Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 30.97 Billion |

| Market Size (2026) | USD 32.49 Billion |

| Market Size (2031) | USD 41.34 Billion |

| Growth Rate (2026 - 2031) | 4.93% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Ready Meals Market Analysis by Mordor Intelligence

The Asia-Pacific ready meals market size is expected to grow from USD 30.97 billion in 2025 to USD 32.49 billion in 2026 and is forecast to reach USD 41.34 billion by 2031 at 4.93% CAGR over 2026-2031. This growth is fueled by rapid urbanization, increasing disposable incomes, and smaller household sizes, all leaning towards the allure of convenient, time-saving food options. In nations like China, Japan, and South Korea, tech-driven cold chains not only bolster product safety but also broaden market reach by ensuring efficient storage and transportation of ready meals. Innovations like 'free-from' ingredients, plant-based proteins, and sustainable packaging are attracting a wider audience by catering to health-conscious and environmentally aware consumers. Concurrently, the surge in digital adoption and advancements in last-mile logistics are steering sales towards e-commerce platforms, enabling consumers to access a variety of ready meal options with greater convenience across the Asia-Pacific ready meals landscape.

Key Report Takeaways

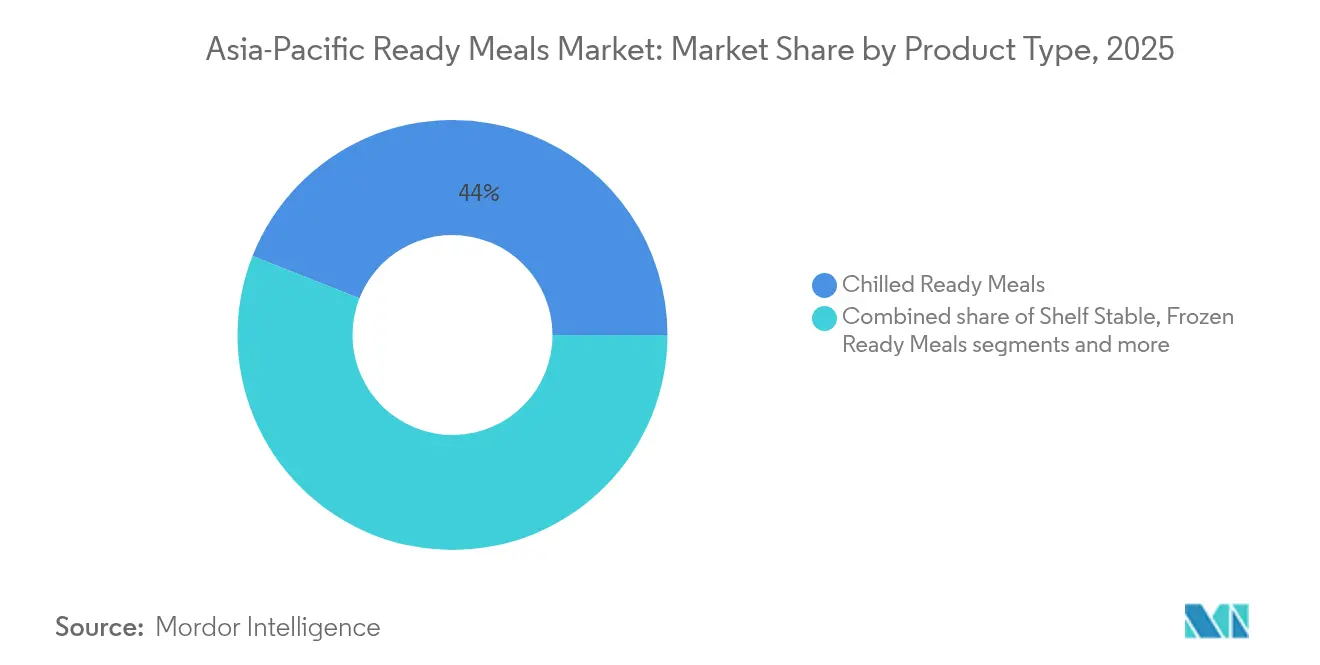

- By product type, chilled products led with 44.02% of Asia-Pacific ready meals market share in 2025, while frozen products are forecast to expand at a 5.16% CAGR through 2031.

- By ingredient, conventional formulations held 81.02% share of the Asia-Pacific ready meals market size in 2025; free-from options record the fastest growth at 5.42% CAGR, through 2031.

- By category, non-vegetarian meals captured 63.02% share of the Asia-Pacific ready meals market size in 2025; vegetarian meals are advancing at a 5.73% CAGR to 2031.

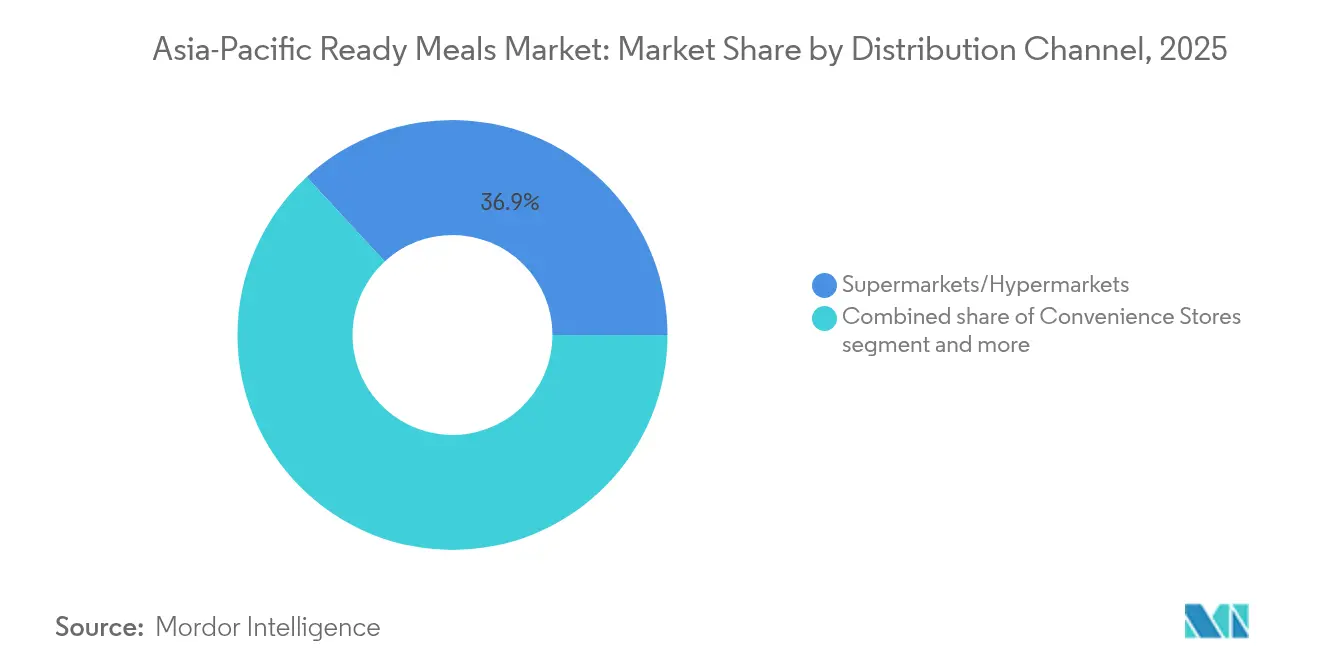

- By distribution channel, supermarkets and hypermarkets accounted for 36.86% of the Asia-Pacific ready meals market share in 2025, while online retail is growing at 6.02% CAGR.

- By geography, China dominated with 30.93% of Asia-Pacific ready meals market share in 2025; the Rest of Asia-Pacific is set to log a 6.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Ready Meals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technological advancements in food preservation | +1.2% | Global, with early adoption in Japan and South Korea | Medium term (2-4 years) |

| Sustainability and eco-friendly packaging | +0.8% | Asia-Pacific core, strongest in Australia and Singapore | Long term (≥ 4 years) |

| Innovation in plant-based and alternative proteins | +0.9% | China, India, and Australia leading adoption | Medium term (2-4 years) |

| Cultural and ethnic diversity | +0.7% | Global, with fusion trends in urban centers | Long term (≥ 4 years) |

| Flavor and culinary trends | +0.6% | Regional variations across all Asia-Pacific markets | Short term (≤ 2 years) |

| Surge in demand for clean-label ready meals | +0.5% | Developed Asia-Pacific markets, expanding to emerging economies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Technological advancements in food preservation

In the Asia-Pacific ready meals market, advanced preservation technologies are not only extending shelf life but also ensuring nutritional integrity and sensory appeal. Governments across the region are actively promoting the adoption of innovative food preservation methods to reduce food waste and enhance food security. For example, the Indian Ministry of Food Processing Industries (MoFPI) has introduced initiatives to modernize food processing infrastructure, including the adoption of advanced preservation methods [1]Ministry of Food Processsing Industries, "Creation/ Expansion of Food Processing/ Preservation Capacities (Unit Scheme)", mofpi.gov.in. Similarly, China's National Development and Reform Commission (NDRC) has emphasized the importance of reducing food waste through technological advancements in food processing and preservation. Moreover, industry associations are playing a crucial role in driving innovation. The Japan Food Industry Association (JFIA) has been actively collaborating with stakeholders to promote research and development in food preservation technologies. These efforts are aimed at addressing the increasing consumer demand for ready meals that offer convenience without compromising on quality or safety.

Sustainability and eco-friendly packaging

The shift towards sustainable packaging is gaining significant momentum across the region, driven by regulatory mandates and the increasing environmental awareness of consumers. Governments in the region are enforcing stricter regulations to reduce plastic waste, while consumers are actively seeking eco-friendly alternatives to align with their values. These efforts have led to the production of carboxymethyl cellulose films, which utilize these agricultural by-products effectively. Additionally, researchers and companies are advancing the development of polylactic acid (PLA) and biogenic vaterite CaCO3-Ag hybrid films. These materials not only exhibit superior antimicrobial properties but also maintain biodegradability, addressing critical concerns related to food safety and environmental sustainability. In markets where sustainability credentials heavily influence purchasing decisions, businesses are capitalizing on this trend. Younger consumers, in particular, are prioritizing eco-friendly options and are willing to pay premium prices for products that align with their environmental values. As a result, the adoption of sustainable packaging solutions is becoming a strategic imperative for companies aiming to thrive in this evolving market landscape.

Innovation in plant-based and alternative proteins

Across the Asia-Pacific, plant-based ready meals are undergoing a wave of innovation. Taiwan's Industrial Technology Research Institute is at the forefront, crafting sophisticated alternatives like plant-based eggs, lobster, and even foie gras, all derived from macroalgae and patented fungal strains. As per the 2023 report by the Good Food Institute, nearly 80% of consumers in Southeast Asia expressed a preference for plant-based meat products, provided these alternatives can be priced 20% lower than their conventional counterparts [2]Good Food Institute, "2023- State of the Industry Report-Plant-Based", www.gfi.org. Government initiatives are further driving this growth. Australia's government introduced grants and subsidies to promote plant-based food production, aligning with its sustainability goals. These measures aim to reduce the environmental impact of traditional meat production while fostering innovation in the food sector. This wave of innovation isn't just about substituting proteins. It's about refining texture, flavor, and nutritional profiles. Companies like Lypid are pioneering plant-based fats that mimic the mouthfeel and cooking properties of their animal-derived counterparts.

Cultural and ethnic diversity

The Asia-Pacific ready meals market is actively leveraging the region's rich culinary heritage by creating fusion cuisines that combine traditional flavors with modern convenience. Korean companies, such as BokManSa, are driving this trend by internationalizing traditional dishes like frozen Gimbap. This approach highlights significant demographic shifts, as the expansion of Asian diaspora communities and the increasing global appreciation for Asian cuisines open up new market opportunities beyond traditional geographic boundaries. Businesses are also extending this cultural fusion into the development of premium products. They are transforming traditional instant noodles into premium offerings by incorporating high-quality ingredients and sophisticated flavor profiles. Indonesians, as reported by the Australian Export Grains Innovation Center in 2024, consume between 12 and 13 billion individual servings of instant noodles annually. This staggering figure represents nearly 15% of the global consumption, translating to roughly 48 packets per person each year. In contrast, Australians average about 16 packets annually, which breaks down to one packet every 3.5 weeks. South Korea stands out as the world's top per capita consumer, with an impressive 73 packets consumed each year, equating to about 1.5 packets weekly [3]Australian Export Grains Innovation Center, "The-Indonesian-noodle-market-2024", www.aegic.org.au

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Short shelf life for premium products | -0.4% | Japan, South Korea, and premium segments across Asia-Pacific | Short term (≤ 2 years) |

| Strong competition from fresh and home-cooked alternatives | -0.6% | Rural areas across Asia-Pacific, strongest in India and Indonesia | Medium term (2-4 years) |

| Taste and quality perception | -0.3% | Global, with cultural variations in acceptance | Long term (≥ 4 years) |

| Limited appeal in rural areas | -0.5% | Rural regions across emerging Asia-Pacific economies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strong competition from fresh and home-cooked alternatives

Traditional cooking practices and a strong preference for fresh food continue to hinder the adoption of ready meals across the Asia-Pacific region. This challenge is particularly pronounced in rural areas, where residents actively engage in cooking due to their well-developed skills and ample time availability. Urban food consumption studies highlight a growing trend of dining out; however, home cooking still holds significant cultural value. For example, rural households in Indonesia consistently choose traditional markets and rice mills over modern retail options. Consumer perception research shows that the packaging of ready-to-eat meals often diminishes their appeal and perceived healthiness. However, when consumers evaluate these products without the influence of packaging, their sensory quality can mitigate these negative perceptions. In markets where food preparation is deeply rooted in cultural identity and family traditions, competition remains intense. As a result, ready meal manufacturers are positioning their products as supplements to traditional meals rather than as complete replacements, aiming to align with these cultural practices.

Short shelf life for premium products

Premium ready meals, particularly those that prioritize fresh ingredients and minimal processing, face significant challenges due to their short shelf life. These constraints actively restrict their distribution reach, as maintaining product freshness becomes increasingly difficult over extended supply chains. The short shelf life not only limits the geographical areas where these products can be sold but also forces manufacturers and retailers to adopt faster turnover strategies to avoid spoilage. Additionally, the limited shelf life elevates inventory risks for manufacturers and retailers, as unsold products are more likely to result in wastage. This issue underscores the importance of efficient logistics, streamlined supply chains, and robust inventory management strategies to mitigate losses and ensure product quality. Companies must also invest in innovative packaging solutions and preservation techniques to extend shelf life without compromising the premium quality that consumers expect. Addressing these challenges is critical for businesses aiming to expand their market presence while maintaining profitability and customer satisfaction.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Frozen Segment Accelerates Despite Chilled Dominance

Chilled ready meals maintain market leadership with 44.02% share in 2025, benefiting from consumer perception of freshness and superior taste profiles compared to frozen alternatives. However, frozen ready meals are experiencing robust growth at 5.16% CAGR through 2031, driven by technological innovations in preservation and expanding cold chain infrastructure across emerging markets. Shelf stable products serve niche applications in rural areas and emergency preparedness, while freeze-dried ready meals target premium outdoor and military segments with extended shelf life capabilities.

Advanced freezing technologies are transforming frozen product quality, with Japanese companies implementing 3D freezing systems that preserve texture and flavor integrity previously achievable only in fresh products. The convergence of preservation technology and consumer convenience preferences suggests frozen segments will continue gaining market share, particularly as distribution networks expand into underserved geographic regions where fresh product delivery remains challenging.

By Ingredient: Free-From Acceleration Challenges Conventional Dominance

In 2025, conventional ingredients dominated the market, holding an 81.02% share. This dominance is attributed to well-established supply chains and the cost advantages associated with traditional formulations, which continue to appeal to manufacturers and consumers alike. Meanwhile, "free-from" products are experiencing significant growth, with a robust 5.42% CAGR projected through 2031. This growth is driven by increasing consumer awareness of health and dietary restrictions, as well as a rising preference for products catering to specific needs, such as gluten-free or allergen-free options. The trend is particularly evident in developed markets, where consumers are more inclined to pay a premium for specialized and health-focused ingredients.

Clean-label trends are exerting a transformative influence on both segments. Conversely, synthetic additives are facing growing resistance due to concerns over their potential health impacts. The ingredient landscape is further evolving due to regulatory developments, including China's proposed labeling standards. These standards aim to enforce clearer ingredient disclosures, which could accelerate the industry's shift toward more recognizable and natural components. Such regulatory changes are expected to impact all product categories, pushing manufacturers to reformulate their offerings to align with consumer demand for transparency and natural ingredients.

By Distribution Channel: Supermarkets/Hypermarkets Dominate, While Online Retail Stoes Surge

In 2025, supermarkets and hypermarkets accounted for 36.86% of the market. This significant contribution was driven by strategic eye-level merchandising, which enhances product visibility and attracts consumer attention. These retail formats also capitalize on impulse purchases, as customers are more likely to add ready meals to their carts when they are prominently displayed. Additionally, supermarkets and hypermarkets offer a wide variety of ready meal options, catering to diverse consumer preferences and dietary needs. Their ability to provide fresh, frozen, and shelf-stable ready meals under one roof makes them a preferred choice for many consumers.

Online retail stores are emerging as a rapidly growing distribution channel in the market. These platforms are projected to experience a 6.02% CAGR through 2031, driven by the increasing penetration of e-commerce and the rising preference for online shopping. Consumers are drawn to the convenience of browsing and purchasing ready meals from the comfort of their homes, with the added benefit of doorstep delivery. Online platforms also offer a broader range of products compared to physical stores, including niche and specialty ready meals that may not be readily available elsewhere. The integration of advanced technologies, such as AI-driven recommendations and personalized shopping experiences, further enhances customer satisfaction.

By Category: Vegetarian Surge Reflects Dietary Evolution

In 2025, non-vegetarian ready meals command a dominant 63.02% market share in the Asia-Pacific ready meals market, buoyed by longstanding preferences for traditional proteins and well-established supply chains for both meat and seafood. The region's cultural inclination toward meat and seafood consumption, coupled with the availability of diverse non-vegetarian ready meal options, has solidified this segment's leadership. Countries like China, Japan, and South Korea are key contributors to this dominance, driven by their rich culinary traditions and high demand for convenience foods. Meanwhile, vegetarian options are on a rapid ascent, boasting a 5.73% CAGR projected through 2031. This surge underscores a shift in dietary choices and a growing environmental awareness, especially among the younger demographic. Urban centers across the region, such as Tokyo, Shanghai, and Taipei, are at the forefront of this movement, witnessing a pronounced acceptance of plant-based alternatives. The increasing influence of Western dietary trends and the rising popularity of flexitarian diets are further fueling the growth of vegetarian ready meals in the Asia-Pacific market.

Driving the expansion of this category is a wave of innovation in plant-based proteins. Notably, research institutes in Taiwan are pioneering advanced alternatives, crafting plant-based seafood and meat analogs from macroalgae and fungal strains. These innovations are not only catering to the growing vegetarian and vegan population but are also appealing to health-conscious consumers seeking sustainable and nutritious meal options. The Asia-Pacific region's robust R&D capabilities, combined with government support for sustainable food production, are expected to accelerate the development and adoption of plant-based ready meals. Additionally, collaborations between food manufacturers and research institutions are playing a pivotal role in enhancing the taste, texture, and nutritional profile of plant-based products, further driving their acceptance among consumers.

Geography Analysis

In 2025, China commands a 30.93% share of the Asia-Pacific ready meals market, capitalizing on its vast urban populace, a well-established cold chain infrastructure, and advanced food processing capabilities. This market thrives on robust domestic demand, fueled by the fast-paced lifestyles of urban dwellers and a rise in disposable income among the middle class. Additionally, China's strong distribution networks and government support for the food processing industry further bolster its dominance in the region. The presence of leading domestic and international players in the country also contributes to the market's growth, as they continue to innovate and expand their product portfolios to cater to evolving consumer preferences.

Meanwhile, the broader Asia-Pacific region showcases the most significant growth potential, projected at a 6.21% CAGR through 2031. This surge is largely attributed to emerging markets such as India, Indonesia, and Vietnam, where ready meal penetration remains low but adoption rates are witnessing a swift uptick. These countries are experiencing rapid urbanization, rising disposable incomes, and a growing preference for convenient food options, which are driving the demand for ready meals. Furthermore, improvements in cold chain logistics and increasing investments by key players in these markets are expected to accelerate growth during the forecast period.

For instance, India is witnessing a surge in demand for frozen and shelf-stable ready meals due to the expanding working population and the influence of Western food habits. Similarly, Indonesia and Vietnam are benefiting from the rising number of supermarkets and hypermarkets, which are improving the accessibility of ready meals to a broader consumer base. The region's growth is also supported by the increasing penetration of e-commerce platforms, enabling consumers to purchase ready meals conveniently. These factors collectively position the Asia-Pacific region as a lucrative market for ready meal manufacturers and suppliers.

Competitive Landscape

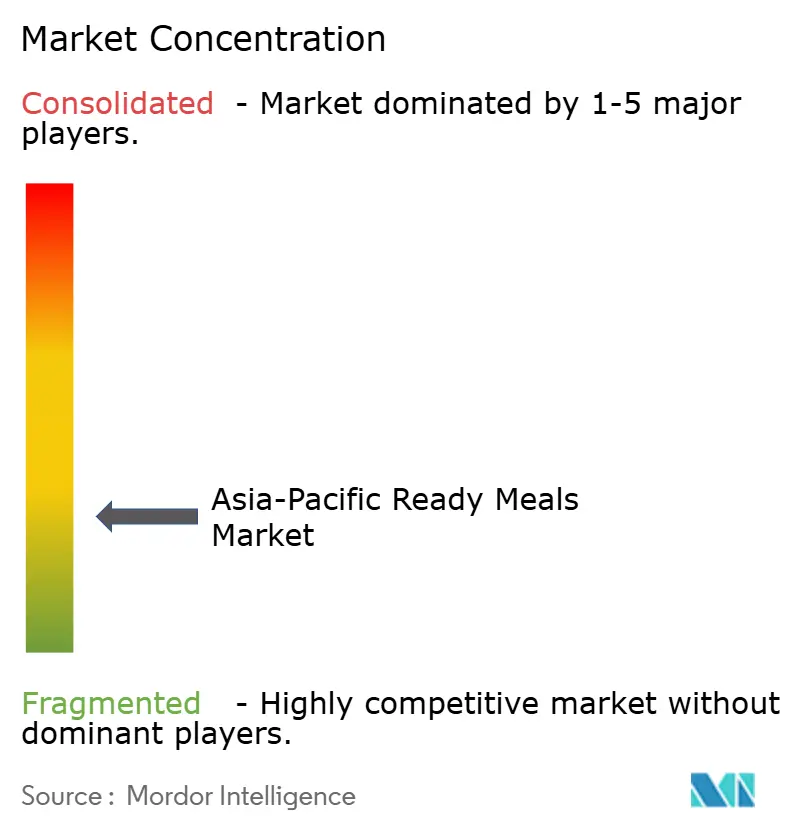

In the Asia-Pacific ready meals market, a concentration score of 3 out of 10 highlights a fragmented competitive landscape. This fragmentation, driven by diverse cultural preferences and regulatory nuances, leans towards regional specialization rather than a one-size-fits-all global approach. The market's diversity creates significant opportunities for both established multinational corporations and emerging local players to differentiate themselves. By focusing on tailored product development and region-specific distribution strategies, companies can effectively address the unique demands of various consumer segments across the region. Additionally, the fragmented nature of the market allows smaller players to thrive by catering to niche markets, while larger corporations can leverage their resources to scale operations and expand their footprint in high-growth areas.

Strategic partnerships and joint ventures are playing a pivotal role in reshaping the competitive dynamics of the market. Notable examples include CP Foods collaborating with Maejo University to conduct hemp research aimed at developing healthier ready meals, catering to the growing consumer demand for nutritious and innovative food options. This partnership underscores the increasing importance of research and development in creating differentiated products that align with evolving consumer preferences. Additionally, the CP Foods-Uoriki joint venture is targeting Thailand's premium seafood market, leveraging their combined expertise to meet the rising demand for high-quality seafood products. Such collaborations not only enhance product offerings but also enable companies to strengthen their market position by tapping into specialized segments.

Furthermore, the competitive landscape is becoming increasingly complex due to the growing influence of e-commerce platforms and direct-to-consumer brands. These channels often bypass traditional retail networks, enabling brands to directly engage with consumers and build stronger relationships. This shift is intensifying competitive pressures on established distribution networks, compelling incumbent players to invest in and develop robust omnichannel strategies to maintain their market relevance and effectively compete in this evolving environment. Companies are increasingly focusing on integrating online and offline channels to provide a seamless shopping experience, ensuring they remain competitive in a market that is rapidly adapting to digital transformation.

Asia-Pacific Ready Meals Industry Leaders

-

McCain Foods Ltd

-

Nestlé SA

-

The Campbell's Company

-

Ajinomoto Co., Inc.

-

Conagra Brands Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Iceland Foods launched its first Asia-Pacific retail operation, in China, in a bid to bring western cuisine to the Chinese retail market. The store forms part of a new strategic tie-up with retail concept company BTG We Link, and will offer shoppers in China over 100 products from the retailer’s frozen range including frozen ready meals from the end of June via multiple ecommerce platforms.

- April 2025: AEON Co., Ltd. has unveiled three new frozen meal products under its private brand, “TOPVALU BestPrice”. The new lineup, dubbed “Frozen One-Plate”, showcases three varieties inspired by beloved Japanese and Western dishes: Gomoku Rice with Chicken in Black Vinegar Sauce, Cheese Curry with Hamburger Steak, and Peperoncino with Tomato Sauce Hamburger Steak.

- December 2024: Hokka-Hokka Tei, a Japanese bento chain, is set to introduce frozen boxed meals, priced at approximately JPY 250 (USD 1.75), in Philippine supermarkets by 2025. The move aims to cater to busy working families and bolster the affordable ready meal segment across Southeast Asia.

- November 2024: Nissin Foods, in collaboration with Nissin Asia, has launched Australia Nissin Foods Pty., Ltd., aiming to tap into the burgeoning instant noodle markets of Australia and New Zealand. The newly formed joint venture will focus on importing and selling a range of products, including instant noodles, snacks, cereals, and other food items, across both countries. This move marks Nissin's strategic establishment of a local footprint in the region.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Asia-Pacific ready meals market as all pre-cooked, shelf-stable, chilled, or frozen entrees that require no further culinary preparation beyond heating before consumption. Products sold through retail and direct-to-consumer channels across China, India, Japan, Australia, South Korea, ASEAN, and other regional economies are captured.

Scope exclusion: food-service meal kits and on-premise cafeteria meals fall outside this boundary.

Segmentation Overview

-

By Product Type

- Frozen Ready Meals

- Chilled Ready Meals

- Shelf Stable

- Freeze-Dried Ready Meals

-

By Ingredient

- Conventional

- Free-From

-

By Category

- Vegetarian

- Non-vegetarian

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail Stores

- Other Distribution Channels

-

By Geography

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

We interviewed processors, cold-chain operators, retail buyers, and e-grocery platforms across China, India, Japan, and Indonesia. Conversations clarified average selling prices, emerging "free-from" claims, channel mix shifts, and inventory turn rates, which our team used to stress-test desk findings and refine assumptions.

Desk Research

Analysts first mined open datasets from bodies such as FAO, UN Comtrade, national statistics bureaus, and trade associations like the Japan Frozen Food Association. They then layered in company 10-Ks and investor decks, retail scanner releases, and press coverage from Dow Jones Factiva and D&B Hoovers. Where supply visibility mattered, shipment traces from Volza and contract notices from Tenders Info helped map cross-border flows. These sources establish baseline production, trade, price, and consumption signals; however, they are illustrative rather than exhaustive, and many additional publications informed the build.

Market-Sizing & Forecasting

A top-down and bottom-up hybrid is employed: regional production plus net imports reconstruct total available supply, which is then reconciled with demand pools derived from urban household counts and per-capita spend patterns. Supplier roll-ups and sampled ASP x volume checks provide a bottom-up reasonableness screen before totals lock. Key variables in the model include:

urbanization rate and dual-income household share, indicating convenience demand,

per-capita disposable income (constant USD) to gauge price headroom,

average retail shelf price per 400 g meal pack,

cold-chain capacity additions, a proxy for chilled/frozen penetration,

e-commerce share of grocery spend signaling online acceleration.

A multivariate regression with scenario overlays projects each driver through 2030; gaps in granular supplier data are smoothed using regional averages and validated through channel-partner feedback.

Data Validation & Update Cycle

Outputs pass anomaly scans against independent food expenditure series, with variances routed to a second-analyst review. Before release, we re-contact key respondents if macro or regulatory events materially shift assumptions. Reports refresh every twelve months, and interim flashes are issued when major developments hit.

Building Confidence in Our Numbers: Why Mordor's Asia-Pacific Ready Meals Baseline Earns Trust

Published estimates often differ because firms pick varied product scopes, price points, and refresh rhythms.

Key gap drivers include: some publishers bundle instant noodles or meal kits, others freeze 2022 exchange rates, while Mordor's page reports 2025 values in constant 2024 USD and excludes meal-service kits entirely. Certain rivals project aggressive e-commerce surges without cross-checking cold-chain limits, whereas we temper forecasts using verified capacity rollouts and primary ASP guidance.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 30.97 Bn (2025) | Mordor Intelligence | - |

| ~USD 23.5 Bn (2025) | Global Consultancy A | Uses fixed 14.5 % regional share of global total; lacks channel-level validation |

| ~USD 33.8 Bn (2025) | Trade Journal B | Assumes 20 % global share and counts meal-kit deliveries within scope |

These comparisons show how differing inclusions and currency bases widen spreads. By anchoring figures to clear product definitions, live exchange rates, and regularly updated primary insights, Mordor Intelligence delivers a balanced, reproducible baseline that decision-makers can rely on.

Key Questions Answered in the Report

How large is the Asia-Pacific ready meals market in 2026?

It is valued at USD 32.49 billion, with a forecast to reach USD 41.34 billion by 2031.

Which product type is growing fastest?

Frozen ready meals register the highest growth at a 5.16% CAGR thanks to 3D-freezing and wider cold-chain reach.

Why is online retail important for ready meals?

E-commerce offers same-day delivery and broad assortment, driving a 6.02% CAGR for online sales channels through 2031.

Which country leads the regional market?

China holds the top position with 30.93% market share, supported by large urban populations and robust cold-chain logistics.

How fragmented is the competitive landscape?

The market is highly fragmented with a concentration score of 3, meaning significant room exists for both multinationals and agile local entrants.

Page last updated on: