Automotive NDT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

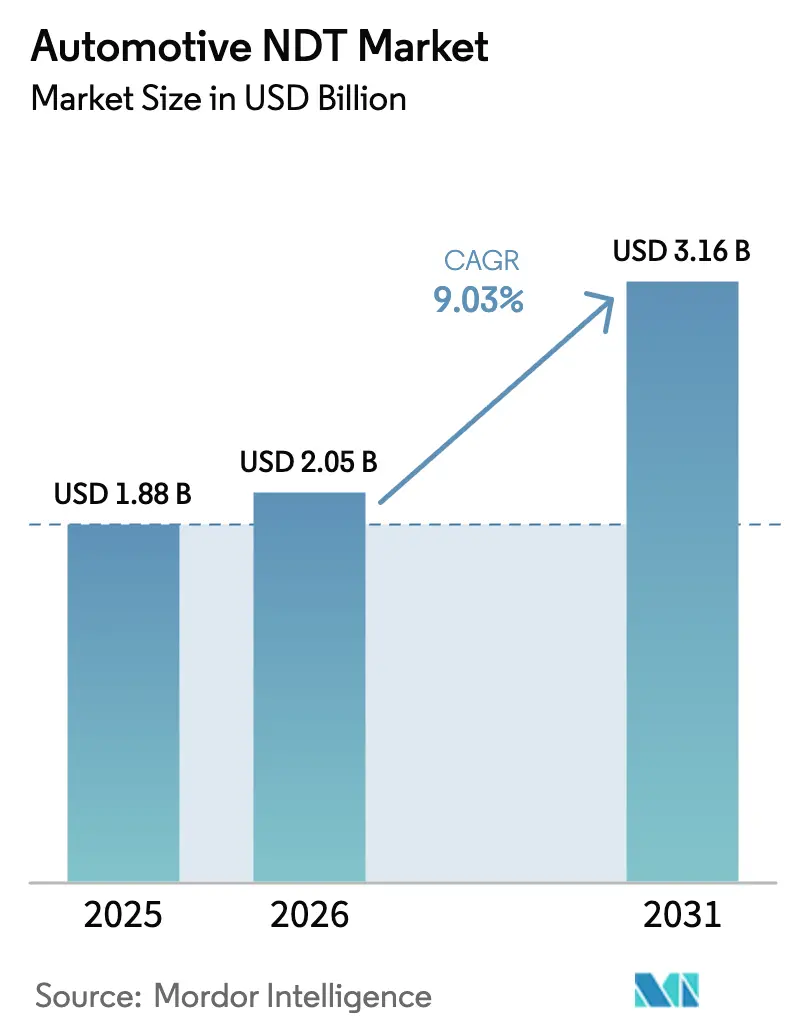

| Market Size (2026) | USD 2.05 Billion |

| Market Size (2031) | USD 3.16 Billion |

| Growth Rate (2026 - 2031) | 9.03% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

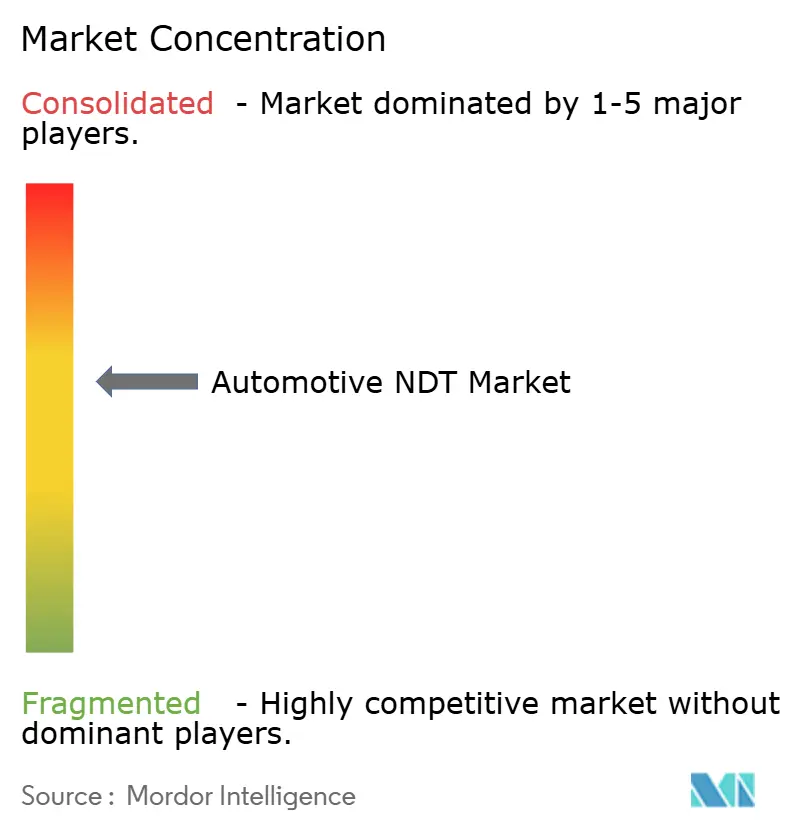

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive NDT Market Analysis by Mordor Intelligence

The Automotive NDT market size was valued at USD 1.88 billion in 2025 and estimated to grow from USD 2.05 billion in 2026 to reach USD 3.16 billion by 2031, at a CAGR of 9.03% during the forecast period (2026-2031). This momentum reflects the industry’s rapidly growing reliance on advanced inspection technologies that safeguard lightweight multi-material structures, validate the integrity of electric-vehicle (EV) batteries, and meet increasingly stringent global safety regulations. Automakers are integrating inline computed tomography (CT) scanners and high-frequency ultrasonic arrays to locate subsurface flaws in aluminum castings and carbon-fiber parts without slowing takt times, while AI-enabled defect recognition software improves detection repeatability to above 97% for critical castings. Heightened capital spending on robotics-ready systems, the spread of Industry 4.0 architectures, and cross-border regulatory harmonization are expanding supplier opportunities across every major production hub. Meanwhile, a shortage of certified technicians is strengthening demand for turnkey inspection services and automated workflows. Strategic consolidation exemplified by SGS’s USD 1.325 billion purchase of Applied Technical Services signals a race to build global reach and full-stack technology portfolios that can address the accelerating requirements of the Automotive NDT market.

Key Report Takeaways

- By component, equipment commanded 48.10% of the Automotive NDT market share in 2025, while software is projected to grow at a 10.05% CAGR to 2031.

- By testing method, ultrasonic testing accounted for 32.20% of the Automotive NDT market size in 2025; computed tomography is expected to expand at a 10.96% CAGR through 2031.

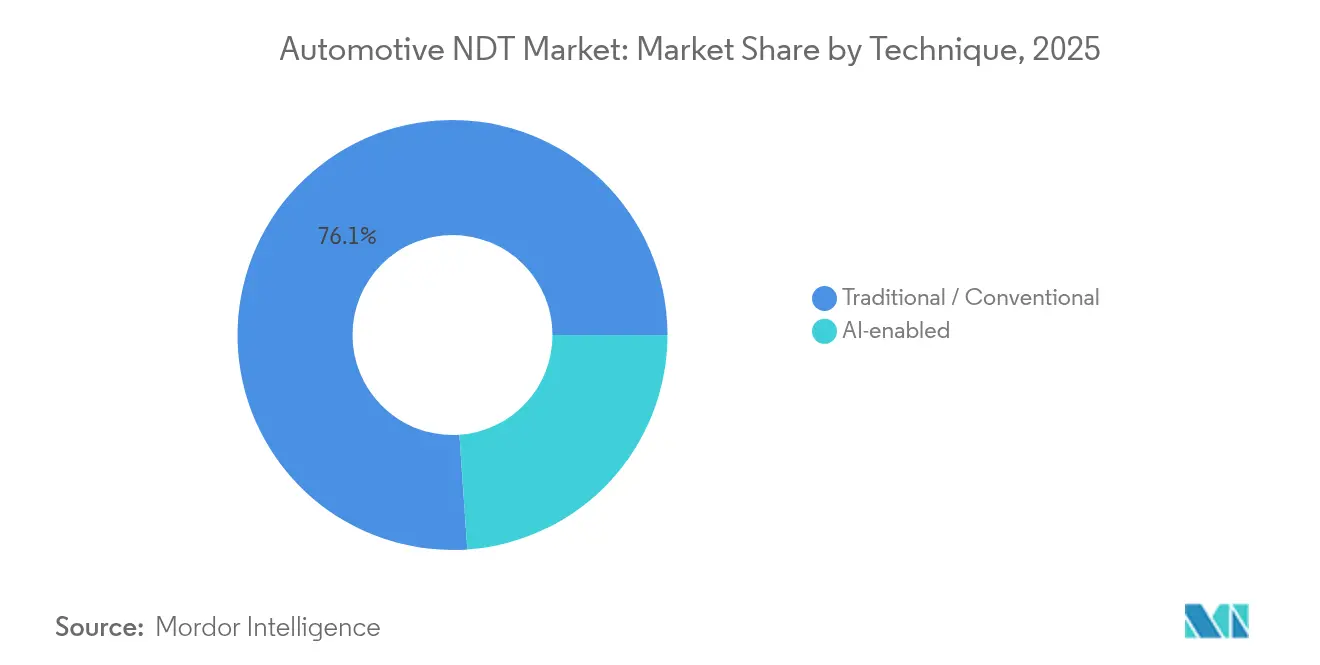

- By technique, traditional methods accounted for 76.10% of the Automotive NDT market share in 2025, whereas AI-enabled systems are forecast to post a 9.88% CAGR to 2031.

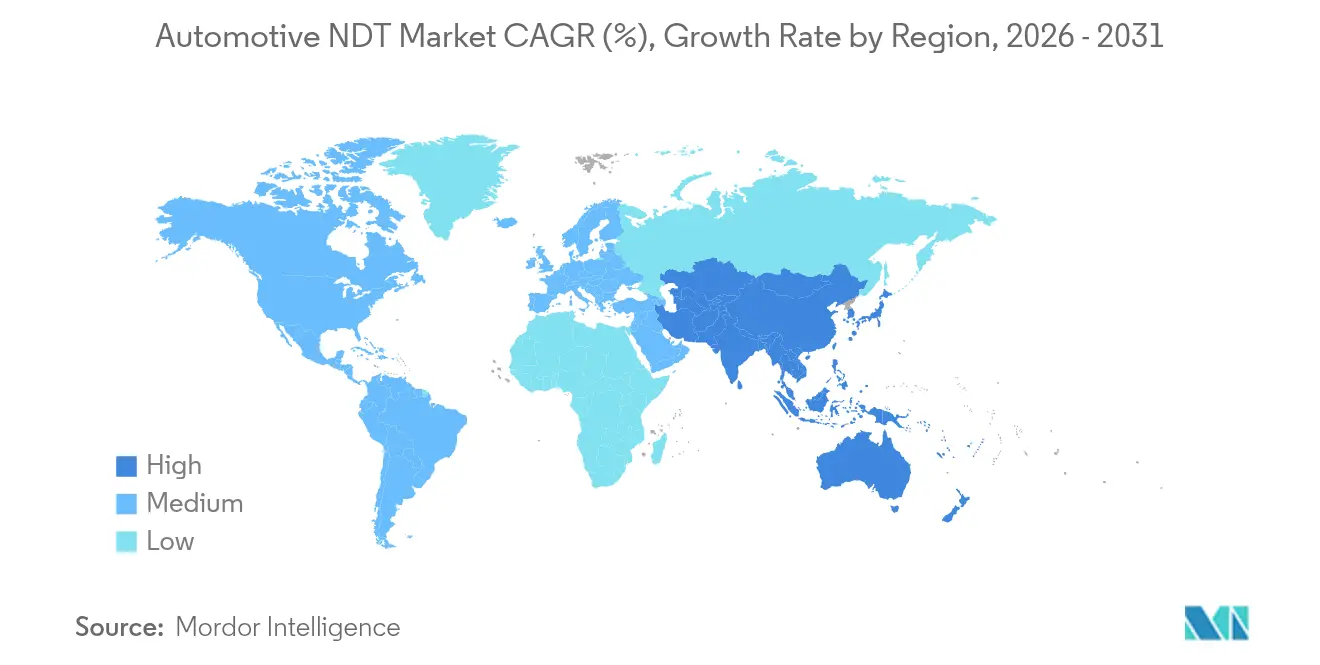

- By geography, North America led the Automotive NDT market with a 37.45% revenue share in 2025; the Asia Pacific is expected to advance at a 10.12% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive NDT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising use of advanced lightweight materials | +2.1% | North America and Europe core; global spill-over | Medium term (2-4 years) |

| Surge in electric-vehicle battery inspections | +2.8% | Asia Pacific and North America early leaders | Short term (≤ 2 years) |

| Stringent global vehicle-safety mandates | +1.9% | Global | Long term (≥ 4 years) |

| Robotics-driven inline NDT automation | +1.7% | North America and Europe; expanding Asia-Pacific | Medium term (2-4 years) |

| Shift to full-CT for additively manufactured parts | +1.4% | North America and Europe | Long term (≥ 4 years) |

| Insurance-led demand for in-service portable NDT | +0.9% | North America and Europe; developed Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Use of Advanced Lightweight Materials

Automakers are swapping traditional steel structures for aluminum alloys and carbon-fiber-reinforced polymers, which boost fuel economy but demand more sophisticated inspection. Ultrasonic phased-array systems now scan bonded joints to catch delamination that could trigger adhesive failure under crash loads. Inline CT units mounted on production conveyors enable 100% volumetric checks without removing parts from the takt schedule, a method BMW employs for carbon-fiber roof frames. AI-powered analytics have lifted void-detection repeatability for aluminum casting to 97.25%, though accuracy in thickness transitions still lags at 86.97% repeatability. ISO 9001 and IATF 16949 certifications require suppliers to demonstrate full traceability, thereby promoting the wider adoption of digital archiving and barcode-linked image storage. As lightweighting trends accelerate, the Automotive NDT market will broaden its equipment base across every new model launch.

Surge in Electric-Vehicle Battery Inspections

Lithium-ion packs introduce thermal-runaway risk that OEMs mitigate through rigorous CT and ultrasonic validation of cell welds, electrode alignment, and coolant-plate bonding. Hexagon has rolled out high-energy CT lines that image 1,000 cells per hour, while VisiConsult secured EUR 1.1 million to commercialize inline CT for prismatic modules. UN 38.3 shipping rules and draft IEC 62660 standards force proof of cell integrity before transportation, generating near-term demand spikes for portable radiography and eddy-current scanners. In-service diagnostics are also advancing: low-frequency ultrasound maps electrolyte volume loss in aging packs to pre-empt warranty claims. These factors reinforce a 2.8% positive contribution to the Automotive NDT market’s CAGR.

Stringent Global Vehicle Safety Mandates

NHTSA’s roadmap introduces THOR-50M and WorldSID anthropomorphic dummies by model year 2027, which raises the bar for structural soundness of sensor brackets and crash-energy paths. Euro NCAP aligns in parallel, compelling multinational OEMs to validate identical crash-reinforcement nodes across regions. Advanced emergency-braking (AEB) rules covering speeds up to 90 mph by 2029 are intensifying scrutiny of radar mounts and camera housings that must stay calibrated after minor impacts. Zendar’s test data showed only 17% of 2023 models fully avoided daytime pedestrian dummies, underscoring the importance of fault-free sensor housing.[1]Zendar Inc., “How OEMs Can Meet NHTSA’s Stringent AEB Requirements,” zendar.io These regulations extend inspection to energy-absorbing bumpers, pedestrian leg-form zones, and carbon-fiber front-end carriers. The result is a multi-year uplift in the Automotive NDT market as OEMs retrofit lines for higher-resolution scanning.

Robotics Driven Inline NDT Automation

Automated spot-weld scanners equipped with six-axis robots now inspect up to 300 welds per vehicle at cycle times under 3 seconds each, quadrupling throughput versus manual sampling. Motion-programmed CT gantries store part recipes that ensure sub-millimeter reproducibility across shifts and plants. GPU-accelerated algorithms flag defects in real-time and feed decisions back to programmable logic controllers for the immediate diversion of non-conforming parts. The Automotive NDT market benefits from reduced operator dependence and higher statistical confidence, convincing tier-one suppliers to budget for fully automated cells in their capital plans for 2026-2028. ISO 13485 and IATF 16949 clauses on measurement uncertainty encourage the adoption of systems with built-in self-calibration, strengthening the mid-term CAGR uplift.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of advanced NDT equipment | −1.8% | Global; emerging markets most impacted | Short term (≤ 2 years) |

| Shortage of certified NDT technicians | −1.3% | North America and Europe acute | Long term (≥ 4 years) |

| Production downtime from radiographic safety zones | −0.9% | Global manufacturing hubs | Medium term (2-4 years) |

| IP concerns over cloud-based analytics | −0.7% | Global; heightened Asia Pacific sensitivity | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Advanced NDT Equipment

Industrial CT cabinets capable of 225-kV scans cost over USD 500,000, and adding conveyors, shielding, and robotic loaders often doubles the expenditure, challenging the ROI thresholds of tier-two suppliers.[2]North Star Imaging, “How 2D Digital Radiography Enhances Automotive and Aerospace Quality Control,” ndt.net Rapid sensor evolution risks obsolescence before depreciation ends, while radiographic rooms demand costly lead lining and exclusion zones that interrupt lean layouts. NHTSA’s forthcoming 2029 AEB mandate already requires OEMs to allocate USD 430 million per brand for sensor upgrades, thereby inflating parallel inspection costs. Financing constraints weigh heaviest on emerging-market plants where local content rules collide with foreign-currency equipment pricing, shaving 1.8 points off the Automotive NDT market CAGR in the near term.

Shortage of Certified NDT Technicians

An aging workforce is exiting at a faster rate than certification bodies can replenish, resulting in unfilled vacancies for ASNT Level III ultrasonic examiners in North America and Europe for months. Modern curricula often lag behind AI-assisted interpretation skills, resulting in machines flagging more defects than operators can validate, which in turn forces line slowdowns. Companies respond by outsourcing audits to service providers, but travel and mobilization costs escalate when peak demand coincides with model launches. Scholarship programs and simulator-based training may ease the crunch, yet meaningful relief is unlikely before 2028, exerting a long-term drag on the expansion of the Automotive NDT market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Equipment Dominance Drives Market Foundation

Equipment accounted for 48.10% of the Automotive NDT market share in 2025, reflecting the sector’s capital-intensive backbone. Nikon, Yxlon, and North Star Imaging report multi-year order backlogs as OEMs refurbish CT lines for EV platforms. Conversely, software revenue is projected to grow at a 10.05% CAGR, driven by AI engines that automate defect classification and cloud portals that store terabytes of DICONDE images. The Automotive NDT market size tied to services remains resilient because outsourcing fills technician gaps and ensures neutrality during supplier audits. Consumables, although smaller, gain from the swelling installed base of digital detectors that require periodic flat-field calibrations.

Regulatory frameworks, such as ISO 17025, require laboratories to recalibrate gauges annually, generating steady demand for certified blocks and verification coupons. Hyundai’s purchase of Nikon X-ray CT units to verify airbag initiators demonstrates how capital equipment sales pull downstream services and consumables along the value chain. Meanwhile, VisiConsult’s ERDF-backed R&D underscores the symbiosis between hardware providers and algorithm specialists, anchoring long-term revenue diversity within the Automotive NDT market.

By Testing Method: Ultrasonic Leadership Faces CT Challenge

Ultrasonic systems accounted for 32.20% of the Automotive NDT market size in 2025, as their time-of-flight diffraction and phased-array modes effectively tackle spot weld, bond-line, and battery-foil inspections. Yet CT’s 10.96% CAGR makes it the fastest riser through 2031, fueled by additive-manufacturing use cases that demand full-volume fidelity. Radiography still shoulders bulk casting checks, but digital detectors and laminography upgrades keep it competitive. Magnetic-particle and liquid-penetrant methods remain staples for forgings and axle shafts, while eddy-current probes gain popularity for conductive EV busbars.

BMW’s inline CT deployment for carbon-fiber lids illustrates CT’s climb toward mainstream status. Volkswagen couples high-energy CT with AI segmentation to measure silicon-carbide inverter housings, cutting sectioning scrap. Meanwhile, visual inspection harnesses machine-vision cameras linked to deep-learning models, trimming false rejects. ASTM E3327 probability-of-detection standards guide all methods toward documented performance baselines, fostering method innovation and the creation of mix-and-match inspection cells within the Automotive NDT market.

By Technique: AI-Enabled Systems Accelerate Traditional Methods

Traditional approaches captured 76.10% of the Automotive NDT market share in 2025, but AI-enabled platforms are set to outperform at a 9.88% CAGR as predictive algorithms mature. Hybrid deployments embed neural networks within existing ultrasonic consoles, enhancing weld-flaw recognition without requiring the scrapping of legacy hardware. Cloud dashboards enable multi-plant comparison of defect trends, allowing for earlier tooling corrections. Suppliers deploying GPU clusters achieve real-time volumetric reconstructions, shortening CT scan cycles from 15 minutes to under 90 seconds.

Data-sovereignty concerns motivate on-premise edge processing, especially in Germany and Japan, yet even there, OEMs pilot encrypted tunnels for supplier data exchange. ISO 27001 compliance and IATF cybersecurity add layers of validation, pushing vendors to harden firmware and audit code bases. As deep-learning misclassification rates fall below 1.5%, AI-enabled modalities continue to edge further into safety-critical domains, such as chassis welds, thereby increasing their contribution to the overall Automotive NDT market.

Geography Analysis

North America generated 37.45% of 2025 revenue, buoyed by NHTSA’s safety regime and a tight feedback loop between Detroit OEMs and Midwest testing labs. Asia Pacific, however, is projected to grow 10.12% annually as China, Japan, and South Korea forge giga-factories and export EV drivetrains worldwide. European volume remains stable, underpinned by premium brands that pioneer composite monocoques and bio-based resins. South America and the MENA region trail, but attract Greenfield plants that embed modern inspection from day one, avoiding legacy equipment pitfalls.

The United States leads investment in robotics-ready CT cells, while Canada specializes in composite research and Mexico focuses on cost-optimized service centers. The Asia Pacific’s Automotive NDT market size is expanding at the fastest rate, thanks to China’s giga-factory boom and Japanese breakthroughs in high-frequency phased arrays that visualize 30-micron voids in solid-state batteries. India is rolling out training schemes with ASNT to fill its technician gap, creating new service outsourcing streams. Europe anchors high-end applications; Germany deploys 9-MeV linear accelerators for CT scanning of diesel-engine blocks, while the United Kingdom advances AI-based defect segmentation software. Harmonized Euro NCAP protocols simplify cross-border supplier approvals, driving demand for pan-European inspection campaigns. South America and Africa, although smaller, are seeing niche growth around export-oriented chassis plants adopting portable ultrasonic crawlers to comply with European customer audits. Collectively, these dynamics diversify the customer mix, spreading Automotive NDT market risk across mature and emerging economies.

Competitive Landscape

The Automotive NDT market is moderately consolidated, with the top five vendors controlling roughly 38% of the 2024 revenue. However, more than 400 regional service firms remain active worldwide. Major players pursue three key levers: technology integration, geographic expansion, and vertical bundling, to outpace their peers. SGS’s USD 1.325 billion ATS acquisition added 85 laboratories and 2,100 staff to its North American roster, sharpening its bid for OEM strategic contracts.[4]OneStopNDT Editorial, “Eddyfi/NDT Completes Acquisition of NDT Global,” onestopndt.com Eddyfi/NDT’s absorption of NDT Global joined ultrasonic, eddy-current, and acoustic-emission assets under one umbrella, allowing cross-selling to auto and pipeline clients.

Strategic moves also include Institut Dr. Foerster’s purchase of Prüftechnik, which brings eddy-current probe IP into Germany’s EV-motor supply chain. TRIGO’s Controreupe buy extends 3D laser-scanning services to French OEMs preparing hydrogen-powered platforms. On the technology front, North Star Imaging launched a GPU-accelerated CT suite that reconstructs 2,048×2,048-pixel volumes in 80 seconds, representing a 6-fold improvement over prior versions. Start-ups such as ZVerse apply generative AI to synthesize missing CT slices, promising defect detection in half the radiation dose. With M&A pipelines robust and AI platforms advancing, competitive intensity is expected to remain high throughout the forecast period.

Automotive NDT Industry Leaders

Baker Hughes Company

Mistras Group Inc.

SGS SA

Intertek Group plc

Applus Services SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: SGS finalized the USD 1.325 billion takeover of Applied Technical Services, merging 85 facilities and 2,100 engineers into its network.

- June 2025: Metalogic acquired Houston-based NDT-PRO Services, bolstering Gulf-Coast operations with a 15,000-sq-ft facility.

- April 2025: Sonaspection International underwent a management buyout backed by private investors to accelerate U.S. expansion.

- March 2025: Testia fully integrated InFactory Solutions, adding automation modules that target zero-defect production lines.

- March 2025: Institut Dr. Foerster signed a deal to purchase Prüftechnik NDT GmbH, broadening its product catalog and global service network.

- January 2025: TRIGO acquired Controreupe, aiming to triple its revenue by 2030 and create 30 new metrology and NDT roles.

Global Automotive NDT Market Report Scope

Non-destructive testing is testing and analysis method used by several industries to test the properties of a material, component, structure, or system for any form of characteristic discrepancies or welding defects. The integrity of a design/structure is verified through this process in a way such that the performance of that component is not degraded due to the test. Hence, it plays a vital role in ensuring the product's viability in the automotive industry.

The NDT in the Automotive & Transportation market is segmented by Type (Equipment, Services), Testing Technology (Radiography Testing, Ultrasonic Testing, Magnetic Particle Testing, Electromagnetic Testing, Liquid Penetrant Testing, Visual Inspection, Eddy Current), and Geography.

| Equipment |

| Software |

| Services |

| Consumables |

| Ultrasonic Testing |

| Radiographic Testing |

| Magnetic Particle Testing |

| Liquid Penetrant Testing |

| Visual Inspection Testing |

| Eddy-Current Testing |

| Acoustic Emission Testing |

| Thermography / Infrared Testing |

| Computed Tomography Testing |

| Traditional / Conventional |

| AI-enabled |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| South-East Asia | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Equipment | |

| Software | ||

| Services | ||

| Consumables | ||

| By Testing Method | Ultrasonic Testing | |

| Radiographic Testing | ||

| Magnetic Particle Testing | ||

| Liquid Penetrant Testing | ||

| Visual Inspection Testing | ||

| Eddy-Current Testing | ||

| Acoustic Emission Testing | ||

| Thermography / Infrared Testing | ||

| Computed Tomography Testing | ||

| By Technique | Traditional / Conventional | |

| AI-enabled | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the forecast value of the Automotive NDT market by 2031?

The market is projected to reach USD 3.16 billion by 2031, growing at a 9.03% CAGR.

Which region leads current spending on automotive non-destructive testing?

North America leads with 37.45% revenue share, supported by stringent NHTSA mandates.

Which testing method is expanding fastest in automotive applications?

Computed tomography is the fastest-growing method, advancing at an 10.96% CAGR through 2031.

How are electric-vehicle batteries influencing NDT demand?

EV battery safety demands high-precision CT and ultrasonic scans, adding 2.8% to the market’s CAGR forecast.

What challenge constrains wider NDT adoption in emerging markets?

High capital costs for advanced CT and robotic setups reduce ROI and slow implementation.

Which companies recently drove consolidation in this space?

SGS’s acquisition of ATS and Eddyfi/NDT’s purchase of NDT Global are among the largest recent deals.

Page last updated on: