Market Overview

| Study Period | 2023 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

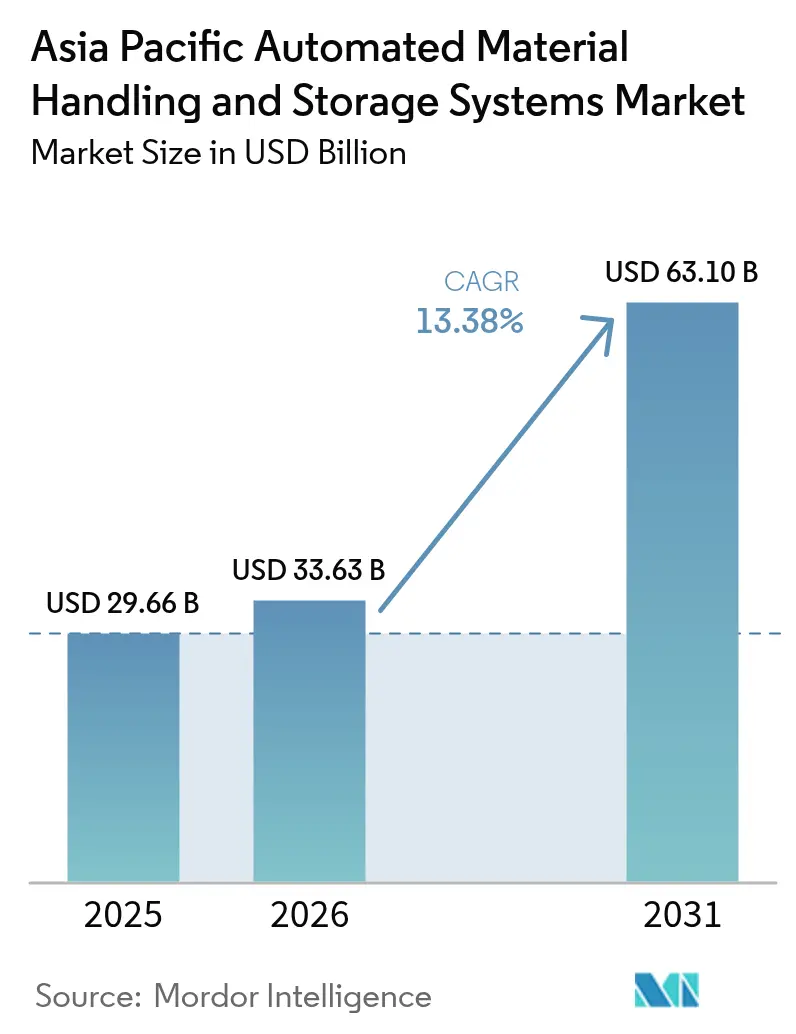

| Base Year Market Size (2025) | USD 29.66 Billion |

| Market Size (2026) | USD 33.63 Billion |

| Market Size (2031) | USD 63.1 Billion |

| Growth Rate (2026 - 2031) | 13.38% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia Pacific Automated Material Handling And Storage Systems Market Analysis by Mordor Intelligence

The Asia Pacific automated material handling and storage systems market size in 2026 is estimated at USD 33.63 billion, growing from 2025 value of USD 29.66 billion with 2031 projections showing USD 63.1 billion, growing at 13.38% CAGR over 2026-2031. Strong policy backing for smart-factory rollouts, widespread 5G industrial IoT deployments, and the rapid build-out of e-commerce fulfilment hubs across tier-2 cities collectively propel the Asia Pacific automated material handling and storage systems market. China anchors demand with a 42.1% 2024 revenue share, while India leads growth at a 15.05% CAGR as Production Linked Incentive schemes accelerate automation investments. Hardware retains leadership at 64% share, yet the software layer is scaling quickly at a 14.52% CAGR as factories prioritize data-driven optimization. Mobile robots already account for 28.3% of equipment deployments, and autonomous mobile robots (AMR) are advancing at 15.11% CAGR as operators favour layout flexibility over fixed infrastructure.[1]AutoStore, “Corporate Overview,” autostore.com

Key Report Takeaways

- By product type, hardware commanded 63.42% of the Asia Pacific automated material handling and storage systems market share in 2025; software solutions are projected to expand at a 14.12% CAGR through 2031.

- By equipment type, AMR deployments represented 27.92% of the Asia Pacific automated material handling and storage systems market size in 2025 and are forecast to grow at a 14.78% CAGR between 2026-2031.

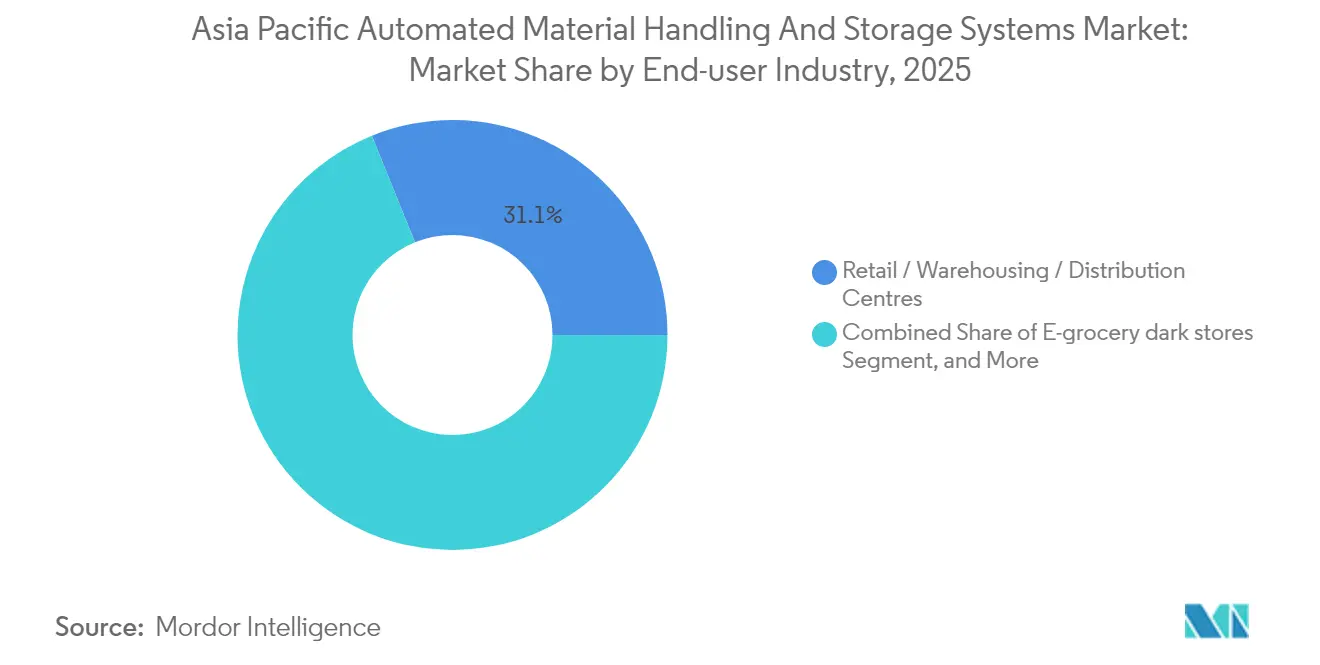

- By end-user industry, retail, warehousing, and distribution centers led with 31.12% revenue share in 2025, while e-grocery dark stores are expected to record the fastest 14.47% CAGR to 2031.

- By function, storage held 34.96% of the Asia Pacific automated material handling and storage systems market size in 2025; sorting activities are slated to post a 14.95% CAGR through 2031.

- By country, China controlled 41.68% revenue in 2025; India is projected to climb at a 14.72% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia Pacific Automated Material Handling And Storage Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming e-commerce fulfillment centers across Tier-2 Asian cities | +2.80% | China, India, Southeast Asia core markets | Medium term (2-4 years) |

| Accelerated adoption of 5G-enabled industrial IoT networks | +2.20% | Japan, South Korea, Singapore, with spillover to APAC | Short term (≤ 2 years) |

| Government incentives for smart-factory automation | +2.10% | China, India, with policy influence across APAC | Long term (≥ 4 years) |

| Cost pressure from rising intra-Asia wages pushing warehouse automation | +1.90% | Vietnam, Thailand, Malaysia, Indonesia | Medium term (2-4 years) |

| Surge in dark-store micro-fulfillment models | +1.70% | Urban centers across APAC, early adoption in Singapore, Hong Kong | Short term (≤ 2 years) |

| ESG-driven demand for energy-efficient material handling systems | +1.40% | Global, with regulatory influence from Japan, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Booming E-commerce Fulfilment Centers Across Tier-2 Asian Cities

The construction boom of automation-ready warehouses in cities such as Chengdu, Pune, and Surabaya sharply elevates demand for standardized yet scalable systems. Operators must harmonize global best practices with local infrastructure constraints, prompting integrators to design modular platforms that support phased rollouts and localized spare-parts ecosystems. Retailers targeting one-day delivery windows view automated picking, sorting, and storage as non-negotiable capabilities, spurring multi-year procurement pipelines that underpin the Asia Pacific automated material handling and storage systems market.[2]Cainiao, “Expansion of Southeast Asia Logistics Network,” alizila.com

Accelerated Adoption of 5G-Enabled Industrial IoT Networks

Private 5G networks shrink latency to sub-10 milliseconds, enabling real-time fleet orchestration, synchronized AMR swarms, and cloud-based digital twins. Early adopters in Seoul and Yokohama report double-digit productivity gains and 30% reductions in unplanned downtime as predictive maintenance algorithms mature.[3]GSMA, “5G Industrial IoT Private Networks,” gsma.com The connectivity layer also underwrites new service models such as remote performance monitoring and outcome-based service contracts, strengthening the recurring-revenue profile of the Asia Pacific automated material handling and storage systems market.

Government Incentives for Smart-Factory Automation

China’s Ministry of Industry and Information Technology subsidizes up to 20% of eligible automation capex, while India’s Production Linked Incentive schemes provide incremental cash disbursements tied to output growth. Such policies mitigate payback risk and expand addressable demand among small and midsize manufacturers, broadening the Asia Pacific automated material handling and storage systems market customer base.[4]Invest India, “Production Linked Incentive Schemes,” investindia.gov.in

Cost Pressure from Rising Intra-Asia Wages Pushing Warehouse Automation

Logistics wages in Ho Chi Minh City and Bangkok climbed at a mid-single-digit pace in 2024, compressing operating margins for export-oriented enterprises. Management teams now schedule automation feasibility studies two to three years earlier than originally planned, with a strong focus on AMR-based order picking and robotic palletizing that can deliver a two-year payback even under conservative throughput scenarios.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial capex and long ROI cycles for SMEs | -1.80% | Developing APAC economies, particularly Indonesia, Philippines | Medium term (2-4 years) |

| Fragmented intra-Asian safety regulations complicating standardization | -1.20% | ASEAN markets with varying compliance frameworks | Long term (≥ 4 years) |

| Cyber-security vulnerabilities in connected automation fleets | -0.90% | Global, with heightened concern in Japan, Singapore | Short term (≤ 2 years) |

| Limited grid power quality in developing economies hampering uptime | -0.70% | Indonesia, Philippines, Vietnam rural areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial Capex and Long ROI Cycles for SMEs

Small and midsize exporters in Jakarta and Manila often confront upfront project costs equalling 1-2 years of free cash flow. Even with vendor financing, a three-to-five-year payback stretches risk tolerance, delaying purchase decisions and marginally tempering the Asia Pacific automated material handling and storage systems market growth trajectory.

Cyber-security Vulnerabilities in Connected Automation Fleets

Ransomware directed at human-machine interfaces and warehouse management databases disrupted material flows in several Singapore sites during 2024, revealing latent cyber-security gaps. Enterprises now insist on zero-trust architectures and periodic penetration testing, adding complexity and incremental cost to new installations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Software Solutions Drive Next-Generation Optimization

The software sub-segment is on track to log a 14.12% CAGR to 2031, reflecting the shift from basic control logic to analytics-enabled orchestration. Advanced warehouse management and digital-twin suites allow predictive slotting and dynamic order batching, bolstering throughput by up to 20% in several Shanghai consumer-electronics facilities. While hardware sustains the bulk of 2024 spending, software-centric value propositions increasingly sway capital-allocation committees, expanding the Asia Pacific automated material handling and storage systems market size among data-mature operators.

Heightened demand for cloud-native applications fuels vendor competition centered on open APIs and edge-to-cloud cybersecurity layers. Providers that bundle software subscriptions with lifecycle services realize higher margins and stickier customer relationships, solidifying long-term revenue streams within the Asia Pacific automated material handling and storage systems market.

By Equipment Type: AMR Technology Reshapes Warehouse Flexibility

AMRs outperform legacy AGVs by navigating dynamic racks and tight aisles without infrastructure-embedded guidance, cutting deployment time by half and accommodating frequent SKU re-profiling. As a result, AMR shipments advance at a 14.78% CAGR, reallocating capital flows away from fixed conveyor expansions toward robot fleets managed by AI-based traffic software.

Automated storage and retrieval systems remain essential in high-throughput omnichannel nodes, though buyers increasingly couple them with AMR-led picking zones. Palletizing robots gain traction among beverage bottlers seeking ergonomic risk mitigation, reinforcing the diversity of demand across the Asia Pacific automated material handling and storage systems market.

By End-user Industry: E-grocery Dark Stores Accelerate Automation Adoption

Dark-store operators emphasize sub-20-minute delivery windows, necessitating goods-to-person stations, high-speed sorters, and micro-shuttles. These requirements underlie the 14.47% CAGR forecast, far surpassing growth in traditional retail distribution. At the same time, automotive assemblers intensify AMR and ASRS investments to align parts flow with electrified vehicle platforms, supporting continued revenue upside for the Asia Pacific automated material handling and storage systems market.

Pharmaceutical manufacturers expand cold chain automation to safeguard product integrity, while semiconductor fabs deploy Class-1 clean-room compliant robots that achieve micron-level positioning accuracy, extending addressable use cases across regulated industries.

By Function: Sorting Applications Lead Growth Trajectory

Cross-border parcel growth averages double digits, forcing operators in Kuala Lumpur and Shenzhen to upgrade from manual chute sorting to vision-guided loop sorters. Segment revenue thereby accelerates at a 14.95% CAGR, eclipsing gains in storage though the latter still commands the single-largest 34.96% revenue share of the Asia Pacific automated material handling and storage systems market size.

Transportation lines relying on modular conveyor blocks integrate seamlessly with AMR fleets, enabling “dynamic hand-offs” that raise facility utilization. Packaging and palletizing record incremental gains as robotics prices continue to decline, making advanced end-of-line automation accessible to mid-tier exporters.

Geography Analysis

China’s 41.68% 2025 revenue share mirrors its expansive manufacturing footprint and over 30,000 certified smart factories subsidized by the central government. Domestic vendors deliver price-competitive AMR and shuttle systems, accelerating uptake in lower-tier provinces and reinforcing the Asia Pacific automated material handling and storage systems market leadership position.

India’s 14.72% CAGR through 2031 stems from converging incentives, including duty credits on capital goods and tax holidays in logistics parks. E-commerce majors finance purpose-built dark stores in Lucknow, Coimbatore, and Guwahati, embedding scalable automation from day one to achieve nationwide two-day service levels without prohibitive labour overhead.

Japan and South Korea demonstrate steady replacement cycles, emphasizing AI-augmented software overlays that extend asset life. Australia and Singapore, both grappling with acute warehouse labour shortages, accelerate conversions to fully automated high-bay facilities. Emerging Southeast Asian economies such as Thailand and Indonesia prioritize phased automation, often beginning with AMR pilots before expanding to ASRS installations, cumulatively enlarging the Asia Pacific automated material handling and storage systems market.

Regulatory Landscape

Across Asia Pacific, automated material handling and storage systems (including AMR/AGV fleets, ASRS, conveyors, and automated warehouses) face a patchwork of machinery-safety, electrical, and increasingly cyber/data-security requirements that vary by country. This has increased compliance and documentation effort for multi-country rollouts. In China, standards have continued to formalize design and operating expectations for automated warehousing, including GB/T 45750-2025 (implemented Dec 1, 2025) for AGV safety risk identification and protection levels, alongside 2026 releases JB/T 10822-2026 (general rules for ASRS design) and WB/T 1147-2026 (general technical requirements for automated warehouses, spanning mechanical/electrical provisions and referenced safety items such as battery and maintenance requirements). In Australia and New Zealand, AS/NZS 4024.3704:2024 aligns rail-dependent storage and retrieval equipment safety requirements with modified EN 528:2021+A1:2022, affecting S/R machine procurement specifications and acceptance testing.

Southeast Asian policy is also shaping deployments through incentives and localized conformity regimes. Malaysia introduced programmatic linkages between warehouse automation and investment incentives through MIDA, with the New Incentive Framework effective March 2026 connecting ASRS, AMR, and automated sortation investments to NIA Scorecard points for tax incentives. Separately, Malaysia announced the MY-ROBO 2026 certification program (via MESTECC) for imported warehouse robotics, with mandatory compliance for new imports from Oct 1, 2026. This adds a distinct certification layer that can influence supplier selection, integration planning, and time-to-commissioning for cross-border equipment shipments.

Competitive Landscape

The competitive field is moderately concentrated, with the top five suppliers controlling approximately 60% of 2024 regional revenue. Daifuku leverages a dense service footprint to win long-term maintenance contracts, while KION Group localized assembly in Xiamen to shorten lead times and comply with country-of-origin rules. SSI Schaefer reported EUR 2.0 billion (USD 2.2 billion) 2024 revenue, aided by large-scale projects in Indonesia and Malaysia.

Regional specialists intensify rivalry by offering turnkey AMR portfolios bundled with cloud analytics. Geekplus expanded joint ventures with integrators in Malaysia and Vietnam, capturing fast-moving retail projects that require highly adaptive fleets. VisionNav Robotics addresses niche autonomous forklift demand, and Grey Orange positions AI-powered orchestration software as a differentiator in multi-vendor environments. Strategic alliances among component providers, telecom operators, and cloud platforms proliferate, underscoring the software-defined evolution of the Asia Pacific automated material handling and storage systems market.

Asia Pacific Automated Material Handling And Storage Systems Industry Leaders

Kardex Group

KION GROUP AG

JBT Corporation

Jungheinrich AG

SSI Schaefer AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term whitespace sits at the intersection of compliance-ready safety engineering and localization for multi-country deployments. Differing safety standards (for example, GB/T 45750-2025 for AGV risk and protection in China and AS/NZS 4024.3704:2024 for rail-dependent S/R equipment in Australia/New Zealand), alongside Malaysia's announced MY-ROBO 2026 certification for imported warehouse robotics (mandatory for new imports from Oct 1, 2026), favor vendors and integrators that package conformity assessment, documentation, and site acceptance testing into turnkey programs. There is also scope for software layers that harden operations (identity, access control, patching discipline, and auditability) as connected fleets and WMS/WCS integrations deepen, particularly for operators standardizing architectures across China, India, and Southeast Asia.

Capacity additions, new partnerships, and regional execution footprints support faster project delivery and wider adoption beyond top-tier hubs. Daifuku commissioning a manufacturing plant in Hyderabad in April 2025 is an example of expanded output for automated warehouses, transport vehicles, and conveyors, while KION Group announcing a large expansion of its Jinan automated material handling plant in January 2025 includes an AI-focused R&D element. On the solutions side, partnerships such as Gorilla Technology Group and Toyota Material Handling Solutions (Thailand) (announced April 2025) point to continued alignment between industrial data/AI capabilities and warehouse automation portfolios, supporting projects where operators want flexible automation (AMR plus high-throughput storage and sortation) with clearer integration ownership. In Southeast Asia, Malaysia's incentive framework (effective March 2026) ties automation capex to tax incentive eligibility, creating additional lanes for ASRS/AMR and sorter deployments in new logistics parks and smart-logistics estates where greenfield design can embed automation earlier than retrofits.

Recent Industry Developments

- May 2026: Kardex Malaysia announced an AutoStore StarterGrid partnership with Fordcon Jaya Sdn Bhd, positioned as the first StarterGrid partnership in Asia-Pacific, for automotive component warehousing. The partnership packages a more standardized, faster-to-deploy goods-to-person concept for customers that want smaller initial footprints and clearer expansion paths. It also strengthens Kardex's channel-led execution in Southeast Asia, where automation projects increasingly require local service coverage and integration support.

- April 2026: KION Group signed a strategic automation partnership agreement with CEL Group (dated April 3, 2026) at a Linde facility in Xiamen, China. The agreement supports a more repeatable approach to automation procurement and deployment rather than one-off projects, which can shorten lead times across multiple sites. It also reinforces the role of KION's Xiamen hub in regional solution localization and lifecycle support for automated warehouses and mobile-robot-enabled intralogistics.

- August 2024: KION Group upgraded its APAC Automation Center of Excellence in Xiamen, China, expanding regional capabilities for engineering, validation, and solution tailoring. The upgrade strengthens local delivery capacity for complex systems such as ASRS, conveyors, and software orchestration layers. It also improves responsiveness to China-led demand and cross-border projects that need regionalized designs, testing, and commissioning resources.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue earned from automated systems used to move, store, pick, and sort materials inside factories, warehouses, and distribution centers across Asia Pacific, including the enabling software and related services when they are part of the automated solution.

Scope exclusions: Non-automated handling equipment and general building construction work are excluded, unless they are sold as part of an automated handling or storage system deployment.

Segmentation Overview

- By Product Type

- Hardware

- Software

- Services

- By Equipment Type

- Mobile Robots

- Automated Guided Vehicle (AGV)

- Automated Forklift

- Automated Tow / Tractor / Tug

- Unit Load

- Assembly Line

- Special Purpose

- Autonomous Mobile Robots (AMR)

- Automated Guided Vehicle (AGV)

- Automated Storage and Retrieval System (ASRS)

- Fixed Aisle

- Carousel

- Vertical Lift Module

- Automated Conveyor

- Belt

- Roller

- Pallet

- Overhead

- Palletizer

- Conventional

- Robotic

- Sortation System

- Mobile Robots

- By End-user Industry

- Airport

- Automotive

- Food and Beverage

- Retail / Warehousing / Distribution Centres / Logistic Centres

- General Manufacturing

- Pharmaceuticals

- Post and Parcel

- Electronics and Semiconductor Manufacturing

- Other End-user Industries

- By Function

- Storage

- Transportation

- Sorting

- Packaging / Palletising

- Assembly / Kitting

- By Country

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Thailand

- Singapore

- Malaysia

- Taiwan

- Rest of Asia Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the market baseline for automated material handling and storage systems in Asia Pacific, and to anchor the model to practical demand signals. We relied on public sources such as national statistics offices, customs import and export data portals, industrial automation or logistics associations, and central bank and ministry publications for macro indicators like industrial output, manufacturing PMI direction, and trade flows.

To keep assumptions grounded, we also reviewed company annual reports, investor presentations, and reputable business press to map where automation spending is moving by industry and country. In countries where public data is thin, an import and export shipment-level database and a company financials and intelligence subscription were used to cross-check supplier footprints and investment cycles (without taking vendor claims at face value). These examples are not exhaustive, and other public and paid sources were also referenced for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary interviews and surveys were used to stress-test the desk inputs and to fill gaps around system pricing, typical project sizes, and adoption timing across key Asia Pacific countries. We spoke with a mix of system integrators, automation equipment suppliers, software providers, and large end users in warehousing and manufacturing. After the initial interviews, we revisited assumptions where responses showed material variance by country or end-use.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 14% | |

| Mid tier: 51% | Functional/Unit leaders: 35% | |

| Smaller Players: 18% | Managers: 51% |

Market-Sizing & Forecasting

The model starts from a top-down build where industrial production growth, warehouse and distribution center expansion, and automation penetration by end-use are used to reconstruct the addressable demand pool across Asia Pacific. Once that demand pool is set, it is translated into value using market-realistic system mix and pricing ranges for major automated solutions.

To keep totals in check, the results are corroborated with selective bottom-up approximations, such as sampled system average selling price times expected unit volumes for conveyors, sortation, ASRS, and mobile robots, followed by channel checks with integrators. Key inputs that were tracked (illustrative, not exhaustive) include country-level manufacturing output and exports, e-commerce fulfillment growth indicators, labor availability and wage pressure in warehousing, typical automation payback expectations, and the mix shift between software and hardware content in projects. For forecasting, scenario analysis was applied around capex cycles, supply chain re-shoring or China-plus-one moves, and the timing of greenfield warehouse builds, and then the scenario weights were aligned to expert consensus from interviews. Where bottom-up visibility was incomplete, ranges were used and narrowed with follow-up calls until the implied installation pace matched realistic deployment capacity.

Data Validation & Update Cycle

Validation is done through multiple checks so the totals remain tied to independent signals. We compare outputs against alternative indicators like automation order commentary, investment announcements, and trade movement for key equipment categories, and then outliers are investigated before sign-off.

If a country or end-use shows an unusual jump, the inputs are re-checked, assumptions are adjusted, and respondents are re-contacted when needed to confirm whether it is a real shift or a timing effect. Reports are refreshed annually, with interim updates when material events occur that can change spending, lead times, or pricing. Before delivery, an analyst performs a fresh pass across the model and key assumptions so clients receive an updated view.

Mordor Intelligence's Asia Pacific Automated Material Handling and Storage Systems Market Market Estimate Compared With Other Published Estimates

Published market values for this space can differ more than users expect because the scope line is not always consistent, and because the mix of equipment and services shifts quickly across Asia Pacific. Differences also come from how firms treat system pricing, which year they label as the base, and how often the model is refreshed.

The main gap comes from whether broader material handling equipment, non-automated trucks, and general warehouse infrastructure are counted together with automated systems, which inflates totals. Some sources also apply a single growth rate to a large starting value without validating it against adoption limits, like integrator delivery capacity and realistic commissioning timelines. The table below shows these scope and assumption choices in a simple way.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 29.66 B (2025) | |

| Research Publisher A | USD 18.60 B (2024) | Uses an earlier base year and tends to bundle warehouse management software mentions with system value without consistently separating pure automation project revenue from adjacent IT spend. |

| Press Release B | USD 92.57 B (2024) | Appears to cover a much wider automated material handling equipment universe for Asia Pacific, which can include large categories beyond automated storage and handling systems and can lift totals materially. |

The spread is mainly explained by scope width and by how pricing and adoption are translated into value across countries. The gap-driver choice is handled by Mordor Intelligence by counting Asia Pacific revenues only when they are tied to automated handling and storage system deployments (including related software and services sold with those projects), and by keeping broader non-automated equipment outside the total. With the same demand signals and repeatable checks applied each year, users get a market value that is easier to trace back to clear inputs.

Key Questions Answered in the Report

What is the projected 2031 value of United States material handling leasing and financing?

The market is forecast to reach USD 3.44 billion by 2031, reflecting a 15.43% CAGR over 2026-2031.

Which equipment category is growing fastest in U.S. warehouse financing?

Automated guided vehicles lead with a 16.02% CAGR forecast through 2031 as firms accelerate automation.

How do Section 179 deductions influence equipment leasing decisions?

Lessees can expense up to USD 1.22 million immediately, making operating leases the preferred structure for fast-turnover fleets.

Why are sale-and-leaseback deals becoming popular among warehouse operators?

They unlock trapped equity from existing fleets, funding automation upgrades without increasing balance-sheet debt, and are projected to grow at 16.81% CAGR.

Which regions are hotspots for new leasing activity?

California's Inland Empire, Texas distribution corridors, and the Southeast logistics belt exhibit the highest growth due to port modernization and e-commerce fulfillment expansion.

Page last updated on: