China NDT Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

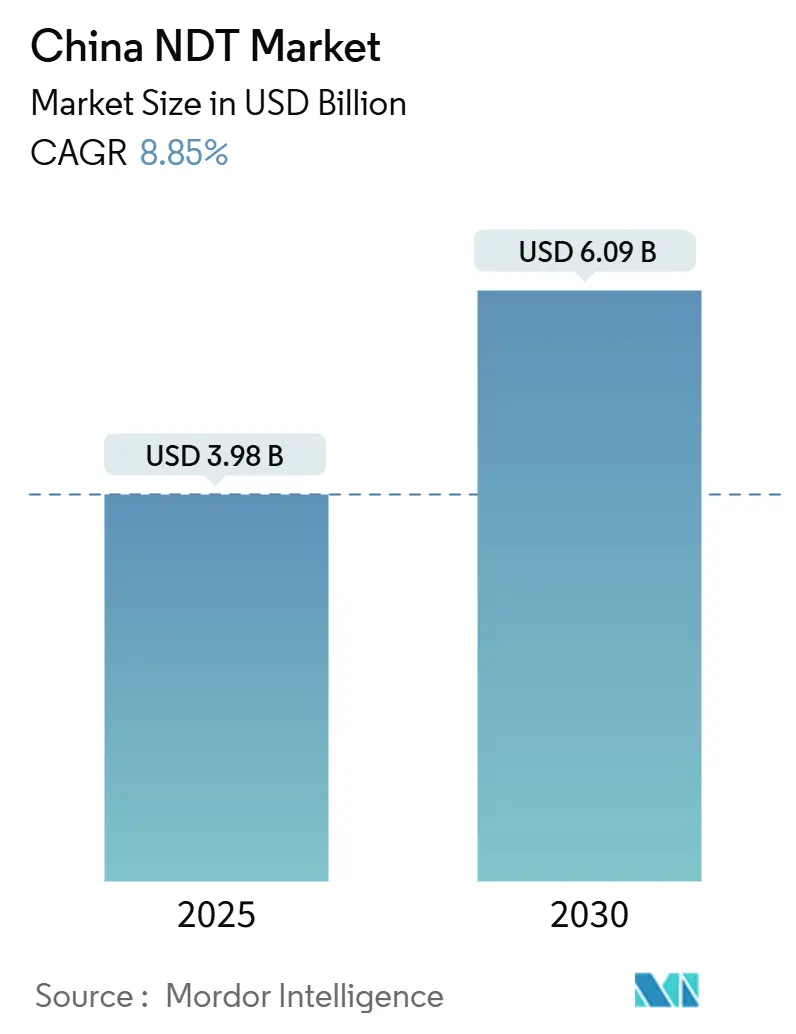

| Market Size (2025) | USD 3.98 Billion |

| Market Size (2030) | USD 6.09 Billion |

| Growth Rate (2025 - 2030) | 8.85% CAGR |

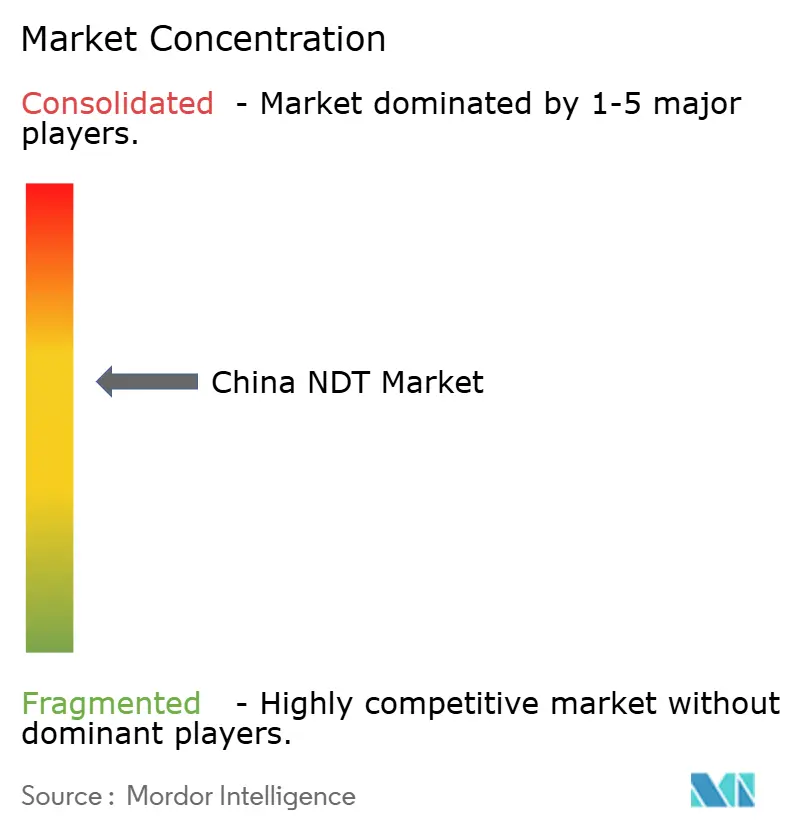

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China NDT Market Analysis by Mordor Intelligence

The China NDT market size was USD 3.98 billion in 2025 and is projected to reach USD 6.09 billion by 2030, representing an 8.85% CAGR and a 53% cumulative growth over the forecast period. Infrastructure safety mandates, the rapid electrification of transportation, and policy-driven localization of high-end inspection equipment drive this sustained rise. Accelerated rail and bridge inspections anchor stable demand, while AI-enabled software cuts inspection cycle time and boosts service productivity. Government procurement incentives favor domestic suppliers, tempering reliance on imports and nudging the China NDT market toward technological self-sufficiency. The growing adoption of automated robots further widens the addressable opportunities across hazardous mining and petrochemical sites.

Key Report Takeaways

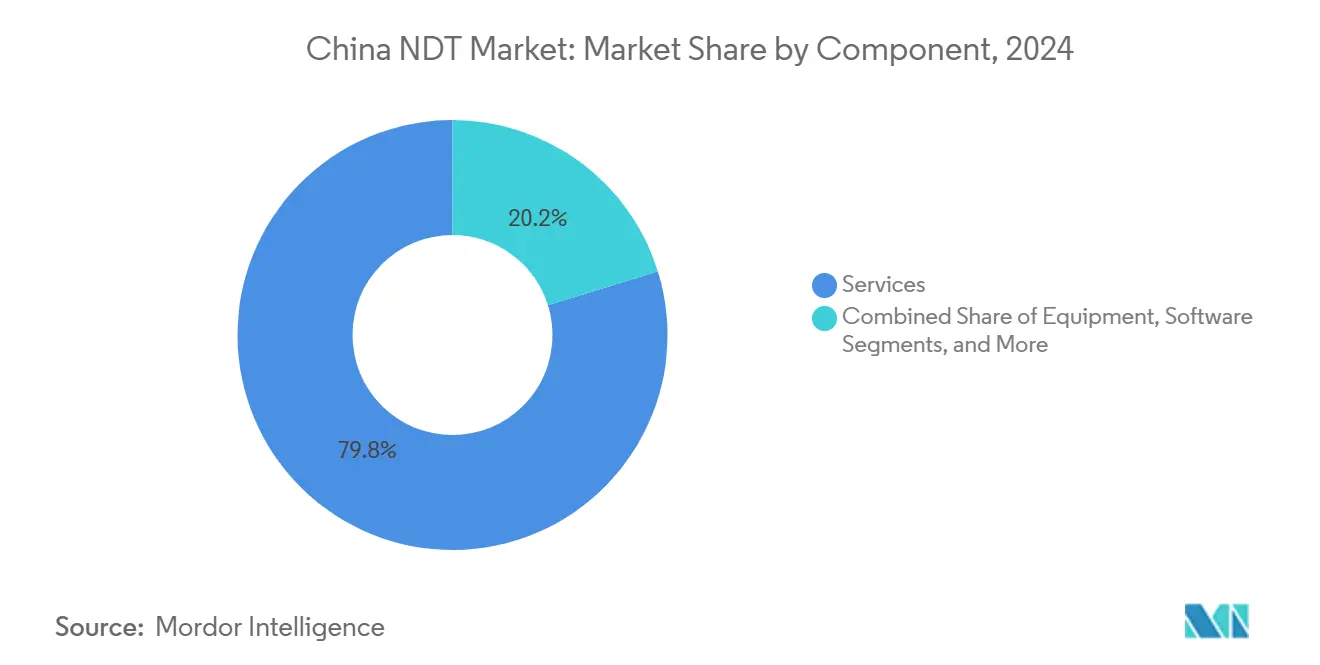

- By component, services led with 79.8% of the China NDT market share in 2024, whereas software is set to expand at a 13.7% CAGR through 2030.

- By testing method, ultrasonic testing held 28.5% of the China NDT market size in 2024, while eddy-current testing is forecast to grow at a 10.7% CAGR.

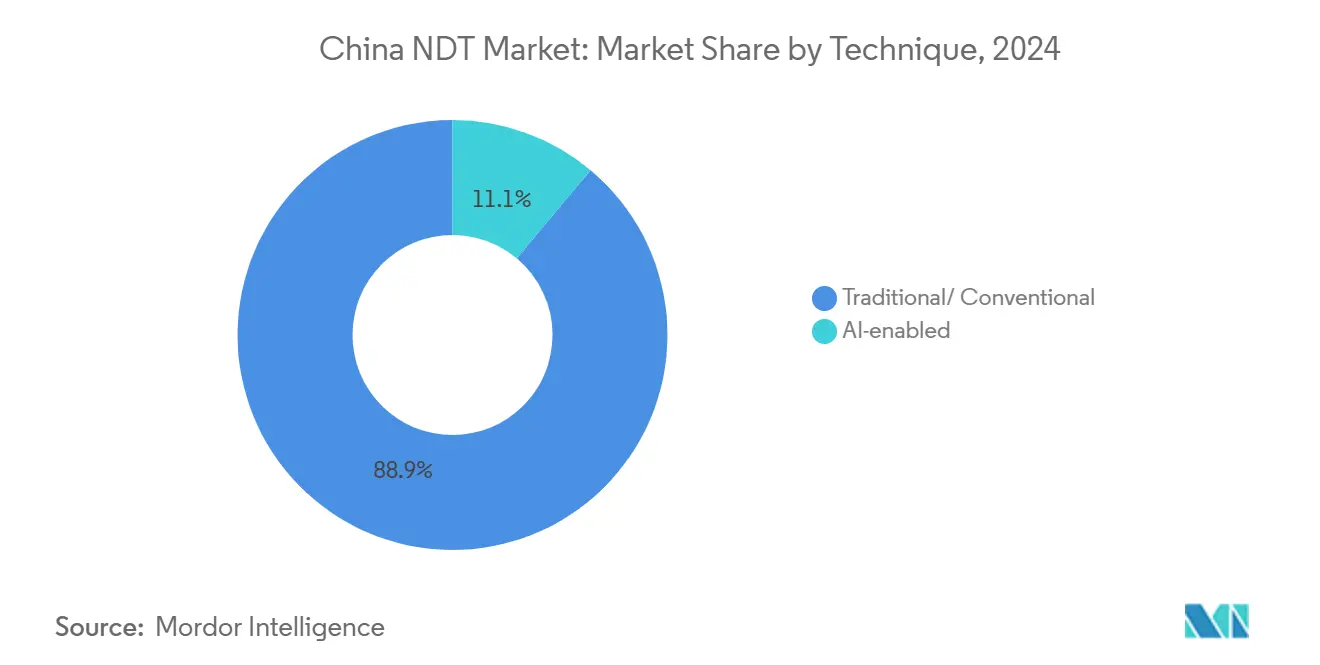

- By technique, traditional approaches captured 88.9% of the China NDT market share in 2024; AI-enabled systems are projected to rise at a 16.8% CAGR to 2030.

- By end-user, oil and gas accounted for 26.1% of the China NDT market size in 2024, whereas the automotive sector is poised for a 10.6% CAGR on the back of electric-vehicle battery testing needs.

China NDT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated infrastructure-safety mandates for bridges, high-speed rail, and pipelines | +2.1% | National, with a concentration in the Yangtze River Delta and the Pearl River Delta | Medium term (2-4 years) |

| Surging demand from the new-energy supply chain (wind-turbine blades, Li-ion batteries, PV panels) | +1.8% | National, with early gains in Jiangsu, Guangdong, and Inner Mongolia | Short term (≤ 2 years) |

| Mandatory in-service inspection reforms for special-equipment licenses (2024-25) | +1.5% | National implementation with provincial variations | Short term (≤ 2 years) |

| Domestic substitution incentives for high-end industrial CT and phased-array UT | +1.2% | National, with manufacturing hubs in Guangdong, Zhejiang, Jiangsu | Medium term (2-4 years) |

| AI-driven defect-recognition adoption is cutting inspection cycle time by ≥35% | +1.0% | Tier-1 cities and advanced manufacturing zones | Medium term (2-4 years) |

| Provincial subsidies for NDT robot deployment in hazardous environments | +0.9% | Mining regions in Shanxi, Inner Mongolia, and Xinjiang | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Infrastructure-Safety Mandates Drive Systematic Inspection Expansion

New bridge, rail, and pipeline rules require asset owners to conduct annual or biennial NDT programs, thereby firmly embedding spending into their operating budgets.[1]Peijie Zhang et al., “Parametric Analysis of Weld Defects in Orthotropic Steel Bridge Deck Based on Eddy Current Excitation Method,” Proceedings of the 6th International Conference on Structural Health Monitoring and Integrity Management, ndt.net The high-speed rail buildout under the 14th Five-Year Plan involves the addition of 40,000 km of track, which must undergo ultrasonic and eddy-current sweeps before commissioning. Pipeline operators now log digital inspection records that regulators audit, elevating demand for integrated software platforms. Offshore wind foundations and urban utility tunnels fall under broadened statutes, extending compliance to both the energy and municipal sectors. Because the rules remain in effect even during macroeconomic slowdowns, they create a recession-resistant revenue stream for qualified providers.

New-Energy Supply Chain Creates Specialized Testing Demand

Wind-blade lengths topping 100 m spark uptake of phased-array UT and thermography tools capable of subsurface detection. Lithium-ion battery producers must pass tighter GB 38031-2025 cell-integrity checks, adding visual and acoustic-emission stages to inline lines. Solar panel makers seek automated flaw identification to maintain 20% module efficiency and uphold export premiums. Provincial grants of up to RMB 50 million (USD 7.1 million) subsidize prototype inspection rigs in Xiong’an New Area, nudging startups into the China NDT market.[2]Xiong’an New Area Administrative Committee, “Measures for Encouraging High-End Testing Equipment Innovation (2024 Edition),” xiongan.gov.cn Together, these factors contribute 1.8 percentage points to growth as manufacturers establish quality controls essential for achieving their carbon neutrality ambitions.

Mandatory In-Service Inspection Reforms Expand Compliance Requirements

Starting in January 2025, pressure vessels, elevators, and industrial boilers will all require shorter inspection intervals performed by Level-III technicians, which is expected to boost recurring service hours.[3]State Administration for Market Regulation, “Special Equipment Safety Technical Code: Periodic Inspection Rules (Effective January 2025),” samr.gov.cn Facilities must archive results through approved software, lifting demand for cloud-linked reporting suites. Permanent sensor installations gain traction where risk thresholds trigger continuous monitoring, opening avenues for acoustic-emission and guided-wave systems. Though capacity tightens as technician shortages persist, accredited firms that scale headcount or adopt AI analysis unlock a protected revenue runway.

Domestic Substitution Policies Accelerate Equipment Localization

The Ministry of Industry and Information Technology awards up to 15% price premiums to state-owned buyers that procure Chinese-made CT and phased-array UT units. Equipment subsidies covering 30% of the purchase price stimulate orders for the SIUI and Beijing Zhongke Innovation Technology platforms. Software developers are eligible for national AI funds, which will accelerate the rollout of defect-recognition algorithms. While component supply gaps for X-ray tubes persist, substitution schemes reduce import exposure by 1.2 percentage points of the CAGR and lay the groundwork for a stronger domestic value chain.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of certified level-III technicians amid fast demand growth | -1.8% | National, with acute shortages in Tier-2 and Tier-3 cities | Short term (≤ 2 years) |

| High upfront cost of advanced CT/PAUT systems for SME fabricators | -1.2% | Manufacturing clusters in Zhejiang, Jiangsu, and Guangdong | Medium term (2-4 years) |

| Fragmented standards across industries are delaying AI algorithm validation | -0.9% | National, with sector-specific variations | Medium term (2-4 years) |

| Import dependence for key sensors and X-ray tubes is causing supply risk | -0.7% | National, with logistics concentration in coastal ports | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Certified Technician Shortage Constrains Service Capacity Expansion

China needs 15,000 additional Level-III specialists by 2030, but training pipelines add fewer than 3,000 annually, widening a skills gap that trims growth by 1.8 percentage points. ISO 9712 certification requires multi-year apprenticeships, which can delay workforce replenishment. Pay premiums siphon talent to tier-1 cities, leaving inland hubs understaffed. Smaller factories face longer wait times and higher service fees, deterring adoption of proactive inspection regimes.

High Equipment Costs Limit SME Adoption of Advanced Technologies

Industrial CT systems priced between USD 800,000 and USD 1.5 million exceed the budgets of fabricators with annual revenues under USD 10 million, hindering the diffusion of technology. Phased-array UT packages exceeding USD 200,000 also require specialized probes and software, lifting lifecycle costs. Financing hurdles persist as banks struggle to value NDT assets, and the thin secondary market curbs leasing options. Consequently, SMEs rely on third-party service providers, sustaining the dominance of the outsourced model but limiting the upside of equipment sales.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Remain Dominant as Software Surges

Services claimed 79.8% of the China NDT market share in 2024, mirroring enterprises’ preference for outsourcing inspections to firms with certified staff and turnkey equipment fleets. Equipment vendors posted steady gains, driven by localization subsidies, while consumables volumes rose in tandem with the mandated inspection frequency. The software sub-segment is projected to accelerate at a 13.7% CAGR, fueled by AI analytics that reduce manual interpretation workloads and meet digital reporting edicts.

Outsourced providers leverage economies of scale to amortize high-end CT and phased-array UT rigs across multiple clients, keeping unit costs attractive. AI-enabled applications have reached 93.7% accuracy in acoustic-emission waveform detection, validating commercial adoption and driving software renewals. Consumables such as coupling gels and penetrants benefit from the stricter annual test cadence on bridges and pipelines. Overall, the service-heavy structure highlights how the China NDT market continues to reward firms that combine field expertise with cloud-based analytics, rather than relying solely on pure-play hardware models.

By Testing Method: Ultrasonic Leads, Eddy-Current Gains Pace

Ultrasonic testing accounted for 28.5% of the Chinese NDT market size in 2024, prized for its versatility across weld inspections, rail flaw detection, and pressure vessel applications. Yet, eddy-current testing is slated for a 10.7% CAGR through 2030, thanks to its superior sensitivity for non-ferromagnetic alloys used in EV batteries and aerospace skins. Radiographic, magnetic-particle, and liquid-penetrant methods retain niche roles for deep penetration or the discovery of surface cracks.

Advances in eddy-current probe design now achieve 93% crack and 90% pitting detection accuracy in stainless steel tubes, surpassing the performance of legacy IRIS ultrasound alternatives. Visual inspection remains relevant for rapid screening, while acoustic-emission systems are gaining traction in the structural health monitoring of bridges. Thermography is gaining a foothold in power-distribution maintenance, and computed tomography supports precision casting validation in aerospace, albeit with limited SME adoption due to the technology's capital-intensive nature.

By Technique: AI-Enabled Inspection Challenges Conventional Practice

Traditional techniques still occupy 88.9% of the Chinese NDT market share, reflecting regulatory comfort and inspector familiarity. However, AI-enabled systems are accelerating at a 16.8% CAGR, tapping labor shortages and the promise of 35% cycle-time savings. Early deployments cluster in automotive and electronics plants that run high-volume production lines and value real-time defect flags.

Multi-model automation that layers anomaly-detection autoencoders with object-recognition networks allows selective human review and maintains near-zero false-negative rates. Regulatory agencies are drafting validation protocols, and once finalized, AI adoption is expected to broaden to the power generation and petrochemical sectors. Conventional practice will persist in safety-critical assets until algorithms clear certification benchmarks, ensuring a gradual rather than abrupt transition.

By End-User Industry: Oil and Gas Tops, Automotive Accelerates

Oil and gas operations accounted for 26.1% of the 2024 spend, as pipeline integrity checks and refinery turnarounds require frequent ultrasonic, radiographic, and magnetic-particle testing. Meanwhile, the automotive and transportation sectors are showing the fastest expansion at a 10.6% CAGR, driven by battery cell testing and lightweight chassis weld verification under GB 38031-2025. Power generation’s nuclear, wind, and hydro assets supply a stable baseline demand through life-extension programs.

Electric-vehicle assemblers require inline CT scans of battery modules to guard against thermal-runaway defects, driving equipment upgrades, and specialized service contracts. Aerospace and defense customers seek computed tomography precision for composite airframe parts, albeit in smaller volumes. Construction, chemical, marine, and mining end-users round out the client base, each with unique access and environmental challenges that favor robotic crawlers and corrosion-mapping ultrasonics.

Geography Analysis

Coastal megaregions dominate the China NDT market. The Yangtze River Delta, encompassing Shanghai, Jiangsu, and Zhejiang, boasts the largest concentration of certified laboratories serving container ports, shipyards, and semiconductor fabs. Proximity to global suppliers and universities sustains a robust pipeline of inspectors and researchers. The Pearl River Delta, led by Guangdong, ranks second owing to electronics and auto exports that mandate precision inspection in assembly lines.

Northern provinces show divergent patterns. Beijing-Tianjin-Hebei integration programs drive bridge retrofit work, while Shanxi and Inner Mongolia deploy NDT robots in coal mines to comply with new safety caps. Western provinces, such as Xinjiang and Tibet, are registering emerging demand tied to the Belt and Road railways and hydropower dams. However, sparse infrastructure and long logistics chains raise operating costs and extend mobilization lead times.

Central China’s Hubei, Hunan, and Henan provinces increasingly attract automotive and rail-equipment factories, leveraging lower land prices and improving logistics corridors. Wuhan’s vehicle battery cluster alone commands multiyear contracts for phased-array UT and CT services, reflecting domestic OEM quality pushes. Collectively, inland growth drives geographic rebalancing, nudging providers to establish satellite depots that shorten response times and cut travel costs.

Competitive Landscape

Market concentration is moderate, with domestic champions gaining share under government substitution programs. Shantou Institute of Ultrasonic Instruments Co Ltd (SIUI) released a cloud-connected SyncScan phased-array detector in April 2025, targeting export markets through Hong Kong channels. Beijing Zhongke Innovation Technology and Unicomp Technology supply CT scanners and real-time X-ray units, scaling capacity to 10 units per month in Shenzhen to meet the demand for electronics.[4]Unicomp Technology, “Real Time X-Ray Machine 60 mm Penetration,” unicompXray.com

International suppliers retain niches in ultra-high-resolution sensors and dual-energy CT, but face a 15% price disadvantage in state-owned tenders. Start-ups focus on AI analytics platforms that retrofit onto existing hardware, attempting to decouple software value from capital expenditure. Service providers differentiate via nationwide technician networks and specialized robots for confined spaces. Despite rising rivalry, regulatory hurdles, and certification protocols, these protections protect incumbents, preventing price erosion in mission-critical inspections.

China NDT Industry Leaders

Shantou Institute of Ultrasonic Instruments Co Ltd (SIUI)

Beijing Zhongke Innovation Technology Co Ltd

Unicomp Technology Co Ltd

Guangdong Zhengye Technology Co Ltd

Dandong Huari Science and Technology Co Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: SIUI launched the SyncScan phased-array ultrasonic detector, featuring weld-simulation software and remote control functionality.

- March 2025: Unicomp Technology expanded Shenzhen CT production to 10 units per month to serve automotive and electronics customers.

- January 2025: Qingcheng AE Institute achieved 93.7% accuracy in AI acoustic-emission pattern recognition using ECAPA-TDNN models, validating automated defect classification for bridge health monitoring.

- January 2025: The State Administration for Market Regulation implemented mandatory Level-III certification for all critical pressure vessel inspections.

China NDT Market Report Scope

| Equipment |

| Software |

| Services |

| Consumables |

| Ultrasonic Testing |

| Radiographic Testing |

| Magnetic Particle Testing |

| Liquid Penetrant Testing |

| Visual Inspection Testing |

| Eddy-Current Testing |

| Acoustic Emission Testing |

| Thermography / Infrared Testing |

| Computed Tomography Testing |

| Traditional / Conventional |

| AI-Enabled |

| Oil and Gas |

| Power Generation |

| Aerospace |

| Defense |

| Automotive and Transportation |

| Manufacturing and Heavy Engineering |

| Construction and Infrastructure |

| Chemical and Petrochemical |

| Marine and Ship Building |

| Electronics and Semiconductor |

| Mining |

| Medical Devices |

| Others |

| By Component | Equipment |

| Software | |

| Services | |

| Consumables | |

| By Testing Method | Ultrasonic Testing |

| Radiographic Testing | |

| Magnetic Particle Testing | |

| Liquid Penetrant Testing | |

| Visual Inspection Testing | |

| Eddy-Current Testing | |

| Acoustic Emission Testing | |

| Thermography / Infrared Testing | |

| Computed Tomography Testing | |

| By Technique | Traditional / Conventional |

| AI-Enabled | |

| By End-user Industry | Oil and Gas |

| Power Generation | |

| Aerospace | |

| Defense | |

| Automotive and Transportation | |

| Manufacturing and Heavy Engineering | |

| Construction and Infrastructure | |

| Chemical and Petrochemical | |

| Marine and Ship Building | |

| Electronics and Semiconductor | |

| Mining | |

| Medical Devices | |

| Others |

Key Questions Answered in the Report

What is the forecast value of the China NDT market in 2030?

The market is projected to reach USD 6.09 billion by 2030, expanding at an 8.85% CAGR.

Which component dominates spending?

Services lead with 79.8% of 2024 revenue due to widespread outsourcing of inspections to certified providers.

Which testing method is growing fastest?

Eddy-current testing is expected to log a 10.7% CAGR through 2030, driven by non-ferromagnetic materials inspection in EV batteries and aerospace parts.

How are AI-enabled techniques impacting inspection cycles?

AI-powered analysis can reduce inspection cycle time by 35%, alleviating technician shortages and increasing throughput.

What regions hold the greatest concentration of NDT demand?

The Yangtze River Delta and Pearl River Delta together account for the largest share owing to dense manufacturing, port, and infrastructure activity.

Page last updated on: