Specialty Malt Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

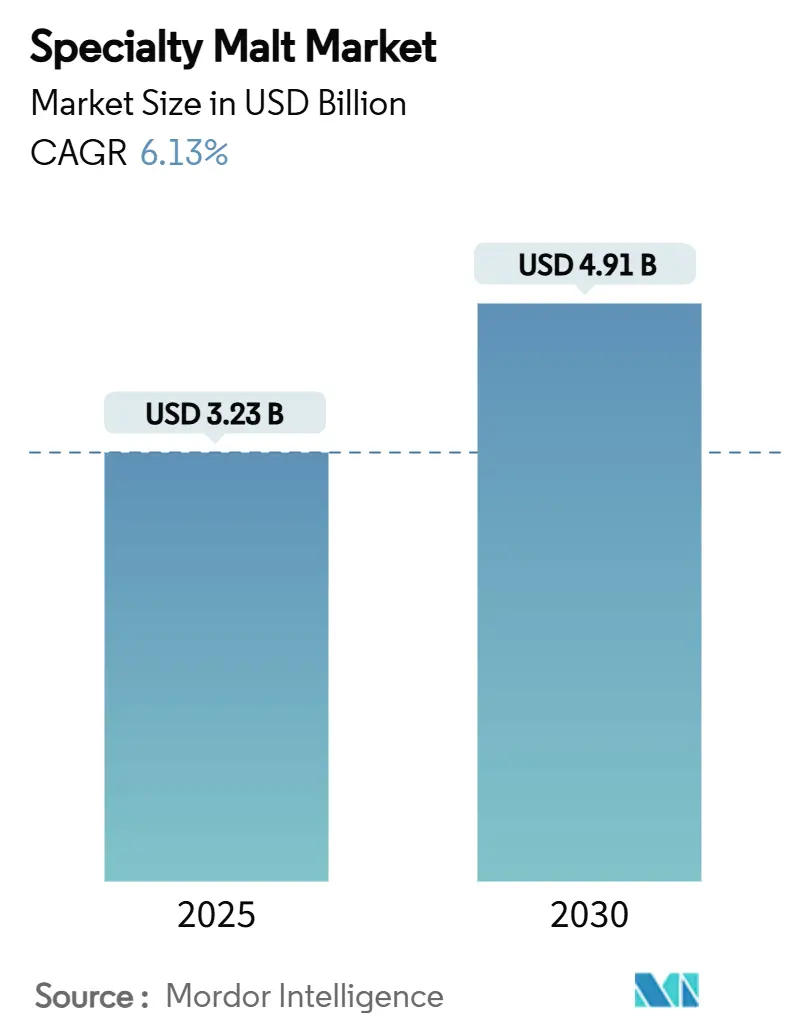

| Market Size (2025) | USD 3.23 Billion |

| Market Size (2030) | USD 4.91 Billion |

| Growth Rate (2025 - 2030) | 6.13% CAGR |

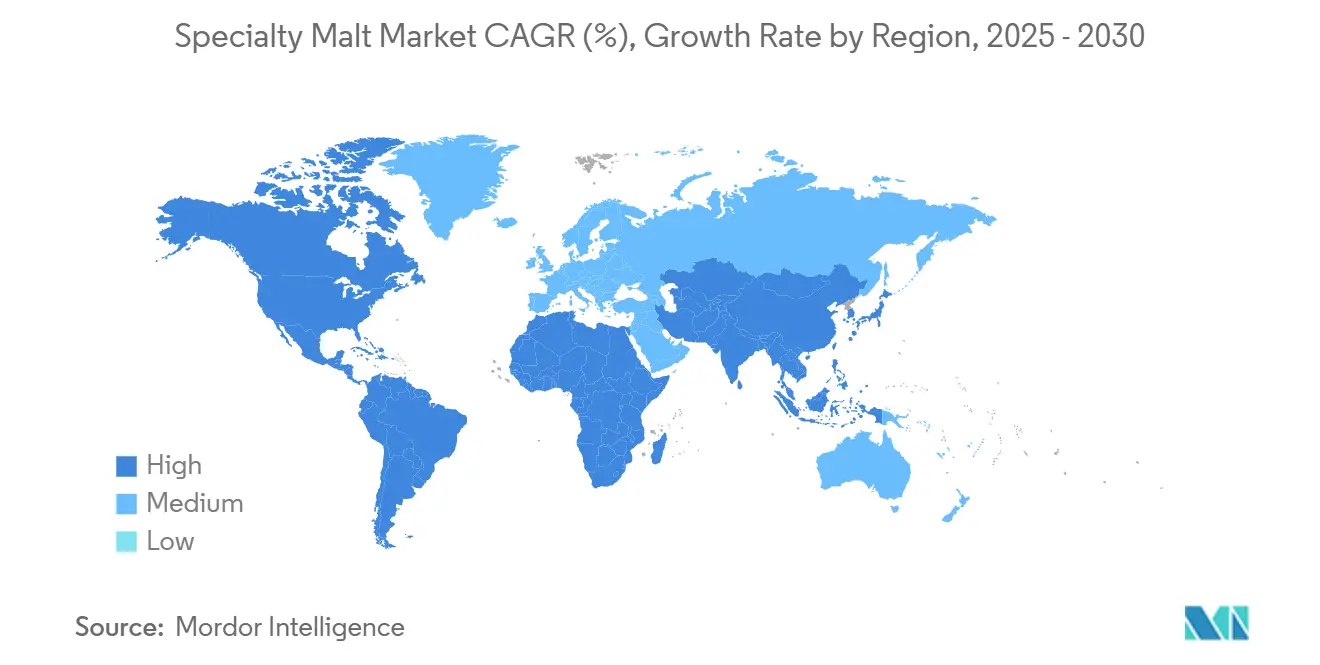

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Specialty Malt Market Analysis by Mordor Intelligence

The specialty malt market size is expected to grow from USD 3.23 billion in 2025 to USD 4.91 billion by 2030, at a CAGR of 6.13%. This growth is primarily driven by increased demand from craft brewers seeking flavor-enhanced grains, expanding non-alcoholic beer production volumes, and the rapid adoption of malt ingredients in plant-based dairy products. Europe remains the primary market due to its established brewing heritage and traditions, while the Asia-Pacific region demonstrates significant growth potential through regulatory changes that enable capacity expansion and premium product development opportunities. To effectively manage barley price volatility, manufacturers are actively diversifying their raw material sources to include oats, rice, and other alternative grains, while simultaneously implementing regenerative agriculture initiatives to secure supply chains and meet carbon reduction targets. Additionally, increased monitoring of acrylamide and other contaminants has led manufacturers to enhance their process control measures and comprehensive testing protocols to maintain distinctive flavor profiles while ensuring strict regulatory compliance.

Key Report Takeaways

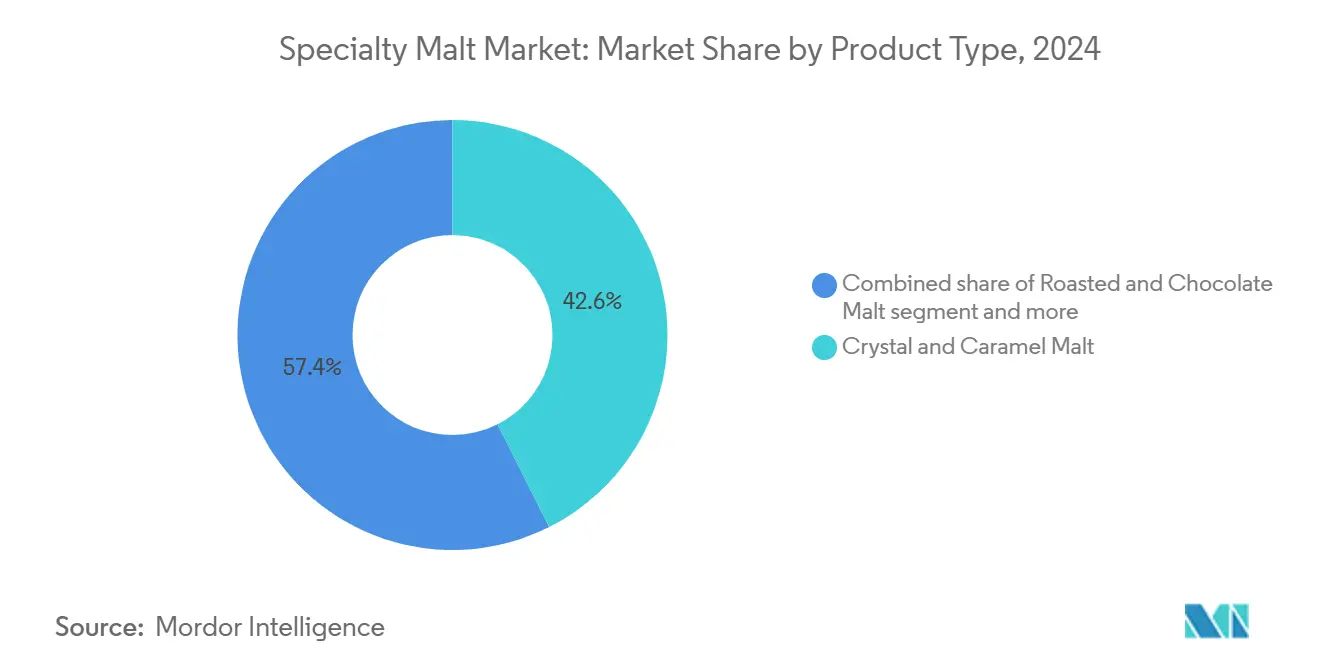

- By product type, crystal and caramel malts led with 42.58% of the specialty malt market share in 2024, while roasted and chocolate malts are on track for the fastest 7.33% CAGR through 2030.

- By source grain, barley retained a 66.19% slice of the specialty malt market size in 2024, yet oats are forecast to grow at an 8.52% CAGR through 2030.

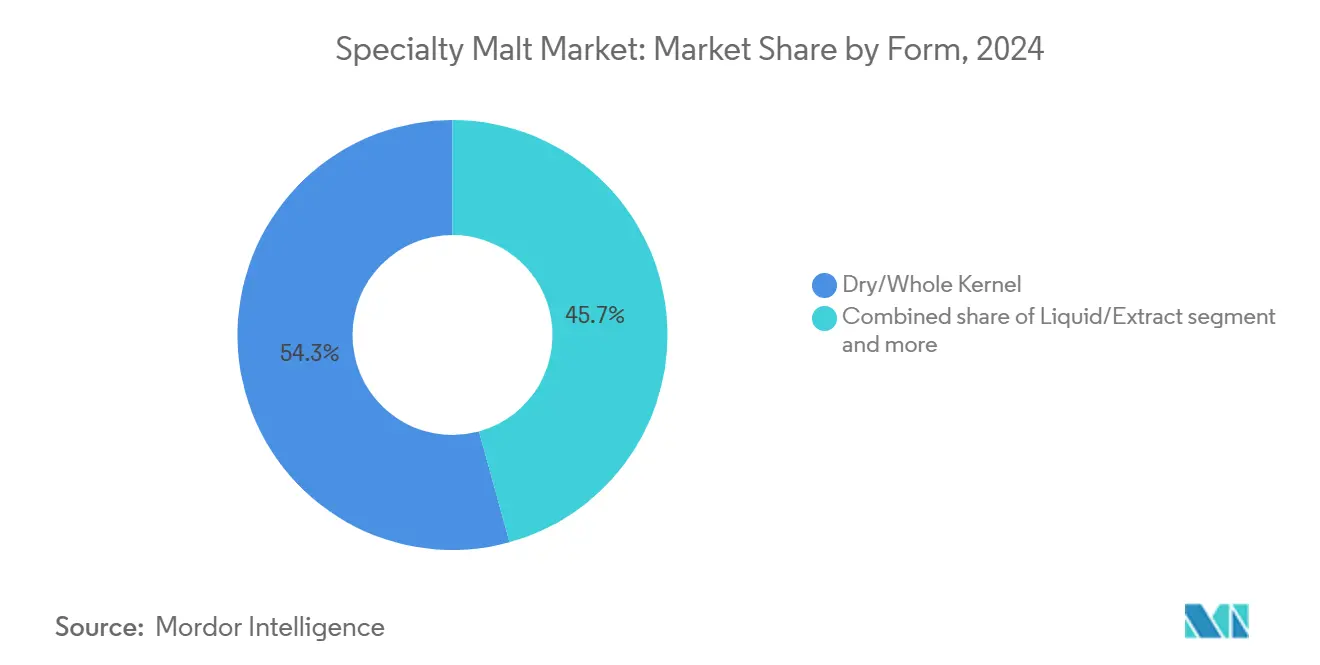

- By form, dry/whole-kernel formats captured 54.27% revenue in 2024; liquid/extracts are projected to advance at a 9.15% CAGR during 2025-2030.

- By application, brewing dominated with 72.08% share in 2024, whereas plant-based dairy analogues are poised for a 9.83% CAGR between 2025-2030.

- By geography, Europe secured 34.25% of global value in 2024; Asia-Pacific is set to register the fastest 9.61% CAGR through 2030.

Global Specialty Malt Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosion of the craft brewing industry | +1.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Gluten-free brewing is gaining mainstream shelf presence | +0.9% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Expanding non-alcoholic and functional beverage segment | +1.2% | Global, led by Europe and North America | Short term (≤ 2 years) |

| Artisanal bakery demand is boosting the use of flavor-rich malt flours | +0.7% | Europe and North America, emerging in Asia-Pacific | Medium term (2-4 years) |

| Shift toward organic and non-GMO specialty malts | +0.6% | North America and Europe, with premium positioning | Long term (≥ 4 years) |

| Adoption of regenerative barley and carbon-neutral malt programs | +0.5% | Global, with early adoption in Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosion of the craft brewing industry

The growth of the craft brewing industry has become a significant driver of the specialty malt market, changing both demand patterns and product development. Consumer preferences have shifted from mass-produced lagers toward distinct flavors and craft beer experiences offered by independent breweries. To create unique products, craft brewers use specialty malts, including caramel, chocolate, and smoked varieties, which provide distinct aromas, colors, and textures in their beers. This trend is particularly evident in North America and Europe, where established craft breweries influence malt suppliers to diversify their product range and develop new grain varieties and roasting processes. The expansion of craft beer production has increased both the volume and value of the specialty malt market globally. The rise in microbreweries has created a mutually beneficial relationship, where craft beer's success directly increases specialty malt usage. Consumer demand for local, traceable, and distinctive beers has encouraged malt producers to collaborate with brewers, expand into organic and heritage grains, and develop customized malt profiles for specific market segments.

Gluten-free brewing is gaining mainstream shelf presence

The surge in gluten-free brewing and its ascent into the mainstream has become a significant growth driver for the specialty malt market. As consumer awareness of celiac disease, gluten intolerance, and general wellness trends rises, breweries are adapting their portfolios to include gluten-free options that appeal to both health-conscious and gluten-sensitive demographics. Key beer brands and craft breweries are now prominently positioning their gluten-free products on retail shelves, and this is translating to increased demand for alternative grains such as sorghum, millet, rice, and buckwheat, grains naturally devoid of gluten and frequently processed into specialty malts with unique flavor attributes. The increasing prevalence of celiac disease in North America and Europe drives the demand for gluten-free beer and specialty malt products. In Italy, the Ministero della Salute reported approximately 265,000 individuals with celiac disease in 2023, with Lombardy recording the highest concentration at 49,200 cases[1]Source: Ministero della Salute, "RELAZIONE ANNUALE AL PARLAMENTO SULLA CELIACHIA," static.celiachia.it. These numbers demonstrate the substantial consumer base requiring gluten-free options, prompting brewers and malt producers to adapt their offerings. The specialty malt market has responded by developing products using gluten-free grains, contributing to market growth and product diversification.

Expanding non-alcoholic and functional beverage segment

The non-alcoholic beverage segment's rapid expansion represents a fundamental shift in consumer behavior that transcends demographic boundaries and geographic markets. Health-conscious consumers demonstrate increasing willingness to pay premium prices for products that deliver complex flavors without alcohol content, driving substantial demand for specialty malts that enhance flavor, color, and mouthfeel characteristics. Muntons' introduction of alcohol-free malt extract in 2024 exemplifies how maltsters are developing products specifically formulated for non-alcoholic applications while addressing technical challenges related to flavor development and stability. The segment's expansion into functional beverages creates significant opportunities, as malt extracts provide natural sweetness, protein content, and enzymatic activity that enhance nutritional profiles. Young consumers' growing association of non-alcoholic beers with refreshment and responsible drinking behaviors indicates sustained demand growth, particularly in markets where health and wellness trends influence purchasing decisions.

Artisanal bakery demand is boosting the use of flavor-rich malt flours

Artisanal bakery applications present significant opportunities for specialty malt producers, as premium bread and confectionery manufacturers require ingredients that provide distinct flavor profiles and functional benefits. Studies indicates that malted triticale flour enhances dietary fiber content while improving starch and protein digestibility, offering potential applications in pasta and bakery products. The malting process modifies grain structure and enzyme activity, enabling bakers to develop complex flavors and improve texture characteristics that distinguish artisanal products from mass-produced items. The higher price points of artisanal bakery products support the use of specialty malt flours, despite their processing requirements and lower production volumes. The increasing demand for clean-label ingredients and traditional production methods aligns with specialty malt producers' capabilities, fostering direct partnerships between maltsters and artisanal bakeries.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in barley and grain prices | -1.4% | Global, with acute impact in import-dependent regions | Short term (≤ 2 years) |

| Stricter acrylamide limits in bakery ingredients | -0.8% | Europe and North America, with regulatory spillover effects | Medium term (2-4 years) |

| Higher cost compared to base malts | -0.6% | Global, with price sensitivity in emerging markets | Medium term (2-4 years) |

| Craft-beer consolidation is reducing small-batch malt demand | -0.9% | North America and Europe, with regional variations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in barley and grain prices

Barley price volatility has become the primary constraint on specialty malt market growth, affecting sourcing decisions and product development across the industry. US barley farm prices rose 7.54% year-over-year to USD 7.70 per bushel in 2024, creating significant cost pressures for malt producers and downstream manufacturers. Western Canadian barley production decreased 10% to 7.84 million tonnes due to adverse weather conditions and reduced seeding area, further straining global supply chains. The supply disruption's effect on malt pricing intensified due to quality issues, as heat stress during the 2024 growing season led to lower test weights and smaller kernel sizes, impacting malting performance and extract yields in production facilities. Companies have responded with vertical integration initiatives and long-term supply agreements to secure consistent barley supplies, though these solutions require substantial capital investment and can reduce operational flexibility during market changes. The industry continues to explore alternative sourcing strategies and process optimizations to mitigate the impact of ongoing price volatility.

Stricter acrylamide limits in bakery ingredients

The specialty malt industry faces regulatory challenges regarding acrylamide levels in food products, particularly affecting producers serving bakery and confectionery markets. The European Union's Commission Regulation 2023/915, which took effect in January 2025, sets maximum contaminant levels in cereals, malt, and related food products[2]Source: European Union, "Commission Regulation (EU) 2023/915 of 25 April 2023 on maximum levels for certain contaminants in food and repealing Regulation (EC) No 1881/2006 (Text with EEA relevance)," europa.eu. The regulation includes specific provisions for cadmium levels in beer production, allowing exemptions when cereal residue is not sold as food. While the regulation focuses on cadmium, it indicates increased regulatory oversight of contaminants in grain-based ingredients. Acrylamide formation during roasting and kilning processes has emerged as a significant concern for specialty malt producers. The FDA's Good Manufacturing Practice regulations under 21 CFR Part 117 require food facilities to implement hazard analysis and preventive controls, including monitoring of chemical contaminants[3]Source: Code of Federal Regulations, "PART 117—CURRENT GOOD MANUFACTURING PRACTICE, HAZARD ANALYSIS, AND RISK-BASED PREVENTIVE CONTROLS FOR HUMAN FOOD," ecfr.gov. To achieve compliance, producers must invest in analytical capabilities, process monitoring systems, and production parameter adjustments, which may impact flavor development and product characteristics. Small specialty malt producers face a greater burden due to limited economies of scale in compliance infrastructure. This situation may result in market consolidation and reduced product variety.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Crystal Malts Drive Premium Positioning

In 2024, crystal and caramel malts command a 42.58% share of the market, thanks to their widespread use in brewing and food production. Valued for their ability to enhance beer profiles and elevate food quality, these malts play a pivotal role in meeting the demands of both commercial and craft brewers. Their versatility allows them to be used in a variety of beer styles, contributing to the growing popularity of craft beers globally. Meanwhile, roasted and chocolate malts are on an upward trajectory, boasting a 7.33% CAGR through 2030. Crystal malts lead the pack, imparting color, flavor, and sweetness without the need for mashing. This quality makes them indispensable for craft brewers, whether they're crafting amber ales or dark lagers, as they provide consistency and depth to the final product.

The rising popularity of roasted and chocolate malts underscores a growing consumer appetite for premium offerings, especially those boasting intricate flavors and natural hues. This trend is evident in both the brewing world and the confectionery realm, notably in artisanal chocolates and specialty drinks. These malts are increasingly used to create unique flavor profiles that cater to evolving consumer preferences for high-quality, authentic products. Dark and black malts are staples in stout and porter crafting, lending distinct coffee and roasted undertones that define these beer styles. At the same time, specialty malts—such as smoked, peated, and acidulated—present fresh avenues for differentiation in both craft brewing and food production. These specialty varieties enable manufacturers to experiment with innovative recipes, offering products that stand out in a competitive market.

By Source Grain: Barley Dominance Faces Alternative Grain Challenge

In 2024, barley commands a dominant 66.19% share of the market. Oats, however, are on the rise, boasting the highest growth rate at an impressive 8.52% CAGR projected through 2030. This surge in oat popularity is largely attributed to their incorporation in plant-based dairy alternatives, such as oat milk, and the burgeoning gluten-free beer segment, which continues to attract health-conscious consumers. Barley maintains its market leadership, bolstered by established supply chains that ensure consistent availability, robust processing capabilities that meet large-scale demand, and a regulatory framework that champions traditional malting practices, ensuring quality and compliance. Meanwhile, wheat malt plays a pivotal role in German-style wheat beers, enhancing key beer attributes like head retention, mouthfeel, and flavor profile, which are critical to consumer satisfaction and product differentiation in the competitive beer market.

Rye malt, with its distinct spicy notes and aromatic compounds, is a favorite among craft brewers aiming for unique and complex brews that appeal to niche markets. Alternative grains such as rice, sorghum, and quinoa are carving out niches, especially in gluten-free and specialty products. These grains cater to consumers with dietary restrictions, such as gluten intolerance, and those on the lookout for novel taste experiences, driving innovation in product development. The rising popularity of oats underscores their adaptability, not just in brewing but also in culinary applications, including baked goods and snacks. This trend is further validated by research highlighting the benefits of enzymatic starch processing for oat milk stability, which improves shelf life and texture, and the enhanced nutritional profiles of oat-based products, making them a preferred choice for health-conscious consumers.

By Form: Liquid Extracts Gain Traction in Functional Applications

In 2024, dry and whole kernel malts command a significant 54.27% market share, thanks to their cost-effectiveness and adaptability in brewing and distilling. These malts are widely preferred due to their ability to enhance production efficiency and reduce overall costs for manufacturers. Meanwhile, the liquid extract segment is on an upward trajectory, boasting a 9.15% CAGR through 2030. Dry malts solidify their market leadership, leveraging advantages like extended shelf life, reduced transportation costs, and flexible timing in production. On the other hand, liquid extracts are witnessing robust growth, favored for their convenience by small-scale brewers and their ability to offer precise flavor control in non-alcoholic and functional beverages. This growth is further supported by the increasing demand for innovative beverage formulations and the rising popularity of craft brewing.

Malt flours and powders find their niche in bakery and confectionery, delivering distinct flavor profiles and functional benefits. These products are essential for achieving specific textures and enhancing the overall sensory experience in baked goods and sweets. In the realm of plant-based dairy, liquid extracts are gaining traction, adding natural sweetness and boosting protein content. This advantage is especially pronounced for craft brewers, who often grapple with limited storage and handling capabilities. Moreover, advancements in processing liquid extracts, such as enhanced concentration and stabilization techniques, are broadening their applications and extending shelf life. These innovations are enabling manufacturers to cater to a wider range of consumer preferences and expand their product portfolios.

By Application: Plant-Based Dairy Emerges as Growth Driver

Brewing applications hold a dominant 72.08% market share in 2024, reflecting the specialty malt market's core position in alcoholic beverage production. Plant-based dairy analogues represent the fastest-growing segment, with a 9.83% CAGR through 2030. The brewing segment's prominence extends across traditional beer production and newer categories, including non-alcoholic beers, hard seltzers, and functional beverages. The distilling segment benefits from growth in premium spirits, notably American single malt whisky, which received official TTB - Alcohol and Tobacco Tax and Trade Bureau's recognition in January 2025, requiring 100% malted barley content[4]Source: TTB - Alcohol and Tobacco Tax and Trade Bureau, "TTB Establishes 'American Single Malt Whisky' Standard of Identity," ttb.gov.

Malt finds its way into bakery and confectionery applications for both its flavor and functional properties, enhancing the overall quality and appeal of the final products. Meanwhile, breakfast cereals and snacks harness malt for its nutritional and taste advantages, contributing to their health benefits and consumer satisfaction. The surge in plant-based dairy analogues is largely fueled by a rising consumer appetite for sustainable protein sources and lactose-free options, with oat milk applications notably propelling the demand for malt extract due to its ability to improve texture, flavor, and nutritional profile.

Geography Analysis

Europe holds a dominant 34.25% market share in 2024, supported by centuries-old traditional brewing expertise, sophisticated supply chain networks, and comprehensive regulations favoring artisanal production methods. Companies like Malteurop demonstrate this regional strength, operating 23 industrial sites across 14 countries and maintaining extensive partnerships with 10,500 farmers to ensure consistent high-quality raw material standards. Germany and the United Kingdom represent the largest markets within Europe, supported by well-established craft brewing segments, extensive distribution networks, and successful premium product positioning strategies.

From 2025 to 2030, the Asia-Pacific region is set to lead with a robust 9.61% CAGR. This surge is fueled by progressive market deregulation, rising consumer incomes, and a swift shift in preferences towards premium alcoholic beverages. In India, modernized production facilities and a trend of urban consumption are driving notable market expansion, supported by increasing disposable incomes and a growing middle-class population. Meanwhile, China's burgeoning craft brewing sector stands poised for significant growth, bolstered by its vast population, rapid urbanization, and a more discerning consumer base, which is increasingly seeking unique and high-quality beverage options.

North America sustains its market position through ongoing innovation in craft brewing, advanced production technologies, and premium spirits production capabilities. The introduction of American Single Malt Whisky standards by the TTB, mandating 100% malted barley content, has significantly increased demand for specialty malting barley and impacted production trends. Additionally, research from the University of Arkansas has demonstrated that malted rice can reduce brewing costs by 2-12% compared to milled rice. This finding is particularly noteworthy as rice produces more sugar per acre than barley while requiring less land for cultivation.

Competitive Landscape

The specialty malt market maintains moderate fragmentation, with established players pursuing vertical integration while emerging companies target niche applications and sustainable production methods. Major companies implement comprehensive supply chain strategies, from raw material sourcing to distribution networks, while smaller players focus on specialized market segments and eco-friendly practices. Companies focus their technological investments on sustainability and process optimization, implementing renewable energy systems, water conservation measures, and alternative fuel sources to reduce environmental impact.

Muntons' sustainability program, which includes biomass energy generation and water recycling systems, and Viking Malt's environmental initiatives, featuring energy-efficient kilning processes and waste reduction programs, demonstrate how improved operational efficiency creates competitive advantages while meeting regulatory requirements. Innovation centers serve as key differentiators in the market, as exemplified by Boortmalt's facilities in Belgium and Argentina that develop customized solutions for craft brewers and distillers. These centers conduct extensive research on flavor profiles, grain varieties, and malting techniques to meet specific customer requirements.

Investing heavily in processing capabilities and market development, players can tap into opportunities in alternative grain processing. These opportunities include the production of ancient grains, which cater to consumers seeking traditional and nutrient-rich options, and gluten-free grains, which address the growing demand from individuals with dietary restrictions. Additionally, plant-based food ingredients are gaining traction due to the rising preference for sustainable and health-conscious diets. Furthermore, specialty products aimed directly at consumers present a lucrative avenue, particularly as e-commerce and direct-to-consumer channels continue to expand.

Specialty Malt Industry Leaders

-

Vivescia Group (Malteurop)

-

Cargill, Incorporated

-

Richardson International Limited (Crisp Malt)

-

Polttimo Oy (Viking Malt)

-

Muntons PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: French & Jupps, the UK's oldest maltster, has launched a new line of pre-milled specialty roasted malts. The range includes 14 varieties, including crystal, amber, chocolate, and roasted barley, available in small batches with minimum orders starting at one pallet layer. This initiative provides craft and independent brewers easier access to high-quality, heritage malts while maintaining freshness and recipe consistency.

- April 2025: Blue Ox Malthouse, Maine's primary floor maltster, has introduced seven new roasted specialty malts using local grains. The range includes Chocolate Rye, Crystal 90, Crystal 120, Golden Triticale, Roasted Barley, Roasted Oats, and Roasted Wheat, offering flavors from dark chocolate to coffee and molasses. Developed with regional breweries and produced at their expanded facility, now the largest floor malt operation outside Europe, these malts are manufactured in small batches to maintain quality standards.

- November 2024: Boortmalt has officially announced an expansion of its Minch Malt facility in Athy, County Kildare, Ireland. The upgrade will add state-of-the-art malting equipment, boosting capacity by 20,000 metric tonnes per year. Scheduled to begin in November 2024 and complete by late 2025, the project is part of a multi-million euro investment, bringing Boortmalt's total spend at Athy to nearly EUR 100 millionThis expansion enables the plant to absorb more high-quality Irish barley, rising from 180,000 MT to over 200,000 MT annually, supporting local farmers and enhancing the country’s premium malt output for brewers and distillers worldwide.

- February 2024: Viking Malt has partnered with Swedish agritech firm Improvin' to implement an AI-driven sustainability platform for tracking and reducing greenhouse gas emissions in their European barley supply chain. The initiative involves over 1,200 farmers across Finland, Sweden, Denmark, Poland, and Lithuania, measuring emissions and biodiversity at the field level. This program targets Viking Malt's Scope 3 emissions, which constitute approximately 87% of their total carbon footprint.

Global Specialty Malt Market Report Scope

| Crystal and Caramel Malt |

| Roasted and Chocolate Malt |

| Dark/Black Malt |

| Others (Smoked, Peated, Acidulated, etc.) |

| Barley |

| Wheat |

| Rye |

| Oats |

| Other Novel Grains (Rice, Sorghum, Quinoa) |

| Dry/Whole Kernel |

| Liquid/Extract |

| Malt Flours and Powders |

| Brewing |

| Distilling |

| Bakery and Confectionery |

| Breakfast Cereals and Snacks |

| Plant-Based Dairy Analogues |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Netherlands | |

| Italy | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Nigeria | |

| Saudi Arabia | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Crystal and Caramel Malt | |

| Roasted and Chocolate Malt | ||

| Dark/Black Malt | ||

| Others (Smoked, Peated, Acidulated, etc.) | ||

| By Source Grain | Barley | |

| Wheat | ||

| Rye | ||

| Oats | ||

| Other Novel Grains (Rice, Sorghum, Quinoa) | ||

| By Form | Dry/Whole Kernel | |

| Liquid/Extract | ||

| Malt Flours and Powders | ||

| By Application | Brewing | |

| Distilling | ||

| Bakery and Confectionery | ||

| Breakfast Cereals and Snacks | ||

| Plant-Based Dairy Analogues | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Netherlands | ||

| Italy | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Nigeria | ||

| Saudi Arabia | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the specialty malt market?

The specialty malt market size is USD 3.23 billion in 2025 and is projected to reach USD 4.91 billion by 2030, reflecting a 6.13% CAGR.

Which region is growing fastest for specialty malts?

Asia-Pacific is forecast to post a 9.61% CAGR through 2030, propelled by regulatory liberalization and rising premium-beer consumption.

Why are liquid malt extracts gaining popularity?

Extracts save storage space and simplify dosing for small brewers, while functional-drink makers value their flavor precision and nutritional contribution.

Which product type holds the largest market share?

Crystal and caramel malts lead with 42.58% of 2024 revenue, thanks to their versatility in imparting color and sweetness across beverage and food applications.

Page last updated on: