Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

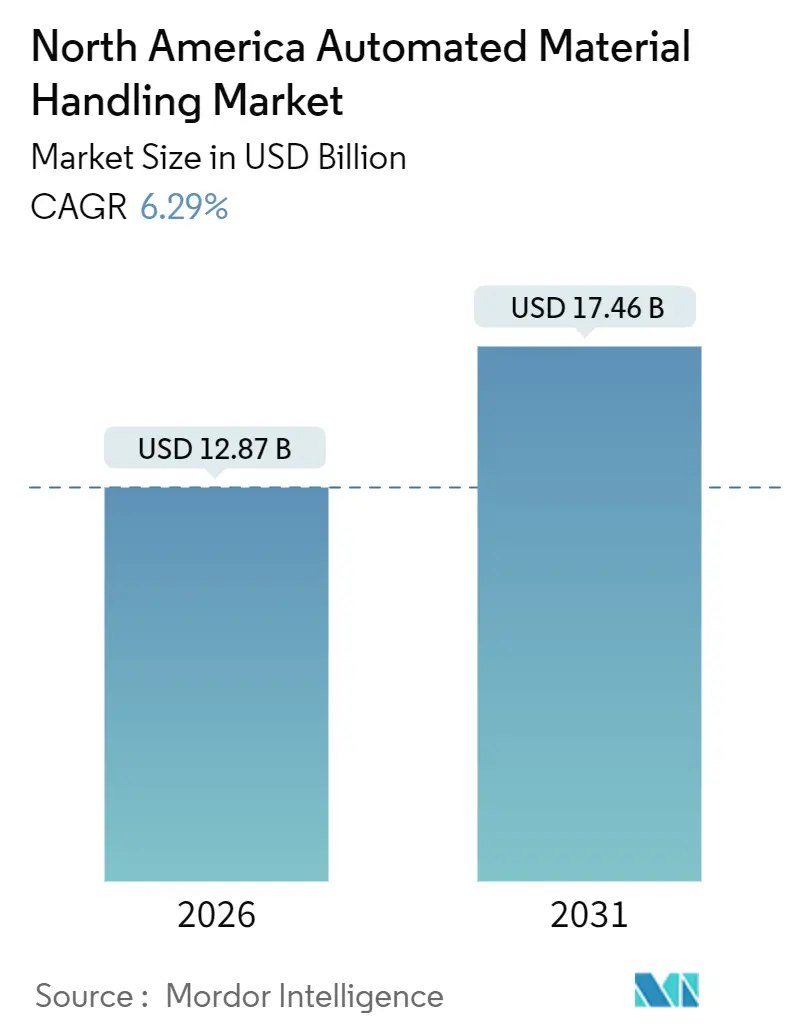

| Base Year Market Size (2025) | USD 12.87 Billion |

| Market Size (2026) | USD 12.87 Billion |

| Market Size (2031) | USD 17.46 Billion |

| Growth Rate (2026 - 2031) | 6.29% CAGR |

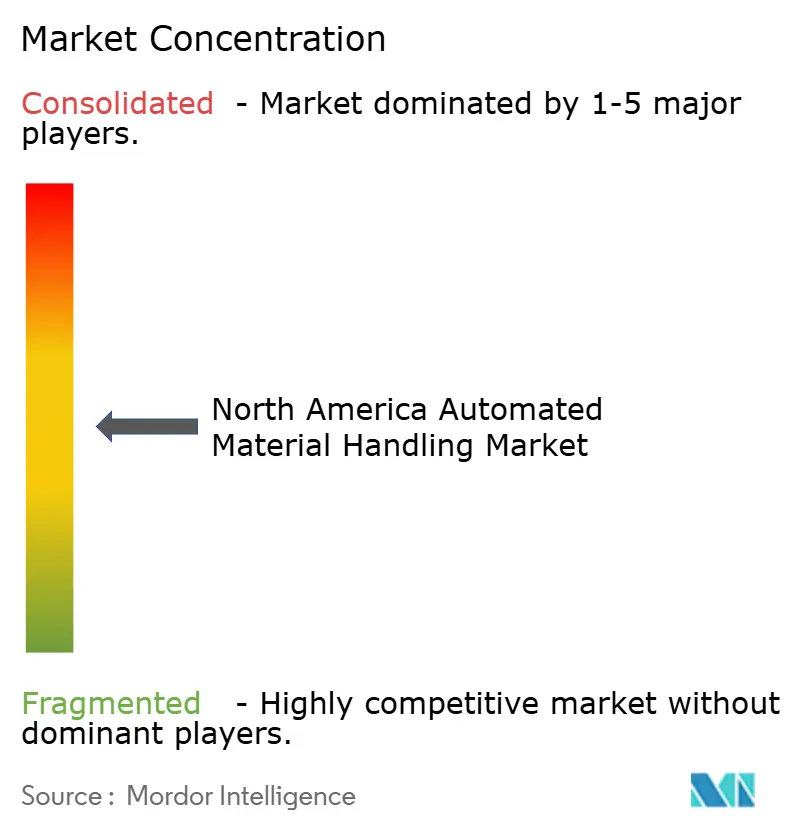

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Automated Material Handling Market Analysis by Mordor Intelligence

The North America automated material handling market reached USD 12.87 billion in 2026 and is forecast to expand to USD 17.46 billion by 2031, translating into a 6.29% CAGR over the period, underscoring the structural shift toward highly automated, software-orchestrated distribution networks. E-commerce penetration, now paired with same-day and next-day delivery expectations, is accelerating adoption of high-throughput equipment and artificial-intelligence-enabled warehouse execution software. Hardware still absorbs most capital outlay, yet intelligence layers have become the decisive differentiator. Autonomous mobile robots, compact shuttle systems, and vision-guided picking solutions are expanding fastest because they retrofit easily into brownfield sites and deliver rapid payback in labor-constrained environments. Investment tax credits in the United States and Canada, combined with acute technician shortages, are driving operators toward turnkey, service-bundled contracts that transfer risk to integrators while raising lifetime system value.

Key Report Takeaways

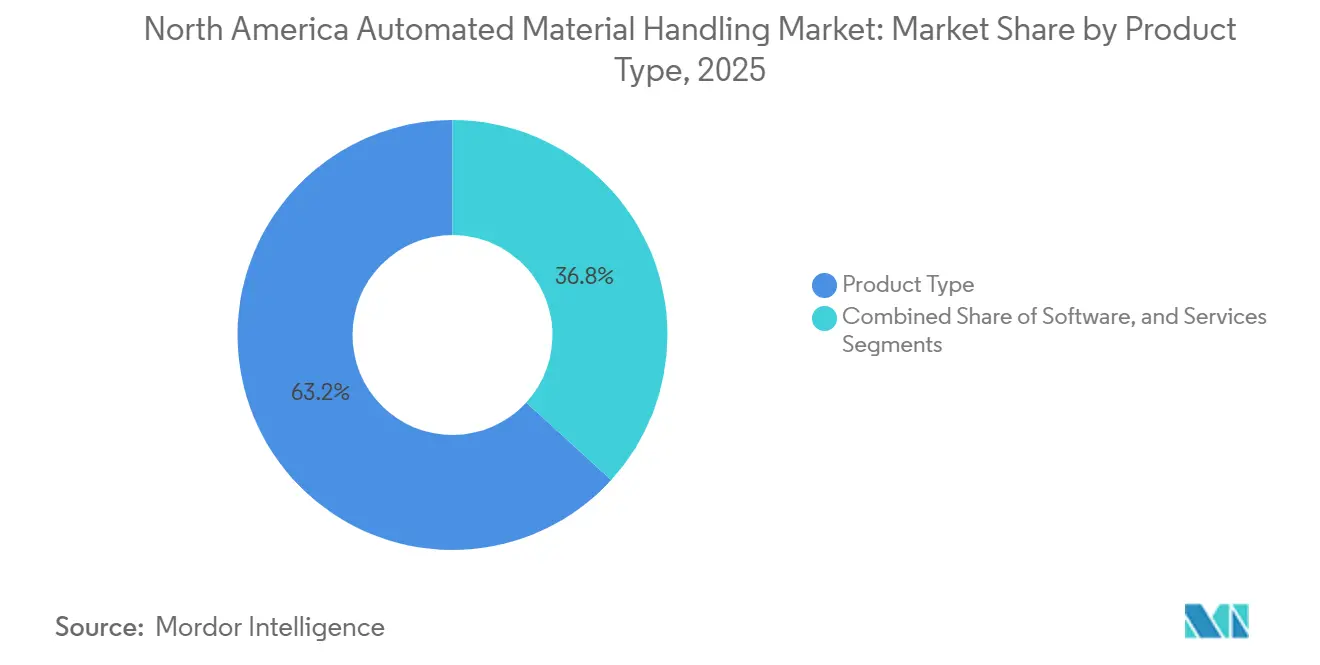

- By product type, hardware led with a 63.21% revenue share in 2025, while software is projected to record the highest growth at a 7.27% CAGR through 2031.

- By equipment type, unit-load AS/RS captured 28.4% of 2025 revenue; autonomous mobile robots are set to expand at a 7.91% CAGR to 2031.

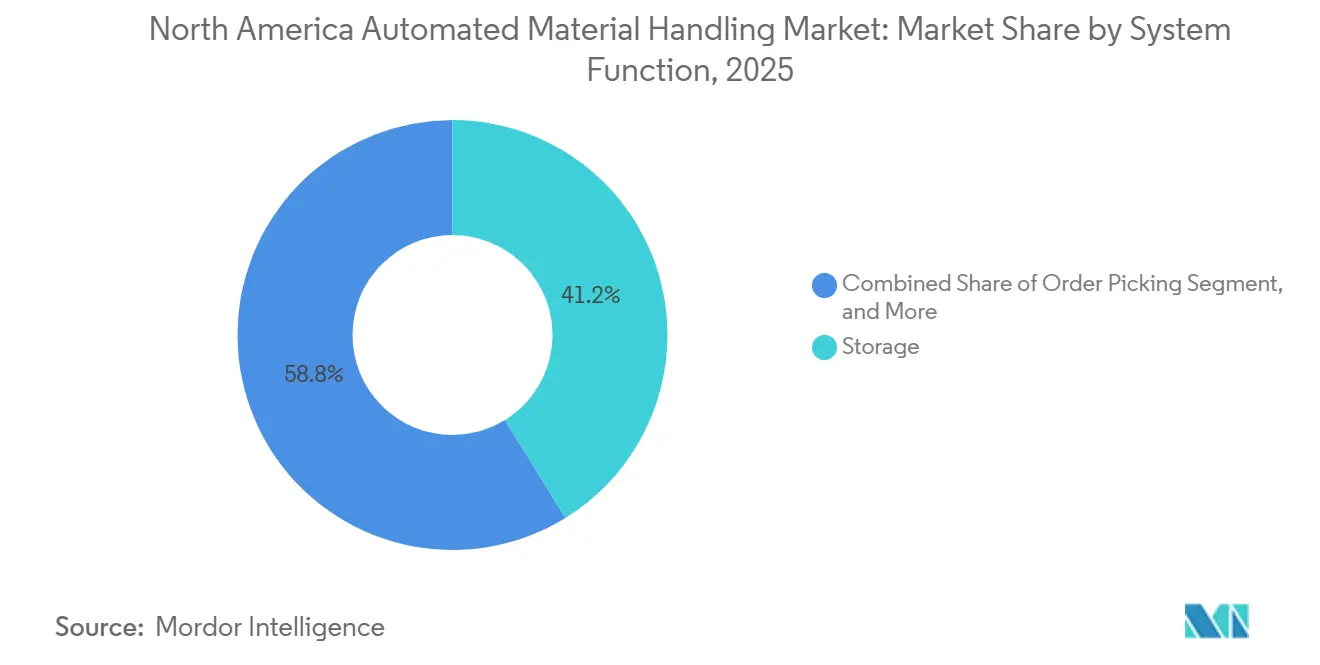

- By system function, storage contributed 41.2% of spending in 2025, whereas order-picking systems will post the fastest rise at a 7.63% CAGR through 2031.

- By end-user vertical, retail, warehousing, and distribution centers dominated with 37.5% share in 2025; e-commerce fulfilment is forecast to grow at a 7.83% CAGR to 2031.

- By country, the United States accounted for 87.9% of 2025 regional revenue, while Canada is projected to advance at an 8.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Automated Material Handling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Warehouse Automation Investments Post-COVID-19 | +1.20% | United States and Canada, concentrated in Midwest and Ontario logistics corridors | Medium term (2-4 years) |

| Rising Adoption of Autonomous Mobile Robots Across 3PL Warehouses | +1.80% | United States, with early density in California, Texas, and New Jersey | Short term (≤ 2 years) |

| E-Commerce Driven Demand for High-Throughput Fulfilment Centers | +2.10% | United States and Canada, urban clusters with population over 1 million | Short term (≤ 2 years) |

| Adoption of AI-Powered Warehouse Execution Systems | +1.40% | United States, led by Fortune 500 retailers and 3PLs | Medium term (2-4 years) |

| Investment Tax Credits and Incentives for Automation in United States and Canada | +0.90% | United States (Section 179, IRA credits) and Canada (SR&ED, SIF) | Long term (≥ 4 years) |

| Sustainability Mandates Driving Energy-Efficient Material Handling Solutions | +0.70% | United States (California, New York) and Canada (British Columbia, Ontario) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Driven Demand for High-Throughput Fulfilment Centers

Parcel volumes in North America surpassed 16 billion units in 2025, pushing retailers and 3PLs to compress order-to-ship cycles below two hours in densely populated cities. Tier-one merchants invested heavily: Amazon operated more than 110 sortation centers and 1,000 delivery stations across the United States in 2025; each designed for peak throughput above one million items per day.[1]Amazon.com, “2025 Annual Report,” amazon.com Walmart earmarked USD 1.4 billion in October 2025 to retrofit 65 distribution centers with AS/RS and robotic palletizers, pursuing same-day delivery coverage for 90% of online orders by 2027.[2]Corporate Walmart, “Supply Chain Investments 2025,” corporate.walmart.com Similar commitments from large chains are cascading to mid-tier operators that now lease space in shared micro-fulfilment hubs equipped with goods-to-person systems, concentrating capital with a handful of integrators.

Rising Adoption of Autonomous Mobile Robots Across 3PL Warehouses

3PLs managed roughly 2.1 billion ft² of warehouse capacity in the United States in 2025, yet only 18% was automated. Robot suppliers seized the opportunity: one leading vendor reported deployments of more than 12,000 collaborative units across facilities run by DHL, GXO Logistics, and Geodis, boosting pick rates by 2.5× over manual methods.[3]Locus Robotics, “Deployment Milestones 2025,” locusrobotics.com Partnerships that integrate fleet management software directly into warehouse management systems have cut commissioning time from six months to as little as eight weeks, accelerating return on investment. Flexibility is paramount because 3PL clients often renegotiate SKUs and volumes every quarter; AMRs, unaffected by fixed guide paths, allow rapid reconfiguration with minimal downtime.

Adoption of AI-Powered Warehouse Execution Systems

Intelligent warehouse execution platforms now optimize task sequencing, resource scheduling, and slotting in real time. A large integrator’s 2025 release embedded predictive analytics that forecast order volumes 48 hours ahead, trimming labour hours per order by 15% in two Fortune 100 pilot sites.[4]Honeywell International, “Momentum WES Launch 2025,” honeywell.com Another vendor’s overnight slotting algorithm improved pick density by 12% in a 500,000 ft² pharmaceutical facility, underscoring the throughput gains available from data-driven orchestration. Software now commands 8%–12% of total project value, establishing a recurring revenue pool that offsets hardware margin compression.

Investment Tax Credits and Incentives for Automation

Section 179 of the Internal Revenue Code lets U.S. businesses expense up to USD 1.16 million in qualifying equipment during 2025, covering most AGV and conveyor projects for mid-sized operators. The Inflation Reduction Act extended accelerated depreciation for energy-efficient equipment, enabling 60% first-year deductions if systems meet Energy Star guidelines. Canada’s SR&ED program disbursed CAD 3.5 billion in 2024, with 9% directed to automation and robotics. Ontario added a 10% Regional Opportunities Investment Tax Credit in January 2025, reducing net capital costs by as much as 35% when stacked with federal incentives. These programs collectively tilt ROI calculations in favour of automation, particularly for operators that historically rented labour rather than capital.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Capital and Integration Costs for Brownfield Sites | -1.30% | United States and Canada, legacy facilities built before 2010 | Short term (≤ 2 years) |

| Shortage of Skilled Technicians for Advanced Automation Maintenance | -0.90% | United States and Canada, acute in secondary markets | Medium term (2-4 years) |

| Cybersecurity Risks in Connected Material Handling Systems | -0.50% | United States and Canada, operators with multi-vendor fleets | Medium term (2-4 years) |

| Building Code and Safety Compliance Complexities in Retrofitting | -0.40% | United States, jurisdictions with stringent seismic or fire codes | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital and Integration Costs for Brownfield Sites

Retrofitting older warehouses typically costs 40%–60% more per square foot than comparable greenfield builds because floors, electrical systems, and HVAC often require upgrades to support 24/7 automation. A 2024 survey of 150 logistics operators found 62% cited integration complexity as the main barrier to adoption. One integrator’s 2024 project at a U.S. automotive parts distributor suffered USD 8 million in cost overruns due to unforeseen structural issues, magnifying investor caution. Lessees face additional risk: landlords frequently decline permanent modifications, leaving tenants liable for decommissioning expenses at lease end.

Shortage of Skilled Technicians for Advanced Automation Maintenance

Demand for industrial machinery mechanics in the United States is projected to climb 13% between 2024 and 2034, yet vocational programs produce only 8,000 certified technicians annually, far below the 15,000 required. Service response times for programmable logic controller repairs rose from 24 hours in 2023 to 38 hours in 2025 at one major integrator, extending downtime for operators in Memphis, Indianapolis, and Columbus. In Canada, 41% of logistics firms reported difficulty hiring staff familiar with industrial networking protocols, prompting integrators to bundle multi-year service contracts that can raise total cost of ownership by up to 18%.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Software Gains as Intelligence Layers Multiply

Hardware commanded 63.21% of 2025 revenue, reflecting the capital intensity of conveyors, AS/RS cranes, and robotic arms, yet software is the fastest-growing component, advancing at 7.27% CAGR as operators chase data-driven throughput gains. Services revenue, tied to installation and long-term maintenance, follows hardware growth but is constrained by the technician shortage. The North America automated material handling market size for software solutions is projected to capture a growing share of expenditures, enabled by modular licensing that allows phased feature activation. In parallel, hardware remains indispensable for new facilities where conveyors and sorters typically consume up to 80% of project budgets, underscoring a dual-track investment pattern that fuses physical capacity with intelligent control.

Second-generation warehouse execution platforms that integrate predictive analytics, digital twins, and fleet orchestration are solidifying recurring revenue streams. One leading supplier reported that software now accounts for 11% of divisional revenue, up from single-digits two years prior, while another’s modular pricing trimmed upfront outlays by 35% yet secured higher lifetime value through annual subscriptions. The North America automated material handling market continues to follow a trajectory where hardware penetrates greenfield sites first, then software increments unlock incremental capacity gains, a pattern mirrored in the rising share of service contracts that embed remote monitoring and preventive maintenance.

By Equipment Type: Autonomous Mobile Robots Disrupt Fixed Infrastructure

Unit-load AS/RS systems held 28.4% of 2025 equipment revenue, demonstrating their enduring appeal for high-throughput environments that prioritize density and pallet-level speed. Nevertheless, autonomous mobile robots represent the fastest-growing category at 7.91% CAGR, driven by their ability to navigate dynamic layouts without fixed guideways. The North America automated material handling market size for AMRs is expanding as brownfield operators seek flexibility that conventional conveyors or AGVs cannot deliver. AGVs maintain relevance in automotive and pharmaceutical settings where predetermined paths and cleanroom requirements prevail, while laser-guided vehicles fill a niche for medium-flexibility applications.

Rising e-commerce parcel volumes and SKU proliferation are tilting purchasing toward robots that can be redeployed quickly as product mixes shift. Leading suppliers now bundle fleet-management software that coordinates tasks across mixed robot brands, easing vendor-lock concerns and fostering multi-fleet strategies. In parallel, fixed infrastructure such as cross-belt sorters remains essential at parcel hubs processing more than 10,000 packages per hour, underscoring that AMRs complement rather than completely displace conveyors in the North America automated material handling market.

By System Function: Order Picking Accelerates as Micro-Fulfilment Scales

Storage functions delivered 41.2% of 2025 value, reflecting the ubiquity of AS/RS and dense racking systems in large distribution centers. Order-picking solutions, however, are set to grow at 7.63% CAGR because micro-fulfilment nodes inside urban zones demand sub-30-minute pick-to-ship cycles. The North America automated material handling market share for order-picking equipment is increasing as retailers deploy goods-to-person technologies that cut walk time, historically 60%-70% of manual pick cycles. Transportation functions, encompassing conveyors and mobile robots that shuttle totes between zones, expand alongside facility footprints, whereas packaging automation gains momentum from sustainability and cost-reduction mandates.

Goods-to-person platforms that combine robotic shuttles with ergonomic workstations now incorporate vision verification that slashes mis-picks by more than 80%, addressing costly returns. Meanwhile, waste-handling automation, though smaller, is growing as corporate sustainability goals force tighter control over recycling streams. Overall, the North America automated material handling market continues to reweight capital toward picking, transportation, and packaging systems that directly influence cycle time, leaving storage investment to scale linearly with facility expansion.

By End-User Vertical: E-Commerce Fulfilment Outpaces Traditional Retail

Retail, warehousing, and distribution centers held 37.5% of 2025 revenue, yet e-commerce fulfilment is advancing fastest at 7.83% CAGR as online penetration rose to 9.02% of U.S. retail sales in late 2025. The North America automated material handling market size allocated to e-commerce operations is expanding because omnichannel merchants and pure-play retailers prioritize speed and accuracy. Automotive distribution remains a significant adopter owing to just-in-time sequencing requirements, though the shift to electric vehicles may reduce parts complexity over time. Food and beverage operators deploy cold-chain automation to counter labour scarcity in refrigerated environments, while pharmaceutical distributors embrace AS/RS for lot-level traceability and temperature monitoring.

Parcel carriers and airport baggage handlers continue to invest in high-speed sortation, but micro-fulfilment centers for last-mile delivery are now the highest-growth subsegment. For general manufacturing, lean-production initiatives spur incremental adoption of AGVs and robotic palletizers that smooth intra-plant material flow. Collectively, diverging growth rates highlight a capital pivot toward sectors with volatile order profiles and stringent delivery windows, reinforcing the strategic importance of software-defined automation.

Geography Analysis

The United States anchors the North America automated material handling market with 87.9% of 2025 revenue, underpinned by vast logistics corridors, pervasive e-commerce, and favourable expensing provisions. Peak parcel volumes now exceed one million units per facility in major hubs, demanding continuous operation of conveyors, sorters, and AMRs. Large retailers retrofitting legacy distribution centers have reshaped capital budgets to emphasize modular, robotics-centric solutions that compress order cycles and curtail labour dependency.

Canada, advancing at 8.22% CAGR to 2031, is riding a wave of federal and provincial incentives that lower net automation costs by up to 35%. Acute technician shortages, cited by 41% of operators, drive demand for long-term service contracts bundled with equipment purchases. While project scale is smaller, the growth runway is longer because automation penetration remains below U.S. levels. Warehouse clusters in Ontario and Quebec benefit from proximity to U.S. manufacturing hubs, facilitating cross-border fulfilment and parts distribution.

Both countries confront integration hurdles in brownfield facilities, where retrofit costs can run 40%-60% above greenfield equivalents. Cybersecurity advisories issued in 2024 and 2025 prompt operators to budget additional resources for network segmentation and software patching, adding complexity to multi-vendor deployments. Overall, geography-specific incentives, labour dynamics, and regulatory landscapes shape distinct yet intertwined paths for the North America automated material handling market.

Competitive Landscape

The market is moderately concentrated: the top five integrators, Dematic, Honeywell Intelligrated, Daifuku, SSI Schaefer, and Bastian Solutions, controlled roughly 45%–50% of 2025 revenue. Competitive advantage hinges on turnkey delivery that bundles hardware, software, and multi-year service. Dematic’s modular software licensing model reduced upfront costs by 35% while securing recurring fees, whereas Honeywell’s Momentum platform trimmed labour per order by 15% through predictive algorithms. Patent filings for vision-guided robotic picking rose 22% between 2024 and 2025, signalling that intellectual property in AI-driven recognition is emerging as a durable moat.

White-space opportunities lie with mid-sized 3PLs managing 500,000–2 million ft² warehouses that require scalable yet cost-effective automation. Smaller specialists such as OPEX and Swisslog win contracts by offering phased, goods-to-person deployments that cap initial investment. Software-centric players coordinate mixed robot fleets, mitigating vendor-lock concerns and fostering ecosystem interoperability. Cold-chain segments, hurt by labour shortages, are adopting robotic palletizers capable of sub-zero operation, drawing interest from food processors and vaccine distributors alike. Consolidation prospects remain high as private equity pursues regional integrators with strong service footprints, epitomized by recent acquisitions executed by Körber Supply Chain.

North America Automated Material Handling Industry Leaders

John Bean Technologies Corporation

Oceaneering International Inc.

Dematic Corp.

Honeywell Intelligrated

Premier Tech Chronos

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Honeywell Intelligrated announced a USD 75 million expansion of its Charlotte, North Carolina manufacturing site, adding 200,000 ft² of capacity to build AMRs and sorters, with completion slated for Q4 2026.

- December 2025: Dematic secured a USD 120 million contract with a leading e-commerce retailer to deploy Multishuttle AS/RS and AI-driven execution software across eight fulfilment centers, targeting Q3 2027 completion.

- November 2025: Daifuku acquired a 60% stake in a Canadian integrator for CAD 85 million (USD 62 million), adding 12 service centers and 180 technicians across Ontario and Quebec.

- October 2025: Walmart committed USD 1.4 billion to retrofit 65 distribution centers with AS/RS, robotic palletizers, and AI-powered execution software, aiming for 30% faster order fulfilment by 2027.

North America Automated Material Handling Market Report Scope

The North America Automated Material Handling Market Report is Segmented by Product Type (Hardware, Software, Services), Equipment Type (Mobile Robots, AS/RS, Conveyors, Palletizers, Sortation Systems), System Function (Storage, Transportation, Packaging, Order Picking, Distribution, Waste Handling), End-User Vertical (Airport, Automotive, Food and Beverage, Retail and Warehousing, Manufacturing, Pharmaceuticals, Parcel, Others), and Geography (United States, Canada). Market Forecasts are Provided in Value (USD).

By Product Type

| Hardware |

| Software |

| Services |

By Equipment Type

| Mobile Robots | Automated Guided Vehicles | Automated Forklift |

| Automated Tow-Tractor | ||

| Unit Load | ||

| Assembly Line | ||

| Special Purpose | ||

| Autonomous Mobile Robots | ||

| Laser Guided Vehicles | ||

| Automated Storage and Retrieval Systems | Fixed Aisle (Stacker Crane + Shuttle) | |

| Carousel (Horizontal + Vertical) | ||

| Vertical Lift Module | ||

| Automated Conveyors | Belt | |

| Roller | ||

| Pallet | ||

| Overhead | ||

| Palletizers | Conventional (High Level + Low Level) | |

| Robotic | ||

| Sortation Systems |

By System Function

| Storage |

| Transportation |

| Packaging |

| Order Picking |

| Distribution |

| Waste Handling |

By End-User Vertical

| Airport |

| Automotive |

| Food and Beverage |

| Retail, Warehousing and Distribution Centers |

| General Manufacturing |

| Pharmaceuticals |

| Post and Parcel |

| Other End-User Verticals |

By Country

| United States |

| Canada |

| Mexico |

| By Product Type | Hardware | ||

| Software | |||

| Services | |||

| By Equipment Type | Mobile Robots | Automated Guided Vehicles | Automated Forklift |

| Automated Tow-Tractor | |||

| Unit Load | |||

| Assembly Line | |||

| Special Purpose | |||

| Autonomous Mobile Robots | |||

| Laser Guided Vehicles | |||

| Automated Storage and Retrieval Systems | Fixed Aisle (Stacker Crane + Shuttle) | ||

| Carousel (Horizontal + Vertical) | |||

| Vertical Lift Module | |||

| Automated Conveyors | Belt | ||

| Roller | |||

| Pallet | |||

| Overhead | |||

| Palletizers | Conventional (High Level + Low Level) | ||

| Robotic | |||

| Sortation Systems | |||

| By System Function | Storage | ||

| Transportation | |||

| Packaging | |||

| Order Picking | |||

| Distribution | |||

| Waste Handling | |||

| By End-User Vertical | Airport | ||

| Automotive | |||

| Food and Beverage | |||

| Retail, Warehousing and Distribution Centers | |||

| General Manufacturing | |||

| Pharmaceuticals | |||

| Post and Parcel | |||

| Other End-User Verticals | |||

| By Country | United States | ||

| Canada | |||

| Mexico | |||

Key Questions Answered in the Report

How fast is the North America automated material handling market growing?

It is projected to rise at a 6.29% CAGR, climbing from USD 12.87 billion in 2026 to USD 17.46 billion by 2031.

Which equipment category is expanding the quickest?

Autonomous mobile robots show the fastest growth at a 7.91% CAGR through 2031 due to flexible deployment in brownfield and micro-fulfillment sites.

Why is software gaining traction in warehouse automation?

Software layers enable real-time task optimization and predictive maintenance, advancing at a 7.27% CAGR and delivering recurring revenue streams for integrators.

What incentives support automation investment in the United States?

Section 179 expensing of up to USD 1.16 million and first-year depreciation of 60% for energy-efficient equipment materially shorten payback periods.

How severe is the technician shortage in North America?

Demand for industrial machinery mechanics outpaces supply by nearly 7,000 technicians annually, extending service response times and driving bundled maintenance contracts.

Page last updated on: