RegTech For Cybersecurity Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

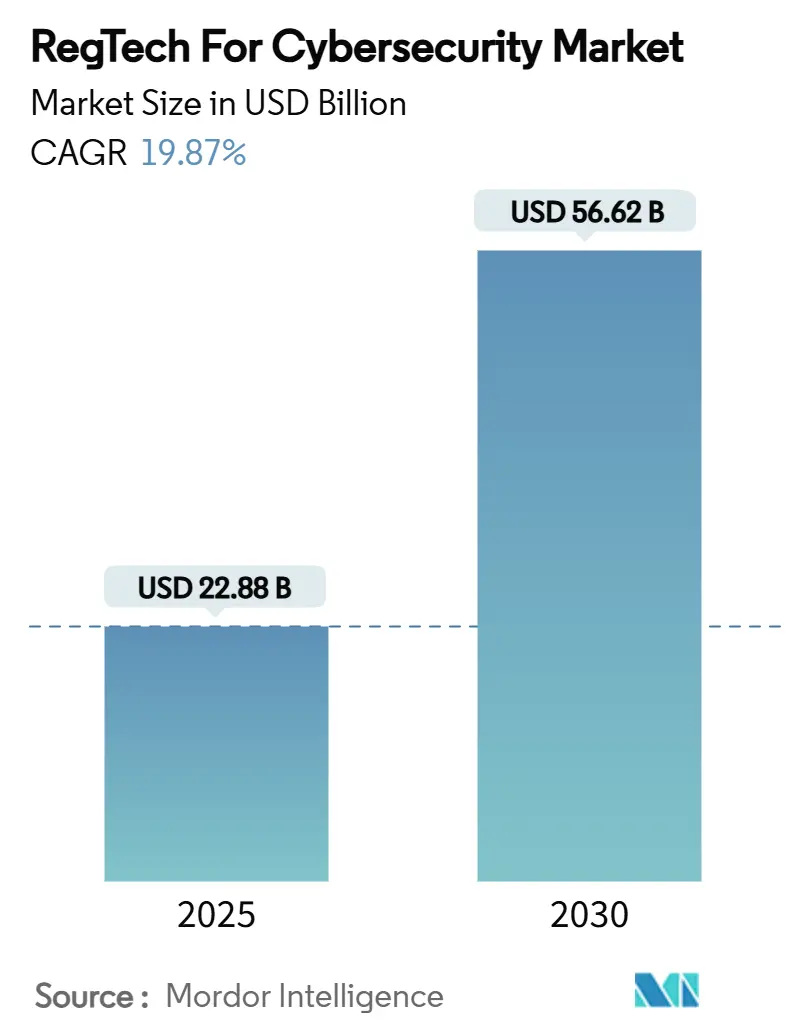

| Market Size (2025) | USD 22.88 Billion |

| Market Size (2030) | USD 56.62 Billion |

| Growth Rate (2025 - 2030) | 19.87% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

RegTech For Cybersecurity Market Analysis by Mordor Intelligence

The RegTech for Cybersecurity market size stands at USD 22.88 billion in 2025 and is forecast to reach USD 56.62 billion by 2030, registering a 19.87% CAGR. Converging cyber-resilience mandates and traditional compliance workflows are giving rise to integrated platforms able to orchestrate regulatory reporting, operational risk, and threat-intelligence feeds within a single pane of glass. Vendor differentiation increasingly hinges on AI-driven regulatory interpretation engines that slash policy-mapping time and support real-time control monitoring. North America retains leadership owing to mature supervisory regimes, while Asia-Pacific accelerates on the back of digital-first finance reforms that require scalable, cloud-native governance tooling. Managed services adoption is climbing as firms look to externalize specialist skills and contain the rising opportunity cost of scarce cyber-compliance talent. Hybrid cloud architectures are gathering pace because they reconcile strict data-residency statutes with the elasticity of public-cloud analytics.

Key Report Takeaways

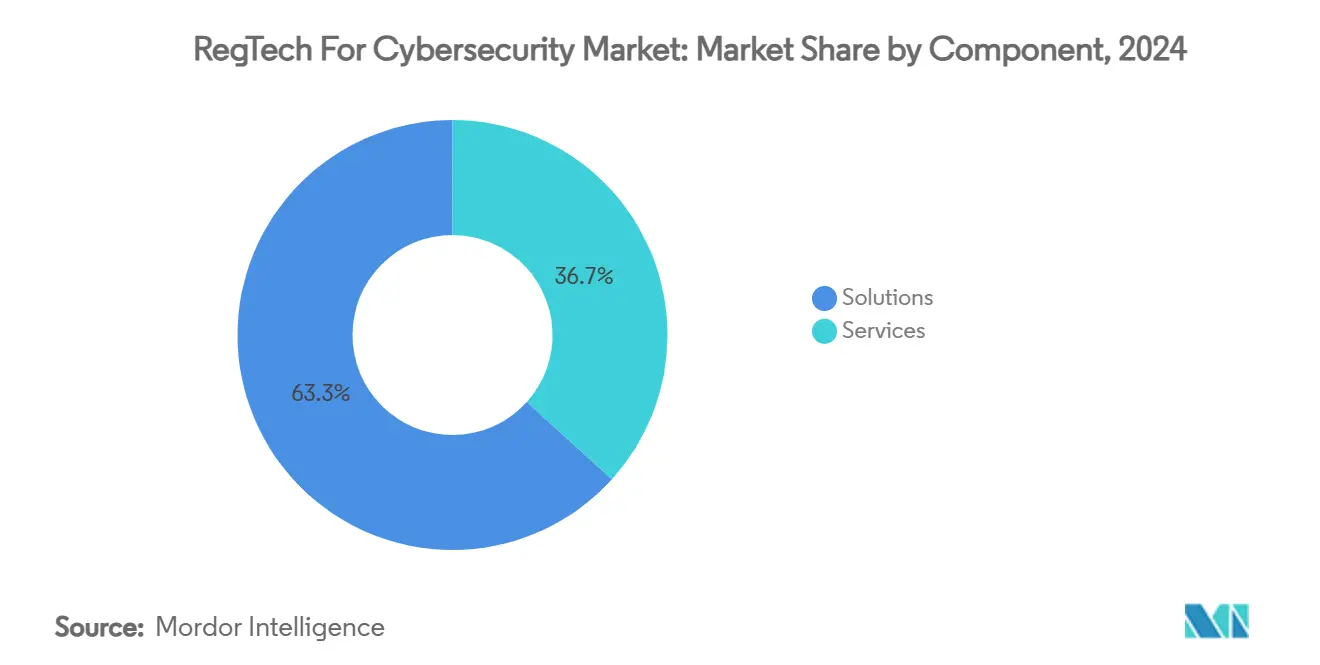

- By component, solutions captured 63.3% of the RegTech for cybersecurity market share in 2024, whereas services are projected to expand at a 23.2% CAGR through 2030.

- By deployment model, the cloud segment held 72.4% share of the RegTech for cybersecurity market size in 2024, while hybrid is advancing at a 24.5% CAGR to 2030.

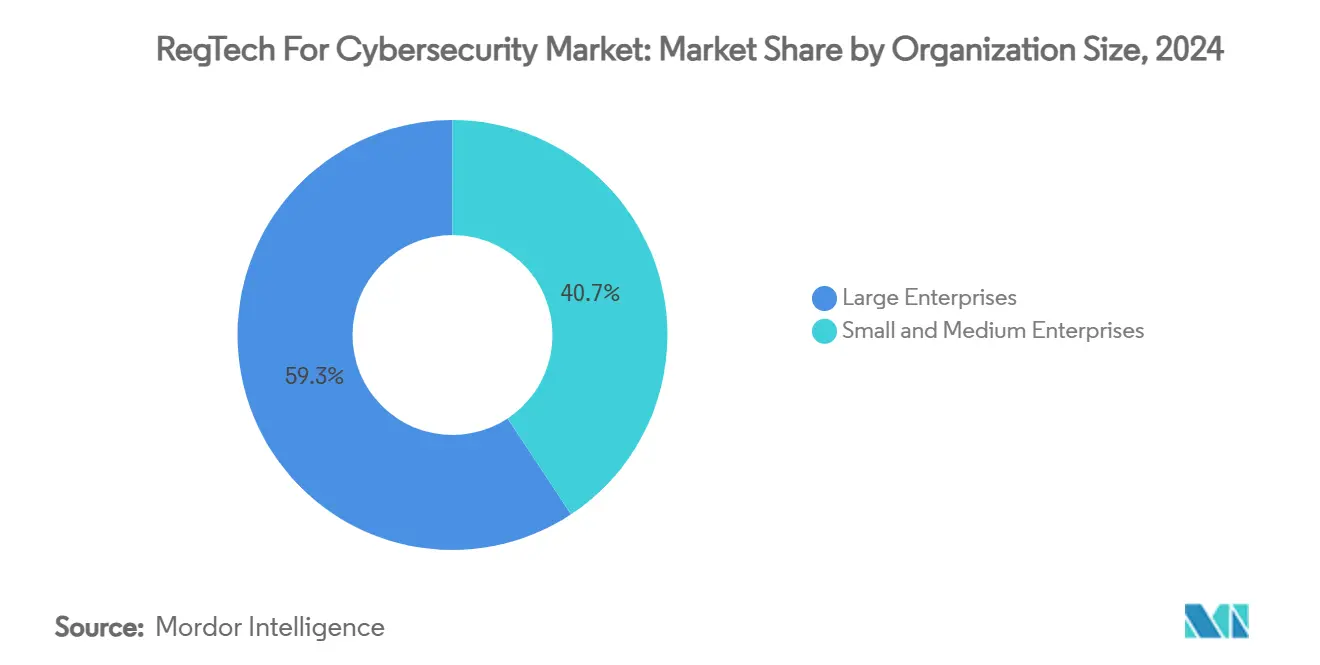

- By organisation size, large enterprises accounted for a 59.3% share of the RegTech for cybersecurity market size in 2024, and SMEs are growing at a 21.3% CAGR through 2030.

- By end-use industry, BFSI led with 41.2% revenue share in 2024; healthcare and life sciences are forecast to grow at a 24.1% CAGR to 2030.

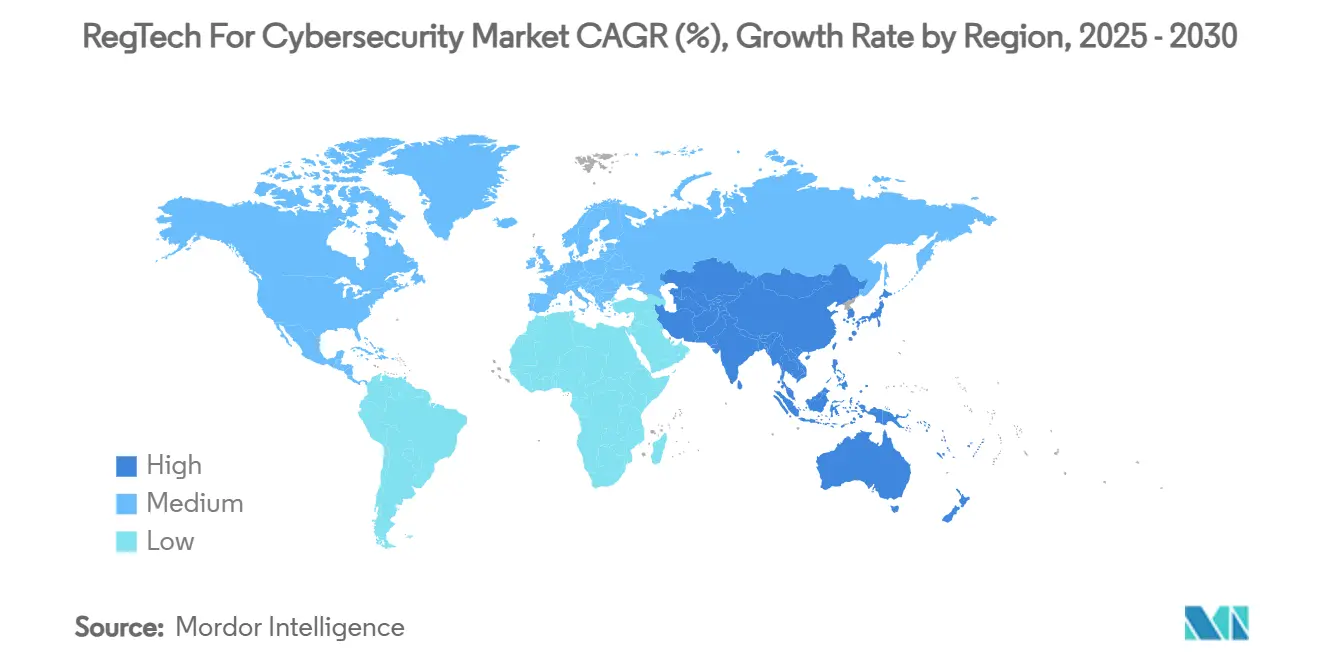

- By geography, North America commanded 38.2% of the RegTech for cybersecurity market share in 2024, whereas Asia-Pacific posts the highest projected CAGR at 23.4% to 2030.

Global RegTech For Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing volume and complexity of cyber-oriented regulations (e.g., DORA, NIS 2) | +4.2% | Global, with concentrated impact in the EU and spillover to North America | Medium term (2-4 years) |

| Escalating cost of non-compliance fines spurring proactive investment | +3.8% | Global, with the highest impact in North America and the EU | Short term (≤ 2 years) |

| Rapid digitalization of BFSI and fintech ecosystems | +3.5% | Asia-Pacific core, with spillover to MEA and Latin America | Medium term (2-4 years) |

| Cloud-native RegTech platforms are lowering the total cost of ownership | +2.9% | Global, with early adoption in North America and the EU | Long term (≥ 4 years) |

| Integration of AI-driven continuous control monitoring (under-reported) | +2.7% | North America and the EU, expanding to the Asia-Pacific | Medium term (2-4 years) |

| Tokenization and DeFi adoption are creating novel compliance gaps (under-reported) | +1.4% | Global, with regulatory focus in the EU and emerging frameworks in the US | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Volume and Complexity of Cyber-Oriented Regulations

Since January 2025, the Digital Operational Resilience Act (DORA) has obliged more than 20,000 European financial entities to maintain ICT-risk registers, classify incidents, and conduct threat-led penetration tests, forcing demand for orchestration layers that handle those five pillars concurrently.[1]Central Bank of Ireland, “Digital Operational Resilience Act (DORA),” centralbank.ie Multinationals must also align with NIS 2, which extends similar duties to energy, transport, and health infrastructures, adding another compliance surface that unified platforms can address. Automated incident-classification engines capable of distinguishing major from minor events within set timelines are becoming baseline buyer requirements. Vendors embedding out-of-the-box cross-regulation mapping logic save customers months in policy harmonization work. As lawmakers add AI-specific bills like the EU AI Act, the regulatory mosaic grows denser, reinforcing purchasing preference for holistic RegTech for cybersecurity market platforms.

Escalating Cost of Non-Compliance Fines Spurring Proactive Investment

DORA breaches can trigger penalties up to 1% of daily worldwide turnover, reframing compliance from discretionary spend to an existential hedge. In 2024, large US banks incurred multi-million-dollar sanctions for incomplete communication surveillance, catalyzing urgent upgrades to cloud-native monitoring suites that capture voice, chat, and video feeds in real time. Continuous controls assurance is supplanting point-in-time audits because regulators now expect live dashboards over monthly attestation files. Executives quantify ROI by comparing annual RegTech subscription fees with headline-grabbing enforcement actions that run into hundreds of millions. Consequently, chief risk officers carve out dedicated RegTech for cybersecurity market budgets immune from wider IT-cost rationalisation cycles.

Rapid Digitalization of BFSI and Fintech Ecosystems

Open-banking APIs, embedded finance, and real-time payments expose institutions to cascading third-party risk that legacy GRC suites cannot visualise end-to-end. DORA names critical ICT providers explicitly, compelling banks to evidence oversight of hyperscalers and SaaS vendors across data-flow chains. Asia-Pacific neobanks release new digital products weekly, stretching manual compliance workflows past the breaking point. RegTech dashboards now ingest telemetry from Kubernetes clusters and blockchain nodes, delivering risk heat-maps that cover both on-premise cores and cloud micro-services. In fintech hubs such as Singapore and Bengaluru, automated licence-renewal reminders and cross-border reporting templates are prized features, positioning the RegTech for the cybersecurity market as a growth lever rather than a defensive purchase.

Cloud-Native RegTech Platforms Lowering Total Cost of Ownership

Pay-as-you-go compliance-as-a-service cuts capex and accelerates deployment from quarters to weeks. Multi-tenant clouds distribute the cost of rule-set updates across hundreds of tenants, ensuring real-time legislative coverage at marginal incremental cost.[2]Number Analytics, “Regulatory Compliance Tech Trends,” numberanalytics.com Built-in AI engines parse regulatory gazettes nightly and surface delta alerts, eliminating manual tracking spreadsheets. SMEs without in-house security architects can now consume bank-grade analytics for a two-digit monthly fee, driving 21.3% CAGR SME uptake. Integrations via RESTful APIs enable bi-directional data exchange with HR, IAM, and SIEM stacks, cementing the RegTech for cybersecurity market platform at the heart of governance architectures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented, region-specific regulatory requirements raise integration costs | -2.8% | Global, with the highest complexity in the EU and emerging markets | Medium term (2-4 years) |

| Shortage of specialised cyber-compliance talent | -2.1% | Global, with acute shortages in North America and the EU | Long term (≥ 4 years) |

| Legacy IT environments are limiting solution interoperability (under-reported) | -1.9% | Global, with the highest impact in established financial markets | Long term (≥ 4 years) |

| Increasing regulator scrutiny of AI models' "explainability" (under-reported) | -1.6% | North America and the EU, with emerging requirements in the Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented, Region-Specific Regulatory Requirements Raising Integration Costs

National supervisors interpret DORA through diverging technical standards, forcing cross-border banks to juggle multiple compliance taxonomies or stand-up translation layers that inflate project budgets. Asia-Pacific fragmentation is sharper: Australian prudential templates differ materially from Singaporean notices, while India rolls out sector-specific data-localisation clauses. Vendors have to maintain geo-fenced data lakes and rules engines, complicating roadmap prioritisation. SMEs shoulder a disproportionate administrative toll, and EU studies indicate that digital-transition costs can erode their competitiveness by up to several basis points of revenue. As a result, procurement cycles elongate, and total contract values plateau in multi-jurisdiction deals, dampening overall RegTech for cybersecurity market velocity.

Shortage of Specialized Cyber-Compliance Talent

Global demand for “compliance super soldiers” who blend law, cybersecurity, and data-science skills outstrips supply by a factor of five, according to 2025 industry surveys. Institutions scramble to pay 30% premiums for certified DORA strategists while internal upskilling pipelines take years to mature. Talent scarcity delays large-scale platform rollouts and inflates managed-service pricing. The gap is most pronounced in explainable-AI governance, where seasoned practitioners can translate model outputs into regulator-friendly artefacts. In effect, the resource constraint tempers near-term conversion of proof-of-concepts into production deployments across the RegTech for cybersecurity market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platform Dominance Accompanied by Services Upshift

Solutions generated the bulk of RegTech for the cybersecurity market revenue, delivering a 63.3% share in 2024 as enterprises opted for unified suites that house policy repositories, threat-intel feeds, and regulatory mapping modules in one environment.[3]MetricStream, “Operational Resilience, Cyber Risk and AI,” metricstream.com The governance, risk, and compliance sub-category remains core, but specialist identity verification and real-time reporting engines post double-digit gains as zero-trust frameworks and near-time filing obligations proliferate. Investors channel funds toward AI-native vendors whose language models trim control-testing time by up to 45%, crystallising a premium valuation tier within the RegTech for cybersecurity market.

Managed services expand fastest at 23.2% CAGR, signalling an operational pivot from “install-and-forget” software licences to outsourced, continuous compliance. Offerings cover 24/7 controls monitoring, regulatory horizon scanning, and remediation advisory, relieving internal teams threatened by resource burnout. Banks increasingly embed service-level agreements that guarantee incident-response times under four hours, turning vendors into quasi-regulatory partners. The convergence of SaaS and managed services transforms the RegTech for cybersecurity market size trajectory by broadening addressable budgets previously classified as labour spend.

By Deployment Mode: Cloud Holds Sway while Hybrid Scales Quickly

Pure cloud implementations captured 72.4% share of the RegTech for cybersecurity market size in 2024, favoured for elastic compute and instant-update semantics that align with fluid rulebooks. Multi-tenant architectures enable regulators to distribute templated questionnaires directly into bank dashboards, compressing supervisory cycles. Total cost-of-ownership studies show up to 40% savings versus on-premises stacks once database licensing, patching, and hardware refreshes are factored in.

Hybrid frameworks—on-premises data vaults fused with cloud analytics—record a 24.5% CAGR as financial institutions reconcile GDPR, sectoral national security directives, and the advent of the EU AI Act. Tier-1 banks keep personally identifiable information within national borders yet export anonymised logs to AI engines hosted on hyperscaler GPUs for anomaly detection. Vendors respond with node-agnostic orchestration layers, underscoring the RegTech for cybersecurity market trend: architecture optionality is now a competitive must-have.

By Organization Size: Enterprise Weight Meets SME Momentum

Large corporations, commanding 59.3% of adoption in 2024, integrate RegTech nodes into vast ERP and IAM estates, unlocking synergies through auto-segmented audit trails and risk dashboards viewable at the board level. Their procurement power seeds custom modules for advanced explainability, resulting in feature spill-over that ultimately benefits the wider RegTech for cybersecurity market.

SMEs are expected to outpace with a 21.3% CAGR as platform subscription tiers start at sub-five-figure annual fees, enabling mid-market lenders and regional hospitals to meet the same statutory bars as global peers. Low-code interfaces shrink deployment windows; pre-configured workflow bundles for DORA or HIPAA reduce consulting overheads. Investor-backed fintechs treat frictionless compliance as a strategic differentiator during licence applications, further fuelling SME uptake.

By End-Use Industry: BFSI Core, Healthcare Surges

Financial services preserved a 41.2% share of the RegTech for cybersecurity market revenue in 2024, owing to multi-layered oversight spanning anti-money laundering, resolution planning, and operational resilience mandates. Banks leverage AI-powered policy engines that parse thousands of pages of supervisory releases weekly, transforming change management from manual triage into automated impact matrices.

Healthcare and life sciences blaze ahead at 24.1% CAGR through 2030 as upcoming HIPAA Security Rule amendments enforce multi-factor authentication and encryption for all electronic health information; first-year compliance spend is pegged at USD 9 billion. Hospitals seek cloud-native vaults with evidence-grade logging to deter ransomware and meet breach-notification windows, cementing the segment’s role as the RegTech for cybersecurity market growth engine.

Geography Analysis

North America commands a 38.2% share of the RegTech for cybersecurity market revenue in 2024, powered by stringent enforcement and abundant venture capital for RegTech scale-ups. US banks channel budgets into AI-governance modules after the Bipartisan AI Task Force outlined principles for model oversight, data lineage, and consumer safeguards.[4]National Law Review, “AI Regulation in Financial Services,” natlawreview.com Canada enforces operational resilience testing akin to DORA, keeping local demand buoyant. The region hosts established cloud regions that satisfy sovereignty clauses, accelerating rollouts.

Asia-Pacific logs the fastest 23.4% CAGR, underpinned by open-banking mandates, rapid fintech proliferation, and state-sponsored digital-identity rails. Chinese regulators consolidate scattered circulars into unified compliance handbooks, sparking bulk procurement of real-time monitoring tools by state-owned banks. Japan refines risk-governance standards for crowdfunding and algorithmic lending, incentivising platforms with multilingual regulatory ontologies. India’s central bank instructs non-bank lenders to ensure board-level cyber risk accountability, driving adoption of automated board reporting features. Southeast Asian markets embrace digital-by-default supervision, fuelling demand for plug-and-play RegTech for cybersecurity market dashboards.

Europe sustains steady growth as DORA’s phased obligations enter force. German, French, and UK incumbents seek modules that reconcile DORA, GDPR, and the soon-to-be-finalised AI Act within the same control library. Nordic banks pioneer cross-sector information-sharing utilities hosted on consortium-run clouds. Meanwhile, the Middle East and Africa mature gradually; Dubai’s Virtual Assets Regulatory Authority codifies crypto-asset reporting, while South African lenders pilot automated conduct-risk dashboards. These differing tempos underpin a multipolar expansion pattern across the RegTech for cybersecurity market.

Competitive Landscape

The market remains moderately fragmented. Legacy GRC heavyweights contend with AI-native entrants that bake generative language models into regulatory change-management workflows. Kroll’s 2024 purchase of Resolver exemplifies a strategy to fuse traditional risk analytics with cloud orchestration, adding up-sell fuel across its incident response customer base. Similar bolt-ons see identity-verification vendors acquiring policy-management start-ups to present unified suites.

Product roadmaps converge around three pillars: explainable AI, cross-regulation mapping at import, and low-code workflow builders for compliance officers without coding skills. Competitive intensity mounts in healthcare, where specialty providers offer HIPAA-focused encryption key management with pre-integrated audit evidence packs. DeFi surveillance emerges as a white space; policy labs at Stanford cite supervisory interest in on-chain analytics that can plug into existing reg-reporting schemas.

Incumbents defend their share through deep regulatory domain expertise, brand trust, and ISO-certified hosting. Challengers woo buyers with month-to-month contracts and micro-service pricing. As the top five vendors’ combined revenue sits below 40%, the RegTech for cybersecurity market scores near-mid fragmentation but shows a trend toward platform consolidation driven by M&A and API interoperability pushes.

RegTech For Cybersecurity Industry Leaders

OneTrust LLC

MetricStream Inc.

Diligent Corporation

RSA Security LLC

LogicGate Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Archer acquired Compliance.ai to embed AI-powered regulatory update parsing into its GRC suite.

- January 2025: US Treasury finalized DeFi 1099-DA reporting rules, granting phased relief through 2028.

- December 2024: Kroll closed the acquisition of Resolver to build an integrated risk-intelligence platform.

- December 2024: US House Task Force published guidance on AI regulation within financial services.

Global RegTech For Cybersecurity Market Report Scope

| Solutions | Governance, Risk and Compliance (GRC) Platforms |

| Identity Verification and Management | |

| Regulatory Reporting Automation | |

| Data Protection and Privacy Management | |

| Risk Analytics and Scorecards | |

| Services | Professional Services |

| Managed Services |

| Cloud |

| On-premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| BFSI |

| Healthcare and Life Sciences |

| Telecom and IT |

| Government and Public Sector |

| Energy and Utilities |

| Manufacturing |

| Retail and E-commerce |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Solutions | Governance, Risk and Compliance (GRC) Platforms | |

| Identity Verification and Management | |||

| Regulatory Reporting Automation | |||

| Data Protection and Privacy Management | |||

| Risk Analytics and Scorecards | |||

| Services | Professional Services | ||

| Managed Services | |||

| By Deployment Mode | Cloud | ||

| On-premises | |||

| Hybrid | |||

| By Organisation Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By End-Use Industry | BFSI | ||

| Healthcare and Life Sciences | |||

| Telecom and IT | |||

| Government and Public Sector | |||

| Energy and Utilities | |||

| Manufacturing | |||

| Retail and E-commerce | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the growth outlook for the RegTech for cybersecurity market to 2030?

Revenue is projected to rise from USD 22.88 billion in 2025 to USD 56.62 billion by 2030, reflecting a 19.87% CAGR.

Which region will expand fastest through 2030?

Asia-Pacific is forecast to post a 23.4% CAGR, propelled by rapid digitalisation and evolving regulatory frameworks.

Why are hybrid deployments gaining traction?

They balance regulatory data-sovereignty rules with the analytics scalability of cloud, leading to a 24.5% CAGR for hybrid models.

Which end-user vertical is the new growth engine?

Healthcare and life sciences show the highest 24.1% CAGR as updated HIPAA rules drive encryption and MFA adoption.

How are fines influencing buying behaviour?

DORA and similar regimes impose penalties up to 1% of daily global turnover, prompting firms to prioritise proactive RegTech investment.

What differentiates leading vendors?

Explainable AI, cross-regulation mapping, and managed-service layers that guarantee rapid compliance updates set top platforms apart.

Page last updated on: