Advanced NDT Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

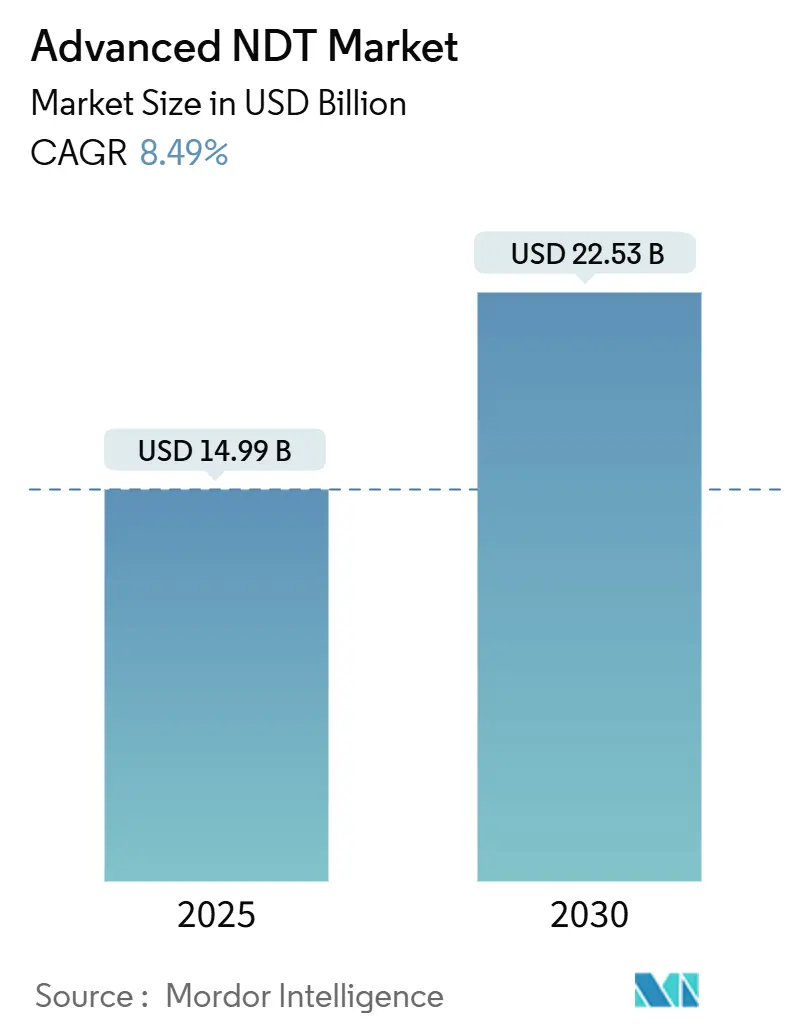

| Market Size (2025) | USD 14.99 Billion |

| Market Size (2030) | USD 22.53 Billion |

| Growth Rate (2025 - 2030) | 8.49% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Advanced NDT Market Analysis by Mordor Intelligence

The advanced non-destructive testing (NDT) market size reached USD 14.99 billion in 2025 and is projected to expand to USD 22.53 billion by 2030, representing an 8.49% CAGR over the forecast period. This robust trajectory positions the Advanced NDT market at the forefront of global quality assurance investments, as hydrogen pipeline integrity mandates, aerospace composite adoption, and gigafactory automation converge to accelerate spending. Regulatory tightening across oil and gas, nuclear, and aviation sectors underpins sustained equipment upgrades, while AI-driven defect analytics redefine inspection speed and consistency. Investments in digital radiography, phased-array ultrasonic platforms, and robotic scanners reinforce structural-health programs, and the scarcity of multi-skilled technicians further fuels demand for automated solutions. Competitive intensity has risen as established vendors acquire niche technology firms to broaden portfolios and defend share against software-centric entrants.

Key Report Takeaways

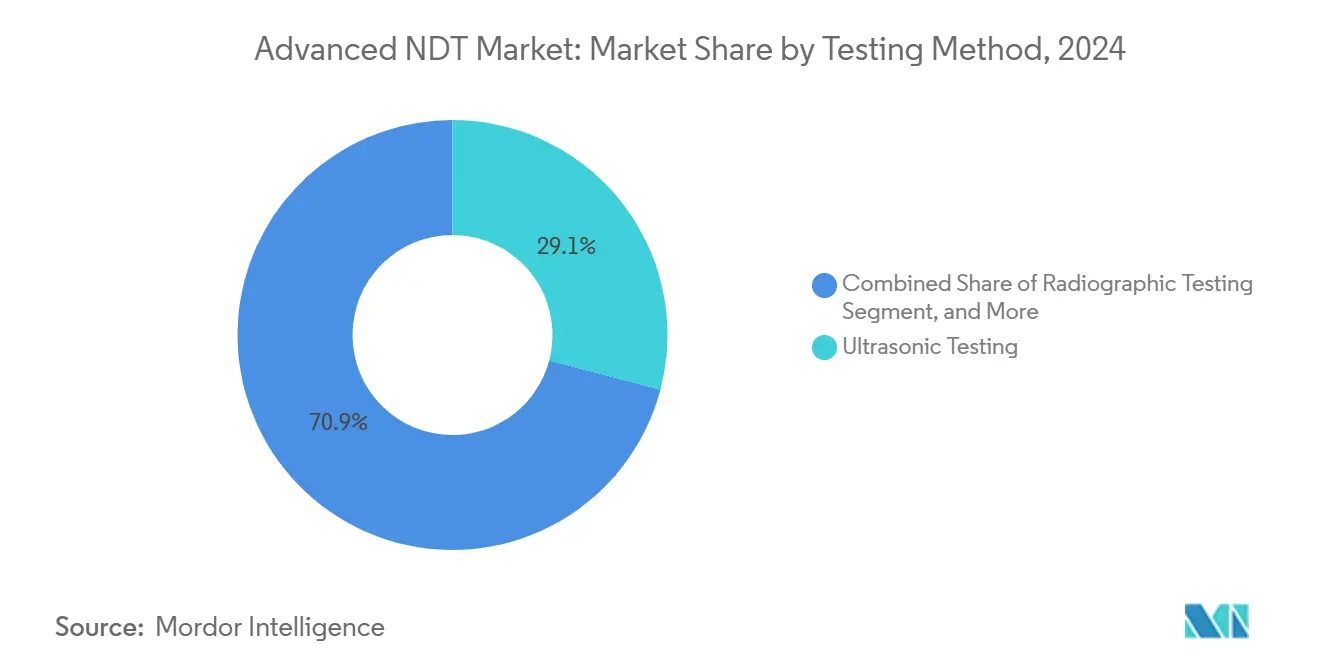

- By testing method, ultrasonic testing led the Advanced NDT market with a 29.1% share in 2024, while eddy-current testing is projected to expand at a 9.8% CAGR through 2030.

- By technique, conventional approaches commanded an 84.8% share of the Advanced NDT market size in 2024; yet, AI-enabled systems are forecast to register a 16.2% CAGR through 2030.

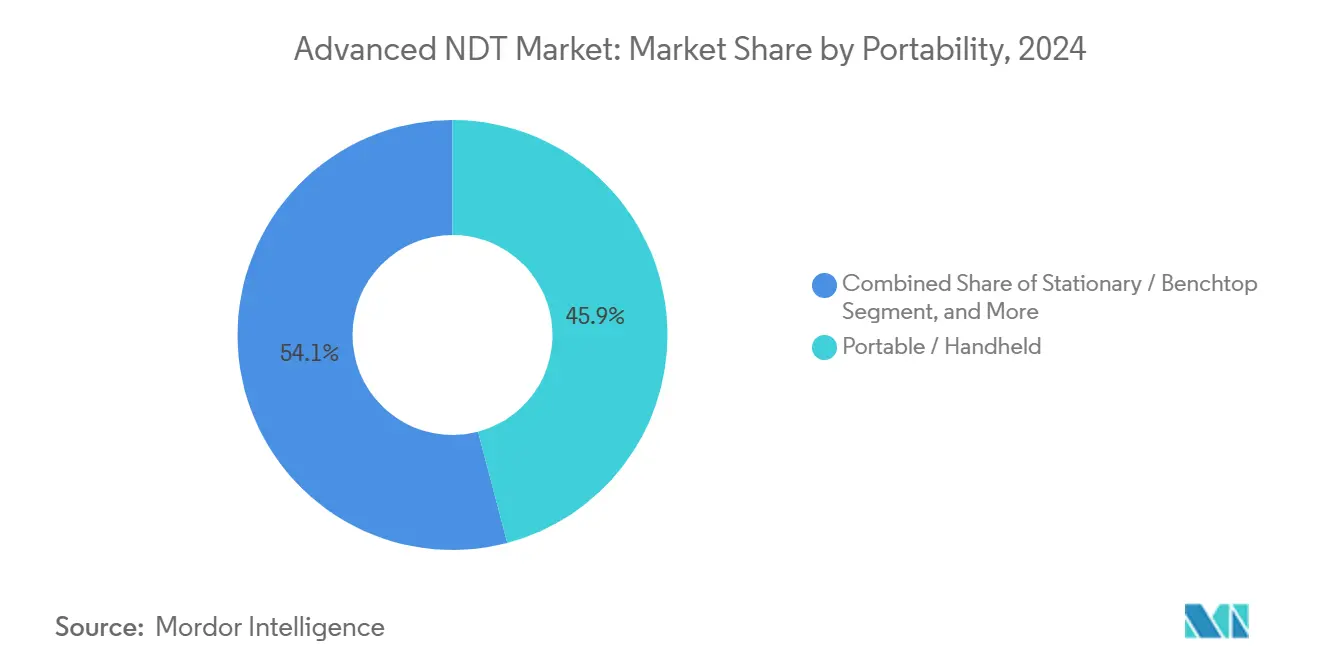

- By portability, portable equipment held a 45.9% revenue share in 2024, whereas automated and robotic systems are expected to advance at a 14.3% CAGR from 2025 to 2030.

- By end-user industry, the oil and gas sector accounted for a 26.2% share of the Advanced NDT market size in 2024; however, the automotive and transportation segment is the fastest-growing, with a 11.4% CAGR projected to 2030.

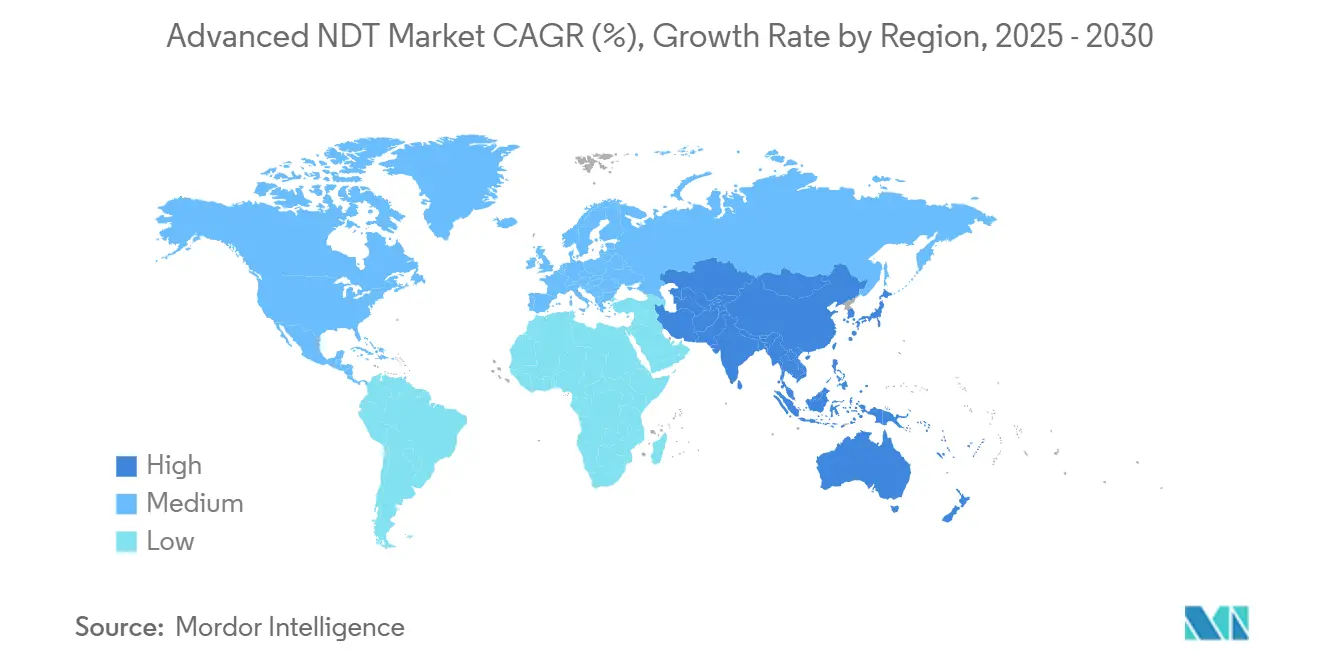

- By geography, North America held a 36.5% revenue share in 2024, whereas Asia-Pacific is expected to advance at a 9.5% CAGR from 2025 to 2030.

Global Advanced NDT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hydrogen pipeline integrity mandates | +1.2% | North America and Europe, extending into the Asia-Pacific | Medium term (2-4 years) |

| Phased-array UT adoption for aerospace composites | +1.0% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Digital radiography for small modular reactors | +0.8% | North America and Europe, selected Asia-Pacific markets | Long term (≥ 4 years) |

| Automated inline NDT in EV gigafactories | +1.4% | Asia-Pacific and North America | Medium term (2-4 years) |

| AI-enabled defect analytics | +1.1% | Early adoption in developed markets | Short term (≤ 2 years) |

| Service outsourcing by tier-2 wind-turbine OEMs | +0.7% | Europe and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Asset-Integrity Mandates in Hydrogen Pipelines

Hydrogen-economy infrastructure programs have created unprecedented inspection requirements. The U.S. Department of Energy’s USD 7 billion hydrogen-hub initiative obliges pipeline operators to deploy guided-wave and electromagnetic acoustic transducer solutions that detect hydrogen-induced cracking before failure.[1]U.S. Department of Energy, “$7 Billion for Clean Hydrogen Hubs,” energy.gov European Hydrogen Backbone expansion mirrors this trend, with Germany alone scheduling integrity assessments across 15,000 km of new lines. ASME B31.12 and API 579 draft updates formalize shorter inspection intervals, ensuring sustained procurement of hydrogen-compatible NDT platforms and certified personnel.

Rapid Adoption of Phased-Array UT in Aerospace Composites

Composite-intensive aircraft programs now rely on phased-array ultrasonic testing (PAUT) to verify the structural soundness of their components. Boeing’s 787 line reported a 40% cut in inspection time after integrating automated PAUT in 2024, while Airbus deployed total-focusing-method algorithms that locate 0.5 mm flaws in multilayer fuselage panels. FAA Advisory Circular 20-107B updates have mandated the use of advanced ultrasonics for critical repairs, anchoring PAUT as a baseline for future wide-body and narrow-body programs.[2]Federal Aviation Administration, “Advisory Circular 20-107B,” faa.gov

AI-Enabled Defect Analytics Cuts Inspection Cycle Time

Machine-learning engines now interpret ultrasonic A-scans and visual data faster than human inspectors. Baker Hughes’ Mentor Visual iQ+ system classifies defect severity in real-time, reducing petrochemical inspection cycles by 35% while reducing false positives by 60%.[3]Baker Hughes, “Mentor Visual iQ+ Launch,” bakerhughes.com Cloud platforms aggregate multi-site data and retrain models via federated learning, continually lifting detection accuracy and enabling predictive maintenance workflows that extend asset life.

Growth of Automated Inline NDT in EV Gigafactories

Electric-vehicle battery and drivetrain production requires 100% quality checks at line speeds. Tesla’s 2024 gigafactory upgrade features robotic ultrasonic cells that inspect 500 battery modules per hour, while eddy-current rigs validate stator windings at a rate of 1,200 units per hour. ISO 26262 safety standards drive full-coverage mandates, and integrated cells now combine liquid-penetrant, thermography, and acoustic-emission modules to meet throughput targets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of multi-skilled PAUT and TOFD technicians | -0.9% | Global, acute in North America and Europe | Long term (≥ 4 years) |

| Slow harmonization of robotic-inspection standards | -0.6% | Global, affecting cross-border projects | Medium term (2-4 years) |

| High CapEx of large-area digital RT panels | -0.4% | Global | Short term (≤ 2 years) |

| Cybersecurity risks in cloud NDT hubs | -0.5% | Critical infrastructure sectors worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scarcity of Multi-Skilled PAUT and TOFD Technicians

Certification pipelines cannot keep pace with industry demand. ASNT indicated in 2024 that Level II PAUT certification now averages 18 months, with European waitlists exceeding 12 months. Salary premiums rose 30% over the past year as service firms compete for scarce talent, constraining field-service capacity and compelling end-users to adopt automation.

Slow Standards Harmonization for Robotic Inspections

Global deployment of robotic scanners faces conflicting code requirements. ISO 19285 revisions have been pushed back to 2026, while EN and ASME criteria diverge on system qualification. Cross-border pipeline and aerospace supply-chain projects, therefore, must validate equipment twice, inflating costs and dampening investment in advanced robotics.[4]International Organization for Standardization, “ISO 19285 Draft,” iso.org

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Testing Method: Ultrasonic Leadership Meets Eddy-Current Disruption

Ultrasonic testing occupied 29.1% of the Advanced NDT market in 2024 and remains indispensable for welds, composites, and thick-section structures. The segment benefits from decades of operator familiarity and a robust training ecosystem. Nevertheless, eddy-current platforms are projected to grow at a 9.8% CAGR through 2030, driven by automotive sheet metal throughput and electronics solder joint inspection. Digital radiography adoption accelerates in nuclear-modular-reactor builds, while magnetic-particle and liquid-penetrant techniques hold niche roles in crack and surface-defect detection. Visual-inspection tools embedded with AI algorithms automate anomaly classification, and acoustic-emission monitoring gains share in bridge and pressure-vessel health programs. Thermography grows in tandem with grid modernization spending, whereas computed tomography retains a foothold in research and additive manufacturing validation.

Second-generation phased-array probes, full-matrix capture processing, and dual-matrix eddy-current arrays enhance performance gains, aligning with real-time analytics that reduce the number of reporting phases. End users are increasingly specifying multi-technique bundles within single procurement cycles, thereby reinforcing vendor cross-selling opportunities and shaping an equipment-plus-software revenue model that redefines the trajectory of the Advanced NDT market.

By Technique: AI-Enabled Systems Challenge Conventional Dominance

Conventional methods still accounted for 84.8% of 2024 revenue, leveraging regulatory familiarity and an established installed base. Yet AI-enabled configurations will log a 16.2% CAGR, outpacing the broader Advanced NDT market. Deep-learning pipelines trained on expansive defect libraries now outperform manual interpretation on noise-rich composite signals, and auto-reporting tools yield instant compliance documentation.

Software-centric disruptors package subscription analytics that retrofit to legacy instruments, making pilot adoption easier. Validation studies conducted under ASTM E2862 and EN 4179 have confirmed performance parity for select aerospace components, paving the way for regulatory endorsement. As predictive-maintenance programs mature, AI-enabled suites will transition from proof-of-concept deployments to line-item budget items, propelling the digitalization of structural health.

By Portability: Automated Platforms Accelerate Adoption Curve

Portable units accounted for 45.9% of the revenue share in 2024, making them indispensable for field service across pipelines, refineries, and wind farms. Battery extensions, Wi-Fi connectivity, and ruggedized casings have stretched uptime and expanded operating envelopes. In parallel, automated and robotic systems are expected to post a 14.3% CAGR, mirroring the shift toward lights-out manufacturing. Six-axis crawler robots equipped with phased-array probes inspect circumferential welds on storage tanks without scaffolding, while drone-mounted thermal imagers survey offshore blades within weather windows previously unreachable by rope teams.

Stationary benches remain relevant for lab-grade metrology and failure analysis centers, ensuring demand stability. Nonetheless, total cost-of-ownership analyses increasingly favor autonomous platforms that eliminate rework costs associated with human variability, validating the strategic pivot that large vendors have signaled through their 2024-2025 mergers and acquisitions (M&A) moves.

By End-User Industry: Oil and Gas Resilience Versus Automotive Momentum

Oil and gas led the Advanced NDT market with a 26.2% stake in 2024, driven by aging pipeline stock and the acceleration of leak-detection budgets in response to emission-reduction programs. Hydrogen-ready retrofits intensify inspection scope, reinforcing market stability. Conversely, the automotive and transportation sectors are expected to chart an 11.4% CAGR, driven by the verification of structural battery packs and high-speed weld inspections on gigacasting lines.

Power-generation demand persists amid nuclear plant life extension and wind turbine blade aging, while aerospace composites continue to meet specialized, high-margin requirements. Manufacturing and heavy-engineering segments integrate embedded sensors and inline scanners within Industry 4.0 frameworks, and infrastructure authorities earmark budgets for bridge cable acoustic-emission monitoring. Electronics miniaturization and medical implant scrutiny nurture micro-focus CT applications, rounding out a diversified end-user landscape that cushions cyclical swings.

Geography Analysis

North America is expected to preserve a 36.5% revenue share in 2024. Federal regulations for pipeline integrity, SMR construction, and FAA composite-repair protocols sustain recurring expenditure, and U.S. vendors lead AI-enabled software exports. Technician training networks and well-capitalized service firms support rapid technology refresh cycles; however, the scarcity of Level III PAUT experts could temper growth if the uptake of automation lags expectations.

Asia-Pacific is on a 9.5% CAGR trajectory through 2030, the strongest regional pace in the Advanced NDT market. China’s Belt and Road pipelines, Japan’s aerospace tier supply chain, and India’s urban rail and renewable energy tower projects collectively elevate inspection volumes. Government incentives encourage the local manufacture of robotic scanners, which curbs import duties and lowers entry thresholds for smaller asset owners. Regional standards bodies are increasingly aligning with ISO, thereby smoothing cross-border service delivery.

Europe maintains a balanced profile, with nuclear lifetime-extension projects anchoring digital radiography transitions and automotive battery-plant deals spurring the rollout of eddy-current equipment. The Middle East and Africa capitalize on upstream oil investments and desalination plant expansions, while South America leverages mining equipment health-monitoring pilots to extend the life of machinery under volatile commodity cycles. Geographic diversification thus continues to buffer global vendors against localized economic dips and regulation-driven delays.

Competitive Landscape

The Advanced NDT market exhibits moderate fragmentation. Baker Hughes, Olympus, and Eddyfi Technologies each expand via bolt-on deals: Eddyfi’s 2025 acquisition of Sonotron added total-focusing-method assets and deepened European composite exposure. Olympus committed USD 120 million to a Singapore automation hub, targeting Asia-Pacific gigafactory demand. Baker Hughes launched Mentor Visual iQ+ with embedded AI to defend service contracts against software-first entrants.

Service majors such as MISTRAS and SGS invest in hydrogen pipeline centers and long-term refinery agreements, adopting asset-integrity outsourcing models. Drone-inspection startups form partnerships with certification bodies to accelerate offshore wind blade coverage, while cloud-platform firms pursue SaaS recurring revenue ratios exceeding 50% of total sales. Patent filings for algorithmic flaw characterization topped 200 in 2024, signaling an innovation arms race that tilts competitive advantage toward data-rich incumbents with federated learning pipelines.

Vendor selection criteria now weigh cybersecurity stack, regulatory compliance roadmaps, and technician-training portals alongside hardware accuracy. Price competition remains muted for mission-critical scopes but intensifies in commoditized weld-inspection segments, nudging smaller suppliers toward niche verticals or regional specialization. Consolidation momentum is expected to persist as portfolio breadth and AI-stack maturity become decisive differentiators.

Advanced NDT Industry Leaders

Baker Hughes (Waygate Technologies)

Olympus Corporation (Evident)

Zetec Inc.

MISTRAS Group

Applus Services SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Baker Hughes launched Mentor Visual iQ+ AI-based remote visual inspection platform, claiming 35% faster cycles.

- August 2025: Eddyfi Technologies acquired Sonotron NDT for EUR 45 million (USD 48.6 million).

- July 2025: Olympus announced a USD 120 million automated-systems plant in Singapore to serve the Asia-Pacific.

- June 2025: MISTRAS Group secured a USD 85 million contract extension with ExxonMobil for hydrogen-compatible pipeline integrity.

Global Advanced NDT Market Report Scope

| Ultrasonic Testing |

| Radiographic Testing |

| Magnetic Particle Testing |

| Liquid Penetrant Testing |

| Visual Inspection Testing |

| Eddy-Current Testing |

| Acoustic Emission Testing |

| Thermography / Infrared Testing |

| Computed Tomography Testing |

| Traditional/ Conventional |

| AI-enabled |

| Portable / Handheld |

| Stationary / Benchtop |

| Automated / Robotic |

| Oil and Gas |

| Power Generation |

| Aerospace |

| Defense |

| Automotive and Transportation |

| Manufacturing and Heavy Engineering |

| Construction and Infrastructure |

| Chemical and Petrochemical |

| Marine and Ship Building |

| Electronics and Semiconductor |

| Mining |

| Medical Devices |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Testing Method | Ultrasonic Testing | ||

| Radiographic Testing | |||

| Magnetic Particle Testing | |||

| Liquid Penetrant Testing | |||

| Visual Inspection Testing | |||

| Eddy-Current Testing | |||

| Acoustic Emission Testing | |||

| Thermography / Infrared Testing | |||

| Computed Tomography Testing | |||

| By Technique | Traditional/ Conventional | ||

| AI-enabled | |||

| By Portability | Portable / Handheld | ||

| Stationary / Benchtop | |||

| Automated / Robotic | |||

| By End-user Industry | Oil and Gas | ||

| Power Generation | |||

| Aerospace | |||

| Defense | |||

| Automotive and Transportation | |||

| Manufacturing and Heavy Engineering | |||

| Construction and Infrastructure | |||

| Chemical and Petrochemical | |||

| Marine and Ship Building | |||

| Electronics and Semiconductor | |||

| Mining | |||

| Medical Devices | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the size of the Advanced NDT market in 2025?

It currently stands at USD 14.99 billion, with projections indicating a rise to USD 22.53 billion by 2030.

Which testing method dominates current spending?

Ultrasonic testing leads, accounting for 29.1% of global revenue in 2024.

Why is Asia-Pacific the fastest-growing region?

Massive infrastructure build-outs, EV factory investments, and expanding aerospace supply chains propel the region to a 9.5% CAGR through 2030.

What role does AI play in inspection workflows?

AI-enabled analytics cut false positives by up to 60% and trim inspection cycle times by roughly one-third.

Which industry vertical is growing the quickest?

The automotive and transportation sector, driven by the need for battery-pack and lightweight-material inspections, is forecast to grow at a 11.4% CAGR.

What is the biggest talent-related challenge?

A global shortage of certified PAUT and TOFD technicians extends qualification timelines and elevates labor costs.

Page last updated on: