Market Overview

| Study Period | 2020 - 2031 |

|---|---|

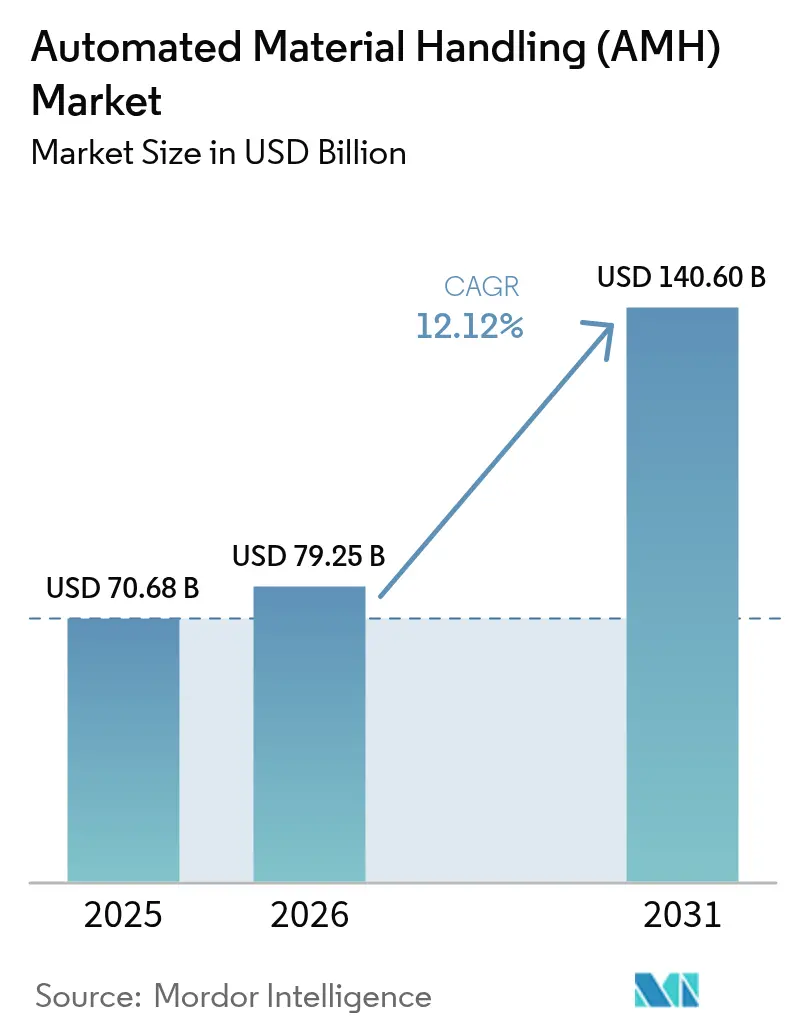

| Market Size (2026) | USD 79.25 Billion |

| Market Size (2031) | USD 140.60 Billion |

| Growth Rate (2026 - 2031) | 12.12% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automated Material Handling (AMH) Market Analysis by Mordor Intelligence

The Automated Material Handling Market size was valued at USD 70.68 billion in 2025 and estimated to grow from USD 79.25 billion in 2026 to reach USD 140.6 billion by 2031, at a CAGR of 12.12% during the forecast period (2026-2031).

Heightened e-commerce fulfillment intensity, Industry 4.0 capex cycles, and labor shortages across OECD logistics hubs have accelerated the shift from manual operations toward intelligent automation. Asia-Pacific dominated with a 46.3% revenue share in 2024 on the back of China’s warehouse-robotics manufacturing strength and Southeast Asian e-commerce growth. Hardware components retained 62.4% market leadership in 2024, yet software solutions expanded fastest at a 19.4% CAGR, underscoring the transition to cloud-based orchestration platforms. Mobile robots, especially Autonomous Mobile Robots, already accounted for 34.2% of equipment revenue in 2024 and are scaling at 27.5% CAGR, signaling a technological inflection toward ai-powered navigation[2].KNAPP AG, “Micro Fulfillment: Automated Solutions for E-Grocery,” knapp.com

Key Report Takeaways

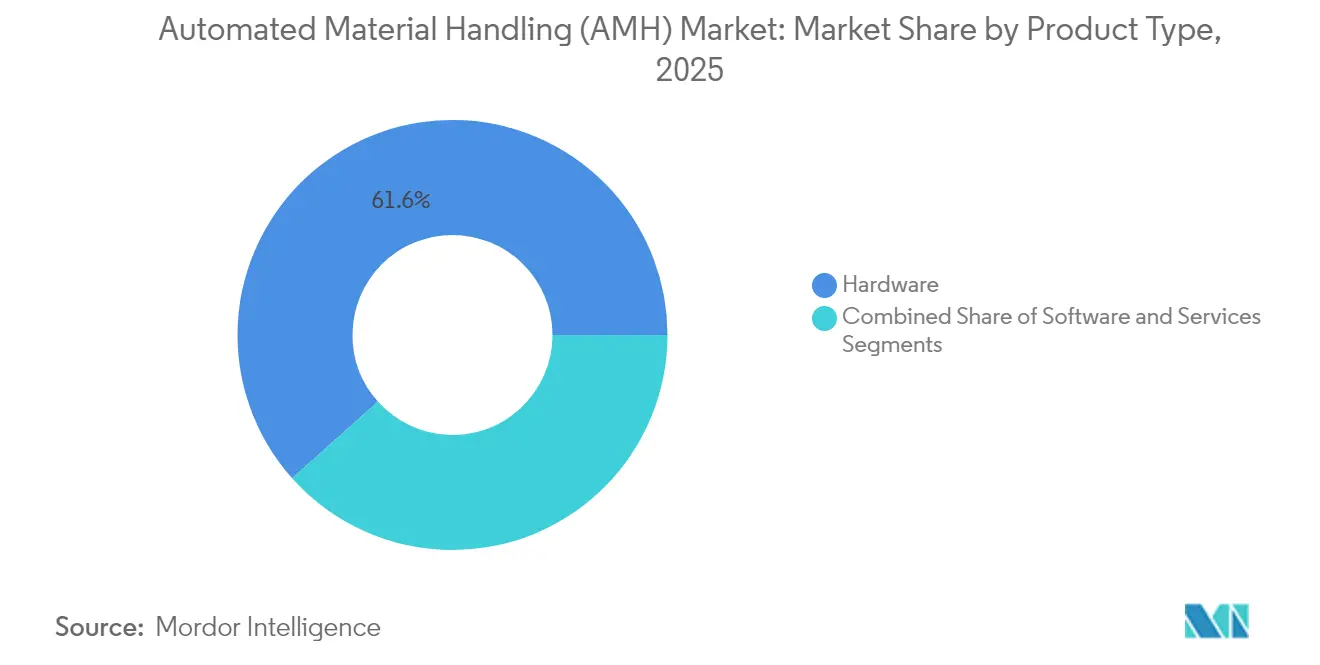

- By product type, hardware led with 61.60% revenue share in 2025; software is forecast to expand at a 18.30% CAGR to 2031.

- By equipment type, mobile robots captured 34.65% of the automated material handling market share in 2025, while Autonomous Mobile Robots are advancing at a 26.20% CAGR through 2031.

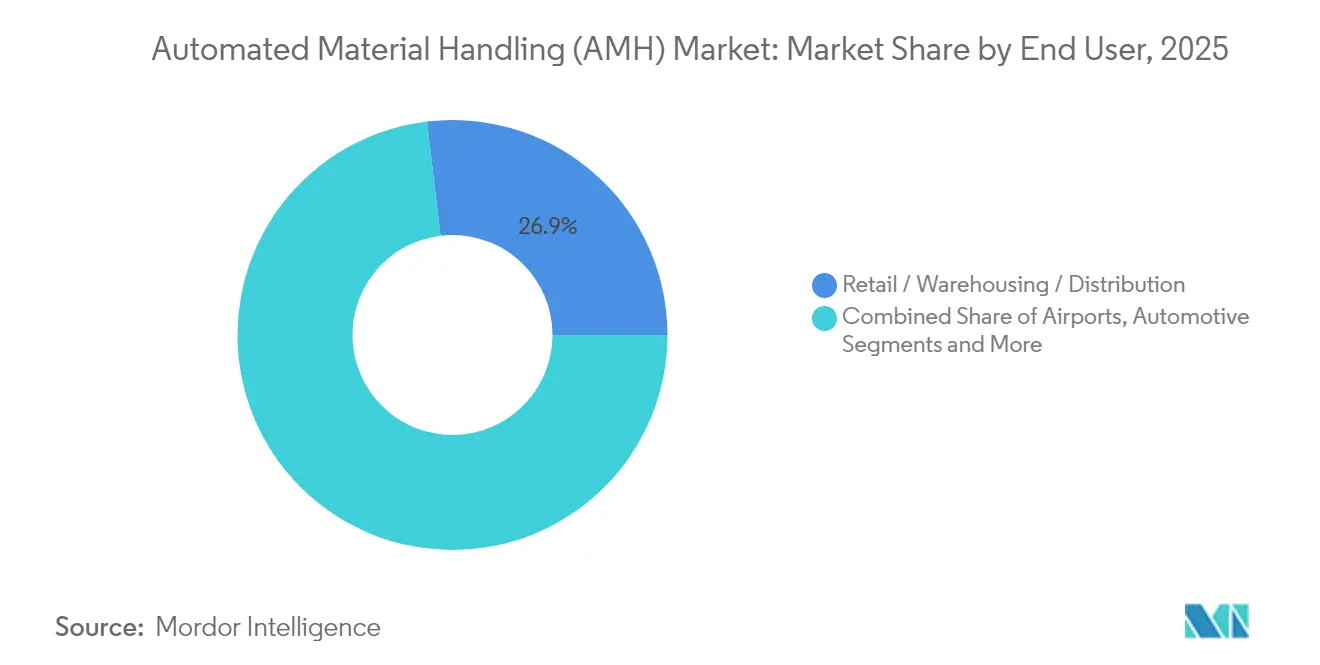

- By end user, retail/warehousing/distribution held 26.90% of 2025 revenue and is projected to grow at 17.40% CAGR through 2031.

- By function, storage held 37.80% of 2025 revenue; picking and placing functions are projected to grow at 23.40% CAGR through 2031.

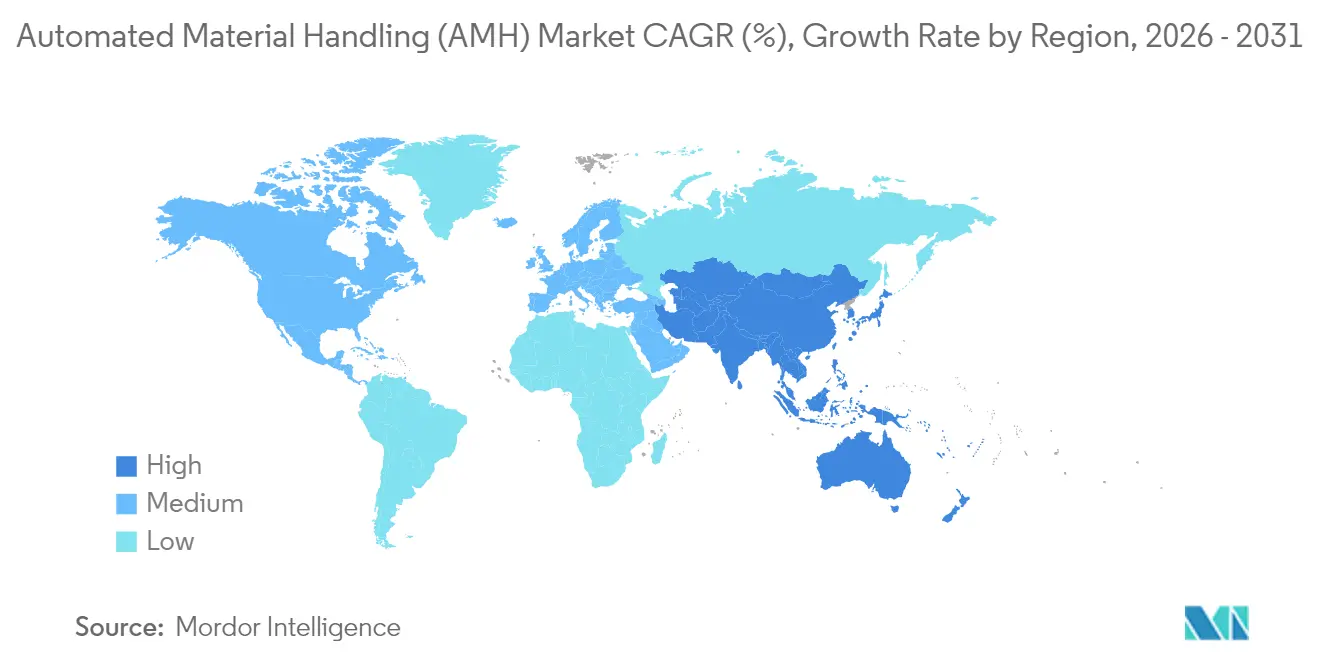

- By geography, Asia-Pacific commanded 45.85% revenue in 2025 and is growing at a 12.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automated Material Handling (AMH) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce fulfillment intensity surge | +2.8% | Global, North America, and Asia-Pacific | Medium term (2-4 years) |

| Industry 4.0-linked capex cycles in brown-field plants | +2.1% | Europe and North America, expanding Asia-Pacific | Long term (≥ 4 years) |

| Labor shortages in OECD logistics hubs | +1.9% | North America, Europe, Japan, Australia | Short term (≤ 2 years) |

| ESG-driven demand for energy-efficient intralogistics | +1.4% | Europe and North America, emerging Asia-Pacific | Medium term (2-4 years) |

| Battery-as-a-Service models for mobile robots | +1.2% | Global, early Europe | Medium term (2-4 years) |

| Micro-fulfilment centre roll-outs | +1.1% | North America and Europe, pilot Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

E-commerce Fulfillment Intensity Surge

Micro-fulfillment centers reshaped order-fulfillment economics, enabling 2-hour delivery windows in spaces as small as 2,000 ft²[1].Locus Robotics, “DHL Supply Chain Expands Partnership and Deploys 5,000 AMRs,” locusrobotics.com Grocery chains using shuttle automation processed 5,000 order lines daily at 99.99% accuracy levels unattainable with manual. The food and beverage sector integrated temperature-controlled automation to satisfy HACCP requirements. Direct-to-consumer models intensified demand for flexible systems able to scale with seasonal SKU spikes, transforming automation from a cost lever into a competitive differentiator. Retailers that automated last-mile nodes secured customer loyalty by meeting delivery promises that traditional warehouses could not sustain.

Industry 4.0-Linked Capex Cycles in Brown-Field Plants.

Manufacturers layered cyber-physical systems onto legacy material-handling assets, creating hybrid workflows that lifted assembly-line efficiency by 33% while cutting labor costs 64%. Digital twin simulations reduced downtime risk and sharpened capital allocation. Pharmaceutical facilities expanded storage capacity 60% while maintaining GMP compliance and temperature integrity through sophisticated brownfield retrofits. The second-wave capex cycle thus focused on interoperability and scalability rather than wholesale equipment replacement, allowing mature plants to unlock Industry 4.0 benefits without dismantling existing flows.

Labor Shortages in OECD Logistics Hubs

Japan’s acute driver shortfall pushed warehouses toward autonomous forklifts priced at JPY 15 million versus JPY 2 million for manual models. Temperature-controlled sites adopted robotics to remove human exposure limits while enhancing safety. European operators observed robotics deployments correlating with lower unemployment rates, indicating job transformation rather than elimination. Skills gaps among automation-literate technicians spawned training partnerships between technology vendors and vocational institutes. Robotics-as-a-Service offerings gained traction by reducing upfront capex and delivering predictable operating expenses.

ESG-Driven Demand for Energy-Efficient Intralogistics

The Corporate Sustainability Reporting Directive compelled firms to factor carbon metrics into automation investments. AutoStore systems consumed 13,600 kWh annually while quadrupling storage density, shrinking facility footprints, and energy bills. Dematic cut greenhouse-gas emissions 14.8% using high-efficiency motors that lowered energy draw by 25%. Solar-integrated warehouses emerged, allowing daylight-hour operations on renewable power. Equipment vendors that are designed for recyclability and circular-economy principles secured a procurement edge.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront integration and retrofit costs | -1.8% | Global; acute in SME segments | Short term (≤ 2 years) |

| Cyber-physical security vulnerabilities | -1.2% | Global; critical infrastructure | Medium term (2-4 years) |

| Scarcity of automation-literate technicians | -1.1% | OECD and developing | Long term (≥ 4 years) |

| Volatile rare-earth and steel prices | -0.9% | Global; China-dependent | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Integration and Retrofit Costs

Comprehensive warehouse automation required USD 2–4 million, a hurdle for mid-market firms. Brownfield sites faced added complexity as operations continued during installation, inflating custom-interface expenses. Robotics-as-a-Service schemes such as BALYO’s reduced capital outlays and promised 30% opex savings under performance-based invoicing. Yet adoption remained cautious due to lock-in fears and higher lifetime costs. Temperature-controlled environments saw capital needs double, prompting SMEs to adopt modular deployments that trade scale for affordability.

Cyber-Physical Security Vulnerabilities

Manufacturing registered more than one-quarter of cyberattacks as interconnected automation increased attack surfaces. Industrial control systems and IoT sensors require continuous monitoring strategies lacking in many organizations. Crown Equipment’s disruption after a cyber incident underscored operational risks. Vendors responded by embedding encryption and network segmentation, yet balancing security with real-time performance remained challenging.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Software Acceleration Outpaces Hardware Dominance

Hardware commanded 61.60% revenue in 2025 as conveyors, AS/RS, and robots anchored capital budgets, while software posted a 18.30% CAGR through 2031. The automated material handling market size for software is projected to climb sharply as AI-based orchestration gains acceptance. Services, though smallest, secured recurring revenue via integration and preventive maintenance contracts that ensured uptime.

The software boom mirrored the automated material handling industry’s pivot toward intelligent decision-making. SaaS delivery allowed continuous updates without hardware swaps. Digital twins linked to warehouse-control software reduced downtime 25% and optimized energy load balancing, enhancing ROI at multinational facilities.

By Equipment Type: Mobile Robots Drive Technological Transformation

Mobile robots captured 34.65% of 2025 equipment revenue, and Autonomous Mobile Robots are accelerating at 26.20% CAGR to 2031. Automated Storage and Retrieval Systems retained share through high-density storage, while conveyors provided ubiquitous material flow.

AMRs’ infrastructure-free navigation lowered deployment time and delivered flexible scaling, exemplified by DHL’s 5,000-unit rollout—the largest AMR project to date. The automated material handling market share held by palletizers and sortation systems grew steadily, thanks to e-commerce volumes, aided by computer-vision upgrades that accommodated SKU shape diversity.

By End User: Retail Dominance with Pharmaceutical Precision

Retail/warehousing and distribution absorbed 26.90% of 2025 spend as omnichannel strategies and same-day delivery promises demanded flexible automation. Automotive facilities combined AMRs and conveyors to shrink parts-movement cycle times, while food and beverage plants integrated HACCP-compliant temperature-controlled systems.

Pharmaceutical warehouses leveraged automated systems to lift storage capacity 60% under GMP requirements, highlighting the automated material handling market size potential in high-value compliance-driven sectors. General manufacturing expanded collaborative-robot use on assembly lines, and airports deployed automated baggage handling that improved throughput and passenger satisfaction.

By Function: Picking and Placing Leads Innovation

Storage retained 37.80% revenue in 2025 as the bedrock of warehouse efficiency, yet picking and placing boasted a 23.40% CAGR to 2031. This functional leap underscored the automated material handling market evolution from static inventory management toward high-velocity order fulfillment.

Robotic picking systems tripled productivity, executing 30 picks per hour versus 9 manually. Transport/tow and sorting maintained relevance, enabling cross-dock efficiency, while packaging and palletizing benefited from cobots that mitigated ergonomic risk in cold-chain environments.

Geography Analysis

Asia-Pacific accounted for 45.85% 2025 revenue and is growing at 12.55% CAGR through 2031, propelled by China’s 52% share of global warehouse-robot output and cross-border e-commerce demand. Regional governments supported automation, illustrated by Daifuku’s new Indian plant and JD Logistics’ high-tech Melbourne hub. Integrated supply chains reduced hardware costs and deployment times, giving local adopters a cost edge.

North America ranked second, featuring large-scale robotics facilities such as Amazon’s 3.5 million ft² Colorado center, hosting 5,000 robots. Walmart’s five high-tech perishable distribution centers doubled throughput while creating 2,000 jobs, demonstrating the region’s brownfield transformation pace. Sustainability mandates spurred energy-efficient retrofits across logistics networks.

Europe’s adoption focused on ESG-compliant solutions and Industry 4.0 convergence. REWE’s Magdeburg facility processed 286,000 packages daily under strict environmental standards, and Dematic’s partnership with Groupe Robert pioneered fully automated cold storage in Quebec, showcasing technology exports. The Corporate Sustainability Reporting Directive drove measurable carbon-reduction targets, encouraging investment in renewable-powered warehouses.

Competitive Landscape

The automated material handling market displayed moderate fragmentation: incumbents Daifuku, Dematic, and Honeywell Intelligrated offered end-to-end systems and global service footprints, while challengers AutoStore and Locus Robotics captured share through cube-storage and AMR platforms, respectively. Competition shifted from pure hardware toward AI-centric software orchestration that optimized multi-robot fleets and predictive maintenance.

Strategic alliances accelerated innovation. Teradyne Robotics’ collaboration with Siemens showcased future-ready automation at MxD Chicago, and Boston Dynamics’ 1,000-robot DHL deal highlighted scale adoption. Humanoid-robot development gained momentum through Foxconn–Nvidia and Jabil–Apptronik partnerships, pointing to long-term disruption prospects.

Patent filings on obstacle recognition and cybersecurity features intensified, positioning IP as a key differentiator. Providers demonstrating robust cyber-physical protection increasingly won contracts among critical-infrastructure clients, integrating encryption and real-time anomaly detection without compromising cycle times.

Automated Material Handling (AMH) Industry Leaders

Daifuku Co. Ltd

Kardex Group

KION Group

JBT Corporation

Jungheinrich AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Foxconn and Nvidia partnered to deploy humanoid robots at a Houston facility slated for Q1 2026 production.

- June 2025: Jabil and Apptronik announced a collaboration to scale Apollo humanoid-robot production.

- June 2025: Synnex unveiled a USD 150 million automated logistics hub in Melbourne, boosting Asia-Pacific capacity.

- May 2025: DHL Group signed an MoU with Boston Dynamics for 1,000 additional robots, extending their 2018 partnership.

Global Automated Material Handling (AMH) Market Report Scope

Automated material handling systems employ computerized devices and robots to handle tasks such as moving, lifting, storing, and retrieving products, replacing traditional human labor. The scope of the study focuses on the market analysis is segmented by product type (hardware, software, and services), equipment type (mobile robots (automated guided vehicle (AGV) and autonomous mobile robot(AMR)), automated storage and retrieval system (fixed aisle, carousel, and vertical lift module), automated conveyor (belt, roller, pallet, and overhead), palletizer (conventional and robotic), and sortation system), end user (airport, automotive, food and beverages, retail/warehousing/distribution centers/logistic centers, general manufacturing, pharmaceuticals, post and parcel, and other end users), and Geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Product Type

| Hardware |

| Software |

| Services |

By Equipment Type

| Mobile Robots | Automated Guided Vehicles (AGV) |

| Autonomous Mobile Robots (AMR) | |

| Automated Storage and Retrieval Systems | Fixed-Aisle |

| Carousel | |

| Vertical Lift Module | |

| Automated Conveyors | Belt |

| Roller | |

| Pallet | |

| Overhead | |

| Palletizers | Conventional |

| Robotic | |

| Sortation Systems |

By End User

| Airports |

| Automotive |

| Food and Beverages |

| Retail / Warehousing / Distribution |

| General Manufacturing |

| Pharmaceuticals |

| Post and Parcel |

| Others |

By Function

| Storage |

| Transport and Tow |

| Picking and Placing |

| Sorting |

| Packaging and Palletising |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Hardware | ||

| Software | |||

| Services | |||

| By Equipment Type | Mobile Robots | Automated Guided Vehicles (AGV) | |

| Autonomous Mobile Robots (AMR) | |||

| Automated Storage and Retrieval Systems | Fixed-Aisle | ||

| Carousel | |||

| Vertical Lift Module | |||

| Automated Conveyors | Belt | ||

| Roller | |||

| Pallet | |||

| Overhead | |||

| Palletizers | Conventional | ||

| Robotic | |||

| Sortation Systems | |||

| By End User | Airports | ||

| Automotive | |||

| Food and Beverages | |||

| Retail / Warehousing / Distribution | |||

| General Manufacturing | |||

| Pharmaceuticals | |||

| Post and Parcel | |||

| Others | |||

| By Function | Storage | ||

| Transport and Tow | |||

| Picking and Placing | |||

| Sorting | |||

| Packaging and Palletising | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is driving rapid growth in the automated material handling market?

Accelerated e-commerce fulfillment, Industry 4.0 investments, and labor shortages collectively pushed the market to a 12.12% CAGR through 2031, with Asia-Pacific leading adoption.

Why are Autonomous Mobile Robots gaining share over Automated Guided Vehicles?

AMRs navigate dynamic environments without fixed infrastructure, enabling faster deployment and a 26.20% CAGR—nearly triple AGV growth.

How are sustainability mandates influencing automation investments?

Regulations such as the Corporate Sustainability Reporting Directive led firms to favor energy-efficient systems like AutoStore’s low-power AS/RS, cutting emissions by double-digit percentages.

Which segment is expanding fastest within the automated material handling industry?

Software solutions, particularly cloud-delivered orchestration and digital twins, are growing at 18.30% CAGR as firms seek optimization beyond hardware.

What barriers hinder mid-market adoption of warehouse automation?

High integration costs of USD 2–4 million and cybersecurity concerns challenge SMEs, though Robotics-as-a-Service models are emerging to ease capital burdens.

Which region offers the strongest expansion prospects beyond Asia-Pacific?

North America, supported by large-scale brownfield retrofits and ESG-driven upgrades, remains the next largest and fast-growing opportunity pool.

Page last updated on: