Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

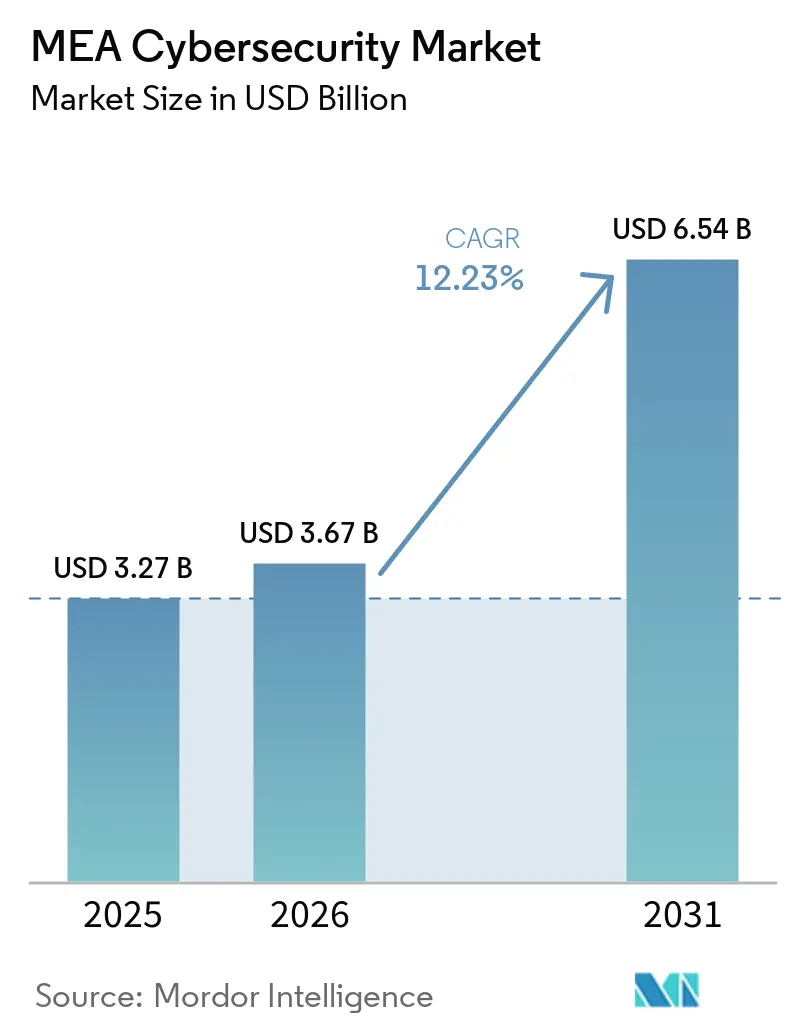

| Base Year Market Size (2025) | USD 3.27 Billion |

| Market Size (2026) | USD 3.67 Billion |

| Market Size (2031) | USD 6.54 Billion |

| Growth Rate (2026 - 2031) | 12.23% CAGR |

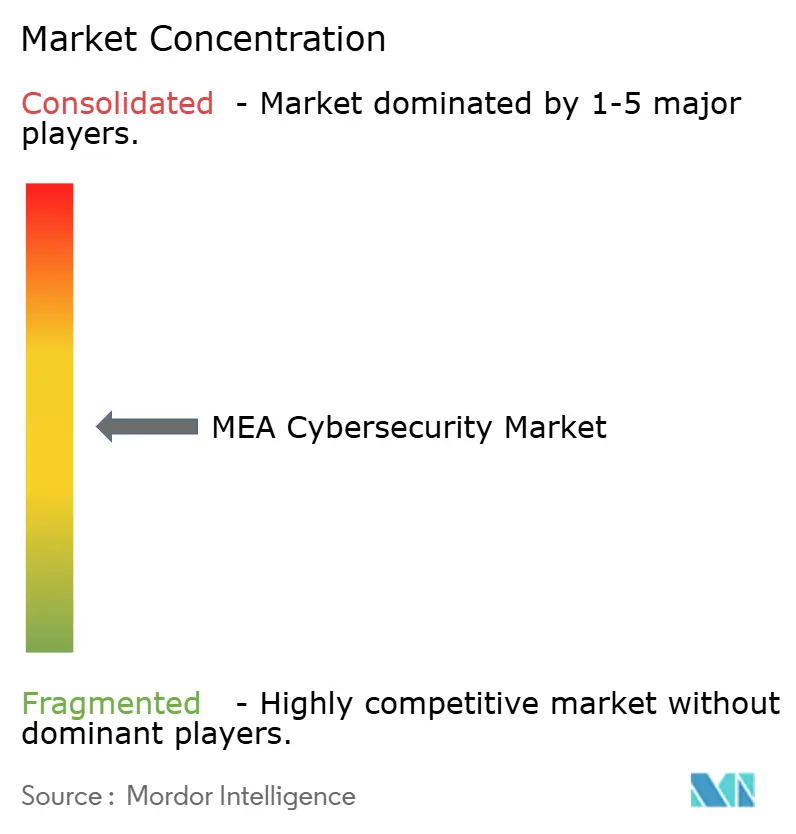

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

MEA Cybersecurity Market Analysis by Mordor Intelligence

Middle East and Africa cybersecurity market size in 2026 is estimated at USD 3.67 billion, growing from 2025 value of USD 3.27 billion with 2031 projections showing USD 6.54 billion, growing at 12.23% CAGR over 2026-2031. Rapid sovereign-cloud rollouts across the Gulf Cooperation Council, mounting operational-technology (OT) threats to regional oil and gas assets, and explosive mobile-money adoption in Sub-Saharan Africa are converging to lift security spending. Mega-event pipelines such as Expo 2030 and NEOM drive hardening of critical national infrastructure, while cloud-delivered security gains traction as organizations modernize toward zero-trust architectures. Parallel cost pressures from an acute talent shortage and fragmented data-protection laws create openings for managed security service providers to capture share in the Middle East and Africa cybersecurity market.

Key Report Takeaways

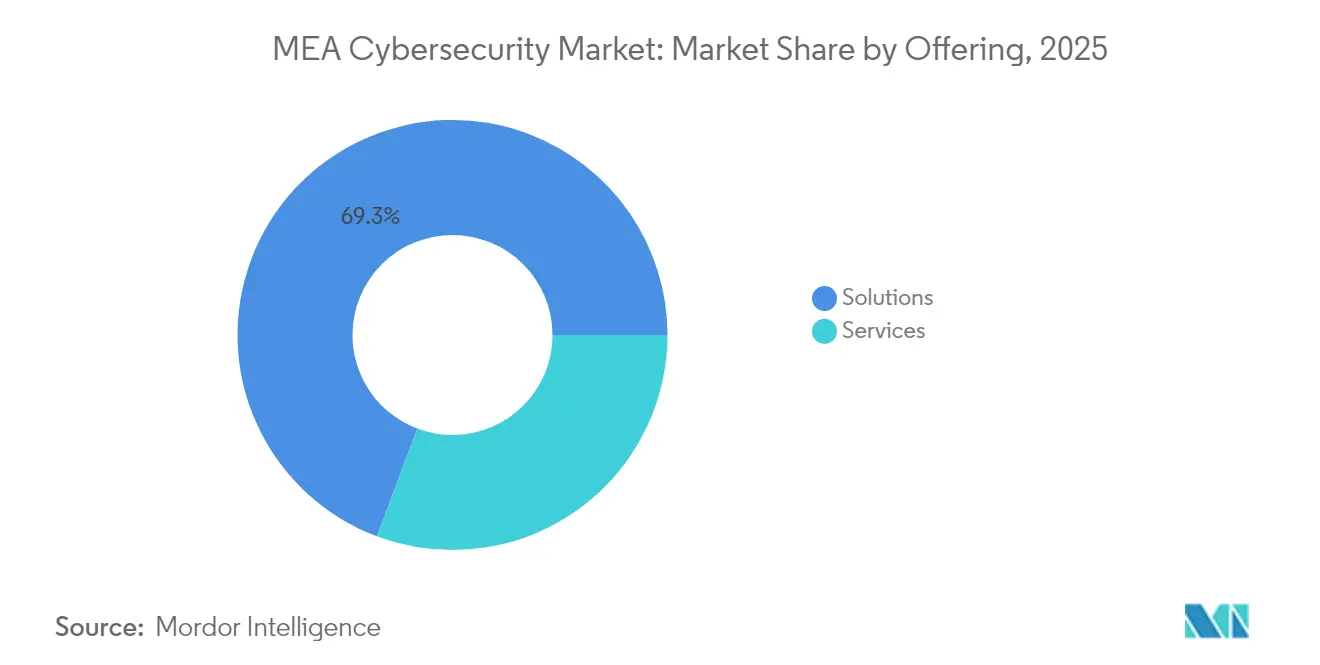

- By offering, solutions held 69.28% of the Middle East and Africa cybersecurity market share in 2025, whereas managed services are forecast to expand at a 14.68% CAGR through 2031.

- By deployment mode, on-premise commanded 61.65% share of the Middle East and Africa cybersecurity market size in 2025, while cloud-delivered security is set to grow at 15.43% CAGR.

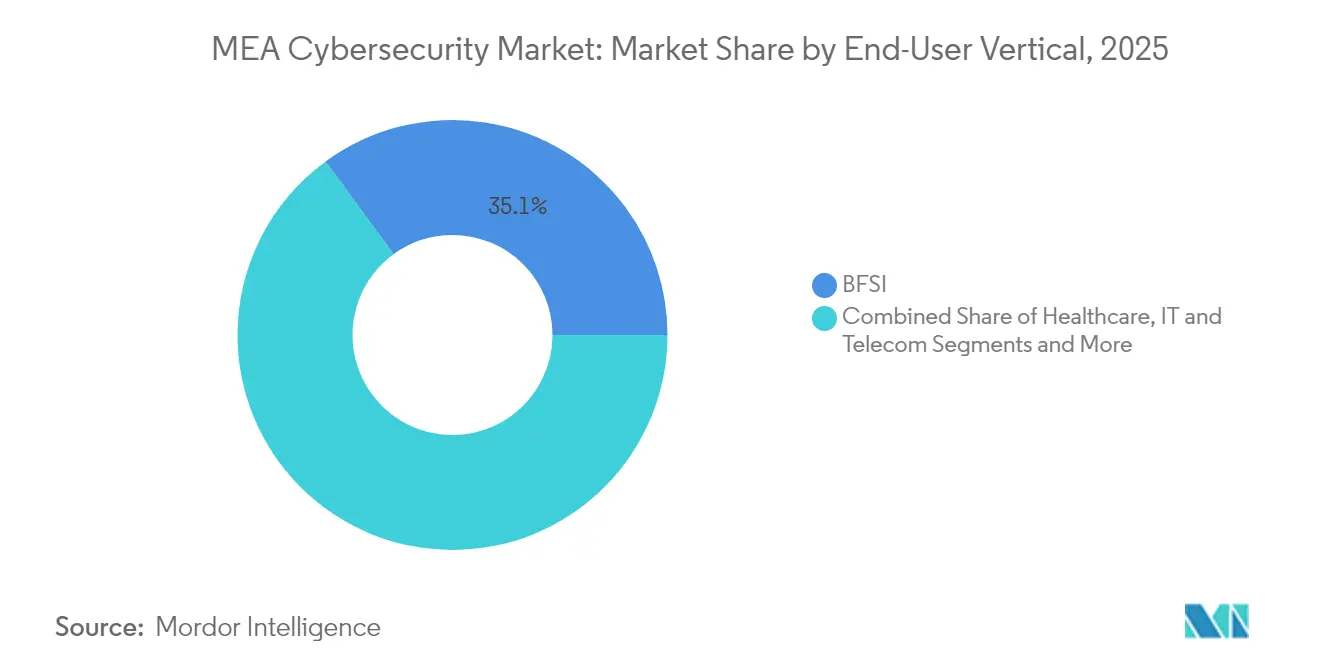

- By end-user vertical, BFSI led with 35.05% revenue share in 2025; healthcare cybersecurity is advancing at a 15.02% CAGR to 2031.

- By enterprise size, large enterprises accounted for 67.45% of spending in 2025, with the SME segment accelerating at a 14.36% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

MEA Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sovereign-cloud and residency mandates across GCC accelerating SOC investments | +2.1% | GCC nations | Medium term (2-4 years) |

| Rapid digital-banking license issuance in KSA and UAE boosting compliance-led security spend | +1.8% | Saudi Arabia, UAE | Short term (≤ 2 years) |

| Escalating OT cyber-attacks on oil and gas assets driving ICS/SCADA security uptake | +1.6% | Middle East, North Africa | Medium term (2-4 years) |

| Explosive mobile-money adoption in Sub-Saharan Africa requiring endpoint and fraud protection | +2.3% | Sub-Saharan Africa | Long term (≥ 4 years) |

| Mega-events pipeline intensifying critical-infrastructure hardening | +1.4% | UAE, Saudi Arabia | Short term (≤ 2 years) |

| New national cyber regulations mandating threat-intelligence sharing | +1.9% | GCC, North Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sovereign-cloud and residency mandates across GCC accelerating SOC investments

Mandates embedded in Saudi Arabia’s Essential Cybersecurity Controls 2024 and the UAE National IoT Security Policy require in-country data processing, pushing organizations to build local security operations centers and indigenous talent pipelines[1]Clyde & Co LLP, “Saudi Arabia Essential Cybersecurity Controls 2024,” clydeco.com. The strategy is reinforced by Qatar’s National Cybersecurity Strategy 2024-2030, which targets USD 11 billion market value by 2027 and prioritizes managed security services to offset talent shortages. As a result, local SOC build-outs and managed services adoption are expected to anchor long-term growth in the Middle East and Africa cybersecurity market.

Rapid digital-banking license issuance in KSA and UAE boosting compliance-led security spend

Saudi Arabia’s cybersecurity regulatory sandbox programs and the UAE’s Personal Data Protection Law compel digital banks to demonstrate robust risk-management frameworks before launch. Multiple regulatory checkpoints from central banks to commerce ministries require continuous audits, driving demand for consulting, third-party assessments, and automation platforms. Compliance-driven purchases add momentum to the Middle East and Africa cybersecurity market as license applications surge.

Escalating OT cyber-attacks on oil and gas assets driving ICS/SCADA security uptake

Energy operators confront sophisticated campaigns that infiltrate refinery control networks and disrupt production. Saudi Aramco’s OT security academy with Dragos reflects escalating investment in dedicated industrial-control protection. The region’s interconnected energy corridors necessitate air-gapped networks, anomaly detection sensors, and 24/7 OT-centric SOCs, reinforcing solution demand across the Middle East and Africa cybersecurity market.

Explosive mobile-money adoption in Sub-Saharan Africa requiring endpoint and fraud protection

Mobile-money transactions reached new peaks yet generated USD 140 million in cybercrime losses, driven by SIM-swapping and social-engineering tactics. Central banks in Nigeria and Kenya introduced mandatory cybersecurity frameworks, compelling financial-service providers to deploy multi-factor authentication, real-time fraud analytics, and secure agent networks. Endpoint and fraud-management vendors gain share as the Middle East and Africa cybersecurity market penetrates financially inclusive ecosystems.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute shortage of cybersecurity talent inflating service costs | −1.8% | GCC and Africa | Long term (≥ 4 years) |

| Fragmented data-protection laws across African nations raising compliance complexity | −1.2% | Sub-Saharan Africa | Medium term (2-4 years) |

| Budget constraints among African SMEs prioritising basic digitisation over security | −1.4% | Sub-Saharan Africa | Medium term (2-4 years) |

| Import dependence on security appliances exposed to geopolitical supply-chain disruptions | −0.9% | Middle East, North Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Acute shortage of cybersecurity talent inflating service costs

Eighty-seven percent of UAE enterprises struggle to recruit qualified professionals despite monthly salaries exceeding AED 13,500 for consultants. Qatar records 434.09 cybersecurity roles per 100,000 residents, yet demand continues to outstrip supply, forcing organizations to outsource monitoring and incident response. Higher wage bills lift overall project costs and temper adoption rates, particularly among mid-tier enterprises, constraining the Middle East and Africa cybersecurity market.

Fragmented data-protection laws across African nations raising compliance complexity

Cameroon, Nigeria, and Egypt maintain disparate privacy statutes that compel multinational service providers to maintain separate compliance playbooks. Varying breach-notification timelines and penalty structures inflate audit workloads and extend project lead times. Companies are defaulting to a highest-bar approach, adopting the strictest controls across the continent, but this raises implementation cost and slows market entry in the Middle East and Africa cybersecurity market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Solutions Outpace Services Yet Momentum Shifts

Solutions captured 69.28% of revenue in 2025 as organizations procured endpoint, network, and cloud-security suites in bulk. This dominance shows the purchasing power of large enterprises that still favor on-premise appliances for critical environments. Continued innovation in AI-driven threat detection reinforces solution spend, with vendors like SentinelOne adding security-posture management to defend shadow AI assets. The Middle East and Africa cybersecurity market nevertheless shows rising appetite for managed services, evident in a 14.68% CAGR outlook fueled by acute talent shortages and compliance burdens.

Professional services grow as integrators tailor complex hybrid architectures across sovereign-cloud environments. SMEs in particular gravitate toward SOC-as-a-Service offerings such as Liquid C2, which bundles monitoring, incident response, and regulatory reporting for a predictable fee structure. The shift reallocates share within the Middle East and Africa cybersecurity industry while preserving solution sales for large renovation projects.

By Deployment Mode: Cloud Traction Gains on On-Premise Lead

On-premises architectures held 61.65% of the Middle East and Africa cybersecurity market size in 2025 due to data-sovereignty rules and legacy SCADA linkages. Yet cloud-delivered security is forecast to expand at 15.43% CAGR as regional providers establish local Points of Presence that meet residency mandates. Cisco’s UAE Secure Service Edge node exemplifies cloud localization that lowers latency and aligns to GCC controls.

Hybrid models now dominate migration roadmaps. Organizations retain sensitive workloads in-country while routing analytics and sandboxing tasks to regional clouds. Gartner summit dialogues underscore zero-trust adoption as enterprises decouple identity from perimeter, further propelling cloud uptake within the Middle East and Africa cybersecurity market.

By End-User Vertical: BFSI Retains Lead, Healthcare Surges

BFSI institutions represented 35.05% of expenditure in 2025, reflecting strict prudential oversight and rising payment-fraud incidents. New digital banking license rounds in Saudi Arabia and the UAE demand ISO 27001-aligned controls, consolidating security budgets with identity, fraud, and data-loss-prevention modules. Conversely, healthcare spending rises at 15.02% CAGR as connected medical devices expand the attack surface. Research from academic consortia documents malware and ransomware risks to hospital IoT fleets.

Government, energy, and manufacturing sectors sustain demand for OT-centric defenses. Retail and e-commerce prioritize payment-gateway security as online transactions proliferate, while telecom carriers invest in back-end hardening and managed security resale programs. These diversified drivers reinforce resilience in the Middle East and Africa cybersecurity market.

By Enterprise Size: SME Adoption Narrows Gap

Large enterprises accounted for 67.45% of 2025 spending, yet SMEs post the fastest trajectory at 14.36% CAGR. Cyberattacks target South African small businesses in 43% of incidents, with average losses of USD 254,445 per breach. Managed service catalogs, open-source SIEM, and subscription-based endpoint suites lower entry barriers and allow SMEs to meet regulatory benchmarks without growing internal headcount.

Budget allocations are rising; accordingly, companies plan 9% annual security-budget uplifts over the next two years, signaling that the Middle East and Africa cybersecurity market will broaden beyond enterprise incumbents. Scalable licensing and consumption pricing are critical to unlocking latent SME demand.

Geography Analysis

The Middle East commands the lion’s share of the Middle East and Africa cybersecurity market, anchored by Saudi Arabia and the UAE. Vision 2030 initiatives finance mega-projects such as the USD 5 billion NEOM DataVolt AI factory, which elevates domestic data-processing capacity and heightens security requirements. The UAE targets AED 18 billion cybersecurity market value across MENA and plans to train 40,000 specialists, aligning workforce development with sovereign-cloud adoption goals. Qatar’s roadmap forecasts USD 11 billion security expenditure by 2027 at 15.6% annual growth, cementing Doha as a GCC cyber hub.

Israel’s advanced startup ecosystem adds innovation depth, backed by Cyberstarts’ USD 300 million fund that strengthens regional talent pools. Turkey, Bahrain, and Oman refine national frameworks to address state-sponsored threat escalation, driving incremental spending on threat-intel platforms and SOC modernization. Africa presents diverse maturity curves. South Africa leads commercial adoption, yet 90% of continental businesses lack adequate protocols, signaling vast whitespace. Nigeria’s Central Bank enforces risk-based guidelines that spur banking-sector investment, while Kenya, Ghana, and Egypt intensify capacity-building after high-profile attacks on government portals and mobile-money platforms. Rest-of-Africa markets enter digital-transformation phases supported by multilateral infrastructure financing, unlocking future revenue pools for vendors in the Middle East and Africa cybersecurity market. Cross-border regulatory divergence hampers rapid deployment; however, organizations increasingly pursue a highest-standard posture to streamline multi-jurisdiction operations. Regional associations are drafting harmonized policy templates, promising medium-term compliance simplification and cost reductions.

Competitive Landscape

The Middle East and Africa cybersecurity market features global incumbents such as Cisco, Palo Alto Networks, and IBM operating alongside regional specialists like Help AG and StarLink. Vendor consolidation is underway as platform players acquire point-solution startups to widen portfolio breadth. G42’s 2025 acquisition of CPX integrates AI-driven analytics with managed-service scale, exemplifying vertical integration as a competitive hedge.

Local presence is pivotal. LogRhythm | Exabeam inaugurated a Riyadh headquarters to align offerings with Saudi Vision 2030, while PureSquare opened dual Gulf offices targeting tenfold regional revenue growth. Technology differentiation centers on AI, machine learning, and zero-trust blueprints; for example, A10 Networks released AI application-security guidelines that resonate with digital-first enterprises.

White-space opportunities cluster around healthcare, SME enablement, and supply-chain security appliances, where fragmented solutions remain common. Emerging disruptors such as Saudi Arabia’s Cipher and Africa-focused Defendis secure funding to scale threat-detection platforms tailored to local attack vectors. The competitive frontier increasingly rewards vendors that combine regulatory fluency, localized support, and talent-development programs with advanced threat analytics.

MEA Cybersecurity Industry Leaders

Cisco Systems Inc.

Dell Technologies

Kaspersky Lab

IBM Corporation

Check Point Software Technologies Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Cyberstarts launched a USD 300 million fund to assist Israeli cybersecurity startups in attracting talent.

- June 2025: UAE unveiled a comprehensive national cybersecurity strategy aimed at securing critical infrastructure.

- May 2025: UAE National Security Advisor met with Cisco CEO to deepen cooperation in AI and cybersecurity.

- February 2025: G42 acquired CPX, integrating 400 specialists into its AI value chain.

MEA Cybersecurity Market Report Scope

Cybersecurity solutions help an organization to monitor, detect, report, and counter cyber threats that are internet-based attempts to damage or disrupt information systems and hack critical information using spyware and malware, and by phishing, to maintain data confidentiality.

The Middle East and Africa cybersecurity market is segmented by offerings (solutions [application security, cloud security, data security, identity access management, infrastructure protection, integrated risk management, network security, end-point security, and other solution types] and services [professional services and managed services]), by deployment (On-premise, and cloud), by organization size (SMEs, large enterprises), by end-user vertical (BFSI, healthcare, IT and telecom, industrial and defense, retail, energy and utilities, manufacturing, and other end-user industries), and by Country (Saudi Arabia, United Arab Emirates, South Africa). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security Equipment | |

| Endpoint Security | |

| Other Services | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| On-Premise |

| Cloud |

By End-User Vertical

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defense |

| Manufacturing |

| Retail and E-commerce |

| Energy and Utilities |

| Manufacturing |

| Others |

By End-User Enterprise Size

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

By Geography

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Bahrain | |

| Kuwait | |

| Oman | |

| Israel | |

| Turkey | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Kenya | |

| Morocco | |

| Rest of Africa |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security Equipment | ||

| Endpoint Security | ||

| Other Services | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | On-Premise | |

| Cloud | ||

| By End-User Vertical | BFSI | |

| Healthcare | ||

| IT and Telecom | ||

| Industrial and Defense | ||

| Manufacturing | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Manufacturing | ||

| Others | ||

| By End-User Enterprise Size | Small and Medium Enterprises (SMEs) | |

| Large Enterprises | ||

| By Geography | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Qatar | ||

| Bahrain | ||

| Kuwait | ||

| Oman | ||

| Israel | ||

| Turkey | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Kenya | ||

| Morocco | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current valuation of the Middle East and Africa cybersecurity market?

The market is valued at USD 3.67 billion in 2026 and is forecast to reach USD 6.54 billion by 2031.

Which segment is growing fastest within the market?

Managed security services post the quickest pace, projected at a 14.68% CAGR through 2031.

Why is healthcare cybersecurity expanding rapidly?

Accelerated digital-health programs and rising IoT medical device deployments expose hospitals to ransomware and malware, supporting a 15.02% CAGR outlook.

How are sovereign-cloud mandates influencing security spending?

Data-residency and Saudization rules compel organizations to build local SOCs and adopt managed services, lifting solution and service demand.

What challenges do African SMEs face in cybersecurity adoption?

Budget constraints and acute talent shortages hinder internal capability building, pushing SMEs toward subscription-based managed services for protection.

Page last updated on: