Vegetable Puree Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

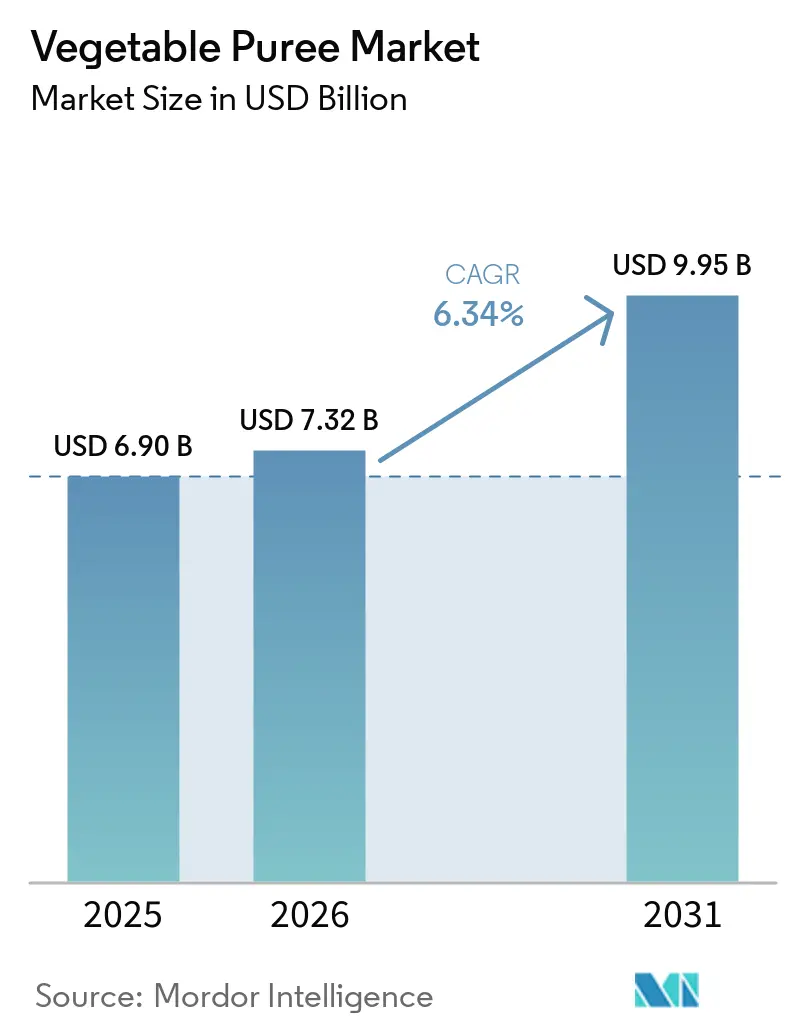

| Market Size (2026) | USD 7.32 Billion |

| Market Size (2031) | USD 9.95 Billion |

| Growth Rate (2026 - 2031) | 6.34% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vegetable Puree Market Analysis by Mordor Intelligence

The vegetable puree market size is projected to be USD 6.90 billion in 2025, USD 7.32 billion in 2026, and reach USD 9.95 billion by 2031, growing at a CAGR of 6.34% from 2026 to 2031. Robust growth reflects tighter infant-food safety rules, rapid adoption of high-pressure processing, and rising consumer affinity for plant-based nutrition. The United States Food and Drug Administration (FDA) capped lead in processed vegetables for babies at 10 ppb in January 2025, compelling intensified raw-material testing and traceability [1]Source: Food and Drug Administration, “Action Levels for Lead in Processed Food Intended for Babies and Young Children,” federalregister.gov. Simultaneously, the USDA’s Strengthening Organic Enforcement rule, effective March 2024, demands organic certificates for all imports, favoring processors with certified domestic supply chains. Investments in stand-up pouches and spouted formats, together with high-pressure and aseptic technologies, are expanding premium retail offerings while mitigating cold-chain costs. Europe remains the anchor region owing to rigorous food-safety laws and mature infrastructure, whereas Asia-Pacific is the quickest-growing territory as governments fund processing capacity and urban consumers seek convenient vegetable-based foods.

Key Report Takeaways

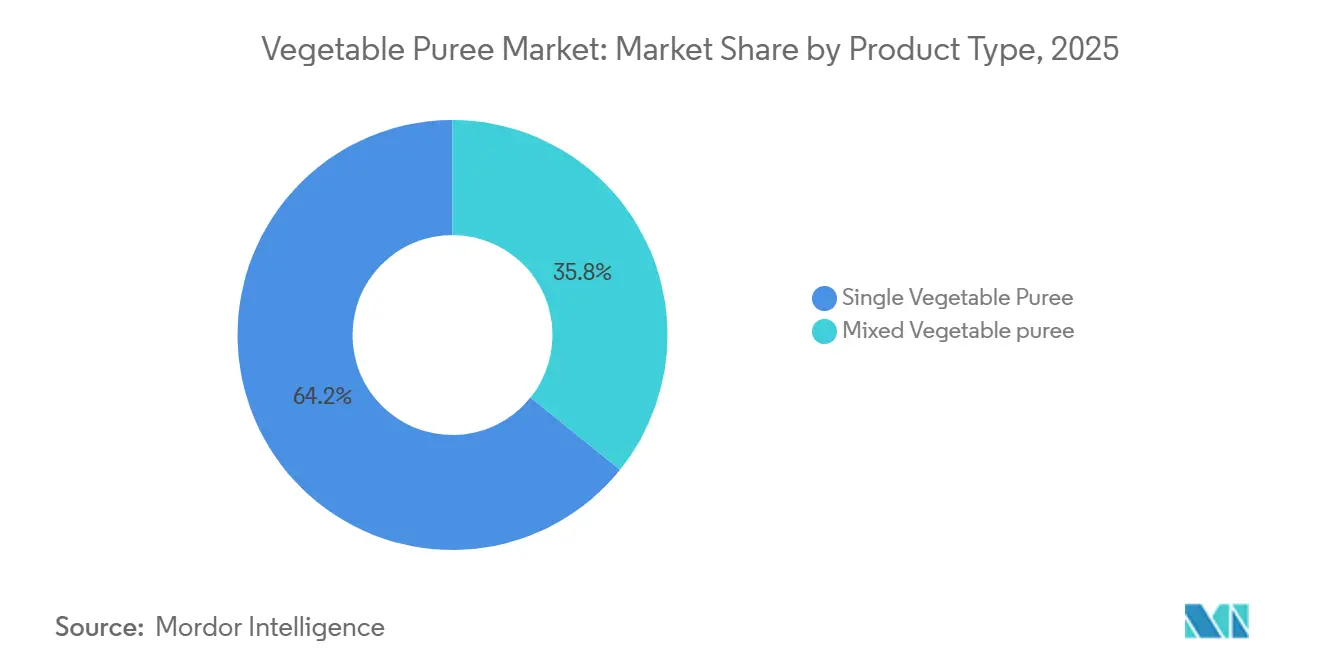

- By product type, single-vegetable purees led with 64.23% of market share in 2025; mixed formulations are projected to expand at a 6.58% CAGR through 2031.

- By nature, conventional processing retained 85.63% share of the vegetable puree market size in 2025, yet organic alternatives are advancing at a 7.75% CAGR to 2031.

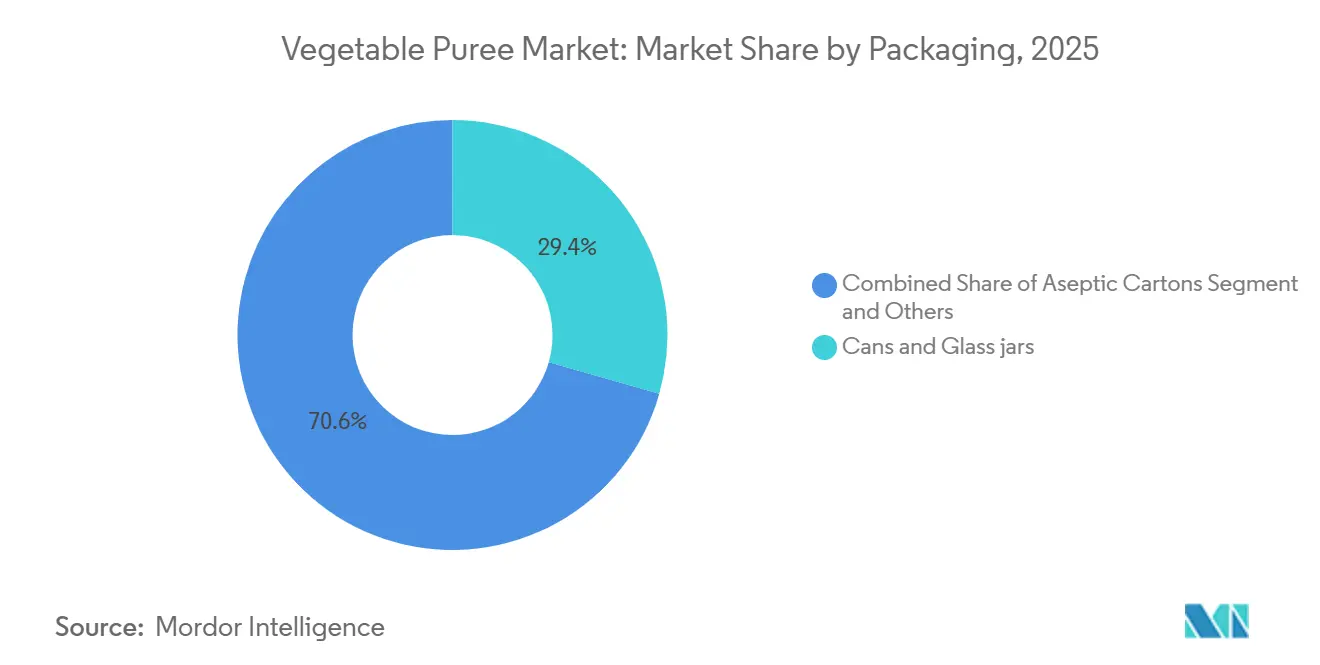

- By packaging, cans and jars commanded 29.40% revenue in 2025, while stand-up pouches are growing fastest at a 7.83% CAGR.

- By end user, industrial food processors captured 51.60% share of the vegetable puree market size in 2025, whereas retail channels are rising at an 8.25% CAGR.

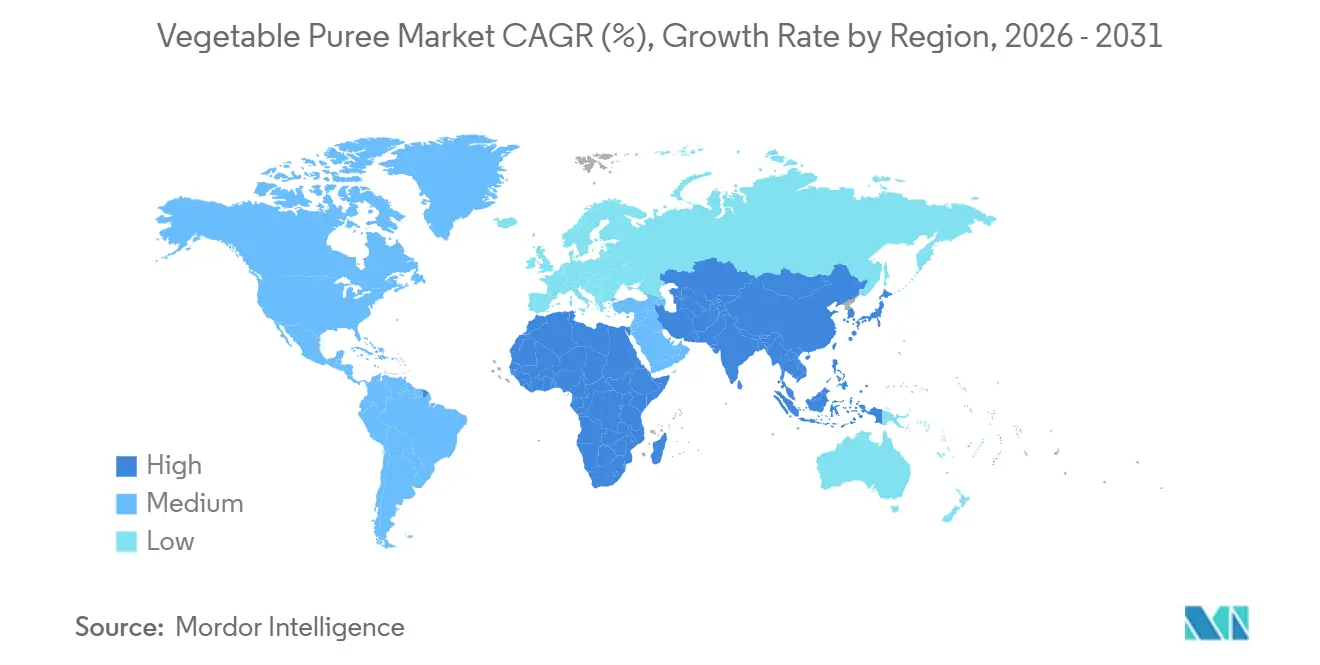

- By geography, Europe accounted for 31.43% of market share in 2025, whereas Asia-Pacific registered the fastest growth at 7.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Vegetable Puree Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for convenient baby-food formulations | +1.8% | Global; strongest in North America & Europe | Medium term (2-4 years) |

| Expansion of plant-based & flexitarian diets | +1.5% | North America & Europe; gaining in APAC | Long term (≥ 4 years) |

| Growth of RTD vegetable-based beverages | +1.2% | Global; led by North America | Medium term (2-4 years) |

| Culinary innovation & product diversification | +0.9% | Europe & North America; emerging in APAC | Long term (≥ 4 years) |

| Waste-valorization partnerships with “ugly-veg” suppliers | +0.6% | Europe & Australia; expanding worldwide | Long term (≥ 4 years) |

| Cold-press/HPP processing enabling nutrient retention | +0.8% | Developed markets worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising demand for convenient baby-food formulations

The demand for convenient, ready-to-use baby food formulations, including vegetable purees, continues to grow as more families seek safe and nutritionally balanced meal solutions. Increasing participation of women in the workforce has shifted consumer preference toward time-saving food products that do not compromise on health or safety. According to the U.S. Bureau of Labor Statistics, more than 72% of mothers with children under 18 were part of the labor force in 2023, driving reliance on prepared foods and underpinning sustained growth in the packaged baby food segment, including purees. Tighter metal-contaminant limits have transformed product-development priorities. Further, the enhanced guidelines propelling in the market are gaining consumer trust. The FDA’s lead guideline obliges producers to invest in advanced testing methods, ingredient segregation, and supplier audits. California’s AB 899 further mandates public disclosure of arsenic, cadmium, mercury, and lead test results, influencing nationwide retail assortments [2]Source: California Department of Public Health, “AB 899 Baby Food FAQs,” cdph.ca.gov.

Expansion of plant-based and flexitarian diets

Mainstream consumers increasingly substitute meat with vegetable-centric meals, elevating demand for versatile purées as bases for sauces, dips, and plant-protein analogues. According to the U.S. Department of Agriculture's Dietary Guidelines for Americans, increased consumption of vegetables is encouraged for disease prevention and overall health. This societal trend translates into a greater market for vegetable purees, as consumers, motivated by health, ethical, and environmental considerations, seek convenient options that fit their evolving dietary habits. Joint ventures such as Kraft Heinz-NotCo employ artificial-intelligence formulation to replicate legacy flavors with vegetable ingredients, accelerating time-to-market for plant-based staples. In Europe, the VALPRO Path project builds short supply chains that let farmers process pulses and vegetables locally, securing higher margins and lowering logistics emissions. Such localization trends support the vegetable puree market by stabilizing raw-material access and responding to sustainability-driven procurement policies.

Growth of ready-to-drink vegetable-based beverages

High-pressure processing (HPP) enables shelf-stable beverages that preserve chlorophyll and carotenoids, bridging traditional juice and puree categories. Kagome’s shift from a tomato-centric identity toward a general “vegetable company” underpins new RTD lines that pair savory notes with dietary fiber, supported by AI-based agronomy partnerships to guarantee raw-material consistency. Data from the USDA’s Economic Research Service confirms expanding innovation and consumption within the vegetable beverage segment, reflecting a broader transition toward on-the-go, health-oriented drinks. Aseptic pouch technology further reduces cold-chain reliance, opening emerging-market distribution channels and reinforcing the value proposition of the vegetable puree market.

Culinary innovation and product diversification

Foodservice operators emphasize regional authenticity and zero-waste cooking, stimulating demand for niche purées from heritage vegetables. Equipment firms such as Provisur now supply refiners capable of artisanal texture at commercial throughput, enabling manufacturers to capture chef-driven demand spikes. Texturization advances, including Clextral’s shear-cell system, blur boundaries between purées and fibrous meat analogues, enlarging application scope. Public sector initiatives and research funding have played a significant role in fostering culinary innovation and product diversification in the vegetable-based food sector. Support for research on novel blends, processing technologies, and fortification methods, referenced in USDA funding announcements and food innovation reports, has led to the introduction of new vegetable puree products, appealing to consumer demand for unique flavors and functional attributes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain volatility for key vegetables | −1.2% | Global; severe in emerging markets | Short term (≤ 2 years) |

| High cold-chain logistics cost in emerging markets | −0.8% | APAC, Latin America, MEA | Medium term (2-4 years) |

| Regulatory hurdles on nitrate limits in leafy-green purées | −0.4% | Europe; spreading to North America | Long term (≥ 4 years) |

| Consumer skepticism over shelf-stable purées vs. fresh | −0.3% | North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply-chain volatility for key vegetables

Climate-induced yield swings are driving up raw-material prices and heightening sourcing risks. European processor Ardo, facing a 15-20% yield drop in open-field crops, has initiated its “Mimosa+” program, focusing on regenerative agriculture to rejuvenate soil fertility. While digital twins and AI-driven demand forecasting enhance inventory planning, they demand capital often out of reach for smaller firms, pushing the vegetable puree market towards consolidation. The vegetable puree market grapples with supply-chain instability, influenced by weather variability, disease outbreaks, and changing production yields. The USDA frequently highlights these challenges, pointing out that erratic harvests can trigger price volatility and supply shortages. Such disruptions pose risks for manufacturers, potentially leading to increased costs or a scarcity of essential puree ingredients.

High cold-chain logistics cost in emerging markets

High costs associated with cold-chain infrastructure pose a serious restraint on the distribution and storage of perishable vegetable purees, especially in emerging markets. According to the Food and Agriculture Organization and corroborated by the USDA Foreign Agricultural Service, inadequate cold-chain capacity leads to significant post-harvest losses and increased logistics expenses. This limits the ability of producers to expand market reach, impacts price competitiveness, and can ultimately constrain market growth where refrigeration and transportation networks are underdeveloped. In India, fragmented infrastructure inflates per-kilogram chilled freight costs, constraining penetration of premium purées. Reusable phase-change packaging from Candor Food Chain maintains temperature for nine days without dry ice, trimming transport expense and emission footprint. Still, up-front equipment expenditures remain a barrier for small processors[3]Source: Packaging Digest, “Candor Food Chain Rolls Out Cool Tech,” packagingdigest.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Single Purées Anchor, Blends Accelerate

Single vegetable offerings held 64.23% of the vegetable puree market share in 2025, reflecting regulatory simplicity and easier nutritional labeling in infant nutrition applications. Producers benefit from streamlined sourcing contracts and process consistency, enabling competitive pricing and reliable quality. Legacy processors maintain dedicated lines for carrots, sweet potatoes, and green peas, optimizing throughput and minimizing cross-contamination risk. Also, Single vegetable purees retain the original flavor, nutrition, and color of the source vegetable, making them appealing to both manufacturers and health-conscious consumers.

Mixed purées, however, are advancing at a 6.58% CAGR to 2031, buoyed by culinary demand for layered flavor and color. This growth is spurred by increasing consumer interest in innovative flavors and products offering enhanced nutritional profiles. Chefs employ blends to mimic regional stews or to enhance plant-protein dishes, supporting menu innovation in HoReCa channels. Industrial equipment capable of gentle particulation preserves sensory attributes in complex formulations, allowing premium pricing. The segment’s momentum feeds into the broader vegetable puree market as brands highlight combined phytonutrient claims and convenience.

By Nature: Organic Momentum Builds on Consumer Trust

Conventional processing dominated 85.63% of the vegetable puree market size in 2025, upheld by cost efficiency and well-established global supply chains. These processors increasingly adopt sustainable farming partnerships and renewable-energy boilers to satisfy retailer scorecards without incurring certification overheads. Also, their broader availability, lower price points, and established supply chains that enable cost-efficient mass production make it more appealing. A significant portion of the food processing industry continues to source conventional vegetable purees for large-scale applications, as price sensitivity remains a key driver in many markets, especially in developing regions.

Organic variants, growing at 7.75% CAGR, are winning loyalty among health-oriented parents. Growing health consciousness and a global surge in demand for clean-label and chemical-free products are major contributors. Consumers become increasingly aware of potential residues in conventional produce and seek high-quality, traceable food sources. The USDA Strengthening Organic Enforcement rule, which requires more entities to secure certification, briefly squeezed supplies but ultimately enhances integrity and transparency. Retailers use blockchain-enabled QR codes to demonstrate farm provenance, reinforcing price premiums.

By Packaging: Flexible Formats Outpace Rigid Containers

Cans and glass jars claimed 29.40% revenue in 2025, prized for hermetic sealing, thermal-retort compatibility, and familiarity among institutional buyers. This legacy dominance is the result of the packaging’s ability to preserve flavor, extend shelf life, and withstand rigorous transport conditions favored by food processors and export markets. Cans and jars are especially valued by industrial and foodservice customers for bulk applications, and their re-sealable nature appeals to both processors and end consumers seeking portion control and minimal waste.

Stand-up pouches, expanding at a 7.83% CAGR, owing to reclosable spouts and reduced material usage. Stand-up pouches are particularly attractive in retail and e-commerce, as they facilitate easy storage, display, and use, especially for on-the-go consumers and small households. Brands are also leveraging spouted or resealable pouch innovations to appeal to parents and younger demographics, making this category a focal point for packaging innovation and sustainability efforts. Also, innovations such as Accredo’s 100% sugarcane-based resin pouch sequester 43 g CO₂ per unit while meeting drop-test and barrier specifications. Amcor’s fully polyolefin recyclable retort pouch adds shelf-stable capability without sacrificing circularity. These advances underpin the sustainability narrative that propels the vegetable puree market.

By End User: Retail Surge Complements Industrial Bedrock

In 2025, industrial processors claimed 51.60% of the vegetable puree market, bolstered by long-term contracts with manufacturers of baby food, soups, and sauces. Thanks to economies of scale in procurement and a continuous-flow production approach, these processors maintain stable margins, even amidst commodity price fluctuations. Vegetable purees are pivotal in crafting baby food, soups, sauces, ready-to-eat meals, and bakery products. The food industry's steadfast dependence on these purees, appreciating their consistency, scalability, and year-round availability, cements their dominance among institutional buyers and manufacturers.

Retail sales, however, are projected to rise at an 8.25% CAGR as direct-to-consumer brands employ HPP and transparent sourcing stories to justify premium shelf prices. Online grocery and subscription models boost household penetration, particularly among millennial parents seeking clean-label convenience. Consumers increasingly seek convenient, healthy cooking aids and prepared foods that can be readily integrated into daily meals. The retail boom, supported by attractive packaging, clean-label trends, and the rise in “do-it-yourself” home cooking, ensures that purees achieve more visibility and trial compared to traditional channels. Compostable containers and on-pack QR traceability strengthen consumer trust, amplifying the broader vegetable puree market trajectory.

Geography Analysis

Europe accounted for 31.43% of vegetable puree market share in 2025 underpinned by the EU Contaminants Regulation 2023/915, which imposes stringent heavy-metal thresholds and favors regionally compliant suppliers. Industry body 'Propel' coordinates more than 500 processors to lobby for pragmatic policies and to disseminate best practices in sustainable cultivation. The Green-loop consortium pioneers compostable barrier films compatible with the forthcoming Packaging and Packaging Waste Regulation, aligning packaging innovation with circular-economy goals.

Asia-Pacific registers the fastest growth at 7.46% CAGR through 2030. India’s growing food-processing outlay illustrates governmental impetus via the Pradhan Mantri Kisan Sampada Yojana and production-linked incentives. Agrana’s purchase of Saikrupa in India and expansion in Changzhou, China, secure regional production bases, reducing lead times and tariff exposure. Kagome’s AI-guided agronomy trials with NEC target improved field yields matching beverage-grade parameters, enhancing supply resilience.

North America benefits from sophisticated HPP capacity and a vibrant organic segment but faces climatic risks such as drought-induced tomato shortfalls. Investment in regenerative agriculture and controlled-environment farming mitigates volatility, sustaining raw-material inflow for the vegetable puree market. South America leverages abundant arable land; processors focus on exporting aseptic purées to Europe under traceable sustainability protocols. Middle East and Africa, characterized by youthful demographics, sees rising quick-service demand for vegetable-based spreads, albeit tempered by logistic and cold-chain challenges.

Competitive Landscape

The vegetable puree market posts a moderate concentration score, with the five largest companies collectively holding roughly 35% of global revenue. Kagome’s January 2024 acquisition of 70% of Ingomar Packing deepened North American integration and added thermal-processing know-how. . Ingredion's USD 100 million modernization of its Indianapolis plant upgraded automation and energy efficiency, setting a benchmark for legacy factories.

Technology partnerships are pivotal. Kraft Heinz-NotCo’s AI co-lab accelerates plant-based formulation cycles, while OctoFrost’s IQF freezers meet emerging demand for rapid-frozen vegetable particulates in South Asia. Sustainability remains a battleground: Amcor’s recyclable retort pouch and Accredo’s bio-based resin packages help brand owners cut Scope 3 emissions. Competitors also forge waste-valorization alliances to secure low-cost inputs and satisfy zero-waste pledges, reinforcing differentiation strategies within the vegetable puree industry.

Regulatory acumen is another competitive lever. Firms with ISO 17025-accredited labs rapidly validate compliance with evolving heavy-metal or nitrate thresholds, reducing time-to-shelf for new SKUs. Regional processors without such capabilities increasingly seek co-manufacturing agreements with global majors, intensifying bargaining power of technology-rich incumbents in the vegetable puree market.

Vegetable Puree Industry Leaders

Bonduelle

Kagome Co., Ltd.

Mutti S.p.A.

Ingredion

Döhler GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Green Giant is debuting its new canned 100% Pure Pumpkin. Sourced from U.S. family-owned farms, the new Green Giant 100% Pure Pumpkin offers home cooks a reliable and tasty option just in time for the holidays. Moreover, when stacked against the leading canned pumpkin brand, Green Giant 100% Pure Pumpkin emerges as a premium yet budget-friendly alternative.

- July 2023: Heinz has launched its new 'Culinary Tomatoes' range, featuring chopped and peeled tomatoes, a traditional pizza sauce, and tomato puree. The lineup also includes tomato bases for cooking sauces, such as passata, chili, curry, and frito.

Global Vegetable Puree Market Report Scope

Vegetable puree includes purees of single and mixed vegetables sold to retail, food processing, and horeca sectors. The Vegetable Puree Market Report is Segmented by Product Type (Single Vegetable Purees, Mixed Vegetable Purees), Nature (Organic, Conventional), Packaging (Cans and Glass Jars, Aseptic Cartons, and More), End User (Food Processing/Industrial, Horeca, Retail), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Single Vegetable Purees |

| Mixed Vegetable Purees |

| Organic |

| Conventional |

| Cans and Glass Jars |

| Aseptic Cartons |

| Frozen Blocks |

| Stand-up Pouches |

| Bulk Drums/IBC |

| Food Processing/Industrial | |

| HoReCa | |

| Retail | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Specialty/Gourmet Stores | |

| Online Retail/E-commerce | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Russia | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Rest of Middle East and Africa |

| By Product Type | Single Vegetable Purees | |

| Mixed Vegetable Purees | ||

| By Nature | Organic | |

| Conventional | ||

| By Packaging | Cans and Glass Jars | |

| Aseptic Cartons | ||

| Frozen Blocks | ||

| Stand-up Pouches | ||

| Bulk Drums/IBC | ||

| By End User | Food Processing/Industrial | |

| HoReCa | ||

| Retail | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Specialty/Gourmet Stores | ||

| Online Retail/E-commerce | ||

| Others | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Russia | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the vegetable puree market?

The vegetable puree market size stands at USD 6.9 billion in 2025 and is projected to reach USD 9.95 billion by 2031.

Which region holds the largest share of the vegetable puree market?

Europe leads with 31.43% share in 2025, benefiting from strict safety regulations and mature processing infrastructure.

Why are stand-up pouches gaining popularity in vegetable puree packaging?

Stand-up pouches offer resealability, reduced material use, and improved sustainability profiles, driving a 7.83% CAGR in their adoption.

How are new safety regulations influencing product development?

The FDA’s 10 ppb lead limit is pushing manufacturers to upgrade testing and traceability systems, elevating premium, clean-label offerings.

Page last updated on: