Manufacturing & Heavy Engineering NDT Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

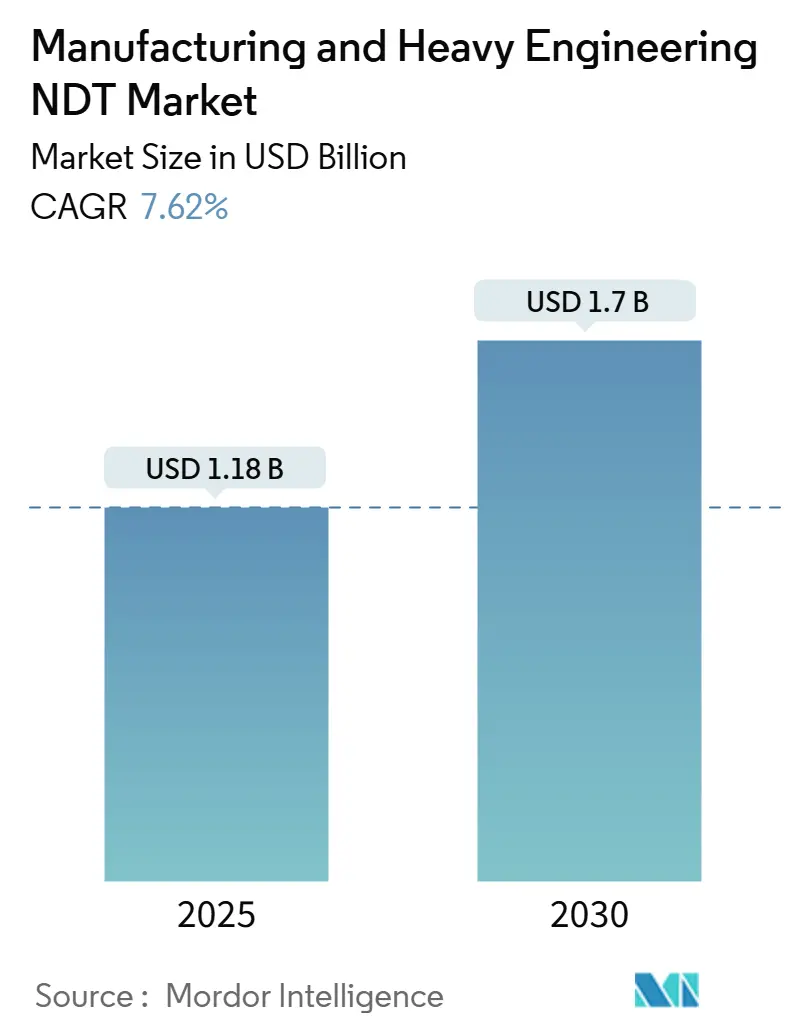

| Market Size (2025) | USD 1.18 Billion |

| Market Size (2030) | USD 1.7 Billion |

| Growth Rate (2025 - 2030) | 7.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

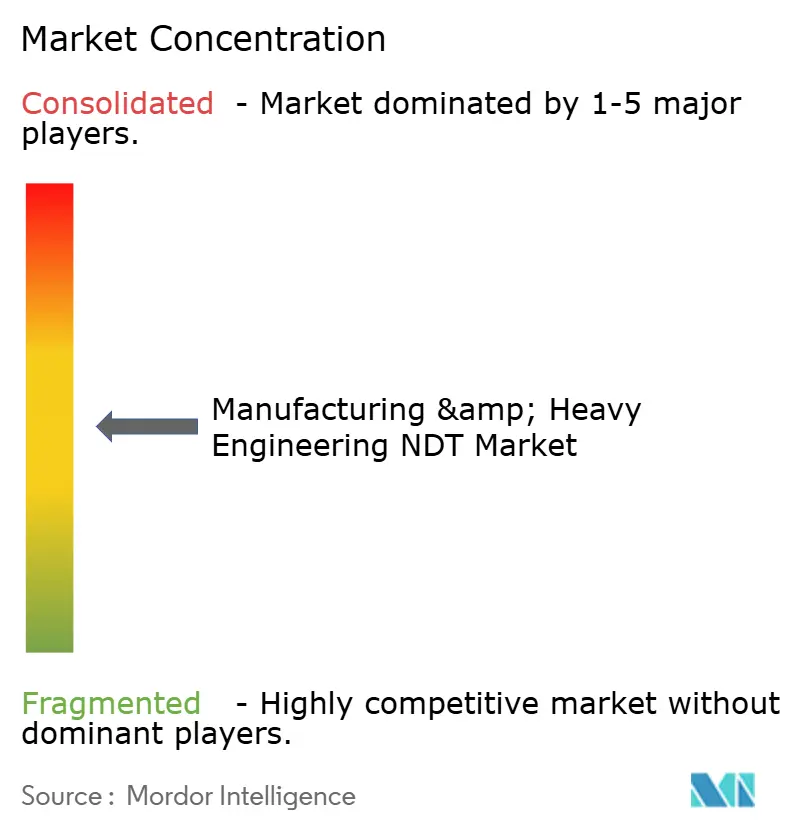

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Manufacturing & Heavy Engineering NDT Market Analysis by Mordor Intelligence

The manufacturing and heavy engineering NDT market size was USD 1.18 billion in 2025 and is projected to reach USD 1.70 billion by 2030, growing at a 7.62% CAGR over the forecast period. Surging shipbuilding activity, the modernization of steel mills, and tighter codes for hydrogen infrastructure are propelling the adoption of precision inspection technologies. Mandatory compliance with ASME Section XIII-2025 and harmonized European standards is accelerating the adoption of phased-array ultrasonics and digital record-keeping, while AI classifiers are reducing inspection cycles for large rotating equipment. The Asia-Pacific region leads demand, driven by expansions in Chinese, Japanese, and South Korean yards, whereas North America sets the regulatory pace that global suppliers must follow. Services remain the revenue backbone, as certified inspectors and field crews remain indispensable for verifying weld integrity, despite rapid advancements in software.

Key Report Takeaways

- By component, services led with 78.8% revenue share in 2024, while software is forecast to expand at a 14.7% CAGR through 2030.

- By testing method, ultrasonic testing accounted for 27.5% of the manufacturing and heavy engineering NDT market share in 2024; eddy-current testing is projected to grow at a 11.7% CAGR through 2030.

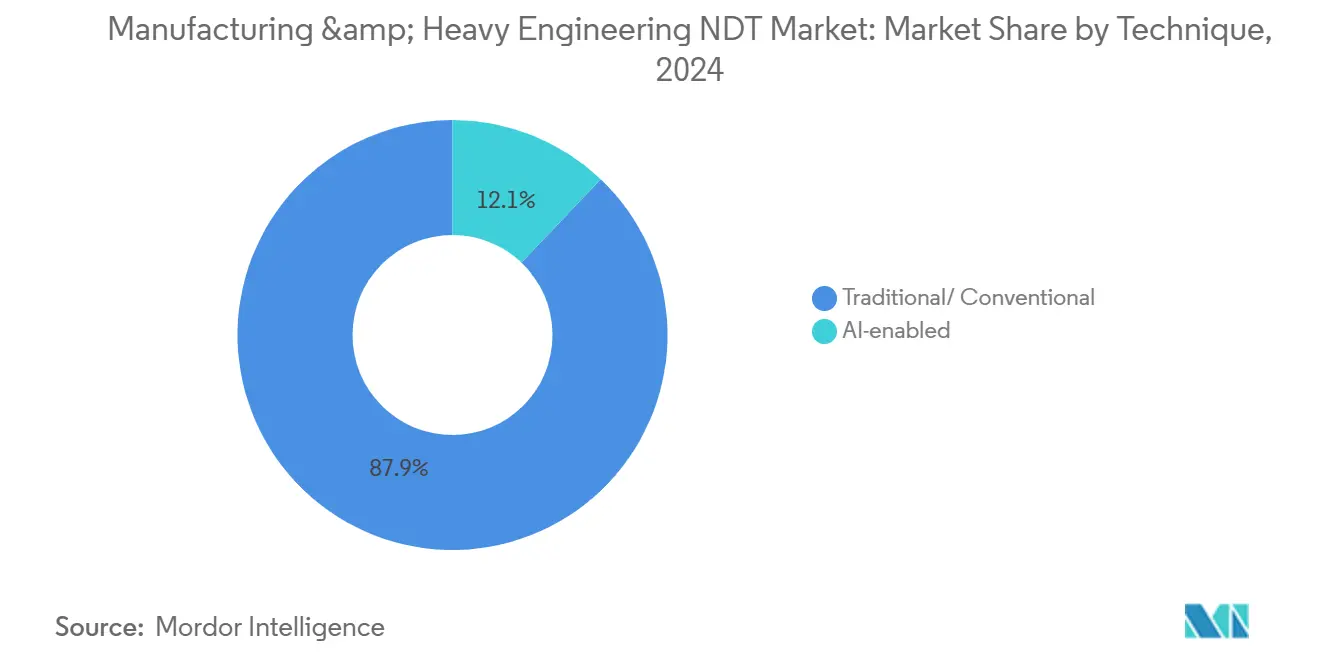

- By technique, traditional inspection approaches held 87.9% share of the manufacturing and heavy engineering NDT market size in 2024, whereas AI-enabled systems are advancing at a 17.8% CAGR through 2030.

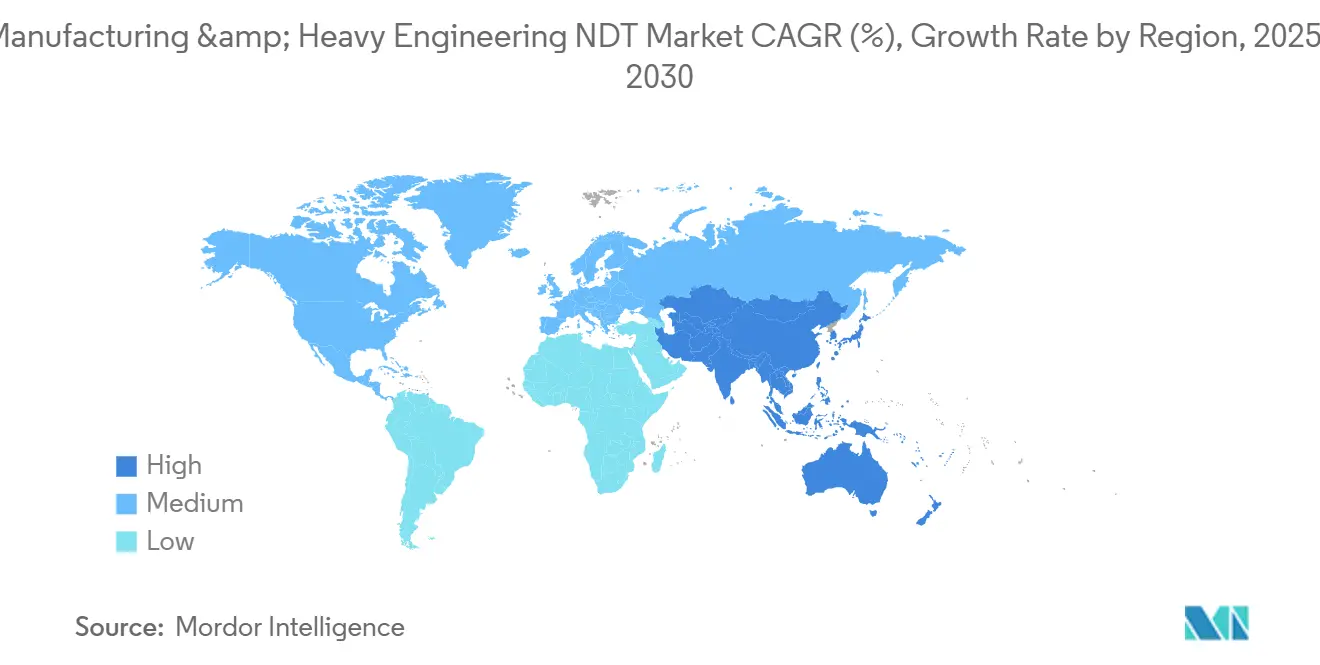

- By geography, the Asia-Pacific region accounted for 36.9% of 2024 revenue and is expected to expand at an 8.3% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Manufacturing & Heavy Engineering NDT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising capex in global shipbuilding and heavy machinery refurbishments | +1.8% | Global, with a concentration in Asia-Pacific and Europe | Medium term (2-4 years) |

| Mandatory weld-integrity audits in next-gen pressure-vessel codes (ASME XIII-2025) | +1.5% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| Digital radiography retrofits across legacy production lines | +1.2% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| AI-assisted phased-array UT slashes shutdown time on steel mills | +1.4% | Asia-Pacific core, spill-over to North America | Short term (≤ 2 years) |

| Expansion of hydrogen infrastructure needs high-precision volumetric NDT | +1.1% | Europe and North America, emerging in the Asia-Pacific | Long term (≥ 4 years) |

| Growing adoption of robotic crawler NDT for offshore wind monopiles | +0.9% | Europe and the Asia-Pacific coastal regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Capex in Global Shipbuilding and Heavy Machinery Refurbishments

Global ship orders jumped 28% in 2024 to 2,580 vessels totaling 48.7 million GT, with South Korean yards securing USD 28.4 billion in contracts.[1]Korea Shipbuilding and Offshore Engineering, “Annual Report 2024,” KSOE.CO.KR Hull integrity checks mandated by IMO SOLAS Chapter II-1 have expanded routine ultrasonic and magnetic particle testing across new builds and retrofits. Parallel heavy-machinery modernization, led by 15% annual capex gains, is enlarging inspection scopes for turbine casings and pressure vessels. Together, these trends are lifting demand for the manufacturing and heavy engineering NDT market, as fleet operators and equipment OEMs allocate larger budgets to minimize warranty risk and downtime.

Mandatory Weld-Integrity Audits in Next-Gen Pressure-Vessel Codes (ASME XIII-2025)

ASME Section XIII Division 2, effective 2025, mandates phased-array UT for welds on vessels rated above 15,000 psi. Manufacturers face a 23% rise in inspection costs but benefit from unified documentation practices that lower liability exposure. The European EN 13445 alignment is fostering a common compliance path for global chemical and hydrogen storage suppliers. The manufacturing and heavy engineering NDT market is therefore seeing rapid uptake of automated scanners and cloud-logged results that Level III inspectors can validate remotely, easing bottlenecks amid a tightening labor pool.

Digital Radiography Retrofits Across Legacy Production Lines

Spending on digital X-ray upgrades reached USD 2.1 billion in 2024, as plants replaced film with flat-panel detectors to reduce cycle times by 40% and eliminate chemistry costs.[2]GE Waygate Technologies, “Digital Radiography Market Analysis,” WAYGATE-TECH.COM Automotive casting lines now log every battery housing in cloud databases that comply with AS9100 Rev D traceability norms. Aerospace and railcar producers follow suit, advancing the manufacturing and heavy engineering NDT industry toward real-time analytics dashboards. The Asia-Pacific region accounts for 60% of retrofits, as legacy mills in China and India leapfrog older Western sites with turnkey digital cells.

AI-Assisted Phased-Array UT Slashing Shutdown Time on Steel Mills

Integrated steel works deploying AI-driven phased-array systems are trimming planned outages by 45%, saving up to USD 1.2 million daily. Algorithms trained on 500,000 defect patterns classify corrosion morphology in seconds and guide maintenance crews to hot spots without halting production. Chinese majors Baosteel and HBIS Group have paired crawler robots with these analytics engines, demonstrating the shift in the manufacturing and heavy engineering NDT market from periodic to predictive maintenance models. North American mills are piloting similar platforms as environmental rules tighten.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of ISO 9712 Level-III certified inspectors | -1.3% | Global, acute in developing markets | Long term (≥ 4 years) |

| Radio-isotope supply bottlenecks for radiographic testing | -0.8% | Global, particularly affecting remote locations | Short term (≤ 2 years) |

| High total cost of ownership for AI-enabled multi-modal systems | -0.7% | Global, more pronounced in cost-sensitive markets | Medium term (2-4 years) |

| Data-sovereignty concerns are slowing cloud-based NDT deployments | -0.5% | Europe and Asia-Pacific, regulatory compliance focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of ISO 9712 Level-III Certified Inspectors

Active Level III certificates totaled only 12,400 worldwide in 2024, compared to 18,500 positions that were needed. The Asia-Pacific region bears the brunt, with China lacking 3,200 inspectors and India 1,800. Five-year experience requirements and exam backlogs that have been pending for 18 months hinder the replenishment process. Companies in the manufacturing and heavy engineering NDT market are addressing this by utilizing tele-expertise portals and AI review tools; however, critical weld approvals still require human sign-off, which keeps capacity tight.

Radio-Isotope Supply Bottlenecks for Radiographic Testing

Iridium-192 output fell 22% in 2024 following extended outages at reactors in Canada and the Netherlands.[3]Canadian Nuclear Laboratories, “Radioisotope Supply Chain Report,” CNL.CA Portable gamma sources for pipeline girth welds became scarce, forcing contractors in remote oil fields to charter shipments at premium freight rates. Although digital radiography adoption is rising, upfront scanner costs deter smaller firms, slowing down the conversion process. This supply tension limits near-term growth for radiographic modalities within the broader manufacturing and heavy engineering NDT market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Anchor Current Revenue while Software Accelerates Digital Shift

Services accounted for 78.8% of 2024 revenue, reflecting the labor-intensive DNA of inspection, where certified crews validate code compliance onsite. The manufacturing and heavy engineering NDT market size for services is forecast to expand in tandem with the growth of hydrogen tank fabrication and offshore wind construction. Software, although it accounts for only a single-digit revenue slice today, is on track for a 14.7% CAGR as AI classifiers and cloud dashboards underpin predictive quality programs. Across 2025-2030, providers that integrate analytics with field execution are expected to win multi-year framework contracts, a shift already visible in the Asian refinery turnaround market.

The equipment segment remains resilient because phased-array probes and robotic crawlers require replacement due to wear and the need for evolving codes. Consumables, primarily film and chemicals, are tapering as digital radiography penetration increases; however, probe wedges and couplants maintain their baseline demand. Overall, the rising complexity of pressure-containing parts is driving spending toward blended offerings that combine hardware, software, and workforce into unified service packages in the manufacturing and heavy engineering NDT market.

By Testing Method: Ultrasonic Testing Dominates while Eddy-Current Gains Momentum

Ultrasonic testing captured 27.5% revenue share due to its depth penetration and absence of radiation concerns. Rolling mills, shipyards, and aerospace primes rely on phased-array sweeps for volumetric weld certification, keeping probe sales brisk. Eddy-current testing is forecast to grow at an annual rate of 11.7% as offshore wind monopile inspections and the inspection of thin-wall hydrogen cylinders demand high-frequency surface screening. The manufacturing and heavy engineering NDT market size for advanced eddy-current arrays is expected to double by 2030 as operators seek ferrite detection in high-nickel alloys.

Radiographic testing still dominates critical weld imaging on heavy sections, but the risk of isotope supply is nudging adopters toward high-energy digital systems. Magnetic particle and liquid penetrant techniques excel in automotive lines, where cast iron and aluminum parts require economical inspections for surface cracks. Thermography is moving beyond electrical maintenance into refractory lining surveys, broadening the thermal map use-case portfolio.

By Technique: Traditional Dominance Persists as AI Systems Scale Quickly

Traditional methods held an 87.9% share in 2024 because global codes and auditor familiarity keep legacy workflows entrenched. Manual UT, RT, MT, and PT services remain the mainstays of compliance in the manufacturing and heavy engineering NDT market, particularly for small shops with limited digital budgets. However, AI-enabled techniques are projected to post a 17.8% CAGR as steel conglomerates pilot full-cycle digital twins. Hybrid models, where robots gather data and cloud AI pre-classifies defects before Level III review, are emerging as the practical bridge.

The historical growth rate of traditional approaches was 4.1% from 2020 to 2024, but stricter documentation rules are expected to push the curve to 6.8% by 2030. AI systems, aided by cost declines and rising compute power at the edge, are scaling from proof-of-concept lines to fleetwide deployments. Vendors offering subscription analytics layered on top of existing probes are unlocking incremental revenue without displacing entire toolchains, thereby smoothing the upgrade process for conservative operators.

Geography Analysis

Asia-Pacific generated 36.9% of 2024 revenue and is forecast to lead regional gains at 8.3% CAGR through 2030, lifted by Chinese infrastructure drives and South Korean yard backlogs. China’s inspection services market reached USD 66 billion, with more than 53,000 agencies, while India recorded USD 659 million, poised to surpass USD 1.13 billion by FY2033. Rapid urbanization and industrial decarbonization programs are spawning opportunities for AI-enabled weld auditing and hydrogen storage validation.

North America benefits from regulatory leadership; ASME XIII-2025 has global ripple effects that funnel consulting and equipment sales back to U.S. suppliers. Reshoring of machinery and semiconductor fabs is catalyzing demand for precision RT and CT evaluations. The regional CAGR is expected to rise to 7.2% through 2030 as stimulus bills channel capital into bridges, rail, and energy infrastructure that require extensive inspection.

Europe focuses on offshore wind and advanced automotive materials, driving uptake of eddy-current and thermography systems. The Middle East and Africa show emerging potential where refinery turnarounds and cross-border pipeline megaprojects seek integrated service partners. Latin America remains modest, but rising renewable energy investments could unlock new investment opportunities. Across these regions, the manufacturing and heavy engineering NDT market is shifting toward a common pivot toward data-centric service models that transcend traditional per-scan billing.

Competitive Landscape

Competition is moderately concentrated, with GE Waygate Technologies, Olympus Evident, Eddyfi Technologies, and MISTRAS Group occupying pivotal positions across equipment and services. Each is expanding its cloud analytics suites and robotics capabilities to differentiate itself from the others. GE launched the Phoenix v|tome|x L450 CT system, featuring 450 kV energy and AI image processing, which reduces scan time by 35%. Olympus expanded its reach by acquiring Zetec for USD 285 million, thereby fortifying its eddy-current coverage in nuclear plants.[4]Olympus Evident, “Ultrasonic Testing Technology Trends,” OLYMPUS-IMS.COM

Service majors such as SGS, TÜV Rheinland, and Intertek are extending laboratory footprints in Asia-Pacific and aligning with local SOEs to secure multi-year framework agreements. Smaller specialists are carving niches in robotic crawler NDT for offshore wind, leveraging partnerships with energy operators like Equinor to gain scale. The manufacturing and heavy engineering NDT market is also witnessing vertical tie-ups, where equipment OEMs absorb service bureaus to secure through-life support contracts.

Investment in hydrogen-ready inspection competencies is accelerating. Baker Hughes earmarked USD 65 million for hydrogen embrittlement labs, recognizing the next decadal tide. Meanwhile, software-first entrants are licensing algorithm libraries to incumbents, narrowing the technology gap and elevating customer expectations around defect-classification accuracy. Collectively, these moves are nudging the market toward integrated platforms that bundle hardware, software, and certified personnel.

Manufacturing & Heavy Engineering NDT Industry Leaders

Olympus Corporation (Evident)

Eddyfi Technologies

MISTRAS Group Inc.

Bureau Veritas SA

SGS SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: GE Waygate Technologies launched the Phoenix v|tome|x L450 CT system with 450 kV energy and AI defect analytics.

- September 2024: Olympus Evident completed a USD 285 million acquisition of Zetec, expanding eddy-current testing capacity.

- August 2024: MISTRAS Group secured a USD 47 million five-year NDT contract with ExxonMobil for Gulf Coast refineries.

- July 2024: Eddyfi Technologies partnered with Equinor to develop AUV inspection for offshore wind monopiles.

Global Manufacturing & Heavy Engineering NDT Market Report Scope

| Equipment |

| Software |

| Services |

| Consumables |

| Ultrasonic Testing |

| Radiographic Testing |

| Magnetic Particle Testing |

| Liquid Penetrant Testing |

| Visual Inspection Testing |

| Eddy-Current Testing |

| Acoustic Emission Testing |

| Thermography / Infrared Testing |

| Computed Tomography Testing |

| Traditional / Conventional |

| AI-enabled |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Equipment | |

| Software | ||

| Services | ||

| Consumables | ||

| By Testing Method | Ultrasonic Testing | |

| Radiographic Testing | ||

| Magnetic Particle Testing | ||

| Liquid Penetrant Testing | ||

| Visual Inspection Testing | ||

| Eddy-Current Testing | ||

| Acoustic Emission Testing | ||

| Thermography / Infrared Testing | ||

| Computed Tomography Testing | ||

| By Technique | Traditional / Conventional | |

| AI-enabled | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the manufacturing and heavy engineering NDT market in 2030?

The market is forecasted to reach USD 1.70 billion by 2030, growing at a 7.62% CAGR.

Which region currently leads the demand for NDT in the heavy engineering sector?

Asia-Pacific commands 36.9% of 2024 revenue and is growing at an 8.3% CAGR.

Which component segment is expanding fastest?

Software is pacing the field with a 14.7% CAGR through 2030 as AI analytics gain traction.

Why are ultrasonic methods so widely used?

They offer volumetric inspection without radiation, securing 27.5% market share in 2024.

What is the biggest challenge facing service providers?

A global shortage of ISO 9712 Level III inspectors is constraining capacity and raising costs.

How are AI systems changing inspection workflows?

AI classifiers reduce steel-mill downtime by 45% and enable predictive maintenance models.

Page last updated on: