Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

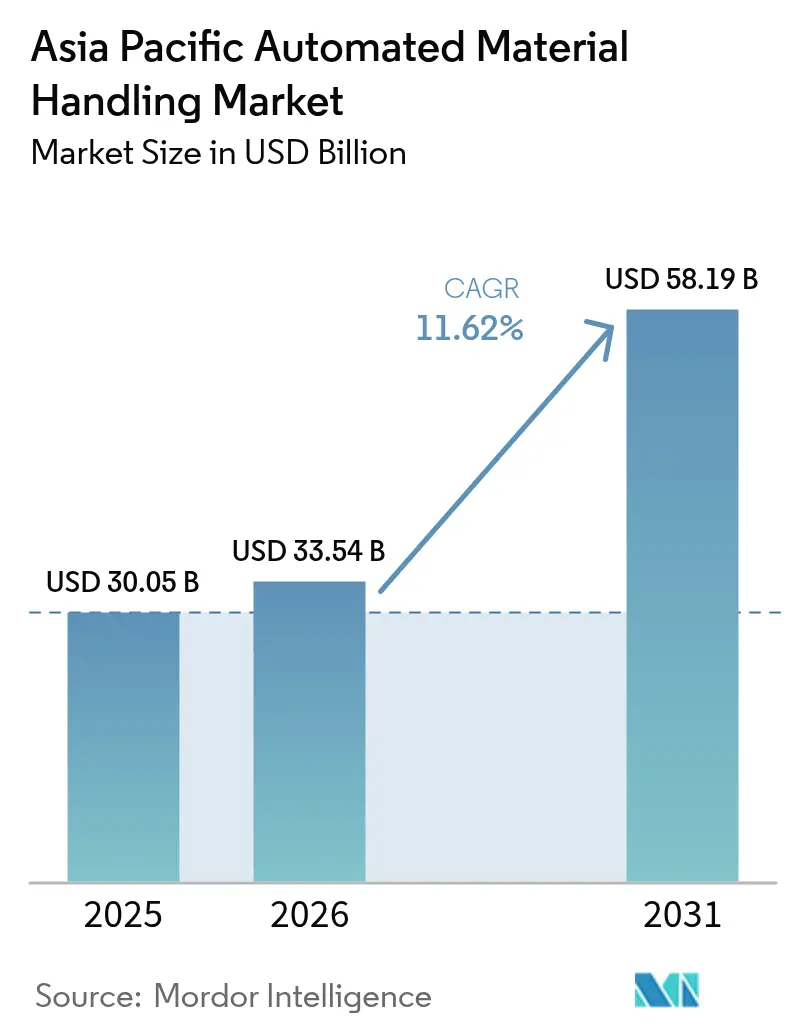

| Base Year Market Size (2025) | USD 30.05 Billion |

| Market Size (2026) | USD 33.54 Billion |

| Market Size (2031) | USD 58.19 Billion |

| Growth Rate (2026 - 2031) | 11.62% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia Pacific Automated Material Handling Market Analysis by Mordor Intelligence

Asia Pacific automated material handling market size in 2026 is estimated at USD 33.54 billion, growing from 2025 value of USD 30.05 billion with 2031 projections showing USD 58.19 billion, growing at 11.62% CAGR over 2026-2031. Rapid digitalization of regional logistics networks, steady Industry 4.0 rollouts, and persistent e-commerce growth underpin this expansion. Capital programs such as China’s USD 1.4 trillion Manufacturing 2025 initiative and ASEAN’s Digital Economy Framework Agreement push factories and warehouses to embed autonomous equipment that bridges information and physical flows. Hardware continues to dominate spending, yet software accelerates fastest as operators pivot toward data-driven orchestration. Mobile robots lead equipment adoption because they reconfigure quickly when order profiles shift, while labor shortages in developed economies and compliance mandates in pharmaceuticals strengthen the business case for autonomy. China retains the largest regional share, but India now delivers the highest growth rate as production-linked incentives stimulate automation investments.

Key Report Takeaways

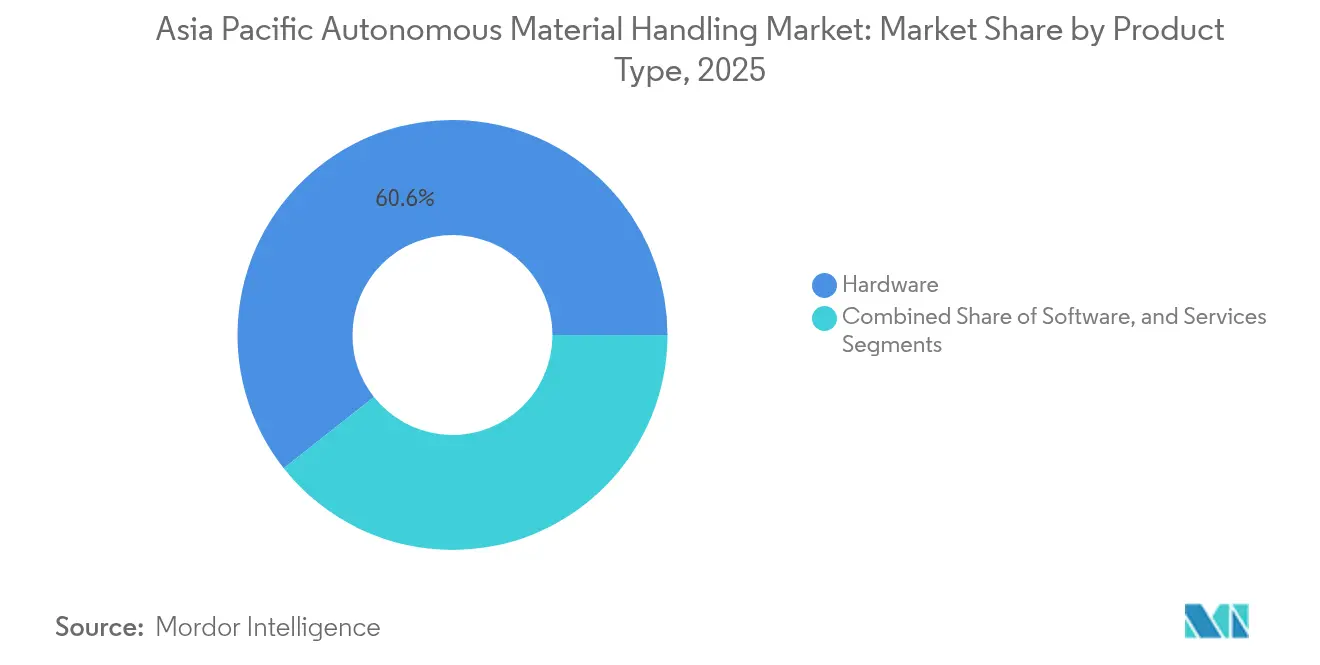

- By product type, hardware captured 60.63% share of the Asia Pacific automated material handling market size in 2025; software is forecast to expand at a 13.32% CAGR to 2031.

- By equipment type, mobile robots held 33.22% share of the Asia Pacific automated material handling market size in 2025, while automated storage and retrieval systems are projected to grow at 10.86% CAGR through 2031.

- By end-user vertical, retail, warehousing, and distribution commanded a 27.41% share of the Asia Pacific automated material handling market size in 2025; pharmaceuticals will post the fastest 11.89% CAGR between 2026 and 2031.

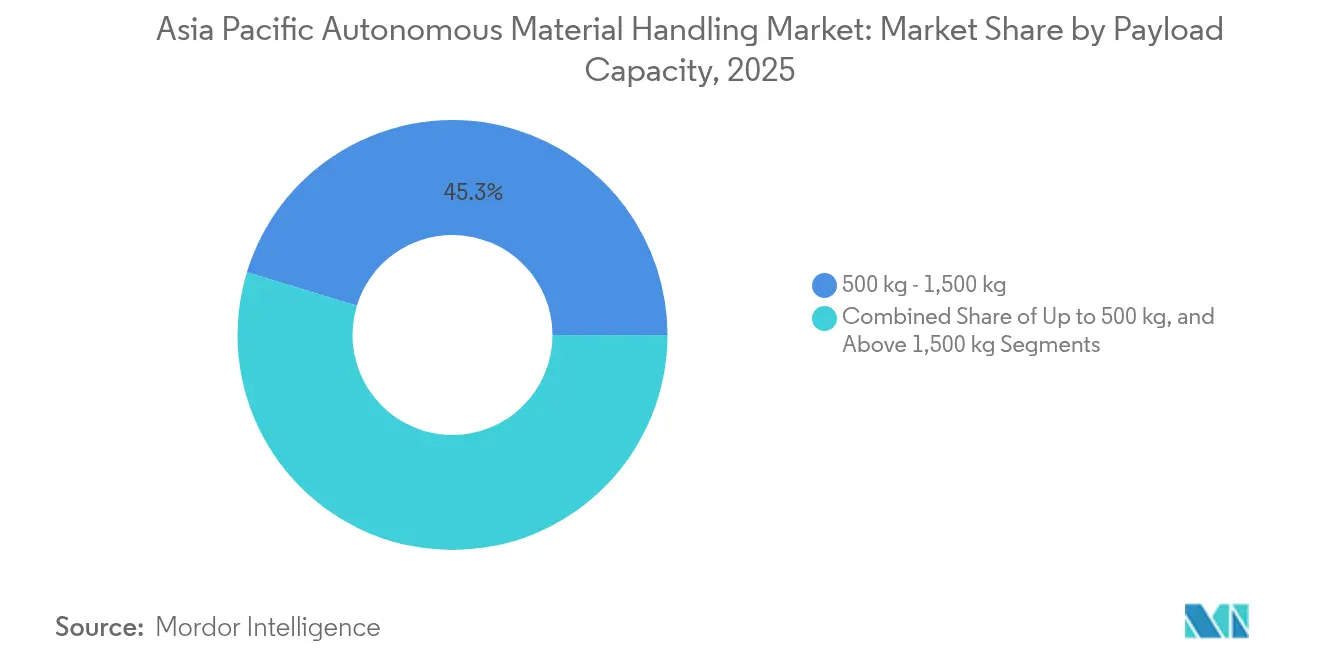

- By payload capacity, 500 kg-1,500 kg systems led with 45.28% share of the Asia Pacific automated material handling market size in 2025, whereas sub-500 kg platforms are expected to grow at a 13.18% CAGR.

- By navigation technology, laser guidance maintained a 37.45% share of the Asia Pacific automated material handling market size in 2025; SLAM-based natural feature guidance is projected to rise at a 12.08% CAGR to 2031.

- By region, China accounted for 41.92% share of the Asia Pacific automated material handling market size in 2025; India is projected to advance at a 12.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia Pacific Automated Material Handling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Industry 4.0 Investments in Logistics Facilities | +2.8% | China, Japan, South Korea, Singapore | Medium term (2-4 years) |

| Proliferation of E-Commerce Fulfillment Centers | +3.1% | China, India, Southeast Asia | Short term (≤2 years) |

| Rapid Adoption of Autonomous Mobile Robots in Warehousing | +2.4% | Core Asia-Pacific markets | Medium term (2-4 years) |

| Rising Labor Cost and Scarcity in Asia Pacific | +2.2% | Japan, South Korea, Singapore, urban China | Long term (≥4 years) |

| Government Incentives for Smart Industrial Parks in ASEAN | +1.1% | Thailand, Malaysia, Indonesia, Vietnam | Medium term (2-4 years) |

| Integration of 5G Private Networks Enabling Real-Time Fleet Coordination | +0.4% | China, South Korea, Japan, Singapore | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Increasing Industry 4.0 Investments in Logistics Facilities

Regional manufacturers channel record budgets into cyber-physical upgrades that unite production lines, warehouse control systems, and enterprise software. China’s annual smart-factory spend already exceeds USD 200 billion, while Japan’s Society 5.0 program earmarks USD 130 billion for industrial IoT.[1]China State Council, “Made in China 2025 Strategy,” gov.cn These commitments translate directly into orders for autonomous tuggers, shuttles, and forklifts that synchronize material flows with real-time planning systems. Singapore’s Smart Nation agenda shows how public co-investment catalyzes adoption: 40% of the city-state’s warehouses had deployed autonomous mobile robots by 2024. Operators now view integrated material handling as a prerequisite for extracting promised Industry 4.0 efficiency gains.

Proliferation of E-Commerce Fulfillment Centers

Asia Pacific online retail penetration rose to 18.3% of total sales in 2024, outpacing all other regions. Massive order surges compress delivery windows, forcing fulfillment hubs to automate picking, sorting, and dispatch. China’s 2024 Singles Day moved 1.48 billion parcels within 24 hours, a feat achievable only through high-throughput autonomous fleets. Platforms such as JD.com now operate more than 1,000 automated warehouses, prompting regional peers Shopee and Lazada to replicate similar robotics playbooks.[2]JD Logistics, “JD Logistics Announces Third Quarter 2024 Results,” ir.jd.com Each new fulfillment node spurs parallel investments in upstream and downstream logistics sites, sustaining a virtuous demand cycle for autonomous solutions.

Rapid Adoption of Autonomous Mobile Robots in Warehousing

Pilot projects have matured into deployments counted in the thousands. Leading providers report productivity gains of 200%-400% over manual picking, mainly through travel-time reduction and real-time task allocation. Geek+ alone has shipped over 30,000 robots across the Asia Pacific.[3]Geek+ Technology, “Geek+ Completes Series E Funding Round of Over USD 100 Million,” geekplus.com Chinese innovators VisionNav and Quicktron supply localized variants that address narrow aisles, mezzanine levels, or outdoor yards, broadening potential use cases. Facility managers prefer AMRs because they re-route easily when SKU mixes or peak seasons change, protecting automation investments against demand volatility.

Rising Labor Cost and Scarcity in the Asia Pacific

Demographics tighten warehouse labor pools in mature economies. Japan faces an estimated 2.8 million shortfall in logistics personnel, and South Korean warehouse wages inflate at roughly 15% each year. Singapore’s foreign-labor quotas amplify the crunch, urging firms to maintain throughput with 30% fewer workers. Autonomous fleets now deliver payback within 18 months, a dramatic improvement from 36 months in 2020. For many operators, robots have shifted from optional efficiency upgrades to essential continuity tools.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Capex of Integrated Automation Projects | -1.8% | Emerging Asia-Pacific economies, SME segments | Short term (≤2 years) |

| Limited Interoperability Standards Across Vendor Ecosystems | -1.2% | Global multi-vendor sites | Medium term (2-4 years) |

| Delayed Port Infrastructure Digitalization in Emerging Economies | -0.8% | Indonesia, Thailand, Malaysia, Philippines | Long term (≥4 years) |

| Data Security Concerns in Cloud-Managed Fleets | -0.6% | Regulated industries worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capex of Integrated Automation Projects

Deploying end-to-end systems often requires USD 2-5 million for a mid-size site, excluding building modifications and change-management costs. Indonesian warehouses earning under USD 10 million annually view such commitments as 25%-50% of yearly turnover. Financing channels remain limited, and robotics-as-a-service plans, while reducing entry fees, can inflate the total cost of ownership. Until equipment prices fall or credit access widens, smaller operators may delay adoption, moderating overall market growth.

Limited Interoperability Standards Across Vendor Ecosystems

Warehouse managers integrating conveyors, AMRs, and shuttle systems from different suppliers encounter proprietary interfaces that complicate command hand-offs. The Industrial Internet Consortium promotes open frameworks, yet intellectual-property concerns keep major vendors invested in closed architectures. As software intelligence grows more valuable than hardware, vendors guard algorithms that orchestrate fleets, hindering cross-brand collaboration. Interoperability challenges increase integration timelines and costs, deterring buyers who favor incremental expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Software Drives Intelligence Revolution

Hardware held 60.63% of the Asia Pacific automated material handling market share in 2025, reaffirming that physical assets still anchor operations. Yet software revenue will climb at a 13.32% CAGR through 2031 as enterprises pursue data-centric performance boosts. The autonomous material handling market size for software is projected to widen each year as predictive maintenance, energy optimization, and AI-based routing stack on top of existing fleets. Services revenues grow steadily because rising system complexity pushes demand for consulting, integration, and lifecycle support. Vendors such as KION expanded into software by acquiring Dematic, illustrating how mechanical-first firms pivot toward holistic solutions.

Hardware growth decelerates from the 2019-2024 period because many first-wave installations are complete. Operators now refine returns through software-enabled tweaks rather than large capital swaps. Regulatory focus also shifts toward firmware safety checks in ISO 3691-4, amplifying the value of code quality over steel strength. As regional networks mature, software-centric offerings should capture incremental budgets while hardware refresh cycles lengthen, deepening the installed base’s stickiness.

By Equipment Type: Mobile Robots Lead Flexibility Revolution

Mobile robots controlled 33.22% of equipment demand in 2025 and will grow at a 12.21% CAGR through 2031. These platforms lower entry barriers because they require minimal fixed infrastructure, enabling brownfield sites to automate aisles without costly retrofits. Within the Asia Pacific automated material handling market size for equipment, automated storage and retrieval systems (ASRS) still corner high-density use cases, while conveyors remain indispensable for bulk flow. Nonetheless, AMRs win share by excelling in variable SKUs and rapid SKU expansion environments.

The shift from automated guided vehicles to natural-navigation AMRs underscores a broader preference for flexibility. AMRs equipped with vision sensors and AI algorithms plot adaptive routes, sidestepping rigid guidepaths. Fixed systems still serve profitable niches, especially where high throughput outweighs change frequency. Yet survey data confirm budget allocations moving toward software-rich mobile platforms that integrate seamlessly with warehouse execution systems. Compliance with IEC 61508 functional safety elevates trust in mobile options across regulated industries.

By End-User Vertical: Pharmaceuticals Emerge as Growth Leader

Retail, warehousing, and logistics centers accounted for 27.41% of 2025 demand, benefiting from early e-commerce automation waves. However, pharmaceuticals will grow fastest at 11.89% CAGR as serialization laws mandate end-to-end traceability. The Asia Pacific automated material handling market size earmarked for pharmaceutical operations expands because temperature-controlled picking and dispensing demand high precision. Cold-chain obligations and contamination risk discourage manual handling, turning autonomous shuttles and AMRs into compliance enablers.

Automotive plants maintain a robust baseline owing to just-in-time production disciplines, while food and beverage factories balance hygiene with throughput. Airports adopt baggage-handling AMRs to address surging passenger volumes. In post and parcel, national posts modernize to combat private couriers’ speed advantage. As drug regulations tighten across China and India, pharmaceutical warehouses will deploy redundant sensor layers and validation software, widening the lead over retail in absolute spending by decade’s end.

By Payload Capacity: Light Systems Drive E-Commerce Adaptation

Platforms rated for 500 kg-1,500 kg commanded 45.28% of 2025 flows, offering versatility across consumer goods and automotive parts. Yet sub-500 kg units will compound at 13.18% CAGR through 2031, mirroring parcel profiles that trend toward lighter, high-velocity orders. As cross-border e-commerce grows, pick faces carry smaller cartons to shuttle zones, making compact robots ideal. Operators thus re-optimize grids for speed rather than tonnage.

Heavy-payload robots above 1,500 kg serve niche metal fabrication or pallet sequencing, but slow 10.52% CAGR. Manufacturing footprints gradually orient toward finished goods rather than raw bulk, decreasing average item weight. ASEAN incentives under the Regional Comprehensive Economic Partnership propel consumer-product plants that mostly ship lighter SKUs, reinforcing the tilt toward lower-capacity fleets. Facility designers now plan multi-tier mezzanines where small bots travel vertical lifts, compressing cubic utilization without sacrificing cycle time.

By Navigation Technology: SLAM Gains Ground on Traditional Methods

Laser guidance preserved a 37.45% share in 2025, prized for millimeter accuracy inside purpose-built aisles. Yet SLAM-based natural feature navigation is poised to outpace all other formats at 12.08% CAGR because it dispenses with reflectors or magnetic tape. The Asia Pacific automated material handling market share commanded by SLAM systems gains momentum where floor plans evolve frequently, such as 3PL multipurpose warehouses.

Magnetic and wire guidance survive in price-sensitive facilities, while vision guidance tackles irregular environments like yard operations. SLAM elevates human-machine collaboration because robots interpret dynamic obstacles without external beacons, fulfilling ISO 13482 stipulations for human-shared spaces. As AI vision components drop in cost, operators reassess total lifetime economics and lean toward navigation technologies that cut infrastructure upkeep, tilting future rollouts decisively toward SLAM.

Geography Analysis

China generated 41.92% of regional value in 2025, buoyed by vertically integrated robotics supply chains and ample subsidy pools under Manufacturing 2025. Domestic brands accelerate iteration cycles by colocating R&D, component manufacturing, and user pilots within single economic zones, compressing concept-to-commercial timelines. Japan and South Korea rank next, focusing on mitigating chronic labor shortages through advanced fleets that merge AMRs with 5G private networks for ultra-reliable low-latency control.

India represents the fastest-growing territory, advancing at 12.19% CAGR through 2031. The Production Linked Incentive scheme injects USD 26 billion into automation expenditures, while fast-growing middle-class consumption swells domestic e-commerce nodes. Multinationals open greenfield factories to hedge supply-chain concentration, driving parallel warehouse investments that embed autonomous sorters and forklifts from day one.

Emerging ASEAN markets, including Indonesia, Thailand, Vietnam, and Malaysia, are scaling adoption behind tax holidays and import duty waivers for robotics under smart-industrial-park programs. Thailand’s Board of Investment grants up to 13-year corporate tax exemptions to autonomated material handling deployments, stimulating uptake in automotive clusters. Singapore anchors regional innovation as a demonstration hub, having reached 40% warehouse automation penetration by 2024. Australia and Taiwan occupy specialized niches: miners automate heavy-duty haulage while semiconductor fabs require wafer-handling precision far exceeding general manufacturing tolerances.

Regulatory Landscape

Safety, cybersecurity, and logistics-standardization requirements increasingly shape AMH deployments across Asia Pacific, particularly for AMRs/AGVs operating in mixed-traffic warehouses. China issued GB/T 45750-2025 (Automated guided vehicle safety specification) in May 2025, with implementation beginning in December 2025, creating a concrete compliance reference for warehouse logistics equipment alongside broader industrial-truck safety standards such as GB/T 10827.4-2023.

In 2026, policy direction tightened around logistics digital transformation and governance of autonomous systems. Japan METI released the Comprehensive Physical Distribution Policy Outline (FY2026 to FY2030) in March 2026, reinforcing logistics DX and GX standardization as a national agenda item. Singapore advanced governance guardrails relevant to cloud-managed, AI-enabled fleets through IMDA's agentic AI governance framework (February 2026), and it continues to point implementers to Singapore Standards Council TR 104-2022 for safe use of AMRs in warehouses. Australia also anchors safety compliance for driverless industrial trucks via AS/NZS ISO 3691.4:2023, which is referenced by workplace safety inspections in practice.

Value Chain Analysis

The AMH value chain in Asia Pacific runs from upstream components (motors, drives, controllers, sensors, batteries, and compute modules) to OEM design and manufacturing (AMRs/AGVs, ASRS, conveyors, sorters), followed by software layers (WMS/WCS/WES, fleet orchestration, simulation, and analytics). It then covers system integration, commissioning, and lifecycle services (spares, uptime contracts, upgrades, and cybersecurity patching). Component and control-system procurement ties the chain to semiconductor availability, while the highest value capture is increasingly concentrated in orchestration software and integration know-how that connects multi-vendor fleets to facility IT and ERP.

Downstream, large e-commerce and 3PL users drive project scope definition and acceptance testing, and scale contracts shape supplier selection and local capacity commitments. DAIFUKU's large automation contract for an Alibaba fulfillment hub in Hangzhou (announced November 2024) and KION Group's announced expansion of its Jinan, China automated material handling plant (January 2025) both illustrate how regional demand links to localized manufacturing, engineering, and service networks. In Japan, partnerships that connect warehouse software to execution platforms, such as Fujitsu and YE DIGITAL working to address logistics labor shortages (January 2024), show how software and integration partners sit between equipment makers and end users to operationalize automation outcomes.

Competitive Landscape

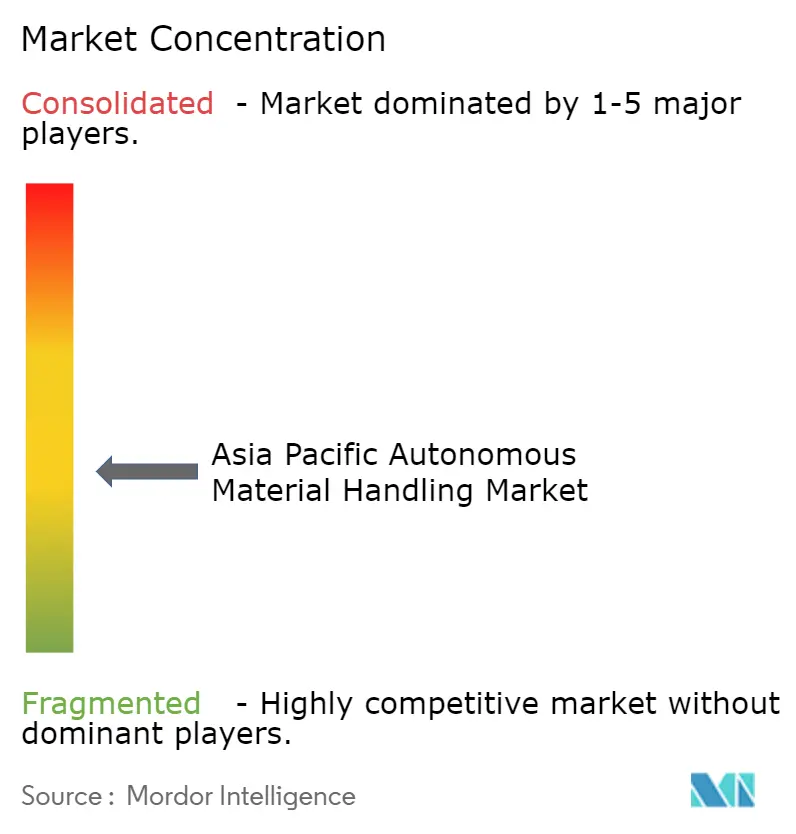

The Asia Pacific automated material handling market shows moderate concentration where global conglomerates coexist with fast-scaling regional specialists. DAIFUKU, KION Group, and Jungheinrich leverage broad portfolios and deep service reach to secure multi-country rollouts for blue-chip customers. Chinese challengers Geek+, Quicktron, VisionNav, and Hai Robotics expand aggressively by customizing solutions for local operating conditions and competing on total cost of ownership.

Strategic plays cluster into three templates. First, global integration: KION acquired Dematic to blend equipment with warehouse execution software, offering turnkey deliverables that reduce integration risk for enterprise accounts. Second, regional specialization: VisionNav centers on autonomous forklifts suited to high-humidity Southeast Asian climates, while Hai Robotics optimizes tote-handling solutions for Chinese e-grocers. Third, technology partnerships: Toyota Industries pairs with SoftBank to embed 5G modules into forklifts, jointly monetizing private-network ecosystems.

Product differentiation pivots increasingly on software. Vendors race to refine traffic simulators, predictive maintenance algorithms, and multi-agent orchestration platforms that boost fleet utilization. Hardware reliability remains essential, yet buyers now scrutinize API openness and cybersecurity certifications such as ISO 27001. Service scope also shapes bids as lifecycle contracts extend 10-15 years. Against this backdrop, vendors able to balance mechanical robustness, advanced analytics, and responsive field service capture share in a market gradually consolidating around full-stack capability.

Asia Pacific Automated Material Handling Industry Leaders

DAIFUKU Co., Ltd.

Kardex Holding AG

KION GROUP AG

John Bean Technologies Corporation

JUNGHEINRICH AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A core whitespace remains in scaling AMH beyond early-adopter mega hubs into standardized, repeatable deployments for mid-sized warehouses and multi-tenant facilities, where capex sensitivity and integration complexity continue to slow adoption. Programs that reduce technical and financial friction create near-term entry points for modular automation: Singapore's A*STAR National Robotics Programme received a new SGD 60 million funding tranche in 2024 to translate robotics into manufacturing and logistics use cases, and Thailand BOI continues to promote automation and robotics investments through tax incentives, including for integration and control system design.

Software-forward deployments are also expanding, particularly those focused on interoperability and governance of AI-enabled fleets, where buyer scrutiny centers on safety validation and cyber risk in cloud-managed operations. On the supply side, announced industrial investments point to ecosystem building around robotics and smart manufacturing in Southeast Asia: in July 2026, Priver Technology (M) Sdn Bhd commenced construction of a manufacturing facility in Senai Airport City, Johor, focused on AI infrastructure, robotics, and smart manufacturing systems. For end-user demand, high-throughput e-commerce fulfillment continues to pull spend, with large-scale automated-warehouse footprints already established by platforms such as JD.com, which operates more than 1,000 automated warehouses, supporting ongoing demand for AMRs, sortation, and warehouse-execution software across new nodes and retrofit programs.

Recent Industry Developments

- July 2026: Colruyt Group and KION Group launched a joint R&D center focused on next-generation supply chain robotics. The initiative strengthens KION's software and robotics development pipeline and supports faster co-innovation with a large retail and distribution operator.

- May 2026: Daifuku announced a JPY 52 billion growth investment program for 2026-2029, covering plant redevelopment and the acquisition of Eisenmann (Germany) for its automotive business. The program broadens Daifuku's capability set and increases capacity and solution depth that can be transferred into Asia Pacific programs through global engineering and sourcing leverage.

- April 2025: Daifuku started full-scale operations at a new manufacturing plant in Hyderabad, India, designed to quadruple regional production capacity for AS/RS, sorters, and conveyors. Localized production supports shorter lead times and service responsiveness for Indian and broader South Asia customer rollouts.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the Asia Pacific automated material handling (AMH) market includes equipment, related software, and supporting services used to move, store, sort, and track materials in factories, warehouses, and distribution operations across Asia Pacific.

Scope exclusions: We exclude non-automated, fully manual handling equipment and general building infrastructure that is not directly part of automated material movement or storage.

Segmentation Overview

- By Product Type

- Hardware

- Software

- Services

- By Equipment Type

- Mobile Robots

- Automated Guided Vehicles (AGV)

- Automated Forklift

- Automated Tow / Tractor / Tug

- Unit Load

- Assembly Line

- Special Purpose

- Autonomous Mobile Robots (AMR)

- Laser Guided Vehicle

- Automated Guided Vehicles (AGV)

- Automated Storage and Retrieval System (ASRS)

- Fixed Aisle (Stacker Crane + Shuttle System)

- Carousel (Horizontal Carousel + Vertical Carousel)

- Vertical Lift Module

- Automated Conveyor

- Belt

- Roller

- Pallet

- Overhead

- Palletizer

- Conventional (High Level + Low Level)

- Robotic

- Sortation System

- Mobile Robots

- By End-User Vertical

- Airport

- Automotive

- Food and Beverage

- Retail / Warehousing / Distribution / Logistics Centers

- General Manufacturing

- Pharmaceuticals

- Post and Parcel

- Other End-User Verticals

- By Payload Capacity

- Up to 500 kg

- 500 kg - 1,500 kg

- Above 1,500 kg

- By Navigation Technology

- Laser Guidance

- Vision Guidance

- Magnetic Tape / Wire Guidance

- Natural Feature Guidance (SLAM)

- By Region

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Thailand

- Singapore

- Malaysia

- Taiwan

- Rest of Asia Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started by mapping where AMH demand originates in Asia Pacific and how buyers typically procure these systems. We relied on public sources such as national statistics agencies for industrial output, trade ministries and customs portals for machinery trade flows, and central bank releases for inflation and exchange rate timing.

To anchor assumptions around end-use activity, we also reviewed association and public-domain inputs, including regional logistics and warehousing bodies, plus port and airport throughput statistics. We included peer-reviewed papers on warehouse automation and robotics adoption to cross-check adoption patterns.

Company annual reports, investor presentations, and product catalogs were used to understand the offer mix across hardware, software, and services, and how pricing tends to vary with system complexity. Where needed, paid subscription sources for company financials and news, along with a patent database and shipment-level import-export data, were used to confirm timelines, installation momentum, and country-level intensity. These examples are indicative only, and we reviewed additional sources for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work focused on confirming what is actually getting installed and why, especially across warehouses, post and parcel networks, automotive plants, electronics lines, and pharmaceuticals. We spoke with a mix of system suppliers, integrators, component partners, and end-user operations teams across APAC. The discussions were then used to test adoption rates, typical project sizes, and the share of software and services attached to equipment deals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 13% | |

| Mid tier: 59% | Functional/Unit leaders: 39% | |

| Smaller Players: 15% | Managers: 48% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where automation spend is reconstructed from the demand pool in key end-use settings, and then allocated into AMH equipment, software, and services based on observed buying patterns. For example, warehousing expansion, e-commerce parcel volumes, manufacturing output, and new facility additions were used to infer where automation budgets are likely to rise.

The model uses practical inputs that can be checked and updated, such as warehouse and distribution center build-outs, throughput growth in post and parcel, labor cost pressure and availability, manufacturing investment cycles in automotive and electronics, and typical system replacement or upgrade rhythms. Assumptions on average project value were kept grounded by ranges gathered in interviews, followed by adjustments for country mix and system type mix (such as mobile robots, ASRS, conveyors, palletizers, and sortation).

For forecasting, scenario analysis was applied so near-term expansions, delayed capex cycles, and faster adoption cases could be compared, and then narrowed to the most realistic path using expert views. Bottom-up approximations were used as a check, including sampling installations by end-use and applying realistic price bands to volumes. Any gaps were handled by conservative interpolation when coverage was thin in smaller countries or niche applications.

Data Validation & Update Cycle

Outputs were cross-checked against independent signals such as industrial machinery trade direction, warehouse automation activity cues, and the implied spend per facility in large end-user groups. When a country or end-use result looked out of line, the drivers were re-tested, and follow-up calls were used to confirm whether the discrepancy came from adoption rates, pricing, or scope interpretation.

Before sign-off, the model goes through stepwise analyst reviews so inputs, conversions, and year-on-year movements stay consistent and explainable. Reports are refreshed annually, and interim updates are made when material events shift demand, supply, or pricing. Right before delivery, a final pass is done so clients receive the latest updated view based on the most recent public releases and fresh primary checks.

Mordor Intelligence's Asia Pacific Automated Material Handling Amh Market Size Measured Against Other Published Estimates

Published market sizes for APAC AMH can differ more than expected because each publisher draws the market box in a slightly different way and then applies different pricing and adoption assumptions. Some also anchor their series to a different base year, which can change the reported current value even if the long-term trend looks similar.

In this study, the key gap drivers are whether software and services are counted alongside equipment, how mobile robots and ASRS are treated when projects are delivered through integrators, and what exchange-rate timing is used for multi-country rollups. The spread also increases when forecasts assume either very fast e-commerce warehouse build-outs or a slower capex cycle in manufacturing. It also widens when older ASPs are carried forward without re-checking recent mix shifts, which is a method choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 30.05 B (2025) | |

| Industry Research Publisher A | USD 27.51 B (2025) | Reported as AMH equipment revenue, which can understate totals when software, integration, and services are treated as out-of-scope or inconsistently attached to equipment projects. |

| Market Publisher B | USD 24.30 B (2024) | Uses an earlier base year and a broader category list, and differences typically come from how functions and system types are classified, plus year-to-year currency and inflation handling across APAC countries. |

The table shows that most of the variation is explained by scope attachment (equipment-only versus equipment plus software and services) and by the choice of base year and conversion timing. By keeping assumptions tied to observable demand signals such as facility additions and parcel throughput, and then re-checking project value ranges through interviews, the estimate stays traceable and repeatable for planning and budgeting.

Key Questions Answered in the Report

What is the current valuation of the autonomous material handling market in Asia Pacific?

The market is valued at USD 33.54 billion in 2026 and is set to reach USD 58.19 billion by 2031.

Which equipment type is gaining the most share in regional warehouses?

Mobile robots lead adoption, holding 33.22% of 2025 deployments and growing at 12.21% CAGR through 2031.

Why are pharmaceuticals investing heavily in autonomous systems?

Drug traceability laws and cold-chain compliance needs drive a 11.89% CAGR for pharmaceutical automation spending.

Which navigation technology is expected to grow fastest?

SLAM-based natural feature guidance will expand at 12.08% CAGR because it removes the need for fixed infrastructure.

How quickly can companies recoup investments in autonomous fleets?

Payback periods have fallen to roughly 18 months in developed APAC markets due to rising labor costs and productivity gains.

Which Asia Pacific country shows the highest growth potential?

India leads with a projected 12.19% CAGR, fueled by production-linked incentives and rapid expansion of e-commerce fulfillment.

Page last updated on: