Industrial Couplings Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

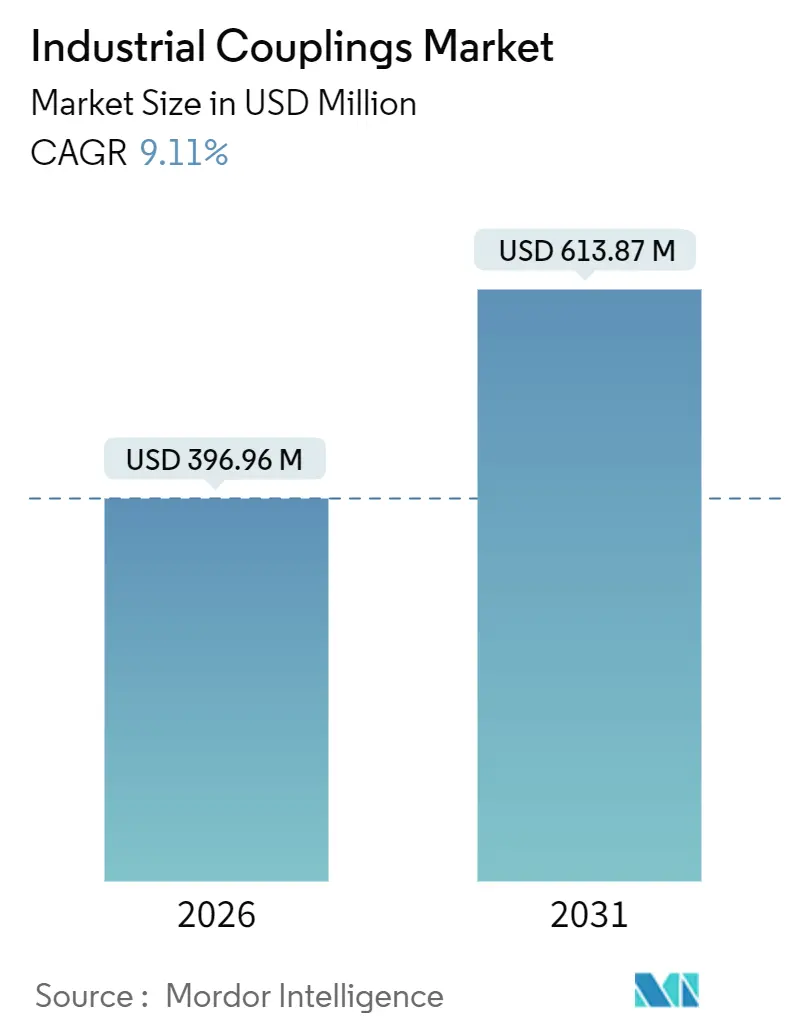

| Market Size (2026) | USD 396.96 Million |

| Market Size (2031) | USD 613.87 Million |

| Growth Rate (2026 - 2031) | 9.11% CAGR |

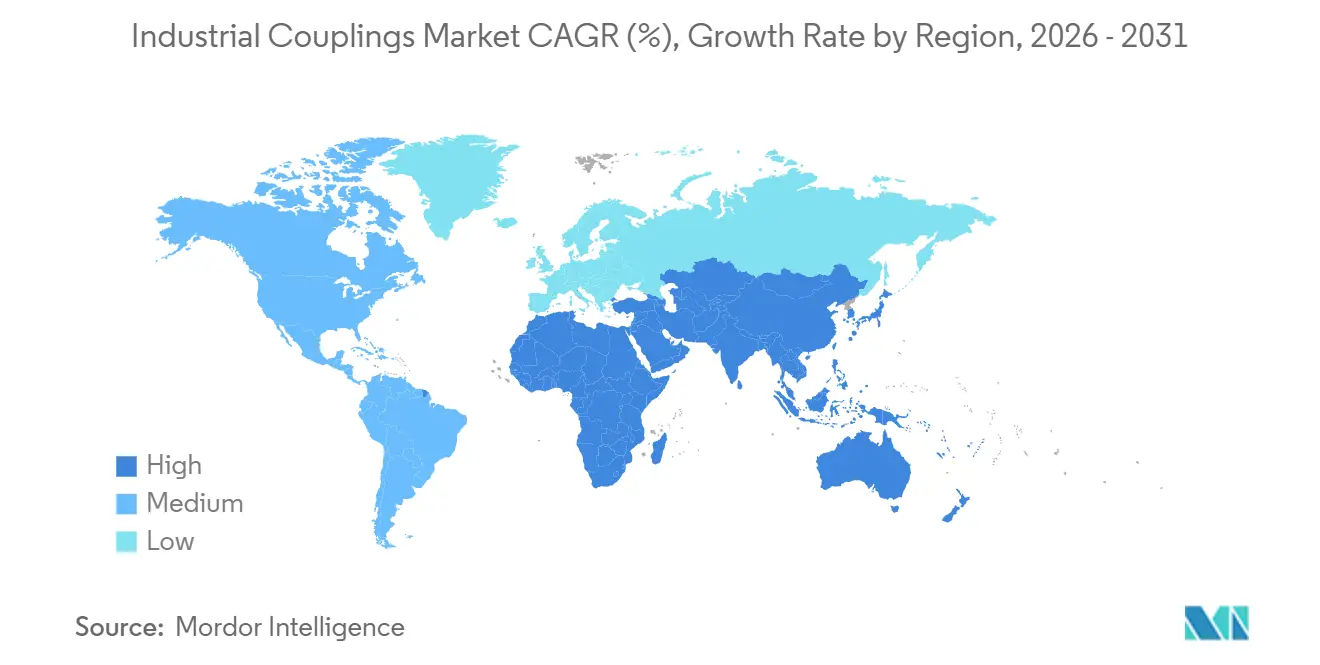

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

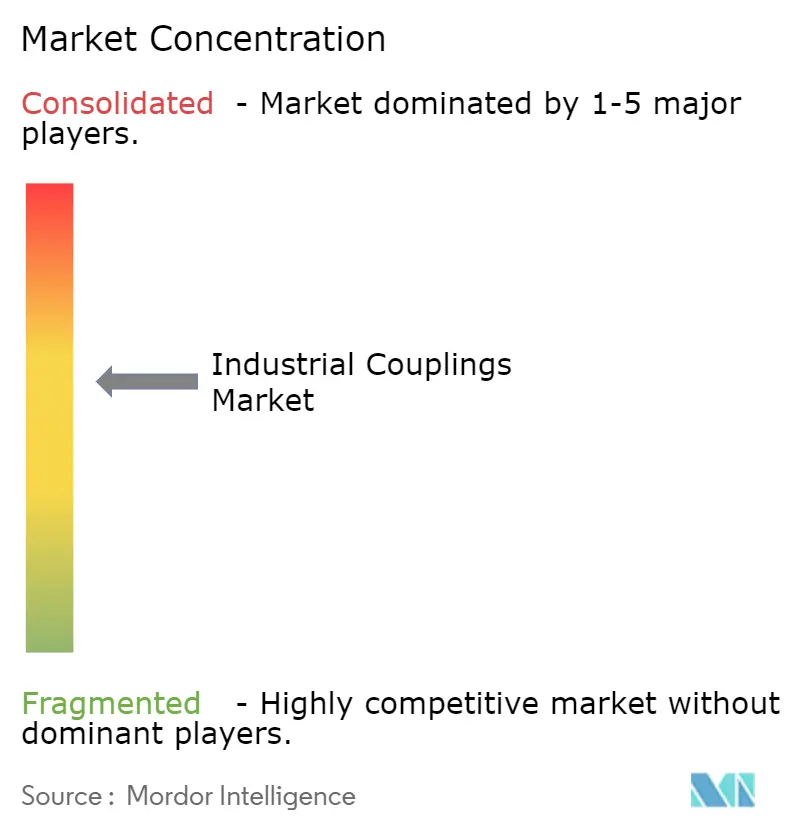

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Couplings Market Analysis by Mordor Intelligence

The industrial couplings market size stood at USD 396.96 million in 2026 and, with a 9.11% CAGR, is projected to reach USD 613.87 million by 2031. The electrification of vehicles, hydrogen electrolyzer rollouts, and the miniaturization of precision motion-control assemblies are pressuring OEMs to specify lighter, cleaner, and higher-speed torque-transfer solutions. Flexible designs presently account for roughly half of demand, yet magnetic variants are gaining momentum as pharmaceutical and semiconductor fabs eliminate any pathways for lubricant ingress. Composite hubs drove double-digit growth in aerospace and medical-device platforms by trimming rotating mass by more than 40%, while Asia-Pacific manufacturers continue to localize production under supportive state subsidies. Competitive intensity has risen as leading brands embed sensors inside hubs to stream real-time torque data, a step that enables predictive maintenance offerings and lifts aftermarket pull-through. Direct-drive motor architectures remain an overhang, but their adoption is confined to low-torque, low-shock niches where couplings add limited functional value.

Key Report Takeaways

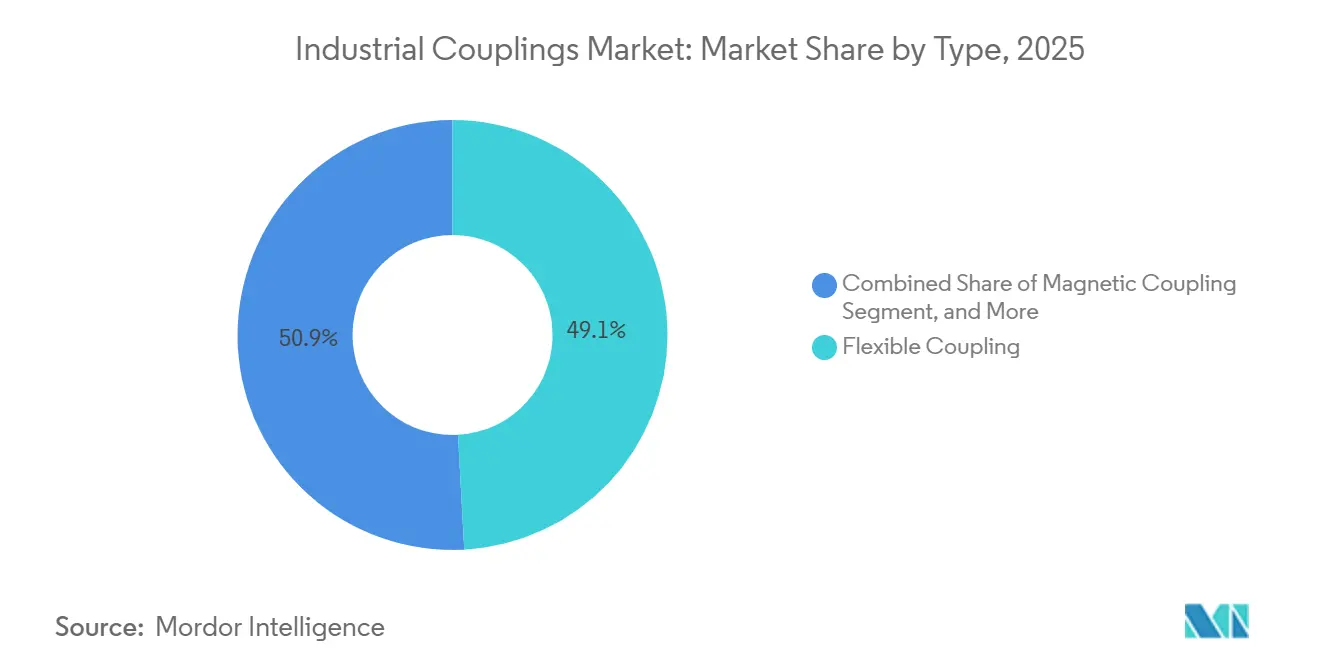

- By type, flexible couplings held 49.13% revenue share in 2025, and magnetic couplings are advancing at a 10.22% CAGR to 2031.

- By material, carbon steel dominated with 37.28% of the industrial couplings market share in 2025, while composite materials are expanding at a 10.29% CAGR through 2031.

- By torque range, Medium (500-5,000 Nm) dominated with a 45.67% share in 2025, while High (Above 5,000 Nm) is expanding at a 9.79% CAGR through 2031.

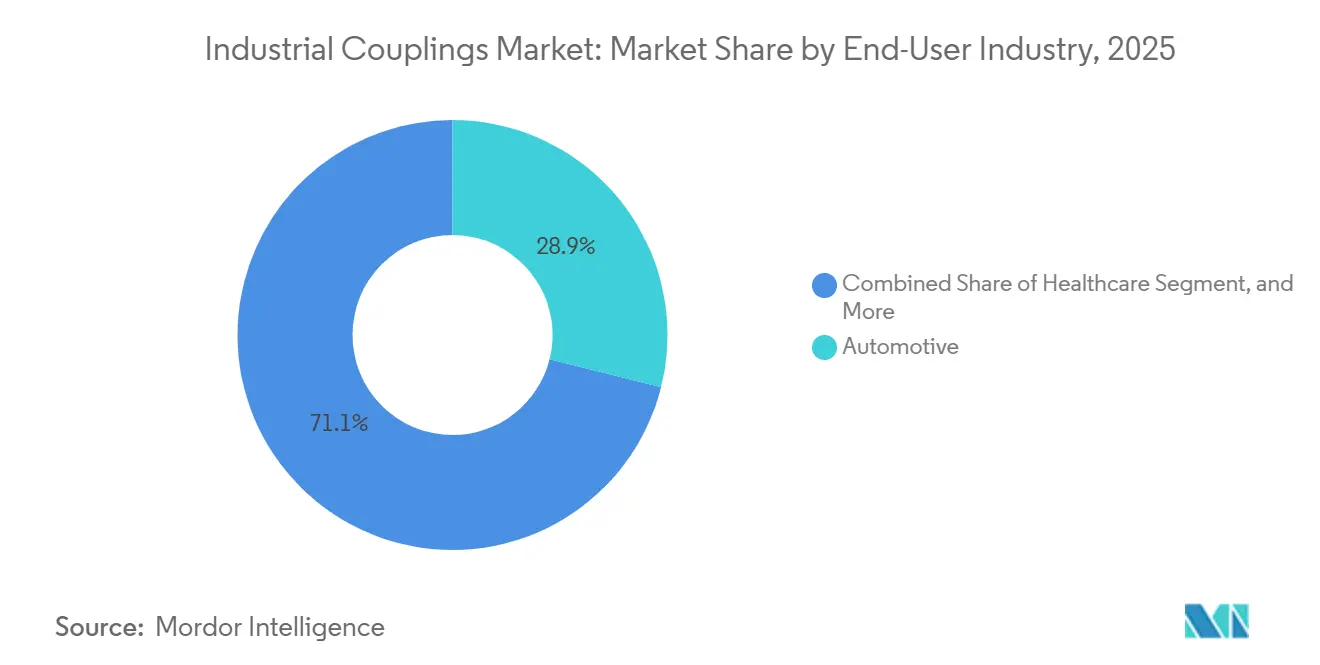

- By end-user industry, automotive accounted for 28.91% of demand in 2025, and healthcare is forecast to post a 10.88% CAGR to 2031.

- By distribution channel, OEM sales accounted for 62.33% of turnover in 2025, and aftermarket transactions are growing at a 9.54% CAGR through 2031.

- By geography, Asia-Pacific captured a 42.76% share in 2025, whereas the Middle East is growing at a 10.17% CAGR over the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Industrial Couplings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding use in precision motion-control systems | +1.8% | Global, with concentration in Germany, Japan, South Korea | Medium term (2-4 years) |

| Growing adoption in high-speed electric powertrains | +2.1% | North America, Europe, China | Short term (≤ 2 years) |

| Rising demand from green hydrogen electrolyzers | +1.5% | Europe, Middle East, Australia | Long term (≥ 4 years) |

| Increased investments in automated intralogistics equipment | +1.3% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Emergence of AI-enabled predictive maintenance platforms | +1.0% | Global, early adoption in North America and Western Europe | Medium term (2-4 years) |

| Government incentives for domestic manufacturing hubs | +1.4% | United States, European Union, India, Saudi Arabia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Use in Precision Motion-Control Systems

Semiconductor lithography, robotic surgery, and coordinate measuring machines demand couplings that maintain angular misalignment below 0.5° while withstanding torque spikes above 1,000 Nm. Bellows and disc formats are now the default because they absorb axial and radial displacement without introducing backlash, preserving micron-level positioning accuracy. Extreme-ultraviolet tools, for instance, rely on multi-stage assemblies that decouple wafer-stage vibration from the reticle carriage, sustaining throughput above 170 wafers per hour.[1]ASML Holding NV, “EUV Lithography Throughput Specifications,” asml.com Collaborative robots used in electronics assembly further favor zero-maintenance couplings that reduce total ownership cost by a quarter over five years. As ISO 9409 flanges converge globally, suppliers can stock a single SKU for multiple verticals, cutting inventory and accelerating custom releases.

Growing Adoption in High-Speed Electric Powertrains

Battery-electric drivetrains operate at 12,000-20,000 rpm, twice the ceiling of legacy combustion units, compelling coupling vendors to tighten balance grades to G2.5 or finer. Shock loads can exceed nominal torque by a factor of 3, prompting elastomeric insert innovations that stiffen progressively under load. Dual-input couplings in hybrid trucks moderate torque blending between diesel and electric sources while compensating for multi-millimeter thermal expansion across long shafts. Efficiency gains of 1.2 percentage points, documented by the United States Department of Energy, translate into 4-6 km of extra range per charge cycle.[2]United States Department of Energy, “Electric Drive Technologies Program Overview,” energy.gov Regulatory momentum, such as Euro 7 tailpipe limits, also nudges adoption, channeling drivetrain redesign budgets toward higher-speed coupling solutions.

Rising Demand from Green Hydrogen Electrolyzers

Electrolyzers producing hydrogen above 30 bar cannot tolerate mechanical seal failures, which is why magnetic couplings have become mandatory in new builds. Installed capacity under construction surpassed 92 GW in 2025, with 60% located in Europe and the Middle East.[3]International Energy Agency, “Global Hydrogen Review 2025,” iea.org Hermetically sealed torque transfer cuts maintenance downtime by 40% and saves USD 15,000-20,000 per megawatt over the asset life. Platforms such as Siemens Energy’s Silyzer 300 specify magnetic drives rated for 85 °C continuous duty, a threshold aligned with ATEX Zone 1 certification. Certification cycles lasting up to 18 months represent both a barrier to entry and a moat for qualified incumbents.

Increased Investments in Automated Intralogistics Equipment

E-commerce fulfillment centers deploy autonomous mobile robots and high-speed conveyors that tolerate up to 5° of misalignment while maintaining positions within 2 mm over 10,000 duty cycles. Flexible jaw or Oldham couplings cushion deceleration shocks as floor robots stop within 0.3 s from 1.5 m/s, extending drivetrain life and trimming downtime. Global intralogistics capex is projected to exceed USD 180 billion by 2027, with more than one-third earmarked for motion-control equipment. Micro-fulfillment footprints now impose 50 mm envelope constraints, pushing designers toward ultra-compact couplings capable of 200 Nm torque ratings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in forged steel and specialty alloy prices | -1.2% | Global, acute in Europe and North America | Short term (≤ 2 years) |

| Competitive threat from direct-drive motor architectures | -1.5% | Global, concentrated in pump and conveyor applications | Medium term (2-4 years) |

| Long replacement cycles in process industries | -0.8% | Mature markets in North America, Europe, Japan | Long term (≥ 4 years) |

| Lack of skilled installers in emerging economies | -0.6% | Southeast Asia, Africa, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Forged Steel and Specialty Alloy Prices

Forged-steel billet values spiked 18% early in 2025 due to iron-ore supply constraints, then fell 12% by mid-year as Chinese mills lifted output. Nickel-alloy surcharges fluctuated between USD 4.20 and USD 6.80 per kilogram, squeezing suppliers' margins for those without hedging programs. Smaller manufacturers with revenue below USD 50 million face steep pricing power deficits at service centers and must adopt quarterly pass-through clauses, a practice that elongates purchase cycles and strains client relationships. Vacuum-arc-remelted alloys, required for couplings above 5,000 Nm, add USD 8-12 per kilogram to base steel cost, intensifying the pressure on specialty product lines.

Competitive Threat from Direct-Drive Motor Architectures

Direct-drive systems mount the payload directly on the motor shaft, cutting parts count by 15% and lifting efficiency by up to 3 percentage points in conveyors and pumps. ABB’s permanent-magnet motors, for example, reach 96% efficiency at partial loads. Although capital outlay is 30-40% higher, payback periods shrink below two years in operations running over 6,000 hours annually. Couplings remain indispensable in shock-prone environments such as crushers or presses, where they safeguard bearings. In low-torque, steady-state applications, however, the elimination trend is real and will likely cap addressable volumes over the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Precision Magnetic Variants Accelerate in Hermetic Duties

Flexible couplings retained 49.13% of revenue in 2025, underscoring their versatility across compressors, HVAC blowers, and automotive assembly lines. Magnetic units, however, are surging ahead at a 10.22% CAGR because pharmaceutical and semiconductor plants cannot afford seal leakage. The industrial couplings market size for magnetic designs is projected to widen substantially as hydrogen electrolyzers and wet-etch tools roll out worldwide. Rigid formats persist in grinding machines where shafts stay aligned within 0.02 mm, while fluid couplings dominate mining haul trucks that crave torque multiplication during startup. Universal-joint styles are used in agricultural and construction equipment that must accommodate more than 10° of angular misalignment. Bellows couplings occupy premium healthcare niches such as MRI gantries, where zero backlash sustains sub-micron accuracy, and elastomeric inserts damp torsional vibration in variable-frequency HVAC drives.

Lightweight disc couplings with carbon-fiber hubs, which cut inertia by 35%, help robots achieve faster acceleration and shorten pick-and-place cycle times. Hybrid designs combining elastomeric dampers with metallic packs now appear in wind-turbine pitch drives that face emergency torque loads above 50,000 Nm. Compliance pressure from the European Union’s Machinery Regulation 2023/1230 obliges suppliers to integrate fail-safe mechanical fuses on collaborative-robot couplings, a requirement that may swell certification spending but shields incumbents from price-led entrants. Taken together, type diversification supports more resilient revenue streams as the industrial couplings market navigates end-user volatility.

By Material: Composites Challenge Steel on Weight and Stiffness

Carbon steel accounted for 37.28% of volume in 2025 because it met cost targets below USD 2.50 per kilogram in the 500-5,000 Nm segment. Stainless steel meets stringent hygienic codes in food and pharma, yet polishing and passivation add USD 12-18 per unit, leaving room for substitution wherever corrosion risks are acceptable. Composite hubs, climbing at a 10.29% CAGR, resonate with aerospace actuators and surgical robots that shave grams to extend mission life or minimize surgeon fatigue. The industrial couplings market share for carbon steel may erode gradually as carbon-fiber-reinforced PEEK and titanium alloys demonstrate comparable stiffness at dramatic weight reductions. Aluminum retains a role in textile looms and labelers that run below 1,000 Nm because its low inertia fosters high acceleration.

Additive manufacturing unlocks latticed geometries that optimize stiffness-to-weight ratios while embedding sensor cavities at no tooling cost. The trade-off remains price: composite units retail at USD 150-300, compared with USD 30-60 for steel, limiting adoption to applications where performance trumps capex. As high-speed electric drives proliferate, however, inertia reduction delivers measurable energy savings, closing the economic gap faster than steel producers can discount raw stock.

By Torque Range: High-Torque Use-Cases Fuel Above-Average Growth

Medium-torque couplings in the 500-5,000 Nm range accounted for 45.67% of shipments in 2025, serving the broad mid-market of pumps, blowers, and conveyors. The high-torque class above 5,000 Nm is forecast to advance at 9.79% CAGR, mirroring capital investment in crushers, cement kilns, and wind-turbine main shafts. The industrial couplings market size for high-torque models benefits from escalating drivetrain ratings in renewable energy and mining. Low-torque devices under 500 Nm remain essential for servo motors that value responsiveness and zero backlash, but price competition is stiffer because of generic alternatives.

Vendors that can certify products to API 671 or ISO 14691 gain preferred-supplier status on petrochemical and LNG projects, a niche where a single purchase order can eclipse annual shipment volumes in low-torque catalog lines. Conversely, direct-drive motors threaten only the sub-500 Nm bracket, leaving the high-torque tier largely insulated for the forecast period, especially when couplings also serve as torsional dampers, preserving gearboxes and bearings.

By End-User Industry: Healthcare Emerges as the Fastest-Growing Vertical

Automotive plants absorbed 28.91% of demand in 2025 across engine test benches, battery-pack assembly, and transmission lines. Healthcare, growing at a 10.88% CAGR, reflects the deployment of MRI and CT scanners, as well as robotic surgery suites that cannot tolerate positional drift. The industrial couplings market for medical use will accelerate as global imaging scanner stock expands and surgical robot adoption widens beyond affluent hospitals. Oil and gas projects continue to procure metallic-disc or diaphragm couplings that handle sour gas and temperature extremes, while metals and mining use elastomeric dampers to tame shock loads in crushers.

Food and beverage processors remain captive to stainless-steel or polymeric designs that meet 3-A Sanitary Standards, while aerospace integrators pursue ever-lighter hubs to extend drone endurance and slash aircraft fuel burn. Regulatory oversight, notably the United States FDA’s 21 CFR Part 820, raises quality-system costs but also entrenches qualified suppliers by making audits and documentation part of the product value proposition.

By Distribution Channel: Aftermarket Momentum Builds with Digital Procurement

OEM assemblies captured 62.33% of 2025 sales because new equipment embeds couplings from day one. Aftermarket revenue, however, is climbing 9.54% annually as installed fleets age and as AI-driven condition-monitoring solutions flag impending failures weeks in advance. Distributors have responded with augmented online catalogs, 3D CAD downloads, and torque calculators, compressing quote-to-order cycles from 6 weeks to 2 days for standardized SKUs. Low-torque items migrate swiftly to e-commerce carts, whereas high-torque or custom builds still necessitate site surveys, finite-element validations, and field commissioning support.

Margin differentials favor replacements: aftermarket gross profit hovers around 45% compared with roughly 27% on first-fit sales. Consequently, leading vendors align inventory and technical resources toward retrofit opportunities, particularly in sectors like pulp-and-paper or cement that run assets on multidecade cycles. As predictive analytics matures, the industrial couplings market will likely tilt further toward proactive upgrades rather than emergency swaps, smoothing quarterly demand patterns and aiding capacity planning.

Geography Analysis

Asia-Pacific supplied 42.76% of global revenue in 2025, buoyed by China’s 30-million-unit vehicle output and India’s USD 26 billion incentive packages for electronics, pharmaceuticals, and advanced materials. Japan maintains premium demand for semiconductor lithography couplings that run beyond 1,000 Nm with sub-micron concentricity, while South Korean shipyards order heavy-duty marine couplings rated above 50,000 Nm. Australia’s mining output, including 900 million t of iron ore in 2025, supports continuous orders for high-torque dampers in haul trucks and conveyors. Government-backed infrastructure spending above USD 1.5 trillion per year stimulates pipelines of metro rails, desalination plants, and petrochemical hubs, each requiring diverse coupling families.

The Middle East, forecast to grow at a 10.17% CAGR, benefits from Saudi Arabia’s USD 500 billion NEOM industrial zone and the United Arab Emirates’ downstream petrochemical expansion, which added 4 million t of polyethylene capacity in 2025. Qatar’s North Field LNG expansion specifies API 610 pump couplings for cryogenic service, while Egypt’s Suez Canal Economic Zone draws textile and food processors that standardize on flexible or elastomeric units. Harmonizing local regulations with ISO standards shortens approval timelines and lowers localization costs for multinational suppliers.

North America and Europe together represented roughly 45% of 2025 turnover, mainly replacement purchases in older factories and energy-efficiency retrofits. The United States CHIPS and Science Act unlocks semiconductor fabs in Arizona, Texas, and Ohio, each of which consumes precision couplings for wafer handling and gas-delivery modules. Germany’s Energiewende is accelerating wind-turbine installations that require pitch-drive dampers certified for 20-year life. Canada’s hydro projects and Norway’s offshore wind clusters further expand the high-torque addressable base. South America registers mid-single-digit growth, concentrated in Brazil’s sugarcane mills and Argentina’s shale rigs, while Africa remains an early-stage play confined to South African mining and Egyptian industrial corridors due to infrastructure gaps and currency volatility.

Competitive Landscape

The industrial couplings market is moderately fragmented: the top five vendors, Altra Industrial Motion, Regal Rexnord, Siemens, ABB, and SKF, account for an estimated 35-40% of revenue. Tier-1 brands differentiate through embedded sensors and analytics platforms that convert hub telemetry into high-margin subscription services. Siemens secured patent EP3985276A1 covering a strain-gauge-infused coupling with wireless data streaming, illustrating the pivot toward “hardware plus software” business models. Mid-size firms such as Ringfeder or Ruland Manufacturing defend their share by delivering rapid customizations in under two weeks via additive manufacturing, undercutting larger competitors’ six-week cycles.

White-space opportunities lie in ultra-high-speed couplings tuned for 25,000 rpm electric-vehicle traction motors or aerospace actuators, both of which require G1.0 balance grades and torsional stiffness above 100,000 Nm per radian. Direct-drive solutions clip volume growth in low-torque commodity pumps and conveyors, driving incumbents to realign portfolios toward precision-demanding sectors like medical imaging and green hydrogen. Barriers to entry remain formidable: ISO 14691 and API 671 compliance testing can cost more than USD 2 million in capital equipment and extend certification timelines to 18 months, discouraging thin-capitalized challengers.

Supply-chain resilience programs also shape competition. Regal Rexnord’s USD 45 million capacity expansion in Wisconsin adds automated machining cells and inline machine-vision defect detection, reducing scrap by 15% and safeguarding lead times against raw-material shocks. Siemens and SKF integrate torque sensors and thermal arrays to forecast wear six to eight weeks in advance, cutting customer downtime by up to 35%. Partnerships such as ABB-Voith on offshore wind couplings pool motor and elastomeric expertise, accelerating time-to-market in high-megawatt turbines. Mergers, notably Altra’s purchase of Coupling Corporation of America, aim to secure high-torque intellectual property and broaden service footprints.

Industrial Couplings Industry Leaders

Altra Industrial Motion Corp.

Baker Hughes Company

Emerson Electric Co.

Siemens AG

ABB Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Regal Rexnord announced a USD 45 million expansion of its Grafton, Wisconsin plant, adding 50,000 ft² of automated machining to support electric-vehicle and renewable-energy demand.

- November 2025: Siemens launched the ELPEX-B high-speed series rated for 20,000 rpm with carbon-fiber hubs that cut inertia 40% versus steel peers.

- October 2025: SKF unveiled its Enlight condition-monitoring suite for couplings, merging accelerometer and thermal imagery to predict wear six to eight weeks ahead of failure.

- September 2025: Altra Industrial Motion closed the USD 120 million acquisition of Coupling Corporation of America, adding three plants and 180 staff.

Global Industrial Couplings Market Report Scope

The Industrial Couplings Market Report is Segmented by Type (Flexible Coupling, Rigid Coupling, Fluid Coupling, Magnetic Coupling, Universal Joint Coupling), Material (Carbon Steel, Stainless Steel, Aluminum, Composite Materials, Other Materials), Torque Range (Low (Below 500 Nm), Medium (500-5,000 Nm), High (Above 5,000 Nm)), End-user Industry (Automotive, Aerospace and Defence, Oil and Gas, Healthcare, Metal and Mining, Power Generation, Food and Beverage, Other End-user Industries), Distribution Channel (OEM, and Aftermarket), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

| Flexible Coupling |

| Rigid Coupling |

| Fluid Coupling |

| Magnetic Coupling |

| Universal Joint Coupling |

| Carbon Steel |

| Stainless Steel |

| Aluminum |

| Composite Materials |

| Other Materials |

| Low (Below 500 Nm) |

| Medium (500-5,000 Nm) |

| High (Above 5,000 Nm) |

| Automotive |

| Aerospace and Defence |

| Oil and Gas |

| Healthcare |

| Metal and Mining |

| Power Generation |

| Food and Beverage |

| Other End-user Industries |

| OEM |

| Aftermarket |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Type | Flexible Coupling | ||

| Rigid Coupling | |||

| Fluid Coupling | |||

| Magnetic Coupling | |||

| Universal Joint Coupling | |||

| By Material | Carbon Steel | ||

| Stainless Steel | |||

| Aluminum | |||

| Composite Materials | |||

| Other Materials | |||

| By Torque Range | Low (Below 500 Nm) | ||

| Medium (500-5,000 Nm) | |||

| High (Above 5,000 Nm) | |||

| By End-user Industry | Automotive | ||

| Aerospace and Defence | |||

| Oil and Gas | |||

| Healthcare | |||

| Metal and Mining | |||

| Power Generation | |||

| Food and Beverage | |||

| Other End-user Industries | |||

| By Distribution Channel | OEM | ||

| Aftermarket | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the projected value of the industrial couplings market by 2031?

The market is forecast to reach USD 613.87 million by 2031 on the back of a 9.11% CAGR.

Which coupling type is growing the fastest through 2031?

Magnetic couplings are advancing at a 10.22% CAGR due to their hermetic, zero-leakage operation.

Why are composites gaining traction in coupling construction?

Composite hubs reduce rotating weight by about 40%, improving acceleration and energy efficiency in aerospace, robotics, and medical equipment.

How is predictive maintenance changing aftermarket dynamics?

Sensor-enabled hubs stream torque and vibration data, allowing AI platforms to schedule replacements ahead of failure, which is boosting aftermarket revenue at a 9.54% CAGR.

Which region offers the highest growth potential for suppliers?

The Middle East, led by mega-projects like NEOM and large LNG expansions, is expected to grow at roughly 10.17% CAGR through 2031.

What competitive strategy are leading vendors adopting to differentiate?

Top players embed IoT sensors in couplings and monetize data analytics subscriptions, securing higher margins than hardware sales alone.

Page last updated on: