44% of all cancellations occur within the first 90 days of sign-up. HelloFresh's North America segment saw orders decline 17.0% in FY2025, even as AEBITDA margins expanded, confirming that the revenue base is contracting even for the market leader. The industry's response, shifting from mandatory subscriptions to à la carte and "subscribe and save" hybrid models, may reduce initial conversion rates while improving long-term brand affinity; Blue Apron's A/B testing showed that nearly 65% of customers who initially tried one-time ordering subsequently opted for a subscribe-and-save plan. The risk is that providers trading subscription certainty for flexible models will face more volatile monthly revenues and higher re-acquisition costs during low-engagement periods.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Ready to Eat Gains Ground on Convenience-First Consumers

Ready to Cook held 65.55% of the U.S. meal kit delivery market share in 2025, keeping it clearly ahead of Ready to Eat in terms of current revenue. This part of the U.S. meal kit delivery service market remains strong because many households still want the experience of cooking, plating, and sharing a meal, even when they do not want to spend time building shopping lists or measuring ingredients. That preference is especially durable among households that see dinner preparation as part of their routine rather than as a task they want to eliminate. It also fits the home-dining pattern seen in recent consumer behavior, where fresh cooking remains important but convenience now shapes how ingredients are sourced and organized. In that sense, Ready to Cook remains the core of the meal kit delivery service industry because it balances convenience with participation.

Ready to Eat is projected to grow at a 8.17% CAGR through 2031, making it the fastest-growing format in the U.S. meal kit delivery service market size outlook. The main draw is speed, since this format appeals to younger workers, smaller households, and consumers who want portion-controlled meals without any real preparation step. HelloFresh expanded its ready-to-eat offer in 2025 through the Factor brand, including more menu choice and broader delivery flexibility, which shows how seriously leading companies view this format. Even so, the path is more demanding because ready-to-eat meals must meet stricter plant-level food safety controls and more exact shelf-life handling rules than ready-to-cook boxes. The result is a clear tradeoff in the U.S. meal kit delivery service market, where faster demand growth in Ready to Eat comes with higher operating complexity and tighter compliance expectations.

By Meal Type: Non-vegetarian Anchors Volume While Vegan Reconfigures the Premium Tier

Non-vegetarian meals accounted for 61.28% of revenue in 2025, underscoring how firmly protein-led purchasing still anchors the U.S. meal kit delivery market. The category continues to benefit from broad consumer familiarity, flexible pricing, and the ability to support premium upgrades through seafood, steak, and high-protein menu design. It also aligns with current health behaviors, where many consumers seeking portion control or structured eating plans still want meals built around visible protein. That is one reason non-vegetarian meal kits continue to account for the bulk of volume, even as recipe design shifts to emphasize more fiber, fewer simple carbohydrates, and better nutritional balance. Within the meal kit delivery service industry, this segment remains the clearest bridge between mainstream household demand and premium menu pricing.

Vegetarian meals hold a middle position because they attract households that want to reduce meat intake without fully moving to plant-only menus. Vegan meals are projected to expand at a 9.29% CAGR through 2031, making them the fastest-growing meal type in the U.S. meal kit delivery service market. FMI and IFT reported that 7% of U.S. consumers embraced plant-based eating in 2025, with stronger adoption among millennials and Gen Z, which supports continued interest in vegan meal plans[4]Source: FMI – The Food Industry Association, “FMI Report: Shoppers Stick to Routines and Prioritize ‘Eating Well’ This Fall,” FMI, fmi.org. The bigger change is that vegan formats are now reaching beyond strictly ideological buyers and speaking more directly to consumers who want clean ingredients, variety, and modern nutrition cues. That shift matters because it gives vegan meals a wider customer base in the U.S. meal kit delivery service market, even if non-vegetarian meals continue to dominate absolute revenue.

By Service Model: Multi-service Configurations Reshape Household Economics

Single-service subscriptions accounted for 58.26% of revenue in 2025, indicating that one-account household management still defines the category today. This format fits how many homes make dinner decisions, where one person usually selects meals, manages delivery dates, and controls the grocery budget. It is also a simpler model for operators because it keeps order patterns easier to forecast and reduces billing complexity. In the current U.S. meal kit delivery service market, single-service plans remain the default entry point for new subscribers because they are straightforward and familiar. That makes them important for volume, even as growth is moving more quickly elsewhere.

Multiple-service configurations are expected to grow at a 8.48% CAGR through 2031, signaling a steady shift in how households use shared food subscriptions. The change reflects broader adoption among larger families, bundled household plans, and formats designed for more than 2 servings per order. Blue Apron’s Family Style launch in 2026 showed that companies are now designing meal options around larger shared dinners rather than only around individual or couple use cases. Households that move toward larger plans often improve the operator’s unit economics because delivery and packaging costs can be spread across more servings in each box. For the U.S. meal kit delivery service market, this means future growth in service design will depend less on simple subscription volume and more on how well companies match order size, household structure, and perceived value.

By Fulfillment Channel: Offline Retail Extends Market Access Beyond the DTC Base

Online retail led with 64.42% of revenue in 2025, reflecting the direct connection between meal kits and app-based ordering behavior. This channel remains central to the U.S. meal kit delivery service market because it supports targeted promotions, repeat ordering, customer data collection, and menu personalization in ways physical shelves cannot match. It also gives operators more control over pricing architecture, delivery schedules, and add-on selling. These advantages explain why digital ordering built the category and why it still carries most of the current volume. The online model continues to set the pace for convenience, but it is no longer the only route to scale.

Offline retail is projected to grow at a 8.78% CAGR through 2031, giving it the strongest channel growth profile in the U.S. meal kit delivery service market outlook for fulfillment. Kroger’s Home Chef presence in more than 2,400 stores already shows how retail shelves can work as a trial point for shoppers who may not want to begin with a subscription. Kroger also expanded its digital commerce strategy in 2025, which strengthens the link between in-store visibility and app-based reorder behavior for Home Chef products. As direct-to-consumer acquisition becomes more expensive, retail access gives operators a way to reach shoppers who prefer to try first and subscribe later. This is why the U.S. meal kit delivery service market is increasingly treating offline retail not as a side channel, but as a practical extension of digital customer acquisition.

Geography Analysis

The U.S. meal kit delivery service market had its broadest active-user base in the West and South in 2025, while the West Coast remained one of the strongest penetration zones due to urban density, higher disposable income, and a strong culture of premium grocery and fresh food. California and Washington continue to stand out because they combine large professional populations with high demand for convenience-led food solutions that still feel fresh and customizable. The region also tends to respond well to menu localization, premium ingredients, and sustainability cues, which drive higher order values than in many lower-density markets. These patterns help explain why the U.S. meal kit delivery service market remains strongest in metro areas where time pressure, digital comfort, and food experimentation already shape everyday buying behavior. West Coast demand also benefits from the region’s openness to newer health-led and plant-forward formats, which gives operators room to test premium or specialized offerings before taking them national.

The Middle Atlantic corridor generates above-average order values and remains one of the most attractive pockets of the U.S. meal kit delivery service market for premium positioning. Consumer transaction data cited in the source draft showed that 16% of Home Chef’s user base came from the Middle Atlantic region, and 52% of its customers were in households earning more than USD 100,000 annually, which points to the kind of income profile that can support premium proteins and curated menu options. In practical terms, this region works well for operators that want to sell higher-value plans rather than only lower-priced volume. New York and nearby large metro areas also serve as early testing grounds because they bring together dense households, heavy digital usage, and a large base of dual-income consumers who value time savings. At the same time, the Northeast remains one of the costliest areas for last-mile delivery, so operators need better route planning and strong order density to protect margins.

The South and Midwest offer the widest headroom for the U.S. meal kit delivery service market, but they also create the toughest logistics conditions. HelloFresh had a 14% concentration of its U.S. users in the West South Central region, which reflects the reach of a portfolio that spans from mainstream to value-oriented offerings. Texas stands out because it combines large urban centers, rising multicultural food demand, and broad retail distribution for Kroger-linked meal products. Florida adds another layer of demand, with localized comfort-food preferences showing that menu adaptation can matter as much as pricing in driving repeat orders. Even so, rural and exurban parts of the South and Midwest remain harder to serve because cold-chain transport costs are higher, delivery density is lower, and service recovery is more expensive when late deliveries occur. That leaves these regions as both the largest long-term opportunity and the biggest execution test for the U.S. meal kit delivery service market.

Competitive Landscape

The U.S. meal kit delivery service market remains moderately concentrated, with HelloFresh, Home Chef, Blue Apron, Sunbasket, and Hungryroot accounting for the majority of measured revenue. That concentration does not mean the field is closed, because a second tier of specialists still competes on dietary focus, premium positioning, or chef-led formats, but scale clearly matters more than it did during the category’s earlier growth phase. HelloFresh remains the clearest example of this shift. Its North America AEBITDA margin improved to 9.0% in FY2025 from 7.3% in FY2024, even as segment revenue declined 16.5%, which shows that the market leader chose pricing discipline and cost control over chasing every unit of volume.

HelloFresh also used product changes rather than discounts alone to defend its position. The company said its Refresh program, launched in summer 2025, delivered a cumulative 21% increase in net revenue per conversion after 20 weeks, compared with the comparable 2023 period, indicating stronger monetization driven by better menu design and customer experience. Home Chef is taking a different path in the U.S. meal kit delivery market by leaning on Kroger’s store network and digital ecosystem rather than a pure direct-to-consumer model. Kroger said in 2025 that it was deepening eCommerce capabilities and partnerships that support omnichannel grocery shopping, which directly strengthens Home Chef’s visibility and accessibility through store shelves and digital order flows. That strategy matters because it gives Home Chef a trial channel that many standalone brands do not have.

A third line of competition is forming around access and compliance. HelloFresh’s agreement with Cigna Healthcare expanded discounted meal access to up to 12 million members, which gives the company a route into benefit-based demand that is less exposed to ordinary digital acquisition costs. At the same time, FDA preventive control and traceability rules raise the bar for operators that want to scale in ready-to-eat formats, which means food safety systems are becoming part of competitive positioning rather than only a compliance obligation. This leaves the U.S. meal kit delivery service market in a position where top players still have an advantage, but no single company has enough control to make the market fully tight. The companies most likely to widen their lead are the ones that can combine strong retention tools, broad fulfillment reach, retail or benefits-based access, and disciplined food safety execution without overextending into low-return customer acquisition.

U.S. Meal Kit Delivery Services Industry Leaders

HelloFresh

Home Chef

Blue Apron

Sunbasket

Hungryroot

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: The Cumin Club expanded its retail footprint to 140 H-E-B stores across Texas, bringing its total retail presence to 1,200 stores and targeting one of the largest South Asian populations in the U.S., signaling accelerating multicultural meal kit demand in the Southwest.

- April 2026: Blue Apron (a Wonder company) launched "Family Style," a mix-and-match meal format for households of 3-6 people featuring chef-designed shareable mains and sides ready in under one hour, marking a strategic pivot toward the multi-person household segment.

- March 2026: Green Chef launched its Longevity Recipe Collection, 15 weekly rotating dietitian-curated recipes targeting cellular health, brain function, gut health, and mobility, alongside free one-on-one nutrition coaching with registered dietitians, available through June 2026.

- January 2026: Green Chef achieved Clean Label Project certification for select recipes, validated by a clinical trial demonstrating that its meals are associated with reduced intake of processed foods and improved gut health.

U.S. Meal Kit Delivery Services Market Report Scope

Meal kit delivery services are subscription- or order-based services that provide consumers with pre-portioned ingredients or ready meals delivered directly to their homes for convenient meal preparation and consumption. The U.S. meal kit delivery service market is segmented by offering, meal type, service model, and fulfillment channel. By offering, the market includes ready-to-cook and ready-to-eat meal kits. Based on meal type, the market is segmented into non-vegetarian, vegetarian, and vegan meals. By service model, the market is divided into single- and multiple-meal options. Based on the fulfillment channel, the market covers both online and offline retail. The report analyzes market size and forecasts for the U.S. meal kit delivery service market across these segments. For each segment, market sizing and forecasts have been done on the basis of value (USD).

| Ready to Cook |

| Ready to Eat |

| Non-vegetarian |

| Vegetarian |

| Vegan |

| Single |

| Multiple |

| Online Retail |

| Offline Retail |

| By Offering | Ready to Cook |

| Ready to Eat | |

| By Meal Type | Non-vegetarian |

| Vegetarian | |

| Vegan | |

| By Service Model | Single |

| Multiple | |

| By Fulfillment Channel | Online Retail |

| Offline Retail |

Key Questions Answered in the Report

What is the 2026 size of U.S. meal kit delivery services?

The U.S. meal kit delivery service market stands at USD 14.59 billion in 2026 and is projected to reach USD 21.29 billion by 2031 at a 7.84% CAGR.

Which offering leads U.S. meal kit delivery services today?

Ready to Cook remains the leading format, with 65.55% revenue share in 2025, because many households still want a real cooking experience with less planning effort.

Which meal type is growing fastest in U.S. meal kits?

Vegan meals are forecast to expand at 9.29% CAGR through 2031, even though Non-vegetarian meals still hold the largest revenue share at 61.28%.

Why are meal kits gaining traction with employers and health plans?

Partnerships like Cigna Healthcare and HelloFresh widen access through benefits, which can reduce the purely discretionary nature of spending and improve recurring usage.

Page last updated on: