Wheat Malt Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 5.76 Billion |

| Market Size (2031) | USD 8.15 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wheat Malt Market Analysis by Mordor Intelligence

The Wheat malt market size was valued at USD 5.46 billion in 2025 and estimated to grow from USD 5.76 billion in 2026 to reach USD 8.15 billion by 2031, at a CAGR of 6.05% during the forecast period 2026-2031. The Wheat malt market is still anchored by steady beverage demand, but its growth path is widening as food manufacturers use malt for texture, flavor, sweetness, and clean-label positioning in a broader set of products. The shift is important because demand is no longer tied only to brewing volumes, and that gives producers more room to balance slower developed markets with faster food ingredient demand. Certification, traceability, and product consistency are becoming stronger purchase criteria across the Wheat malt market, especially where organic, specialty, and food-grade formats command better pricing than standard grades. Regional demand remains uneven, with Europe holding the largest share while Asia-Pacific is expanding faster and drawing more commercial focus from suppliers. Competition in the Wheat malt market remains moderate, with established maltsters using product quality, certified production, and customer proximity to defend share while also moving into adjacent food ingredient categories.

Key Report Takeaways

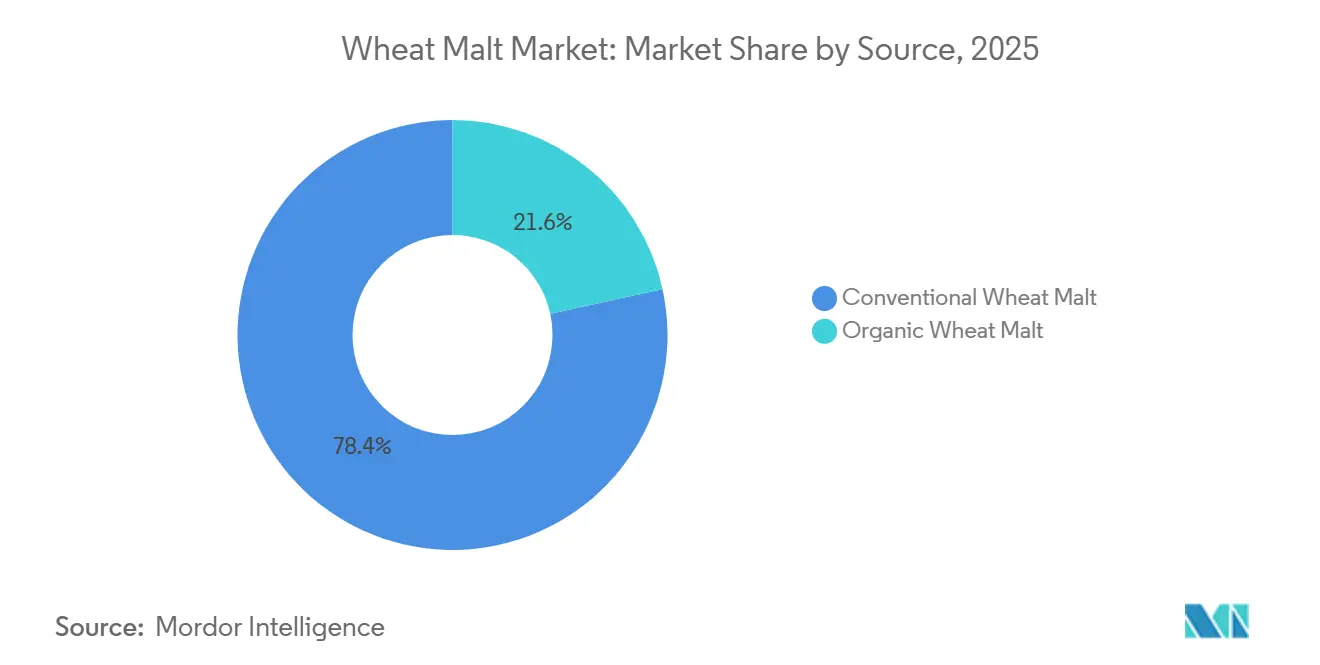

- By source, conventional held 78.42% of the Wheat malt market share in 2025, while organic is forecast to expand at a 7.86% CAGR through 2031.

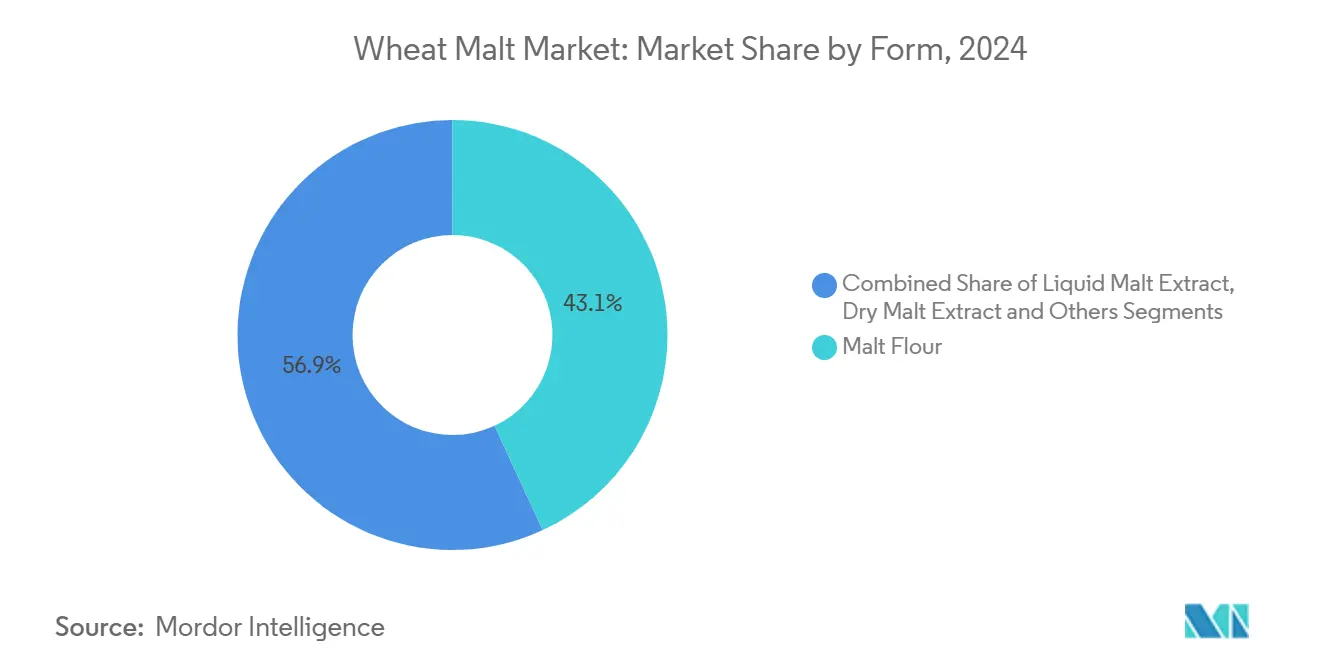

- By form, Malt Flour accounted for a 45.62% share of the wheat malt market size in 2025, while Liquid Malt Extract is projected to grow at an 8.03% CAGR through 2031.

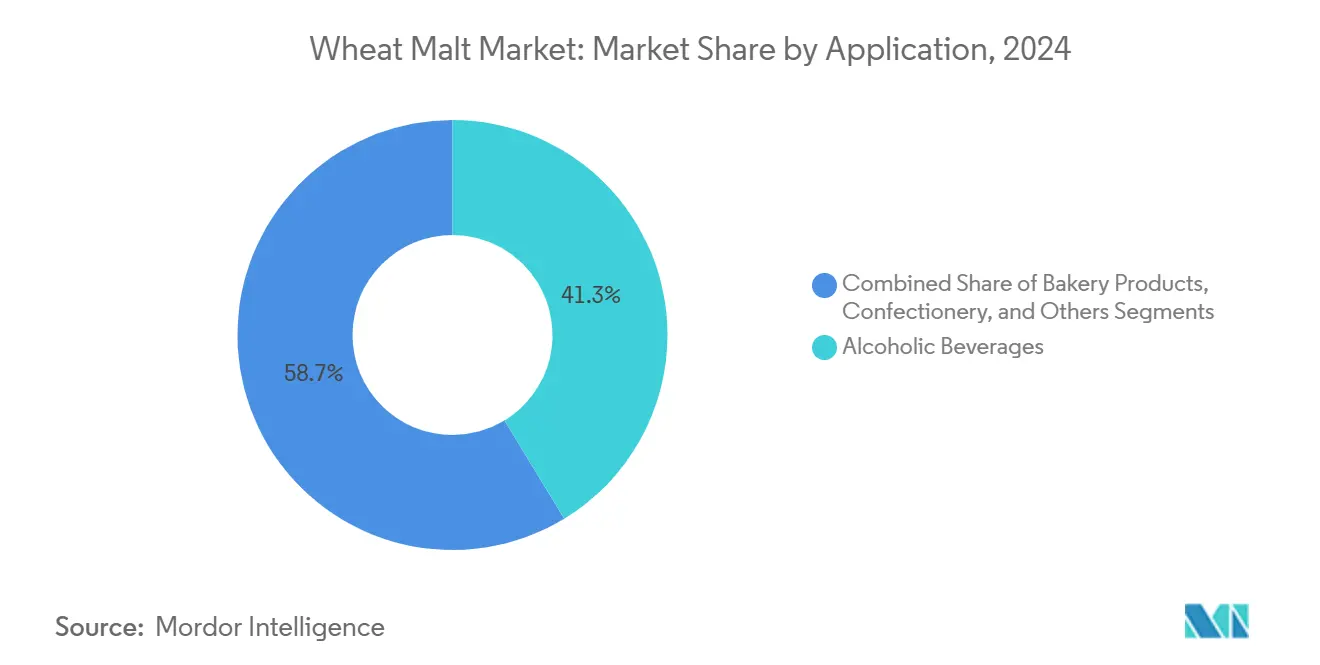

- By application, Beverages accounted for a 75.68% share of the wheat malt market size in 2025, while Food is forecast to expand at a 7.66% CAGR through 2031.

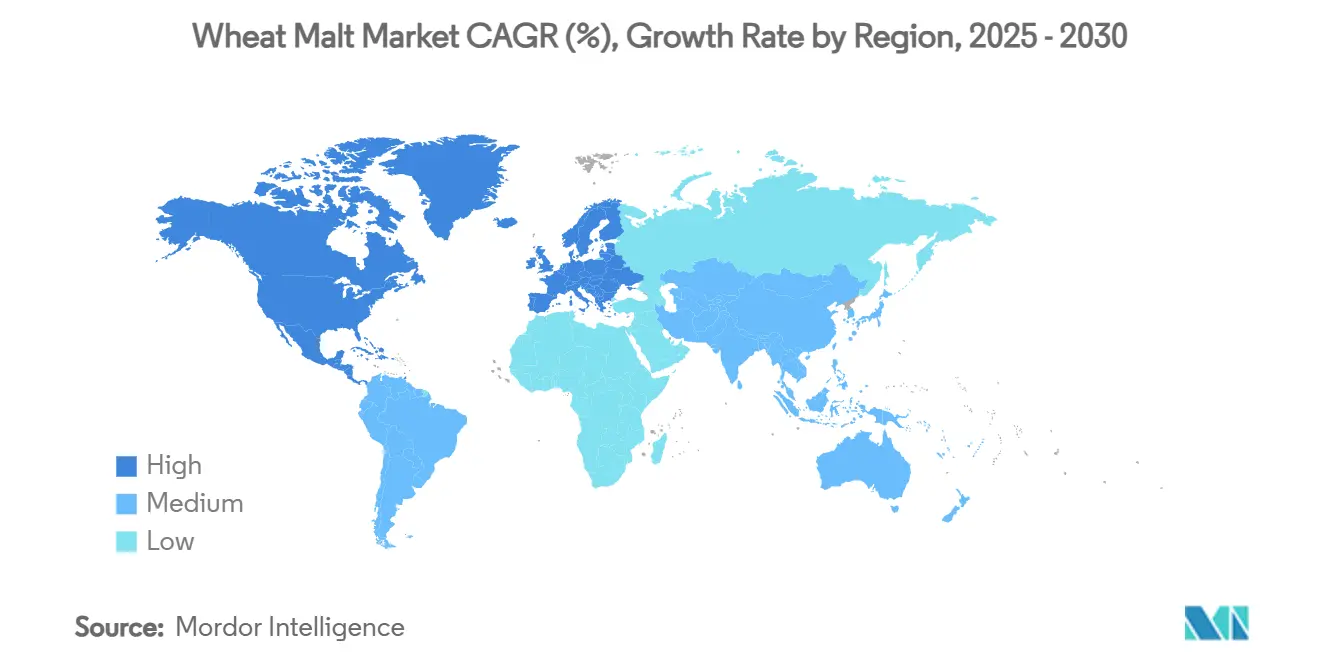

- By geography, Europe led with a 33.47% revenue share in 2025, while Asia-Pacific is projected to post the highest 7.89% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Wheat Malt Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of the global craft brewing industry | +1.2% | Global, with structural growth concentrated in Asia-Pacific and South America | Medium term (2-4 years) |

| Technological advancements in malting processes | +0.9% | Global, with early adoption in Germany, Belgium, and North America | Long term (≥ 4 years) |

| Growing popularity of malt-based functional and nutritional beverages | +1.0% | Global, led by Asia-Pacific, Middle East, and North America | Medium term (2-4 years) |

| Increasing demand for premium bakery ingredients | +0.8% | Global, strongest in Europe and Asia-Pacific | Medium term (2-4 years) |

| Growth of organic and specialty malt products | +1.0% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Rising consumer preference for natural and clean-label ingredients | +0.7% | Global, led by North America, Europe, and urban Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion of the Global Craft Brewing Industry

The Wheat malt market still benefits from the craft brewing base, even though conditions in mature markets became more selective in 2025. U.S. craft brewery volumes declined 4% in 2025 to 22.034 million barrels, but the sector still contributed USD 71.8 billion to the economy and supported more than 415,000 jobs, which shows that the channel remains commercially meaningful for specialty malt demand[1]Source: Brewers Association, “A Year of Correction for Craft Beer, With Early Signals of Recovery,” Brewers Association, brewersassociation.org. That matters for the Wheat malt market because wheat-based beer styles depend on protein profile, haze, and mouthfeel that are harder to replicate with standard barley-led formulations. Growth is also shifting toward regions where wheat beer adoption is coming from a lower base, which keeps room open for new customer wins in Asia-Pacific and South America. The result is a demand pattern where developed markets offer depth and technical requirements, while emerging markets offer expansion potential. Producers that already support brewers with formulation advice, consistent specifications, and local distribution hold a better position as buying patterns become more selective.

Technological Advancements in Malting Processes

Process improvement is helping the Wheat malt market reduce time loss, improve consistency, and widen the range of usable wheat inputs. Research published in Molecules in 2025 showed that the degree of hydrolytic and cytolytic modification in wheat malts varied meaningfully by cultivar and nitrogen fertilization level, which gives maltsters better control over extract and enzyme performance when matching malt to end use. A separate study in Food and Bioproducts Processing found that ultrasound-assisted drying reduced malting process time by up to 56% and improved alpha-amylase activity by up to 88% relative to oven drying, while also improving bread-making performance in downstream applications. These findings matter because the Wheat malt market serves both brewers and food formulators, and each group expects tighter process control than before. Better process design can lower variability, shorten production cycles, and improve the fit between wheat malt properties and the technical needs of baking, beverage, and nutrition products. Over time, that shifts competition away from simple volume supply and toward specification control, application relevance, and repeatable product quality.

Growing Popularity of Malt-Based Functional and Nutritional Beverages

The Wheat malt market is seeing stronger pull from uses that sit outside traditional beer production. Demand from food and beverage producers is moving toward recognizable ingredients that can add flavor, body, sweetness, and nutritional value without relying on synthetic-sounding labels. This is one reason the Wheat malt market is drawing more interest from manufacturers of fortified drinks, malt-based beverages, and nutrition-led formulations that need both processing functionality and a familiar ingredient profile. The strongest signal inside the current data set is that Food is growing faster than the overall market at 7.66% through 2031, which points to a broader commercial base beyond brewing. Muntons reported record annual financial results in 2025 and linked performance to strong demand for malted ingredients across global food and beverage markets, which supports the view that non-brewing demand is becoming more material for suppliers. As a result, the Wheat malt market is becoming more balanced, with growth tied to both beverage tradition and ingredient-led innovation.

Growth of Organic and Specialty Malt Products

Organic and specialty grades are reshaping the value mix in the Wheat malt market. The appeal is not only consumer-facing, because certified and traceable inputs also help food manufacturers meet internal sourcing standards and simplify product positioning across premium retail channels. Muntons launched Climate Positive Malt at BeerX 2025 and said the product offered up to 30% lower CO2 emissions per tonne than the UK malt average, showing how sustainability credentials are being packaged together with premium malt positioning instead of being treated as a separate offer. Weyermann also commissioned a malt flour mill in September 2025 with Bioland and Demeter organic-certified grades, which shows that organic capability is being built into mainstream operating platforms rather than managed as a sideline [2]. This combination of certification, traceability, and product specialization supports higher-value demand pockets across the Wheat malt market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from barley malt and other malt alternatives | -0.8% | Global, most acute in Europe and North America | Short term (≤ 2 years) |

| Stringent food safety and quality regulations | -0.5% | Global, most compliance-intensive in EU and North America | Medium term (2-4 years) |

| Limited availability of high-quality malting wheat | -0.7% | Europe, particularly the UK and Germany; secondary spill-over to North America | Medium term (2-4 years) |

| Rising competition from enzyme and flavor alternatives | -0.4% | Global, primarily in industrial food and beverage applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition from Barley Malt and Other Malt Alternatives

The Wheat malt market still competes against a larger and more established barley malt base in many mainstream brewing programs. Barley offers a wider standard use case for lagers and broader-volume beer styles, which limits how far wheat malt can penetrate high-volume brewing on price alone. In food processing, some industrial buyers can also turn to enzyme systems or alternative cereal inputs when cost, color control, or processing simplicity matters more than clean-label ingredient recognition. This means the Wheat malt market tends to perform best where buyers want differentiated flavor, texture, provenance, or certification rather than the lowest-cost fermentable or functional input. The commercial upside is that these niches often carry better margins, but the tradeoff is a smaller addressable base than standard barley-led categories. Suppliers that can document enzyme activity, origin, and certification stand a better chance of defending business when buyers compare wheat malt against substitutes.

Limited Availability of High-Quality Malting Wheat

Input quality remains a practical constraint for the Wheat malt market because product performance depends heavily on grain characteristics and supply consistency. AHDB reported in June 2026 that the UK barley area fell to its lowest level in 16 years and that the share of malting-approved varieties declined to 62% from 65% in 2025 and 68% in 2024, which points to weaker support for high-specification malting grain supply more broadly [2]Source: AHDB, “Analyst Insight, Mixed Outlook for Crops as GB Barley Area Falls,” AHDB, ahdb.org.uk. The USDA Foreign Agricultural Service also reported that UK food, starch, and industrial cereal use is forecast at 1.70 MMT in 2026-27, down from 1.96 MMT in 2025-26, reflecting softer demand from brewing, malting, and distilling channels[3]Source: USDA Foreign Agricultural Service, “Grain and Feed Annual, United Kingdom,” USDA Foreign Agricultural Service, apps.fas.usda.gov. While these figures are not limited to wheat, they still matter for the Wheat malt market because reduced grower incentive can weaken the supply outlook for high-quality malting grain over time. That raises the value of long-term sourcing agreements, certified growers, and tighter quality screening. Suppliers with stronger grain procurement discipline will be better placed if high-specification wheat becomes harder to secure in key European sourcing regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Conventional Scale Meets Organic Momentum

Conventional wheat malt held 78.42% of the wheat malt market share in 2025, while organic wheat malt is projected to expand at a 7.86% CAGR through 2031. The size gap shows that the Wheat malt market still relies on conventional supply for mainstream brewing and higher-volume food uses where cost efficiency and established sourcing remain decisive. Conventional grades benefit from mature production infrastructure, steady buyer familiarity, and broader availability across commercial channels. Those strengths keep conventional wheat malt central to the current volume base, especially where procurement teams prioritize dependable supply over premium claims.

Organic wheat malt is growing faster because the value equation is different in premium applications across the Wheat malt industry. The segment supports better pricing because buyers often treat certified sourcing, traceability, and cleaner label positioning as part of the product offer rather than an optional upgrade. The Wheat malt market is therefore splitting into a scale-led conventional lane and a value-led organic lane, with the latter finding stronger traction in craft beverages, infant nutrition, and other premium food formulations. Weyermann’s September 2025 commissioning of a malt flour mill with Bioland and Demeter organic-certified grades shows that leading suppliers are building certified flexibility into core assets as demand shifts toward more specialized customer requirements.

By Form: Malt Flour Anchors Demand, Liquid Malt Extract Leads Growth

Malt Flour held 45.62% of market value in 2025, while Liquid Malt Extract is forecast to expand at an 8.03% CAGR through 2031. This split captures a basic operating reality in the Wheat malt market, where dry formats remain deeply embedded in established ingredient systems while liquid formats gain ground in applications that value dosing accuracy and process convenience. Malt Flour remains the anchor because it is versatile, easy to store, and compatible with bakery, brewing, and food manufacturing routines that already use dry ingredient handling. Its role is especially strong where producers need a format that blends easily into formulations and can move through existing supply chains without process redesign.

Liquid Malt Extract is growing faster because it fits modern production lines that prioritize consistency, lower handling complexity, and easier integration into continuous processing. The Wheat malt market is benefiting from that shift because liquid formats can serve both premium beverage production and food manufacturing lines that require stable, ready-to-use functionality. Dry Malt Extract keeps an important middle position, especially where shelf life, transport simplicity, and export practicality matter more than immediate dosing convenience. The result is a form mix where no single format solves every need, but each one serves a distinct operational role across end uses.

By Application: Beverages Drive Volume, Food Accelerates Value Creation

Beverages accounted for 75.68% share of the wheat malt market size in 2025, while Food is forecast to grow at a 7.66% CAGR through 2031. The scale of beverages reflects wheat malt’s longstanding role in beer styles that depend on haze, mouthfeel, and protein contribution, particularly where wheat character is central to the final product profile. This keeps beverage demand at the core of the Wheat malt market, even as some mature brewing regions show slower volume momentum than before. Alcoholic beverages remain the largest use inside this segment, but non-alcoholic malt-based drinks are also contributing to broader commercial relevance in markets that value nutrition, flavor, and familiar ingredient cues.

Food is growing faster because wheat malt can perform several jobs at once in formulation. It can support browning, flavor development, softness, sweetness, and a more natural ingredient label in baked goods and adjacent categories. That combination gives the Wheat malt market a stronger route into bakery, confectionery, and other processed food categories where reformulation is active and ingredient scrutiny is rising. The category also benefits from the fact that food demand often behaves differently from brewing demand, which helps smooth revenue exposure for suppliers that serve both channels.

Geography Analysis

Europe retained 33.47% of the Wheat malt market share in 2025, making it the largest regional base in the current category structure. The region benefits from long-established wheat beer traditions, dense specialty malting capacity, and a customer base that understands the value of differentiated malt characteristics. That keeps the Wheat malt market well supported in countries with strong brewing cultures and active premium ingredient channels. Europe also stands out because leading suppliers are using the region as a base for higher-value specialization rather than only for standard malt output. Weyermann’s September 2025 malt flour mill commissioning in Bamberg and Muntons’ continued work around sustainability and product differentiation both show how European producers are extending the category into the premium food ingredient space as well as brewing.

Asia-Pacific is the fastest-growing region in the Wheat malt market, with a projected CAGR of 7.89% through 2031. Growth in this region is broader than a single channel because brewing demand, bakery demand, and malt-based beverage demand are rising together in several markets. That gives suppliers multiple ways to participate, which is important when customer adoption is still spreading from a lower base. The regional role in the Wheat malt market is therefore becoming more strategic, not only because it is growing faster, but also because it can support both beverage and food applications at the same time.

North America remains structurally important to the Wheat malt market because it still has a large specialty brewing ecosystem and established ingredient buyers. The Brewers Association reported 9,578 operating breweries in the United States in 2025, which shows that the commercial base remains sizable even after a more difficult year for volumes. Briess Malt & Ingredients marked its 150th anniversary in 2026, and Manitowoc, Wisconsin, was designated the “Specialty Malt Capital of the World,” which reflects the depth of specialty malt capability in the region. South America is still an emerging play in the Wheat malt market, with room to grow in both brewing and food-grade uses as local adoption deepens. The Middle East and Africa also remain relevant, especially where non-alcoholic malt beverages support demand from younger populations and expanding retail channels.

Competitive Landscape

The Wheat malt market shows moderate concentration, with a visible group of established producers alongside many regional suppliers that serve local brewers and food manufacturers. The largest players are not competing only on price, because premium customers increasingly expect consistent specifications, certified production, and technical support. This makes quality systems and product breadth more important competitive tools in the Wheat malt market than simple scale on its own. European producers remain prominent because they combine legacy malt expertise with expanding food ingredient capabilities. At the same time, North American suppliers continue to matter where specialty malts, customer service, and application flexibility are decisive for buyers.

Recent company actions show that strategy in the Wheat malt market is moving in 2 clear directions: premiumization and adjacency expansion. Weyermann’s malt flour mill launch in September 2025 shows a direct move into bakery and food ingredient applications from a strong brewing heritage base. Muntons’ Climate Positive Malt launch in March 2025 shows how sustainability positioning is being used to strengthen premium product appeal for brewing customers. Muntons’ partnership with Best Way Foods Ukraine in September 2025 also shows how suppliers are extending commercial reach through distribution and ingredient channel relationships rather than relying only on domestic demand.

The wider competitive field in the Wheat malt market includes many smaller or regional players that remain relevant because customer needs are often local and application specific. Buyers may value shorter delivery cycles, identity-preserved grain programs, or closer technical collaboration as much as large global scale. This creates room for specialized producers to compete effectively when they understand brewery, bakery, or nutrition customer requirements in detail. It also means the Wheat malt market is not locked into winner-takes-all behavior, even though established brands still enjoy visibility and trust.

Wheat Malt Industry Leaders

Richardson International Limited

Bindewald & Gutting Verwaltungs-GmbH

Interquell cereals GmbH

InVivo Group

VIVESCIA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: IREKS GmbH acquired a 13,000 sqm land plot in Chitila, near Bucharest, Romania, in a deal brokered by Cushman & Wakefield Echinox, with plans to develop an administrative headquarters, customer center, and logistics warehouse. The expansion supports the company's continued Eastern European growth and its dual positioning as a baking ingredient and malt supplier across more than 90 countries.

- April 2025: Great Western Malting (part of the Soufflet Malt family) launched two new brewer-driven products: Low Color Wheat Malt and Chit Malt. The Low Color Wheat Malt provides brewers with a malt that delivers maximum body and head retention while keeping beer color minimal, ideal for hazy beer styles like Hefeweizens and IPAs. Chit Malt is a cost-effective, lightly processed malt that boosts foam stability and mouthfeel, designed as a local alternative to imported chit malt.

- February 2025: Riverbend Malt House became the first malt house to receive third-party certification for regenerative agriculture in 2024 and launched Certified Regenified Malt. This product was asserted to align with rising sustainability demands, offering malt produced under regenerative farming practices emphasizing environmental stewardship and soil health.

- January 2025: Durst Malz launched a selection of authentic German malts to North American craft brewers. The lineup included six premium malts such as Dark Munich Malt 40 EBC, Munich Malt 20 EBC, Pale Ale Malt, Pilsen Malt, Vienna Malt, and Wheat Malt. The Wheat Malt adds body, haze, and a soft mouthfeel to Hefeweizens and Weissbiers.

Global Wheat Malt Market Report Scope

| Conventional |

| Organic |

| Malt Flour |

| Liquid Malt Extract |

| Dry Malt Extract |

| Others |

| Food | Bakery and Confectionery |

| Infant and Baby Foods | |

| Functional Foods | |

| Others | |

| Beverages | Alcoholic Beverages |

| Non-Alcoholic Beverages | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Source | Conventional | |

| Organic | ||

| Form | Malt Flour | |

| Liquid Malt Extract | ||

| Dry Malt Extract | ||

| Others | ||

| Application | Food | Bakery and Confectionery |

| Infant and Baby Foods | ||

| Functional Foods | ||

| Others | ||

| Beverages | Alcoholic Beverages | |

| Non-Alcoholic Beverages | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current outlook for wheat malt through 2031?

The Wheat malt market was valued at USD 5.46 billion in 2025, stands at USD 5.76 billion in 2026, and is projected to reach USD 8.15 billion by 2031 at a 6.05% CAGR.

Which end-use area contributes the most revenue?

Beverages remain the largest application, accounting for 75.68% of total value in 2025, which keeps brewing and malt-based drinks central to category demand.

Which segment is growing the fastest by application?

Food is the fastest-growing application at a 7.66% CAGR through 2031, supported by bakery, confectionery, infant nutrition, and functional food uses.

Which product form leads the category today?

Malt Flour held 45.62% of market value in 2025 because it fits established dry ingredient systems across bakery, brewing, and food processing.

Page last updated on: