United States Material Handling Leasing And Financing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

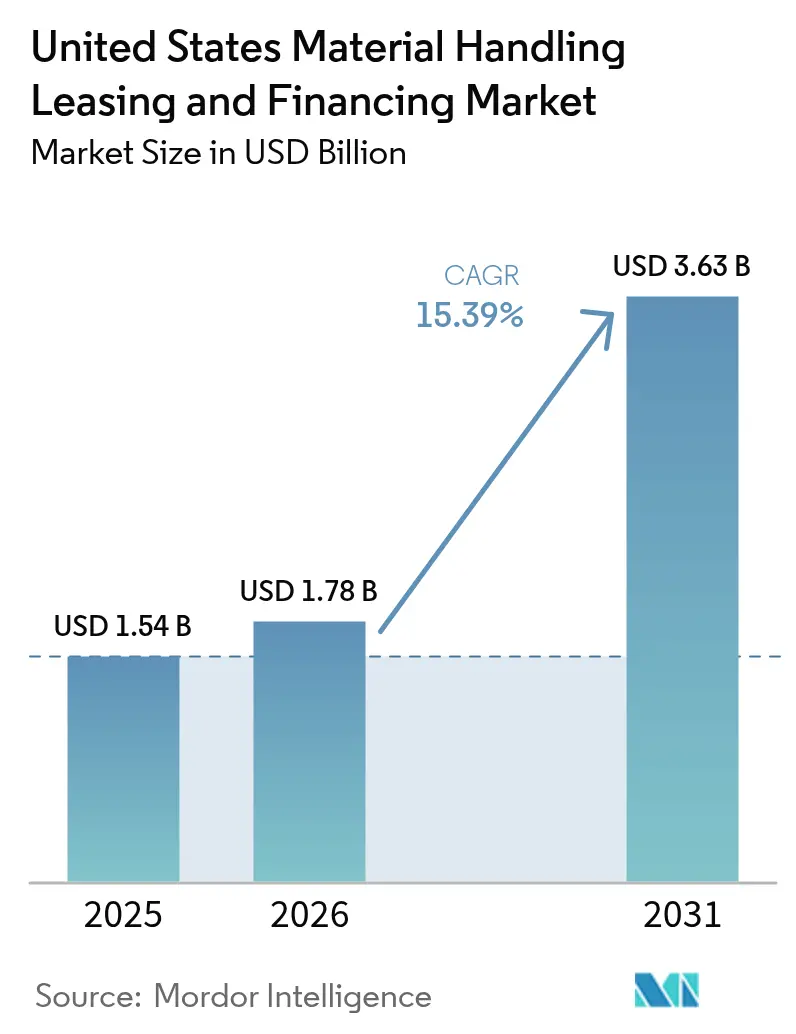

| Base Year Market Size (2025) | USD 1.54 Billion |

| Market Size (2026) | USD 1.78 Billion |

| Market Size (2031) | USD 3.63 Billion |

| Growth Rate (2026 - 2031) | 15.39% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Material Handling Leasing And Financing Market Analysis by Mordor Intelligence

The United States material handling leasing and financing market size is expected to grow from USD 1.54 billion in 2025 to USD 1.78 billion in 2026 and is forecast to reach USD 3.63 billion by 2031 at 15.39% CAGR over 2026-2031. This powerful upswing is propelled by e-commerce warehouse buildouts that demand capital-intensive automated equipment, federal tax optimization under Section 179, and the spread of equipment-as-a-service contracts that lower balance-sheet risk for small and medium enterprises. New business volume for material handling assets advanced 12% during 2024 as large retailers and third-party logistics operators accelerated network expansion.[1]Equipment Leasing and Finance Association, “2024 Annual Survey Results,” elfaonline.org Financiers have responded by developing hybrid lease structures that combine traditional operating leases with embedded technology service clauses, a design that mitigates residual-value uncertainty on automated guided vehicles. In parallel, ESG-linked loan incentives are narrowing the spread between electric and internal-combustion equipment, unlocking new demand in high-regulation states. Competitive intensity is rising because technology-enabled entrants are bundling telemetry, predictive maintenance, and insurance into single monthly invoices, thereby altering fee economics for incumbent lessors.

Key Report Takeaways

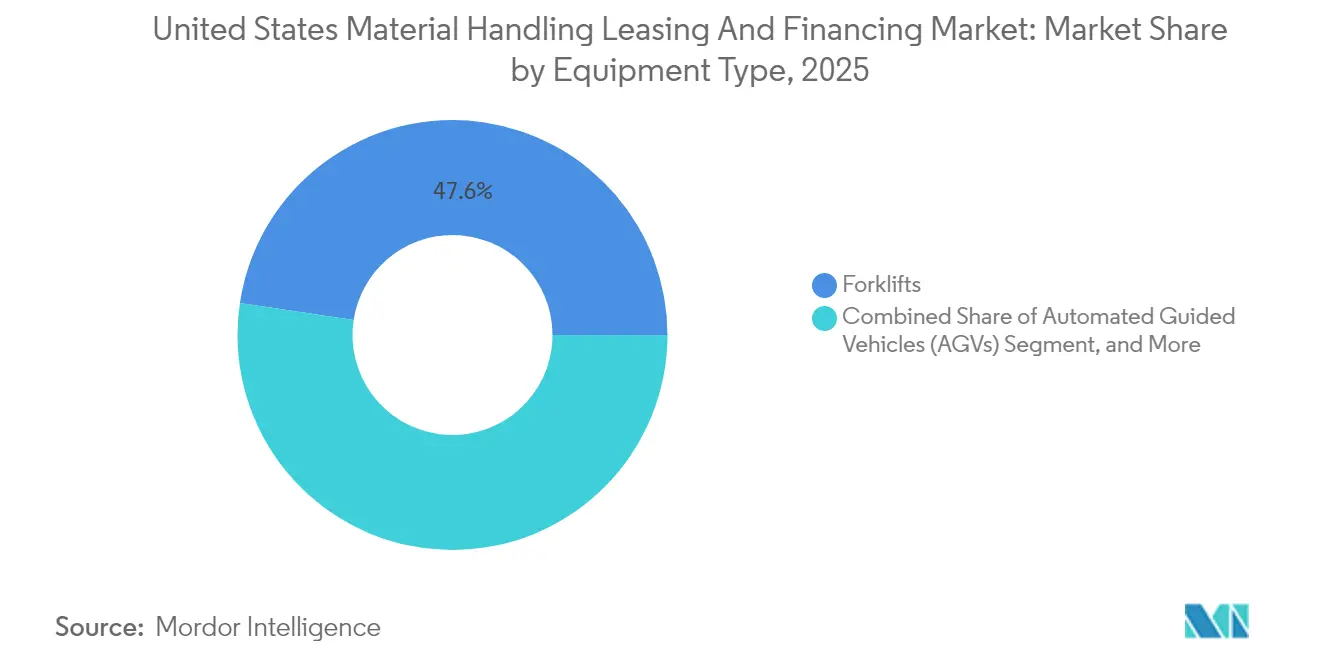

- By equipment type, forklifts led with 47.62% revenue share in 2025 while automated guided vehicles are projected to expand at a 16.03% CAGR to 2031.

- By end-user industry, e-commerce and third-party logistics providers accounted for 36.78% of 2025 financing volume, and pharmaceuticals show the fastest 16.49% CAGR through 2031.

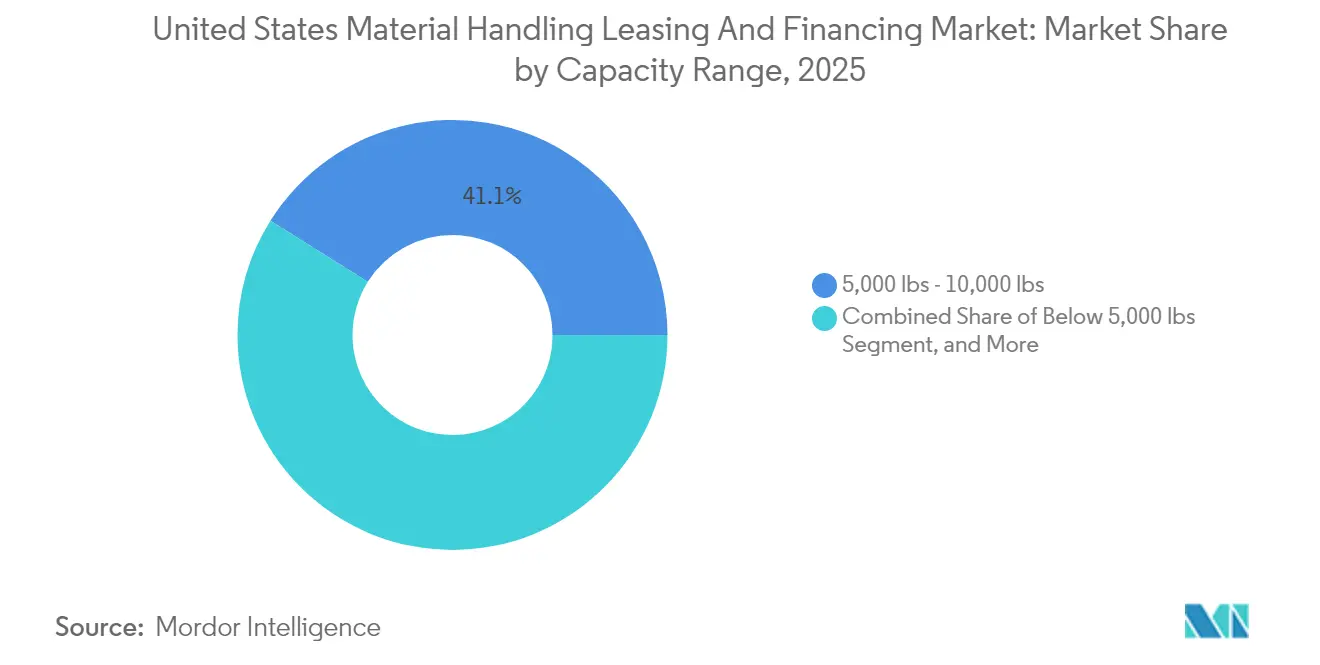

- By capacity range, the 5,000-10,000 pound band captured 41.08% of 2025 activity, yet the sub-5,000 pound class is advancing at a 17.62% CAGR on micro-fulfilment demand.

- By financing type, operating leases held 51.73% share in 2025, whereas sale-and-leaseback arrangements exhibit the strongest 16.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Material Handling Leasing And Financing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising e-commerce warehouse expansion | +3.20% | National, concentrated in logistics corridors | Medium term (2-4 years) |

| Growing preference for "as-a-service" models among SMEs | +2.80% | National, strongest in urban markets | Short term (≤ 2 years) |

| Accelerated automation mandates due to labor constraints | +2.10% | National, acute in high-wage regions | Long term (≥ 4 years) |

| ESG-linked financing incentives from U.S. banks | +1.90% | National, leadership from major metropolitan areas | Medium term (2-4 years) |

| Secondary market liquidity for used equipment | +1.40% | National, regional variations in availability | Short term (≤ 2 years) |

| Federal tax advantages under Section 179 deduction | +1.80% | National, higher impact in high-tax states | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising E-commerce Warehouse Expansion

E-commerce fulfilment networks are the single largest catalyst for the United States material handling leasing and financing market, as operators pack more automation into each square foot to achieve same-day delivery commitments. Amazon committed USD 15 billion to new warehouses for 2024-2025, translating to an estimated USD 3 billion in lift trucks, conveyor lines, and automated guided vehicles.[2]Amazon Investor Relations, “Amazon Announces Major Warehouse Expansion,” aboutamazon.com Regional third-party logistics firms mirror this strategy by deploying micro-fulfilment hubs within 10 miles of dense population clusters, where ceiling heights are lower, and automation density is 40% higher than legacy bulk warehouses. Lease demand spikes because landlords and tenants want off-balance-sheet structures for assets that risk technological obsolescence within five to seven years. Forward-looking lessors package predictive-maintenance telemetry and de-risk the deal with residual-value insurance to remain competitive when bidding for these fast-cycle projects.

Growing Preference for “As-a-Service” Models Among SMEs

Cash-constrained small and medium enterprises increasingly choose bundled offerings that wrap financing, maintenance, battery management, and software upgrades into one invoice. A 2024 survey showed 67% of SME logistics operators evaluating an equipment-as-a-service option after pandemic-era supply shocks exposed the hazards of outright ownership.[3]PwC, “Equipment-as-a-Service Adoption Survey,” pwc.com Programs such as Toyota Material Handling’s Total Solutions require no down payment, provide technology refreshes every 36 months, and fold insurance into the monthly rate. The cost certainty of these packages supports working capital planning and reduces reliance on revolving credit facilities during seasonal demand peaks. Lenders gain high lifetime value because service-rich contracts lock in renewals and generate fee streams long after the original asset repayment, thereby improving return on equity even when base interest margins compress.

Accelerated Automation Mandates Due to Labor Constraints

Warehouse job vacancy rates topped 15% in several high-wage regions during 2024, pushing wage costs up by 8.3% year-on-year.[4]Bureau of Labor Statistics, “Warehouse Worker Wage Data,” bls.gov Management teams therefore deploy automated storage, shuttle, and robotic picking systems to curb labour spend and meet productivity quotas. These complex solutions command premium lease rates, but lenders are engineering hybrid structures that share uptime risk with OEMs through service-level-agreement credits. Honeywell’s Intelligrated unit pioneered “automation-as-a-service” deals that guarantee throughput metrics, effectively anchoring a performance-based rental price and shifting part of the failure risk to the supplier. Such models accelerate capital commitment because CFOs can now benchmark automation’s total cost of ownership against a predictable per-unit-handled fee.

ESG-Linked Financing Incentives from U.S. Banks

Electric forklifts and lithium-ion powered AGVs benefit from rate discounts of 25-50 basis points under new green-lease programs rolled out by large banks. Bank of America carved out USD 500 million specifically for warehouse electrification, citing studies that place material handling fleets at 30% of facility-level emissions. Wells Fargo structures these contracts with step-down coupons that reward customers for hitting verified carbon-reduction targets. The discounted funding narrows the total cost gap between electric and internal-combustion units, especially in states with renewable-heavy grids. Lessors consequently see stronger resale appetite for late-model electric fleets, which improves residual-value assumptions and lowers headline lease payments for customers in sustainability-driven verticals such as pharmaceuticals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High residual-value uncertainty for AGVs | -1.80% | National, concentrated in tech-forward markets | Medium term (2-4 years) |

| Bank tightening on credit scores post-2024 | -2.10% | National, acute for SME borrowers | Short term (≤ 2 years) |

| Volatility in benchmark interest rates | -1.60% | National, uniform impact across regions | Short term (≤ 2 years) |

| Cyber-risk premiums embedded in lease contracts | -0.90% | National, higher in critical infrastructure sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Residual-Value Uncertainty for AGVs

Automated guided vehicles depreciate much faster than conventional forklifts because control software revisions arrive every 12-18 months, creating obsolescence risk and shrinking the secondary buyer pool. Market data show three-year-old AGVs retain only 35-45% of original cost, versus 60-70% for standard lift trucks. Lessors therefore load an additional 150-200 basis-point premium into AGV lease rates to offset potential residual losses. This price delta slows adoption outside top-tier retailers that can absorb the higher carrying cost. Insurers are experimenting with residual-value guarantees, but underwriting capacity remains thin, meaning lenders must cap exposure or insist on technology refresh clauses mid-lease.

Bank Tightening on Credit Scores Post-2024

The Federal Reserve’s rate cycle triggered a recalibration of commercial credit policy, driving minimum FICO thresholds on unsecured equipment loans from 620 to 680 during 2024. Approval rates on small-ticket transactions fell to 65% as regional banks insisted on stronger collateral and shorter amortization schedules. SMEs without lengthy financial histories face borrowing spreads 200-400 basis points above prime, pushing them toward captive finance arms or fintech platforms that price risk algorithmically. The two-tier funding landscape widens competitiveness gaps and may slow penetration of automated solutions among emerging operators that lack seasoned credit profiles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Automation Drives Premium Segment Growth

Forklifts retained a 47.62% share of the United States material handling leasing and financing market in 2025 because their universal utility aligns with standardized lease templates that deliver quick credit decisions. At the same time, automated guided vehicles recorded a 16.03% CAGR forecast to 2031 as labour scarcity and rising land costs compel operators to harvest every square foot of cubic storage. Conveyor lines and sorters steady the mid-range, especially inside parcel hubs where volume dictates continuous-flow handling. The United States material handling leasing and financing market size for forklift contracts is forecast to broaden by high-single-digits, yet OEM telemetry add-ons are reshaping residual-value math by enabling condition-based resale pricing. Lessors that integrate IoT analytics into underwriting gain underwriting precision and trim reserve buffers, lowering all-in rates for customers.

Increasing automation shifts lease structures from simple rent-to-own toward performance-linked service contracts bundling software licenses, artificial-intelligence guidance, and on-site technical support. Tesla’s Gigafactory, for instance, embedded a multi-year “equipment availability” guarantee in its agreement with KION Group, obligating the supplier to restore uptime inside a two-hour window or face penalty credits. Such clauses affect cash-flow models because lenders must verify that OEM service capacity can protect throughput targets underpinning the lease. For traditional finance houses, partnering with systems integrators has become essential to protect collateral value, especially for conveyor-plus-robotic hybrids whose resale hinges on modular adaptability.

By End-User Industry: Pharmaceuticals Emerge as Growth Leader

E-commerce and third-party logistics players absorbed 36.78% of 2025 financing volume, yet the pharmaceuticals customer base is forecast to achieve a 16.49% CAGR, driven by stringent cold-chain regulations that mandate advanced storage, lift, and shuttle systems. The United States material handling leasing and financing market share attributable to pharmaceutical operators is set to climb rapidly as firms add high-density automated storage serving cell-and-gene therapy pipelines. Financing tickets skew larger because compliance requires stainless-steel lifts, redundant power, and validated software, each inflating asset cost. Lenders price in FDA validation’s beneficial effect on residuals, as validated equipment often resells at a premium to emerging biomanufacturers seeking pre-qualified machinery.

Manufacturing and retail verticals still supply predictable baseline demand, but their growth rates trail automation-heavy sectors. Food and beverage facilities rely on captive finance channels able to underwrite temperature-controlled lift trucks equipped with corrosion-resistant components. Meanwhile, brick-and-mortar retail invests in back-of-store micro-fulfilment pods, often financed under short-cycle operating leases to accommodate evolving omnichannel strategies. Lessors tailor covenants to handle seasonality, allowing holiday-period payment deferrals that align cash outflows with revenue inflows.

By Capacity Range: Micro-Fulfilment Drives Lightweight Demand

Equipment rated 5,000-10,000 pounds claimed 41.08% of 2025 financed assets, representing the ergonomic sweet spot for general distribution. Nonetheless, units below 5,000 pounds are scheduled for a 17.62% CAGR, as dense urban fulfilment nodes adopt narrow-aisle trucks and compact autonomous mobile robots. The United States material handling leasing and financing market size for light equipment will likely double before 2031. Shorter lease tenors and streamlined documentation draw SME entrants who need agile financing when opening last-mile depots on month-to-month real-estate terms. Residual-value risk is comparatively mild because the secondary market for lightly used Class III pallet trucks remains liquid across foodservice, beverage, and manufacturing outlets.

In contrast, 10,001-20,000-pound models serve bulk manufacturing and port terminals where duty cycles run three shifts, compelling 60-month or longer capital-lease terms. Here, lessors bake in higher maintenance provisions or insist on OEM service contracts to maintain asset condition. Equipment above 20,000 pounds fills niche heavy-industry roles, demanding interest-only structures or balloon payments that synchronize with project lifecycles such as refinery turnarounds.

By Financing Type: Sale-Leaseback Gains Momentum

Operating leases dominated 51.73% of 2025 activity, buoyed by Section 179 tax deductibility that lets lessees’ expense up to USD 1.22 million immediately. The United States material handling leasing and financing market size attributable to operating leases continues to climb, yet sale-and-leaseback transactions show the sharpest 16.95% CAGR as corporates unlock trapped equity. Prologis pioneered facility-plus-equipment packages that monetize tenant fleets while embedding flexible renewal options tied to occupancy terms. Capital leases remain relevant for specialized crane systems whose economic life exceeds 12 years, while traditional loans attract investment-grade borrowers seeking lowest-cost capital.

Sale-leaseback proceeds increasingly fund automation retrofits, allowing operators to tap existing forklift pools for liquidity without diluting shareholder equity. Lessors mitigate risk by coupling residual guarantees with equipment condition assessments conducted at transaction close. Asset tracking via RFID tags feeds dashboards that rank lessee utilization patterns and flag abnormal wear, enabling early intervention and protecting collateral integrity.

Geography Analysis

California, Texas, and the Northeast logistic corridor collectively generated roughly 44.62% of United States material handling leasing and financing market volume in 2025, thanks to port density, consumer concentration, and entrenched manufacturing. The Inland Empire alone accounts for about 7.84% of national bookings, underpinned by Asian import flows funnelled through the Port of Long Beach’s USD 2.6 billion modernization pipeline. Lessors active in these hot zones can price more aggressively because asset redeployment options are plentiful within a 50-mile radius, trimming idle time between contracts.

The Southeast and Mountain West are the fastest-growing territories as e-commerce networks hunt for lower land cost and congestion relief. States such as Georgia and Arizona lure fulfilment centers with tax credits that stack atop Section 179 deductions, compressing effective lease yields and enhancing project IRRs. FedEx’s USD 1.5 billion Memphis superhub revamp includes cutting-edge sorters, shuttles, and autonomous tugs financed chiefly under long-term operating leases, cementing the region’s status as a multi-modal nexus.

Interest-rate volatility influences regional spreads: coastal lenders face stiff competition from national banks, while inland borrowers rely on captive finance or local lenders who demand higher coupons to offset thinner resale channels. Public-private partnerships at major ports foreground a new template in which municipal agencies avoid upfront capital outlays by leasing automated cranes and automated stacking carriers from private lessors, aligning equipment payments with throughput-based concession revenue.

Competitive Landscape

The United States material handling leasing and financing market remains moderately concentrated, with the top ten players capturing close to 60% of funded volume. Still, niche lenders and fintech entrants inject fragmentation by targeting underserved verticals such as micro-fulfilment and robotics. Element Fleet Management’s USD 450 million portfolio acquisition strengthened its presence in high-tech warehouse automation, underscoring a strategic pivot toward solutions expertise rather than pure capital supply.

Technology integration is the new battleground. Wells Fargo’s Smart Fleet portal streams real-time utilization, fault codes, and battery state of charge, enabling dynamic lease renewals aligned with actual wear patterns. Traditional lessors that lack digital telemetry risk commoditization as clients favour partners able to deliver uptime guarantees. Pacific Rim Capital competes on agility – funding approvals in under 48 hours – appealing to retailers racing to open pop-up distribution centers before holiday surges.

Manufacturer-captive finance companies tighten the circle by layering extended warranty, operator training, and software license fees into monthly rentals, gradually absorbing services revenue that once flowed to third-party dealers. Independent lessors respond by offering multi-brand fleet structures, an advantage for clients running mixed OEM environments across national footprints. Mergers such as CIT’s union with First Citizens Bank illustrate scale economics – a wider balance sheet lowers cost of funds, allowing sharper rate quotes while still meeting yield targets.

United States Material Handling Leasing And Financing Industry Leaders

CIT Group Inc.

Crest Capital LLC

Element Fleet Management Corp

Trust Capital LLC

DLL Finance LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: DLL Finance LLC introduced a cloud-based origination tool that pre-qualifies warehouse equipment leases under USD 150,000 in 15 minutes, targeting e-commerce startups.

- September 2024: CIT Group Inc. announced that its Real estate finance business acted as lead arranger on a USD 53 million financing for purchasing six industrial properties. Aminim Group purchased the portfolio of properties in the Baltimore-Washington DC area and included easy access to major transportation corridors. Nearly 500,000 sq ft of industrial space are spread across the properties, and the leases with the current tenants are solid.

- August 2024: Wells Fargo Equipment Finance rolled out “Smart Fleet,” a digital platform delivering predictive maintenance alerts and automated renewal prompts.

- July 2024: Toyota Material Handling secured a USD 2 billion credit facility to scale its Total Solutions equipment-as-a-service projects.

United States Material Handling Leasing And Financing Market Report Scope

Material handling equipment is mechanical equipment used for moving, storing, controlling, and protecting materials, products, and goods throughout manufacturing, distribution, and disposal.

The report covers the Material Handling Leasing and Financing Market in the United States.

| Forklifts |

| Automated Guided Vehicles (AGVs) |

| Conveyor Systems |

| Storage and Retrieval Systems |

| Cranes and Hoists |

| E-commerce and 3PL |

| Food and Beverage |

| Manufacturing |

| Retail (non-e-commerce) |

| Pharmaceuticals |

| Below 5,000 lbs |

| 5,000 - 10,000 lbs |

| 10,001 - 20,000 lbs |

| Above 20,000 lbs |

| Operating Lease |

| Capital Lease |

| Loan / Hire-Purchase |

| Sale and Lease-Back |

| By Equipment Type | Forklifts |

| Automated Guided Vehicles (AGVs) | |

| Conveyor Systems | |

| Storage and Retrieval Systems | |

| Cranes and Hoists | |

| By End-User Industry | E-commerce and 3PL |

| Food and Beverage | |

| Manufacturing | |

| Retail (non-e-commerce) | |

| Pharmaceuticals | |

| By Capacity Range | Below 5,000 lbs |

| 5,000 - 10,000 lbs | |

| 10,001 - 20,000 lbs | |

| Above 20,000 lbs | |

| By Financing Type | Operating Lease |

| Capital Lease | |

| Loan / Hire-Purchase | |

| Sale and Lease-Back |

Key Questions Answered in the Report

What is the projected 2031 value of United States material handling leasing and financing?

The market is forecast to reach USD 3.63 billion by 2031, reflecting a 15.39% CAGR over 2026-2031.

Which equipment category is growing fastest in U.S. warehouse financing?

Automated guided vehicles lead with a 16.03% CAGR forecast through 2031 as firms accelerate automation.

How do Section 179 deductions influence equipment leasing decisions?

Lessees can expense up to USD 1.22 million immediately, making operating leases the preferred structure for fast-turnover fleets.

Why are sale-and-leaseback deals becoming popular among warehouse operators?

They unlock trapped equity from existing fleets, funding automation upgrades without increasing balance-sheet debt, and are projected to grow at 16.95% CAGR.

Which regions are hotspots for new leasing activity?

California's Inland Empire, Texas distribution corridors, and the Southeast logistics belt exhibit the highest growth due to port modernization and e-commerce fulfillment expansion.

Page last updated on: