Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 9.03 Billion |

| Market Size (2031) | USD 10.47 Billion |

| Growth Rate (2026 - 2031) | 3.02% CAGR |

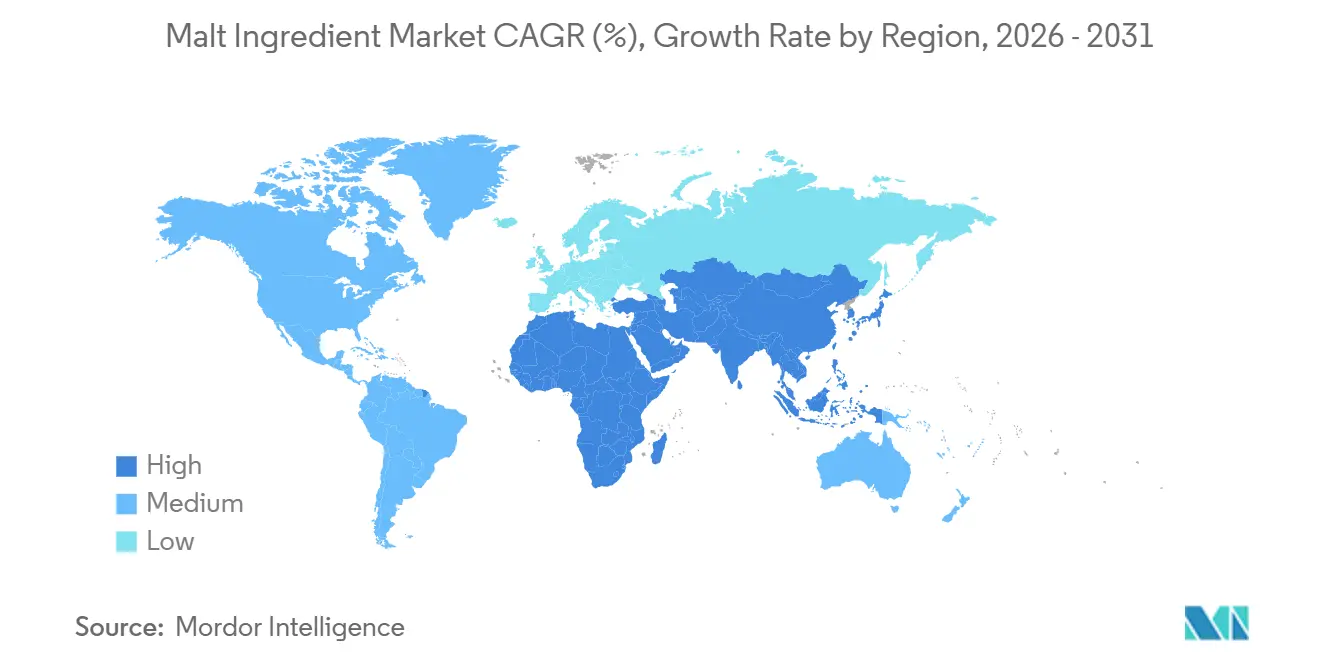

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

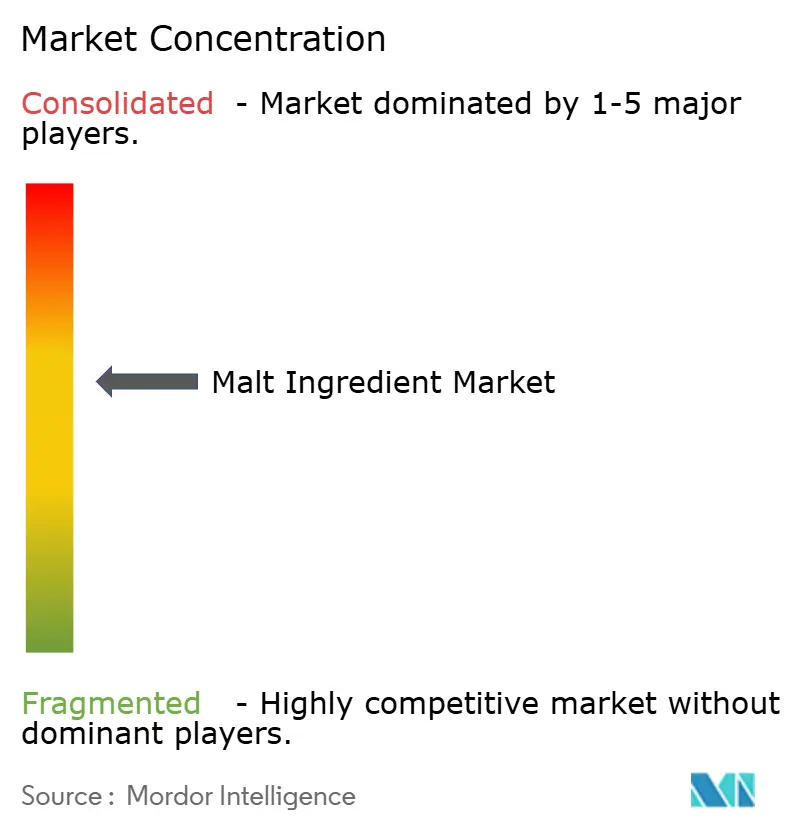

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Malt Ingredient Market Analysis by Mordor Intelligence

The malt ingredient market size was valued at USD 8.83 billion in 2025 and is estimated to grow from USD 9.03 billion in 2026 to reach USD 10.47 billion by 2031, at a CAGR of 3.02% during the forecast period (2026-2031). This growth is supported by the consistent demand for clean-label sweeteners, precisely formulated non-alcoholic malt beverages, and multi-functional food ingredients. Craft brewers are increasingly shifting toward lighter wheat and specialty grain profiles, while large brewers are managing barley price volatility through multi-year contracts and varietal diversification. Organic certification premiums, which typically range from USD 800 to USD 900 per tonne above conventional grades, are encouraging vertically integrated maltsters to invest in segregated storage and processing facilities. In the Asia-Pacific region, importers are strengthening their supply relationships with Australia and Canada due to increasing beer production and fragmented domestic malting capacity. Furthermore, digital agronomy tools that monitor soil carbon and nitrogen flows are becoming widely adopted, helping to reduce Scope 1 and Scope 2 emissions. This adoption is also widening the sustainability gap between large-scale producers and regional specialists.

Key Report Takeaways

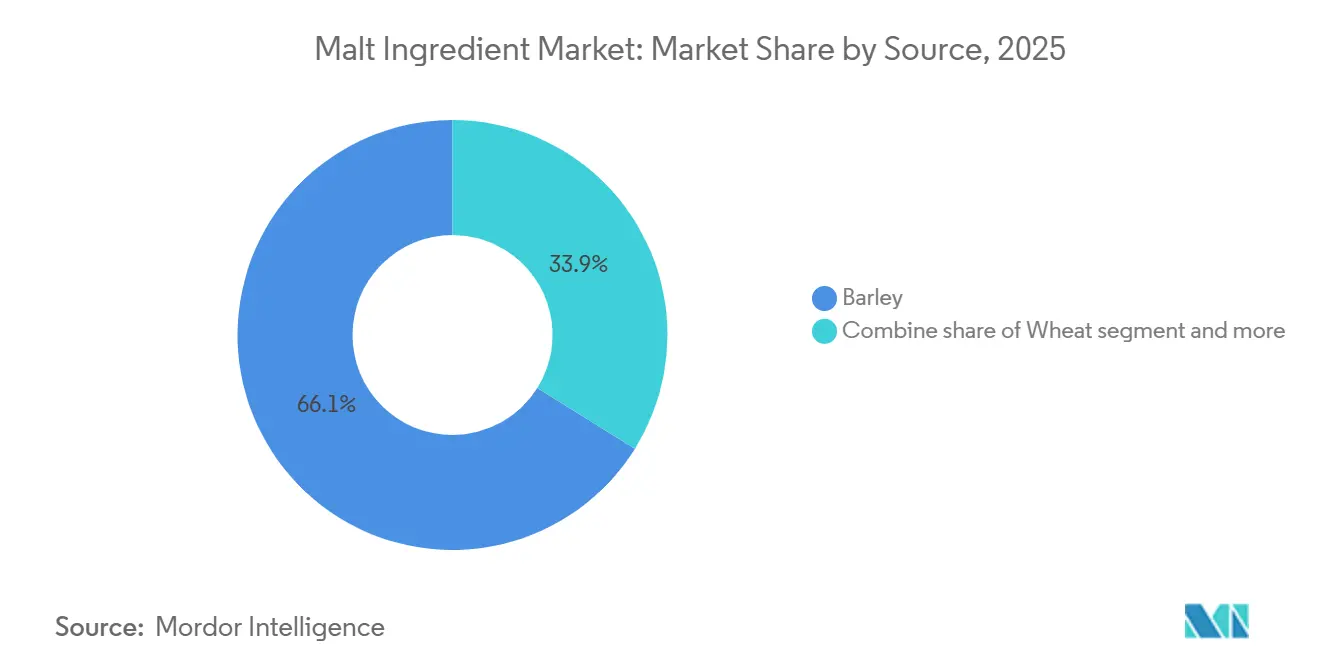

- By source, barley captured 66.13% of malt ingredient market share in 2025, while wheat is set to post the fastest growth at a 3.98% CAGR through 2031.

- By nature, conventional grades held 79.40% of the malt ingredient market size in 2025; organic variants are on course to expand at a 4.13% CAGR to 2031.

- By application, alcoholic beverages accounted for 46.82% of volume in 2025, whereas the food industry segment is forecast to grow at a 4.32% CAGR through 2031.

- By geography, Europe retained 35.32% of malt ingredient market share in 2025, but Asia-Pacific is projected to advance at a 3.92% CAGR over the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Malt Ingredient Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for natural and clean-label sweetening and flavoring agents | +0.5% | Global | Medium term (2-4 years) |

| Growth of craft beer, specialty brewing, and distilling | +0.4% | North America and Europe | Short term (≤ 2 years) |

| Increasing use of malt ingredients in non-alcoholic malt beverages | +0.6% | Global, with early gains in Europe and North America | Medium term (2-4 years) |

| Functional and nutritional benefits driving use in health-oriented foods | +0.4% | North America and Asia-Pacific | Long term (≥ 4 years) |

| Expansion of bakery and confectionery applications | +0.3% | Europe and Asia-Pacific | Medium term (2-4 years) |

| Consumer preference for traditional and heritage ingredients | +0.2% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for natural and clean-label sweetening and flavoring agents

Regulatory pressure and consumer skepticism toward synthetic additives are driving the adoption of malt extracts in mainstream food formulations. The FDA has granted Generally Recognized as Safe (GRAS) status to malt, malt syrup, and maltodextrin, allowing their use in bakery, dairy, and beverage categories without requiring additional approvals. Cargill's SweetPure M product, a blend of wheat and barley malt syrup, provides approximately 40% of sucrose's sweetness while offering benefits such as enzymatic browning and moisture retention. These attributes enable bakers to reduce sugar content without compromising texture. Malt Products Corporation has invested USD 50 million in capacity upgrades, including a USD 15 million spray-drying plant, to address the growing demand from organic snack brands seeking alternatives to high-fructose corn syrup. Additionally, European Union Regulation 1169/2011 mandates front-of-pack ingredient transparency, accelerating reformulation efforts among confectioners. Malt, regarded as a heritage ingredient, aligns with both regulatory compliance and marketing objectives [1]Source: European Union,“Regulation (EU) No 1169/2011 of the European Parliament and of the Council,” eur-lex.europa.eu.

Growth of craft beer, specialty brewing, and distilling

Craft distillers and microbreweries focus on the importance of terroir and the origin of ingredients, which has created a demand for specialty malts that commodity suppliers cannot satisfy. In the United States, there were 2,800 active craft distillers as of August 2024. However, total case volumes decreased by 6.1% year-over-year to 12.7 million cases, reflecting a maturing market and growing competition. Meanwhile, Japan's whisky exports reached JPY 56.8 billion (USD 380 million) in 2023, marking a 21% increase compared to the previous year. This growth is attributed to global interest in limited-edition single malts that rely on specific barley varieties and traditional floor malting techniques [2]Source: American Craft Spirits Association, “Market Report 2024,” americancraftspirits.org. A study conducted by Pennsylvania State University found that 66% of craft brewers are willing to pay a premium for locally sourced barley, while 75% are willing to do so for fruits grown within their state. This underscores the influence of neolocalism on procurement strategies. Additionally, Germany's Reinheitsgebot, also known as the German Beer Purity Law, was enacted in 1516 and restricts beer ingredients to barley, hops, water, and yeast. This regulation continues to support traditional malt demand, even as Germany exports approximately 1.5 billion liters of beer annually.

Increasing use of malt ingredients in non-alcoholic malt beverages

Zero-alcohol beer has experienced significant growth, encouraging maltsters to innovate and create products that retain mouthfeel and flavor complexity without relying on the masking effects of ethanol. Heineken 0.0 has successfully expanded into more than 50 markets, while Athletic Brewing Company achieved a valuation of USD 800 million in 2023, with annual production exceeding 500,000 barrels. This growth highlights that non-alcoholic beer variants are no longer confined to niche markets and have the potential for widespread acceptance and scalability. Specialty malts, such as caramel, chocolate, and roasted malts, play a crucial role in providing Maillard-reaction compounds that replicate the sensory profile of traditional beer. This is a technical challenge that standard barley malt cannot address effectively. Erdinger Alkoholfrei, which is Germany's leading non-alcoholic wheat beer, incorporates isotonic formulations enriched with B vitamins that are naturally present in malt. This approach positions the beverage as an ideal option for post-exercise recovery, appealing to health-conscious consumers.

Functional and nutritional benefits driving use in health-oriented foods

Malt extract provides essential vitamins B1, B2, B3, and B6, along with important minerals such as magnesium, phosphorus, and iron, making it a highly beneficial ingredient in sports nutrition products and infant formula. These nutrients contribute to energy metabolism, muscle function, and overall health, enhancing the nutritional profile of the products in which malt extract is used. Diastatic malt powder contains active alpha-amylase and beta-amylase enzymes, which play a crucial role in enhancing starch conversion during fermentation. This enzymatic activity is particularly valuable for artisan bakers, as it helps improve dough extensibility, enhances crumb structure, and contributes to the overall texture and quality of baked goods. Non-diastatic malt, which undergoes heat treatment to deactivate enzymes, serves multiple functions, including acting as a natural colorant and humectant in biscuits and crackers. By retaining moisture and improving texture, it contributes to extending the shelf life of these products by 15% to 20% compared to formulations that rely solely on refined sugar. Additionally, emerging research on malt oligosaccharides highlights their potential prebiotic benefits, which could support gut health by promoting the growth of beneficial gut bacteria. However, clinical trials exploring these benefits remain limited, and regulatory pathways for substantiating health claims are still uncertain, requiring further investigation and validation.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuating raw material prices and input cost pressure | -0.4% | Global | Short term (≤ 2 years) |

| Competition from alternative sweeteners and carbohydrate sources | -0.3% | North America and Europe | Medium term (2-4 years) |

| Risk of allergens and gluten-related concerns | -0.2% | Global | Medium term (2-4 years) |

| Regulatory scrutiny on alcoholic beverages in some regions | -0.2% | Middle East and Asia-Pacific select markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fluctuating raw material prices and input cost pressure

Global barley production decreased to 145 million tonnes in the 2024-2025 crop year, compared to 155 million tonnes in the previous season. This decline led to a tighter supply of malting-grade barley, pushing prices to USD 250 to 350 per tonne, up from USD 200 to 280 in 2023. The European Union harvested 47.8 million tonnes of barley in 2024, representing a 6% year-over-year decrease, as drought conditions in France and Germany reduced yields. Canada, the largest global exporter of barley, also faced challenges due to climate volatility. Meanwhile, Australia's resumption of barley exports to China, following the lifting of a three-year trade restriction in 2023, only partially compensated for global supply shortfalls. Higher fertilizer and energy costs added to margin pressures, with nitrogen fertilizer prices remaining 40 to 50% above pre-2021 levels despite recent declines. Maltsters with long-term barley contracts and vertical integration into farming operations were better equipped to manage these challenges. However, smaller regional players experienced margin compression of 200 to 300 basis points during spot price increases. This constraint is estimated to reduce baseline growth by 0.4 percentage points, with short-term impacts primarily affecting regions that depend on imported barley.

Competition from alternative sweeteners and carbohydrate sources

Stevia, monk fruit, allulose, and erythritol provide zero-calorie sweetness, a feature that malt extracts cannot replicate, leading to fragmentation within the natural sweetener market. Malt extracts offer approximately 40% to 50% of the sweetness of sucrose, necessitating higher usage levels, which in turn increase formulation costs. However, malt extracts provide functional advantages such as enzymatic browning, moisture retention, and texture enhancement, which high-intensity sweeteners do not offer. This positions malt extracts as complementary ingredients rather than direct substitutes. In response to these dynamics, bakery and confectionery product developers are increasingly combining malt extracts with stevia or monk fruit to achieve the desired sweetness levels while maintaining essential process functionality. This strategic approach helps sustain the demand for malt extract volumes but limits the ability to increase pricing significantly.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Barley Dominance Persists Amid Wheat Momentum

Barley is expected to account for 66.13% of source-based volume in 2025, due to its superior enzymatic activity, high fermentable extract yield, and well-established supply chains across Canada, Australia, the European Union, and Argentina. Wheat malt is anticipated to grow at the fastest rate, with a Compound Annual Growth Rate (CAGR) of 3.98% through 2031, driven by craft brewers producing lighter-bodied ales and lagers that appeal to consumers transitioning from wine and spirits. Rye malt, known for its spicy phenolic notes in Roggenbier and rye whiskey, remains a niche segment concentrated in Germany and North America. At the same time, rice malt is gaining traction in the Asia-Pacific region for gluten-free applications, despite being 17% more expensive than barley malt. Sorghum, millet, oat, and corn malts collectively account for less than 5% of global volume but are expanding rapidly in Africa and North America, where the prevalence of celiac disease and demand for gluten-free labeling are driving reformulation efforts.

Rice malt delivers 2 to 3 times higher yield per hectare compared to barley, reducing land requirements by 50% to 67% for equivalent extract volumes. This sustainability advantage aligns with the objectives of brewers aiming for carbon-neutral operations. The International Grains Council forecasts barley acreage to stabilize around 50 million hectares through 2031. However, climate volatility and water scarcity in key growing regions, including Canada, Australia, and the European Union, are expected to sustain price premiums for malting-grade barley and accelerate the diversification into alternative grains.

By Nature: Organic Premiums Justify Certification Costs

Conventional malt accounted for 79.40% of the volume in 2025, supported by established agronomic practices, lower input costs, and supply-chain efficiencies that organic alternatives have yet to achieve. Organic malt is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.13% through 2031, driven by demand from premium beer segments and health-food brands willing to pay price premiums of USD 800 to 900 per tonne over conventional grades. The United States Department of Agriculture (USDA) National Organic Program and European Union Organic Regulation 2018/848 require a three-year transition period for farmland converting to organic production. This requirement limits supply flexibility and sustains price premiums despite increasing demand [3]Source: United States Department of Agriculture, "Organic Resources for Farms, Ranches, & Businesses,"ams.usda.gov.

Weyermann, a German specialty maltster, has expanded its organic malt portfolio to include caramel, chocolate, and roasted variants, catering to craft brewers who view organic certification as a brand differentiator capable of supporting 10% to 15% retail price premiums. Similarly, Simpsons Malt has achieved organic certification for its floor-malted products, combining traditional processing methods with sustainability credentials. These products command prices of USD 1,200 to 1,500 per tonne in niche whisky and craft beer markets.

By Application: Food Industry Outpaces Alcoholic Beverages

Alcoholic beverages accounted for 46.82% of the application volume in 2025. However, the food industry is projected to grow at the fastest rate, with a Compound Annual Growth Rate (CAGR) of 4.32% through 2031. This growth is attributed to bakery chains and confectioners increasingly replacing synthetic sweeteners with malt extracts to meet clean-label requirements. Beer remains the largest sub-segment within alcoholic beverages, utilizing approximately 85% of the malt allocated to this category. Despite this, craft beer volumes in the United States declined by 1 to 2% in 2024 due to market saturation and consumer fatigue.

Whiskey and spirits consume 10 to 12% of the malt used in alcoholic beverages, with Japan's whisky exports reaching JPY 56.8 billion (USD 380 million) in 2023, marking a 21% year-over-year increase as global collectors seek limited-edition single malts. Non-alcoholic beverages, including zero-alcohol beer and malted milk drinks, are expected to grow at a CAGR of 5 to 6%, driven by health-conscious consumers under 35 years old and demand from Islamic markets where alcohol consumption is restricted.

Geography Analysis

Europe maintained its position as the leading segment, accounting for 35.32 percent of geographic volume in 2025. This dominance is supported by Germany's Reinheitsgebot purity law, enacted in 1516, which restricts beer ingredients to barley, hops, water, and yeast, thereby preserving traditional malt demand. Germany also exports approximately 1.5 billion liters of beer annually. Belgium's beer culture, recognized as a UNESCO Intangible Cultural Heritage in 2016, strengthens consumer associations between traditional malting methods and product authenticity. In the United Kingdom, the craft-brewing renaissance continues to drive demand for specialty malts produced through floor malting, a labor-intensive technique that commands premiums of USD 200 to 300 per tonne. Additionally, Boortmalt's 2024 expansions in Scotland added 55,000 tonnes of capacity across its Buckie and Glenesk facilities, while its Irish Minch site gained 20,000 tonnes. These developments collectively increased the group's capacity to 3.0 million tonnes, reinforcing Europe's position as the world's largest malting hub.

The Asia-Pacific region is projected to experience the fastest growth, with a compound annual growth rate (CAGR) of 3.92 percent through 2031. This growth is driven by China's annual beer production of 360 million hectoliters, India's 350-plus craft breweries expanding at 25 to 30 percent annually, and Japan's whisky exports, which reached JPY 56.8 billion (USD 380 million) in 2023, reflecting a 21 percent year-over-year increase. In Southeast Asia, rising middle-class populations and urbanization are fueling beer consumption in countries such as Vietnam, Thailand, and Indonesia. However, limited domestic malting capacity in these nations necessitates imports from Australia and Canada, adding USD 50 to 100 per tonne in freight and logistics costs. In India, the state-by-state alcohol licensing system creates 28 distinct regulatory regimes, increasing distribution costs and delaying product launches by 6 to 12 months. Despite these challenges, craft brewers are focusing on metropolitan markets such as Mumbai, Bangalore, and Delhi, where regulatory enforcement is more predictable.

North America accounted for approximately 20 to 22 percent of global volume in 2025. The United States is home to 2,800 active craft distillers and more than 9,000 craft breweries. However, consolidation and market saturation led to a 1 to 2 percent decline in craft-beer volumes in 2024. In February 2024, Rahr Corporation merged its malting division with Brewers Supply Group (BSG), streamlining supply chains and emphasizing the need for mid-tier players to scale or specialize to compete with vertically integrated giants. Canada, which supplies approximately 30 percent of global malting barley exports, faced challenges due to climate volatility that reduced 2024 yields and elevated farmgate prices. This tightening of North American malt supply prompted brewers to secure multi-year contracts to mitigate risks.

Regulatory Landscape

Regulation of malt ingredients varies by end use (food formulations vs malt beverages) and by jurisdiction, with several long-standing frameworks shaping labeling, formulation, and speed-to-market. In the United States, malt syrup and malt extract are affirmed as GRAS under 21 CFR 184.1445, permitting use as flavoring agents, adjuvants, colorants, and sweeteners under CGMP. This supports broad adoption in bakery, dairy, and beverage applications without additional pre-market approvals. For alcoholic beverages, the Alcohol and Tobacco Tax and Trade Bureau (TTB) Ruling 2015-1 reduces formula filing burden for malt beverages made with traditionally used brewing ingredients, including malt, when the product meets the beer definition under 27 CFR 25.11.

In the European Union, Regulation (EC) No 1333/2008 on food additives excludes malt and malt products from its scope when used as foods for flavor or nutritional purposes. This shifts compliance emphasis toward general food law and labeling requirements rather than additive authorizations. India permits malt and maltodextrin as ingredients in specified dairy applications under Food Safety and Standards Authority of India (FSSAI) regulations (Food Products Standards and Food Additives). Use is controlled through category standards and applicable safety limits, which adds application-specific compliance considerations for brands operating across food and beverage categories.

Value Chain Analysis

The malt ingredient value chain starts with grain production (primarily malting barley, and increasingly wheat and select gluten-free alternatives), followed by procurement through contract farming and grain merchants, and then malting operations (steeping, germination, kilning, and deculming). These steps convert grain into base and specialty malts and malt extracts. Large maltsters commonly rely on multi-year grower contracts and varietal diversification to secure malting-grade supply and manage price volatility, while specialty producers differentiate through floor malting, custom roasting profiles, and technical support tailored to craft brewers, distillers, and food formulators.

Downstream, malt ingredients are distributed in bulk and packaged formats to breweries, distilleries, non-alcoholic beverage producers, and food manufacturers (bakery, confectionery, cereals, and nutrition products). Performance attributes such as color development, enzymatic activity, and moisture retention support clean-label reformulation. Trade bodies and associations including EUROMALT, the Maltsters Association of Great Britain (UK), and the American Malting Barley Association (US) influence quality norms and sustainability practices. Operational bottlenecks are tied to climate-driven barley supply variability, energy intensity in kilning, water use, and logistics costs in import-dependent regions, particularly across parts of Asia-Pacific.

Competitive Landscape

The malt ingredients market shows moderate consolidation. The top five maltsters, including Malteries Soufflet, Axereal, Cargill, Archer Daniels Midland, and Malteurop, collectively control about half of the global capacity. At the same time, numerous regional players focus on serving niche craft and specialty segments. In November 2023, Malteries Soufflet acquired United Malt Group for AUD 1.5 billion (USD 1.0 billion), creating a combined entity with an annual malting capacity of 3.7 million tonnes. This acquisition reinforced its position as the largest maltster globally and underscored the importance of scale economies and vertical integration in maintaining a competitive edge.

Boortmalt operates 27 malting plants across Europe, North America, South America, and Africa, with a total capacity exceeding 3.0 million tonnes. The company launched the Atlantis Malt Series, which uses Tritordeum, a hybrid grain combining durum wheat and wild barley, to stand out in the craft-brewing segment. Technology adoption in the market is centered on precision agriculture partnerships. For example, Simpsons Malt collaborates with Yara and OCI to source low-carbon fertilizers and utilizes BASF's Xarvio digital platform to trace barley provenance. These initiatives have helped reduce Scope 1 and 2 emissions by 11% compared to 2019 levels.

Growth opportunities are concentrated in areas such as organic certification, gluten-free alternatives, and non-alcoholic beverage formulations. However, the commodity-focused infrastructure of major players limits their ability to address niche demand effectively. Smaller specialty maltsters, such as Weyermann, Simpsons, Muntons, and Briess, are able to command premiums of USD 200 to 400 per tonne by offering floor-malted products, custom roasting profiles, and technical support that larger commodity suppliers cannot easily replicate. Emerging disruptors, including enzyme suppliers like Novozymes, are enabling brewers to replace barley malt with adjuncts such as corn, rice, and sorghum while maintaining fermentable extract yields. This innovation could potentially reduce malt demand in cost-sensitive segments. Vertical integration into farming remains a strategic priority, with companies like Malteurop and Axereal contracting directly with growers to secure malting-grade barley and mitigate price volatility. Smaller maltsters, who often lack agronomic expertise, face challenges in adopting this model. Regulatory compliance costs also favor larger players, as meeting standards like the European Union Organic Regulation 2018/848 and the United States Department of Agriculture (USDA) National Organic Program certification requires dedicated production lines and third-party audits. These requirements result in capital expenditures ranging from USD 2 million to 5 million per facility.

Malt Ingredient Industry Leaders

-

Malteries Soufflet

-

Cargill Inc.

-

Archer Daniels Midland Co.

-

Malteurop Groupe

-

Axereal

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Capacity localization around major breweries and import-dependent markets is a clear whitespace where investments are already underway. Soufflet Malt and HEINEKEN Beverages announced a commercial partnership in South Africa that includes a EUR 100 million malting facility planned beside HEINEKENs Sedibeng Brewery to locally supply malt, and Soufflet Malt also announced an AI-driven malthouse project in South Rajasthan, India, with 110,000 tonnes of annual capacity in partnership with United Breweries Limited. These moves aim to reduce freight exposure and improve supply reliability in markets where domestic malting capacity is fragmented and logistics can add material cost per tonne.

Process efficiency and decarbonization-linked product innovation open further areas tied to buyer sustainability requirements and premium positioning. Boortmalt introduced its Ionsmoke approach for peated malt, using ionisation to cut peat consumption by 30% to 40%, addressing resource constraints around peat while keeping a distinctive flavor input for whisky and specialty beer. On the demand side, clean-label reformulation and non-alcoholic beer expansion continue to pull malt extracts and specialty malts into food and beverage innovation pipelines, while tightening allergen and labeling attention in some markets increases the value of traceability, segregated handling for organic lines, and clearly specified malt ingredient declarations across multinational product portfolios.

Recent Industry Developments

- July 2026: Cargill closed its malthouse in Salzgitter, Germany, removing about 80,000 tonnes of annual malt production capacity from the market. The move reflects structural rationalization in mature European supply and can tighten availability for buyers dependent on regional spot volumes.

- February 2026: Soufflet Malt announced a EUR 100 million investment to build an AI-powered malthouse in South Rajasthan, India, in partnership with United Breweries Limited, targeting an initial capacity of 110,000 tonnes per year. The project strengthens local sourcing for a large brewer and raises the bar for automation and process control in a fast-growing, capacity-constrained market.

- December 2024: Boortmalt announced investments to expand its Scottish maltings, adding 40,000 tonnes at Buckie and 15,000 tonnes at Glenesk, with upgrades due on stream in early 2026 using the 2025 barley harvest. The expansion increases supply for Scotch distilling demand while reinforcing Scotlands position as a premium malting origin tied to local barley growers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the malt ingredient market covers malted grains and processed malt derivatives used as functional and flavor inputs across beverages, food, and other downstream uses, measured as the value generated from sales of these ingredients in each geography.

Scope exclusions: We exclude finished alcoholic drinks, finished bakery and confectionery products, and on-premise retail margins, since only the ingredient value is counted.

Segmentation Overview

-

By Source

- Barley

- Wheat

- Rye

- Rice

- Others

-

By Nature

- Organic

- Conventional

-

By Application

-

Alcoholic Beverages

- Beer

- Whiskey and Spirits

- Other Alcoholic Beverages

- Non-Alcoholic Beverages

- Food Industry

- Pharmaceuticals and Nutraceuticals

- Animal Feed

- Others

-

Alcoholic Beverages

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building a clean view of demand pools and supply signals that are visible in public data, before assumptions were set. We leaned on sources such as USDA, FAOSTAT, UN Comtrade trade statistics, the World Bank macro series, and government food and agriculture ministries for grains, trade flows, and price direction.

Along with this, we reviewed company annual reports, investor decks, product specifications, and credible press coverage to understand how malt formats are positioned across brewing, distilling, and food uses. When needed, our team also checked paid subscriptions that cover company financials and intelligence, patent databases, and shipment-level import export data to confirm capacities, expansion activity, and cross-border movements. The sources listed here are illustrative only, and many other public and industry references were also used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary conversations were used to pressure-test what desk research cannot fully show, especially application-wise mix, realistic price bands, and regional differences in usage. We spoke with ingredient suppliers, maltsters, distributors, and procurement and technical roles in downstream users so the model could be adjusted where published data was too broad.

Because this is a global market, inputs were also checked across Americas, EMEA, and APAC so regional volume signals and pricing logic stayed consistent during the final triangulation.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 22% | APAC: 46% |

| Mid tier: 50% | Functional/Unit leaders: 33% | EMEA: 33% |

| Smaller Players: 22% | Managers: 45% | Americas: 21% |

Market-Sizing & Forecasting

Sizing was built using a top-down demand reconstruction, where grain processing into malt, trade balances, and application-level consumption signals were translated into ingredient demand, and then valued using realistic price ranges. The totals were then corroborated with selective bottom-up checks like sampled supplier revenue bands, channel feedback on mix by malt form, and volume times average selling price snapshots, which helped us correct for over-counting and regional timing gaps.

Key inputs used in the model included malt usage intensity in beer and spirits production, growth in non-alcoholic malt beverages, bakery and cereal inclusion rates, the split between dry and liquid malt formats, and import dependency in countries with limited malting capacity. For forecasting, we relied on scenario analysis supported by expert views on pricing pass-through, grain availability, and demand elasticity, and then linked those scenarios to macro indicators such as beverage output and food processing growth. Where bottom-up visibility was weak for smaller markets, gaps were handled through proxy indicators like trade inflows, capacity utilization cues, and conservative penetration assumptions that were rechecked through interviews.

Data Validation & Update Cycle

After the model was built, outputs were cross-checked against independent signals such as trade trends, grain price cycles, and observed shifts in beverage and food manufacturing activity. Variances were reviewed in steps, starting with unit checks and currency conversion timing, followed by peer review from another analyst before the numbers were signed off.

The report is refreshed on an annual cycle, and interim updates are triggered when there are material events such as capacity additions, major policy changes affecting grains or trade, or sharp input cost swings. Before delivery, we run a final freshness check so clients receive the latest updated view.

Mordor Intelligence's Malt Ingredient Market Size Compared With Other Published Estimates

Published market sizes for malt ingredients often do not match because each publisher draws the market scope differently and uses different value points in the chain. Differences also come from how prices are treated over time, which applications are counted as ingredient demand, and how frequently assumptions are refreshed.

In this market, the biggest gaps usually come from whether the estimate counts only ingredient sales versus adding downstream product value, and whether volume is tied back to visible production and trade signals. Some estimates also apply broad average pricing across all malt formats, which can inflate totals when the mix shifts between liquid extract, dry malt, and flour.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 9.03 B (2026) | |

| Trade Journal A | USD 23.06 B (2024) | Uses factory-gate values and an earlier base year, and it is likely to include a wider set of malt-related products beyond ingredient-only sales, which lifts the reported total. |

| Regional Consultancy B | USD 27.40 B (2025) | Appears to use a broader category definition and a mix-insensitive pricing build across formats, with limited visibility on checks against production and trade-linked volume signals. |

The table points to scope and value-chain treatment as the main drivers of variance, followed by base-year choice and how price and mix are handled. When only ingredient sales are counted and volumes are cross-checked against production and trade signals, the total typically lands lower, and that is how the model is constrained in Mordor Intelligence.

Key Questions Answered in the Report

What is the current value of the malt ingredients market?

The malt ingredients market size is valued at USD 9.03 billion in 2026.

How fast is the market expected to grow?

It is forecast to register a 3.02% CAGR, reaching USD 10.47 billion by 2031.

Which region will grow the fastest?

Asia-Pacific is projected to expand at a 3.92% CAGR, driven by rising beer output and limited local malting capacity.

Why are organic malts gaining traction?

Premium beer and health-food brands pay USD 800–900 per tonne premiums for certified organic malt to meet sustainability and clean-label goals.

How are maltsters mitigating barley price volatility?

Leading firms secure multi-year grower contracts and invest in climate-resilient barley varieties while optimizing energy-efficient kilns.

Page last updated on: