Flexible Substrate Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

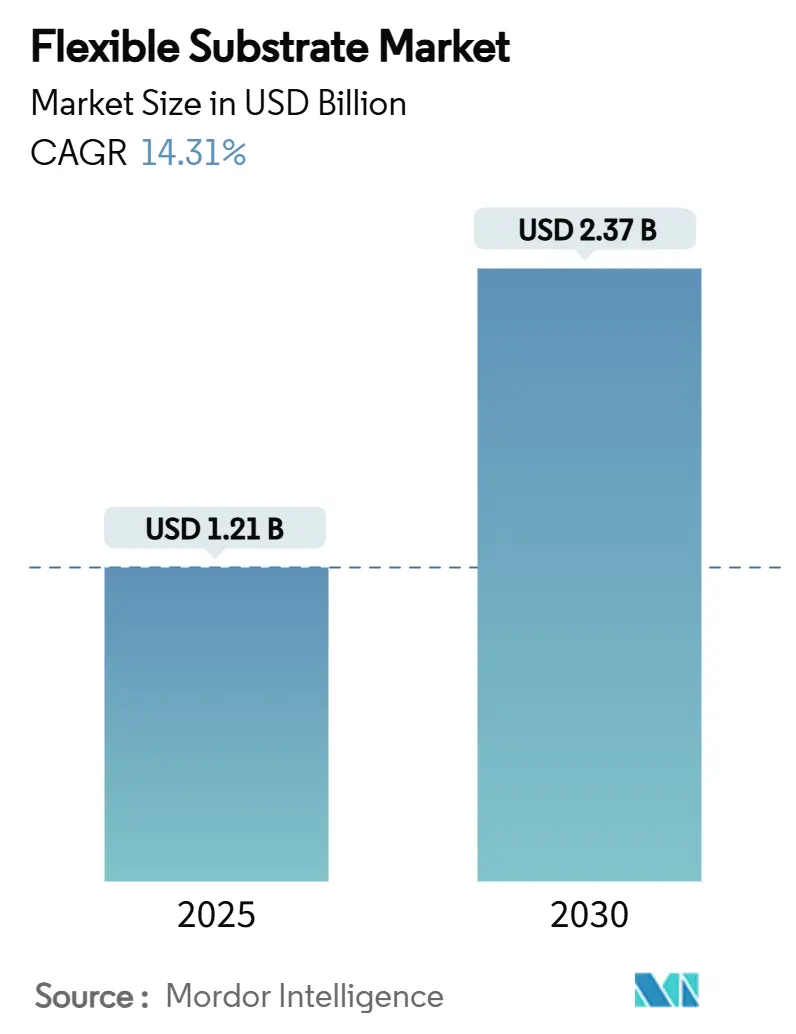

| Market Size (2025) | USD 1.21 Billion |

| Market Size (2030) | USD 2.37 Billion |

| Growth Rate (2025 - 2030) | 14.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Flexible Substrate Market Analysis by Mordor Intelligence

The flexible substrate market size reached USD 1.21 billion in 2025 and is forecast to climb to USD 2.37 billion by 2030, reflecting a 14.31% CAGR over the period. Robust growth stems from accelerating adoption of bendable, foldable and stretchable electronics in smartphones, automotive cockpits and satellite systems, coupled with cost-reducing roll-to-roll (R2R) manufacturing lines and public incentives that localize semiconductor supply chains. Polyimide films, copper conductors and hybrid additive–subtractive processes underpin next-generation circuit architectures, while 5G millimeter-wave modules and low-Earth-orbit (LEO) satellites open lucrative high-frequency niches. Environmental regulations such as the 2024 EPA methylene-chloride ruling press suppliers to adopt greener chemistries that differentiate early movers. Consolidation continues as large material providers spin off focused electronics businesses, intensifying competition around colorless polyimide (CPI) films, LCP laminates and graphene composites.

Key Report Takeaways

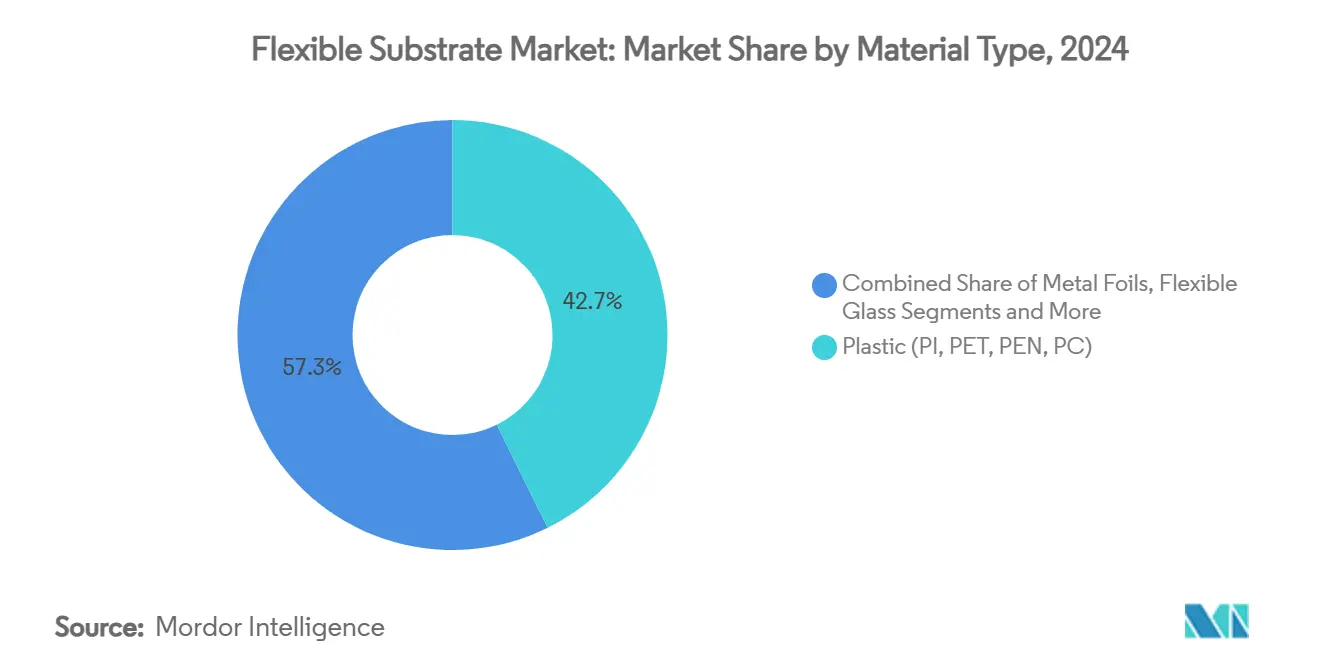

- By material type, polyimide films held 42.7% of flexible substrate market share in 2024; colorless polyimide is expanding at a 16.3% CAGR to 2030.

- By application, flexible displays led with a 38.5% revenue share in 2024, while foldable displays are forecast to advance at a 15.1% CAGR through 2030.

- By end-use industry, consumer electronics accounted for 46.3% of the flexible substrate market size in 2024; healthcare and medical devices are poised for a 15.5% CAGR to 2030.

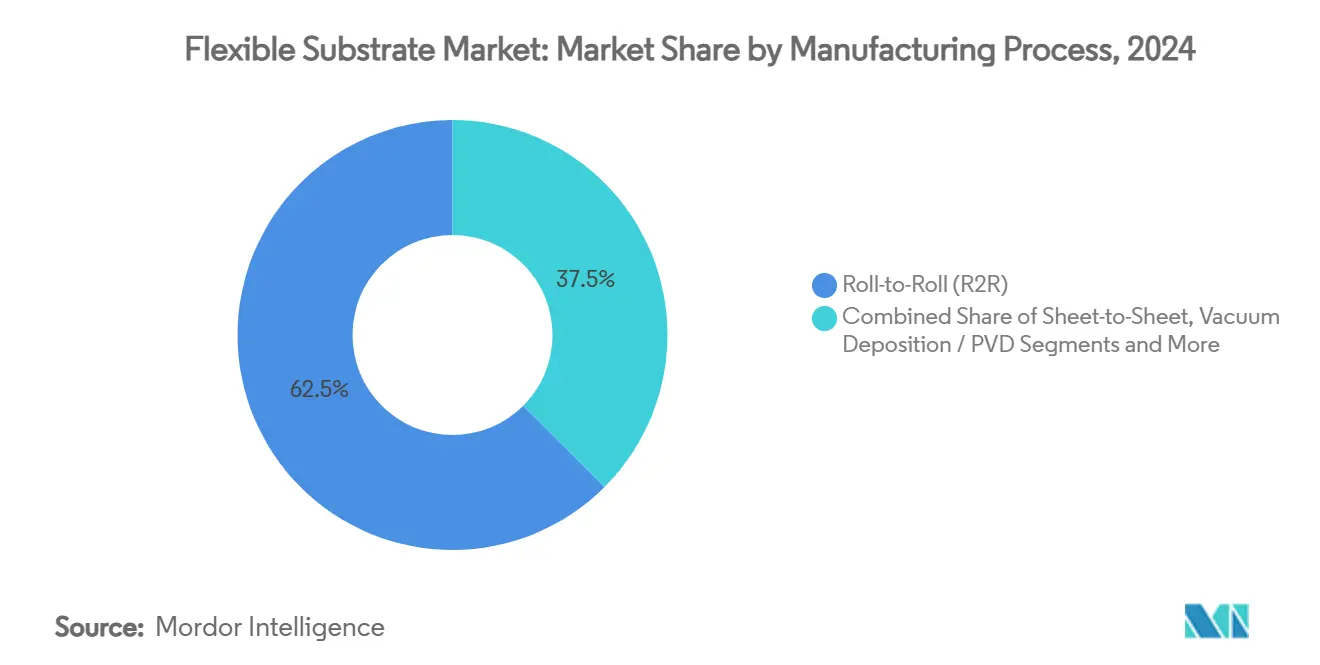

- By manufacturing process, roll-to-roll captured 62.5% share of the flexible substrate market size in 2024, whereas hybrid additive–subtractive processing is set to grow at 16.2% CAGR to 2030.

- By conductive layer, copper-clad laminates commanded 70.3% share in 2024; graphene and carbon-nanotube conductors are registering the fastest 14.9% CAGR through 2030.

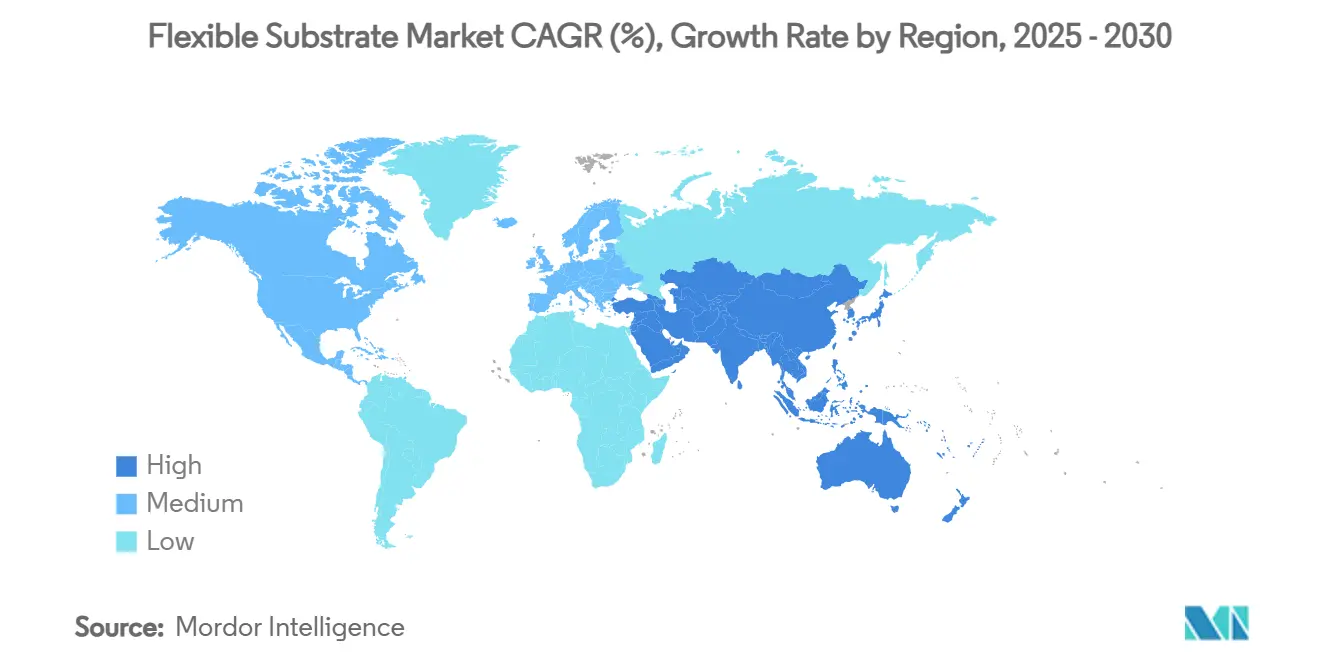

- By geography, Asia Pacific dominated with 54.5% revenue share in 2024 and remains the fastest-growing region at a 14.5% CAGR to 2030.

Global Flexible Substrate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of OLED and foldable displays | +3.2% | Global, with APAC leadership | Medium term (2-4 years) |

| Surge in 5G antenna/RF module demand | +2.8% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Cost-down in roll-to-roll printing lines | +2.1% | Global manufacturing hubs | Long term (≥ 4 years) |

| Government incentives for domestic PCB capacity | +1.9% | US, EU, Japan, Korea | Medium term (2-4 years) |

| Emerging need for substrate-integrated battery layers | +1.7% | APAC core, spill-over to Americas | Long term (≥ 4 years) |

| Space-qualified ultra-thin metal foils for LEO satellites | +1.4% | US, EU, emerging in India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid adoption of OLED and foldable displays

Samsung Display aims for foldables to exceed 50% of premium-smartphone shipments by 2025, pushing demand for colorless polyimide that endures repetitive bending without optical distortion. BOE’s capacity additions are on track to give the firm 26% of global flexible OLED share by 2028, ensuring multi-supplier pull for CPI and copper-clad laminates. Automotive cockpits follow mobile devices, with AUO’s 2025 Smart Cockpit concept integrating Micro-LED sunroof panels that rest on ultra-thin substrates.[1]BHTC, “AUO Opens New Chapter in Mobility at CES with Trailblazing Smart Cockpit 2025,” bhtc.com Local sourcing strategies add complexity: Samsung is qualifying SKC CPI films to cut reliance on Japanese imports. Together, these trends solidify display-driven momentum for the flexible substrate market.

Surge in 5G antenna/RF module demand

Millimeter-wave radios above 28 GHz require substrates with low dielectric loss; DuPont’s Pyralux AP polyimide rivals costlier liquid-crystal-polymer (LCP) laminates up to 60 GHz. Graphene-clad flexible PCBs show comparable performance to copper while improving bend radius for wearable antennas. Rogers Corporation’s CLTE-MW sheets exhibit a 0.0015 loss tangent at 10 GHz, supporting automotive radar. Stretchable PDMS-based antennas maintain signal integrity from 0.99 to 9.41 GHz, broadening IoT use cases. Process engineers therefore refine impedance control methods that keep insertion loss within tight budgets even under flex.

Cost-down in roll-to-roll printing lines

Continuous R2R printing can trim manufacturing cost by 50% against batch photolithography, provided overlay accuracy reaches sub-micron thresholds. The NREL multilab program demonstrates energy-efficient R2R coating for batteries and photovoltaics, cutting waste and cycle time. [2]NREL, “Roll-to-Roll Manufacturing Multilab Collaboration,” nrel.govReverse-offset printing coupled with photonic sintering delivers 9.86 Ω/sq transparent electrodes at 90% transmittance, enabling flexible OLED lines. Machine-vision alignment maintains <100 µm registration at 5 m/min web speed, critical for multilayer circuits. Green electricity sourcing further lowers operating costs and improves ESG scores, reinforcing long-term adoption of R2R platforms.

Government incentives for domestic PCB capacity

The US CHIPS Act earmarks USD 1.6 billion for advanced packaging, with USD 300 million directed to substrate materials research. Treasury regulations extend a 25% investment credit to substrate equipment, directly offsetting capex. Korea’s 2024 plan supplies KRW 150 trillion in low-interest loans and broader tax breaks to bolster domestic substrate sites. European energy-transition funds, such as Sweden-based Midsummer’s 200 MW CIGS facility, illustrate how green-tech subsidies also create substrate pull for thin-film photovoltaics. Policy incentives thus reduce overseas dependency and accelerate local capacity ramps.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in PI and LCP precursor prices | -2.3% | Global, acute in specialty chemicals | Short term (≤ 2 years) |

| Stringent clean-room humidity specs | -1.8% | Global manufacturing hubs | Medium term (2-4 years) |

| Recycling challenges for multi-layer laminates | -1.2% | EU regulatory focus, expanding globally | Long term (≥ 4 years) |

| Limited high-frequency test standards <110 GHz | -0.9% | Advanced markets (US, EU, Japan) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in PI and LCP precursor prices

Closure of large propylene refineries has pushed US polymer-grade propylene above 40 ¢/lb, inflating imide monomer costs and squeezing substrate margins. Trade frictions intensify swings, exemplified by Samsung Display’s drive to diversify CPI sources away from Japanese suppliers. Frequent price renegotiations destabilize annual contract models, forcing producers to absorb short-term shocks or hedge feedstock exposure. Development of bio-based or recycled imides promises smoother cost curves, yet qualification cycles remain lengthy. Until supply balances, the flexible substrate market must contend with margin compression.

Stringent clean-room humidity specs

ISO 6–8 clean-rooms now demand <1% relative humidity during key PI coating and copper etch steps, raising HVAC energy loads that already account for up to 60% of fab operating costs. [3]AFRY FDA, “Clean Room Atmosphere Requirements for Battery Production,” afry.comrecognition of ISO 14644-4 tightens compliance for medical-grade substrates. Semiconductor NESHAP regulations add monitoring and abatement hardware capital outlays. Smaller firms struggle to fund upgrades, prompting industry consolidation or contract manufacturing partnerships. Innovations in desiccant wheel dehumidification and closed-loop solvent recovery cut utility bills but require upfront investment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Polyimide Films Drive Innovation

Plastics include Polyimide films held 42.7% of flexible substrate market share in 2024, reflecting unmatched thermal stability that prevents copper delamination during high-temperature reflow. Colorless polyimide posted a 16.3% CAGR and enables foldable screens that require optical transmission above 90% without yellow tint. Hybrid fluorinated backbones further raise glass-transition temperatures to 360 °C, supporting next-generation LEO satellites. Metal foils such as 12 µm copper remain essential for heat-spreading layers in RF modules, while flexible glass addresses scratch-resistant wearables.

Paper and cellulose substrates serve low-cost, disposable RFID tags where biodegradability trumps performance. Graphene-assisted laser lift-off now achieves 2.9 µm CPI webs that cut device profile by 30%. Liquid-crystal-polymer (LCP) films gain share in 77 GHz automotive radar because of dielectric constants near 3 and stability up to 250 °C. Collectively, these advances broaden material choice while reinforcing the dominance of advanced polyimides within the flexible substrate market.

By Application: Flexible Displays Lead Market Transformation

Flexible displays captured 38.5% revenue in 2024 on the back of smartphone and automotive demand. Foldable panels alone are growing 15.1% CAGR to 2030 as brands plan dual-fold, rollable and slidable form factors. Printed stretchable sensors track biometrics from skin-mounted patches, driving medical substrate volumes. Lightweight photovoltaics leverage CPI frontsheets that replace glass and eliminate 700 g/m² from module weight.

RFID and antenna substrates must retain impedance across bends; PDMS composites now span 0.99–9.41 GHz for IoT wearables. Solid-state lighting modules exploit flex to conform to curved interiors, expanding architectural options. As such, display and sensor innovations cement their role as prime revenue pillars for the flexible substrate market.

By End-Use Industry: Consumer Electronics Dominance Challenged

Consumer electronics commanded 46.3% of the flexible substrate market in 2024, buoyed by smartphones, tablets and notebooks. Healthcare is, however, accelerating at 15.5% CAGR, propelled by implantable bioelectronics that demand biocompatible conductors and elastomeric encapsulants. Automotive electrification needs flexible circuits for battery management systems and panoramic cockpit displays.

Energy applications span building-integrated photovoltaics and thin-film batteries on steel roofs, while aerospace seeks radiation-resistant copper-polyimide foils for LEO constellations. The printed electronics market in mobility rose from USD 421 million in 2024 and could reach USD 960 million by 2034, reinforcing transportation’s pull on substrate suppliers.

By Manufacturing Process: Roll-to-Roll Supremacy

Roll-to-roll processes dominated with 62.5% of flexible substrate market size in 2024 thanks to superior throughput and 50% lower unit cost relative to batch etching. The hybrid additive–subtractive method, growing at 16.2% CAGR, deposits copper by inkjet then lasers away over-spray for ≤15 µm lines. Sheet-to-sheet remains vital for aerospace and medical devices that require micron-level tolerances.

Vacuum deposition targets high-purity metal oxide barriers for moisture-sensitive OLED stacks, while ambient printing of native oxides removes capital-heavy vacuum chambers altogether. Machine-learning control systems cut defectivity by 40% on R2R webs, highlighting digitalization as a lever for yield and sustainability in the flexible substrate market.

By Conductive Layer Type: Copper Dominance Faces Innovation

Copper-clad laminates provided 70.3% share in 2024 due to unmatched conductivity and cost-effective plating lines. Yet graphene and carbon-nanotube films post a 14.9% CAGR, bringing sheet resistance below 20 Ω/sq at 90% transparency for touch sensors. Silver-nanowire meshes enable transparent electrodes, though price volatility of precious metals prompts research into copper-nanowire films with oxidation-resistant coatings.

Conductive polymers prove attractive where skin contact requires metal-free circuitry. Self-healing elastomer-copper hybrids now recover 95% conductivity after 1,000 bend cycles, improving device lifespan. As innovation accelerates, copper retains dominance but faces credible challenges that will diversify material sourcing in the flexible substrate market.

Geography Analysis

Asia Pacific led with 54.5% revenue in 2024 and sustains the fastest 14.5% CAGR to 2030 as governments prioritize semiconductor sovereignty and display capacity. Taiwan’s Unimicron, Kinsus and Nan Ya PCB regained double-digit growth once AI-server demand cleared ABF substrate bottlenecks. China is on course to command 74% of global display production by 2028, feeding substrate orders for BOE, CSOT and Tianma.

North America benefits from CHIPS-backed subsidy flows that fund advanced-packaging lines and encourage reshoring of R2R pilot plants. SEMI projects 300 mm fab-equipment spending in the region to double from USD 12 billion in 2024 to USD 24.7 billion by 2027, lifting demand for high-frequency polyimide substrates. [4]SEMI, “300 mm Fab Equipment Spending Forecast,” semi.orgEurope pushes sustainability leadership; Saica Flex’s target of 100% recyclable flexible packaging exemplifies regulatory pull for substrates with circular end-of-life options.

Manufacturing diversification is evident as Kinsus explores Malaysian capacity to hedge geopolitical risk. Middle East and Africa remain nascent but attract pilot photovoltaic substrate projects leveraging abundant solar resources. Overall, regional dynamics underline the need for agile supply strategies within the flexible substrate market.

Competitive Landscape

The flexible substrate market remains moderately fragmented, yet consolidation progresses as large chemical groups carve out dedicated electronics units. DuPont’s planned Qnity spin-off, slated for completion in November 2025, positions a 10,000-strong entity focused on CPI films, silver nanowires and Pyralux laminates. Partnerships deepen technology moats; DuPont and Zhen Ding Technology signed a pact to co-develop high-end PCBs for AI accelerators. Hyundai Motor Group allies with Toray to apply carbon-fiber-reinforced polymers for EV chassis electronics, broadening automotive substrate demand.

White-space innovation flourishes among academic spin-outs; MIT created light-cured recyclable substrates processed at room temperature, addressing e-waste concerns. Patent filings concentrate on CPI fluorination, laser-assisted delamination and graphene-copper hybrid films. Sustainability drives differentiation as EPA methylene-chloride limits spur solvent-free coating lines. Strategic moves in 2025—from LG Chem’s nano-silver pastes to LG Innotek’s glass-substrate pilot—underscore an industry racing to secure footholds in high-value niches.

Flexible Substrate Industry Leaders

-

DuPont

-

Kaneka Corporation

-

Kolon Industries

-

Corning Inc.

-

Teijin Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Top Bright announced mass production of HVLP5+ copper foil in Q4 2025, supporting new materials growth.

- June 2025: LG Chem partnered with Noritake to produce nano-silver paste for automotive power semiconductors.

- May 2025: DuPont unveiled Qnity as the future electronics spin-off brand serving semiconductor customers.

- April 2025: LG Innotek disclosed plans to sample glass substrates by end-2025, diversifying beyond camera modules.

Global Flexible Substrate Market Report Scope

| Plastic (PI, PET, PEN, PC) |

| Metal Foils (Cu, Al, SS) |

| Flexible Glass |

| Paper and Cellulose |

| Flexible Displays |

| Printed and Stretchable Sensors |

| Photovoltaics / Flexible Solar Cells |

| RFIDs and Antennas |

| Solid-state Lighting and E-paper |

| Consumer Electronics |

| Automotive and Transportation |

| Healthcare / Medical Devices |

| Energy and Power |

| Aerospace and Defense |

| Roll-to-Roll (R2R) |

| Sheet-to-Sheet (S2S) |

| Vacuum Deposition / PVD |

| Hybrid Additive-Subtractive |

| Copper Clad |

| Silver Nanowire |

| Graphene and CNT |

| Conductive Polymers |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Material Type | Plastic (PI, PET, PEN, PC) | ||

| Metal Foils (Cu, Al, SS) | |||

| Flexible Glass | |||

| Paper and Cellulose | |||

| By Application | Flexible Displays | ||

| Printed and Stretchable Sensors | |||

| Photovoltaics / Flexible Solar Cells | |||

| RFIDs and Antennas | |||

| Solid-state Lighting and E-paper | |||

| By End-Use Industry | Consumer Electronics | ||

| Automotive and Transportation | |||

| Healthcare / Medical Devices | |||

| Energy and Power | |||

| Aerospace and Defense | |||

| By Manufacturing Process | Roll-to-Roll (R2R) | ||

| Sheet-to-Sheet (S2S) | |||

| Vacuum Deposition / PVD | |||

| Hybrid Additive-Subtractive | |||

| By Conductive Layer Type | Copper Clad | ||

| Silver Nanowire | |||

| Graphene and CNT | |||

| Conductive Polymers | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the flexible substrate market?

The flexible substrate market reached USD 1.21 billion in 2025 and is projected to grow rapidly through 2030.

Which region leads the flexible substrate market?

Asia Pacific accounted for 54.5% of global revenue in 2024 and is the fastest-growing region at a 14.5% CAGR.

Which material holds the largest share in flexible substrates?

Polyimide films dominated with 42.7% market share in 2024 due to their high thermal stability and compatibility with copper conductors.

What segment is growing fastest within applications?

Foldable displays are the fastest-growing application, advancing at a 15.1% CAGR to 2030.

How does roll-to-roll processing benefit manufacturers?

Roll-to-roll lines can cut manufacturing costs by up to 50% while enabling high-volume production of multilayer flexible circuits.

What are the main restraints affecting market growth?

Volatile precursor pricing, stringent clean-room humidity specifications, recycling challenges for laminates and limited ultra-high-frequency test standards collectively moderate growth.

Page last updated on: