Material Handling Integration Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

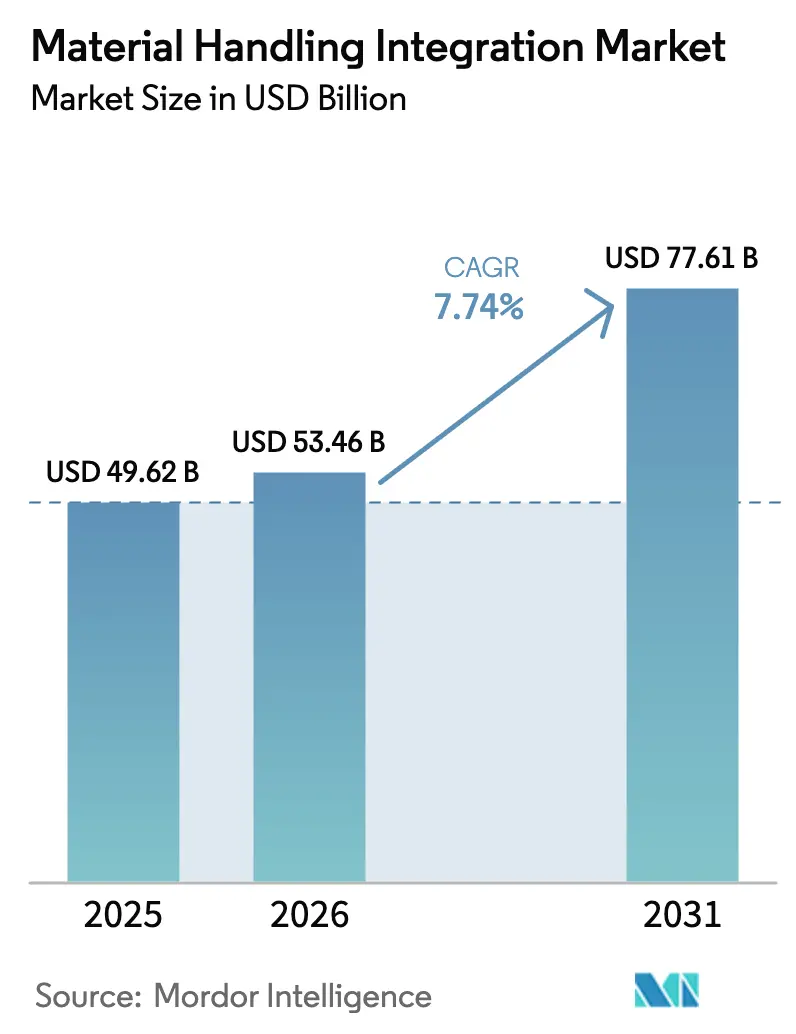

| Market Size (2026) | USD 53.46 Billion |

| Market Size (2031) | USD 77.61 Billion |

| Growth Rate (2026 - 2031) | 7.74% CAGR |

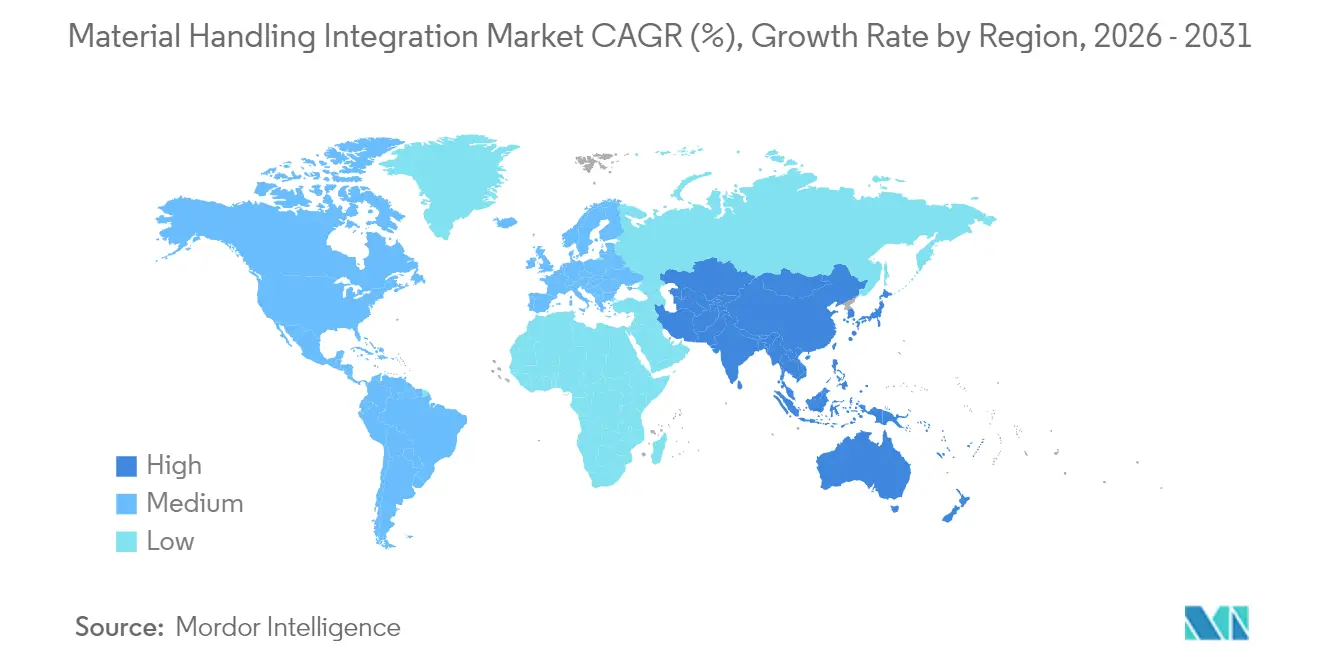

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Material Handling Integration Market Analysis by Mordor Intelligence

Material handling integration market size in 2026 is estimated at USD 53.46 billion, growing from 2025 value of USD 49.62 billion with 2031 projections showing USD 77.61 billion, growing at 7.74% CAGR over 2026-2031. Demand momentum stems from the tight labor pool, which is driving operators toward robotics-centric projects, the steady convergence of operational and information technology stacks, and the proliferation of cyber-secure edge architectures that enable legacy assets to communicate with cloud analytics platforms. North America currently captures the largest revenue share, due to its established e-commerce backbone and early proof points from warehouse digital twins. The Asia Pacific is closing the gap rapidly, thanks to industrial policy support and a growing middle class that is shopping online in higher volumes. Hardware retains the largest share of current spending, while software exhibits the fastest growth rate as value creation shifts toward data-driven orchestration, predictive maintenance, and simulation. On the systems side, conveyors still carry the bulk of parcels, but flexible robotic cells are scaling quickest as fulfillment profiles grow more variable across SKUs.

Key Report Takeaways

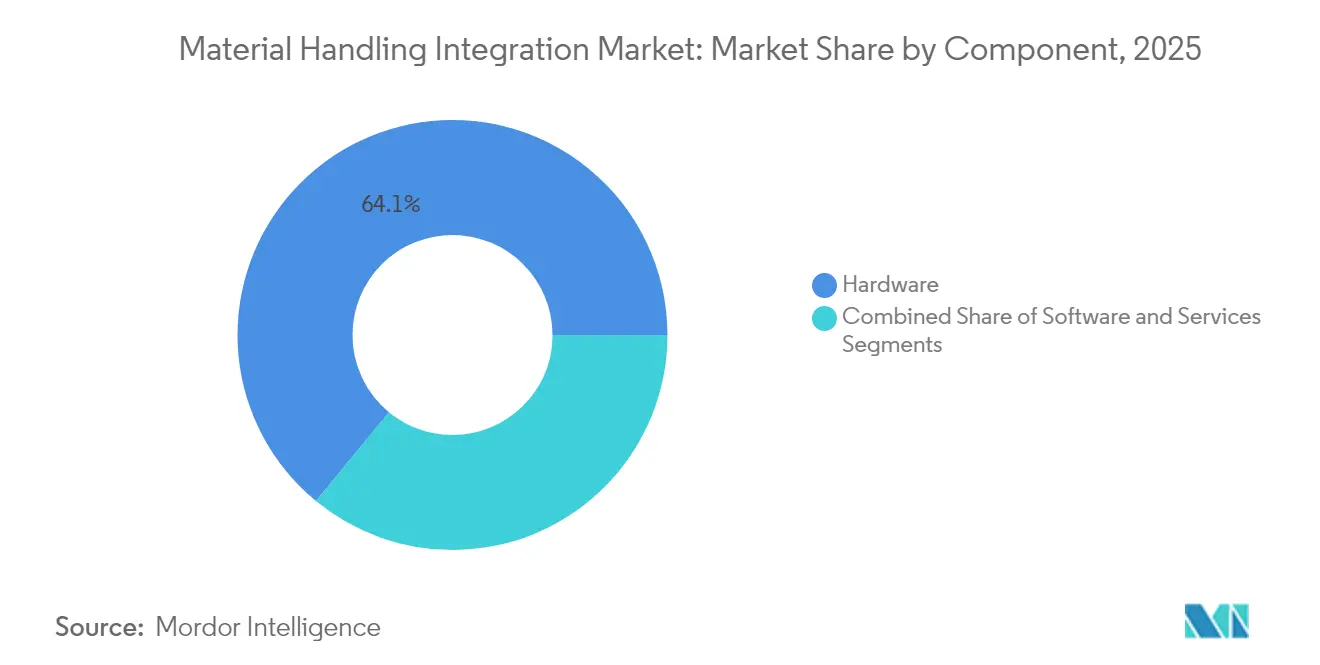

- By component, hardware led with a 64.05% share of the material handling integration market in 2025, while software is expected to advance at a 9.02% CAGR through 2031.

- By system type, conveyors accounted for 30.25% of the 2025 revenue of the material handling integration market, whereas robotic systems are forecast to expand at an 10.55% CAGR to 2031.

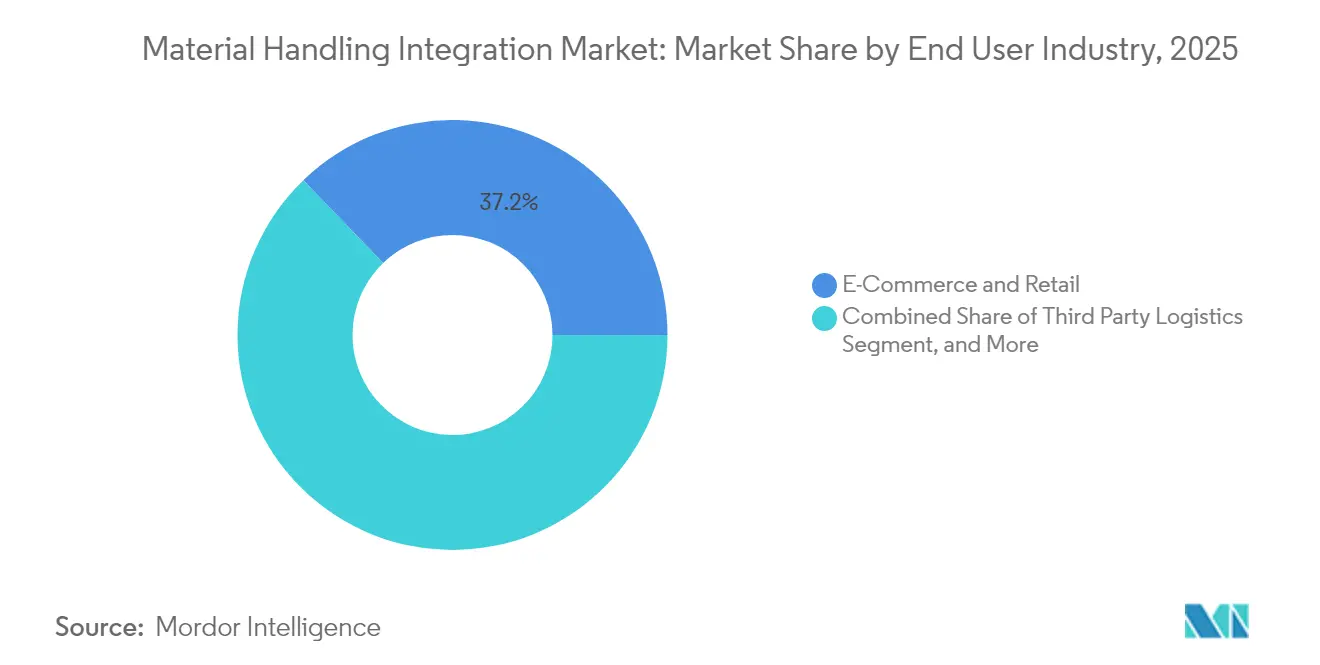

- By end-user industry, e-commerce and retail accounted for 37.20% of the revenue in the material handling integration market in 2025; third-party logistics is the fastest-growing vertical, with a 11.05% CAGR during the outlook.

- By facility size, installations in the 100,000-500,000 square-foot bracket captured 57.35% of the 2025 demand for the material handling integration market, but mega sites above 500,000 square feet are projected to grow at a 9.12% CAGR through 2031.

- By geography, North America accounted for 36.85% of the 2025 revenue in the material handling integration market, while the Asia Pacific is poised to grow at a 9.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Material Handling Integration Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Warehouse-digital-twin adoption accelerating ROI | +1.2% | Global, early gains in North America and Europe | Medium term (2-4 years) |

| OT-IT convergence pushing integrated control platforms | +1.5% | Global, strongest in developed markets | Long term (≥ 4 years) |

| Labor scarcity driving robotics-centric integration | +1.8% | North America and Europe core, spillover to Asia Pacific | Short term (≤ 2 years) |

| Sustainability mandates propelling energy-optimized systems | +0.9% | Europe and North America, expanding to Asia Pacific | Medium term (2-4 years) |

| Cyber-secure edge gateways easing brown-field retrofits | +0.7% | Global, priority in critical-infrastructure regions | Medium term (2-4 years) |

| Rapid pay-as-you-grow SaaS WES models | +1.1% | Global, fastest adoption in emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Warehouse-Digital-Twin Adoption Accelerating ROI

Early adopters of warehouse digital twins have achieved efficiency gains of 15-25% within 18 months, equivalent to annual cost savings of nearly USD 2.3 million for large footprints. The virtual replicas simulate material flow, allowing operators to stress-test integration scenarios before ordering hardware, a shift that is trimming engineering hours and eliminating guesswork in brownfield retrofits.[1]Deloitte, “Digital Twins: The Foundation of the Enterprise Metaverse,” Deloitte.com Inventory-holding costs have decreased by as much as 30% in projects that integrate digital twins with predictive analytics, and order-accuracy levels now exceed 99.5% in benchmark sites. Benefits scale sharply in buildings above 250,000 square feet, where material paths grow complex and simulation delivers disproportionate payback.

OT-IT Convergence Pushing Integrated Control Platforms

Demand for unified control has increased by 40% since 2024, as sites rush to connect programmable logic controllers to cloud-based warehouse management systems.[2]Rockwell Automation, “The Convergence of OT and IT in Manufacturing,” Rockwellautomation.com Seamless data pipelines reduce commissioning time by up to 50% and enable operators to drive closed-loop optimization in real-time. Growth in edge computing is solving latency hurdles, ensuring millisecond response for high-speed sortation while still feeding enterprise analytics in the cloud.

Labor Scarcity Driving Robotics-Centric Integration

Warehouse payrolls rose only 2.1% in 2024, despite a 12% increase in U.S. e-commerce throughput, which widens a talent gap that cannot be closed solely by hiring. Operators are therefore weaving autonomous mobile robots, collaborative palletizers, and AI-based sorters into holistic ecosystems that triple pick rates compared with manual lanes.[3]Amazon Web Services, “Industrial Robotics Solutions,” aws.amazon.com Third-party logistics players experience the largest uplift because they must adapt rapidly to multiple client catalogs.

Sustainability Mandates Propelling Energy-Optimized Systems

Environmental rules and corporate climate pledges are prompting warehouses to adopt energy-efficient material handling systems that reduce utility bills and lower emissions. The European Union now mandates that large companies reduce their energy use by 11.7% by 2030, so operators are favoring equipment that demonstrates clear savings before they sign off on upgrades. Regenerative conveyors that harvest braking energy already trim total facility consumption by 20-30% in live logistics hubs. Smart power software fine-tunes motors and lifts in real-time, allowing buildings to earn demand-response revenue when the grid is strained. Sites that couple these controls with on-site batteries can keep pallets moving during peak-rate windows without pulling from the utility. Together, these steps turn sustainability compliance into a direct operating-cost win.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inter-vendor interoperability gaps | -0.8% | Global, acute in fragmented vendor sets | Medium term (2-4 years) |

| High upfront CAPEX for brown-field facilities | -1.2% | Global, challenging in mature markets | Short term (≤ 2 years) |

| Limited standardization across regional safety codes | -0.5% | Global, varies by jurisdiction | Long term (≥ 4 years) |

| Skilled integrator talent shortages | -0.9% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Inter-Vendor Interoperability Gaps

Material handling projects often stall when equipment from different brands cannot exchange data reliably, pushing integration timelines well beyond initial plans. A recent survey by the Material Handling Industry Association found that 67% of warehouses experienced project delays of more than six months due to control software and field devices using incompatible protocols. Facilities that favor best-of-breed hardware feel this pain most acutely because proprietary standards block real-time coordination across systems. Integrators must then write custom middleware or install protocol translators, both of which add cost and increase long-term maintenance risk. Industry working groups, such as the Industrial Internet Consortium, are promoting common frameworks; however, adoption remains uneven and is slowest in brownfield sites that still run legacy controllers. Until universal standards are established, every multi-vendor rollout will require an additional budget for software bridges and testing.

High Upfront CAPEX for Brown-Field Facilities

Retrofitting an existing warehouse with advanced automation strains capital budgets far more than building a new site from scratch. Reinforcing mezzanines, relocating electrical runs, and re-engineering legacy conveyors inflate project costs and extend payback periods to well beyond the comfort level of many midsized operators. Financing options are available, but lenders often require detailed return-on-investment models that smaller firms struggle to prepare, which can delay approvals and break implementation momentum. Subscription models, such as robotics-as-a-service, promise to shift part of the spend from capital to operating expenses; however, they can include utilization clauses and higher lifetime fees that offset short-term savings. As a result, many brownfield owners still postpone large-scale upgrades until existing assets reach the end of life or competitive pressure becomes impossible to ignore.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Acceleration Reshapes Hardware Dominance

Hardware retained 64.05% of 2025 revenue, underscoring its central role in lifting cartons and pallets. Software, however, records the swiftest climb at a 9.02% CAGR, a trajectory that underscores how analytics, AI routing, and predictive maintenance now set the pace for value creation. The material handling integration market size attached to software grew faster than any other spend category in 2026, a sign that decision-makers view code as the lever for squeezing more throughput from existing conveyors and robots.

Warehouse execution platforms that re-configure task priorities on the fly are gaining favor, especially in e-commerce hubs where order profiles whipsaw hourly. Microsoft reports a 150% jump in sites that anchor their integrations on Azure IoT, signaling a shift toward cloud orchestration and edge decision logic. Services revenue is rising in parallel because operators need lifecycle partners that can integrate, support, and continuously tune those software stacks.

By System Type: Robotics Disrupts Conveyor Supremacy

Conveyors still accounted for 30.25% of global spend in 2025, given their unbeatable cost per case on predictable, high-volume lines. Yet robotic cells, mobile units, and articulated arms are expanding at an 10.55% CAGR to 2031, rapidly eating space once reserved for fixed mechanization. The material handling integration market share tied to robotic systems is expanding as more sites switch from monolithic loops to nimble fleets that reroute instantly when order priorities change.

Adoption rates are especially high in palletizing and depalletizing, where collaborative units can handle mixed SKU layers safely alongside human pickers. Boston Dynamics experienced a 300% surge in warehouse installations last year, with buyers citing quick deployment and lower fit-out requirements as key factors. Sortation, AS/RS, and shuttle technologies continue to carve out roles where storage density and speed take precedence over flexibility.

By End User Industry: Third-Party Logistics Drives Transformation

E-commerce and retail generated 37.20% of 2025 revenue, mirroring consumers’ expectations for two-day or even same-day shipments. Third-party logistics companies, however, are sprinting ahead with an 11.05% CAGR to 2031 because brands increasingly outsource fulfillment to specialists. The material handling integration market size booked by 3PLs is scaling quickly as these firms chase multi-tenant contracts that demand both cost leverage and SKU agility.

The food and beverage, automotive, and pharmaceutical industries maintain steady adoption, albeit with specialized compliance layers. DHL alone earmarked USD 1.2 billion for new automation in 2024. Pharmaceutical logistics introduces serialization, temperature monitoring, and audit-trail requirements that enhance the software’s role in any integration project.

By Facility Size: Mega Facilities Drive Scale Economics

Installations between 100,000 and 500,000 square feet secured 57.35% of 2025 deployments, the sweet spot where automation returns meet capital discipline. The material handling integration market size for mega facilities exceeding 500,000 square feet is nonetheless expanding at a 9.12% CAGR, as organizations concentrate regional inventory in high-throughput hubs.

Amazon’s average new fulfillment center now spans 1.2 million square feet, complete with end-to-end robotics from go-live. Larger footprints promise unparalleled picking capacity, yet integration grows trickier as system counts and data traffic escalate. To bridge the gap, vendors are releasing modular kits and mobile fleets that scale zone by zone inside those cavernous buildings.

Geography Analysis

North America accounted for 36.85% of global revenue in 2025, driven by a mature parcel network, early digital-twin pilots, and high labor costs that favor the adoption of robotics. Growth is steady but slowing, as many tier-one retailers have completed their first-wave automation rollouts, shifting the focus to optimization add-ons and brownfield retrofits.

Asia Pacific is the clear acceleration zone, rising at a 9.88% CAGR through 2031. Government incentives and industrial policy, including China’s USD 1.4 trillion digital infrastructure commitment, are fueling a wave of green-field smart factories that bundle conveyors, AS/RS, and autonomous robots from the outset. E-commerce penetration from India to Southeast Asia is likewise lifting the case for micro-fulfillment nodes that require dense but flexible automation.

Europe maintains solid mid-single-digit growth anchored by sustainability directives that oblige energy-positive buildings. The material handling integration market share held by regenerative systems and smart power controllers is therefore higher in the region than in any other geography. The Middle East and Africa, as well as South America, show emerging pockets of demand tied to large free-trade zones and port expansions, although currency volatility and limited technical talent temper the rollout speed.

Competitive Landscape

The playing field is moderately fragmented. Heavyweights such as Daifuku, KION Group, and Honeywell defend their share with broad portfolios and global service fleets. Software-native integrators and robotics start-ups are nonetheless winning bids where customers want plug-and-play intelligence layered onto older conveyors. M&A activity is brisk as incumbents buy niche robotics or simulation firms to fill capability gaps.

KION’s EUR 800 million acquisition of Element Logic in October 2024 exemplifies the race to control automated micro-fulfillment platforms that slot into urban footprints. Patent filings for edge computing frameworks by Siemens increased by 45% in 2024, underscoring the challenge of securing intellectual property that underpins cyber-secure integrations.[4]United States Patent and Trademark Office, “Patent Search Database,” uspto.gov Vendors are also pivoting to subscription pricing, mirroring the robotics-as-a-service trend that eases customer CAPEX and locks in multiyear revenue for suppliers.

Capacity constraints in skilled integration talent add another layer of complexity. Projects can stall for quarters while customers wait for certified teams that can mesh legacy PLC code with cloud APIs. Firms that package turnkey, cybersecurity-ready stacks are thus gaining premium pricing power even amid intense competition.

Material Handling Integration Industry Leaders

Daifuku Co., Ltd.

KION Group AG

Honeywell International Inc. (Honeywell Intelligrated)

Swisslog Holding AG

Vanderlande Industries B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Vanderlande Industries announced a USD 300 million contract to automate Walmart's new fulfillment network across 15 distribution centers in North America, featuring integrated robotic systems and AI-powered sortation technology. The multi-year project will incorporate next-generation autonomous mobile robots capable of handling 200,000 items per day per facility, with completion expected by 2027.

- September 2025: KION Group completed its USD 450 million acquisition of Locus Robotics, significantly expanding its autonomous mobile robot portfolio and software capabilities. The acquisition provides KION with proven warehouse robotics technology deployed across more than 350 facilities globally, strengthening its position in the rapidly growing collaborative robotics segment.

- August 2025: Honeywell Intelligrated secured a USD 180 million contract to implement comprehensive material handling automation at Amazon's new robotics fulfillment center in Ohio. The installation will feature advanced AI-driven inventory management systems and collaborative robotic arms designed to work alongside human associates in picking operations.

- July 2025: Daifuku announced the opening of its USD 120 million advanced manufacturing facility in Mexico, designed to serve the growing Latin American market for material handling integration solutions. The facility will produce conveyor systems, sortation equipment, and automated storage solutions specifically configured for regional customer requirements.

- June 2025: Swisslog Holding completed a strategic partnership with NVIDIA to develop AI-accelerated warehouse management platforms, combining Swisslog's material handling expertise with NVIDIA's edge computing capabilities. The collaboration will focus on real-time optimization algorithms that can reduce energy consumption by up to 40% in automated facilities.

- May 2025: SSI Schäfer invested USD 85 million in expanding its North American operations, establishing new integration centers in Texas and Georgia to support growing demand for automated storage and retrieval systems. The expansion includes dedicated research facilities focused on developing cyber-secure material handling solutions for critical infrastructure applications.

Global Material Handling Integration Market Report Scope

| Hardware |

| Software |

| Services |

| Conveyor Systems |

| Automated Storage and Retrieval Systems |

| Sortation Systems |

| Robotic Systems |

| Palletising and Depalletising Systems |

| Other System Types |

| E-Commerce and Retail |

| Food and Beverage |

| Automotive |

| Pharmaceuticals |

| Third Party Logistics |

| Other End User Industries |

| Small and Medium Facilities (<100k sq ft) |

| Large Facilities (100k-500k sq ft) |

| Mega Facilities (>500k sq ft) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Singapore | |

| Rest of Asia Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Component | Hardware | |

| Software | ||

| Services | ||

| By System Type | Conveyor Systems | |

| Automated Storage and Retrieval Systems | ||

| Sortation Systems | ||

| Robotic Systems | ||

| Palletising and Depalletising Systems | ||

| Other System Types | ||

| By End User Industry | E-Commerce and Retail | |

| Food and Beverage | ||

| Automotive | ||

| Pharmaceuticals | ||

| Third Party Logistics | ||

| Other End User Industries | ||

| By Facility Size | Small and Medium Facilities (<100k sq ft) | |

| Large Facilities (100k-500k sq ft) | ||

| Mega Facilities (>500k sq ft) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Rest of Asia Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the material handling integration market in 2026?

It reached USD 53.46 billion in 2026, with a 7.74% CAGR forecast to push value to USD 77.61 billion by 2031.

Which region is expanding fastest?

Asia Pacific is projected to grow at a 9.88% CAGR through 2031 due to rapid industrialization and government incentives.

What system type is growing quickest?

Robotic systems show the highest growth at an 10.55% CAGR as firms shift from fixed conveyors to flexible automation.

Why is software demand accelerating?

Data-driven orchestration, predictive maintenance, and cloud analytics make software the fastest-rising component at a 9.02% CAGR.

What is the main barrier to faster adoption?

High upfront CAPEX in brown-field sites raises payback periods to as long as seven years, deterring some mid-market operators.

Page last updated on: