Market Overview

| Study Period | 2021 - 2031 |

|---|---|

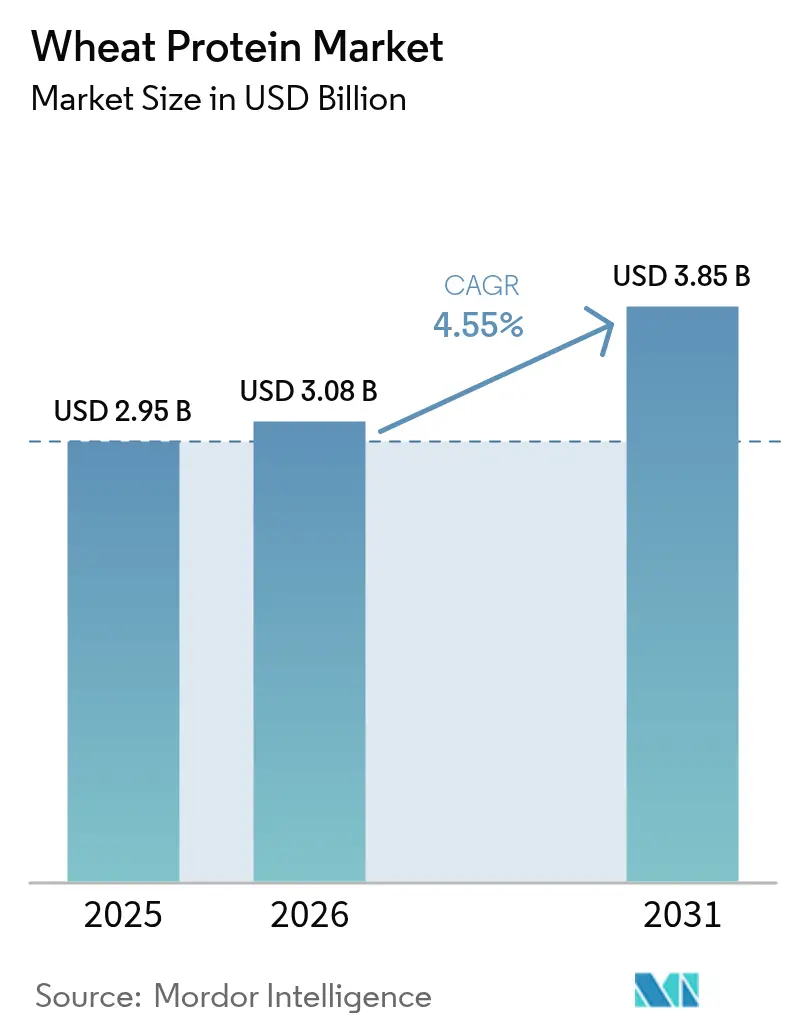

| Market Size (2026) | USD 3.08 Billion |

| Market Size (2031) | USD 3.85 Billion |

| Growth Rate (2026 - 2031) | 4.55% CAGR |

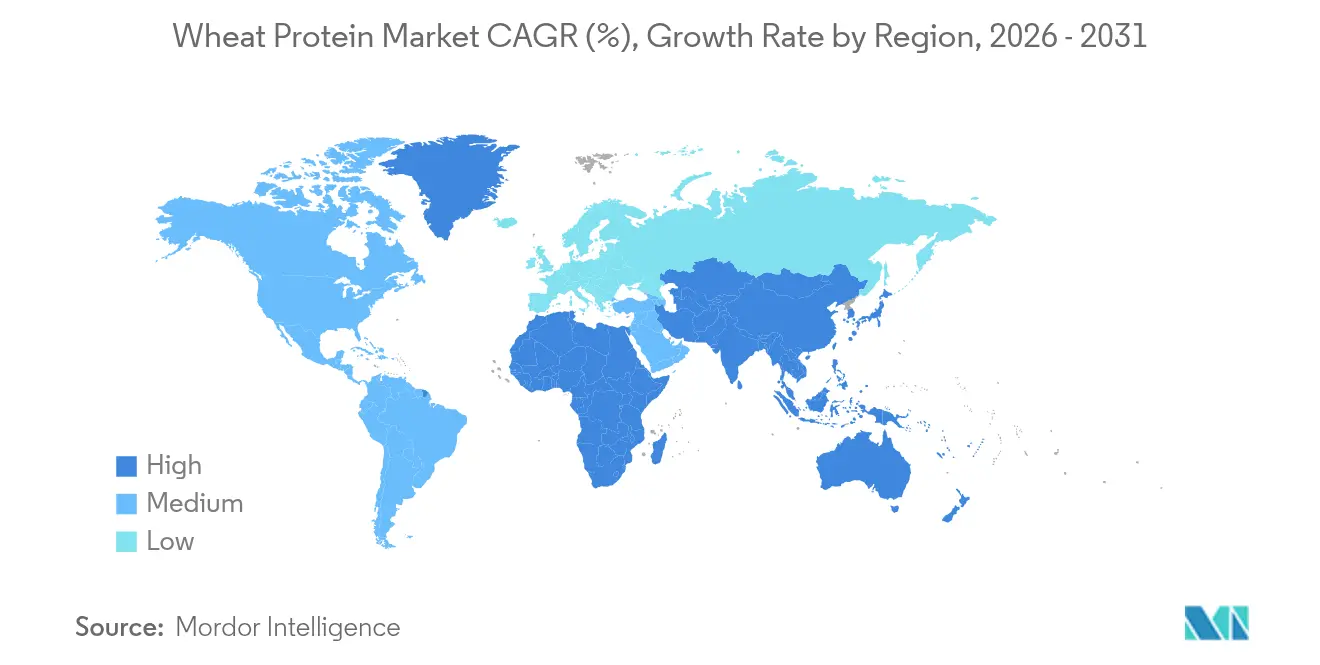

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Wheat Protein Market Analysis by Mordor Intelligence

The wheat protein market size is expected to grow from USD 2.95 billion in 2025 to USD 3.08 billion in 2026 and is forecast to reach USD 3.85 billion by 2031 at 4.55% CAGR over 2026-2031. Adoption is pivoting toward higher-margin applications—organic, non-GMO and functional isolates—while supply chain volatility and persistently tight gluten-free regulations temper headline growth. Consumer interest in protein fortification, clean label claims and plant-based foods keeps volume demand resilient even as processors confront wheat price cycles and logistics risk. Premium segments—such as organic isolates—show faster uptake despite modest volumes, illustrating how value creation is shifting from commodity sales to differentiated solutions. Europe retains scale leadership through entrenched bakery traditions and rigorous quality norms, whereas Asia-Pacific advances the fastest as alternative protein policies gain traction and urban diets diversify.

Key Report Takeaways

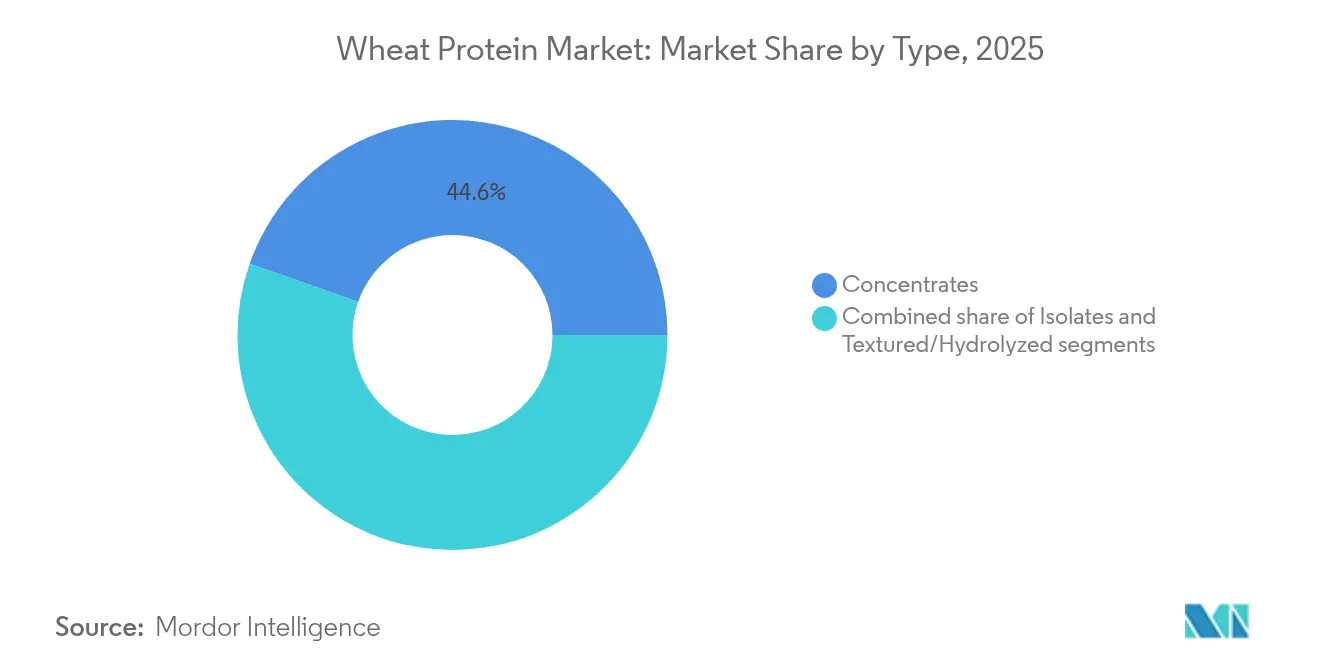

- By type, concentrates led with 44.62% of the wheat protein market share in 2025, while isolates posted the highest 6.42% CAGR over the same period.

- By nature, conventional products captured 89.12% share in 2025; organic wheat protein expands at 8.47% CAGR to 2031.

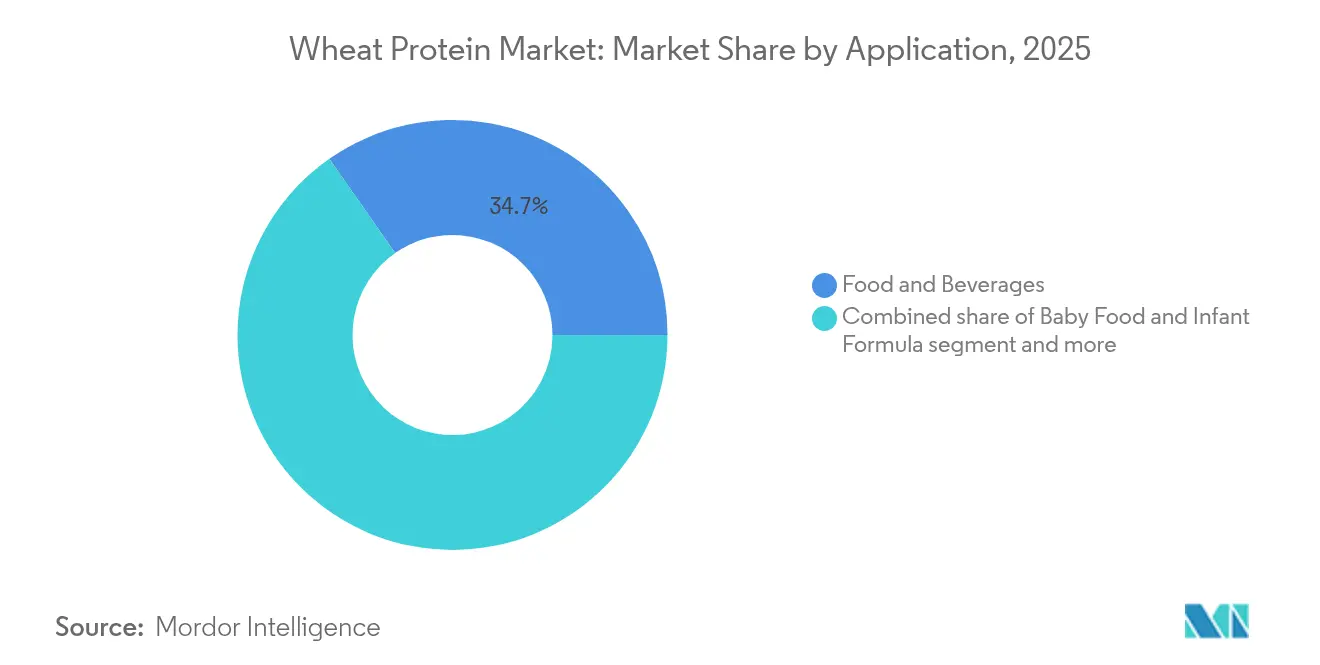

- By application, food and beverages held a 34.71% share of the wheat protein market size in 2025, whereas sports and functional nutrition are projected to rise at 7.88% CAGR through 2031.

- By geography, Europe commanded 33.68% of the wheat protein market in 2025; Asia-Pacific is poised for a 7.12% CAGR by 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wheat Protein Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for high-protein bakery products | +1.2% | North America, Europe | Medium term (2-4 years) |

| Surge in demand for clean label and natural ingredients | +1.0% | North America, Europe | Long term (≥ 4 years) |

| Rising demand for plant-based proteins in meat alternatives | +0.8% | Asia-Pacific, Global | Medium term (2-4 years) |

| Growing application in sports and nutritional supplements | +0.7% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Growing preference for Non-GMO ingredient declarations | +0.5% | North America, Europe | Long term (≥ 4 years) |

| Growing adoption of wheat protein in animal feed and pet food | +0.4% | Global, led by North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for High-Protein Bakery Products

Wheat protein enhances dough structure and increases protein content, enabling manufacturers to remove synthetic conditioners while maintaining product volume and texture. The protein's molecular structure forms a strong gluten network that traps gas bubbles during fermentation, resulting in improved bread volume and crumb structure. Oklahoma State University has developed high-strength wheat varieties—Paradox, Breadbox, and Firebox—demonstrating agricultural innovations that favor natural texturizing agents over chemical additives. These varieties contain higher protein levels and superior gluten quality compared to conventional wheat. Ingredient manufacturers offer wheat protein concentrates and isolates that maintain dough elasticity, providing both functional and nutritional benefits. The proteins can be customized for specific applications, from bread and pastries to pasta and snacks. This dual functionality supports higher pricing in artisanal bread products and healthier snack options, as consumers increasingly seek clean-label alternatives with enhanced nutritional profiles.

Surge in Demand for Clean Label and Natural Ingredients

The clean label movement has evolved from marketing preference to regulatory necessity, with 11% of people in the United States following clean eating habits, according to the International Food Information Council data from 2024 [1]Source: International Food Information Council, "Type of Eating Pattern or Diet Followed", hific.org. This consumer sentiment translates into procurement mandates for food manufacturers seeking to eliminate synthetic additives and preservatives from formulations. Wheat protein's inherent functionality in water binding, emulsification, and gel formation positions it as a natural replacement for chemical processing aids, particularly in applications where protein content and clean label status create competitive differentiation. The FDA's gluten-free labeling regulations, requiring products to contain less than 20 ppm of gluten, paradoxically drive demand for wheat protein in non-gluten-free applications where its functional properties can be fully utilized, according to the Food and Drug Administration.

Rising Demand for Plant-Based Proteins in Plant-Based Meat Alternatives

Alternative protein development in Asia-Pacific has gained momentum comparable to the clean energy transition, with wheat protein serving as a foundational ingredient in meat analog formulations. Wheat gluten's unique viscoelastic properties enable the creation of fibrous textures that closely mimic animal muscle structure, making it indispensable in products like seitan and hybrid meat alternatives. The challenge lies in wheat protein's functional limitations compared to animal proteins, particularly in terms of amino acid completeness and digestibility, which drives innovation in protein blending and processing technologies. Cargill's partnership expansion with ENOUGH to scale mycoprotein production to over 1 million tons by 2033 illustrates how established players are diversifying protein portfolios while maintaining wheat protein as a core component. The plant-based meat segment's growth creates sustained demand for wheat protein isolates and textured variants, though success depends on continued innovation in processing techniques that enhance nutritional profiles and sensory attributes.

Growing Application in Sports and Nutritional Supplements

Sports and nutritional supplement consumption are rising due to increased sports participation and active lifestyles worldwide. This growth is particularly evident in developed regions where health consciousness and fitness activities have become integral parts of daily routines. According to Sports England data from 2024, 6,695.5 thousand people in England attended fitness classes twice a month, demonstrating the significant market potential [2]Source: Sports England, "Sports Participation in England", sportsengland.com. Owing to this, the use of wheat protein in sports nutrition supplements is increasing. Wheat protein benefits from an established supply chain and favorable cost structure, making it suitable for mass-market sports nutrition products that cannot sustain premium pricing. The efficient production processes and widespread availability of wheat as a raw material contribute to its competitive advantage in the market. The segment's growth depends on processing innovation that enhances wheat protein's solubility and digestibility while preserving its clean label characteristics. These improvements are essential for meeting consumer demands for high-quality, natural protein supplements that deliver optimal nutritional benefits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prevalence of Celiac Disease and Gluten Sensitivity | -0.8% | Global, with higher impact in North America & Europe | Long term (≥ 4 years) |

| Availability and Preference for Other Plant-Based Proteins | -0.6% | Global, with Asia-Pacific showing diverse protein adoption | Medium term (2-4 years) |

| Fluctuating Raw Material Prices | -0.5% | Global, with particular impact on price-sensitive markets | Short term (≤ 2 years) |

| Functional Limitations Compared to Animal Protein | -0.4% | Global, affecting premium applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Prevalence of Celiac Disease and Gluten Sensitivity

According to the Australian Broadcasting Corporation data from 2024, 1 in 70 people in Australia had celiac disease [3]Source: Australia Broadcasting Corporation, "Prevalence of Celiac Disease in Australia", abc.net.au. The FDA's gluten-free labeling requirements limit gluten content to less than 20 ppm, preventing wheat protein use in products for gluten-sensitive consumers. This regulation creates a permanent demand constraint that processing innovations cannot address. The restriction affects product development, formulation strategies, and manufacturing processes across the food industry. While the growing global market for gluten-free products reduces wheat protein applications, it also consolidates wheat protein demand in traditional segments where its functional properties remain essential. These segments include bakery products, pasta, and processed meat applications, where gluten's unique viscoelastic properties are crucial for product quality. Wheat protein manufacturers operate within these regulatory boundaries by focusing on applications where gluten functionality delivers unique value, particularly in conventional food products that rely on wheat protein's binding, texturizing, and structure-building capabilities.

Fluctuating Raw Material Prices

Wheat price volatility creates margin compression for protein processors, with the World Bank projecting wheat prices at USD 265 per metric ton in 2025-2026, representing a USD 55.65 decline from 2024 levels, according to the World Bank data. This price decline, while potentially stimulating downstream demand, creates procurement planning challenges for wheat protein manufacturers who must balance inventory costs against price risk exposure. Geopolitical factors, including the ongoing Ukraine conflict and trade policy uncertainties, introduce additional volatility that complicates long-term supply agreements and pricing strategies. The USDA's projection of wheat stocks-to-use ratios at 47% for 2025/26, above the 16-year average of 41%, suggests continued price pressure that could benefit wheat protein demand while challenging processor profitability. Successful wheat protein companies are implementing hedging strategies and diversifying supply sources to mitigate price volatility impacts while maintaining competitive positioning in price-sensitive market segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Concentrates Dominate Through Cost Efficiency

Wheat protein concentrates command a 44.62% market share in 2025, leveraging their cost-effectiveness in high-volume food applications where moderate protein content meets functional requirements without premium pricing constraints. The segment's dominance reflects the food industry's pragmatic approach to protein fortification, where concentrates provide sufficient functionality for bakery applications, processed foods, and animal feed formulations at price points that maintain mass-market accessibility. Isolates represent the fastest-growing segment at 6.42% CAGR through 2031, driven by specialized applications in sports nutrition, infant formula, and premium food products where higher protein purity justifies cost premiums.

The segment dynamics reflect broader industry trends toward functional differentiation, with companies like MGP Ingredients strategically migrating sales toward higher-margin specialty wheat products, including their Arise® and Proterra® lines. Processing technology advances enable isolated production with protein content exceeding 83%, as demonstrated by Roquette's VITEN® product line, creating opportunities for premium positioning in applications where protein density drives value creation

By Nature: Organic Acceleration Despite Conventional Dominance

Conventional wheat protein maintains an 89.12% market share in 2025, reflecting its dominance due to established supply chains, cost competitiveness, and proven functionality across diverse applications where organic certification does not command sufficient premiums to justify higher input costs. The segment's sustainability depends on continued consumer demand for organic products and successful farmer transition programs that expand organic wheat production capacity.

Organic wheat protein accelerates at a 8.47% CAGR through 2031 despite conventional products dominating the market, reflecting the premium segment's rapid expansion as U.S. organic wheat production rebounded 22% to 24.41 million bushels in the 2023–24 marketing year, according to the United States Department of Agriculture. The USDA's announcement of USD 10 million in funding to support organic producer transitions indicates government recognition of organic agriculture's strategic importance, potentially expanding organic wheat protein supply in future periods.

By Application: Sports Nutrition Leads Growth While Bakery Maintains Market Dominance

The food and beverages segment maintains its market leadership position with a 34.71% share in 2025, supported by well-established supply chain networks and documented functional benefits in various baked goods applications. Sports and functional nutrition applications are experiencing significant growth at 7.88% CAGR through 2031, driven by increasing consumer demand for protein-enriched performance products. Baby food and infant formula segments require specific processing methods and quality controls to ensure proper digestibility, nutrient absorption, and safety standards. The elderly nutrition and medical nutrition segments focus on specialized protein formulations that meet distinct metabolic needs and address age-related nutritional requirements.

Wheat protein demonstrates exceptional adaptability across various applications, serving both basic binding functions in processed foods and fulfilling complex nutritional requirements in specialized products. The protein's functional properties enable it to act as an effective emulsifier, stabilizer, and texture modifier in different food systems. The animal feed segment provides consistent volume through regular demand cycles but shows limited growth prospects due to competition from alternative protein sources. Personal care and cosmetics emerge as promising opportunities, utilizing wheat protein's film-forming capabilities and moisture-retention properties for non-nutritional applications in skincare and haircare products.

Geography Analysis

In 2025, Europe holds the largest market share at 33.68%, supported by advanced food processing infrastructure, strict EFSA regulations, and a focus on quality and safety. These regulations drive innovation in areas like fortified bakery, premium meat alternatives, and clinical nutrition. Rising demand for plant-based products with functional benefits is pushing wheat protein into high-value segments. Companies are differentiating through proprietary technologies and partnerships with health and wellness brands to enhance market penetration.

The Asia-Pacific region is the fastest-growing market, with a projected 7.12% CAGR through 2031. Growth is driven by food security concerns, a growing middle class, and government initiatives promoting alternative proteins for nutrition and sustainability. Countries like China, India, and Southeast Asia are adopting wheat protein in processed foods due to its affordability and versatility. Governments are investing in food-tech R&D, expanding plant protein infrastructure, and encouraging private-sector collaborations to reduce reliance on animal protein and meet climate goals. Domestic food processors are also driving demand for cost-effective, localized protein sources.

The Middle East and Africa represent emerging opportunities where population growth and dietary diversification drive protein demand, though infrastructure limitations constrain market development in some areas. Regional wheat protein trade patterns are evolving in response to geopolitical tensions, with the Ukraine conflict demonstrating supply chain resilience as global wheat shipments withstood initial disruptions through supplier diversification and strategic stockpile utilization. The geographic distribution of wheat protein demand increasingly reflects local food culture integration, with Asian fermentation traditions creating unique applications for wheat protein in traditional and modern food products.

Competitive Landscape

The wheat protein market exhibits moderate fragmentation, characterized by a balance of established global ingredients companies and specialized protein manufacturers competing across multiple application segments. Major players in the market include Archer Daniels Midland Company, Cargill, Incorporated, Roquette Frères, MGP Ingredients, Inc., and Kerry Group plc. Strategic differentiation centers on processing technology advancement, with leaders like Cargill investing in proprietary processes that enhance the functional properties of wheat proteins for specific applications.

Vertical integration is emerging as a competitive advantage, with companies controlling the value chain from wheat sourcing to protein fractionation, achieving superior cost positions and quality control. White space opportunities exist primarily in specialized application development, particularly in the personal care sector, where hydrolyzed wheat proteins are gaining traction for their moisturizing and conditioning properties.

Technology deployment is increasingly central to competitive strategy, with artificial intelligence applications accelerating ingredient discovery and formulation optimization, potentially disrupting traditional R&D timelines and enabling smaller players to compete through innovation agility rather than scale advantages.

Wheat Protein Industry Leaders

-

Archer Daniels Midland Company

-

Cargill, Incorporated

-

Roquette Frères

-

MGP Ingredients, Inc.

-

Kerry Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: ACI Group introduced high-performance plant-based proteins to help manufacturers address changing consumer dietary preferences. The product range includes wheat protein crispies and serves multiple applications, including dairy alternatives, beverages, desserts, and meat substitutes. The proteins enable manufacturers to achieve specific formulation requirements including neutral flavor profiles, increased protein content, enhanced texture, and clean-label characteristics.

- April 2025: Tritica Biosciences launched the Wheat-Based Protein Synthesis platform. Tritica Biosciences LLC, along with three partners, collaborated with Ginkgo Bioworks of Boston on a USD 29 million contract with the Advanced Research Projects Agency for Health (ARPA-H). The contract spans two years.

- August 2024: Wheat processor Crespel & Deiters invested USD 20.7 million in constructing a silo building at its main site in Ibbenbüren, Germany. The new facility expands the company's storage and handling capacities while strengthening its value chain and global operational flexibility.

- November 2023: Amber Wave launched a wheat protein facility with investment from Summit Agricultural Group. The facility features a fully automated 27,500-centum Sangati Berga mill, automation technology and air handling systems from Kice Industries, gluten extraction and drying equipment from Flottweg and VetterTec, and packaging equipment from Premier Tech.

Global Wheat Protein Market Report Scope

Wheat protein is one of the plant proteins (along with soy) most commonly used for various applications. Wheat Protein is the natural protein derived from wheat or wheat flour.

The market studied is segmented by type into concentrates, isolates, and textured/hydrolyzed. By form, the market is segmented into dry and liquid. By nature, the market is segmented into organic and conventional. By end-user, the market is segmented into animal feed, personal care & cosmetics, and food & beverages. Food and beverages are further segmented into bakery, breakfast cereals, condiments/sauces, confectionery, meat/poultry/seafood, and meat alternatives. By distribution channels, the market is segmented into business-to-business and business-to-consumer. The latter segment is further segmented into supermarkets & hypermarkets, specialty stores, and online retail. The market is segmented by geography into North America, Europe, Asia, South America, the Middle East, Africa, and Oceania.

The market sizing has been done in value terms in USD for all the abovementioned segments.

By Type

| Concentrates |

| Isolates |

| Textured/Hydrolyzed |

By Nature

| Conventional |

| Organic |

By Application

| Food and Beverages | Bakery and Snacks |

| Breakfast Cereals | |

| Meat/Poultry/Seafood and Meat Alternative Products | |

| RTE/RTC Food Products | |

| Condiments/Sauces | |

| Sport/Performance Nutrition | |

| Baby Food and Infant Formula | |

| Elderly Nutrition and Medical Nutrition | |

| Animal Feed | |

| Personal Care and Cosmetics |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Concentrates | |

| Isolates | ||

| Textured/Hydrolyzed | ||

| By Nature | Conventional | |

| Organic | ||

| By Application | Food and Beverages | Bakery and Snacks |

| Breakfast Cereals | ||

| Meat/Poultry/Seafood and Meat Alternative Products | ||

| RTE/RTC Food Products | ||

| Condiments/Sauces | ||

| Sport/Performance Nutrition | ||

| Baby Food and Infant Formula | ||

| Elderly Nutrition and Medical Nutrition | ||

| Animal Feed | ||

| Personal Care and Cosmetics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the wheat protein market?

The wheat protein market is worth USD 3.08 billion in 2026 and is projected to reach USD 3.85 billion by 2031.

Which product type leads the market?

Concentrates lead with 44.62% share in 2025 owing to their cost-efficiency in high-volume bakery and snack applications.

Which application is growing the fastest?

Sports and functional nutrition is expanding at an 7.88% CAGR through 2031 as consumers switch to plant-based performance products.

Why is Asia-Pacific the fastest-growing region?

Policy support for alternative proteins and rising urban incomes drive a 7.12% CAGR for the region’s wheat protein demand.

Page last updated on: