HER2-positive Breast Cancer Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

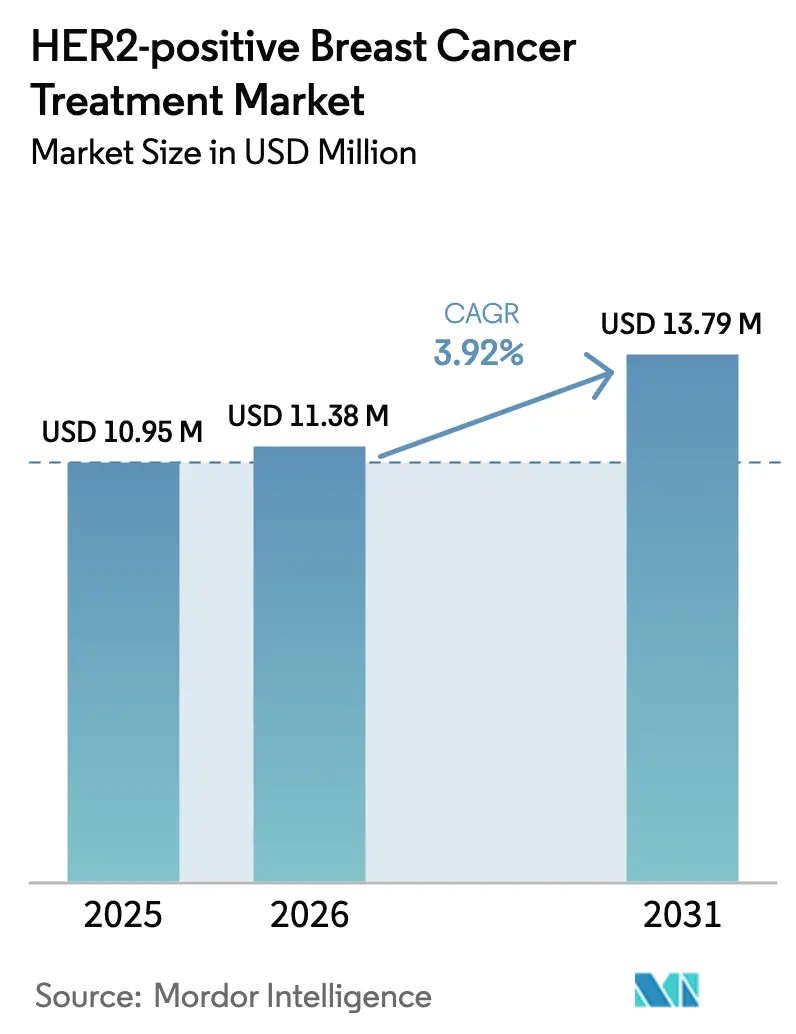

| Market Size (2026) | USD 11.38 Million |

| Market Size (2031) | USD 13.79 Million |

| Growth Rate (2026 - 2031) | 3.92% CAGR |

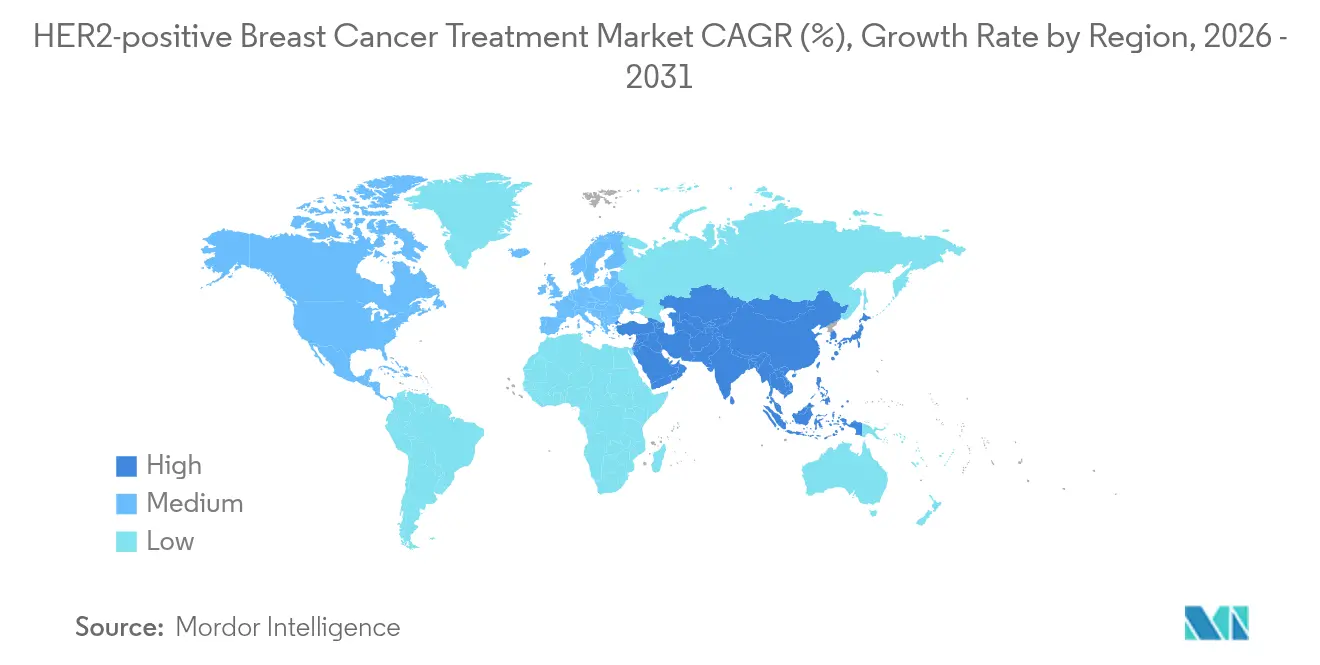

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HER2-positive Breast Cancer Treatment Market Analysis by Mordor Intelligence

HER2-positive breast cancer treatment market size in 2026 is estimated at USD 11.38 billion, growing from 2025 value of USD 10.95 billion with 2031 projections showing USD 13.79 billion, growing at 3.92% CAGR over 2026-2031. The HER2-positive breast cancer treatment market is progressing along a moderate yet resilient growth trajectory as mature monoclonal antibodies absorb biosimilar pressure, while next-generation antibody-drug conjugates (ADCs) command premium prices and expand their clinical use. Precision-medicine advances now extend eligibility from classic HER2-positive tumors to HER2-low and HER2-ultralow expressions, thereby enlarging the addressable pool of HER2-targeted therapeutics. Regional growth patterns hinge on faster regulatory approvals across the Asia-Pacific, supply-chain expansion, and widening reimbursement, while digital channels are increasingly influencing patient access. Capacity constraints for complex bioconjugation, evolving FDA accelerated approval guidelines, and cardiotoxicity monitoring requirements pose operational and compliance risks for manufacturers.

Key Report Takeaways

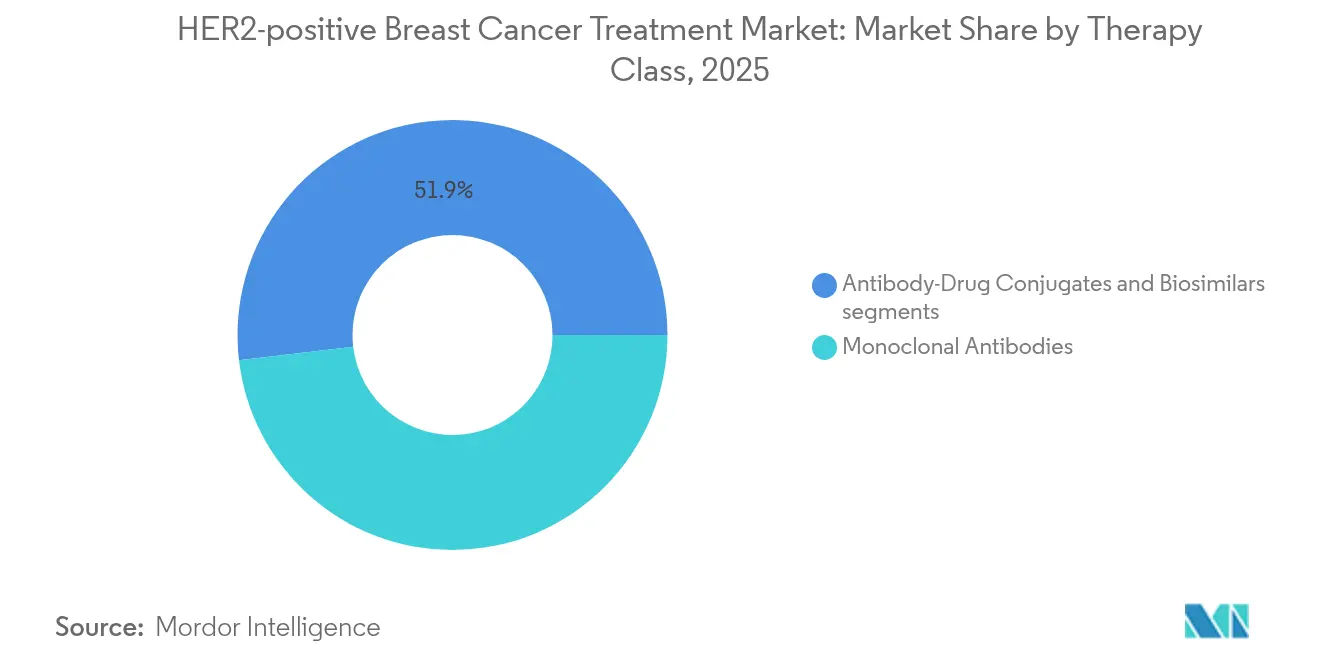

- By 2025, monoclonal antibodies led the HER2-positive breast cancer treatment market with 48.12% of the market share, whereas ADCs are projected to expand at a 4.70% CAGR through 2031.

- By disease stage, metastatic/recurrent disease accounted for 56.62% of the HER2-positive breast cancer treatment market size in 2025 and is projected to grow at a 4.79% CAGR.

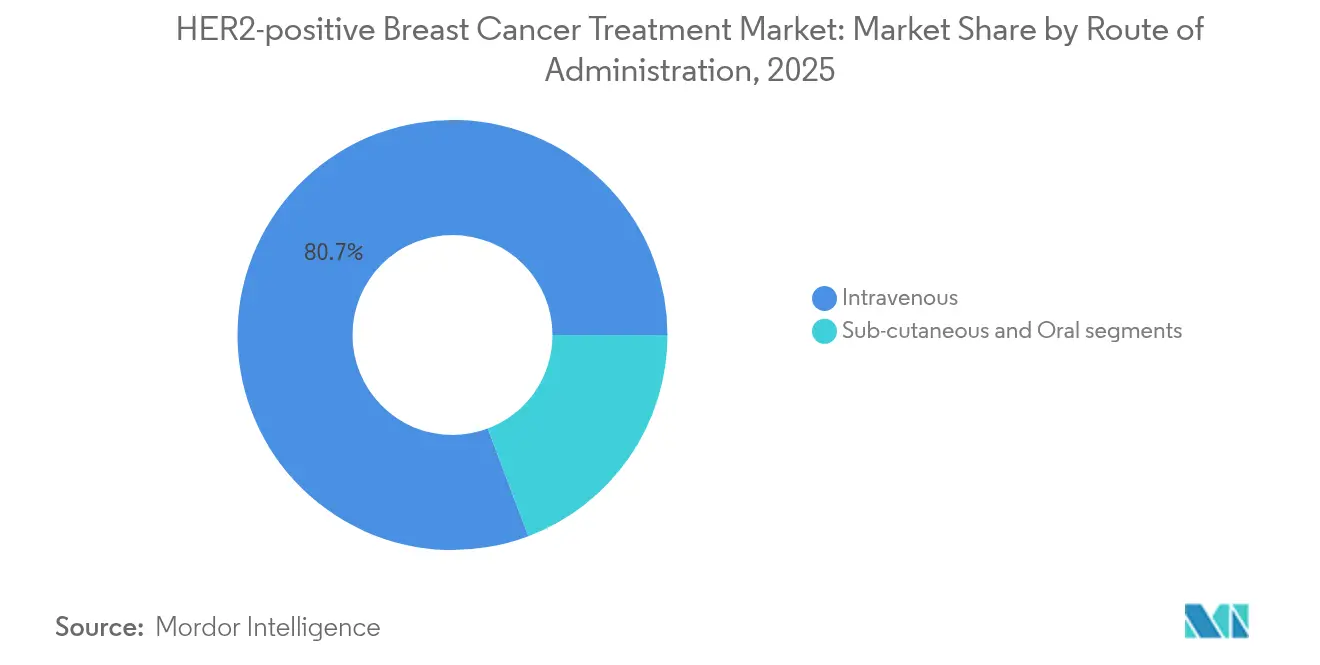

- By route of administration, intravenous products dominated with 80.74% revenue in 2025; subcutaneous formulations posted the strongest 4.88% CAGR to 2031.

- By distribution channel, hospital pharmacies controlled 63.74% of 2025 sales, while online pharmacies are forecast to post a 4.97% CAGR.

- By geography, North America accounted for 41.52% of the revenue in 2025; the Asia-Pacific region exhibits the fastest growth at a 5.04% CAGR from 2025 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global HER2-positive Breast Cancer Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mainstay efficacy of HER2-targeted mAbs & ADCs | +0.8% | Global | Long term (≥ 4 years) |

| Rapid ADC pipeline progress & FDA RMAT designations | +1.2% | North America & EU, spill-over to APAC | Medium term (2-4 years) |

| Sub-cutaneous, fixed-dose combos raising adherence | +0.6% | Global, with early gains in developed markets | Medium term (2-4 years) |

| Biosimilar uptake widening global patient access | +0.7% | Global, particularly emerging markets | Short term (≤ 2 years) |

| AI-driven HER2 scoring improving eligible pool | +0.5% | North America & EU core, expanding to APAC | Long term (≥ 4 years) |

| Low-HER2 & HER2-mutant labeling expansions | +0.9% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mainstay efficacy of HER2-targeted mAbs and ADCs

Decades of real-world data confirm that trastuzumab and pertuzumab remain clinical workhorses across early and metastatic breast cancer, sustaining volume even as biosimilars proliferate. The PERSEPHONE study showed that six-month adjuvant trastuzumab delivers disease-free survival comparable to a 12-month course, preserving outcomes while nearly halving drug spend. ADCs such as trastuzumab deruxtecan achieve objective response rates above 50% in breast, gastric, and lung tumors, setting new efficacy benchmarks. Their tumor-agnostic potential widens the HER2-positive breast cancer treatment market by reclassifying patients previously labeled “HER2-negative.” Payers, therefore, remain willing to reimburse premium ADC prices to capture improved survival, offsetting revenue lost to antibody biosimilars.

Rapid ADC pipeline progress and FDA RMAT designations

The FDA now extends its RMAT framework to innovative ADC platforms that demonstrate transformative benefit, shortening development timelines by several months and catalyzing investment. Daiichi Sankyo and AstraZeneca have more than ten late-stage ADCs in the clinic, supported by over USD 4 billion in global manufacturing projects[1]Source: AstraZeneca PLC, “AstraZeneca to Build ADC Manufacturing Facility in Singapore,” astrazeneca.com. Purpose-built sites in Singapore and Germany add conjugation capacity and lower logistical risk. These capital projects underpin the next wave of indications, sustaining the HER2-positive breast cancer treatment market as first-generation biologics plateau

Subcutaneous fixed-dose combinations raising adherence

Phase III data from FeDeriCa proved that nearly 90% of patients prefer subcutaneous trastuzumab-pertuzumab over intravenous infusion, citing convenience and shorter clinic visits. Fixed dosing eliminates weight-based calculations, cuts chair time to under 30 minutes, and reduces nursing hours, which helps offset higher acquisition costs. Hospital administrators increasingly factor total-cost-of-care savings when negotiating supply contracts, bolstering commercial traction for subcutaneous launches by Roche and its partners.

Biosimilar uptake widening global patient access

European buying consortia report price declines of 30-50% following the fourth listing of trastuzumab biosimilars. Emerging-market ministries of health are translating these savings into population-wide treatment protocols, raising volumes in public oncology programs. Originator firms are countering margin erosion by pivoting toward newer modalities and securing formulary preference for differentiated presentations, yet the volume lift preserves a sizable base for the HER2-positive breast cancer treatment market.

Restraints Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cardiotoxicity monitoring costs & infrastructure gaps | -0.4% | Global, particularly emerging markets | Short term (≤ 2 years) |

| ADC manufacturing capacity bottlenecks | -0.6% | Global | Medium term (2-4 years) |

| Rising biosimilar price pressure on innovators | -0.3% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| Molecular resistance via p95HER2 & MUC4 masking | -0.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cardiotoxicity monitoring costs and infrastructure gaps

Regular echocardiography or MUGA scans add up to USD 2,000 in annual per-patient costs, which can exceed median household incomes in lower-middle-income countries. Limited imaging suites create scheduling delays that defer therapy starts, dampening uptake even when drugs are reimbursed. Training cardio-oncology specialists has lagged behind the therapeutic boom, leading to uneven service quality that constrains the HER2-targeted ttreatment market rollout in resource-strained geographies.

ADC manufacturing capacity bottlenecks

Conjugation lines demand high-containment infrastructure and analytic redundancy to handle cytotoxic payloads. Current global utilization exceeds 85%, stretching lead times for clinical supplies. Lonza[2]Source: Lonza Group, “Lonza Expands Visp Bioconjugation Capacity,” lonza.com and Fujifilm are adding multi-ton lines but most will not be fully operational before 2028, causing a temporary drag on product launch velocity. The supply pinch is particularly acute for mid-size biotech firms that rely on contract partners, limiting competitive breadth in the HER2-positive breast cancer treatment market until capacity expansions come online

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy Class: ADCs Drive Premium Growth

The HER2-positive breast cancer treatment market size for therapy classes shows monoclonal antibodies capturing 48.12% revenue in 2025, yet ADCs post a peer-leading 4.70% CAGR. Trastuzumab deruxtecan’s expansion into HER2-low or ultralow tumors lifts the HER2-positive breast cancer treatment market by accessing up to 40% of breast cancer cases previously untreated. Conversely, biosimilar copies of trastuzumab and pertuzumab penetrate hospital formularies, driving volume but compressing unit margins. TKIs remain niche but indispensable for oral maintenance, while biosimilars supply cost-effective backbone therapy. Manufacturing barriers and accelerated approvals provide ADC innovators with durable protection against imitation, reinforcing their contribution to the HER2-positive breast cancer treatment market through 2031.

Competitive tactics within classes mirror the balance between revenue defense and growth. Originator antibody manufacturers bundle drug with diagnostic programs to entrench share. ADC developers prioritize co-development deals that secure manufacturing slots early, mitigating supply risk. Across modalities, companies increasingly integrate AI-guided patient-selection algorithms into clinical trial design. These real-world evidence platforms reduce screening failures and quicken time-to-market, magnifying the addressable HER2-positive breast cancer treatment market.

By Disease Stage: Metastatic Dominance Persists

In 2025, metastatic disease accounted for 56.62% of global revenue, reflecting both the high incidence of late-stage presentations and the expanded use of tumor-agnostic labeling for ADCs. The HER2-positive breast cancer treatment market size for metastatic indications is forecasted to grow at a 4.79% CAGR, as earlier-line ADC adoption pushes premium therapies into first- and second-line settings. DESTINY-Breast06 demonstrated a 13.2-month median progression-free survival advantage over chemotherapy, prompting oncologists to reassess treatment algorithms. Early and adjuvant settings benefit from improved screening that detects disease sooner, yet face pronounced pricing pressure from biosimilars. Nonetheless, shorter trastuzumab regimens validated by PERSEPHONE support diffusion into lower-income systems, maintaining volume growth even as metastatic sales outpace.

Treatment sequencing is also evolving. Clinicians are leveraging real-time ctDNA monitoring to detect minimal residual disease, triggering escalation to ADCs before overt progression. This approach elongates response durations and further integrates high-value products into the HER2-positive breast cancer treatment market pathway. Payers are beginning to reimburse such biomarker-triggered intensification because it avoids the cost of unmanaged progression.

By Route of Administration: Subcutaneous Gains Momentum

Intravenous infusions held 80.74% share in 2025, yet subcutaneous deliveries will post a 4.88% CAGR to 2031. Subcutaneous injections reduce chair time from up to four hours to under half an hour and cut infusion reactions by eliminating large fluid volumes. Hospitals reallocate saved nursing hours to higher-acuity services, generating systemic efficiency. The technical complexity of formulating biologic combinations in a ready-to-inject syringe slows biosimilar follow-on entries, enabling originators to command steady premiums and expand the overall HER2-positive breast cancer treatment market. Oral TKIs remain limited to niche maintenance settings but still provide an adherence-friendly option that online pharmacies can distribute easily.

Capacity for home administration further widens the convenience gap. Pilot programs in Canada and the United Kingdom dispatch nurses to patient residences to deliver subcutaneous therapy safely. Early feedback shows high satisfaction and reduced travel burden, trends that could expand the HER2-positive breast cancer treatment market by reaching patients who previously forewent therapy due to logistical hurdles.

By Distribution Channel: Digital Transformation Accelerates

Hospital pharmacies accounted for 63.74% of 2025 revenue, confirming that complex drugs continue to flow through controlled channels. Yet the 4.97% CAGR forecast for online pharmacies signals a maturing e-commerce infrastructure in oncology. Electronic prescribing platforms now transmit validated and shipped orders directly to accredited specialty pharmacies that maintain cold-chain integrity. For oral TKIs and supportive medications, door-to-door delivery improves adherence tracking through integrated apps that record dosing events. Retail outlets remain a vital channel, particularly in markets where regulations require in-person pickup. As online interfaces sync with electronic health records, refill algorithms will further cement their role in the HER2-positive breast cancer treatment market continuum

Geography Analysis

North America generated 41.52% of global revenue in 2025, benefitting from early access to every major FDA-approved HER2 therapy, widespread insurance coverage, and dense networks of cardio-oncology centers. Uptake of trastuzumab deruxtecan in US academic centers is rapid because payers reimburse tumor-agnostic use shortly after approval. Growth in Canada is steadier as public health assessments impose cost-effectiveness filters, yet biosimilar savings are recycled into funding ADC uptake. The HER2-positive breast cancer treatment market in the United States must still navigate intensifying formulary reviews that challenge list-price increases, but patient volumes remain secure thanks to broad screening and guideline integration.

Asia-Pacific is the fastest-growing territory with a 5.04% CAGR through 2031. China’s National Medical Products Administration cleared trastuzumab deruxtecan for HER2-low breast cancer in 2024, opening a national market of more than 200,000 patients annually. Domestic firms such as BeiGene invest in end-to-end ADC manufacturing hubs in Guangzhou, ensuring localized supply. Japan drives high-value uptake via national health insurance that reimburses dual-target regimens once the Central Social Insurance Medical Council confirms economic benefit. India leans on biosimilars to bridge accessibility gaps, yet metastatic volumes rise as urban oncology networks expand diagnostic reach. As supply scales and regional trials proliferate, theHER2-positive breast cancer treatment market in Asia-Pacific will diversify beyond imported brands toward mixed local-global portfolios.

Europe maintains a balanced profile. The European Commission green-lit trastuzumab deruxtecan for HER2-ultralow tumors in 2025, synchronizing with FDA timelines. However, single-payer systems deploy centralized tenders that have driven biosimilar penetration above 60% for first-generation antibodies, sustaining public-sector budgets. Health technology assessment agencies reward robust real-world evidence and patient-reported outcomes, motivating manufacturers to collect granular data. The HER2-positive breast cancer treatment market in smaller Central and Eastern European nations benefits from pan-EU reference pricing, enabling quicker adoption once high-income states set precedents.

South America and the Middle East & Africa trail in absolute size but exhibit catch-up potential as local manufacturing joint ventures emerge. Brazil’s Fiocruz is exploring technology-transfer agreements for trastuzumab biosimilars, while Saudi Arabia’s Vision 2030 plan funds oncology centers that adhere to international guidelines. Incremental infrastructure growth improves the foundation for the HER2-positive breast cancer treatment market in these regions, but cardiology capacity and reimbursement hurdles remain medium-term challenges.

Competitive Landscape

The HER2-targeted therapeutics industry shows moderate concentration. Roche, AstraZeneca, Daiichi Sankyo, and Pfizer still command the lion's share, yet no single firm breaches dominance thresholds. Biosimilar entrants from Samsung Bioepis and Celltrion are eroding unit margins on legacy antibodies, while specialized biotech firms drive the ADC pipeline. Roche augmented its portfolio through the USD 1.0 billion Poseida Therapeutics acquisition, broadening into cell therapies that could complement ADC regimens. AstraZeneca and Daiichi Sankyo are jointly investing USD 1.5 billion in an ADC plant in Singapore to secure supply for expanding indications.

Strategic alliances dominate innovation funding. ArriVent's USD 615.5 million tie-up with Alphamab exemplifies risk-sharing models that grant access to Chinese discovery engines while reserving commercialization rights in the West. Large contract development and manufacturing organizations such as Lonza invest USD 1.2 billion to double bioconjugation capacity; these partners gain bargaining power as manufacturers jostle for slots. Diagnostic partnerships are also flourishing. Roche obtained FDA Breakthrough Device Designation for its AI-enabled HER2 IHC assay, embedding companion tests into product life cycles and reinforcing customer lock-in.

Competitive differentiation increasingly rests on manufacturing agility and diagnostic integration rather than molecule count alone. Companies that secure both dedicated production lines and regulatory-cleared diagnostics are better positioned to weather biosimilar erosion and sustain premium pricing, thereby shaping the future HER2-positive breast cancer treatment market landscape.

HER2-positive Breast Cancer Treatment Industry Leaders

Pfizer Inc.

AstraZeneca

F. Hoffmann-La Roche Ltd

Merck & Co., Inc.

Bayer AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Lotte Biologics opened its ADC manufacturing site in Syracuse, New York, after a USD 100 million retrofit.

- January 2025: FDA approved trastuzumab deruxtecan for unresectable or metastatic hormone receptor-positive HER2-low or ultralow breast cancer

Global HER2-positive Breast Cancer Treatment Market Report Scope

As per the scope of the report, HER2 (human epidermal growth factor receptor 2) is a protein that promotes the quick growth of breast cancer cells. Similarly, Her2-positive is a condition in which breast cancer cells have higher levels of HER2 proteins than normal levels. Overall, HER2-positive breast cancer is a type of cancer that tests positive for a protein called HER2.

The HER2-positive breast cancer treatment is segmented by treatment type, end user, and geography. By treatment type, the market is segmented into chemotherapy, targeted drug therapy, and other treatment types. By end user, the market is segmented into hospitals, specialty centers, homecare, and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (USD) for the above segments.

| Antibody-Drug Conjugates |

| Biosimilars |

| Early/ Neoadjuvant |

| Adjuvant |

| Metastatic/ Recurrent |

| Intravenous |

| Sub-cutaneous |

| Oral |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| Monoclonal Antibodies | Antibody-Drug Conjugates | |

| Biosimilars | ||

| By Disease Stage | Early/ Neoadjuvant | |

| Adjuvant | ||

| Metastatic/ Recurrent | ||

| By Route of Administration | Intravenous | |

| Sub-cutaneous | ||

| Oral | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the HER2-positive breast cancer treatment market?

The HER2-positive breast cancer treatment market size stands at USD 11.38 billion in 2026 and is projected to reach USD 13.79 billion by 2031 at a 3.92% CAGR.

Which therapy class is expanding the fastest?

ADCs are the fastest-growing segment, advancing at a 4.70% CAGR as they penetrate HER2-low and ultralow tumors and command premium pricing.

Why is Asia-Pacific the most rapidly expanding region?

Accelerated regulatory approvals, local manufacturing investments, and rising cancer incidence fuel a 5.04% CAGR, making Asia-Pacific the fastest-growing cluster within the HER2-positive breast cancer treatmentmarket.

How do biosimilars affect overall market growth?

Biosimilars lower costs by 30-50%, broaden access in price-sensitive regions, and push innovators to differentiate through ADCs and subcutaneous formulations, sustaining net market expansion.

What operational bottlenecks could restrict supply?

ADC manufacturing capacity remains tight, with global utilization above 85%; supply chain relief is expected once new plants in Singapore, Germany, and Switzerland come online between 2027 and 2029.

Page last updated on: