Malware Analysis Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

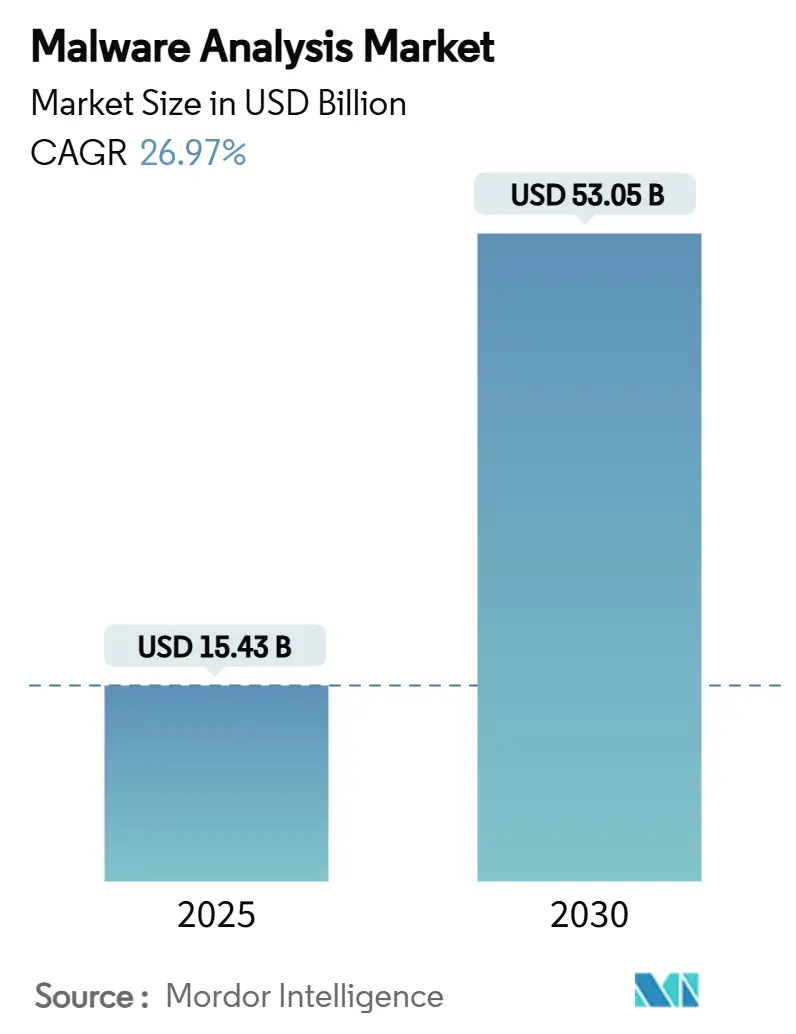

| Market Size (2025) | USD 15.43 Billion |

| Market Size (2030) | USD 53.05 Billion |

| Growth Rate (2025 - 2030) | 26.97% CAGR |

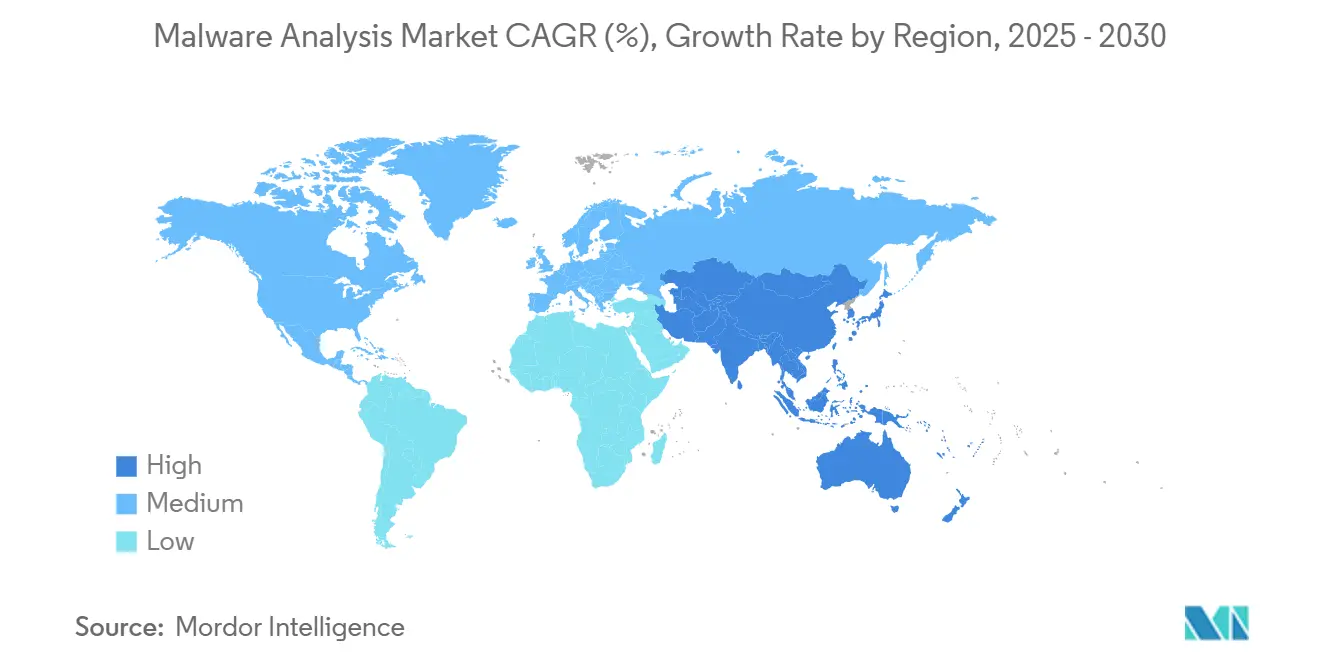

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

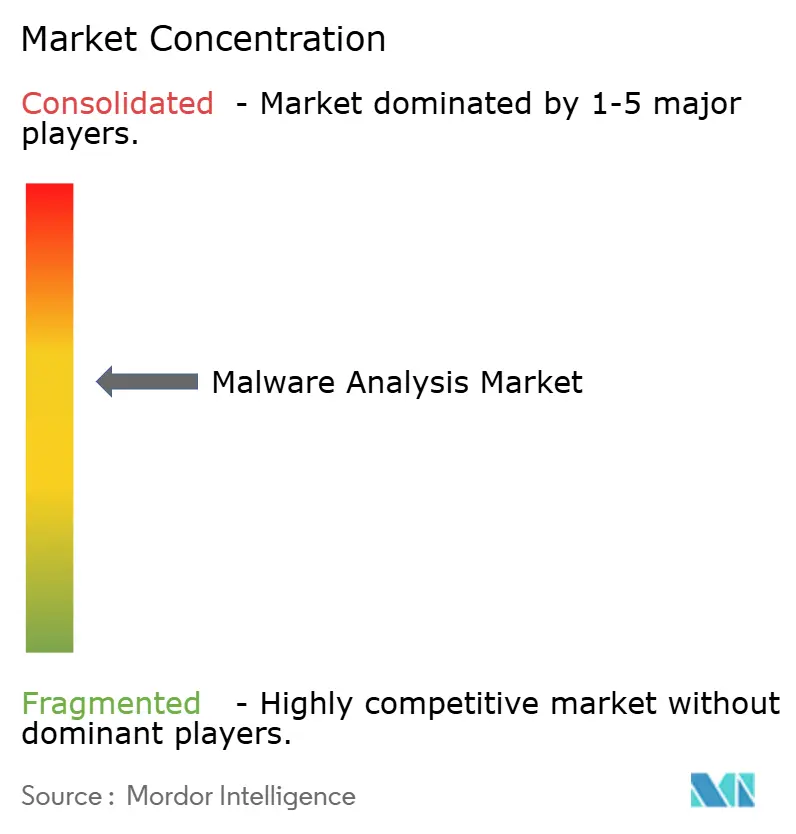

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malware Analysis Market Analysis by Mordor Intelligence

The malware analysis market size stands at USD 15.43 billion in 2025 and is forecast to reach USD 53.05 billion by 2030, reflecting a robust 26.97% CAGR. Persistent advances in polymorphic malware, tougher disclosure mandates, and the integration of artificial intelligence into both attacks and defenses are amplifying demand. Organizations now prioritize automated, behavior-centric inspection over legacy signature matching, while platform vendors bundle malware analytics into extended detection and response suites to streamline security operations. Parallel investment in cloud-native sand-box-free architectures is accelerating adoption among enterprises that must inspect thousands of samples daily without degrading performance.

Key Report Takeaways

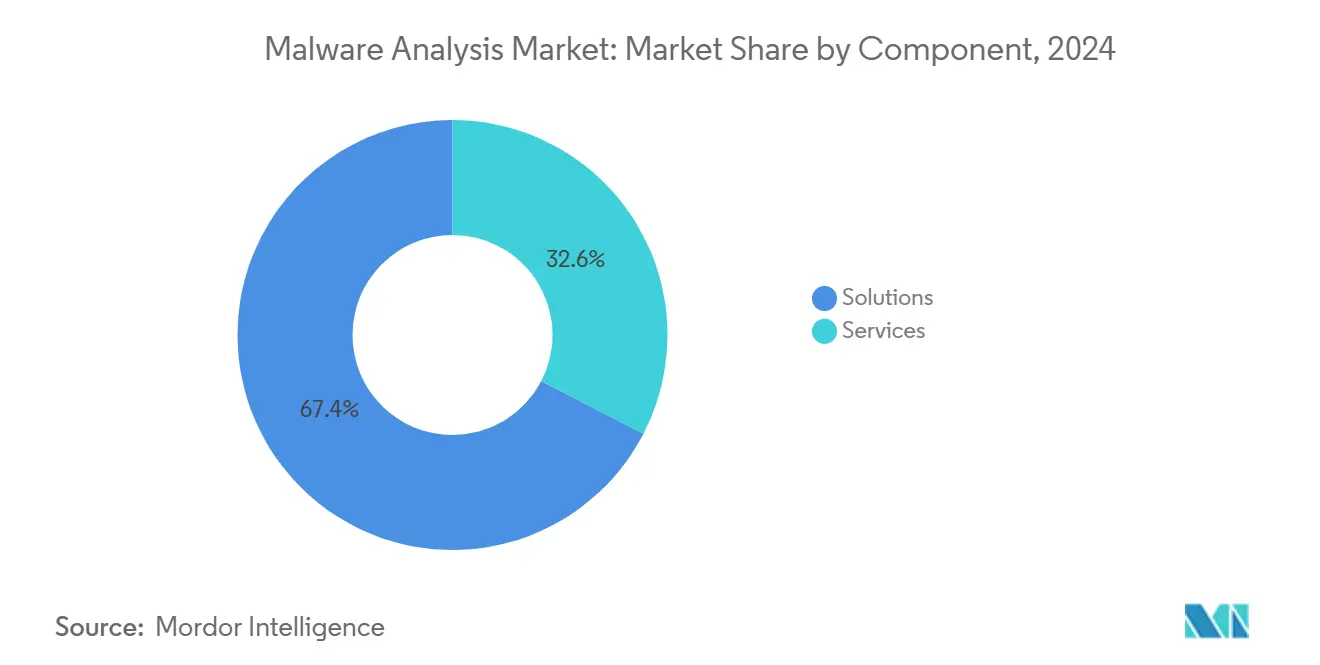

- By component, Solutions controlled 67.4% revenue in 2024; services lagged as firms pivoted to unified platforms that simplify operations and lower total cost of ownership.

- By deployment mode, Cloud deployment secured a 57.0% share in 2024, whereas on-premises models trailed; cloud is also projected to post the fastest 27.5% CAGR to 2030.

- By organization size, Large enterprises accounted for 71.2% of 2024 demand, yet small and medium-sized enterprises will register the highest 28.5% CAGR through 2030.

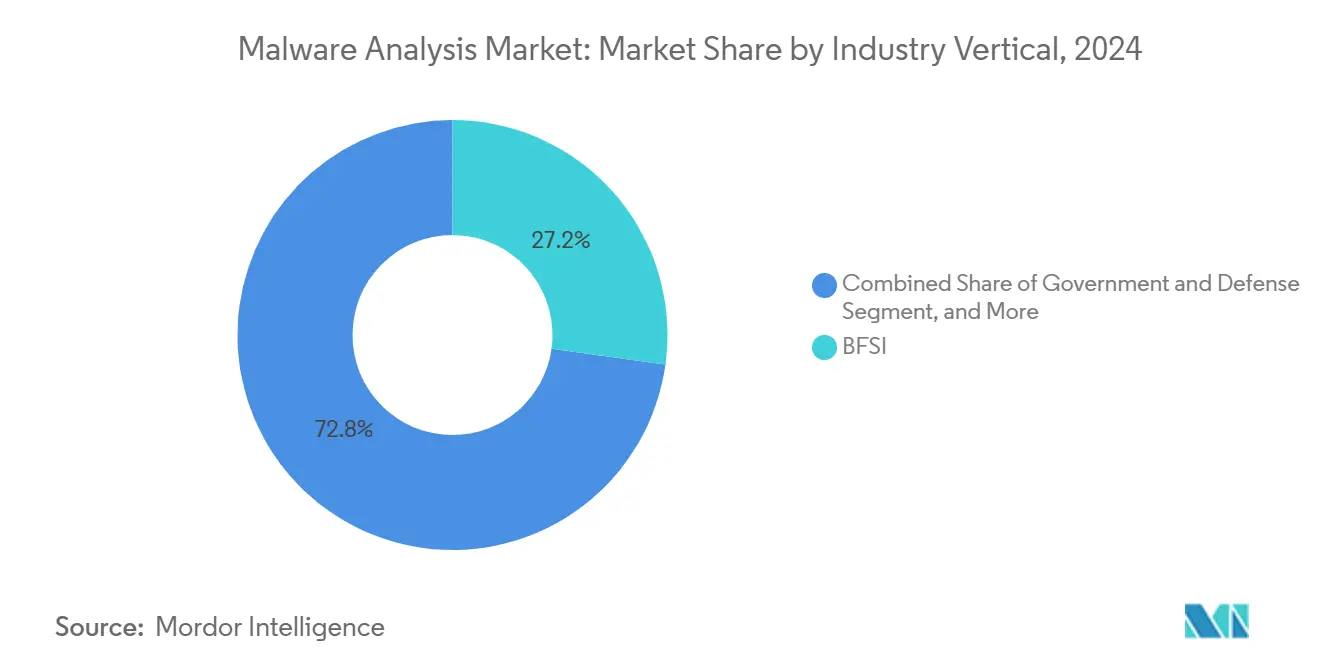

- By industry vertical, Banking, financial services, and insurance led vertical spending with 27.2% share in 2024, while healthcare will expand most quickly at 29.1% CAGR through 2030.

- By analysis technique, Static code analysis held 47.2% share in 2024; hybrid ML-assisted inspection is positioned for the swiftest 29.8% CAGR through 2030.

- By geography, North America captured 35.1% of 2024 revenue, but Asia-Pacific is forecast to be the fastest-growing region at 28.5% CAGR to 2030.

Global Malware Analysis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sophistication of polymorphic malware and AI-driven threats | +6.5% | North America, Europe, Global spillover | Medium term (2-4 years) |

| Surge in supply-chain–oriented attacks on DevSecOps pipelines | +5.8% | North America, Asia-Pacific | Short term (≤ 2 years) |

| Rapid adoption of cloud-native workloads requiring sandbox-free analysis | +4.2% | North America, Europe, Global | Medium term (2-4 years) |

| Mandatory breach-reporting windows (24- to 72-hour) in new cyber-regulations | +3.1% | North America, Europe, Asia-Pacific expansion | Short term (≤ 2 years) |

| "Zero-trust'' funding waves from public-sector stimulus programs | +2.7% | North America, Europe, Developed Asia-Pacific | Medium term (2-4 years) |

| Convergence of XDR and malware sandboxing in single-pane platforms | +1.9% | Global, early uptake in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sophistication of Polymorphic Malware and AI-Driven Threats

AI language models such as DeepSeek R1 can generate functional keyloggers, ransomware loaders, and data exfiltration scripts that mutate their code on demand, collapsing release cycles from months to days. Rust-based BlackCat ransomware illustrates how memory-safe languages complicate static inspection, pushing defenders toward behavior analytics. Enterprises now invest in hybrid engines that fuse static, dynamic, and ML-aided heuristics to detect payloads without relying on brittle signatures. The malware analysis market has responded with offerings that correlate API calls, registry edits, and network telemetry in near real time. Vendors able to train models on diverse telemetry have gained an edge in detecting zero-day exploits.

Surge in Supply-Chain-Oriented Attacks on DevSecOps Pipelines

Threat actors increasingly weaponize software components before they reach production, as demonstrated by the nullifAI technique that implants malicious Pickle files inside AI models hosted on community repositories [1]ReversingLabs, “ReversingLabs Identifies Novel ML Malware Hosted on Leading Hugging Face AI Model Platform,” reversinglabs.com. Because ML artifacts bypass traditional code reviews, they expose development pipelines to silent compromise. Many organizations now scan binaries and containers at every commit, integrating malware analytics into continuous integration flows. Solutions such as Spectra Assure automate binary lineage tracing, highlighting suspicious modifications before release. The shift elevates malware inspection from an incident-response task to an integral part of secure software supply-chain governance.

Rapid Adoption of Cloud-Native Workloads Requiring Sandbox-Free Analysis

Containerized micro-services spin up and down in seconds, making legacy sandbox isolation impractical. Real-time telemetry embedded at the orchestrator layer now inspects process behavior without quarantining samples[2]Palo Alto Networks, “What is Container Security,” paloaltonetworks.com. Cloud hyperscalers provide elastic compute fences that detonate suspected objects in parallel, eliminating infrastructure bottlenecks. Amazon Web Services’ purpose-built analysis environments isolate malware while maintaining strict egress controls, letting security teams triage thousands of artifacts per hour. These developments favor vendors that can blend endpoint telemetry, network capture, and cloud workload protection into unified dashboards.

Mandatory Breach-Reporting Windows in New Cyber-Regulations

CISA’s 72-hour reporting rule for critical infrastructure and the SEC’s four-business-day disclosure requirement for public issuers force security teams to produce forensically sound findings on compressed timelines. Automated classification that tags malware family, entry vector, and business impact speeds compliance drafts that once took weeks. Demand has surged for platforms that auto-generate regulator-ready narratives alongside indicators of compromise, reducing legal exposure. These mandates also raise the premium on accurate attribution because firms must state whether incidents represent isolated events or coordinated campaigns.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic shortage of reverse-engineering talent | -2.8% | Global, acute in North America and Europe | Long term (≥ 4 years) |

| Persistent false-positive rates in automated dynamic analysis | -1.9% | Global, all deployment modes | Medium term (2-4 years) |

| Encryption-at-rest mandates limiting sample sharing across borders | -1.4% | Global, varied compliance | Medium term (2-4 years) |

| Volatility of open-source malware‐analysis frameworks undermining ROI | -0.9% | Global, greater impact on SMEs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Chronic Shortage of Reverse-Engineering Talent

The global cybersecurity workforce gap exceeds 4 million professionals, and malware reverse engineering ranks among the hardest roles to fill [3]ISC2, “Cybersecurity Workforce Study,” isc2.org. Healthcare organizations report an 89% vacancy rate despite premium pay, slowing incident triage and prolonging dwell time. Vendors counter by embedding explainable AI that annotates disassembly listings, but complex kernel-level threats still demand human review. The talent crunch incentivizes acquisitions of niche analysis startups by larger platforms eager to internalize scarce expertise. While automation helps, most enterprises acknowledge that erasing the skills deficit will take years.

Persistent False-Positive Rates in Automated Dynamic Analysis

Behavioral sandboxes sometimes flag legitimate high-performance applications, particularly in capital-markets and research computing, as malicious due to aggressive memory or network usage. Excess alerts erode analyst confidence and inflate response workloads. To improve precision, vendors now layer static code similarity checks and contextual threat intelligence atop behavioral outputs. Active-learning models like PromptSAM+ retrain on mislabeled samples to suppress false alarms while retaining high recall. Even with these advances, enterprises adopt multi-engine correlation to validate verdicts before triggering containment actions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Lead Platform Consolidation

Solutions held 67.4% of the malware analysis market in 2024 as enterprises favored turnkey platforms that combine detonation, ML scoring, and workflow orchestration. Services remain essential for tailored threat hunting and incident forensics, but cannot match the scalability of embedded engines. Platform providers now embed advanced triage that surfaces root cause and recommended response within minutes, shrinking mean-time-to-detect. Consolidation continues as extended detection and response suites absorb stand-alone sandboxes to cut integration overhead.

Revenue for solutions is projected to climb at a 27.3% CAGR to 2030. Competitive emphasis has shifted from raw sample throughput toward contextual enrichment and automated compliance reporting, a change that reflects board-level scrutiny of security spending. The transition also demonstrates the widening gulf between feature-rich platforms and lightweight utilities, driving smaller vendors to seek acquisition exits.

By Deployment Mode: Cloud Dominates Scalability Requirements

Cloud options commanded 57.0% share in 2024 and are forecast to post the highest 27.5% CAGR through 2030, propelled by elastic compute and pay-per-use economics. Large datasets can be processed in parallel across serverless frameworks, shortening analysis cycles from hours to minutes. Cloud models also receive continuous ML model updates, ensuring current verdict logic without local patching.

On-premises deployments persist among heavily regulated sectors that require strict data residency, yet many of these organizations adopt hybrid designs that keep sensitive artifacts on site while outsourcing bulk pattern matching. Providers differentiate by offering private-cloud enclaves with sovereign hosting guarantees, balancing compliance needs with the performance benefits of distributed compute.

By Organization Size: SMEs Drive Democratization

Large enterprises contributed 71.2% of 2024 revenue, reflecting deep budgets and compliance obligations. However, SMEs will experience a 28.5% CAGR to 2030 as subscription pricing and managed security services lower adoption barriers. The malware analysis market share held by SMEs is expected to rise at a significant rate by 2030 as cloud portals provide wizard-driven triage and pre-built playbooks.

Managed service providers bundle monitoring, sandboxing, and incident response into one-click offerings, enabling smaller firms to meet insurance underwriting criteria. Partnerships like SuperOps-Malwarebytes deliver integrated dashboards that present detection context alongside IT operations metrics, narrowing the expertise gap [4]Malwarebytes, “SuperOps and Malwarebytes Partner to Transform Cybersecurity,” malwarebytes.com.

By Industry Vertical: Healthcare Accelerates Beyond BFSI

BFSI held 27.2% of revenue in 2024 due to high-value data and stringent oversight, yet healthcare will expand at a 29.1% CAGR as ransomware targets patient records and connected devices. The Department of Health and Human Services' cybersecurity goals now call for continuous malware inspection across electronic health record servers and imaging endpoints, driving accelerated procurement.

Manufacturing, retail, and telecom also intensify spending as operational technology convergence and e-commerce growth widen attack surfaces. Government and defense agencies maintain elevated investments to counter state-sponsored espionage, demanding advanced reverse-engineering features and air-gap compatibility. Vertical-specific rule packs and compliance templates have become critical differentiators for vendors courting regulated industries.

By Analysis Technique: Hybrid ML-Assisted Analysis Transforms Detection

Static inspection accounted for 47.2% revenue in 2024, yet hybrid techniques that blend signature checks with ML-driven behavior scoring will register the swiftest 29.8% CAGR. Hybrid engines mitigate blind spots inherent in single-method approaches, raising accuracy without unacceptable false-positive inflation. The malware analysis market size for hybrid methods is projected to surpass USD 25 billion by 2030, underscoring the shift toward learning algorithms.

Vendors refine model training pipelines with transfer-learning and active-learning frameworks to ingest new families quickly. Sandbox telemetry now feeds into continuous retraining loops, producing adaptive heuristics that track evolving obfuscation trends. While model explainability remains a research topic, early implementations embed human-readable justifications into analyst consoles to foster trust.

Geography Analysis

North America generated 35.1% of global revenue in 2024 on the back of mature cybersecurity investment, federal stimulus programs, and a dense ecosystem of solution providers. Funding from the State and Local Cybersecurity Grant Program and Infrastructure Investment and Jobs Act channels capital into malware analytics tools for public entities [5]CISA, “State, Local, Tribal, and Territorial Cyber Grant Program,” cisa.gov. Mandatory incident disclosure has further entrenched automated triage platforms across critical infrastructure, financial services, and healthcare.

Asia-Pacific is the fastest-growing territory at 28.5% CAGR, propelled by rapid cloud adoption and government-backed digital-economy blueprints. Nations such as Singapore and Japan offer co-funding incentives for security controls, enabling local enterprises to deploy advanced analytics without prohibitive capital outlay. Regional managed security providers also bundle threat intelligence and malware analytics into scalable packages suited to small businesses, accelerating democratization.

Europe maintains steady double-digit growth as the Network and Information Security Directive and GDPR enforce prompt breach notification and data residency. Sovereign cloud frameworks stimulate hybrid deployments that keep sensitive artifacts within national borders while leveraging ML engines from pan-European security clouds. Cross-border initiatives through Europol’s European Cybercrime Centre improve sharing of malware indicators, increasing demand for analysis platforms capable of publishing standardized threat intelligence feeds.

Competitive Landscape

The malware analysis market features a moderately fragmented mix of legacy firewall vendors, endpoint security specialists, and emerging AI-native disruptors. Established players such as Cisco, Palo Alto Networks, and CrowdStrike integrate behavioral detonation engines into broader extended detection and response suites to capture platform revenue synergies. Niche providers like VMRay and ReversingLabs differentiate through specialty capabilities in kernel-mode unpacking or software supply-chain assurance.

Acquisition activity has intensified as platform vendors seek to fill technical gaps and secure scarce reverse-engineering talent. Deep Instinct’s release of DIANNA, an AI-powered analyst co-pilot, underscores the shift toward labor-saving automation. Competitive advantage now hinges on model accuracy, workflow integration, and compliance documentation speed rather than raw sandbox throughput.

White-space opportunities include containerized workload inspection and natural-language threat explanation that reduces analyst onboarding time. Generative AI prototypes promise to draft incident narratives and remediation playbooks, though production readiness varies. Vendors that balance innovation with provable precision are more likely to capture share as buyers scrutinize efficacy claims amid tightening budgets.

Malware Analysis Industry Leaders

Cisco Systems Inc.

Palo Alto Networks Inc.

Google LLC (Alphabet, Inc.)

Broadcom Inc.

CrowdStrike Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: ThreatDown endpoint security from Malwarebytes integrated into SuperOps’ IT management suite to enhance MSP visibility.

- March 2025: CISA published a Malware Analysis Report on the RESURGE variant, including detection signatures for critical infrastructure defenders.

- February 2025: ReversingLabs uncovered the nullifAI technique that weaponizes AI model repositories, illustrating new supply-chain risks.

- November 2024: ReversingLabs introduced Spectra Assure, unifying binary analysis with software supply-chain vetting.

Global Malware Analysis Market Report Scope

| Solutions |

| Services |

| On-premises |

| Cloud |

| Large Enterprises |

| Small and Medium-Sized Enterprises (SMEs) |

| BFSI |

| Government and Defense |

| Healthcare and Life Sciences |

| IT and Telecom |

| Retail and e-Commerce |

| Manufacturing |

| Static (Code) Analysis |

| Dynamic (Behavioral) Analysis |

| Hybrid / ML-assisted Analysis |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Component | Solutions | ||

| Services | |||

| By Deployment Mode | On-premises | ||

| Cloud | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium-Sized Enterprises (SMEs) | |||

| By Industry Vertical | BFSI | ||

| Government and Defense | |||

| Healthcare and Life Sciences | |||

| IT and Telecom | |||

| Retail and e-Commerce | |||

| Manufacturing | |||

| By Analysis Technique | Static (Code) Analysis | ||

| Dynamic (Behavioral) Analysis | |||

| Hybrid / ML-assisted Analysis | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the malware analysis market by 2030?

The market is forecast to reach USD 53.05 billion by 2030, growing at a 26.97% CAGR.

Which deployment model is expanding fastest?

Cloud deployment is set to grow at 27.5% CAGR, reflecting its 57.0% share and elasticity advantages.

Why is healthcare the fastest-growing vertical?

Ransomware targeting patient records and regulatory pressure drive healthcare’s 29.1% CAGR in malware analytics investment.

How are supply-chain attacks influencing purchasing behavior?

Organizations now embed binary and ML-model scans into DevSecOps pipelines, boosting demand for automated analysis platforms.

Page last updated on: