UK NDT Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

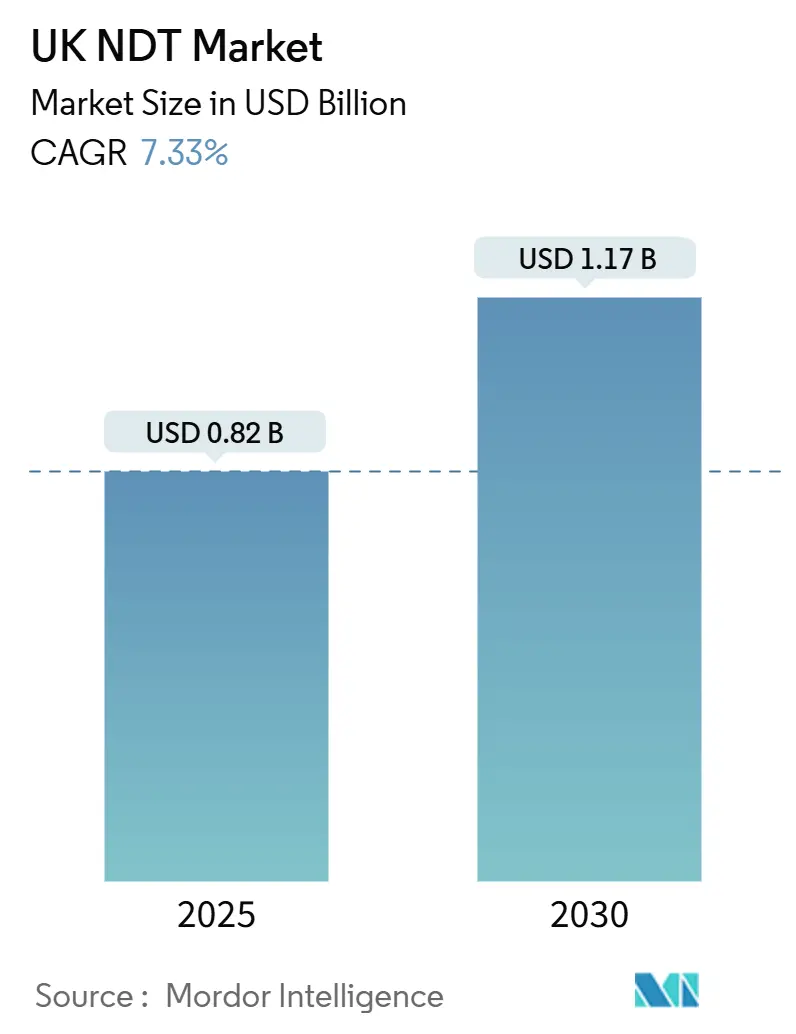

| Market Size (2025) | USD 0.82 Billion |

| Market Size (2030) | USD 1.17 Billion |

| Growth Rate (2025 - 2030) | 7.33% CAGR |

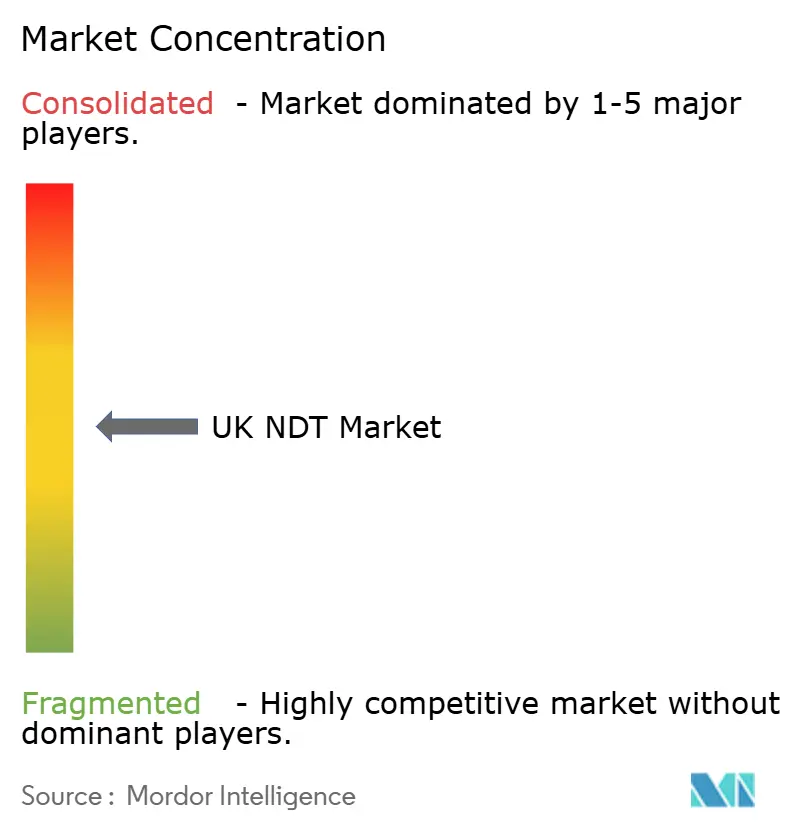

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UK NDT Market Analysis by Mordor Intelligence

Current estimates place the UK NDT market size at USD 0.82 billion in 2025, and the sector is forecast to reach USD 1.17 billion by 2030, translating into a 7.33% CAGR over the period. Mandatory inspection cycles for the aging nuclear fleet, the escalating installation of offshore wind farms, and the steady rollout of Industry 4.0 programs underpin this expansion. The market is also buoyed by service outsourcing that addresses persistent shortages of Level III certified inspectors, as well as by software-centric offerings that turn inspection data into actionable insights. Growth opportunities further arise from hydrogen infrastructure integrity projects and from heightened demand for automated defect recognition in aerospace and automotive production.

Key Report Takeaways

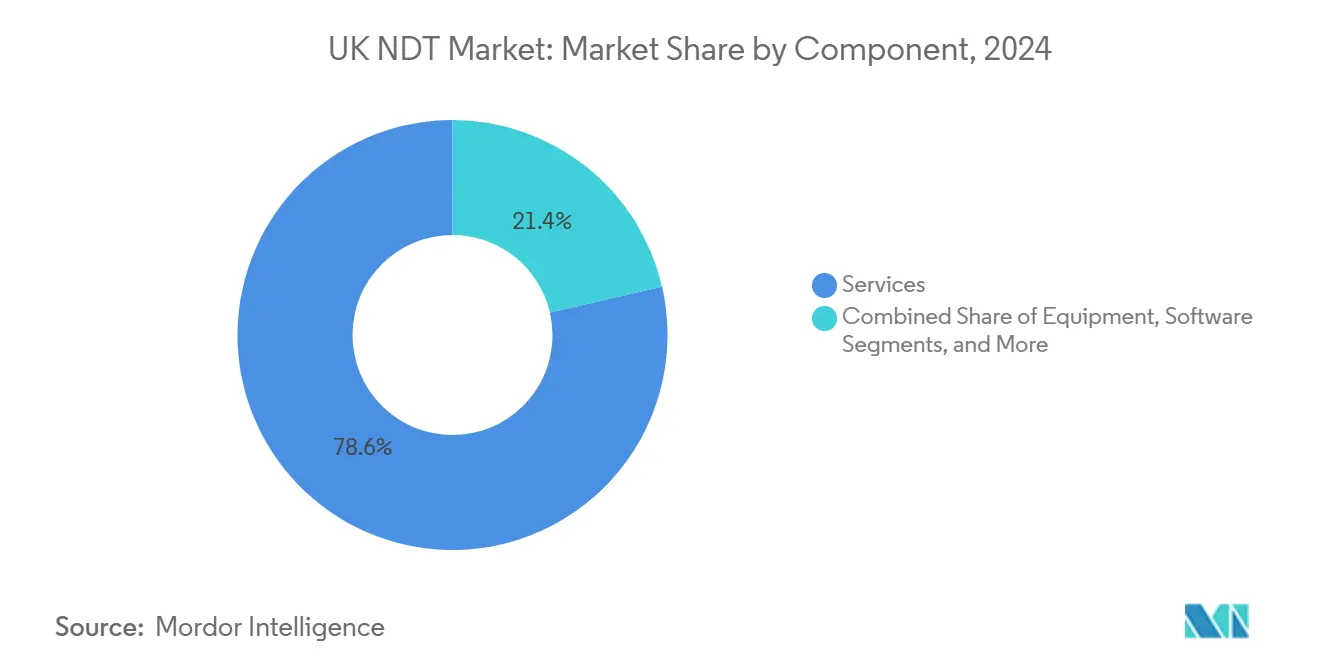

- By component, services led with a 78.6% revenue share in 2024; software is forecast to expand at a 11.1% CAGR to 2030, reflecting its role in enabling predictive maintenance across the UK NDT market.

- By testing method, ultrasonic testing accounted for 27.3% of the UK NDT market share in 2024; eddy-current testing is projected to advance at a 7.9% CAGR through 2030.

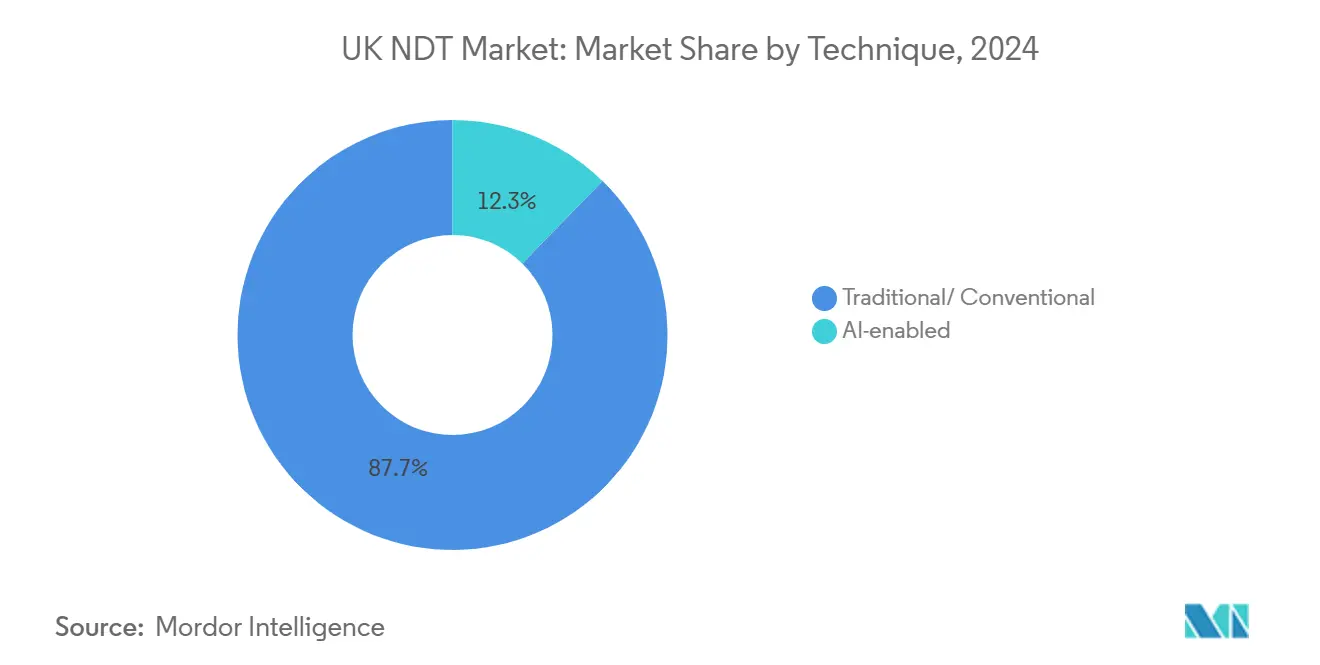

- By technique, traditional methods accounted for 87.7% share of the UK NDT market size in 2024; AI-enabled techniques are projected to rise at 14.2% CAGR through 2030.

- By end-user industry, the oil and gas sector held a 24.8% share of the UK NDT market size in 2024; the automotive and transportation sector is poised to grow at an 8.1% CAGR between 2025 and 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

UK NDT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption of phased-array ultrasonic systems | +1.8% | Scotland's offshore wind sector and nationwide aerospace hubs | Medium term (2-4 years) |

| Expansion of renewable-energy infrastructure | +1.5% | UK coastal regions and Scotland wind zones | Long term (≥ 4 years) |

| Mandatory inspection cycles for the aging nuclear fleet | +1.2% | England's nuclear sites and Scotland's Torness facility | Short term (≤ 2 years) |

| Government incentives for Industry 4.0 digital inspection solutions | +1.0% | Northern England industrial zones and national manufacturing clusters | Medium term (2-4 years) |

| Rising skill gap, outsourcing to specialist service providers | +0.9% | Major industrial centers | Short term (≤ 2 years) |

| Drive to certify hydrogen pipeline integrity | +0.6% | England's hydrogen corridors and Scotland's green projects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Phased-Array Ultrasonic Systems

The wider adoption of phased-array ultrasonic testing (PAUT) is driving the UK NDT market toward higher-resolution inspections. Aerospace manufacturers are increasingly mandating PAUT for composite components, while oil and gas operators are adopting it for complex weld geometries. One PAUT probe can replace multiple conventional transducers, cutting inspection time by as much as 50% without compromising volumetric coverage.[1]Health and Safety Executive, “Pressure Equipment Safety Regulations,” HSE.GOV.UK Recent updates to pressure equipment regulations list PAUT as an acceptable alternative to radiographic methods, erasing regulatory obstacles and supporting adoption across other safety-critical sectors. Service providers are capitalizing on upskilling personnel and by bundling PAUT with real-time data analytics platforms that translate inspection results into integrity dashboards.

Expansion of Renewable-Energy Infrastructure

Wind turbine construction is surging as the country aims to reach 50 GW of offshore wind capacity by 2030. NDT demand spans blade manufacturing, foundation welds, and subsea cables, creating multi-year service pipelines in coastal regions. Drone-borne thermography and robotic crawlers are replacing rope access for tower inspections, improving worker safety and inspection repeatability. ScotWind seabed leasing alone adds more than 25 GW of new projects that will require lifetime inspection regimes, turning NDT from a compliance function into a strategic differentiator for wind-farm operators. Vendors offering turnkey inspection packages that integrate blade monitoring, corrosion mapping, and digital record-keeping are well-positioned to capture these new contracts.

Mandatory Inspection Cycles for the Aging Nuclear Fleet

The average UK reactor is more than 35 years old and now falls under stricter protocols released by the Office for Nuclear Regulation (ONR) in 2024.[2]The Crown Estate, “Offshore Wind Leasing Strategy,” THECROWNESTATE.CO.UK Operators must perform more frequent volumetric inspections on reactor vessels, steam generators, and primary piping, pushing steady revenue into the UK NDT market. Specialized techniques—such as high-temperature ultrasonics and radiation-hardened robotics—are seeing renewed investment. Decommissioning projects at Sellafield create additional demand for waste-package characterization and remote visual inspection in radioactive zones, thereby extending the market opportunity beyond operating reactors.

Government Incentives for Industry 4.0 Digital Inspection Solutions

Through the Made Smarter program and Innovate UK grants, government funding accelerates the commercialization of AI-based defect recognition and cloud-hosted inspection management tools. Tax incentives enable manufacturers to recover up to 130% of qualifying digital technology investments, lowering barriers for mid-sized firms. Consequently, software uptake grows at a rate of more than 11% CAGR, transforming raw inspection data into predictive maintenance alerts that reduce unplanned downtime. Regional development agencies in Northern England further encourage adoption by co-funding pilot projects that integrate AI platforms with factory MES and ERP systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of advanced radiographic equipment | −0.8% | Nationwide, with a higher impact on small providers | Short term (≤ 2 years) |

| Limited standardization for AI-enabled defect characterization | −0.6% | Aerospace clusters and nuclear facilities | Medium term (2-4 years) |

| Shortage of Level III certified inspectors in niche techniques | −0.5% | National safety-critical sectors | Long term (≥ 4 years) |

| Environmental concerns over industrial radiography isotopes | −0.3% | Nuclear and heavy industry corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Advanced Radiographic Equipment

Industrial computed tomography platforms often exceed GBP 500,000 (USD 625,000), pushing smaller service companies to delay upgrades or form rental consortia. Compliance in radiographic bays demands costly shielding and licensing, driving total ownership far above headline equipment prices. Supply chain delays following Brexit have extended lead times and reduced vendor competition, adding financing risk that can dampen near-term investment. Consequently, some operators switch to alternative methods such as PAUT to manage budget constraints, although radiography remains irreplaceable for certain complex geometries.

Limited Standardization for AI-Enabled Defect Characterization

Regulators require objective evidence of algorithm performance before approving AI systems for mission-critical inspections in aerospace and nuclear sectors. Current frameworks, such as ASTM E3166, provide guidance but lack detailed verification metrics, resulting in certification bottlenecks.[3]Office for Nuclear Regulation, “Aging Management Guidance Update,” ONR.ORG.UK Proprietary data formats hinder interoperability between AI platforms and existing QA workflows, while differing validation protocols among industry bodies lengthen approval timelines. Until a robust consensus standard emerges, most asset owners continue to mandate human review of AI outputs, limiting productivity gains from full automation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Dominance Reflects Outsourcing Trend

Services continue to dominate the UK NDT market, accounting for 78.6% of revenue in 2024. Outsourcing helps asset owners secure disciplined compliance amid acute shortages of Level III expertise, especially in nuclear and aerospace settings. Inspection contracts are increasingly bundling data analytics, risk-based inspection planning, and regulatory reporting into multi-year frameworks. Software, although accounting for just 7% of 2024 revenue, is the fastest-growing component, with a 11.1% CAGR, as cloud portals ingest raw inspection data and feed AI models that predict failure modes. Equipment sales grow steadily through replacement cycles, as aging analog devices are swapped for digital radiography, phased-array ultrasonics, and miniature crawlers. Consumables—such as ultrasonic couplants, penetrant dyes, and magnetic particles—generate recurring aftermarket revenue, helping to stabilize vendor cash flows.

Looking ahead, services firms are expanding their training academies to boost internal Level III capacity, while OEMs are embedding subscription-based software licenses within hardware packages. The British Institute of Non-Destructive Testing reported a 23% increase in Level III certification applications in 2024. This talent influx should marginally ease labor constraints by 2027, yet the complexity of advanced techniques keeps high-end expertise in short supply, reinforcing the premium placed on specialist service providers across the UK NDT market.

By Testing Method: Ultrasonic Testing Leads Amid Technological Evolution

Ultrasonic testing (UT) retained a 27.3% share of the UK NDT market in 2024. Its non-radiographic nature, portability, and volumetric coverage make UT indispensable for pipeline welds, wind-tower flanges, and aircraft composites. The rapid adoption of PAUT and full-matrix capture enhances UT’s value by adding 3D visualization and improving defect sizing accuracy. Eddy-current testing posted the quickest gains, expanding at 7.9% CAGR as electric-vehicle OEMs and aerospace primes inspect aluminum skins and carbon-fiber laminates. Digital radiography still holds a niche advantage for dense components, though safety protocols and capex barriers cap growth. Magnetic particle and liquid penetrant techniques remain staples for surface defect detection in casting and forging plants, while thermography gains traction in predictive maintenance for rotating machinery.

UT vendors are increasingly supplying integrated systems that pair dual-matrix probes with AI classification, which flags crack-like indications in live displays. In 2024, the Health and Safety Executive broadened pressure-equipment guidelines to accept UT alternatives, spurring wider field adoption. Consequently, hybrid inspection packages now combine phased-array UT for weld bodies with eddy-current arrays for heat-affected zones, giving operators a one-stop solution under a consolidated software environment.

By Technique: Traditional Methods Dominate Despite AI Advancement

Traditional approaches still hold 87.7% of 2024 revenue, reflecting entrenched regulatory acceptance and operator familiarity. Techniques such as manual UT, magnetic particle testing, and film-based radiography continue to hold their place of pride in asset integrity programs. Even so, AI-enabled inspection is growing at a 14.2% CAGR as algorithms surpass human repeatability in identifying subtle anomalies. Automotive stamping lines utilize AI vision to reject defective panels in milliseconds, while power station operators employ machine learning to track wall thickness loss across boiler tubes. Integration hurdles persist—legacy data silos, cybersecurity concerns, and limited training sets, but collaborative pilots with TWI demonstrate that AI achieves near-zero false negatives on validated weld. Over the forecast window, regulatory bodies are expected to formalize performance benchmarks, enabling AI adoption to accelerate, yet human verification will likely remain mandatory for critical acceptance decisions.

By End-User Industry: Oil and Gas Leads Amid Energy Transition

Oil and gas captured 24.8% of the revenue in 2024, driven by ongoing North Sea maintenance, which necessitates frequent inspections due to corrosive seawater, high pressure, and extended service life. The decommissioning of mature installations adds pipeline cleaning, pigging verification, and integrity confirmation scopes, keeping NDT crews busy. The automotive and transportation sector is the fastest-growing at an 8.1% CAGR, driven by aluminum and composite chassis, battery enclosures, and additive-manufactured engine parts, all of which require bespoke inspection techniques. Power generation remains robust, thanks to effective nuclear aging management and the expansion of wind farms. Aerospace benefits from additive manufacturing and composite airframe expansion, while heavy engineering relies on real-time monitoring to prevent unexpected shutdowns. In 2024, the Civil Aviation Authority tightened composite inspection requirements, resulting in prolonged in-service UT and radiography intervals, which increased demand for high-fidelity flaw characterization.[4]Department for Business, Energy and Industrial Strategy, “Manufacturing Strategy 2024,” GOV.UK

Geography Analysis

England accounts for the lion’s share of the UK NDT market revenue owing to its concentration of nuclear plants, Midlands aerospace assembly lines, and Southeast petrochemical terminals. Scotland follows, driven by Aberdeen's oil and gas operations and offshore wind fabrication in Fife and Dundee. The Humber cluster in northeast England is emerging as a high-growth corridor thanks to turbine blade factories and monopile yards that require extensive weld inspection. Wales contributes consistent demand from Port Talbot steelworks and from Wylfa nuclear decommissioning, while Northern Ireland’s Belfast aerospace cluster sustains UT and eddy-current needs for fuselage panels and nacelle components.

Growth trajectories vary. Scottish revenue is forecast to outpace national averages as new floating wind projects move from consent to construction. England remains the volume anchor but sees modest mid-single-digit growth as mature assets plateau and new nuclear reactors face long commissioning horizons. Regional skills initiatives—such as the Scottish NDT apprenticeship scheme—address labor gaps and may temper wage inflation. Meanwhile, post-Brexit mutual recognition deals with EU conformity bodies restored continuity for cross-border inspection of aviation parts and offshore equipment, alleviating a temporary certification bottleneck in 2024.

Competitive Landscape

The UK NDT market exhibits moderate concentration. Intertek, Element Materials Technology, and SGS command sizeable national footprints through multi-disciplinary service portfolios that cover radiography to robotics. Sonomatic’s 2024 acquisition of Innospection injected advanced crawler robotics into its oil and gas offering, illustrating technology-focused consolidation. Fairley Gunn Group added Axi-Tek and Metrix NDT, extending its reach into the Midlands aerospace and northern manufacturing sectors. Element expanded pressure-vessel services via the ISS Inspection Services deal, strengthening coverage in heavy industry.

Competition now centers on differentiated technology stacks—AI analytics engines, digital twins, and autonomous mobile crawlers—that lower cost per inspection while improving data richness. Vendors are partnering with software specialists to embed secure cloud pipelines that convert ultrasonic A-scans into actionable maintenance insights. Early-mover advantage is especially evident in hydrogen pipeline integrity, where only a handful of firms possess traceable procedure qualifications. To maintain their market share, incumbents invest in training, ISO 17025 laboratories, and field-service digitization, which integrates scheduling, reporting, and invoicing into unified portals.

UK NDT Industry Leaders

Mistras Group Ltd

Eddyfi UK

Olympus Europa Holding GmbH (UK branch)

Zetec Inc (UK)

SGS United Kingdom Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Nexxis UK announced the development of robotic inspection crawlers for confined spaces.

- September 2024: Sonomatic Group completed the acquisition of Innospection Limited, expanding its robotics and automation capabilities for pipeline inspection services.

- August 2024: Fairley Gunn Group acquired Axi-Tek NDT Limited and Metrix NDT Limited, enhancing geographic coverage and advanced ultrasonic testing capacity.

- July 2024: Element Materials Technology acquired ISS Inspection Services Limited, broadening pressure-vessel inspection services.

UK NDT Market Report Scope

| Equipment |

| Software |

| Services |

| Consumables |

| Ultrasonic Testing |

| Radiographic Testing |

| Magnetic Particle Testing |

| Liquid Penetrant Testing |

| Visual Inspection Testing |

| Eddy-Current Testing |

| Acoustic Emission Testing |

| Thermography / Infrared Testing |

| Computed Tomography Testing |

| Traditional / Conventional |

| AI-enabled |

| Oil and Gas |

| Power Generation |

| Aerospace |

| Defense |

| Automotive and Transportation |

| Manufacturing and Heavy Engineering |

| Construction and Infrastructure |

| Chemical and Petrochemical |

| Marine and Ship Building |

| Electronics and semiconductor |

| Mining |

| Medical Devices |

| Others |

| By Component | Equipment |

| Software | |

| Services | |

| Consumables | |

| By Testing Method | Ultrasonic Testing |

| Radiographic Testing | |

| Magnetic Particle Testing | |

| Liquid Penetrant Testing | |

| Visual Inspection Testing | |

| Eddy-Current Testing | |

| Acoustic Emission Testing | |

| Thermography / Infrared Testing | |

| Computed Tomography Testing | |

| By Technique | Traditional / Conventional |

| AI-enabled | |

| By End-user Industry | Oil and Gas |

| Power Generation | |

| Aerospace | |

| Defense | |

| Automotive and Transportation | |

| Manufacturing and Heavy Engineering | |

| Construction and Infrastructure | |

| Chemical and Petrochemical | |

| Marine and Ship Building | |

| Electronics and semiconductor | |

| Mining | |

| Medical Devices | |

| Others |

Key Questions Answered in the Report

What is the projected value of the UK NDT market in 2030?

The UK NDT market is expected to reach USD 1.17 billion by 2030, growing at a 7.33% CAGR.

Which component will record the fastest growth?

Software is forecast to increase at a 11.1% CAGR as AI platforms and cloud solutions gain traction.

Why do services hold such a high share?

Outsourcing mitigates shortages of Level III inspectors and bundles compliance expertise, resulting in a 78.6% revenue share for services in 2024.

Which testing method leads the market?

Ultrasonic testing accounts for 27.3% of 2024 revenue, favored for its volumetric coverage and absence of radiation risks.

How will renewable energy affect NDT demand?

Offshore wind expansion to 50 GW capacity will drive sustained demand for inspections of blades, towers, and subsea structures through 2030.

What challenges slow AI adoption in NDT?

The primary challenges are high validation requirements and limited standardization for AI algorithms, delaying regulator approval in safety-critical sectors.

Page last updated on: