Clustering Software Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

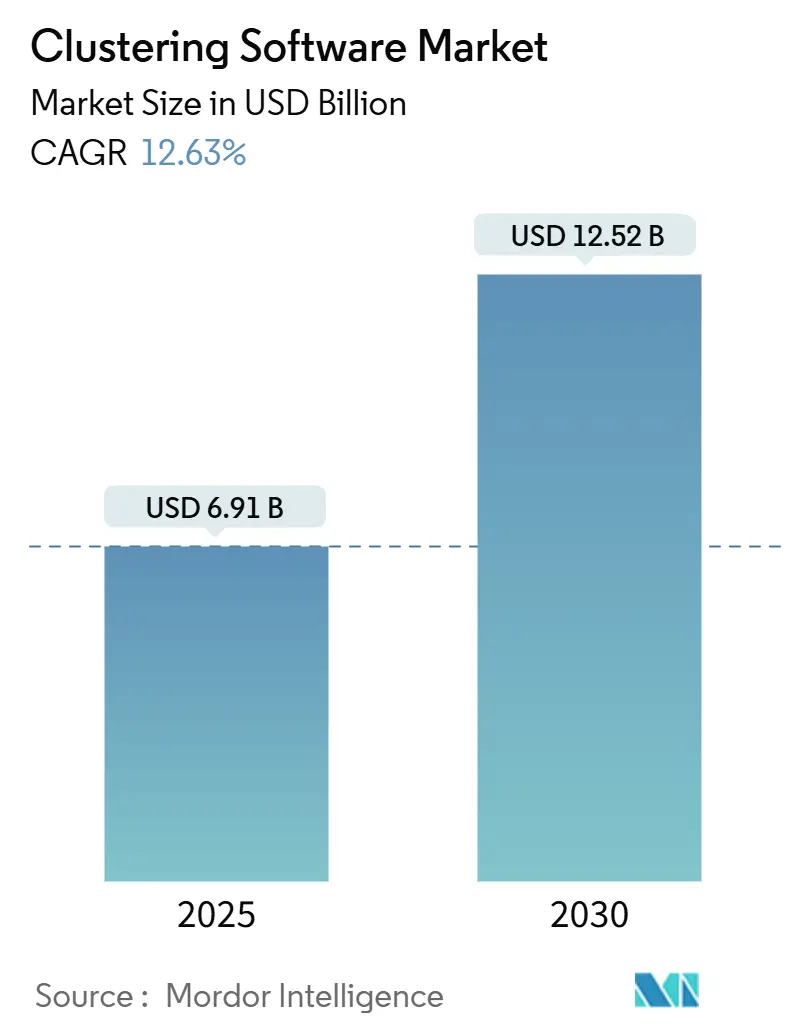

| Market Size (2025) | USD 6.91 Billion |

| Market Size (2030) | USD 12.52 Billion |

| Growth Rate (2025 - 2030) | 12.63% CAGR |

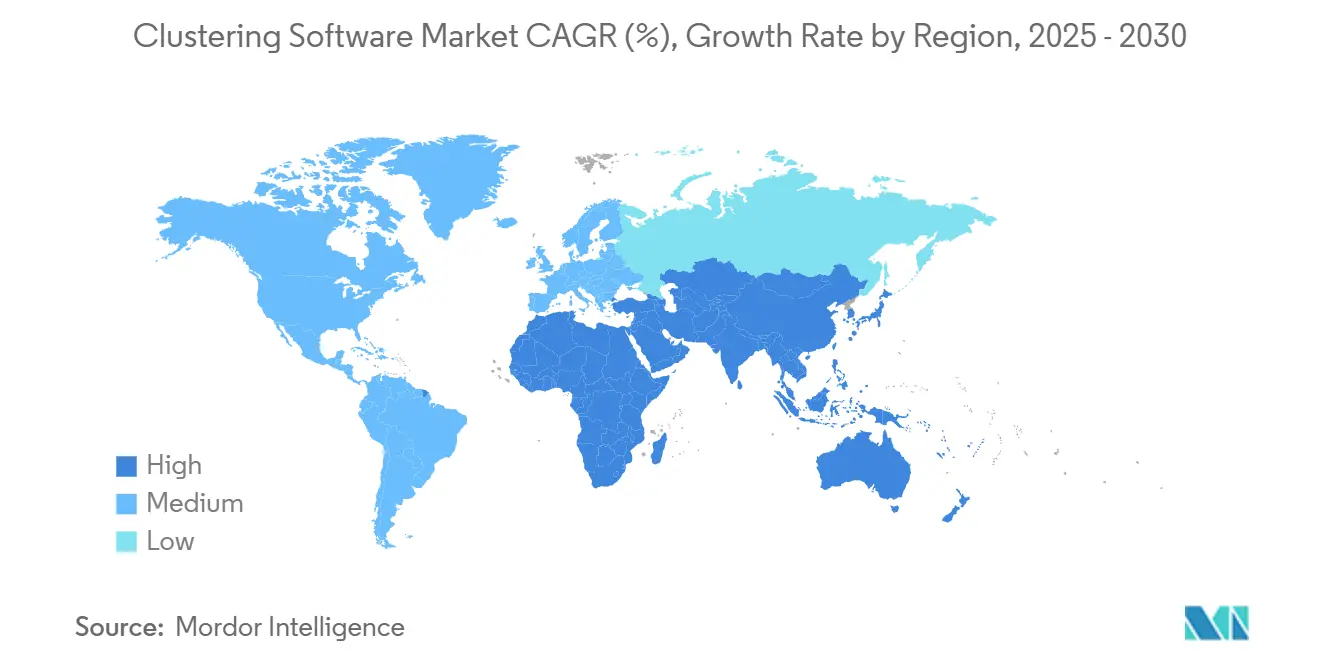

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Clustering Software Market Analysis by Mordor Intelligence

The clustering software market is estimated at USD 6.91 billion in 2025, and is expected to reach USD 12.52 billion by 2030, at a CAGR of 12.63% during the forecast period. The expansion reflects enterprises’ migration to distributed computing architectures that can process the increasing workloads of AI and real-time analytics. Cloud-native transformation, the expansion of edge deployments, and the need for elastic compute clusters are the primary drivers of growth. Vendors that embed orchestration into AI stacks gain an edge as organizations simultaneously modernize legacy applications and accelerate new AI initiatives. Heightened competition is driving suppliers to enhance ecosystem integration, streamline deployment, and strengthen security controls, thereby creating additional momentum in the clustering software market.

Key Report Takeaways

- By deployment, cloud-based solutions captured 61.98% of the clustering software market share in 2024 while expanding at a 13.00% CAGR through 2030.

- By organization size, large enterprises held 69.6% of the clustering software market share in 2024, whereas small and medium enterprises registered the fastest 12.8% CAGR through 2030.

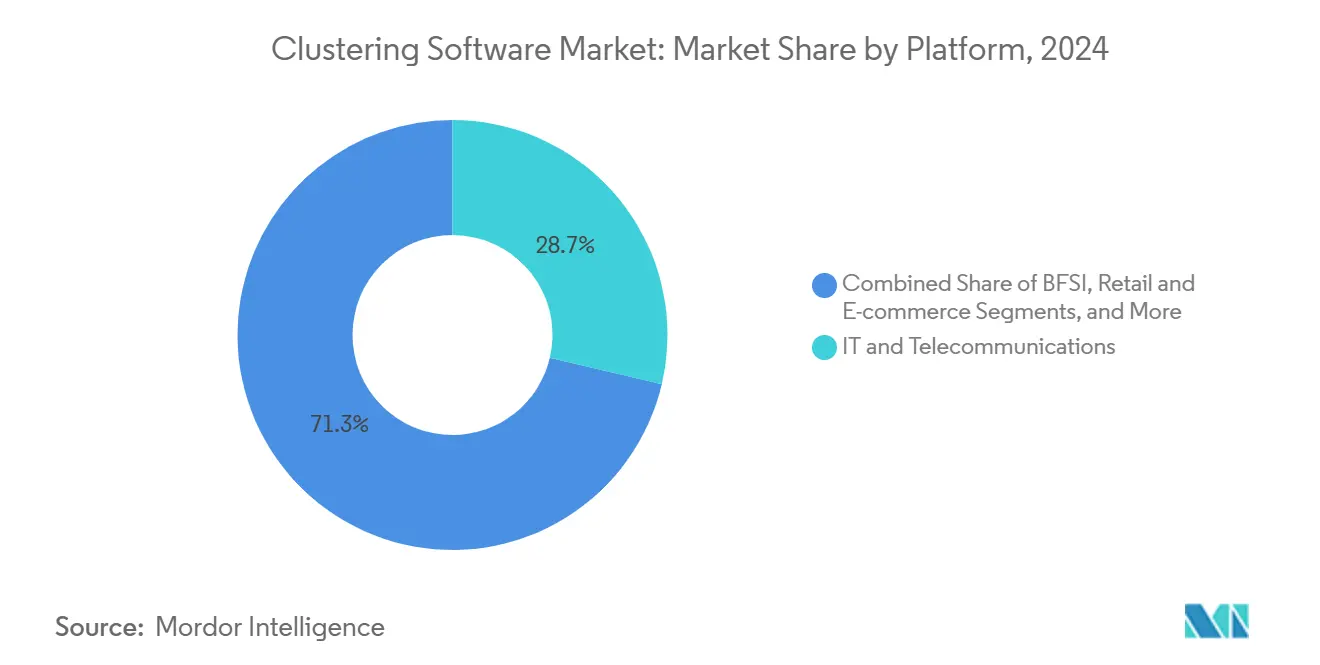

- By end-use industry, IT and Telecommunications commanded a 29.5% revenue share in 2024, and the Healthcare and Life Sciences sector is projected to grow at a 13.6% CAGR through 2030.

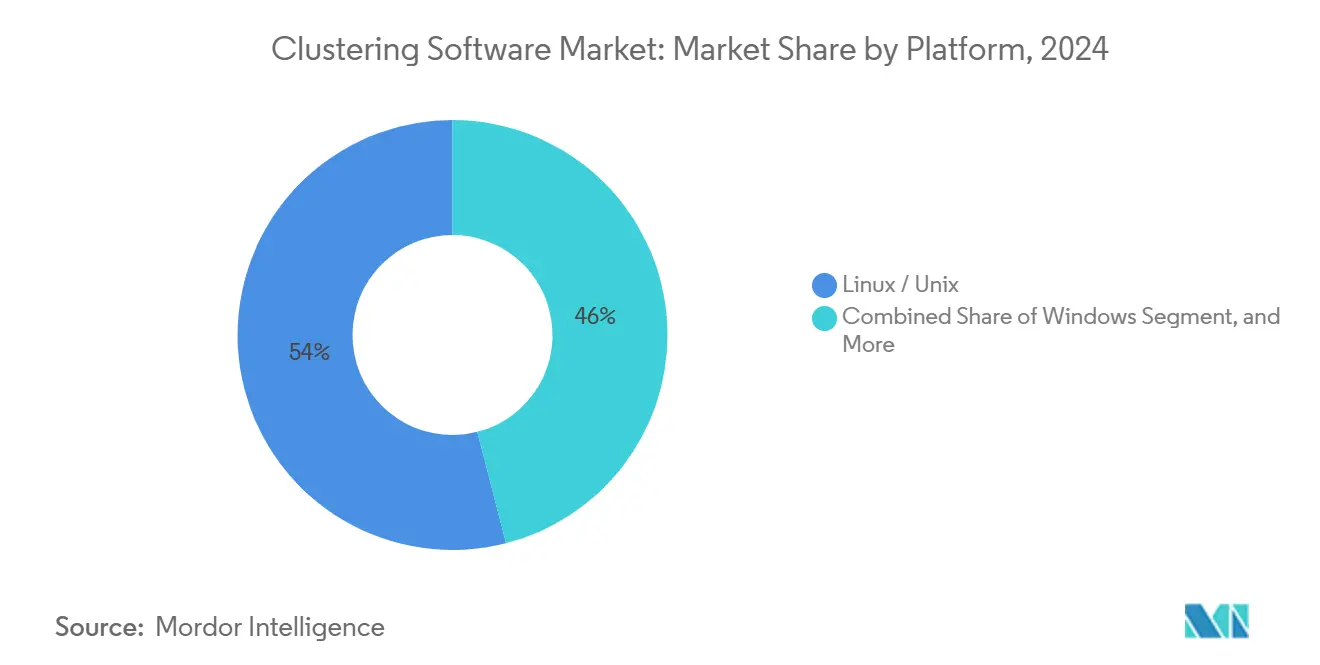

- By platform, Linux / Unix led with 53.15% share in 2024 and is advancing at a 12.9% CAGR.

- By geography, North America maintained a 37.95% share in 2024, while Asia-Pacific is on track for a 13.2% CAGR through 2030.

Global Clustering Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of big data analytics | +2.8% | North America and Asia-Pacific | Medium term (2-4 years) |

| Growth of cloud-native architectures | +3.2% | North America and Europe | Short term (≤ 2 years) |

| High availability and load balancing demand | +2.1% | North America and European Union | Medium term (2-4 years) |

| Expansion of AI / ML workloads | +2.9% | Global with rapid Asia-Pacific uptake | Long term (≥ 4 years) |

| Edge clusters for real-time analytics | +1.8% | Asia-Pacific core shifting to North America | Long term (≥ 4 years) |

| Open-source frameworks and sovereign tech | +1.4% | Europe and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth of Cloud-Native Architectures and Kubernetes Adoption

Kubernetes manages significant production clusters, reflecting its status as the default orchestrator for container workloads. More than 56% of enterprises operate over 10 clusters, multiplying management complexity and fueling demand for robust clustering software. Vendors that streamline multi-cluster governance attract investment, evidenced by Spectro Cloud’s USD 75 million Series C and triple-digit recurring revenue growth. [1]Spectro Cloud, “State of Production Kubernetes 2024,” spectrocloud.com Automated clustering optimization delivers noticeable performance gains, with Databricks users recording up to 10 times faster queries after activating liquid clustering. The combination of performance improvement and cost control reinforces cloud-native clustering as the dominant deployment approach in the clustering software market.

Expansion of AI / ML Workloads Requiring Distributed Training

Large language models generate petabyte-scale datasets that must be processed across GPU clusters. IBM booked USD 6 billion in AI revenue in Q1 2025, a testament to surging infrastructure demand. GPUStack’s open-source manager lets organizations form unified clusters from mixed GPU brands, lowering entry barriers for advanced AI workloads. [2]Databricks, “Automatic Liquid Clustering,” databricks.comHealthcare providers illustrate the benefit: patient clustering for autism therapy optimization has improved clinical outcomes while shortening intervention cycles. As organizations add generative AI workloads, the clustering software market experiences sustained upside from distributed training requirements.

Rising Adoption of Big Data Analytics and Need for Scalable Compute Clusters

Manufacturers rely on edge clusters to process machine data locally for predictive maintenance. Siemens Industrial Edge allows analyses at the source, reducing latency and boosting production efficiency. Financial institutions demonstrate the economic value: Regions Bank improved fraud capture by 95% and saved USD 10 million annually using clustered analytics. These achievements illustrate how scalable clusters transform raw operational data into actionable insights, locking the clustering software market into enterprise modernization roadmaps

Increasing Demand for High Availability and Load Balancing in Enterprise Apps

Users expect significant uptime, pressuring IT teams to deploy automatic failover and load balancing. Arista Networks embedded cluster load balancing in its EOS Smart AI Suite to distribute AI traffic intelligently. United Overseas Bank achieved significant ATM cash availability while reducing restocking trips by 30% using clustered optimization. As mission-critical applications move to microservices, the clustering software market gains momentum from enterprises that must assure continuous service under variable loads.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Global Relevance | Impact Timeline |

|---|---|---|---|

| Deployment and management complexity | -1.9% | Global with SME emphasis | Short term (≤ 2 years) |

| Data security and compliance in multi-tenant | -1.4% | North America and European Union | Medium term (2-4 years) |

| Skills shortage in parallel programming | -1.1% | Worldwide with emerging-market impact | Long term (≥ 4 years) |

| Rising licensing costs for proprietary tools | -0.8% | North America and Europe enterprise | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Complexity of Deploying and Managing Clustered Environments

Although Kubernetes adoption is broad, 76% of users acknowledge that complexity slows projects. [3]Source: Relyance AI, “Data Journeys Platform,” relyance.aiDay-two operations from upgrades to policy enforcement drain engineering capacity and elevate risk. Three-quarters of organizations report operational issues, while 82% struggle to grant developers safe cluster access. Vendors answer with automation and managed services, yet the learning curve continues to restrain the clustering software market, especially for SMEs that lack deep DevOps resources.

Data Security and Compliance Concerns in Multi-Tenant Clusters

Shared clusters increase attack surfaces and complicate data isolation. Axis Bank invested in hybrid models to satisfy regulator expectations while leveraging clustering benefits. Regulatory mandates such as GDPR oblige strict data lineage tracking. Relyance AI’s Data Journeys platform visualizes flows to help enterprises demonstrate compliance. Despite vendor progress, governance gaps still lengthen sales cycles and slow adoption in heavily regulated sectors of the clustering software market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Open-Source Leadership Persists

Linux/Unix platforms represented a 53.15% share because enterprises favor open frameworks that avoid lock-in and minimize licensing costs. Red Hat has doubled annual revenue since its IBM acquisition, validating enterprise-grade open-source monetization.

Windows clusters maintain relevance in environments with extensive Microsoft footprints. However, licensing costs and limited kernel customization moderate uptake. Niche platforms such as BSD serve research institutions seeking distinct security controls. Collectively, platform diversity underscores the centrality of operating-system choice in the clustering software market.

Democratization Accelerates SME Uptake

Large enterprises controlled 69.6% of the revenue in 2024, reflecting deep budgets and seasoned engineering teams that integrate clustering software across their global footprints. Their rollouts span fraud analytics, supply-chain optimization, and omnichannel personalization, anchoring vendor roadmaps.

Small and medium enterprises recorded a 12.8% CAGR, benefiting from pay-as-you-use pricing and simplified orchestration portals. Rank-order clustering delivered 47.64% inventory cost savings for SMEs in a recent study. OECD research shows data-driven decision-making among SMEs reached 72% in 2024. As turnkey offerings proliferate, SMEs will constitute a growing revenue slice of the clustering software market.

Healthcare and Life Sciences Outpace Volume Leaders

IT and Telecommunications accounted for 29.5% of 2024 revenue, thanks to constant network data flows and CSP investment in cloud-native stacks. Telcos deploy clustering software for network function virtualization, fraud detection, and customer experience analytics.

The healthcare and Life Sciences Sectors are projected to advance at a 13.6% CAGR, as real-time patient monitoring and precision medicine rely on fast clustering. GE HealthCare is co-developing generative models with AWS to streamline diagnostics, underscoring the demand for scalable clusters in the domain. Banking, retail, and manufacturing continue to adopt specialized clustering workloads that sustain broad vertical diversity inside the clustering software market.

Hybrid Strategies Redefine Cost Control

Cloud deployments owned a 61.98% stake in the clustering software market in 2024 and delivered a 13% CAGR, highlighting a preference for elastic capacity without capital expenditure. Hybrid is gaining status as the default architecture, balancing cloud burst capabilities with on-premise performance consistency. Nearly 47% of US IT leaders are building generative AI on premises to curb escalating cloud fees. [4]Lenovo Press, “On-Premise vs Cloud: Generative AI Total Cost of Ownership,” lenovopress.lenovo.com/lp2225-on-premise-vs-cloud-generative-ai-total-cost-of-ownershipAs economics evolve, enterprises continuously re-evaluate workload placement and maintain flexible clustering footprints.

On-premise clusters remain essential where data residency laws mandate local processing. Organizations leverage on-premise accelerators for latency-sensitive AI inference, then burst compute-intensive training jobs to hyperscalers. This workload portability sustains diversified revenue streams inside the clustering software market.

Geography Analysis

North America accounted for 37.95% of the clustering software market revenue in 2024, driven by deep cloud adoption and a robust ecosystem of hyperscalers, chipmakers, and software innovators. The United States alone spent heavily on AI infrastructure, as reflected in AMD’s USD 25.8 billion full-year 2024 revenue, with data-center sales up 69% year over year. Canada’s federal digital strategy and Mexico’s manufacturing digitization sustain regional adoptions. Growth is stabilizing as early-mover enterprises shift from expansion to optimization, but AI demand continues to refresh spending.

Asia-Pacific is the fastest-growing region with a 13.2% CAGR, led by China, Japan, and India. NEC’s launch of high-speed generative AI models that incorporate clustering illustrates indigenous innovation. SAP’s 39% cloud revenue acceleration in the Asia-Pacific and Japan region signals a strong appetite among enterprises for scalable computing. ASEAN manufacturers deploy edge clusters to enhance production efficiency, while Australian miners utilize clustering to manage sensor data from remote sites.

Europe shows consistent growth driven by data-sovereignty mandates and industrial automation. German automotive groups install edge clusters on assembly lines, while UK financial institutions use clustered analytics to accelerate customer insights. Russia, despite geopolitical constraints, invests in sovereign-cloud clusters. South America, the Middle East, and Africa remain nascent but accelerate as connectivity improves and public-sector digitization budgets rise. Multinational vendors localize offerings to tap these emerging pockets of the clustering software market.

Competitive Landscape

The clustering software market is moderately fragmented, but consolidation is intensifying. NVIDIA’s USD 700 million purchase of Run: ai bolsters its GPU orchestration and signals a shift toward vertically integrated stacks that couple hardware with clustering middleware. IBM’s HashiCorp integration strengthens hybrid-cloud positioning by adding infrastructure as code and zero-trust capabilities. Acquisition activity underscores the premise that ecosystem depth, not point features, drives purchasing decisions.

Competition centers on performance, operability, and integration. Databricks’ automatic liquid clustering reduces tuning overhead and cuts query latency tenfold for test clients, illustrating how automation differentiates. Arista Networks marries networking and clustering by embedding load balancing directly into its EOS operating system. Edge-focused entrants design lightweight clustering for constrained devices, seizing white-space in manufacturing and telecom edge clouds.

Innovation pipelines remain active. Patent filings around distributed edge service orchestration are growing, with IBM securing rights for multi-access service delivery that could extend clustering to 5G base stations. Academic breakthroughs such as the 97.7% accurate Torque clustering algorithm from the University of Technology Sydney hint at future performance leaps. Vendors that wrap such advances into user-friendly products will shape the future trajectory of the clustering software market.

Clustering Software Industry Leaders

Microsoft Corporation

Amazon Web Services, Inc.

Google LLC

IBM Corporation

Cloudera, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Databricks announced Automatic Liquid Clustering in public preview, enabling automated optimization of clustering columns on Unity Catalog tables and delivering up to 10 times faster queries.

- May 2025: Arctera released InfoScale to provide real-time data resilience for hybrid and multi-cloud clusters.

- March 2025: Clearwater Analytics completed a USD 1.5 billion purchase of Enfusion, integrating front-to-back investment operations in a single cloud platform.

- March 2025: Progress acquired ShareFile for USD 875 million, adding an AI-driven document collaboration platform that deepens its clustering portfolio.

Global Clustering Software Market Report Scope

| Windows |

| Linux / Unix |

| Others Platforms (macOS, BSD, etc.) |

| Large Enterprises |

| Small and Medium-sized Enterprises (SMEs) |

| IT and Telecommunications |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Retail and E-commerce |

| Manufacturing |

| Others End-Use Industry |

| On-premise |

| Cloud |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Platform | Windows | ||

| Linux / Unix | |||

| Others Platforms (macOS, BSD, etc.) | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium-sized Enterprises (SMEs) | |||

| By End-Use Industry | IT and Telecommunications | ||

| Banking, Financial Services and Insurance (BFSI) | |||

| Healthcare and Life Sciences | |||

| Retail and E-commerce | |||

| Manufacturing | |||

| Others End-Use Industry | |||

| By Deployment | On-premise | ||

| Cloud | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is clustering software?

Clustering software is middleware that links multiple servers or nodes so they operate as a single logical system, delivering high availability, load balancing, and parallel processing for data-intensive workloads.

How fast is the clustering software market growing?

The clustering software market size is projected to expand from USD 6.91 billion in 2025 to USD 12.52 billion by 2030 at a 12.63% CAGR.

Which industries are driving the fastest adoption?

Healthcare & Life Sciences leads growth with an 13.6% CAGR because real-time patient analytics and generative AI models require scalable compute clusters.

Why are small and medium enterprises adopting clustering?

Cloud-delivered offerings and simplified management interfaces enable SMEs to realize benefits such as 47.64% inventory cost savings with payback in roughly.

What role does Kubernetes play in this market?

Kubernetes orchestrates 97.42% of production clusters, making it the standard for managing containerized workloads across multi-cluster environments.

What is the primary barrier to wider deployment?

Seventy-six percent of users cite deployment and operational complexity as the biggest hurdle, prompting demand for automation and managed services.

Page last updated on: