3D Printing / Additive Manufacturing NDT Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

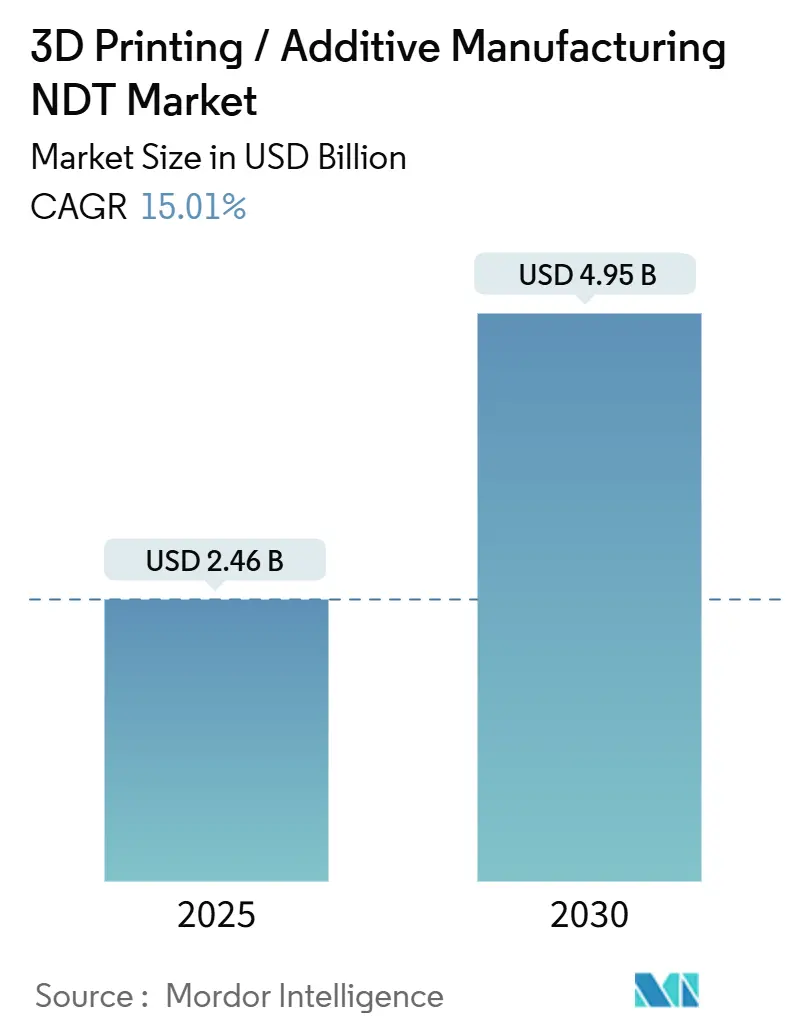

| Market Size (2025) | USD 2.46 Billion |

| Market Size (2030) | USD 4.95 Billion |

| Growth Rate (2025 - 2030) | 15.01% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

3D Printing / Additive Manufacturing NDT Market Analysis by Mordor Intelligence

The 3D printing/additive manufacturing NDT market size was USD 2.46 billion in 2025 and is projected to reach USD 4.95 billion by 2030, reflecting a sturdy 15.01% CAGR during the forecast period. The acceleration mirrors a maturing additive manufacturing landscape, stricter part-qualification mandates in aerospace and medical devices, and the availability of AI-enabled in-process inspection platforms that prevent costly scrap. Hardware remains the backbone of the 3D printing NDT market, yet value is rapidly shifting toward software analytics that unlock predictive insights from sensor data. Regulatory bodies on both sides of the Atlantic now specify continuous monitoring for safety-critical components, compelling companies to invest in real-time quality assurance strategies. Regional dynamics also influence growth: North America optimizes established aerospace programs, whereas Asia Pacific builds greenfield Industry 4.0 factories that rely on fully digital inspection workflows.

Key Report Takeaways

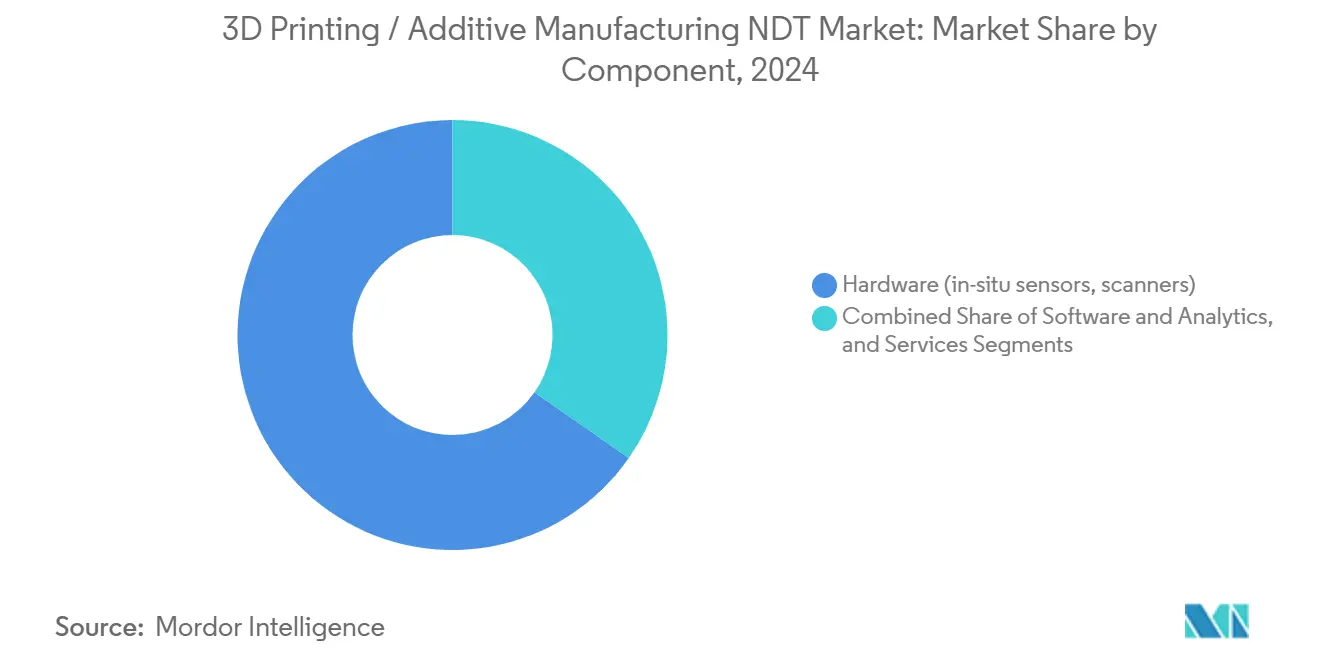

- By component, hardware captured 65.3% of the 3D printing NDT market share in 2024, while software and analytics recorded the fastest CAGR at 19.8% through 2030.

- By testing method, computed tomography led with 29.1% revenue share in 2024; thermography and infrared are advancing at an 18.5% CAGR to 2030.

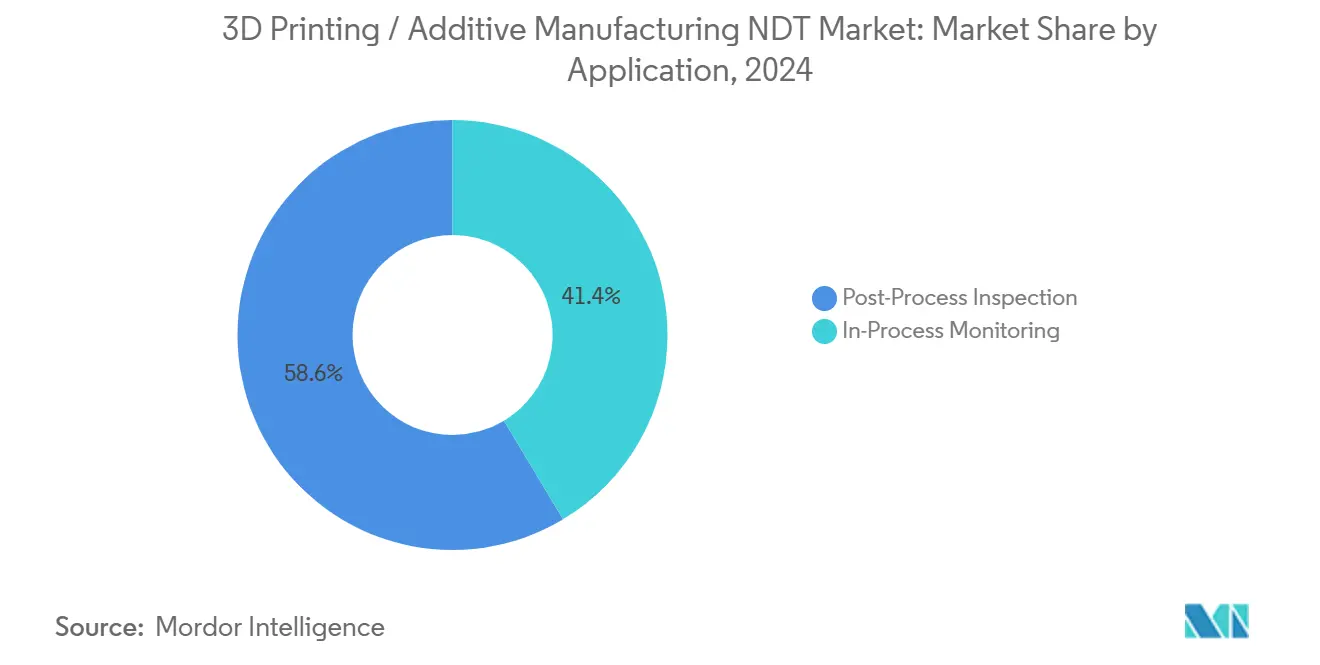

- By application, post-process inspection accounted for 58.6% of the 3D printing NDT market size in 2024, and in-process monitoring is expected to expand at a 20.4% CAGR to 2030.

- By end-user industry, the aerospace sector accounted for 23.5% of demand in 2024, while the medical devices sector was projected to have the highest CAGR at 20.6% through 2030.

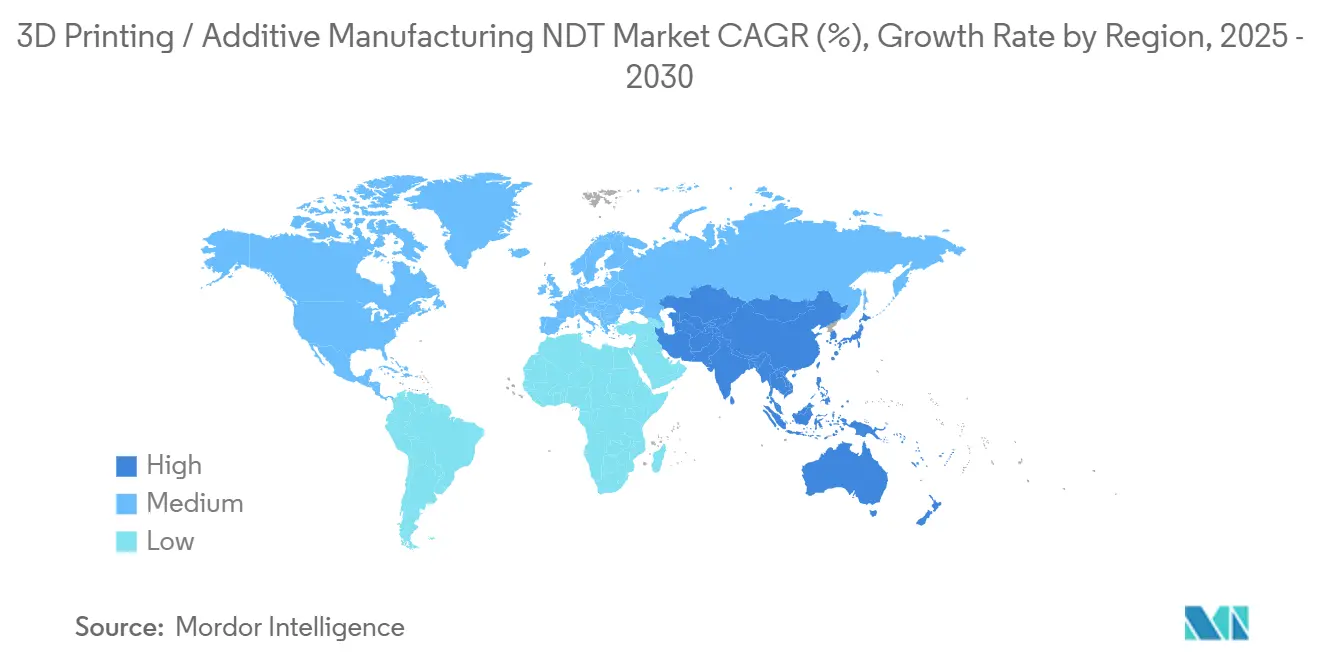

- By geography, North America accounted for 29.5% of the revenue in 2024; the Asia Pacific is forecast to post the strongest CAGR of 17.3% up to 2030.

Global 3D Printing / Additive Manufacturing NDT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing penetration of metal additive manufacturing in aerospace MRO | +3.2% | North America and Europe | Medium term (2-4 years) |

| Cost reduction benefits of in-process NDT integration | +2.8% | Global | Short term (≤ 2 years) |

| Increasing regulatory push for part certification (FAA, EASA) | +2.5% | North America and Europe | Long term (≥ 4 years) |

| Shift toward serial production in medical implants | +2.1% | Global | Medium term (2-4 years) |

| Expansion of industrial-scale binder-jetting lines | +1.9% | APAC core, spill-over to North America | Medium term (2-4 years) |

| AI-enabled real-time defect prediction platforms | +2.6% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Penetration of Metal Additive Manufacturing in Aerospace MRO

The adoption of metal additive manufacturing in maintenance, repair, and overhaul now extends to turbine blades, heat exchangers, and structural brackets. The FAA’s 2024 guidance requires operators to implement continuous inspections for titanium and nickel alloys, thereby elevating demand for inline CT and high-energy X-ray solutions. In Europe, EASA requires documented traceability from powder feedstock to the finished part, prompting the use of integrated database tools that log every melt layer.[1]European Union Aviation Safety Agency, “Certification Specifications for Additive Manufacturing,” easa.europa.eu Boeing’s validated 3D-printed brackets on the 787 program proved that lattice-rich geometries can pass stringent fatigue tests when monitored during each build pass. The complexity of internal cooling channels pushes traditional ultrasound to its limits, opening headroom for acoustic emission arrays coupled to AI filtration. As airlines adopt digital spares strategies, MRO facilities view the 3D printing NDT market as the most reliable path to maintaining airworthiness certifications without increasing turnaround times.

Cost Reduction Benefits of In-Process NDT Integration

Real-time monitoring reduces waste by up to 40% by flagging porosity before it cascades across layers, as demonstrated at leading automotive plants. General Electric observed a 60% reduction in post-processing queues once multi-sensor platforms streamed anomalies directly into MES dashboards, revealing savings that exceeded USD 10,000 per rejected aerospace bracket. Eliminating standalone inspection booths reduces floor space and minimizes crane movements for heavy metal builds, resulting in cumulative throughput gains. Cloud analytics further predicts tool wear, allowing planners to schedule maintenance during slack shifts instead of pausing high-value runs. These compounding efficiencies make the 3D printing NDT market integral to profitability in sectors that once accepted high scrap as the price of design freedom.

Increasing Regulatory Push for Part Certification (FAA, EASA)

Certification roadmaps now embed non-destructive evaluation from powder acceptance onward. Advisory Circular 20-170A defines continuous monitoring as the default approach for aircraft structural parts, compelling printers to integrate multi-axis sensors and high-speed infrared cameras. EASA mirrors the stance, layering additional documentation for directed-energy deposition, while ISO/ASTM 52941 provides harmonized terminology that streamlines global supply-chain audits. Qualification periods of 18-24 months create recurring demand for calibrated equipment and service contracts. Manufacturers lacking validated inspection packages risk certification delays that can stall program launches worth hundreds of millions of USD. Consequently, quality assurance budgets are increasingly allocated to providers who can package hardware, analytics, and training within turnkey kits, reinforcing the long-term pull on the 3D printing NDT market.

Shift Toward Serial Production in Medical Implants

Personalized knee, hip, and cranial implants have transitioned from pilot runs to batches of hundreds per day, particularly since the FDA’s 2024 guidance formalized continuous process validation. Johnson and Johnson scaled its Ethicon facility to output patient-specific orthopedic devices monitored on a layer-by-layer basis, confirming mechanical integrity without post-process sectioning.[2]Johnson & Johnson, “Additive Manufacturing for Medical Devices,” jnj.com Titanium lattices that encourage osseointegration demand high-contrast CT to prove pore interconnectivity, while cobalt-chromium dental arches need eddy-current sweeps to verify full fusion. Automated robotics transfer implants from build plates to cleaning stations, and the same robot triggers inspection macros that store data against unique device identifiers. As reimbursement models in orthopedic care shift toward outcome-based contracts, manufacturers regard robust NDT evidence as indispensable for liability management, ensuring sustained momentum for the 3D printing NDT market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of standardized inspection protocols for complex lattice structures | -1.8% | Global | Medium term (2-4 years) |

| High upfront cost of integrated monitoring hardware | -2.1% | Global | Short term (≤ 2 years) |

| Limited skilled workforce in hybrid AM-NDT operations | -1.5% | Global | Long term (≥ 4 years) |

| Data security concerns around cloud-based inspection analytics | -1.2% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Lack of Standardized Inspection Protocols for Complex Lattice Structures

Most ASTM and ISO documents still target castings and forgings, leaving additive lattices without prescriptive acceptance criteria. Consequently, aerospace primes draft proprietary standards that suppliers must decipher, eroding scale economies across global supply chains. The American Society for Testing and Materials has committees working on method-specific annexes, yet broad ratification may slip beyond 2026. Without a global consensus, auditors often demand redundant scans, thereby inflating inspection labor costs on low-margin parts. Medical regulators tread cautiously, approving implants on a case-by-case basis until public standards are established. This uncertainty tempers investment in new inspection capacity and slows the overall CAGR of the 3D printing NDT market.

High Upfront Cost of Integrated Monitoring Hardware

A full stack of high-energy CT, powder-bed cameras, and laser profilometers can top USD 500,000 per metal line, a daunting entry ticket for small contract manufacturers. While leasing models alleviate cash stress, CFOs still weigh the risk of technology obsolescence in a rapidly evolving field. Emerging-market firms face even steeper hurdles: scarce local service networks lengthen downtime when equipment fails, dampening ROI calculations. Although subscription analytics offset some capital pain, firms must still retrofit machines with ruggedized sensors. Until hardware ASPs compress or financing spreads tighten, the 3D printing NDT market loses potential customers, as they are unable to clear the investment bar.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Dominance Faces Software Disruption

Hardware led the 3D printing NDT market in 2024, accounting for 65.3% of revenue through sensors, scanners, and imaging modules that anchor every inspection workflow. CT gantries, phased-array ultrasound heads, and infrared cameras form the first line of data capture. Yet software is recasting the value equation, expanding at a 19.8% CAGR as AI routines classify voxels, quantify porosity, and generate automated compliance certificates that regulators now accept as audit evidence. Services contribute through calibration, validation, and process consulting engagements that knit hardware and analytics into unified solutions.

The convergence of physical instrumentation and cloud processing is accelerating. Hexagon AB’s defect-classification suite ships pre-loaded on its CT systems, transforming what was once a standalone kit into a data appliance. Service partners piggyback by offering continuous improvement programs that mine inspection logs for design-for-manufacture tweaks. Over 2025-2030, OEMs expect subscription software to outpace capex hardware in margin contribution, underlining a strategic pivot within the 3D printing NDT market.

By Testing Method: Computed Tomography Leadership Challenged by Thermal Innovation

Computed tomography retained 29.1% command of the 3D printing NDT market share in 2024, prized for non-destructive visibility of hidden voids and cooling passages that define aerospace and medical excellence. Thermography and infrared, although historically secondary, are scaling quickly at an 18.5% CAGR because they deliver frame-rate feedback during each laser pass and do not interrupt production. Ultrasonic arrays are well-suited for thick metal builds, while radiographic sources address niche alloy stacks that require high penetration energy.

The competitive dynamic now favors hybrid stacks. ZEISS Group’s inline CT unit combines fan-beam scans with thermographic overlays, merging spatial resolution and temporal insight in a single console. Machine-vision visual inspection resurrects the oldest NDT technique, utilizing AI guidance to sort surface anomalies at pixel resolutions previously unattainable. Acoustic-emission probes whisper early warning signs of micro-crack propagation, enabling proactive parameter tuning rather than scrapping at the end of the build. Such method mash-ups keep the 3D printing NDT market vibrant as buyers seek multipurpose systems that amortize investment across part families.

By Application: Post-Process Dominance Yields to Real-Time Prevention

Final inspection workflows still generated 58.6% of 2024 revenue, reflecting the entrenched aerospace and FDA-linked protocols that demand proof at delivery. However, in-process monitoring rockets ahead at 20.4% CAGR, signaling a philosophical pivot from detection to prevention. Inline cameras, photodiodes, and melt-pool pyrometers detect powder spatter or balling within milliseconds, triggering immediate recoats or layer aborts that salvage material.

Desktop Metal’s Live Inspect ecosystem integrates melt-pool analytics with printer firmware, ensuring defects cannot propagate undetected. Post-process still matters, especially for dimensional metrology, but its role skews toward documentary assurance rather than primary flaw discovery. The sweet-spot strategy blends both: in-process data drives closed-loop control, while selective CT verifies regulatory milestones, yielding a balanced cost-quality harmony that propels the 3D printing NDT market.

By End-User Industry: Aerospace Maturity Contrasts Medical Device Acceleration

Aerospace accounted for 23.5% of 2024 demand, a testament to the industry's long lead times and a culture that budgets generously for safety validation. FAA and EASA decrees mandate integrated inspections for turbine blades, brackets, and environmental control system parts, solidifying aerospace as the leading client segment. In contrast, medical devices, although smaller in absolute dollars, grow at a 20.6% CAGR as orthopedic and dental firms transition prototypes into mass-personalization pipelines.

Stryker, Zimmer Biomet, and Johnson and Johnson now wield fleets of calibrated printers, each paired with CT towers tuned for trabecular gradient structures. Automotive adoption is steadier but increases annually as lightweight brackets and e-motor cooling jackets transition to additive routes, which demand high-throughput vision systems. Energy, marine, and semiconductor users add incremental volume, each bringing specialized inspection quirks that broaden the 3D printing NDT market’s solution palette.

Geography Analysis

North America retained 29.5% of global revenue in 2024, driven by entrenched aerospace, defense, and space programs that had institutionalized additive manufacturing a decade earlier. The FAA’s clear rulebook reassures investors, while defense primes such as Lockheed Martin and Boeing embed inspection protocols inside every part-qualification dossier.[3]Lockheed Martin Corporation, “Manufacturing Capabilities,” lockheedmartin.com Canada contributes to Bombardier’s aggressive CT adoption for regional-jet components, whereas Mexico’s automotive corridor champions mid-cost infrared units for lightweight bracket runs.

The Asia Pacific region is projected to post the fastest 17.3% CAGR through 2030, as China’s Made in China 2025 policy directs subsidies toward integrated print-and-inspect factories. Government institutes in Shanghai and Shenzhen procure large-volume CT scanners for public R&D test beds that regional suppliers can rent, thereby lowering entry friction. Japan leads robotics-assisted inspection: cobots shuttle parts from binder-jet modules into multi-sensor bays without human touch. South Korea piggybacks on semiconductor packaging applications that require micron-scale CT, while India’s nascent aerospace sector offsets attract pilot orders for ultrasound solutions, expanding the customer pool for the 3D printing NDT market.

Europe remains a precision-engineering powerhouse. Germany wields automotive heft, fitting Siemens-led smart factories with AI-powered defect dashboards. France’s Safran and Airbus invest in lattice-focused eddy-current arrays, whereas the United Kingdom nurtures research clusters around Renishaw’s sensor suites. Southern Europe is inching forward as Italian and Spanish firms add additive spare parts operations for rail and energy, albeit at lower volumes. The region’s sustainability agenda favors additive refurbishment, demanding inspection regimes that confirm life-extension claims and further energize the 3D printing NDT market.

Competitive Landscape

The 3D printing NDT market exhibits moderate concentration, with legacy titans and agile specialists competing for integrated contracts. Baker Hughes couples ultrasound pedigrees with laser powder-bed cameras, rolling out an AM-specific platform that cuts inspection windows by 35% at launch for customers.[4]Baker Hughes, “Inspection Technologies,” bakerhughes.com Hexagon AB spends USD 45 million on defect-classification AI, betting that algorithms, not hardware, will differentiate future bids. ZEISS Group has leveraged its medical-device CT expertise to create inline assemblies that are now integrated into orthopedic implant lines, reducing validation time without compromising resolution.

Strategic tie-ups multiply. GE Waygate partners with two leading aerospace OEMs to co-author inspection routines for cooling channels unreachable by borescopes, effectively creating de facto standards that the broader sector may adopt. Olympus Corporation acquired a Belgian AI start-up to strengthen its software stack, signaling a shift in services beyond optical instrumentation. Materialize and 3D Systems court cloud analytics, aggregating multi-site scan logs into centralized dashboards that feed design feedback loops.

Patent filings underscore intensity. Cognex advances machine-vision claims with pixel-level melt-pool characterization, while Renishaw secures coverage for multi-wavelength laser profilometry in powder-bed fusion quality maps. Price competition intensifies, but differentiation through turnkey bundles protects margins. Customers increasingly prefer single-invoice solutions that combine hardware, analytics, and compliance paperwork, a trend likely to reinforce the trajectory of the 3D printing NDT market.

3D Printing / Additive Manufacturing NDT Industry Leaders

Baker Hughes Inspection Technologies

Hexagon AB

Waygate Technologies (A GE Business)

Olympus Corporation

Eddyfi Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Stratasys boosted polymer-printing inspection capabilities to support automotive volumes.

- September 2024: Baker Hughes launched an integrated NDT platform for metal additive manufacturing that combines ultrasonic testing with real-time process monitoring, achieving a 35% cut in inspection time at early aerospace customers.

- August 2024: Hexagon AB invested USD 45 million to expand AI-powered defect classification and CT solutions for serial production lines.

- July 2024: ZEISS Group introduced an inline CT inspection system tailored for additive manufacturing, reducing cycle times for medical device production.

Global 3D Printing / Additive Manufacturing NDT Market Report Scope

| Hardware (in-situ sensors, scanners) |

| Software and Analytics |

| Services |

| Ultrasonic Testing |

| Radiographic Testing |

| Magnetic Particle Testing |

| Liquid Penetrant Testing |

| Visual Inspection Testing |

| Eddy-Current Testing |

| Acoustic Emission Testing |

| Thermography / Infrared Testing |

| Computed Tomography Testing |

| In-Process Monitoring |

| Post-Process Inspection |

| Oil and Gas |

| Power Generation |

| Aerospace |

| Defense |

| Automotive and Transportation |

| Manufacturing and Heavy Engineering |

| Construction and Infrastructure |

| Chemical and Petrochemical |

| Marine and Ship Building |

| Electronics and semiconductor |

| Mining |

| Medical Devices |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Hardware (in-situ sensors, scanners) | ||

| Software and Analytics | |||

| Services | |||

| By Testing Method | Ultrasonic Testing | ||

| Radiographic Testing | |||

| Magnetic Particle Testing | |||

| Liquid Penetrant Testing | |||

| Visual Inspection Testing | |||

| Eddy-Current Testing | |||

| Acoustic Emission Testing | |||

| Thermography / Infrared Testing | |||

| Computed Tomography Testing | |||

| By Application | In-Process Monitoring | ||

| Post-Process Inspection | |||

| By End-user Industry | Oil and Gas | ||

| Power Generation | |||

| Aerospace | |||

| Defense | |||

| Automotive and Transportation | |||

| Manufacturing and Heavy Engineering | |||

| Construction and Infrastructure | |||

| Chemical and Petrochemical | |||

| Marine and Ship Building | |||

| Electronics and semiconductor | |||

| Mining | |||

| Medical Devices | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the 3D printing NDT market?

The 3D printing NDT market size reached USD 2.46 billion in 2025.

What is the market's expected growth rate?

It is forecast to advance at a 15.01% CAGR, hitting USD 4.95 billion by 2030.

Which component segment is growing the quickest?

Software and analytics lead growth with a 19.8% CAGR as AI becomes central to inspection workflows.

Why is aerospace a key adopter of NDT in additive manufacturing?

FAA and EASA mandates require continuous quality monitoring for flight-critical 3D-printed parts, driving sustained investment in this area.

What restrains smaller firms from adopting integrated inspection?

High upfront costs, often surpassing USD 500,000 per line, remain a primary barrier for small and medium-sized manufacturers.

Which region is forecast to record the highest growth rate?

The Asia Pacific, driven by China, Japan, and South Korea, is projected to expand at a 17.3% CAGR through 2030.

Page last updated on: