Material Handling Equipment Telematics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

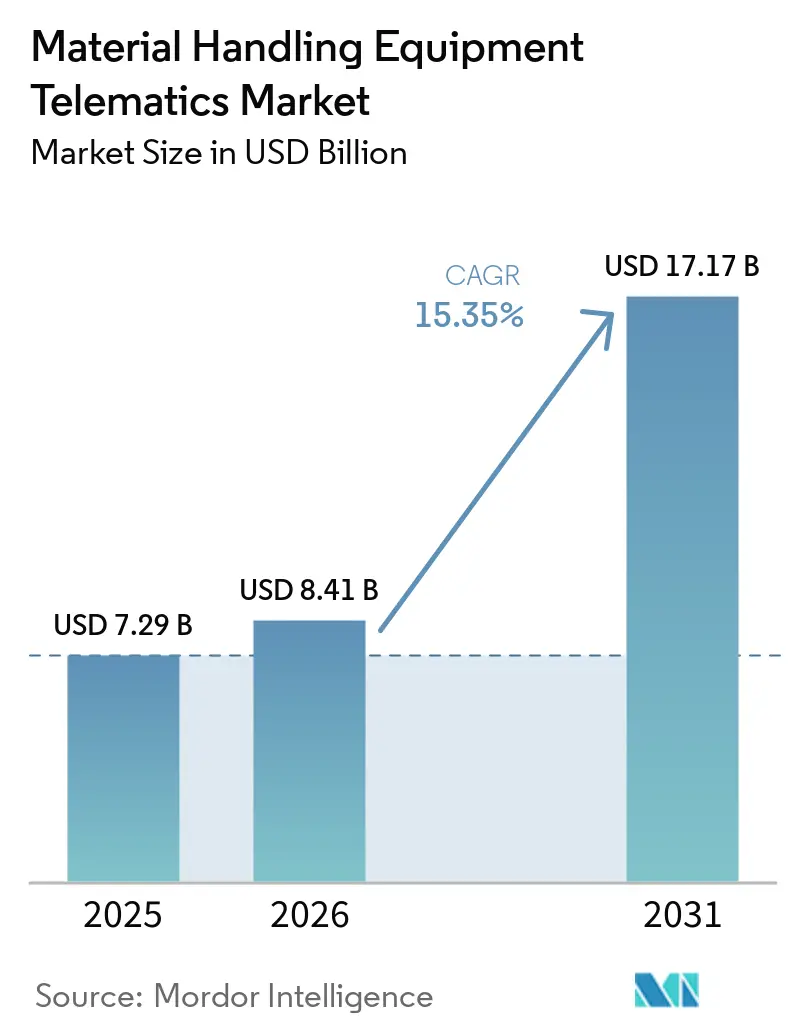

| Market Size (2026) | USD 8.41 Billion |

| Market Size (2031) | USD 17.17 Billion |

| Growth Rate (2026 - 2031) | 15.35% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

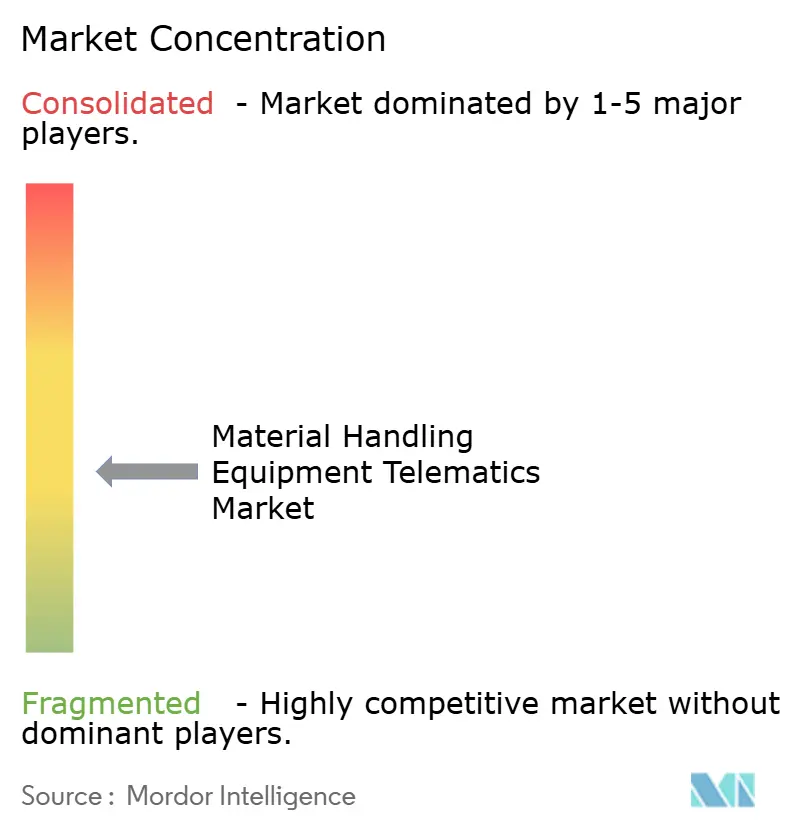

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Material Handling Equipment Telematics Market Analysis by Mordor Intelligence

The material handling equipment telematics market size is expected to increase from USD 7.29 billion in 2025 to USD 8.41 billion in 2026 and reach USD 17.17 billion by 2031, growing at a CAGR of 15.35% over 2026 to 2031. The material handling equipment telematics market is entering a phase in which operators expect live recommendations and workflow guidance rather than passive reports, and this shift is elevating the operational role of telematics across warehouses and industrial sites. Demand is being supported by tighter safety oversight, broader adoption of cloud-native fleet platforms, and closer integration between AI tools and IIoT sensor networks within connected fleets. The material handling equipment telematics market is also benefiting from the way fleet data is increasingly tied to uptime, labor productivity, and equipment utilization, making telematics relevant to day-to-day operating decisions rather than only for compliance. Competitive positioning is changing as hardware becomes easier to compare and vendors try to stand out through analytics, software subscriptions, and integration depth across mixed fleets. Even with strong momentum, the material handling equipment telematics market still faces friction from cybersecurity exposure, retrofit costs, and indoor signal constraints that can limit positioning accuracy in dense warehouse environments.

Key Report Takeaways

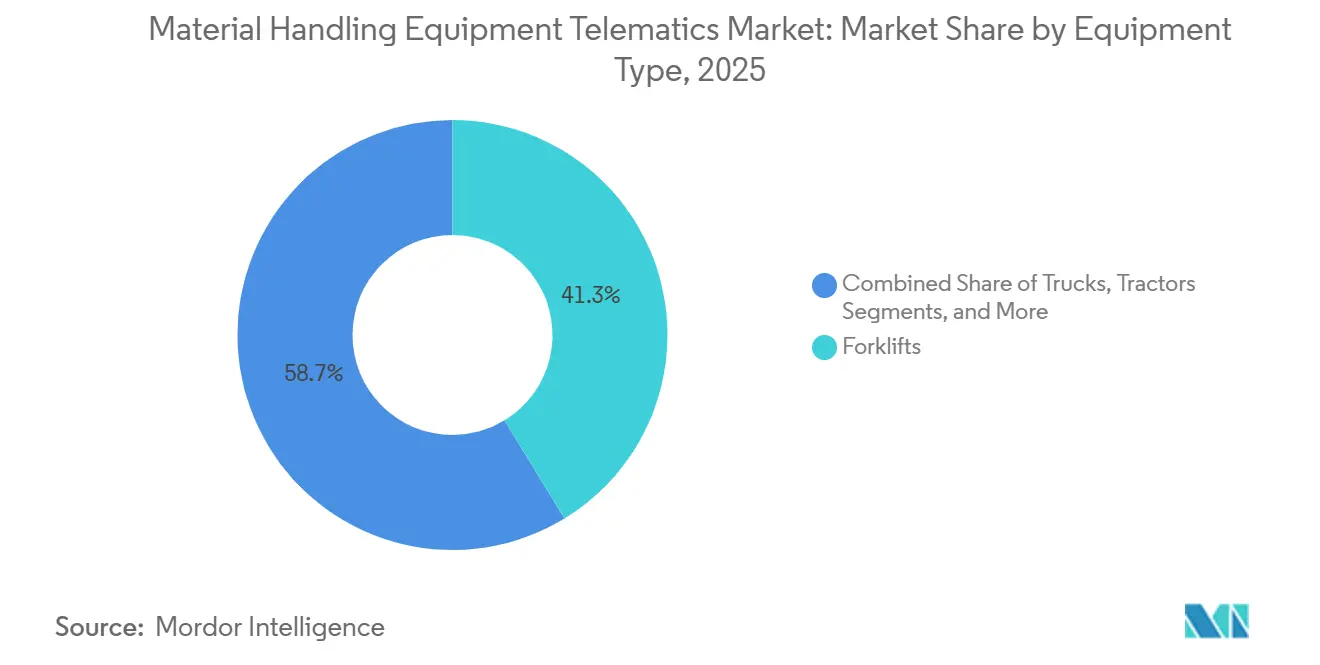

- By equipment type, forklifts led with 41.28% share of the material handling equipment telematics market in 2025, while AGVs are forecast to expand at a 15.41% CAGR through 2031.

- By solution type, fleet management held 34.36% share of the material handling equipment telematics, while predictive maintenance recorded the highest projected CAGR at 15.56% through 2031.

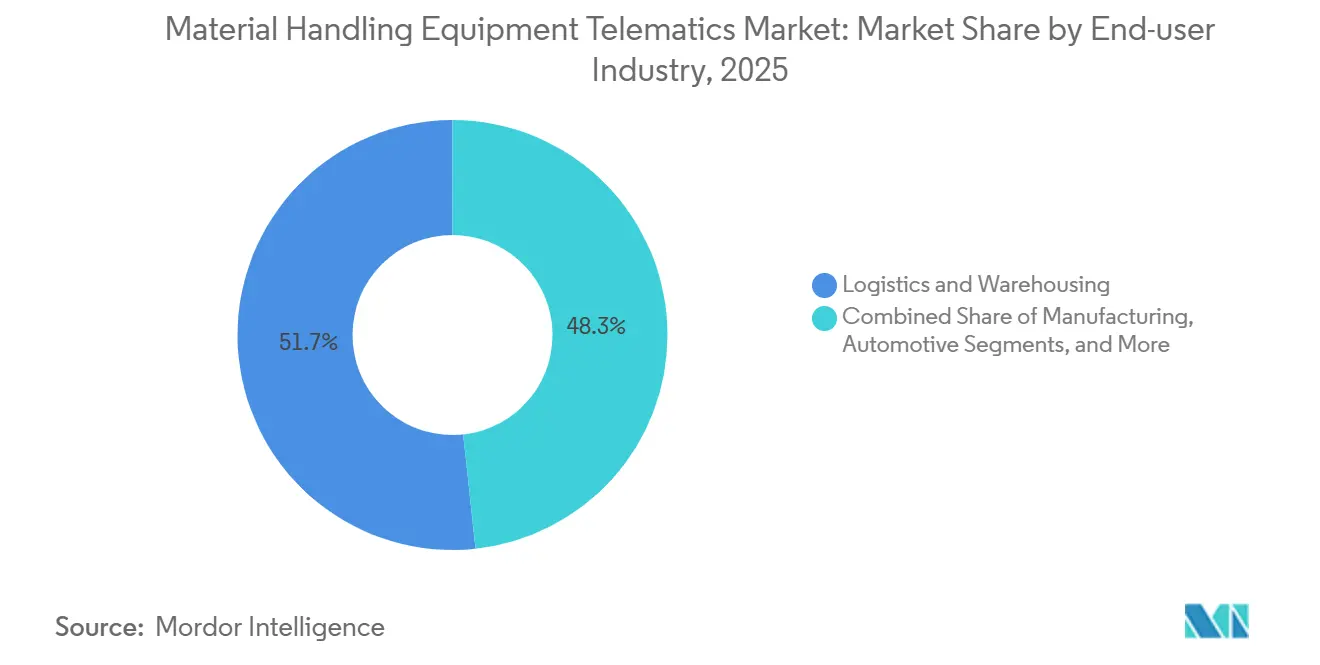

- By end-user industry, logistics and warehousing accounted for 51.71% share of the material handling equipment telematics market, while construction is advancing at a 15.69% CAGR through 2031.

- By technology, GPS captured 44.22% share of the material handling equipment telematics market, while AI-based predictive systems are projected to grow at a 16.02% CAGR through 2031.

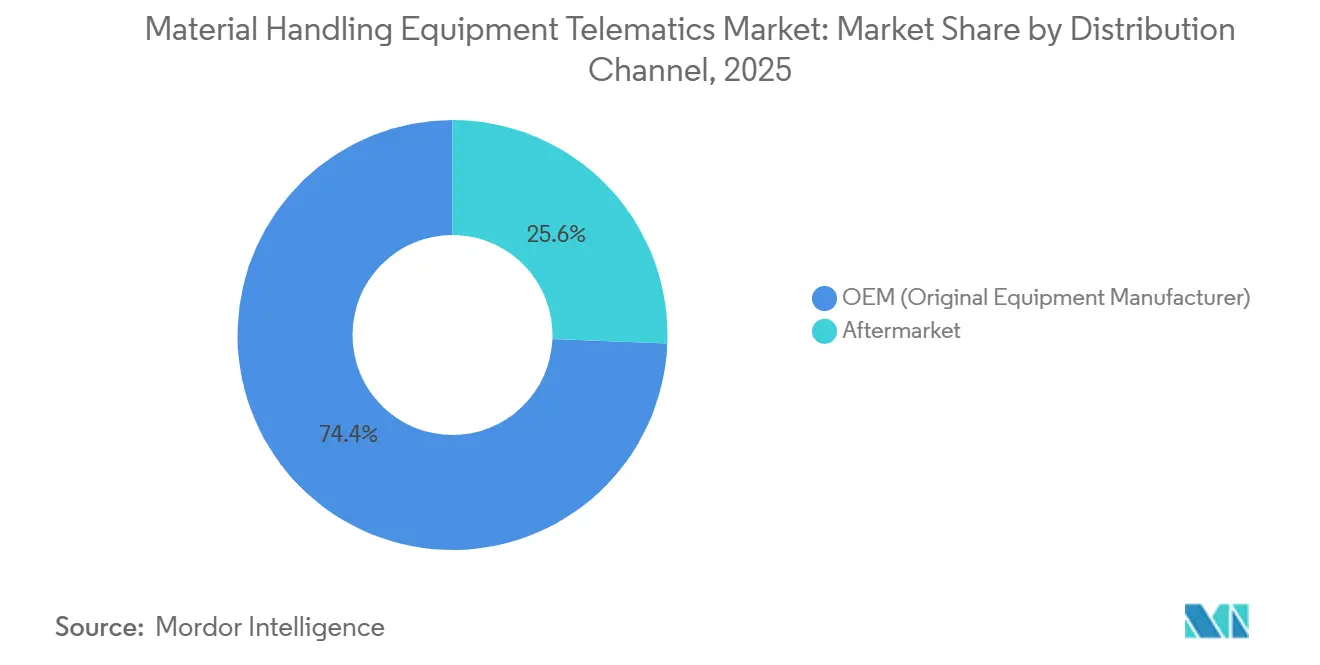

- By distribution channel, OEM-integrated telematics represented 74.37% share of the material handling equipment telematics, while aftermarket channels are projected to expand at a 15.97% CAGR through 2031.

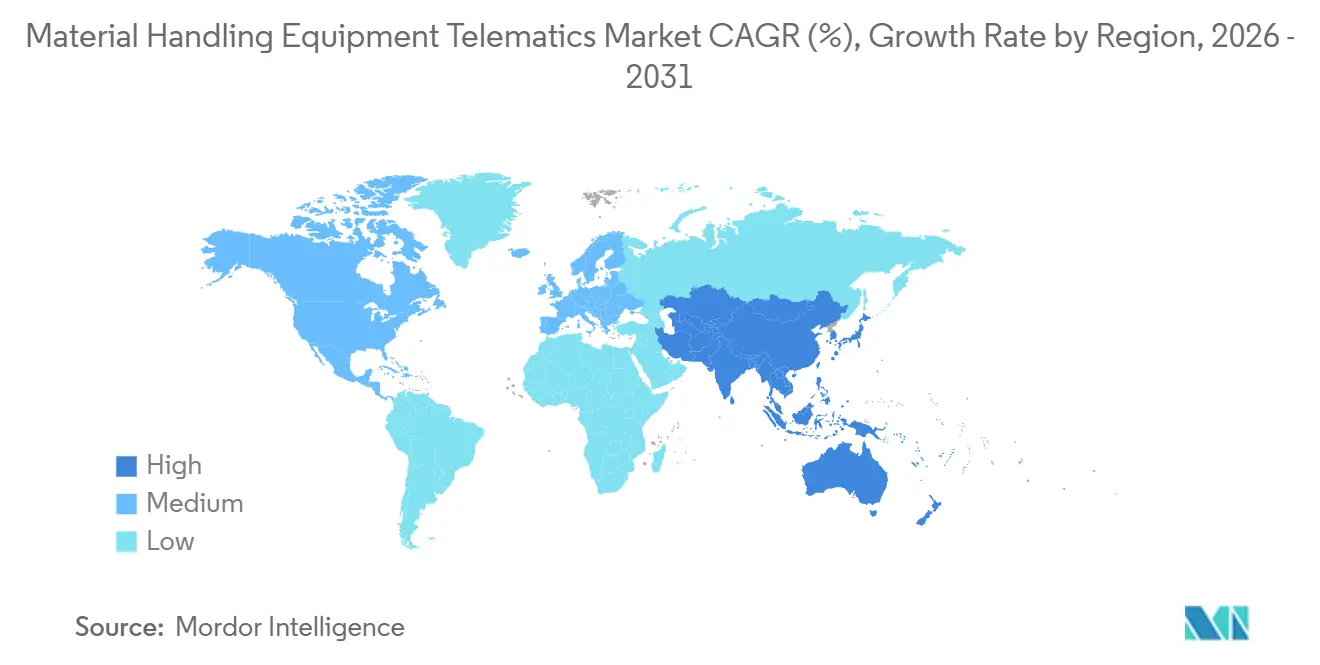

- By geography, North America held 38.54% share of the material handling equipment telematics, while Asia-Pacific is expected to grow at a 15.83% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Material Handling Equipment Telematics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Warehouse Automation And E-Commerce Fulfillment Density | +3.1% | Global, with concentrated gains in North America, Europe, and APAC core, China, India, South Korea | Short term (≤ 2 years) |

| Growing Need For Fleet Utilization And Downtime Reduction | +2.6% | Global, highest adoption pressure in North America and Western Europe | Short term (≤ 2 years) |

| Expansion Of Cloud, IoT, And AI-Enabled Remote Diagnostics | +2.3% | Global, with early scaling in North America and Europe, and rapid uptake in APAC | Medium term (2-4 years) |

| Tightening Safety And Compliance Requirements For Powered Industrial Trucks | +1.9% | North America and EU core, with growing influence in Japan, South Korea, and Australia | Short term (≤ 2 years) |

| Telematics Integration With WMS And Intralogistics Orchestration Platforms | +1.5% | North America and Europe, with spillover to India and Southeast Asia | Medium term (2-4 years) |

| Lithium-Ion Battery Analytics Becoming A Fleet Control Layer | +1.2% | Global, accelerated in markets with strong electric fleet transition policies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Warehouse Automation And E-Commerce Fulfillment Density

The material handling equipment telematics market is gaining traction in warehouse environments that now operate under tighter throughput targets and higher equipment density. As facilities add more automation, more assets must be continuously monitored so managers can see utilization, congestion points, and safety events in real time. That need is pushing telematics beyond location tracking and into a wider control role across forklift, robot, and dock activity. OneTrack states that AI-driven fleet intelligence can reduce fleet costs by 15-25% by identifying excess capacity and underused equipment, which fits the current drive toward tighter fleet sizing.[1]Intelligent Flying Machines Inc., “Forklift Fleet Management Software | AI Monitoring | OneTrack,” OneTrack, onetrack.ai The material handling equipment telematics market is responding well to this shift because unmonitored equipment now creates a larger operational risk in high-density fulfillment settings. As a result, telematics is becoming part of the operating logic of automated warehouses rather than a separate monitoring tool.

Growing Need For Fleet Utilization And Downtime Reduction

The rising cost of avoidable downtime in fast-moving warehouse and plant operations is also lifting the material handling equipment telematics market. Operators increasingly want systems that show which vehicles are idle, which units are overworked, and where maintenance risk is building before a failure interrupts a shift. This is changing buying priorities from simple visibility toward utilization management and preventive action. MHS Lift notes that predictive maintenance in forklift fleets relies on continuous monitoring of machine health indicators so teams can address issues before they become breakdowns. In practical terms, the material handling equipment telematics market is gaining strength because right-sizing and maintenance planning often deliver value faster than broader automation projects. That shorter payback cycle makes telematics easier to justify in facilities that need quick operational gains.

Expansion Of Cloud, IoT, And AI-Enabled Remote Diagnostics

Cloud platforms, IoT sensors, and AI models are moving the material handling equipment telematics market toward a split architecture in which some actions occur on the vehicle and broader analysis occurs across sites. This matters because many material-handling tasks take place indoors, where response speed is critical and continuous cloud reliance is not always practical. Edge processing supports local decisions for speed control, hazard alerts, and collision avoidance, while cloud layers compare fleet behavior across facilities and shifts. Verizon states that its 5G Edge AGV Management offering uses on-site 5G and private mobile edge computing to support near-real-time fleet status and collision-avoidance analytics for robotic fleets. The material handling equipment telematics market is therefore shifting from isolated devices toward connected operating systems that combine local response with wider optimization. That architecture also supports more reliable remote diagnostics as fleets become more distributed and software-led.

Tightening Safety And Compliance Requirements For Powered Industrial Trucks

The material handling equipment telematics market continues to benefit from stricter safety requirements for powered industrial trucks and greater operator accountability. OSHA maintains detailed requirements under 29 CFR 1910.178 for powered industrial trucks, and those rules continue to shape inspection, training, and maintenance practices across U.S. facilities. Telematics platforms help operators translate those obligations into digital checklists, operator access controls, certification tracking, and impact records that can be reviewed quickly. That matters more in large fleets because paper-based processes become harder to manage as equipment counts rise across sites and shifts. The material handling equipment telematics market is also gaining from the fact that safety data now has value beyond compliance, since it can inform training, supervision, and internal performance management. This makes telematics useful both before and after an incident, broadening its role within risk management programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Retrofit, Integration, And Change-Management Costs | -1.7% | Global, most acute in SME-dominated markets in South America, Middle East, and Africa | Short term (≤ 2 years) |

| Cybersecurity And Data Governance Risks In Multi-Site Fleets | -1.2% | Global, with highest compliance burden in North America and Europe | Medium term (2-4 years) |

| Mixed-Fleet Interoperability Gaps Across OEM And Aftermarket Systems | -0.9% | Global, with heightened impact in large enterprises operating multi-brand fleets | Medium term (2-4 years) |

| Signal Degradation In Dense Metal-Rack And High-Interference Indoor Environments | -0.7% | Global, particularly limiting in automated high-rack warehouses and underground mining operations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Retrofit, Integration, And Change-Management Costs

High retrofit and integration costs remain a real brake on the material handling equipment telematics market, especially for operators running older equipment or mixed-brand fleets. Factory-fitted systems are easier to deploy, but many fleet owners still depend on legacy units that need additional hardware, custom wiring, and protocol bridging before data can be standardized. Integration becomes even more challenging when telematics must connect with warehouse management systems, ERP tools, and site-specific workflow rules. The challenge is not only capital spending; change management demands also rise when supervisors, technicians, and operators have to adopt new digital processes simultaneously. Smaller operators feel this pressure more sharply because they often lack in-house IT and OT support. These cost and implementation hurdles can delay decisions even when the long-term case for telematics is clear.

Cybersecurity And Data Governance Risks In Multi-Site Fleets

Cybersecurity risk is another significant restraint for the material handling equipment telematics market because connected fleets consolidate sensitive operational data in a single environment. The CISA advisory ICSA-25-140-11 identified a high-severity vulnerability, CVE-2025-4364, with a CVSS v4 score of 8.7, in a commercial fleet management system and demonstrated how weaknesses can expose sensitive information and administrative credentials. Large operators now have to think beyond device installation and build formal policies around access control, data retention, authentication, and platform oversight. Geotab also highlights cybersecurity management practices as a core requirement for telematics environments, which shows how security is becoming part of vendor evaluation rather than a separate IT discussion.[2]Geotab, “Cybersecurity Telematics Management Best Practices,” Geotab, geotab.com The material handling equipment telematics market can therefore face slower adoption when buyers believe governance controls are weaker than the value of the data being collected. That concern is strongest in multi-site operations where location data, operator identities, and maintenance records sit in the same connected stack.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Forklifts Anchor Share While AGVs Lift Growth

Forklifts held 41.28% of the material handling equipment telematics market share in 2025, making them the largest equipment category, as they remain central to logistics, manufacturing, retail, and cold-chain operations. Their lead also reflects long-standing OEM investment in embedded connectivity, operator management tools, and service-linked data layers. The Raymond Corporation states that its iWAREHOUSE Enterprise system combines vehicle certification management, impact notifications, and battery analytics into a single fleet intelligence platform.[3]The Raymond Corporation, “Forklift Fleet Management Software | Forklift Telematics,” The Raymond Corporation, raymondcorp.com Toyota Material Handling also positions MyInsights as a native telematics layer that supports compliance, usage visibility, and battery-related monitoring on connected forklifts. In the material handling equipment telematics market, cranes, telehandlers, and yard-oriented vehicles are increasingly adopting telematics features, but their adoption base is less standardized than forklifts. That difference keeps forklifts at the center of most fleet digitization programs.

AGVs are projected to grow at a 15.41% CAGR through 2031, making them the fastest-growing equipment category in the material handling equipment telematics market. Their telematics needs are structurally different because AGV systems depend on continuous coordination of routing, battery status, traffic logic, and task assignment. KINEXON states that its fleet manager for AMR and AGV environments supports centralized orchestration and VDA 5050 compatibility, reflecting the shift toward software-led fleet control. This is important because growth in AGVs does not simply add more connected vehicles; it expands the role of telematics into active intralogistics control. The material handling equipment telematics industry is therefore widening from operator-focused forklift monitoring toward machine-to-system orchestration across autonomous fleets. Aerial work platforms and earth-moving equipment in indoor or semi-indoor environments remain a smaller but emerging area where vendors are adapting telematics to more complex positioning needs.

By Solution Type: Fleet Management Holds The Core While Predictive Maintenance Gains Speed

Fleet management accounted for 34.36% of the material handling equipment telematics market in 2025, confirming its role as the base solution layer for most deployments. Buyers still tend to start with asset visibility, operator authentication, digital inspections, and usage dashboards before expanding into deeper analytics. That sequence matters because these basic functions lay the foundation for later safety, maintenance, and productivity applications. Toyota and Raymond both present telematics around this broader fleet management model, where compliance records, access control, and utilization visibility sit within a single operating view. In the material handling equipment telematics market, asset tracking and safety monitoring still absorb a large share of first-stage spending because they address urgent operational needs with a familiar payback path. Energy optimization is also becoming more visible as electric fleets expand and battery use has to be managed more carefully across shifts.

Predictive maintenance is expected to grow at a 15.56% CAGR through 2031, and this is where the material handling equipment telematics market is starting to reshape value capture. MHS Lift describes predictive maintenance as a model built on sensor data from engine temperature, battery condition, hydraulic performance, and other equipment health signals, enabling faults to be addressed before failure. That approach changes telematics from a monitoring tool into a cost-control tool because the most valuable outcome becomes avoided disruption rather than historical reporting. It also raises the importance of vendors that can turn raw readings into clear maintenance actions for technicians and managers. The material handling equipment telematics industry is therefore moving toward systems that prescribe what to do next rather than simply showing what has happened. Compliance requirements around equipment safety are also influencing design choices, which supports more structured and auditable predictive workflows.

By End-User Industry: Logistics Leads Demand While Construction Expands The Fastest

Logistics and warehousing held a 51.71% share in 2025, giving this segment the largest position in the material handling equipment telematics market because it consolidates fleet density, labor pressure, and safety exposure in a single setting. These facilities rely on forklifts, pallet movement, dock flows, and high asset utilization, creating a strong case for continuous visibility and digital controls. Powerfleet states that on-site IoT solutions for material handling focus on operator behavior, safety, and asset usage, all of which align closely with warehouse operating priorities. The segment also benefits from the fact that telematics can be used by operations, maintenance, and safety teams simultaneously, spreading its value across multiple decision-makers. In the material handling equipment telematics market, manufacturing and automotive remain important users because they need zone controls, internal traffic coordination, and traceable operator activity. This broad functional relevance helps logistics and warehouse sites remain the main center of demand.

Construction is forecast to grow at a 15.69% CAGR through 2031, making it the fastest-rising end-user segment in the material handling equipment telematics market. Growth here comes from a more varied asset base that includes telehandlers, cranes, earth-moving equipment, and support vehicles across dispersed and changing job sites, reflecting broader adoption trends in the construction machinery telematic market. Geotab introduced Geotab Build as a mixed-fleet management solution for the construction sector, demonstrating how telematics vendors are adapting platforms to combine on-highway and off-highway asset oversight in a single environment. These developments align with broader trends in the construction equipment telematics market. That platform direction matters because construction operators usually need visibility across equipment classes that were historically tracked in separate systems. The material handling equipment telematics market is also gaining traction in mining and terminal operations, though those use cases still face connectivity and indoor or underground positioning limitations. Even so, construction is expanding quickly because the operational benefit of unified fleet oversight is becoming easier to see on large project sites.

By Technology: GPS Stays Foundational While AI-Based Systems Advance Faster

GPS accounted for 44.22% of the market in 2025 and remained the foundational technology in the material handling equipment telematics market, as it continues to handle core location, route, and geofencing tasks across outdoor and large-footprint operations. GPS alone does not meet every telematics need, but it remains the first layer for many deployments and the reference point for broader data capture. IoT sensors then add machine-level detail on voltage, temperature, vibration, hydraulic pressure, and load conditions that location data cannot provide. Verizon notes that real-time AGV management depends on low-latency connectivity and continuous status data, which illustrates how location services now work alongside richer sensor and edge layers. In the material handling equipment telematics market, edge computing is becoming increasingly important because safety-critical decisions cannot always wait for cloud responses. This keeps GPS important, but increasingly as part of a larger and more connected technology stack.

AI-based predictive systems are projected to grow at a 16.02% CAGR through 2031, making them the fastest-growing technology segment in the material handling equipment telematics market. The driver here is not just more data, but the growing need to convert complex operating inputs into decisions that supervisors can act on quickly. AI tools are being used to anticipate failures, flag risk patterns, compare asset cohorts, and support autonomous response in selected workflows. Cargill’s private 5G scale-up with NTT DATA across 50 facilities illustrates how stable industrial connectivity is becoming a necessary base for wider AI use in operational settings. The material handling equipment telematics market is therefore moving from visibility to inference and prescription, which changes how buyers measure value. As those systems mature, vendors with stronger analytics layers are likely to hold a larger share of the premium end of the market.

By Distribution Channel: OEM Integration Dominates While Aftermarket Retrofitting Gains Pace

OEM-integrated telematics captured a 74.37% share in 2025, underscoring how strongly the material handling equipment telematics market still favors factory-fitted connectivity. OEM systems have an advantage because they can access vehicle data directly, preserve warranty alignment, and offer a simpler support model for large operators. Mitsubishi Forklift Trucks launched FleetVSiON in January 2026 as a cloud-based telematics platform built on Microsoft Azure IoT with digital checklists, maintenance planning data, and GPS tracking through standard API integration. Toyota continues to embed similar functions through MyInsights, including compliance tools and battery analytics within the vehicle environment. In the material handling equipment telematics market, this native integration gives OEM channels a strong starting position because operators can activate telematics without building a separate hardware stack. That said, the dominance of OEM channels does not remove the need for cross-brand visibility in older or more diverse fleets.

Aftermarket channels are expected to grow at a 15.97% CAGR through 2031, which makes them the fastest-expanding route in the material handling equipment telematics market. This growth reflects a large installed base of legacy equipment and mixed fleets that cannot be replaced quickly but still need centralized oversight. GemOne states that its Sapphire platform can be installed on any forklift make or model and supports connected visibility across more than 100,000 assets, which captures the appeal of vendor-neutral retrofits. ForkOn also presents its platform as a cloud telematics system for forklifts and AGVs that supports AI-led recommendations and access control in aftermarket deployments. The material handling equipment telematics market is therefore opening more space for suppliers that help operators unify older assets rather than replace them. The material handling equipment telematics industry will likely continue to see faster aftermarket growth as safety requirements and audit exposure push existing fleets toward faster adoption of instrumentation.

Geography Analysis

North America held 38.54% of the material handling equipment telematics market share in 2025. The region benefits from advanced warehouse infrastructure, strong OEM telematics penetration, and a regulatory environment that keeps safety documentation and operator control in focus. OSHA’s powered industrial truck standard continues to shape employer obligations around training, operation, and recordkeeping across warehouses and industrial sites. The United States remains the core demand center because fleets are larger, automation budgets are deeper, and multi-site operational oversight is more common. Canada and Mexico also add regional momentum as telematics expands across safety, visibility, and cross-border fleet operations.

Asia-Pacific is projected to grow at a 15.83% CAGR through 2031, making it the fastest-growing geography in the material handling equipment telematics market. The region is benefiting from manufacturing diversification, expanding e-commerce fulfillment networks, and broader investment in automated logistics infrastructure. India, South Korea, Southeast Asia, and parts of East Asia are creating new telematics opportunities, as greenfield facilities can adopt connected systems from the start rather than retrofitting older site layouts. That matters because new warehouses and industrial buildings can integrate fleet software, sensors, and digital workflows more cleanly than legacy operations. As a result, the material handling equipment telematics market is gaining traction across Asia-Pacific, not only from volume growth, but also from a more software-ready operating base.

Europe remains the third-largest region in the material handling equipment telematics market and stands out for its regulatory discipline and a mature provider ecosystem. Procurement standards in the region place significant emphasis on information security, interoperability, and documented operational controls. SYNAOS highlights its ISO 27001 certification for its intralogistics platform, reflecting the growing importance of security readiness in product qualification among buyers in Europe.[4]SYNAOS, “About The Platform,” SYNAOS, synaos.com Trackunit also expanded its partnership with Sunbelt Rentals UK and Ireland in late 2025, extending connected asset coverage through the IrisX platform in the off-highway sector. South America, the Middle East, and Africa are developing from a smaller base, where construction, mining, logistics, and port material handling equipment vehicle market investments are creating space for adoption, but retrofit costs and governance readiness still limit faster scaling.

Competitive Landscape

The material handling equipment telematics market shows moderate competitive intensity, with a mix of broad telematics platforms and specialist material handling providers competing across hardware, subscriptions, and analytics. Horizontally positioned players such as Geotab, Samsara, and Powerfleet use larger data ecosystems and partner networks to compete across on-road and industrial environments. Specialist providers such as GemOne, ELOKON, SIERA.AI, and Ubiquicom compete by offering deeper workflow features for forklifts and industrial vehicles, including access control, pedestrian proximity alerts, and site-specific fleet monitoring.[5]ELOKON GmbH, “ELOfleet, #1 MHE Asset Management Cloud Portal,” ELOfleet, elofleet.com This structure means a single vendor does not define the material handling equipment telematics market, because customers often compare platform breadth to equipment-specific functionality. It also explains why price pressure in hardware is pushing competition toward analytics quality, implementation speed, and system interoperability.

A major competitive opening in the material handling equipment telematics market is mixed-fleet interoperability, where buyers want one operating view across OEM systems, aftermarket devices, and older installed assets. Powerfleet addressed this in Release 26.7 by adding Samsara Level 1 and Geotab Level 2 integrations to its Unity platform, which directly supports unified visibility across existing telematics bases. GemOne’s aftermarket model is another example of a vendor using hardware-neutral deployment to widen its addressable fleet base. Geotab also strengthened its platform direction through hardware and AI upgrades announced in 2026, reinforcing the shift toward more layered fleet intelligence offerings. These moves show that the material handling equipment telematics market is rewarding vendors that reduce fragmentation for customers rather than adding another isolated data source. That priority is especially important in large enterprises that operate across sites, brands, and equipment classes.

Standards and adjacent technology providers are also shaping competition in the material handling equipment telematics market. SYNAOS and Navitec Systems both reference interoperability around AGV and AMR fleet control, which matters as autonomous and manual vehicles increasingly share the same operating space. Smaller challengers remain relevant where precision indoor positioning, condition monitoring, or specialized safety logic are more important than broad platform scale. Samsara’s asset-tracking expansion and passive network approach also point to a model in which visibility relies less on dedicated site infrastructure and more on distributed network effects. Overall, the material handling equipment telematics market is likely to keep rewarding vendors that combine strong integration, security credibility, and prescriptive analytics in a single usable system.

Material Handling Equipment Telematics Industry Leaders

PowerFleet, Inc.

ELOKON GmbH

GemOne NV

Davis Derby Limited

Litum Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: TELUS and Powerfleet launched Vision 360, an AI-powered 360-degree video telematics solution for fleet safety, designed to address Transport Canada's mandate for perimeter visibility systems on school buses by November 2027. Powerfleet data indicates the solution can reduce collision incidents by up to 60% and reduce insurance costs by up to 25%. The partnership integrates Powerfleet's video AI with TELUS' national network, offering cross-sector applicability, including material handling fleets.

- April 2026: ORBCOMM refinanced its existing debt facility, securing USD 460 million from Carlyle, Bain Credit's Private Credit Group, and Morgan Stanley Private Credit to accelerate market leadership in IoT connectivity for asset tracking and fleet management.

- April 2026: Positioning Universal's TT600 and TT603 solar-powered asset trackers became available through the Geotab Marketplace Order Now program, enabling direct procurement for construction, rental, logistics, and industrial markets. Positioning Universal also announced plans to expand the portfolio with the FJ2500, a wired telematics gateway for heavy equipment, later in 2026.

- March 2026: Geotab launched "Geotab Build," a telematics solution designed to unify mixed-fleet management in the construction industry by integrating on-highway vehicles with off-highway assets into a single environment. Early access was made available to strategic customers in Q2 2026, with general availability planned for Q4 2026.

Global Material Handling Equipment Telematics Market Report Scope

The Material Handling Equipment Telematics Market is Segmented by Equipment Type (Forklifts, Cranes, Automated Guided Vehicles (AGVs), Earth-moving Equipment, Telehandlers, Trucks, Tractors, and Aerial Work Platforms), Solution Type (Asset Tracking, Fleet Management, Predictive Maintenance, Safety and Compliance Monitoring, Energy Optimization, Operational Analytics, and Others), End-User Industry (Manufacturing, Logistics and Warehousing, Automotive, Construction, Mining, Transportation, and Others), Technology (GPS, IoT Sensors, AI-based Predictive Systems, Edge Computing, and 5G-enabled Telematics), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Forklifts |

| Cranes |

| Automated Guided Vehicles (AGVs) |

| Earth-moving Equipment |

| Telehandlers |

| Trucks |

| Tractors |

| Aerial Work Platforms |

| Asset Tracking |

| Fleet Management |

| Predictive Maintenance |

| Safety and Compliance Monitoring |

| Energy Optimization |

| Operational Analytics |

| Other Solution Types |

| Manufacturing |

| Logistics and Warehousing |

| Automotive |

| Construction |

| Mining |

| Transportation |

| Other End-User Industries |

| GPS |

| IoT Sensors |

| AI-based Predictive Systems |

| Edge Computing |

| 5G-enabled Telematics |

| OEM (Original Equipment Manufacturer) |

| Aftermarket |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Israel | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Equipment Type | Forklifts | |

| Cranes | ||

| Automated Guided Vehicles (AGVs) | ||

| Earth-moving Equipment | ||

| Telehandlers | ||

| Trucks | ||

| Tractors | ||

| Aerial Work Platforms | ||

| By Solution Type | Asset Tracking | |

| Fleet Management | ||

| Predictive Maintenance | ||

| Safety and Compliance Monitoring | ||

| Energy Optimization | ||

| Operational Analytics | ||

| Other Solution Types | ||

| By End-User Industry | Manufacturing | |

| Logistics and Warehousing | ||

| Automotive | ||

| Construction | ||

| Mining | ||

| Transportation | ||

| Other End-User Industries | ||

| By Technology | GPS | |

| IoT Sensors | ||

| AI-based Predictive Systems | ||

| Edge Computing | ||

| 5G-enabled Telematics | ||

| By Distribution Channel | OEM (Original Equipment Manufacturer) | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the material handling equipment telematics market?

The material handling equipment telematics market stood at USD 8.41 billion in 2026 and is projected to reach USD 17.17 billion by 2031 at a 15.35% CAGR.

Which equipment category leads adoption in connected fleet systems for material handling?

Forklifts led adoption with 41.28% share in 2025 because they remain the most widely used vehicles across warehousing, manufacturing, retail, and cold-chain operations.

Which solution area is expanding the fastest in connected material handling fleets?

Predictive maintenance is the fastest-growing solution, with a 15.56% CAGR through 2031, as operators focus more on reducing failures and avoiding downtime.

Why is North America the largest regional demand center for telematics in material handling fleets?

North America led with 38.54% share in 2025 because of stronger warehouse automation, broad OEM integration, and tighter enforcement around powered industrial truck safety.

What is driving faster growth in Asia-Pacific for these fleet intelligence systems?

Asia-Pacific is projected to grow at 15.83% through 2031, supported by manufacturing relocation, new fulfillment infrastructure, and greater investment in automated logistics sites.

Why are aftermarket telematics platforms gaining traction in older fleets?

Aftermarket channels are forecast to grow at 15.97% through 2031 because operators with mixed-brand and legacy fleets need vendor-neutral visibility without replacing working equipment.

Page last updated on: