Ransomware Protection Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 30.04 Billion |

| Market Size (2031) | USD 63.56 Billion |

| Growth Rate (2026 - 2031) | 16.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ransomware Protection Market Analysis by Mordor Intelligence

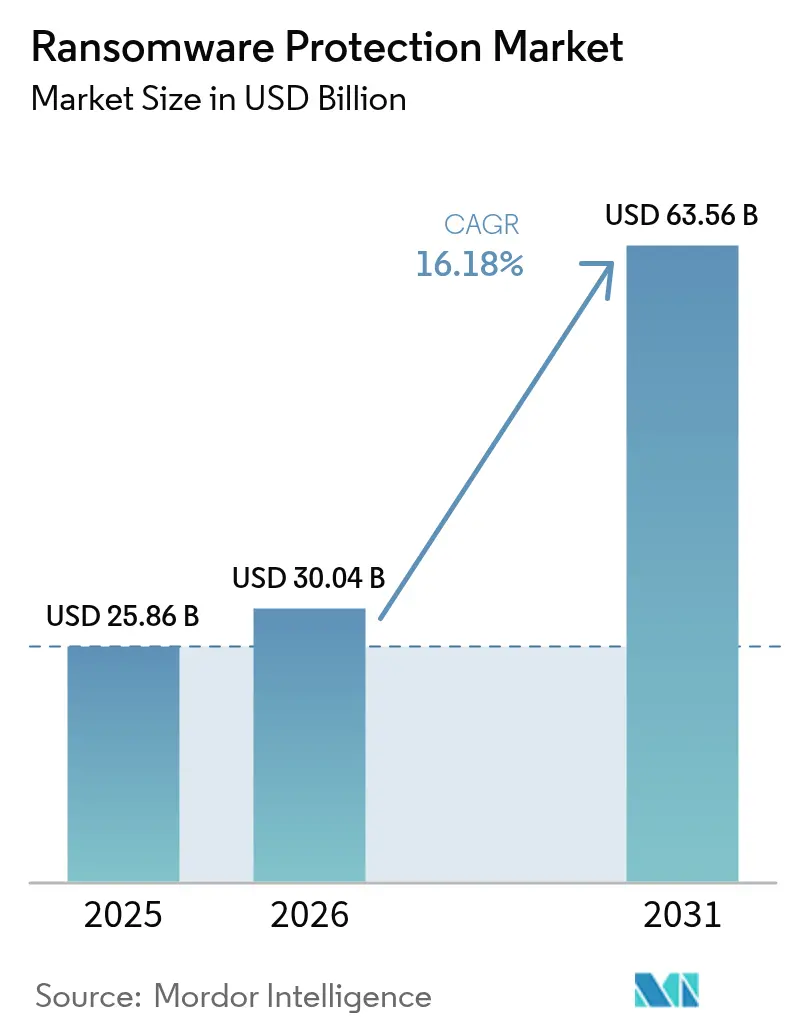

The ransomware protection market size was valued at USD 25.86 billion in 2025 and estimated to grow from USD 30.04 billion in 2026 to reach USD 63.56 billion by 2031, at a CAGR of 16.18% during the forecast period (2026-2031). Expanding ransomware-as-a-service ecosystems, the rise of triple-extortion threats, and a widening operational-technology attack surface keep spending momentum strong. Enterprises now emphasize integrated prevention, detection, and rapid recovery so they can maintain business continuity even when encryption succeeds. Cloud workload exposure, tightening global disclosure laws, and higher cyber-insurance thresholds are shifting budgets toward zero-trust controls, immutable backups, and behavioral analytics. Vendor consolidation intensifies because end users favor unified platforms that blend endpoint, identity, cloud, and backup capabilities with managed detection and response services.

Key Report Takeaways

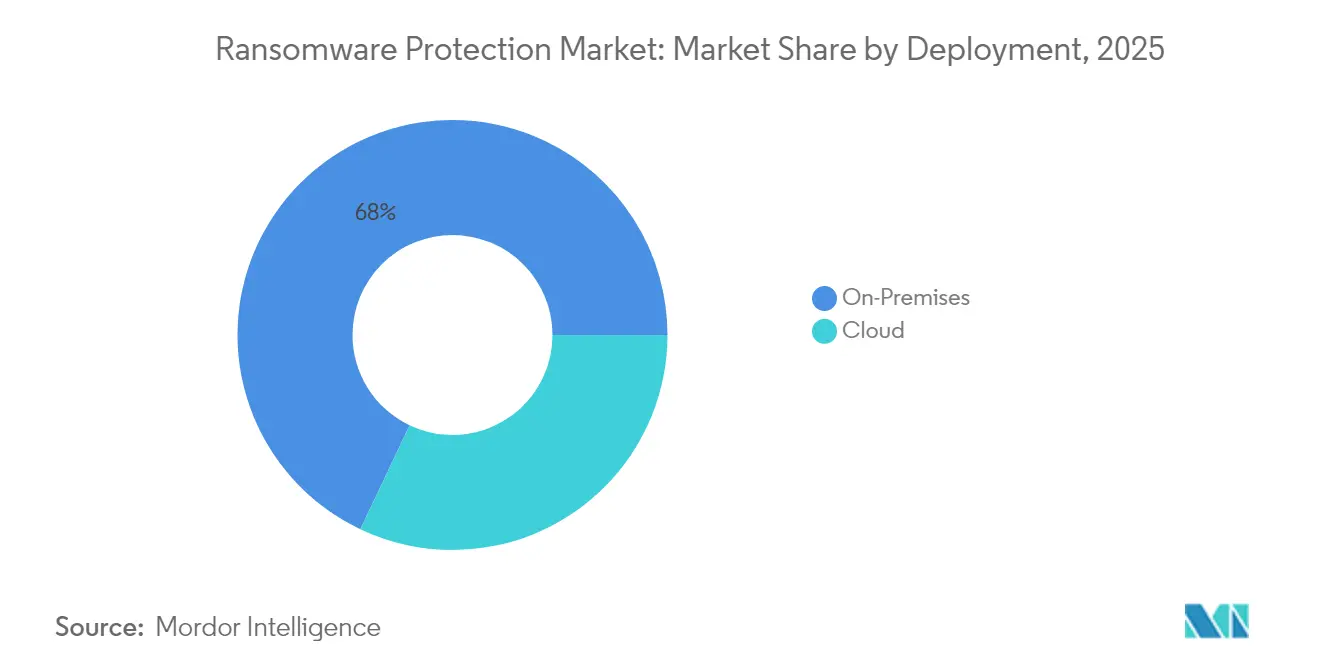

- By deployment, on-premises retained 67.95% of the ransomware protection market share in 2025 while cloud solutions are expanding at an 17.55% CAGR through 2031.

- By application, endpoint protection led with 43.65% revenue share in 2025; backup and recovery is forecast to advance at a 16.7% CAGR to 2031.

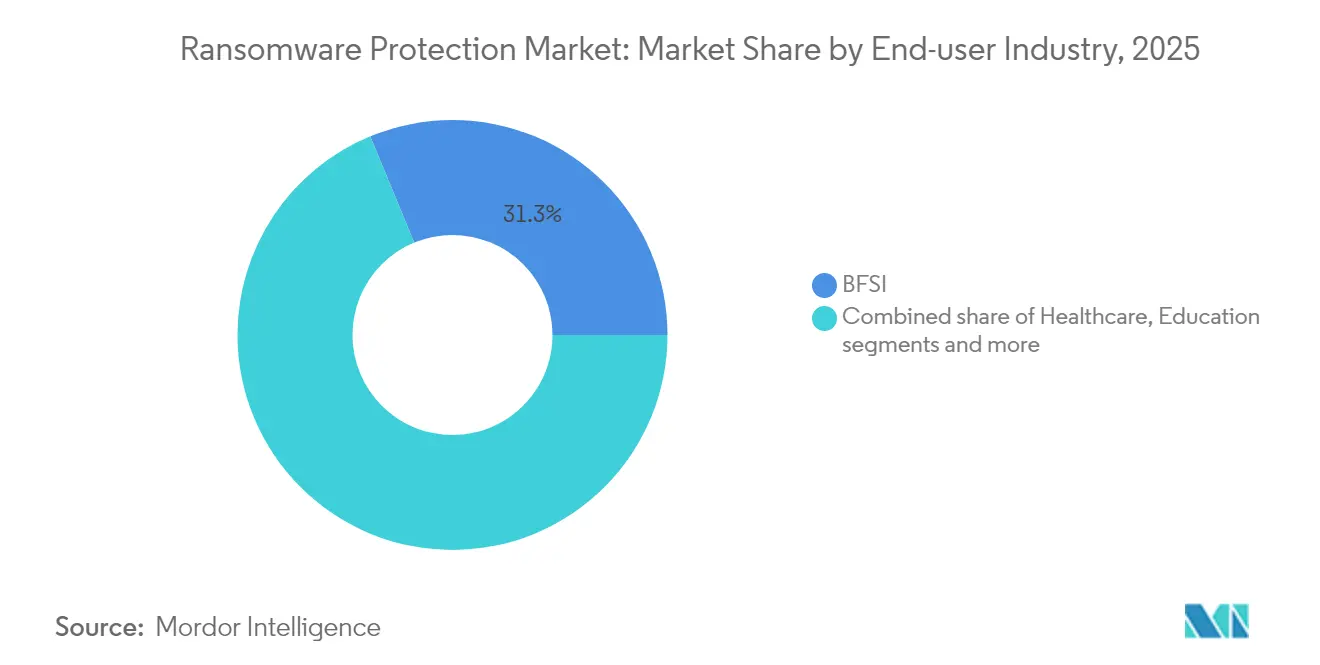

- By end-user industry, banking, financial services, and insurance captured 31.25% of the ransomware protection market share in 2025, whereas healthcare is progressing at a 16.75% CAGR through 2031.

- By organisation size, large enterprises commanded 71.60% of 2025 revenues while small and medium enterprises record the highest projected CAGR at 17.35% to 2031.

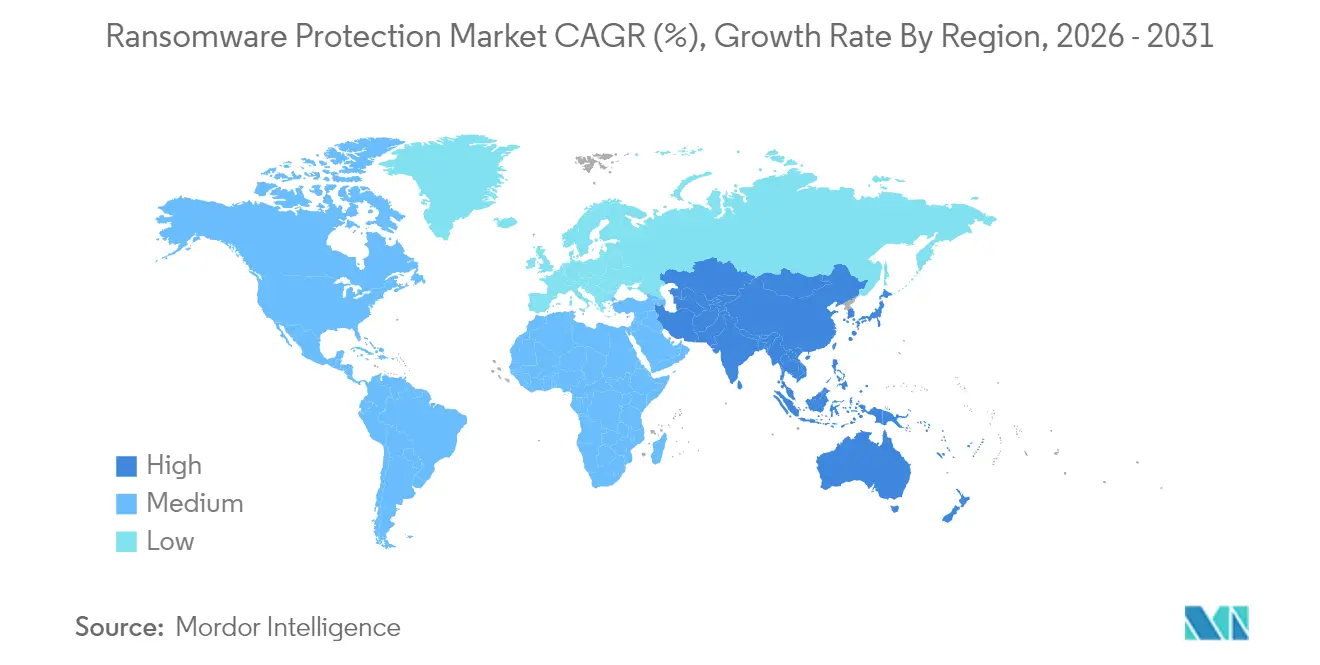

- By geography, North America led with 35.90% revenue share in 2025; Asia-Pacific is set to grow at a 16.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ransomware Protection Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating phishing and targeted breaches | +2.8% | Global, with concentration in North America & Europe | Short term (≤ 2 years) |

| Ransomware-as-a-Service (RaaS) boom | +3.2% | Global, particularly APAC and emerging markets | Medium term (2-4 years) |

| Cloud/SaaS migration enlarging attack surface | +2.1% | North America & EU leading, APAC following | Medium term (2-4 years) |

| Cyber-insurance mandates for advanced controls | +1.9% | North America & EU regulatory frameworks | Short term (≤ 2 years) |

| Zero-trust and micro-segmentation adoption | +2.4% | Global enterprise adoption, government-led initiatives | Long term (≥ 4 years) |

| Rise of data-exfiltration and triple-extortion tactics | +2.7% | Global, with higher impact in regulated industries | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Phishing and Targeted Breaches

Generative-AI voice cloning turns conventional phishing into persuasive “vishing,” increasing credential compromise rates in 2025. Microsoft’s Phishing Triage Agent in Defender XDR now auto-labels suspicious messages, allowing security teams to shorten response cycles while boosting accuracy[1]Tom Burt, “Defender XDR Adds AI-Powered Phishing Triage,” microsoft.com. Financial institutions say 56% of recent breaches originated from unpatched VPN flaws, pushing them to deploy user-entity behavior analytics that flag anomalous session activity. Heightened focus on social-engineering countermeasures fuels demand for continuous email, endpoint, and identity monitoring that work in concert rather than in silos.

Ransomware-as-a-Service Boom

More than half of active malware kits sold on underground forums are ransomware variants, and RaaS operators typically collect a 10%–40% cut of every extortion payment. Low technical barriers enable affiliates to attack industrial firms, driving an 87% surge in OT-focused incidents. Enterprises increasingly subscribe to threat-intelligence feeds that pinpoint emerging affiliate groups and pre-release indicators of compromise, allowing them to update detection rules before weaponization.

Cloud and SaaS Migration Enlarging Attack Surface

Workload migration drives a 75% rise in cloud intrusions year over year. The shared-responsibility model leaves identity and key management in customer hands, yet many teams lack skills to enforce least-privilege policies across multicloud estates. Cloud-native application protection platforms combine posture management, runtime protection, and container scanning to give security operations a single control plane. Fortinet’s planned integration of AI anomaly detection into its CNAPP suite reflects market appetite for automated drift-analysis that pinpoints misconfigurations before attackers do.

Cyber-Insurance Mandates for Advanced Controls

Underwriters now demand evidence of multi-factor authentication, network segmentation, and immutable backups before binding ransomware cover. Eighty-three percent of organizations purchase cyber policies, and average extortion payments rose from USD 335,000 to USD 6.5 million within two years, pushing carriers to tighten technical prerequisites. Vendors respond by bundling warranty programs—Bitdefender offers up to USD 1 million breach compensation—to help customers satisfy insurer questionnaires.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Free basic endpoint tools depress spend | -1.8% | Global, particularly price-sensitive SMB segments | Short term (≤ 2 years) |

| Law-enforcement wins cutting ransom payments | -1.2% | Global, with stronger impact in jurisdictions with active enforcement | Medium term (2-4 years) |

| Cyber-talent shortage for complex roll-outs | -2.1% | Global, acute in North America & Europe | Long term (≥ 4 years) |

| High total cost of full-stack XDR for SMBs | -1.6% | Global SMB market, particularly in emerging economies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Free Basic Endpoint Tools Depress Spend

Integrated protections inside Windows and major browser platforms deliver baseline anti-malware at no added cost. While these tools curb commoditized ransomware strains, they rarely offer behavioral analytics, deception, or automated rollback. Some SMB owners, misjudging their exposure, delay paid upgrades, eroding prospective revenue for specialist vendors. Commercial suppliers therefore highlight advanced response functions, supply-chain telemetry, and insurance-eligibility reports to justify premium tiers.

Law-Enforcement Wins Cutting Ransom Payments

Global takedowns have dismantled several ransomware infrastructures and helped recover funds, potentially undermining criminal ROI and tempering panic-driven procurement. The United States, United Kingdom, and Australia now share ransom-payment disclosures with financial-crime units, letting investigators trace laundering paths[2]CISA, “Joint Cybersecurity Advisory: Play Ransomware,” cisa.gov. Yet attackers adapt quickly, switching to data-wiper or harassment tactics that cause business disruption without large payments, ensuring ongoing need for resilient defenses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud Momentum Grows Alongside Control-Centric On-Premises Environments

In 2025, on-premises implementations accounted for 67.95% of revenue, underlining compliance and data-sovereignty demands among heavily regulated enterprises. Nevertheless, cloud subscriptions are sprinting forward at an 17.55% CAGR through 2031. The ransomware protection market size for cloud-delivered offerings is projected to rise sharply as buyers embrace elastic analytics and simplified updates. Hybrid designs are now standard, pairing local sensors with SaaS-based correlation engines so teams keep telemetry on-site while leveraging off-premises scale.

Automated snapshot orchestration shortens mean time to recover. Commvault’s Cloud Rewind now restores full tenant environments in minutes, rallying interest from organizations that previously hesitated due to recovery uncertainty. Continuous posture monitoring, integrated key management, and policy-as-code pipelines further attract development teams that favor DevSecOps alignment over hardware refresh cycles.

By Application: Backup and Recovery Outpace a Maturing Endpoint Core

Endpoint protection delivered 43.65% of 2025 revenue and remains the first purchase in any ransomware defence stack. Still, backup and recovery are on track for a 16.7% CAGR, the highest among application groups. Immutable and air-gapped repositories now act as a last-line assurance when prevention layers fail. ExaGrid’s non-network-facing tier and delayed delete feature exemplify designs that stop attackers from tampering with restore points.

Email and web-gateway modules evolve via secure access service edge architectures that route traffic through cloud inspection nodes, lowering latency for distributed workforces. Network segmentation features also move into these platforms, blurring lines between categories while strengthening containment. As buyers push toward platform consolidation, vendors bundle previously discrete modules into unified licences, a pattern reinforcing the ransomware protection market momentum.

By End-User Industry: Regulation Drives Healthcare Investment Beyond Financial Sector Leadership

The banking, financial services, and insurance segment led with 31.25% revenue share in 2025, reflecting entrenched regulatory scrutiny and high asset attractiveness. Healthcare follows with the fastest 16.75% CAGR, propelled by stricter HIPAA Security Rule amendments that require multi-factor authentication and encryption for electronic protected health information. The ransomware protection market size for healthcare entities is set to expand swiftly as providers modernize legacy systems and roll out zero-trust networks inside clinical environments.

Manufacturers contend with converged IT-OT infrastructures; 68% of industrial ransomware incidents in early 2025 hit production facilities, prompting investments in asset-visibility platforms. Education institutions, despite budget constraints, accelerated security spending after a 70% spike in attacks during the prior academic year. Across verticals, insurers and auditors now ask for proof of immutable backups and tabletop recovery drills as part of annual policy renewals.

By Organisation Size: SME Adoption Rises as Managed Services Close Capability Gaps

Large enterprises held 71.60% revenue share in 2025 thanks to sizable security staffs and multi-layer architectures. Yet small and medium enterprises are growing at 17.35% CAGR, underpinning democratization of enterprise-grade controls. Cloud-native protection suites with per-endpoint subscriptions remove capital barriers and embed best-practice policies out of the box.

Security-focused managed service providers (MSPs) play a pivotal role, bundling monitoring, patching, and incident response so customers sidestep talent shortages. Partnerships such as Guardz and SentinelOne integrate AI-powered detection with simplified dashboards, letting MSPs deploy across dozens of tenants efficiently. As ransomware groups increasingly target businesses under 1,000 employees, SMEs perceive cyber spending as a direct business-continuity cost rather than discretionary IT outlay, reinforcing ransomware protection market expansion.

Geography Analysis

North America led with 35.90% revenue share in 2025, anchored by mature compliance regimes in finance and healthcare plus sizeable enterprise budgets. Federal initiatives such as mandatory incident reporting for critical infrastructure further elevate baseline security expectations. The ransomware protection market size for United States-based organizations will continue to climb as insurance underwriters harden coverage terms.

Asia-Pacific posts the fastest 16.95% CAGR to 2031. New laws in Australia require ransom-payment disclosures, and Southeast Asia recorded more than 135,000 ransomware cases in 2024, spotlighting regional exposure. Many APAC governments launch subsidy programs that help mid-market firms adopt zero-trust controls, accelerating uptake beyond multinational headquarters.

Europe benefits from the NIS2 directive, which covers up to 150,000 essential entities and sets fines at EUR 10 million for non-compliance. The ransomware protection market share for EU-based SMEs is expected to rise as they implement mandatory risk assessments and supply-chain monitoring. Meanwhile, the Middle East and Africa foresee security outlays exceeding USD 3 billion in 2025 as enterprises invest in generative-AI analytics and breach-response retainers. Latin America grapples with a ransomware involvement rate notably higher than the global average, driving new regulation in Brazil that forces disclosure within three days, thereby enlarging regional opportunity for managed security providers.

Competitive Landscape

The vendor arena remains moderately fragmented yet tilts toward platform consolidation. Sophos’ USD 859 million purchase of Secureworks adds managed detection and response depth to its endpoint base, strengthening integrated incident-response pipelines. CyberArk’s USD 1.54 billion acquisition of Venafi marries machine identity management with human privilege controls, tackling credential abuse in multicloud environments.

AI-first specialists gain traction by focusing exclusively on ransomware defeat. Halcyon reached a USD 1 billion valuation through real-time behavior blocking and exfiltration prevention. Established players counter by infusing machine-learning analytics into backup and identity modules, thereby offering “detect-protect-recover” loops from a single console. Cloud alliances surge: CrowdStrike and Google Cloud expanded their partnership to embed managed detection into hyperscale logging, shortening investigation cycles for joint customers.

Success metrics move away from raw malware block rates toward measurable downtime reduction. Vendors that can demonstrate sub-hour recovery via orchestrated snapshot rollback enjoy premium pricing leverage, steering procurement teams toward outcome-based evaluations rather than feature checklists.

Ransomware Protection Industry Leaders

McAfee, LLC

AO Kaspersky Lab

Bitdefender

FireEye, Inc.

Microsoft

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: CISA, FBI, and the Australian Cyber Security Centre issued updated guidance on Play ransomware, urging multi-factor authentication and offline backups.

- May 2025: Australia enacted mandatory ransom-payment reporting for companies with annual revenues above AUD 3 million, increasing transparency of criminal cash flows.

- March 2025: NTT DATA and Rubrik unveiled Fortune 500 Ransomware Shield services that align with zero-trust principles across on-premises and cloud estates.

- February 2025: Halcyon raised USD 100 million in Series C financing to extend anti-ransomware coverage to Mac, Linux, and multicloud workloads.

- October 2024: EU member states completed transposition of NIS2, expanding mandatory cybersecurity measures to critical suppliers across multiple sectors.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the ransomware protection market as all purpose-built software, cloud services, and integrated hardware that prevent, detect, contain, and help recover from ransomware incidents across endpoints, email, networks, and backup environments, measured in end-user spending. According to Mordor Intelligence, this market will reach USD 25.86 billion in 2025 before expanding to USD 55.42 billion by 2030.

Scope exclusion: generic antivirus suites that lack dedicated anti-ransomware engines and pure incident-response retainer fees sit outside our numbers.

Segmentation Overview

- By Deployment

- On-Premises

- Cloud

- By Application

- Endpoint Protection

- Email Protection

- Network / Web Security

- Backup and Recovery / DR

- By End-user Industry

- BFSI

- Healthcare

- Government and Public Sector

- IT and Telecom

- Manufacturing and Industrial

- Education

- By Organisation Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed CISOs, managed security service providers, backup-as-a-service operators, and cyber-insurers across North America, Europe, and key Asia-Pacific hubs. Their feedback clarified real deployment volumes, typical user seats protected per license, and the speed at which zero-trust frameworks are replacing legacy perimeter tools, letting us fine-tune penetration and price assumptions.

Desk Research

We began by mapping the universe of published threat reports and policy briefs from trusted bodies such as CISA, ENISA, FBI IC3, and the OECD digital-economy unit, which give baseline attack frequency, ransom payment trends, and regulatory triggers. Our team then drew company-level revenue signals from SEC 10-Ks, regional cyber-insurance filings, and procurement portals, while patent insight from Questel and shipment clues from Volza provided technology diffusion markers.

Next, we extracted benchmark pricing for backup immutability, endpoint EDR, and deception tools through investor presentations and channel catalogs to ground average selling price (ASP) curves. These secondary inputs feed our starter model before any primary validation.

The sources listed here are illustrative; many additional publications were referenced during data collection and cross-checks.

Market-Sizing & Forecasting

A structured top-down build converts documented ransomware incident counts and average protection spend per infected endpoint into a demand pool, which is then sanity-checked through selective bottom-up vendor roll-ups and channel checks. Key variables like attack prevalence, insured recovery caps, cloud workload share, cyber-skills staffing costs, and mandatory disclosure timelines drive yearly adjustments. We forecast with multivariate regression, where incident growth and cloud adoption act as leading indicators, and scenario analysis captures policy shocks such as new breach-notification fines. Gaps in supplier revenue disclosure are bridged by triangulating survey-reported seat counts against sampled ASPs.

Data Validation & Update Cycle

Analysts run multi-stage anomaly screens and peer reviews before sign-off. The model refreshes every twelve months, with interim updates triggered by material M&A, mega-breaches, or policy shifts; a last-mile check happens just before each client download.

Why Mordor's Ransomware Protection Baseline Inspires Confidence

Published market values often diverge because studies differ in scope breadth, base years, and refresh cadence. We acknowledge these variances upfront and show where major gaps arise.

Key gap drivers include narrower solution baskets that exclude backup immutability, single-region sampling, outdated currency conversions, and aggressive linear growth extensions that overlook regulation-driven spend plateaus.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 25.86 bn (2025) | Mordor Intelligence | - |

| USD 23.8 bn (2024) | Global Consultancy A | Omits managed detection and response, uses constant ASP across regions |

| USD 5.7 bn (2024) | Industry Research Firm B | Counts software licenses only, no cloud or backup spend |

| USD 24.54 bn (2024) | Trade Journal C | Employs straight-line growth, lacks primary validation |

The comparison shows that when scope omissions or static pricing creep in, estimates swing widely.

By blending transparent variables with continuous expert feedback, Mordor Intelligence delivers a balanced baseline that boards and planners can trace, replicate, and trust.

Key Questions Answered in the Report

What is the current size and growth rate of the ransomware protection market?

The market is valued at USD 30.04 billion in 2026 and is set to reach USD 63.56 billion by 2031, reflecting a 16.18% CAGR.

Which deployment model is expanding the quickest?

Cloud-based ransomware protection shows the fastest trajectory with an 17.55% CAGR through 2031, even though on-premises still holds the larger revenue share.

Why are backup and recovery solutions seeing stronger budget allocation?

Backup and recovery tools are growing at a 16.7% CAGR because immutable and air-gapped storage offers the last line of defense when prevention layers fail.

Which industry vertical is projected to increase spending the most?

Healthcare is forecast to rise at a 16.75% CAGR, spurred by stricter HIPAA Security Rule revisions that mandate multi-factor authentication and encryption.

How do new regulations influence market demand?

Measures such as the EU’s NIS2 directive and Australia’s ransom-payment reporting law compel thousands of organizations to adopt zero-trust controls, driving fresh demand for comprehensive protection platforms.

What strategies help vendors stay competitive in this market?

Leading providers differentiate through platform consolidation, AI-driven detection, and rapid recovery capabilities, often supported by acquisitions and strategic cloud alliances.

Page last updated on: