Male Hypogonadism Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

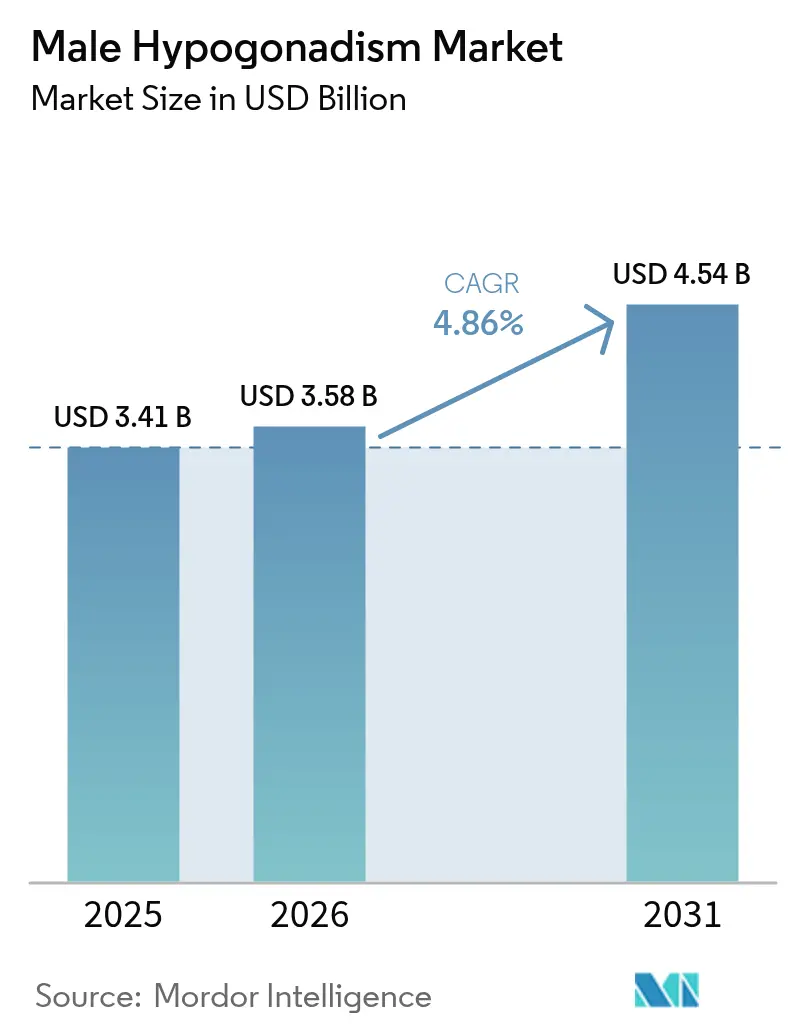

| Market Size (2026) | USD 3.58 Billion |

| Market Size (2031) | USD 4.54 Billion |

| Growth Rate (2026 - 2031) | 4.86% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Male Hypogonadism Market Analysis by Mordor Intelligence

male hypogonadism market size in 2026 is estimated at USD 3.58 billion, growing from 2025 value of USD 3.41 billion with 2031 projections showing USD 4.54 billion, growing at 4.86% CAGR over 2026-2031. Sustained growth reflects a favorable mix of demographic aging, higher obesity prevalence, and recent regulatory actions that lowered prescribing barriers for testosterone products. The February 2025 withdrawal of cardiovascular warnings from testosterone labels removed a long-standing deterrent for physicians and patients. At the same time, multiple oral testosterone undecanoate approvals and the continuing shift toward tele-endocrinology platforms are expanding therapy access. Competitive intensity is rising as firms invest in long-acting injectables, oral delivery systems, and vertically integrated supply chains to buffer raw-material shocks.

Key Report Takeaways

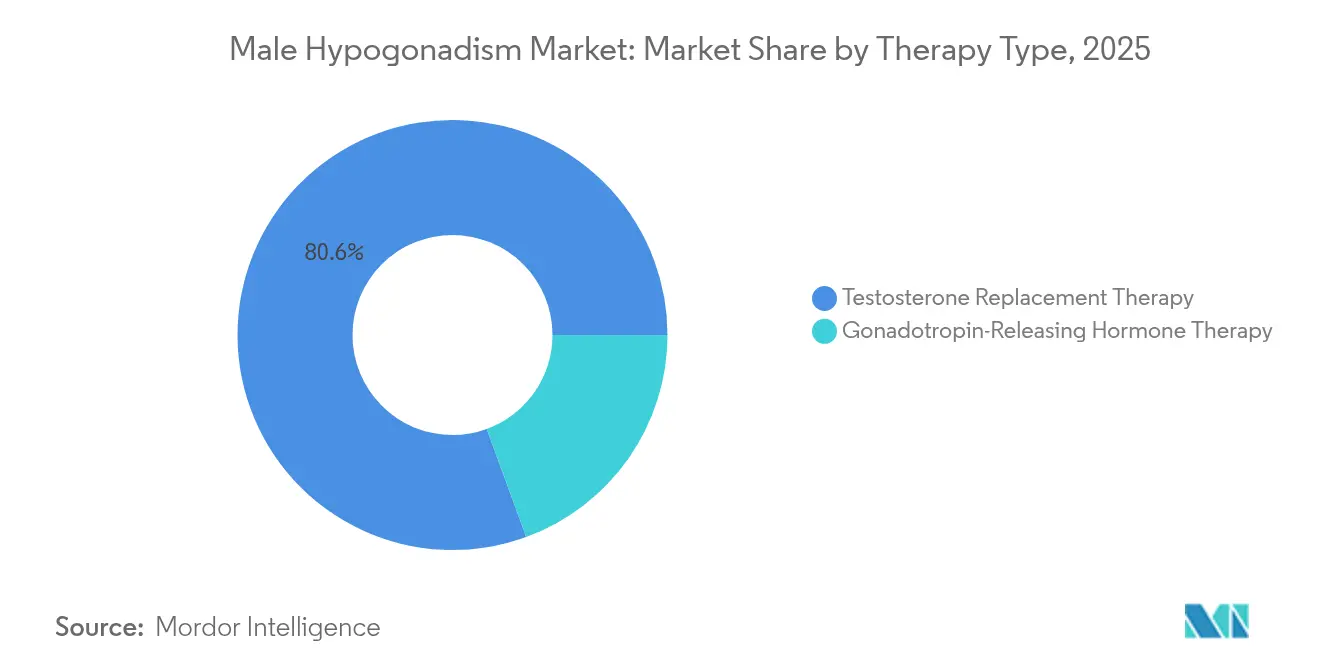

- By therapy type, testosterone replacement therapy held 80.57% of male hypogonadism market share in 2025, while gonadotropin-releasing hormone therapy is tracking a 5.42% CAGR through 2031.

- By route of administration, injectables led with 60.42% share of the male hypogonadism market size in 2025; oral formulations are projected to expand at a 5.53% CAGR to 2031.

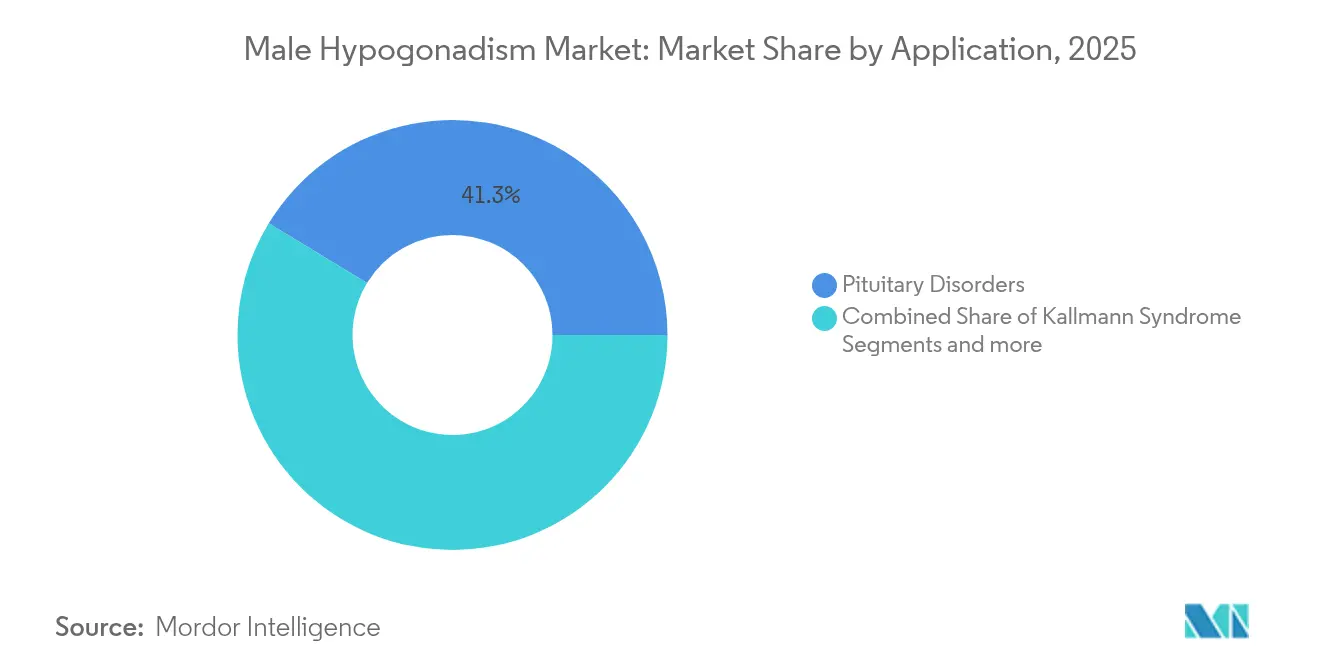

- By application, pituitary disorders commanded 41.31% of the male hypogonadism market share in 2025, whereas Kallmann syndrome treatments are set to grow at a 5.66% CAGR between 2026-2031.

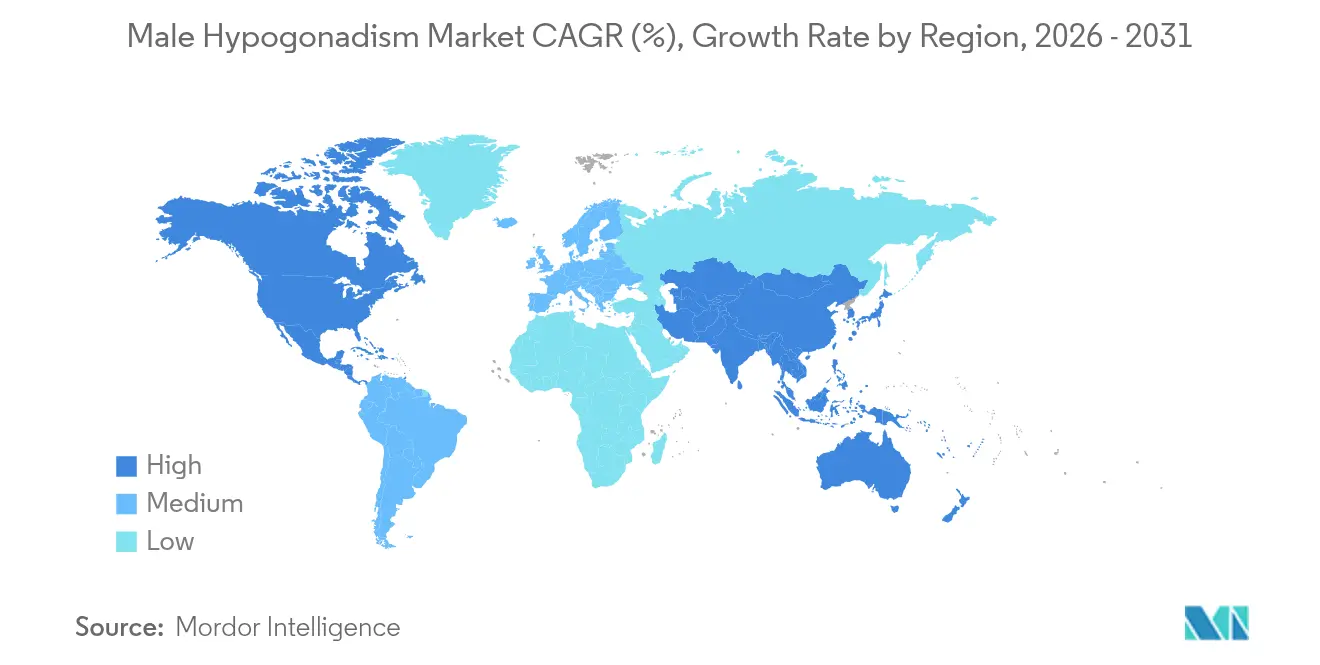

- By geography, North America accounted for 40.79% of 2025 revenue, while Asia-Pacific is poised for the fastest 5.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Male Hypogonadism Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global prevalence of testosterone-deficiency diagnoses | +1.2% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Rapid uptake of long-acting injectable & oral testosterone formulations | +0.9% | North America & EU primary, APAC emerging | Short term (≤ 2 years) |

| Growing use of tele-endocrinology & direct-to-consumer online pharmacies | +0.7% | North America core, expanding to APAC urban centers | Medium term (2-4 years) |

| Ageing/obesity co-morbidity funnel enlarging the treatable pool | +1.1% | Global, accelerated in developed markets | Long term (≥ 4 years) |

| Payer shift toward covering hypogonadism as quality-of-life disorder | +0.6% | North America & Western Europe | Medium term (2-4 years) |

| Military & sports-medicine screening programmes in emerging markets | +0.3% | APAC, MEA, with pilot programs in Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Prevalence of Testosterone-Deficiency Diagnoses

Automated free-testosterone assays cleared in 2025 report results in 48 minutes and improve detection accuracy in obese patients with low sex-hormone-binding globulin [1]Revvity Diagnostics, “Automated Free Testosterone Assay Clearance,” revvity.com. Clear diagnostic algorithms and wider physician training reduce historical under-screening, raising the number of confirmed cases. Payers now view early therapy as cost-effective because untreated hypogonadism drives metabolic and cardiovascular comorbidities. As screening becomes routine for men over 40, the diagnosed population feeding into the male hypogonadism market keeps enlarging.

Rapid Uptake of Long-Acting Injectable & Oral Testosterone Formulations

Oral testosterone undecanoate normalizes hormone levels in 87.8% of patients without dose titration. Subcutaneous autoinjectors such as Xyosted simplify self-administration, cut clinic visits, and reduce injection-site reactions. Long-acting intramuscular products given every 10-14 weeks stabilize serum curves and improve adherence. Firms owning advanced delivery patents—Antares Pharma alone holds 26 U.S. autoinjector patents valid through 2038—protect pricing power and sustain expansion. These innovations underpin volume growth across all mature regions of the male hypogonadism market.

Growing Use of Tele-Endocrinology & Direct-to-Consumer Online Pharmacies

Digital platforms pair at-home testosterone testing with virtual endocrinology consults, addressing the 40% of men over 45 who present with low hormone levels. Relaxed interstate licensing and controlled-substance e-prescribing rules widen reach, especially in rural U.S. counties and APAC megacities. Algorithms guide dose adjustments, while subscription kits bundle medications, needles, and follow-up labs, embedding lifetime value. These models expand access and bring new, younger cohorts into the male hypogonadism market.

Ageing/Obesity Co-Morbidity Funnel Enlarging the Treatable Pool

Clinical data link body-mass-index increases to steeper testosterone decline, raising type 2 diabetes risk when levels fall below 16 nmol/L. Weight-loss programs improve endogenous production, while testosterone therapy itself aids fat-mass reduction and insulin sensitivity. Military studies show supplementation limits muscle loss under operational stress, hinting at preventive uses in physically demanding occupations. As global obesity remains unchecked, the treatable pool for the male hypogonadism market steadily widens.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cardio-vascular & prostate-cancer safety concerns | -0.8% | Global, with heightened scrutiny in EU regulatory markets | Short term (≤ 2 years) |

| Stringent US & EU REMS / controlled-substance regulations | -0.5% | North America & Europe primary, cascading to other regions | Medium term (2-4 years) |

| Supply instability of API testosterone & compounded products | -0.6% | Global, with acute impact in North America & Canada | Short term (≤ 2 years) |

| Social-media-driven OTC misuse prompting tighter oversight | -0.4% | North America & Europe core, expanding to APAC urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cardio-vascular & Prostate-Cancer Safety Concerns

The TRAVERSE trial met non-inferiority on major cardiac events, leading to February 2025 FDA label updates, yet higher pulmonary embolism and atrial-fibrillation signals require continued blood-pressure surveillance [2]U.S. Food and Drug Administration, "FDA issues class-wide labeling changes for testosterone products," fda.gov. European regulators still recommend conservative use until more long-term outcomes surface [3]European Medicines Agency, “EMA Surveillance of Testosterone Product Safety,” ema.europa.eu. Mandatory prostate screening raises patient costs and perceptions of risk, tempering uptake in otherwise eligible populations and dampening near-term male hypogonadism market growth.

Stringent US & EU REMS / Controlled-Substance Regulations

Stringent US &Schedule III status obliges secure storage, inventory audits, and verified prescriber enrollment, lifting compliance expenses for pharmacies and telehealth firms. REMS documentation slows onboarding of new entrants and limits cross-border shipments. Diverse national rules compel manufacturers to fragment supply chains, elevating working-capital needs and constraining the male hypogonadism market in lower-income regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy Type: TRT Dominance Faces GnRH Innovation

Testosterone replacement therapy commanded 80.57% of 2025 revenue, reinforcing its status as the first-line option for most etiologies. Injectables, patches, gels, and newly approved oral capsules anchor broad clinical familiarity, giving TRT a scale advantage within the male hypogonadism market. Gonadotropin-releasing hormone (GnRH) therapy, however, is advancing at a 5.42% CAGR on the appeal of fertility preservation in younger men.

Combination regimens that pair TRT with hCG or GnRH are gaining academic interest for optimizing spermatogenesis and symptom relief. Military research showing testosterone undecanoate’s efficacy in extreme-stress environments opens a path for performance maintenance indications. Continued patent activity around micro-encapsulation and lymphatic-absorption enhancers is likely to shape competitive positioning and sustain mid-term growth across both categories in the male hypogonadism market.

By Route of Administration: Injectable Leadership Challenged by Oral Innovation

Injectables retained 60.42% share in 2025, leveraging long-acting pharmacokinetics and physician habit. Prefilled autoinjectors now enable at-home administration, cutting ancillary clinic revenue yet driving adherence. Oral testosterone products, cleared after rigorous food-effect and hepatotoxicity studies, are scaling at a 5.53% CAGR. Their convenience targets needle-averse patients and aligns with chronic-disease adherence strategies, giving this modality outsized momentum inside the male hypogonadism market.

Transdermal gels and patches serve patients needing steady daily titration or those contraindicated for injectables. Supply-chain fragility around sterile glass vials underscores why oral capsules are viewed as a hedge. Manufacturers diversifying into multiple routes distribute risk and appeal to broader patient personas, reinforcing incremental gains for the overall male hypogonadism market size.

By Application: Pituitary Disorders Lead Kallmann Syndrome Growth

Secondary hypogonadism tied to pituitary dysfunction, obesity, and metabolic syndrome secured 41.31% of 2025 revenue. Screening protocols now bundle testosterone levels with HbA1c and lipid panels, integrating therapy into cardiometabolic care pathways. In contrast, Kallmann syndrome occupies a small base but is pacing at a 5.66% CAGR as improved genetic testing raises detection rates and patient advocacy expands access to specialized centers.

Klinefelter and chemotherapy-induced cases round out demand, each with well-defined clinical algorithms. Fertility-preservation counseling has become standard for younger cohorts, influencing the choice between TRT monotherapy and gonadotropin add-ons. Tailored approaches keep segment differentiation intact and sustain healthy competitive dynamics across the male hypogonadism market.

Geography Analysis

North America generated 40.79% of global sales in 2025 on the back of generous insurance coverage, telehealth penetration, and the post-label-change rebound in testosterone prescribing. The United States alone saw prescription volumes triple versus 2014 baselines, illustrating how regulatory clarity and digital health infrastructure accelerate therapy uptake. Cannibalization of older topical formulations by autoinjectors and orals is underway yet additive to total dollars, supporting steady male hypogonadism market growth.

Europe displays balanced forward momentum as guideline harmonization and payer willingness to fund quality-of-life therapies offset more conservative cardiovascular safety positions. EMA monitoring frameworks emphasize confirmed biochemical deficiency before initiation, channeling volumes toward certified specialty clinics. Supply scarcities in select EU states sparked cross-border pharmacy transactions that, while temporary, showcased latent demand elasticity within the male hypogonadism market size.

Asia-Pacific is the fastest-rising region at a 5.55% CAGR through 2031. Aging populations in Japan, South Korea, and urban China, coupled with expanding obesity prevalence, create sizable addressable cohorts. Local launches of oral undecanoate products sidestep injection-related stigma, while national military-fitness programs amplify screening. Market penetration remains low in tier-2 cities, leaving ample runway for future expansion of the male hypogonadism market.

Competitive Landscape

Industry structure is moderately fragmented. AbbVie, Bayer, and Pfizer anchor the top tier with broad modality portfolios and entrenched prescriber relationships. These incumbents defend share through lifecycle management, including novel dosing devices and co-marketing with telehealth clinics. Mid-sized innovators such as Marius Pharmaceuticals and Clarus Therapeutics ride patent-protected oral technologies to carve out loyalty among compliance-focused patients.

Delivery-platform specialization is a critical moat. Antares Pharma’s expansive autoinjector patent wall shields margins until at least 2038 while attracting white-label deals from larger biologics players. Vertical integration into active-pharmaceutical-ingredient synthesis—pursued by Bayer and a handful of Indian contract manufacturers—mitigates supply instability, an advantage spotlighted by 2024’s North American shortages.

Strategic transactions signal further consolidation. The March 2025 Mallinckrodt-Endo merger combines sterile-injectable capacity with testosterone product franchises to capture scale synergies and negotiate better wholesaler terms. Digital-health partnerships proliferate as traditional drug makers seek data-rich patient funnels. The competitive chessboard therefore balances brand heft, technology control, and channel agility, shaping future leadership in the male hypogonadism market.

Male Hypogonadism Industry Leaders

-

Endo International Plc

-

AbbVie Inc

-

Pfizer Inc

-

Teva Pharmaceutical Industries Ltd

-

Allergan Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Mallinckrodt and Endo announced a merger to create a diversified pharmaceutical platform with AVEED testosterone undecanoate among its flagship assets.

- March 2025: Marius Pharmaceuticals partnered with a major academic medical center to expand research and physician education on oral testosterone therapy.

- February 2025: The FDA removed cardiovascular warnings from all testosterone labels and added mandatory blood-pressure monitoring requirements after reviewing TRAVERSE trial data.

- December 2024: Azurity Pharmaceuticals launched AZMIRO, the first FDA-approved prefilled 200 mg/mL testosterone cypionate syringe for hypogonadal men.

Global Male Hypogonadism Market Report Scope

As per the scope of the report, Male hypogonadism or testosterone deficiency, is a failure of the testes to produce the male sex hormone testosterone, sperm, or both. It can be due to the result of a disease process involving the hypothalamus and pituitary gland or testicular disorder. Male hypogonadism market is segmented by therapy type, application and geography.

| Testosterone Replacement Therapy | |

| Gonadotropin-Releasing Hormone Therapy | Human Chorionic Gonadotropin (hCG) |

| Follicle-Stimulating Hormone (FSH) | |

| Gonadotropin-Releasing Hormone (GnRH) | |

| Other Gonadotropin Therapies |

| Injectable |

| Oral |

| Others |

| Kallmann Syndrome |

| Klinefelter's Syndrome |

| Pituitary Disorders |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapy Type | Testosterone Replacement Therapy | |

| Gonadotropin-Releasing Hormone Therapy | Human Chorionic Gonadotropin (hCG) | |

| Follicle-Stimulating Hormone (FSH) | ||

| Gonadotropin-Releasing Hormone (GnRH) | ||

| Other Gonadotropin Therapies | ||

| By Route of Administration | Injectable | |

| Oral | ||

| Others | ||

| By Application | Kallmann Syndrome | |

| Klinefelter's Syndrome | ||

| Pituitary Disorders | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the male hypogonadism market in 2026?

It is valued at USD 3.58 billion, with a 4.86% CAGR projected through 2031.

Which therapy type currently dominates treatment?

Testosterone replacement therapy accounts for 80.57% of 2025 revenue.

What region is growing the fastest for male hormone therapy?

Asia-Pacific is forecast to expand at a 5.55% CAGR between 2026-2031.

Why are oral testosterone products gaining share?

They eliminate needle aversion, offer dose convenience, and match injectables on efficacy while simplifying supply logistics.

How did the 2025 FDA label change affect demand?

Removing prior cardiovascular warnings lowered prescriber hesitation, directly boosting new-therapy initiations in North America.

What is the highest-impact growth driver going forward?

Rising diagnostic rates from automated free-testosterone testing are expected to add 1.2% to the forecast CAGR.

Page last updated on: