Wheat Gluten Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

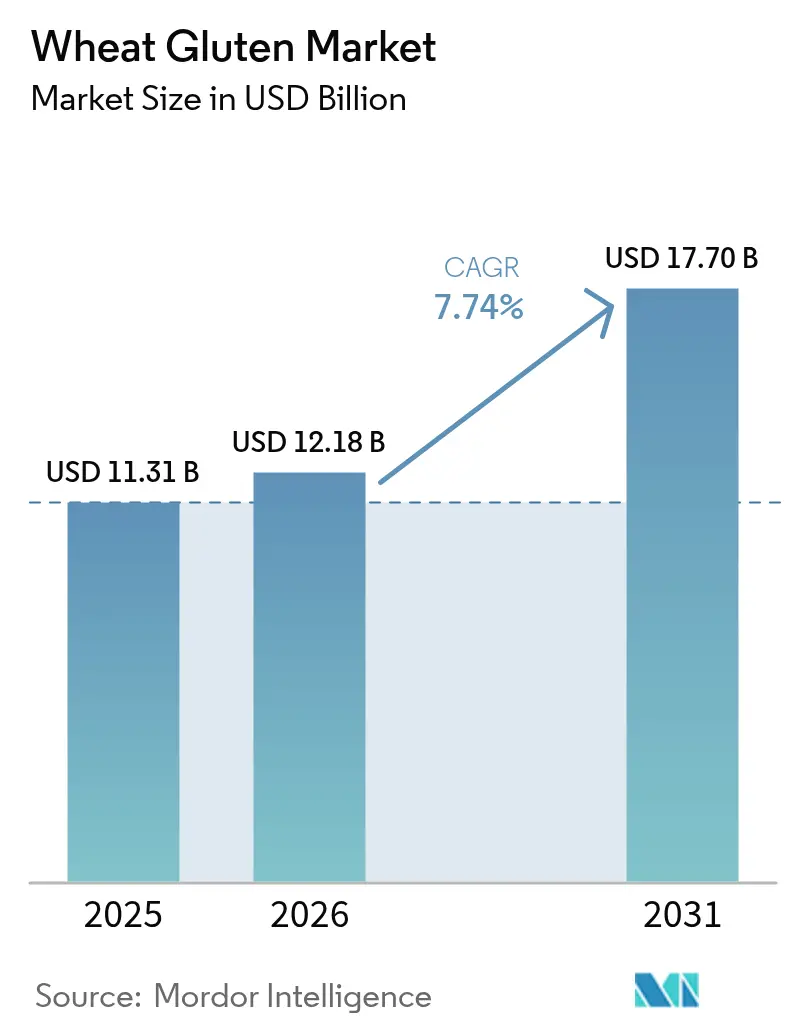

| Market Size (2026) | USD 12.18 Billion |

| Market Size (2031) | USD 17.7 Billion |

| Growth Rate (2026 - 2031) | 7.74% CAGR |

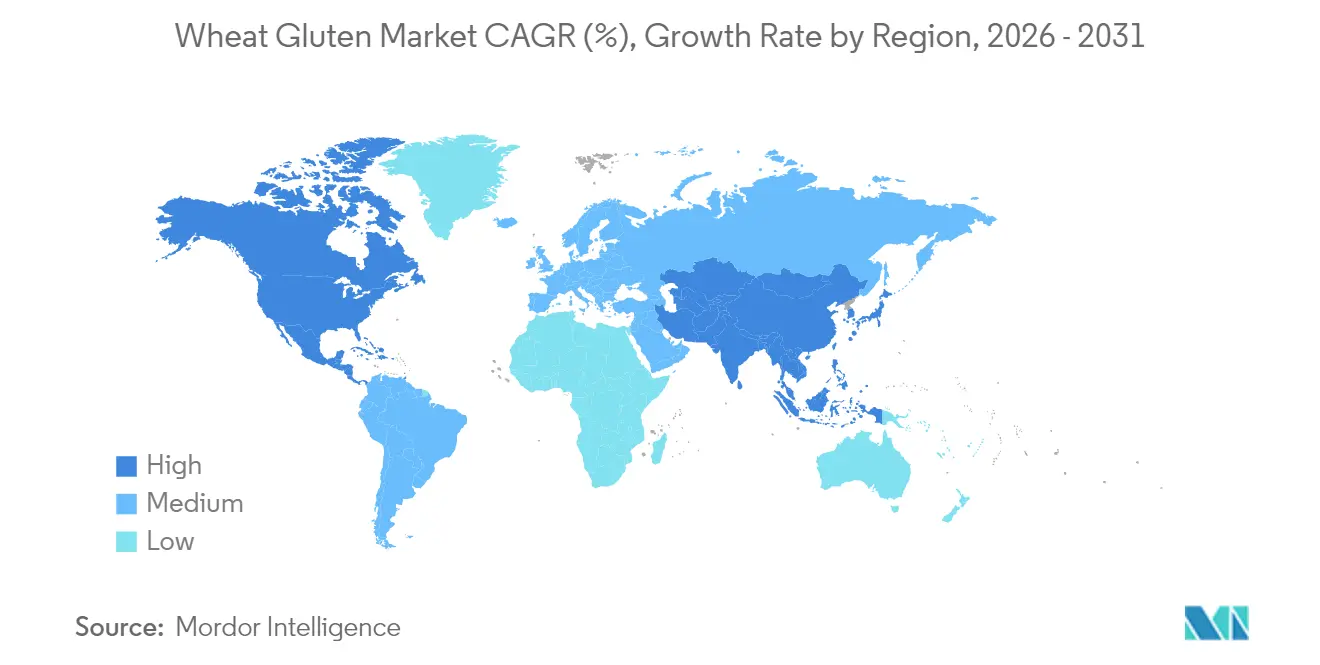

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Wheat Gluten Market Analysis by Mordor Intelligence

The wheat gluten market size is expected to grow from USD 11.31 billion in 2025 to USD 12.18 billion in 2026 and is forecast to reach USD 17.7 billion by 2031 at 7.74% CAGR over 2026-2031. Rising demand for plant-based proteins, sustained bakery consumption, and clean-label reformulations are expanding the addressable customer base and lifting average selling prices. Meat analog brands are scaling global launches, leveraging wheat gluten's viscoelasticity to mimic animal-protein texture. Liquid formulations gain traction in automated production lines, while organic variants earn shelf premiums in natural food channels. The increasing adoption of wheat gluten in sports nutrition products and protein supplements further strengthens market growth. Food manufacturers' focus on cost-effective, sustainable protein alternatives continues to boost wheat gluten consumption across various applications. On the supply side, technological upgrades in protein extraction, coupled with FDA[1]Source: FDA, “GRAS Notice Inventory,” fda.gov GRAS status, enhance processing yields and regulatory certainty. Moderate fragmentation allows both multinationals and ingredient specialists to compete through functional customization, sustainability credentials, and regional sourcing strategies.

Key Report Takeaways

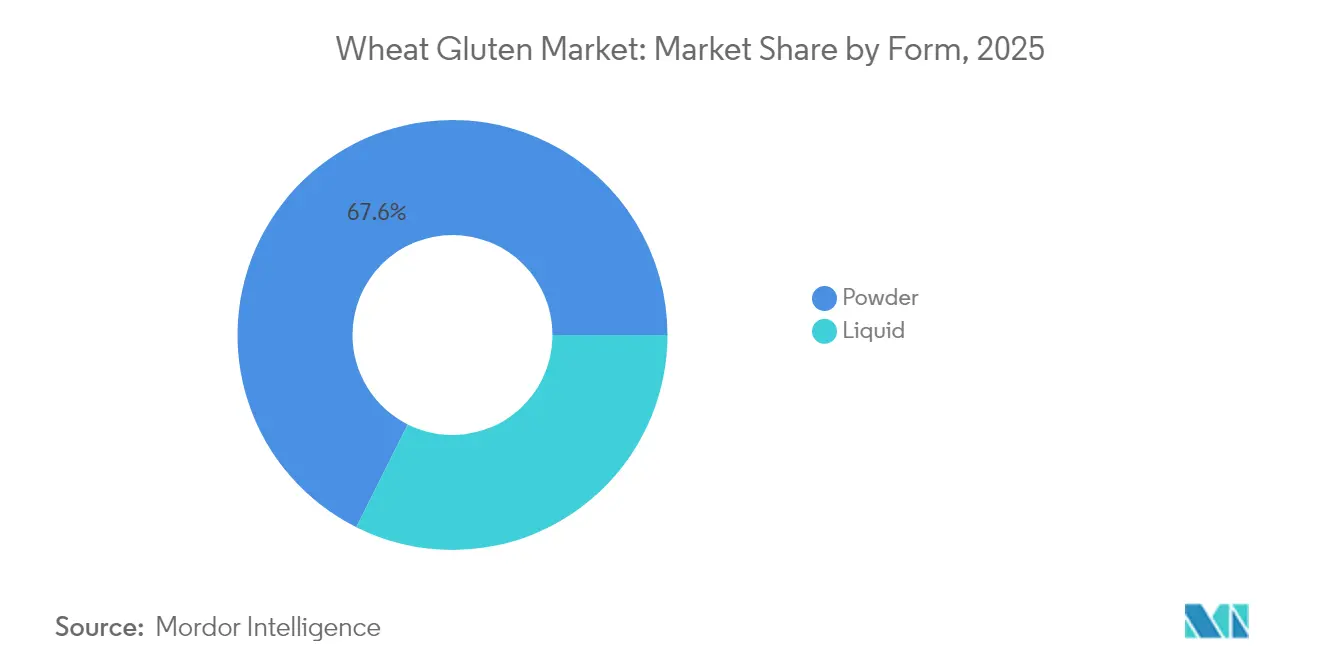

- By form, powder held 67.62% of the wheat gluten market share in 2025 and liquid is projected to expand at a 9.62% CAGR through 2031.

- By nature, conventional products retained 89.12% of the wheat gluten market size in 2025, while organic is set to grow at 10.06% CAGR.

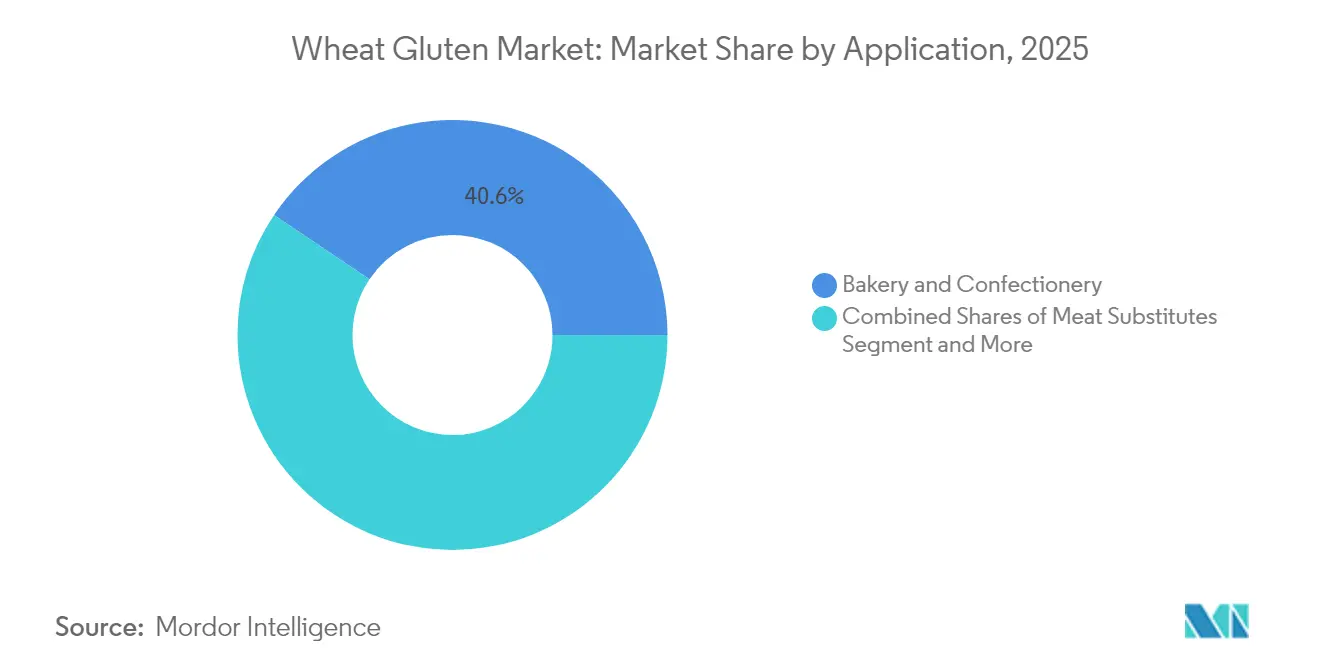

- By application, bakery and confectionery captured 40.58% of the wheat gluten market size in 2025; meat substitutes will post the fastest 9.88% CAGR.

- By geography, North America led with 34.12% wheat gluten market share in 2025, whereas Asia-Pacific is forecast to record 9.44% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wheat Gluten Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand in Bakery and Confectionery for Dough Strength and Texture | +1.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Superior Functional Properties in Diverse Food Applications | +1.5% | Global | Long term (≥ 4 years) |

| Increasing Demand for Plant-Based and High-Protein Food Products | +2.1% | North America, Europe, Asia-Pacific urban centers | Short term (≤ 2 years) |

| Trend Toward Protein Enrichment in Packaged Foods and Beverages | +1.3% | Global, led by developed markets | Medium term (2-4 years) |

| Expansion of Clean Label and Natural Ingredient Trends | +1.0% | North America and European Union primarily | Medium term (2-4 years) |

| Rising Awareness of Wheat Gluten as a Cost-Effective Protein Source | +0.9% | Asia-Pacific, Latin America, Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand in Bakery and Confectionery for Dough Strength and Texture

Commercial bakeries depend on wheat gluten's viscoelastic properties to maintain consistent dough performance across different flour qualities and processing conditions. The growing market for artisanal and specialty bread products increases demand, as bakers aim to maintain traditional fermentation characteristics while optimizing production efficiency. The industry's focus on clean-label formulations has increased the use of wheat gluten, particularly in hard red spring wheat flour blends, which provide better dough strengthening compared to synthetic additives. This enables manufacturers to use recognizable ingredients while maintaining product quality. The premium bakery segment benefits from this trend, as distinct textures command higher margins, creating ongoing demand for wheat protein isolates with specific functional properties. The expansion of industrial bakeries in emerging markets has intensified the need for standardized wheat gluten products to ensure uniform product quality. Additionally, the rise in health-conscious consumers seeking protein-enriched baked goods has further strengthened the market position of wheat gluten as a natural protein source.

Superior Functional Properties in Diverse Food Applications

Wheat gluten's unique protein composition, consisting primarily of gliadin and glutenin subunits, delivers unmatched elasticity and water-binding capabilities that extend beyond traditional applications into emerging food categories. The ingredient's ability to form cohesive protein networks makes it indispensable in meat analog production, where it provides the chewy texture characteristic of seitan and other plant-based proteins. Advanced processing techniques are unlocking new functionality through protein modification, with citric acid and enzymatic treatments enhancing foam stability and mechanical properties for specialized applications, including biodegradable packaging materials. The protein's thermal stability and film-forming properties position it as a versatile ingredient in processed foods requiring specific textural attributes, from pasta reinforcement to sauce thickening. MGP Ingredients' Arise protein isolate family demonstrates how targeted modifications can optimize wheat proteins for specific dough systems, achieving enhanced water absorption and mixing tolerance that traditional wheat flour cannot deliver.

Increasing Demand for Plant-Based and High-Protein Food Products

The plant-based protein revolution is fundamentally reshaping wheat gluten demand patterns, with meat substitute applications experiencing the highest growth rates across all market segments. Consumer acceptance of wheat-based proteins in athletic nutrition is expanding, with research identifying common wheat (Triticum aestivum) among the 52 plant taxa most frequently used in sports nutrition products, reflecting growing recognition of plant proteins' performance benefits. Regulatory frameworks in Asia-Pacific markets are accelerating adoption, with Singapore's Food Agency and Australia's FSANZ establishing streamlined approval processes for novel protein applications that include wheat-based alternatives. The protein's cost-effectiveness compared to other plant proteins creates competitive advantages in price-sensitive markets, while its established GRAS status eliminates regulatory barriers that constrain newer protein sources. European Union regulations supporting alternative protein commercialization are expected to drive further innovation in wheat gluten applications, particularly in hybrid products combining multiple plant protein sources for enhanced nutritional profiles.

Trend Toward Protein Enrichment in Packaged Foods and Beverages

Food manufacturers are increasingly incorporating wheat gluten into mainstream packaged products to meet consumer demands for higher protein content without compromising taste or texture profiles. The ingredient's neutral flavor profile and excellent solubility make it particularly suitable for beverage fortification, where other plant proteins often create undesirable sensory characteristics. Textured wheat flour applications in bakery technology demonstrate how protein enrichment can simultaneously improve nutritional value and product functionality. The trend extends beyond traditional food categories into snack foods and convenience products, where wheat gluten's binding properties enable protein fortification without structural compromises. Regulatory support through FDA's recognition of wheat gluten as a nutrient supplement facilitates widespread adoption across food categories, while manufacturing scalability advantages over newer protein sources ensure cost-effective implementation for mass-market products.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Prevalence of Celiac Disease and Gluten Intolerance | -1.4% | Global, higher impact in developed markets | Long term (≥ 4 years) |

| Wheat Price Volatility and Supply Chain Disruptions | -0.9% | Global | Short term (≤ 2 years) |

| Stringent Regulatory Restrictions and Labeling Requirements | -0.6% | European Union, North America primarily | Medium term (2-4 years) |

| Presence of Viable Alternatives | -0.8% | Global, concentrated in premium segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Prevalence of Celiac Disease and Gluten Intolerance

Celiac disease affects the global population, with higher prevalence rates among first-degree relatives and certain ethnic groups, creating a significant and growing market exclusion for wheat gluten products. According to the Ministry of Health, the number of individuals affected by celiac disease in Italy as of 2023 were Lonbardy-49,278, Lazio-26,854, Campania-25,266, and so on. The condition's increasing recognition and diagnosis rates, particularly in regions transitioning to wheat-based diets, are expanding the gluten-free consumer base beyond medically diagnosed individuals to include those with perceived gluten sensitivity. According to IfD Allensbach, the number of people in Germany who bought gluten-free products in the last 14 days from 2021 to 2023 rose from 2.03 million in 2021 to 2.16 million in 2023. The economic burden of celiac disease, including healthcare costs and dietary restrictions, creates sustained demand for gluten-free alternatives that directly compete with wheat gluten applications.

Wheat Price Volatility and Supply Chain Disruptions

Global wheat markets face persistent volatility driven by geopolitical tensions, climate variability, and trade policy uncertainties that directly impact wheat gluten production costs and availability. USDA projections indicate wheat prices averaging USD 265 per metric ton in 2025-2026, representing continued pressure on input costs for wheat gluten manufacturers, according to the World Bank data [2].Source: United States Department of Agriculture, "World Agricultural Supply and Demand Estimates", usda.govSupply chain analysis reveals that wheat stocks-to-use ratios, while improving to 47% in 2025-2026 compared to historical averages, remain vulnerable to production shocks in major wheat-producing regions, including Russia, Ukraine, and Australia, according to the USDA data [3]Source: United States Department of Agriculture, "USDA projects below-average wheat, corn, sorghum prices for 2025/26 marketing year", www.usda.gov. The concentration of wheat gluten production in specific geographic regions amplifies supply chain risks, with disruptions in key processing centers potentially affecting global availability. Agricultural commodity factors, including U.S. dollar strength, geopolitical tensions, and weather volatility, create ongoing uncertainty for wheat gluten procurement strategies, forcing food manufacturers to consider alternative protein sources with more stable supply chains

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Liquid Segment Gains Momentum Despite Powder's Dominance in the Market

Specialized food processing requirements are driving liquid wheat gluten adoption at 9.62% CAGR through 2031, despite powder form maintaining 67.62% market share in 2025. The liquid segment's growth reflects increasing demand for ready-to-use protein solutions in automated food production systems, where powder reconstitution creates processing inefficiencies and quality control challenges. Industrial bakeries particularly favor liquid wheat gluten for continuous mixing operations, where consistent protein dispersion eliminates the variability associated with powder hydration and reduces labor costs. The adoption of liquid wheat gluten is further accelerated by manufacturers seeking to minimize production downtime and improve batch-to-batch consistency in large-scale operations.

Powder wheat gluten continues dominating through cost advantages and storage stability that align with traditional food manufacturing practices, while liquid formulations command premium pricing due to specialized processing requirements and shorter shelf life. The powder segment benefits from established distribution networks and packaging infrastructure optimized for bulk ingredient handling, creating barriers to liquid segment expansion in price-sensitive applications. However, emerging applications in ready-to-eat products and convenience foods favor liquid formulations that integrate seamlessly into existing production lines without additional processing steps. The market dynamics are shifting as food manufacturers increasingly prioritize operational efficiency over raw material costs, driving investment in liquid wheat gluten handling systems.

By Nature: Organic Growth Accelerates Amid Clean Label Demands

Clean label positioning drives organic wheat gluten growth at 10.06% CAGR through 2031, while conventional products maintain 89.12% market share in 2025 through established supply chains and cost competitiveness. Organic certification requirements create supply constraints that limit market expansion but enable premium pricing strategies that offset volume limitations. The organic segment particularly benefits from European and North American markets where regulatory frameworks support organic claims and consumer willingness to pay premiums for certified ingredients. The growing consumer preference for clean-label and organic products in these regions continues to drive manufacturers toward organic wheat gluten sourcing despite the supply limitations.

Conventional wheat gluten maintains dominance through industrial-scale applications where organic certification provides a limited value proposition, particularly in animal feed and technical applications where functional properties outweigh organic positioning. Supply chain analysis reveals that organic wheat production constraints limit ingredient availability, creating procurement challenges for large-scale food manufacturers requiring consistent volumes. The conventional segment's established processing infrastructure and quality control systems provide reliability advantages that organic suppliers struggle to match at comparable scales. The extensive global network of conventional wheat producers ensures a stable supply chain that supports the growing industrial demand for wheat gluten.

By Application: Meat Substitutes Drive Innovation Beyond Bakery Stronghold

Meat substitute applications emerge as the fastest-growing segment at 9.88% CAGR through 2031, challenging bakery and confectionery's 40.58% market share dominance in 2025. Plant-based protein adoption is fundamentally reshaping application priorities, with seitan and hybrid meat analogs requiring specialized wheat protein functionality that commands premium pricing compared to traditional bakery applications. The segment benefits from regulatory support in Asia-Pacific markets, where streamlined approval processes for alternative proteins accelerate product development and market entry. The growing consumer preference for clean-label and sustainable protein sources further strengthens wheat gluten's position in the plant-based segment.

Bakery and confectionery applications maintain market leadership through established consumption patterns and industrial-scale processing infrastructure that creates switching costs for alternative ingredients. Other applications, including technical uses and biodegradable materials, represent nascent opportunities where wheat gluten's unique properties create differentiation advantages over conventional protein sources. The versatility of wheat gluten in improving texture, moisture retention, and shelf life continues to drive its adoption across diverse food applications.

Geography Analysis

North America maintains market leadership with a 34.12% share in 2025, supported by advanced food processing infrastructure and high per-capita bakery consumption that creates sustained demand for wheat gluten across multiple applications. The region benefits from established supply chains connecting major wheat-producing areas with processing facilities, while regulatory frameworks, including the FDA's GRAS status for wheat gluten, facilitate widespread adoption across food categories. Industrial bakery consolidation in North America creates opportunities for specialized wheat protein suppliers who can meet large-scale quality and consistency requirements that smaller processors cannot match.

Asia-Pacific emerges as the fastest-growing region at 9.44% CAGR through 2031, driven by rising protein consumption, expanding middle-class populations, and increasing adoption of Western dietary patterns across China, India, and Southeast Asian markets, according to the Australian Government data. Regulatory frameworks in key markets, including Singapore and Australia, are establishing streamlined approval processes for alternative proteins that include wheat-based applications, reducing barriers to market entry for innovative products. These supportive regulatory environments are encouraging manufacturers to develop new wheat gluten-based products, particularly in the meat substitute and protein-enriched food segments.

Europe represents a mature market with established organic and clean-label preferences that favor premium wheat gluten applications, while South America and Middle East & Africa show emerging growth potential driven by expanding food processing industries and increasing protein consumption. Regional trade dynamics, including Brexit impacts and EU regulatory harmonization, continue shaping competitive positioning, while emerging markets in Latin America and Africa present growth opportunities for cost-effective protein solutions that wheat gluten can uniquely provide. The increasing adoption of Western dietary patterns in these regions is further accelerating the demand for wheat gluten in various food applications.

Competitive Landscape

The wheat gluten market exhibits moderate fragmentation, indicating significant opportunities for both established players and specialized suppliers to capture market share through differentiated product offerings and targeted application focus. Major players, including Manildra Group, Cargill Incorporated, Archer Daniels Midland Company, Roquette Frères, and Tereos SCA, leverage integrated supply chains and processing scale to maintain cost leadership, while mid-tier specialists like MGP Ingredients focus on high-value protein isolates and customized formulations that command premium pricing.

Competitive dynamics increasingly favor companies with technical expertise in protein modification and application development, as customers seek specialized solutions beyond commodity wheat gluten. Strategic patterns reveal increasing emphasis on sustainability initiatives and clean-label positioning, with companies investing in organic certification and transparent supply chain documentation to meet evolving customer requirements. The market's growth trajectory is further strengthened by manufacturers developing customized wheat gluten solutions that address specific functional requirements across diverse applications.

Technology adoption focuses on protein functionality enhancement and processing efficiency improvements, with companies developing proprietary modification techniques that create intellectual property barriers and customer lock-in effects. White-space opportunities exist in emerging applications, including biodegradable materials and specialized nutrition products, where wheat gluten's unique properties can command premium pricing compared to traditional food applications. The integration of advanced processing technologies enables manufacturers to optimize wheat gluten's functional properties, resulting in higher-value products that meet specific industry demands.

Wheat Gluten Industry Leaders

-

Manildra Group

-

Cargill, Incorporated

-

Archer-Daniels-Midland

-

Roquette Frères

-

Tereos SCA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Tritica Biosciences launched the Wheat-Based Protein Synthesis platform. Tritica Biosciences LLC, along with three partners, collaborated with Ginkgo Bioworks of Boston on a USD 29 million contract with the Advanced Research Projects Agency for Health (ARPA-H). The contract spans two years.

- April 2025: ACI Group introduced high-performance plant-based proteins to help manufacturers address changing consumer dietary preferences. The product range includes wheat protein crispies and serves multiple applications, including dairy alternatives, beverages, desserts, and meat substitutes. The proteins enable manufacturers to achieve specific formulation requirements including neutral flavor profiles, increased protein content, enhanced texture, and clean-label characteristics.

- November 2023: Amber Wave launched a wheat protein facility with investment from Summit Agricultural Group. The facility features a fully automated 27,500-centum Sangati Berga mill, automation technology and air handling systems from Kice Industries, gluten extraction and drying equipment from Flottweg and VetterTec, and packaging equipment from Premier Tech.

- August 2023: Lantmännen Biorefineries opened its new wheat protein (gluten) extraction facility in Norrköping, Sweden, with an investment of SEK 800 million (USD 73.95 million). The facility increases production capacity to address growing market demand.

Global Wheat Gluten Market Report Scope

Wheat gluten is composed of mainly two types of proteins, i.e., glutenins and gliadins. The wheat gluten market is segmented by form into liquid and powder, and by application, the market is segmented into bakery & confectionery, supplements, animal feed, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, Middle East & Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

| Liquid |

| Powder |

| Conventional |

| Organic |

| Bakery and Confectionery |

| Supplements and Sports Nutrition |

| Animal Feed and Pet Food |

| Meat Substitutes |

| Other Application |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Form | Liquid | |

| Powder | ||

| By Nature | Conventional | |

| Organic | ||

| By Application | Bakery and Confectionery | |

| Supplements and Sports Nutrition | ||

| Animal Feed and Pet Food | ||

| Meat Substitutes | ||

| Other Application | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the wheat gluten market?

The wheat gluten market stands at USD 12.18 billion in 2026 and is projected to reach USD 17.7 billion by 2031.

Which region leads global demand?

North America commands 34.12% of 2025 revenue thanks to entrenched bakery consumption and robust processing infrastructure.

Why is liquid wheat gluten gaining popularity?

Liquid formats simplify dosing in automated lines, cut labor, and support continuous mixing, driving a 9.62% CAGR through 2031.

How fast is the meat-substitute segment growing?

Meat analogs using wheat gluten are forecast to climb at a 9.88% CAGR between 2026 and 2031, the fastest among applications.

Page last updated on: