Global HER-2 Negative Breast Cancer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.97 Billion |

| Market Size (2031) | USD 2.91 Billion |

| Growth Rate (2026 - 2031) | 8.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global HER-2 Negative Breast Cancer Market Analysis by Mordor Intelligence

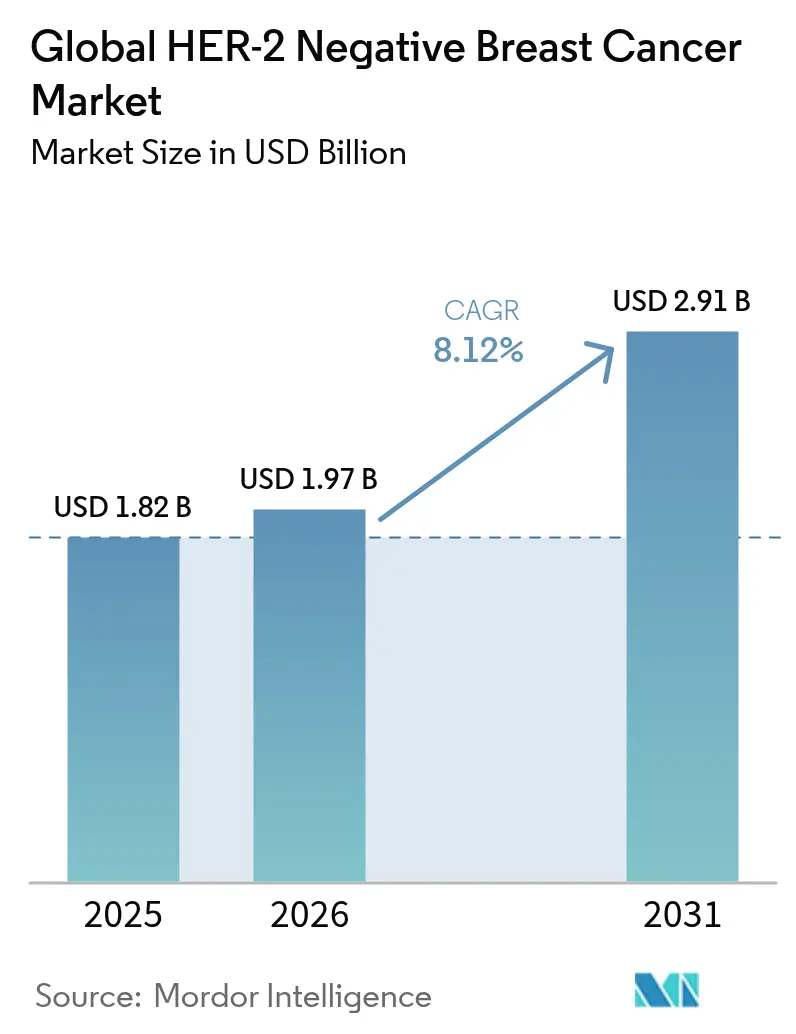

The HER-2 negative breast cancer market size is expected to grow from USD 1.82 billion in 2025 to USD 1.97 billion in 2026 and is forecast to reach USD 2.91 billion by 2031 at 8.12% CAGR over 2026-2031. Precision diagnostics, expanding antibody-drug conjugate (ADC) indications, and recognition of HER2-low tumors as a new therapeutic category combine to accelerate growth. Hormone receptor-positive/HER2-negative tumors represent 70% of incident cases, while triple-negative disease accounts for 15-20% and drives high unmet need. Targeted therapy shows the most rapid uptake as PARP inhibitors and next-generation ADCs displace conventional chemotherapy regimens. Geographic momentum shifts toward Asia-Pacific, where rising incidence and growing access to precision medicine reshape global demand. Payer adoption of value-based reimbursement and indication-specific pricing seeks to contain costs without stalling innovation.

Key Report Takeaways

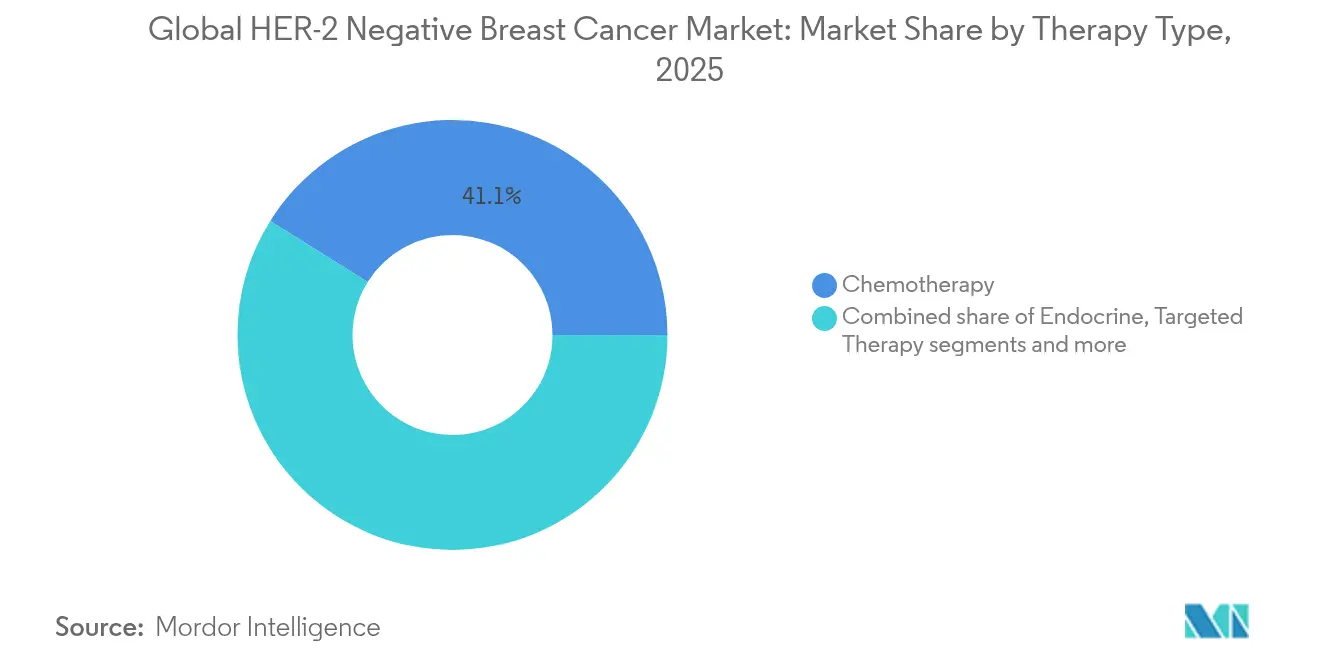

- By therapy type, chemotherapy held 41.10% of the HER-2 negative breast cancer market share in 2025, while targeted therapy is set to expand at a 9.02% CAGR through 2031.

- By biomarker sub-type, hormone receptor-positive/HER2-negative tumors captured 57.25% of the HER-2 negative breast cancer market size in 2025, whereas triple-negative breast cancer is projected to post a 9.42% CAGR to 2031.

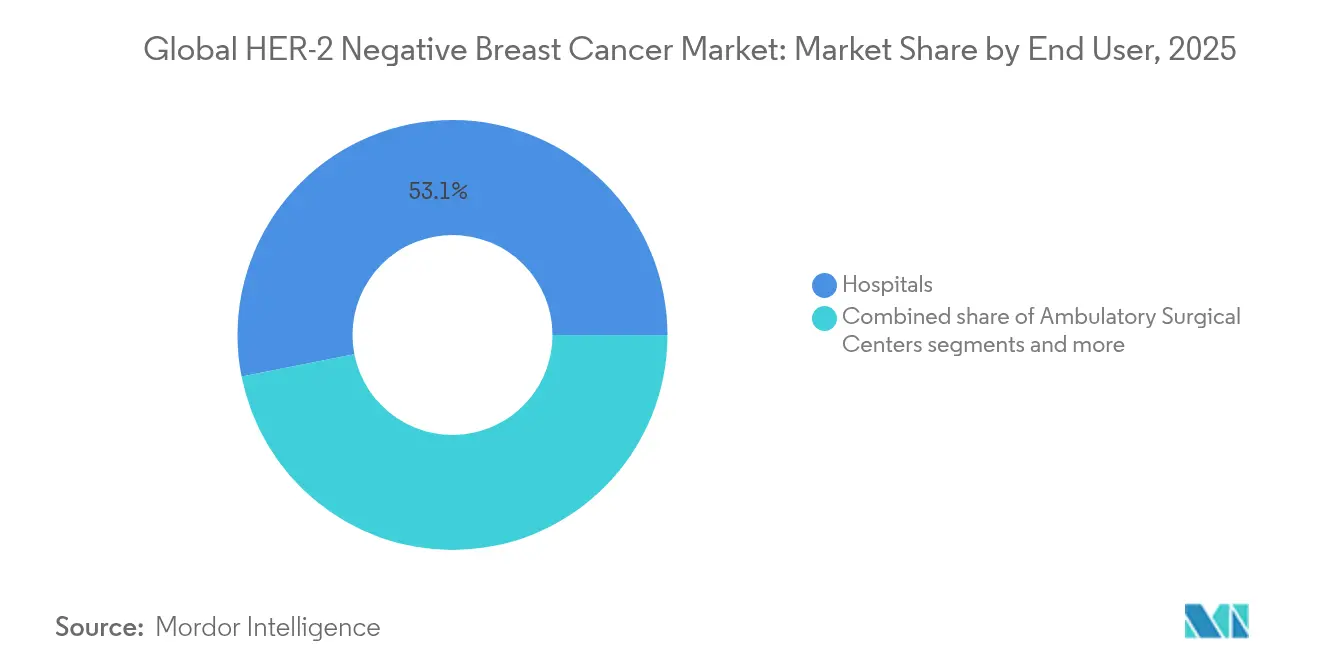

- By end user, hospitals accounted for 53.10% of the HER-2 negative breast cancer market size in 2025, and specialty cancer centers are forecast to grow at a 9.95% CAGR through 2031.

- By geography, North America led with 41.85% revenue share in 2025, while Asia-Pacific is poised to expand at a 10.35% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global HER-2 Negative Breast Cancer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Precision-diagnostics uptake in early-stage disease | +2.1% | Global, early gains in North America and Europe | Medium term (2-4 years) |

| Expanding approvals of PARP inhibitors in HR-positive disease | +1.8% | North America and Europe, spill-over to Asia-Pacific | Short term (≤ 2 years) |

| Growing reimbursement for ADCs | +1.5% | North America and Europe, gradual Asia-Pacific adoption | Medium term (2-4 years) |

| Rising neoadjuvant therapy adoption | +1.2% | Global, faster in high-income regions | Long term (≥ 4 years) |

| Tumor-agnostic trial designs | +0.9% | Global, led by North America | Long term (≥ 4 years) |

| AI-guided trial-matching platforms | +0.6% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Precision-diagnostics uptake in early-stage disease

Routine genomic assays such as Oncotype DX changed treatment recommendations for 65% of early-stage patients in Brazil and cut chemotherapy use by 66%. Lombardy, Italy pioneered reimbursement, proving public-payer willingness to fund genomic testing when clinical utility is clear. Adoption is uneven; under-representation in validation cohorts reduces test accuracy for African American women. Artificial-intelligence models now predict treatment response with 91% accuracy, promising equitable performance across ancestries. Precision diagnostics therefore lower overtreatment, identify high-risk patients earlier, and expand the HER-2 negative breast cancer market by enabling targeted therapy in adjuvant settings.

Expanding approvals of PARP inhibitors in HR-positive disease

Olaparib’s approval for high-risk early HER-2 negative breast cancer with BRCA mutation widened PARP inhibitor reach beyond metastatic TNBC. Homologous-recombination deficiency affects 20-30% of hormone-receptor-positive tumors, creating a larger addressable pool. Talazoparib proved cost-effective in China and the United States with incremental cost-effectiveness ratios of USD 2,484 and USD 6,815 per QALY, respectively. Trials testing PARP inhibitors with CDK4/6 inhibitors or immunotherapy show synergistic efficacy and could further lift adoption. As label expansions accumulate, PARP agents move from niche to foundational therapy, accelerating HER-2 negative breast cancer market growth.

Growing reimbursement for antibody–drug conjugates

Trastuzumab deruxtecan’s February 2025 approval for HER2-low disease expanded eligibility to nearly 90% of hormone-receptor-positive, HER2-negative cases. Datopotamab deruxtecan’s January 2025 clearance cut disease-progression risk by 37% versus chemotherapy. Positive health-technology-assessment outcomes reach 58% for single-manufacturer combinations but only 42% for dual-manufacturer regimens, underscoring pricing-coordination hurdles. Insurers impose step therapy, forcing failure on two CDK4/6 inhibitors before ADC funding, yet indication-specific pricing may ease budget impact. As payers align coverage with value, ADC reimbursement broadens and bolsters the HER-2 negative breast cancer market.

Rising neoadjuvant therapy adoption

The I-SPY2.2 trial showed datopotamab deruxtecan plus durvalumab achieved strong responses in early-stage disease, supporting ADC-immunotherapy combinations before surgery. De-escalation studies report 94% four-year disease-free survival after short neoadjuvant chemotherapy in HER2-positive cases and 92.7% in TNBC. The TROPION-Breast04 study is evaluating similar regimens in treatment-naïve patients. Early Ki-67 reduction predicts pathological response and guides adaptive therapy duration. Personalized neoadjuvant strategies therefore create earlier demand for targeted agents and enlarge the HER-2 negative breast cancer market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High attrition of TNBC immunotherapy assets | -1.4% | Global, pipeline concentrated in North America | Short term (≤ 2 years) |

| Cost–efficacy concerns of ADCs in community settings | -1.1% | North America and Europe, emerging Asia-Pacific | Medium term (2-4 years) |

| Limited biomarker testing rates in low-income markets | -0.8% | Asia-Pacific, Middle East & Africa, Latin America | Long term (≥ 4 years) |

| Emerging payer pressure on combination regimens | -0.7% | North America and Europe, spreading globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High attrition of TNBC immunotherapy assets

Pembrolizumab plus chemotherapy improved survival only in PD-L1 positive TNBC patients, revealing the challenge of heterogeneity. Immune checkpoint inhibitors yield durable responses in fewer than 20% of cases, and toxicity escalates in combination regimens. The NIMBUS trial produced 20% objective-response rates overall, but 60% when tumor mutational burden exceeded 14 mutations per Mb. Combination approaches face 48.6% adverse-event rates versus 17.1% for monotherapy. As attrition curbs pipeline output, HER-2 negative breast cancer market expansion in TNBC slows.

Cost–efficacy concerns of ADCs in community settings

Trastuzumab deruxtecan’s incremental cost-effectiveness ratio surpasses USD 296,873 per QALY in HER2-low disease, well above payer thresholds. Community practices struggle to manage ADC-related interstitial-lung-disease rates of 4.2% with datopotamab deruxtecan, requiring specialized monitoring. Precise HER2-low classification depends on advanced pathology services often lacking outside academic centers. Step therapy and prior authorization delay access, and full care costs include monitoring, supportive care, and potential discontinuation. These factors temper HER-2 negative breast cancer market growth in community settings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy Type: Targeted therapy disrupts traditional paradigms

Chemotherapy retained a 41.10% share of the HER-2 negative breast cancer market size in 2025, but targeted therapy is forecast to grow at 9.02% CAGR between 2026 and 2031. PARP inhibitors, CDK4/6 inhibitors, and ADCs deliver longer progression-free survival with fewer systemic toxicities, prompting clinicians to shift treatment algorithms. Olaparib’s success in adjuvant BRCA-mutant disease extends PARP relevance beyond metastatic settings. CDK4/6 inhibitors combined with aromatase inhibitors provide median progression-free survival over 30 months, surpassing historical endocrine monotherapy. Immunotherapy is standard in PD-L1 positive TNBC after the KEYNOTE-522 trial. ADCs such as trastuzumab deruxtecan broaden reach to HER2-low tumors and re-define sequencing. The HER-2 negative breast cancer market therefore pivots toward mechanism-specific regimens that personalize benefit.

Endocrine therapy remains backbone treatment for hormone receptor-positive disease, yet resistance drives demand for next-generation agents. Selective estrogen-receptor degraders like imlunestrant improved progression-free survival in ESR1-mutant populations and foreshadow a new combination partner for CDK4/6 inhibitors. The influx of biosimilars in chemotherapy and HER2-targeted segments exerts price pressure, but advanced targeted regimes sustain premium pricing through differentiated efficacy. Cumulatively, targeted therapy adoption accelerates the HER-2 negative breast cancer market and relegates conventional chemotherapy to later-line or combination use.

By Biomarker Sub-Type: TNBC momentum challenges HR-positive dominance

Hormone receptor-positive/HER2-negative tumors held 57.25% share of the HER-2 negative breast cancer market size in 2025, yet triple-negative breast cancer will grow fastest at 9.42% CAGR through 2031. Sacituzumab govitecan plus pembrolizumab cut disease-progression risk by 35% in PD-L1 positive metastatic TNBC, establishing ADC-immunotherapy synergy. Multiple ADCs targeting TROP-2 and LIV-1 are in late development, diversifying options for TNBC patients historically limited to chemotherapy.

Resistance to endocrine and CDK4/6 regimens in HR-positive disease propels innovations such as inavolisib, which lowered progression-risk by 57% in PIK3CA-mutated tumors. The KENDO trial showed CDK4/6 inhibitors outperformed chemotherapy with 19.9 months median progression-free survival versus 11.2 months. Although HR-positive disease retains volume dominance, TNBC growth outpaces due to greater unmet need, bolstering overall HER-2 negative breast cancer market expansion.

By End User: Specialty centers capitalize on complexity

Hospitals controlled 53.10% of market revenue in 2025, yet specialty cancer centers are predicted to grow at a 9.95% CAGR because precision-oncology delivery demands integrated genomic testing, multidisciplinary teams, and advanced toxicity management. Seventy-two percent of metastatic tumors harbor actionable alterations requiring molecular-tumor-board review. ADC-related safety monitoring calls for high-resolution imaging and pulmonology support, capacities more common in tertiary centers.

AI-enabled trial-matching systems achieve 93.3% accuracy and are being adopted fastest in academic networks. Community practices, constrained by reimbursement cuts and staff shortages, struggle to invest in genomic platforms and clinical-research infrastructure. Consequently, referral patterns shift complex HER-2 negative breast cancer market cases to specialty centers, consolidating expertise and fostering faster uptake of innovative therapies.

Geography Analysis

North America captured 41.85% of 2025 revenue, driven by early adoption of precision diagnostics, robust clinical-trial ecosystems, and streamlined FDA approvals for datopotamab deruxtecan and trastuzumab deruxtecan. AI-guided trial-matching cuts screen-failure rates and accelerates first-patient-in timelines, reinforcing the region’s leadership. Yet payers question ADC value as cost-effectiveness ratios exceed USD 296,873 per QALY, leading to step therapy protocols that slow uptake. Canada exemplifies cost management through de-escalated bone-targeted-agent schedules that reduce expenditures without compromising outcomes.

Europe follows with mature health-technology-assessment frameworks and pan-EU regulatory coordination. Lombardy’s genomic-testing reimbursement paved the way for wider adoption, and CHMP backed trastuzumab deruxtecan for HER2-low disease in February 2025. However, dual-manufacturer combination regimens see lower reimbursement approval, reflecting payer concern over bundled pricing. Eastern-European markets still lack widespread biomarker-testing infrastructure, delaying entry of complex targeted therapies.

Asia-Pacific posts the highest growth rate at 10.35% CAGR as breast-cancer incidence rises from 1.25 million cases in 2021 to 1.68 million by 2030. Japan approved and launched datopotamab deruxtecan within 90 days, highlighting regulatory agility. China’s projected breast-cancer cost surge from USD 8 billion in 2021 to USD 14 billion by 2030 underscores the economic weight of the HER-2 negative breast cancer market.Thailand’s Pathum Raksa initiative shows how public-private models can extend testing capacity and could be replicated across emerging markets.

Competitive Landscape

Competition is intensifying as precision approaches displace legacy chemotherapy. CDK4/6 inhibitors—palbociclib, ribociclib, and abemaciclib—dominate HR-positive therapy, but biosimilar erosion looms once patents lapse. ADC developers pursue novel targets such as TROP-2, LIV-1, and HER3; trastuzumab deruxtecan’s success in HER2-low tumors spurred a wave of follow-on programs. Combination development aligns therapies with molecular drivers and aims to delay resistance, exemplified by datopotamab deruxtecan plus durvalumab in neoadjuvant trials.

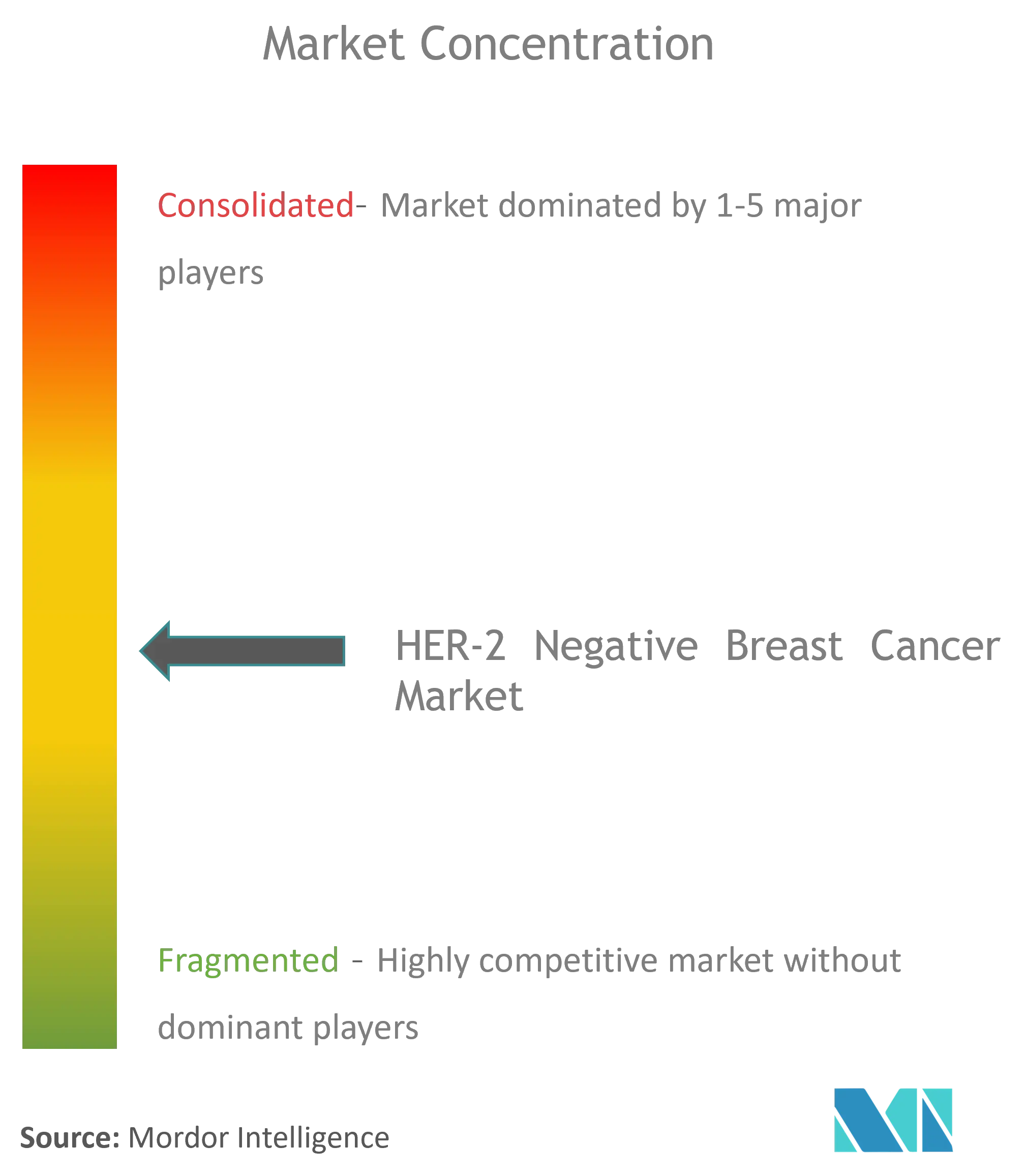

Technology partnerships bring AI into clinical-trial matching, reducing recruitment timelines by double digits and improving portfolio productivity. Price pressure fosters indication-specific pricing and value-based agreements to reconcile premium drug costs with constrained health-budget growth. Biosimilars, including FDA-approved trastuzumab-strf, will lower prices but manufacturing complexity delays similar dynamics for ADCs. Overall, the HER-2 negative breast cancer market exhibits moderate fragmentation as innovators race to capture emerging molecular niches while defending incumbent franchises.

Global HER-2 Negative Breast Cancer Industry Leaders

Eli Lilly and Company

AstraZeneca

GSK

Novartis AG

Pfizer

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: AstraZeneca began the Phase III TROPION-Breast04 neoadjuvant study of datopotamab deruxtecan plus durvalumab in early-stage triple-negative or HR-low/HER2-negative disease.

- January 2025: FDA approved DATROWAY for unresectable or metastatic HR-positive, HER2-negative disease after endocrine therapy and chemotherapy, citing a 37% risk reduction in progression versus chemotherapy

Global HER-2 Negative Breast Cancer Market Report Scope

The HER-2 negative breast cancer is less occurrence among women and accounts for about 15% of all types of breast cancers. The HER-2 Negative Breast Cancer Market is segmented By Type of Treatment (Chemotherapy, Radiation Therapy, Hormonal Therapy, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report offers the value (in USD million) for the above segments.

| Chemotherapy |

| Endocrine Therapy |

| Targeted Therapy (PARP, PI3K, AKT, ADCs) |

| Immunotherapy |

| HR-Positive / HER2-Negative |

| Triple-Negative Breast Cancer (TNBC) |

| Hospitals |

| Specialty Cancer Centers |

| Others |

| North America | United States |

| Canada | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Therapy Type (Value) | Chemotherapy | |

| Endocrine Therapy | ||

| Targeted Therapy (PARP, PI3K, AKT, ADCs) | ||

| Immunotherapy | ||

| By Biomarker Sub-Type (Value) | HR-Positive / HER2-Negative | |

| Triple-Negative Breast Cancer (TNBC) | ||

| By End User (Value) | Hospitals | |

| Specialty Cancer Centers | ||

| Others | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the HER-2 negative breast cancer market?

The HER-2 negative breast cancer market size is USD 1.97 billion in 2026, with an 8.12% CAGR projected to lift revenue to USD 2.91 billion by 2031.

Which therapy segment is growing fastest?

Targeted therapy—including PARP inhibitors, CDK4/6 inhibitors, and antibody-drug conjugates—is projected to grow at a 9.02% CAGR from 2026-2031.

Why is Asia-Pacific considered the most attractive regional market?

Asia-Pacific shows the highest forecast CAGR of 10.35% owing to rising disease incidence, rapid regulatory approvals, and expanding access to precision medicine.

What is driving growth in specialty cancer centers?

Complex biomarker testing, multidisciplinary care, and management of ADC-related toxicities push patients toward specialty centers, which are forecast to grow at 9.95% CAGR.

Page last updated on: