Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

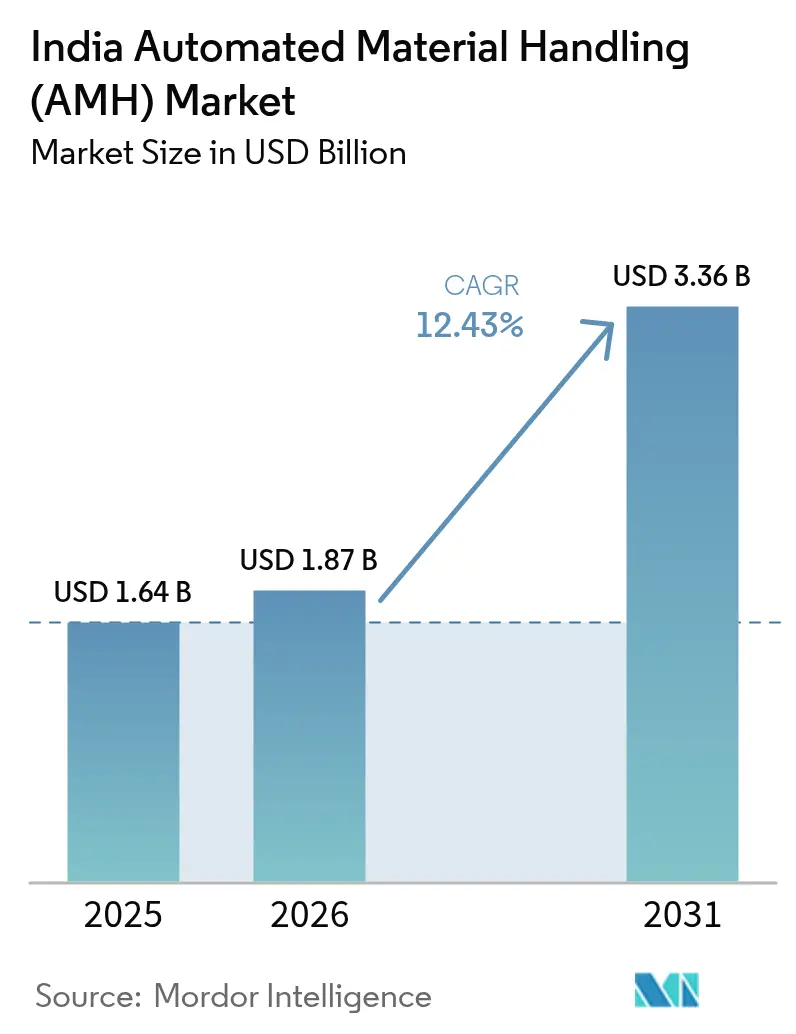

| Base Year Market Size (2025) | USD 1.64 Billion |

| Market Size (2026) | USD 1.87 Billion |

| Market Size (2031) | USD 3.36 Billion |

| Growth Rate (2026 - 2031) | 12.43% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Automated Material Handling (AMH) Market Analysis by Mordor Intelligence

The India automated material handling market size is projected to expand from USD 1.64 billion in 2025 and USD 1.87 billion in 2026 to USD 3.36 billion by 2031, registering a CAGR of 12.43% between 2026 and 2031. Capital spending is accelerating as fulfilment centers now carry 3-4 times the stock-keeping unit density of traditional warehouses, while the Production Linked Incentive program has unlocked USD 23.6 billion of factory investments that depend on reliable, traceable in-plant flows. Warehouse operators in Mumbai, Delhi-NCR, Bangalore, and other Tier-1 hubs report annual labour attrition above 35% and wage inflation near 12%, forcing a shift toward robots that repay themselves in three to four years. Cold-chain facilities serving vaccines, biologics, and perishable foods have embraced high-density automated storage that triples pallet positions per square meter, and cuts electricity use by up to 30% through LED lighting and variable-frequency conveyors. Grid unreliability averaging 2.5 hours of monthly outages has led buyers to allocate 15-20% of their automation budgets to backup power, embedding resilience costs directly into project economics.

Key Report Takeaways

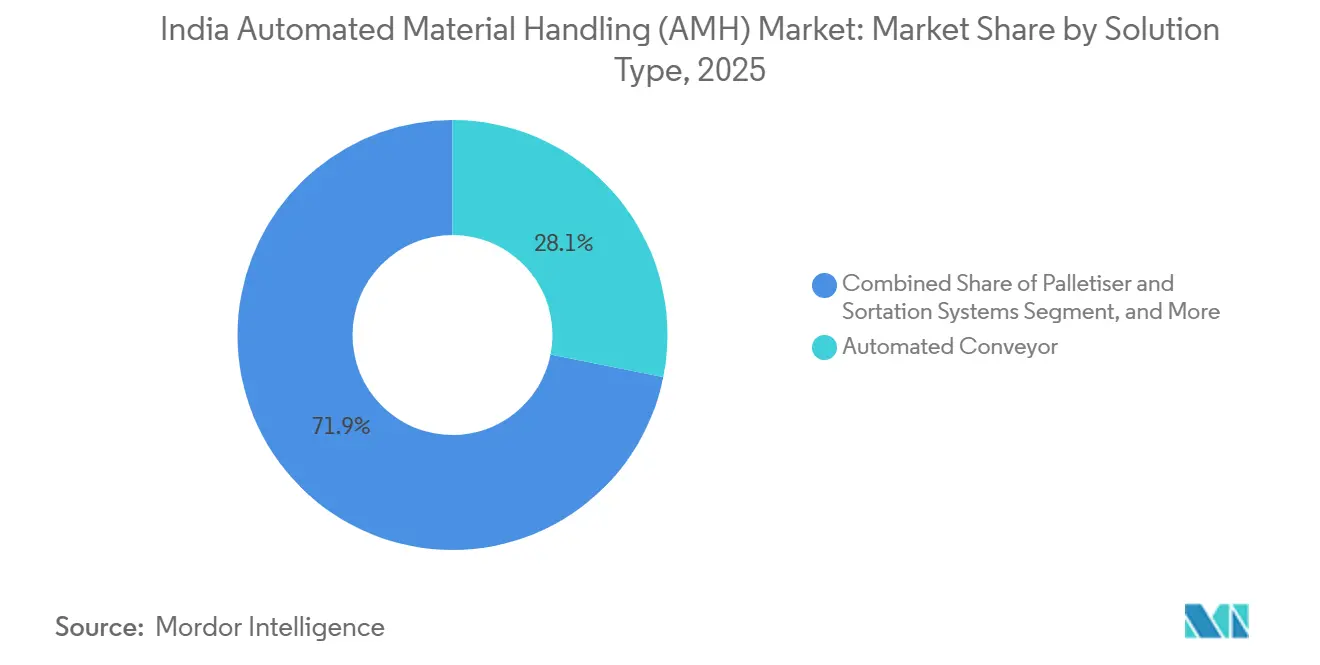

- By solution type, automated conveyors led with 28.13% revenue share in 2025 while Automated Guided Vehicles and Autonomous Mobile Robots are forecast to expand at a 13.22% CAGR through 2031.

- By function, storage accounted for 34.58% of the India automated material handling market share in 2025 and picking and sorting is advancing at a 13.89% CAGR through 2031.

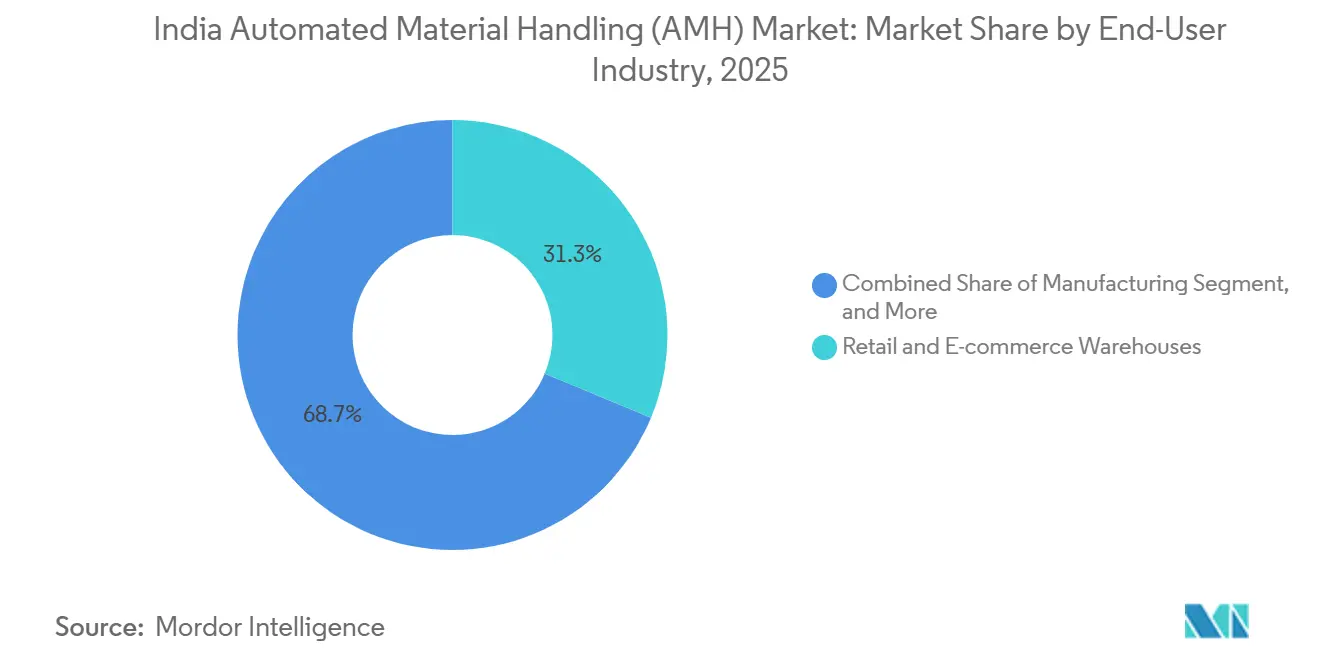

- By end-user industry, retail and e-commerce warehouses commanded 31.29% of 2025 demand; pharmaceuticals and healthcare represent the fastest growth, rising at a 13.16% CAGR to 2031.

- By load type, unit-load systems represented 63.11% of 2025 revenue and are expected to progress at a 12.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Automated Material Handling (AMH) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce Fulfillment Expansion Accelerating Warehouse Automation | +2.80% | National, concentrated in Mumbai, Delhi-NCR, Bangalore, Hyderabad, Pune | Medium term (2-4 years) |

| Government Production Linked Incentive Scheme Catalysing Factory Automation Investments | +2.30% | National, with clusters in Tamil Nadu, Gujarat, Uttar Pradesh, Karnataka | Long term (≥ 4 years) |

| Rising Urban Wage Costs and Labour Scarcity in Tier-1 Logistics Hubs | +1.90% | Tier-1 cities: Mumbai, Delhi-NCR, Bangalore, Chennai, Pune | Short term (≤ 2 years) |

| Temperature-Controlled Pharma and Food Cold Chain Requiring High-Density Automated Storage | +1.60% | National, early gains in Gujarat, Maharashtra, Andhra Pradesh | Medium term (2-4 years) |

| Sustainability Mandates Pushing Energy-Efficient, Electrified AMH Systems | +1.20% | National, driven by corporate ESG commitments and Bureau of Energy Efficiency standards | Long term (≥ 4 years) |

| 5G Private Networks and Edge AI Enabling Real-Time Control of Large AGV Fleets in Mega-Warehouses | +1.50% | Tier-1 and Tier-2 manufacturing and logistics hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Fulfilment Expansion Accelerating Warehouse Automation

Fulfilment platforms racing to compress order-to-dispatch times have triggered a surge in conveyance, sorting, and goods-to-person robotics. Quick-commerce dark stores process 2,000-3,000 orders daily from inventories of 10,000-15,000 stock-keeping units, conditions that push manual error rates above 2-3%. Amazon’s plan to add 15 million cubic feet of capacity and Flipkart’s 1,500-hub network both depend on sorters capable of 5,000-10,000 parcels per shift. The competitive cascade is evident: Reliance’s JioMart automated a grocery warehouse in May 2025, cutting labour by 25% and pushing rivals toward similar upgrades.[1]Addverb Technologies, “Reliance JioMart Automation,” addverb.com

Government Production Linked Incentive Scheme Catalysing Factory Automation Investments

The scheme’s USD 23.6 billion of committed spending aligns neatly with three- to five-year automation payback periods. Tata Electronics in Hosur orchestrates Automated Guided Vehicle fleets over a 5G private network, trimming cycle time by roughly 20% and securing parts traceability below 50 parts per million.[2]Tata Communications, “5G Private Network at Hosur Plant,” tatacommunications.com As funds are disbursed over four to six years, beneficiaries view automation as a prerequisite to ensure incentive compliance and quality standards.

Rising Urban Wage Costs and Labor Scarcity in Tier-1 Logistics Hubs

Monthly wages of INR 18,000-25,000 (USD 216-300) now climb 10-12% each year, while attrition tops 35%. A 100,000-square-foot manual warehouse can burn USD 264,000 in annual payroll, compared with an USD 840,000 automated sortation line that breaks even in four years. Falcon Autotech’s 9,000-parcel-per-hour sorter eliminated 40-50 manual positions at DTDC Express and maintained throughput during Diwali peaks.[3]Falcon Autotech, “Sortation System for DTDC Express,” falconautotech.com

Temperature-Controlled Pharma and Food Cold Chain Requiring High-Density Automated Storage

India’s cold-chain deficit has prompted shuttle-based Automated Storage and Retrieval Systems that store 3.5-4 pallets per square meter in sub-zero zones. Indicold’s 10,000-pallet facility in Gujarat, launched in April 2025, maintains 2-8 °C with real-time logging, meeting National Cold Chain guidelines while saving up to INR 2 million in annual power costs.[4]Indicold Logistics, “Automated Cold Chain Network in Gujarat,” indicold.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Capex and Long ROI Cycles for SMEs | -1.80% | National, acute in Tier-2 and Tier-3 cities | Short term (≤ 2 years) |

| Legacy Brownfield Layouts Limiting Retrofit Feasibility | -1.30% | National, concentrated in older industrial zones in Mumbai, Delhi, Kolkata | Medium term (2-4 years) |

| Escalating Cyber-security Risks Across Connected AMH Assets | -0.90% | National, heightened in multi-site enterprise deployments | Medium term (2-4 years) |

| Grid Reliability Gaps and Backup Power Costs Impacting System Uptime | -1.10% | National, severe in Uttar Pradesh, Bihar, Jharkhand; moderate in Maharashtra, Gujarat | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Capex and Long ROI Cycles for SMEs

An entry-level sortation line for a 50,000-square-foot site costs USD 480,000-720,000, equal to two to three years of operating profit for many logistics providers. Paybacks stretch to seven years when throughput is low, and ceiling heights below 10 meters preclude high-bay storage, forcing costly structural reinforcements. Leasing and automation-as-a-service models remain nascent, limiting adoption among operators running on 8-12% margins.

Legacy Brownfield Layouts Limiting Retrofit Feasibility

Warehouses built in the 1990s feature 8–10-meter heights, narrow column grids, and floors rated at only 2 tonnes per square meter. Retrofitting can cost 60-70% of a greenfield project but still yield 20-30% lower throughput, discouraging investment. Electrical upgrades, transformer replacements, and regulatory approvals add six to nine months, a timeline many tenants cannot absorb.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: AGV and AMR Fleets Redefine Flexibility

Automated conveyors held 28.13% of 2025 revenue because fixed belts and rollers still dominate high-volume parcel hubs that demand 8,000-12,000 cartons per hour. Automated Storage and Retrieval Systems thrive in cold-chain and pharma sites where land prices exceed INR 15,000 per square meter. Palletizer and sortation lines at courier depots achieve 99.8% accuracy while Warehouse Management and Control Software tighten inventory accuracy. Robotic picking remains niche but attractive in apparel centers that justify USD 240,000 per cell to reach 400 picks per hour.

Automated Guided Vehicles and Autonomous Mobile Robots will grow at a 13.22% CAGR to 2031, the fastest trajectory among solutions in the India AMH market. GreyOrange’s Relay Pick travels 4 m per second and offers 400 presentations per hour, letting one associate pick 150-200 orders per shift. A 5G private network at Tata Electronics delivers sub-10 millisecond latency to synchronize 50-100 robots, overcoming Wi-Fi dead zones and enabling layouts that adapt to seasonal stock-keeping unit changes without civil work.

By Function: Picking and Sorting Automation Gains Momentum

Storage secured 34.58% of 2025 revenue as vertical AS/RS installations offset scarce urban land and keep pharmaceutical lots in first-in-first-out order. Transportation combines conveyors and AGVs to ferry goods from inbound docks to dispatch lanes. Retrieval, often bundled with storage, ensures serialized inventory rotation while packaging and palletizing robots remove repetitive strain injuries and lift end-of-line speed.

Picking and sorting is advancing at a 13.89% CAGR, the quickest functional climb, fuelled by single-unit online orders that multiply pick lines per shift. Quick-commerce sites now generate 16,000-36,000 discrete picks daily, overwhelming manual teams. Vision-guided piece-picking covers 60-80% of clothing and electronics stock-keeping units, and Falcon Autotech’s system cut mis-sorts from 1.2% to 0.08%. Dynamic slotting powered by artificial intelligence moves high-velocity goods to forward areas overnight, reducing travel distance by 30-40%.

By End-User Industry: Pharmaceuticals Emerge as Growth Leader

Retail and e-commerce warehouses commanded 31.29% of 2025 spending as firms poured USD 3 million into each 100,000-square-foot building to reach same-day dispatch. Manufacturing plants in automotive and electronics harness AMH to align takt time with just-in-sequence parts arrival, slashing work-in-process by up to 50%. Food and beverage companies add cold-safe palletizers, and airports install tilt-tray sorters that process 3,000-4,000 bags hourly during holiday peaks.

Pharmaceuticals and healthcare will grow at a 13.16% CAGR to 2031, outpacing all others in the India AMH market. Vaccine supply chains need 2-8 °C compliance, and Indicold’s frozen site stores 3.5 pallets per square meter while logging temperature in real time. Serialization rules effective since 2024 require flawless barcode capture, tilting economics toward RFID-enabled cranes and robots that all but eliminate manual data entry errors.

By Load Type: Unit-Load Dominance Reflects Palletization Trends

Unit-load systems held 63.11% of 2025 revenue and are poised for a 12.89% CAGR through 2031. Pallet-based flows dominate organized retail and contract logistics where single sites move 80-120 pallets per hour around the clock, justifying USD 2 million AS/RS projects that pay back within four years.

Bulk-load automation targets loose cartons, totes, and piece picks prevalent in fashion and quick-commerce. Systems such as Relay Pick offer 400 presentations per hour but cost roughly double pallet-handling AGVs, tempering uptake. Yet as single-item consumer orders rise toward half of e-commerce volume, bulk-load robotics will gain share, especially in health and personal care categories where item level handling is non-negotiable.

Geography Analysis

Tier-1 cities Mumbai, Delhi-NCR, Bangalore, Hyderabad, Pune, and Chennai host roughly 65% of 2025 installations because they combine Grade-A warehouses, last-mile hubs, and large manufacturing clusters. Maharashtra and Gujarat lead cold-chain automation; Indicold’s and Wagh Bakri’s high-bay stores illustrate how dense storage offsets land priced at INR 20,000 per square meter. Tamil Nadu and Karnataka dominate electronics and automotive flows: Tata Electronics and Bosch both rely on 5G private networks to choreograph AGV fleets in Hosur and Bidadi respectively.

Tier-2 cities such as Ahmedabad, Jaipur, and Lucknow attract fresh builds due to land priced around INR 6,000 per square meter, but grid outages and skill shortages inflate operating costs by up to 20%. Uttar Pradesh and Madhya Pradesh together absorbed 12-15% of new space in 2025, driven by logistics providers that want regional reach beyond the big six metros. Operators still budget 15-20% of project cost for diesel generators, a burden that postpones automation among smaller tenants.

Relative to international markets, India’s per-capita robot density remains far below the United States, Europe, or China, but parallels with China’s 2016-2018 playbook modular systems, local manufacturing, phased deployments suggest convergence by 2030-2032. States with dependable power, supportive labour pools, and highway connectivity will continue to win the highest-throughput installations, reinforcing existing clusters through at least 2028.

Competitive Landscape

The India AMH market exhibits moderate fragmentation: the top five vendors Daifuku, Dematic, SSI Schaefer, Vanderlande, and Honeywell Intelligrated collectively control roughly 35-40% share. Their turnkey capability and global maintenance fleets command premiums yet imported components leave them 15-20% costlier than domestic challengers. Localization is rising Daifuku opened a USD 27.2 million Hyderabad plant in April 2025 and targets 95% domestic content to narrow the gap.

Indian manufacturers such as Addverb, GreyOrange, and Godrej Consoveyo capitalize on lower engineering costs, eight-to-twelve-week shorter lead times, and willingness to tailor systems for 20,000-30,000-square-foot buildings that multinationals often ignore. Software capability now marks a key battleground: vendors bundling advanced Warehouse Control Software can command 20-25% higher prices by offering predictive maintenance that cuts downtime below 1%.

White-space opportunities remain in Tier-2 cities where 70-75% of warehouses are still manual, in brownfield retrofits that need modular low-ceiling robots, and in sector niches like airport cargo and textiles. Cybersecurity has emerged as a differentiator; buyers favour ISO/IEC 27001-certified solutions and air-gapped operational networks after CERT-In recorded 1.391 million incidents in 2023.

India Automated Material Handling (AMH) Industry Leaders

Daifuku India Private Limited (Incl. Vega Conveyors & Automation

Godrej Consoveyo Logistics Automation Ltd (GCLA)

Kardex India Storage Solutions Private Limited

Armstrong Ltd.

Space Magnum Equipment Pvt. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Wagh Bakri Tea Group commissioned a 200-meter-tall, automated storage system at Dakor, Gujarat, investing INR 1.4 billion (USD 16.8 million) to house 180,000 tea chests in a temperature-controlled space.

- May 2025: Daifuku India inaugurated a INR 2.27 billion (USD 27.2 million) manufacturing plant in Hyderabad to achieve 95% local content across conveyors, AS/RS, and sorters.

- April 2025: Indicold opened a 10,000-pallet shuttle-based frozen store in Gujarat that meets pharmaceutical and biologic distribution norms.

- March 2025: Addverb deployed goods-to-person robots at a Reliance JioMart grocery site, improving order speed by 40% and trimming headcount by 25%.

India Automated Material Handling (AMH) Market Report Scope

The India Automated Material Handling Market Report is Segmented by Solution Type (Automated Conveyor, AS/RS, AGV/AMR, Palletiser and Sortation Systems, WMS/WCS, Robotic Picking Systems), Function (Storage, Transportation, Picking and Sorting, Retrieval, Packaging and Palletising), End-User Industry (Airports, Manufacturing, Retail and E-commerce, Food and Beverage, Pharma and Healthcare, Others), Load Type (Unit Load, Bulk Load). The Market Forecasts are Provided in Value (USD).

By Solution Type

| Automated Conveyor |

| Automated Storage and Retrieval System (AS/RS) |

| Automated Guided Vehicles and Autonomous Mobile Robots (AGV/AMR) |

| Palletiser and Sortation Systems |

| Warehouse Management System and Warehouse Control Software (WMS/WCS) |

| Robotic Picking Systems |

By Function

| Storage |

| Transportation |

| Picking and Sorting |

| Retrieval |

| Packaging and Palletising |

By End-User Industry

| Airports |

| Manufacturing |

| Retail and E-commerce Warehouses and Logistics Centres |

| Food and Beverage |

| Pharmaceuticals and Healthcare |

| Other End-User Industries |

By Load Type

| Unit Load |

| Bulk Load |

| By Solution Type | Automated Conveyor |

| Automated Storage and Retrieval System (AS/RS) | |

| Automated Guided Vehicles and Autonomous Mobile Robots (AGV/AMR) | |

| Palletiser and Sortation Systems | |

| Warehouse Management System and Warehouse Control Software (WMS/WCS) | |

| Robotic Picking Systems | |

| By Function | Storage |

| Transportation | |

| Picking and Sorting | |

| Retrieval | |

| Packaging and Palletising | |

| By End-User Industry | Airports |

| Manufacturing | |

| Retail and E-commerce Warehouses and Logistics Centres | |

| Food and Beverage | |

| Pharmaceuticals and Healthcare | |

| Other End-User Industries | |

| By Load Type | Unit Load |

| Bulk Load |

Key Questions Answered in the Report

How large will the India automated material handling market be by 2031?

It is projected to reach USD 3.36 billion by 2031, growing at a 12.43% CAGR from 2026.

Which solution type is growing the fastest?

Automated Guided Vehicles and Autonomous Mobile Robots are forecast to expand at a 13.22% CAGR through 2031.

Why are pharmaceuticals investing heavily in automation?

Serialization mandates and temperature-controlled vaccine logistics demand precise, traceable, automated flows that deliver three- to four-year paybacks.

What is the main barrier for small and medium enterprises?

Upfront costs of USD 480,000-720,000 and paybacks of five to seven years deter many smaller operators.

Which cities dominate new installations?

Mumbai, Delhi-NCR, Bangalore, Hyderabad, Pune, and Chennai together host about 65% of deployments, thanks to Grade-A warehouses and skilled labor.

How are vendors addressing cybersecurity concerns?

Leading suppliers now offer ISO/IEC 27001-certified solutions and air-gapped operational networks to mitigate ransomware risks.

Page last updated on: