Merkel Cell Carcinoma Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

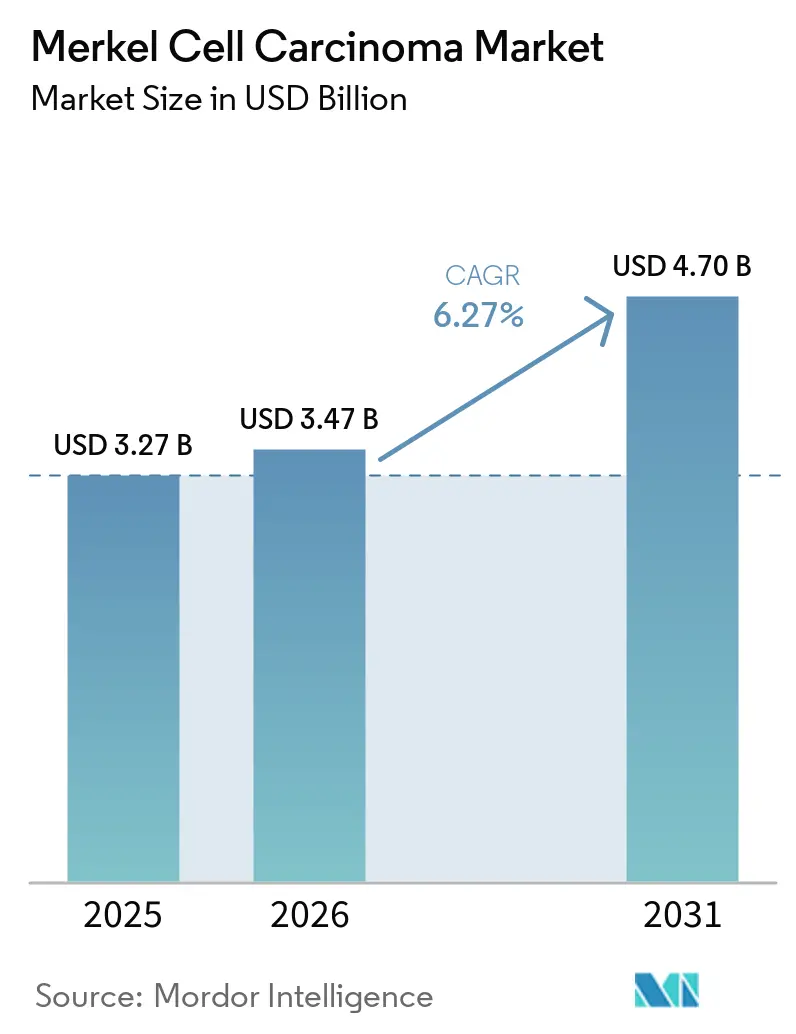

| Market Size (2026) | USD 3.47 Billion |

| Market Size (2031) | USD 4.70 Billion |

| Growth Rate (2026 - 2031) | 6.27% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Merkel Cell Carcinoma Market Analysis by Mordor Intelligence

The Merkel Cell Carcinoma Market size was valued at USD 3.27 billion in 2025 and is estimated to grow from USD 3.47 billion in 2026 to reach USD 4.70 billion by 2031, at a CAGR of 6.27% during the forecast period (2026-2031).

The disease remains commercially significant due to its rarity, aggressive nature, and its concentration among older and immunocompromised patients, whose numbers are increasing globally. Registry data from the United States shows a median diagnosis age above 75 years, with 76% of patients aged over 65. This ties the Merkel cell carcinoma market closely to aging demographics and the growing demand for long-term oncology care. The Merkel cell carcinoma market is expanding as newer drug approvals have increased the treated population rather than merely replacing older therapies. Additionally, emerging data on combination immunotherapies is shaping the competitive landscape. Market growth is further supported by longer treatment durations, closer patient follow-ups, and stronger adoption across specialist centers, reflecting the evolving dynamics of institutional care.

Key Report Takeaways

- By modality, treatment accounted for 68.32% of revenue in 2025, while diagnosis is projected to expand at a 7.96% CAGR through 2031.

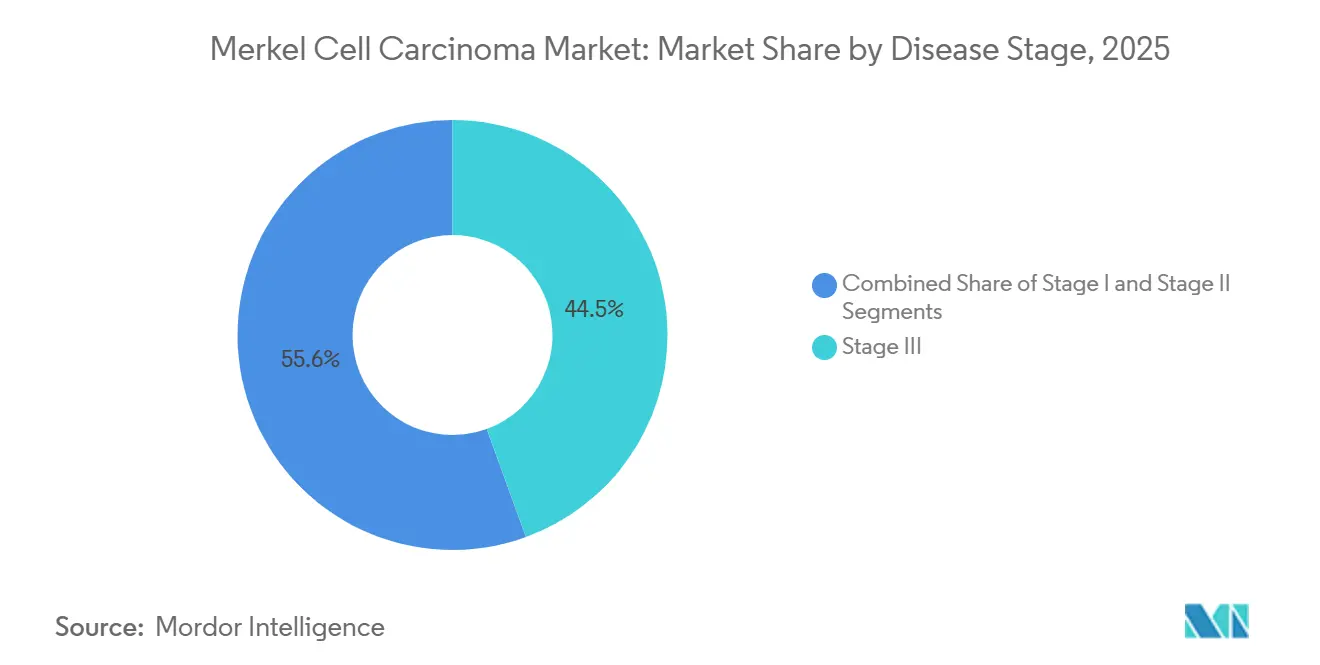

- By disease stage, Stage III held 44.45% of the Merkel cell carcinoma market share in 2025, and it is also forecasted to record the highest CAGR at 7.28% through 2031.

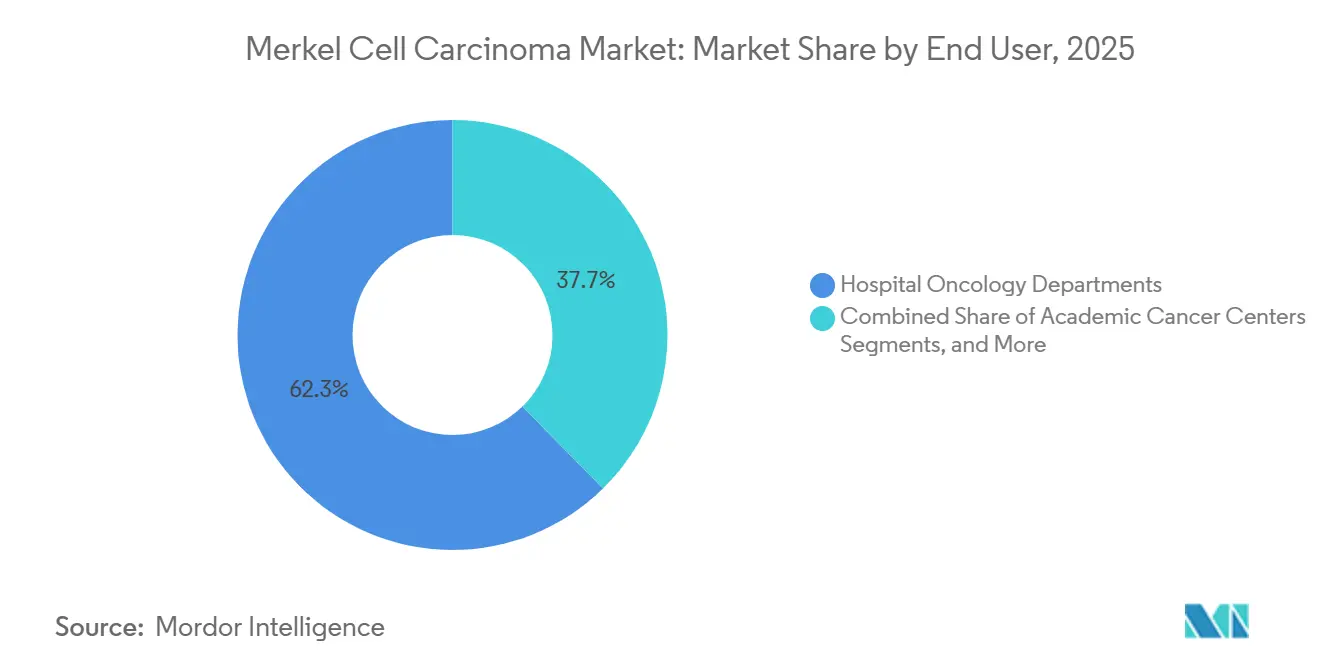

- By end user, Hospital Oncology Departments captured 62.34% of revenue in 2025, while Academic Cancer Centers are projected to grow at an 8.35% CAGR through 2031.

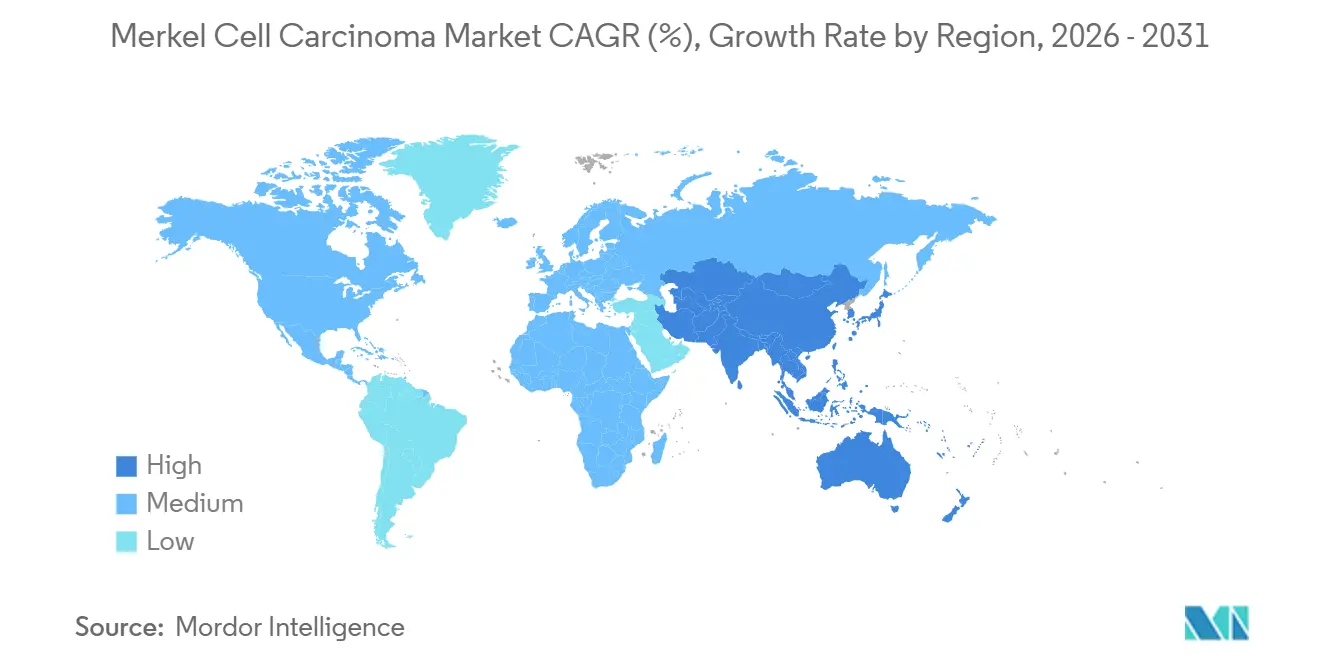

- By geography, North America remained the largest regional contributor in 2025, while Asia-Pacific is the fastest-growing region over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Merkel Cell Carcinoma Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising elderly and immunosuppressed patient population | +1.4% | Global, with concentrated effect in North America, Europe, Japan, and Australia | Long term (≥ 4 years) |

| Checkpoint inhibitors entrenched in treatment guidelines | +1.2% | North America and EU, with spillover to APAC | Medium term (2-4 years) |

| Additional PD-1 option broadening patient access | +0.5% | US, EU, Canada, Switzerland, Japan | Short term (≤ 2 years) |

| Chemo-to-immunotherapy treatment shift in systemic therapy | +0.6% | Global, with highest delta impact in emerging markets transitioning from chemotherapy | Medium term (2-4 years) |

| ctDNA-guided surveillance adoption expanding monitoring revenue | +0.5% | North America, with early uptake in EU academic centers | Short term (≤ 2 years) |

| Adjuvant immunotherapy readouts expanding eligible patient pool | +0.4% | North America and EU first, followed by APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Elderly and Immunosuppressed Patient Population

The Merkel cell carcinoma market benefits from a rising patient base, particularly among older demographics where the disease is most prevalent. A review of 11,574 cases in the United States reported a median diagnosis age of 77 years, with diagnoses from 2016 to 2021 linked to improved survival rates, indicating better detection in older groups.[1]National Comprehensive Cancer Network, “NCCN Clinical Practice Guidelines in Oncology, Merkel Cell Carcinoma, Version 2.2026,” NCCN Guidelines, merkelcell.org Additionally, a 23.8-fold increased risk in solid organ transplant recipients and a 13.4-fold risk in untreated HIV-positive individuals highlight the market's reliance on high-risk immunosuppressed populations. This demand is further driven by the need for frequent monitoring and specialist care, ensuring sustained market growth despite the disease's rarity.

Checkpoint Inhibitors Entrenched in Treatment Guidelines

Checkpoint inhibitors have become the standard treatment for advanced Merkel cell carcinoma, replacing chemotherapy in major reimbursement settings. NCCN guidelines list pembrolizumab, avelumab, nivolumab, and retifanlimab as first-line options for unresectable or metastatic cases. Clinical studies show a median response duration of 39.8 months for pembrolizumab, with 36% of patients maintaining responses beyond 24 months. This shift ensures consistent treatment patterns and strengthens the market's commercial foundation in the United States, Europe, and select Asia-Pacific regions.

ctDNA-Guided Surveillance Expanding the Diagnostic Market

Post-treatment surveillance through ctDNA testing is reshaping the Merkel cell carcinoma market. NCCN updates recommend tri-monthly testing with Signatera, supported by studies showing a hazard ratio of 18.1 for clinical recurrence in persistently ctDNA-positive patients. Additional research confirms ctDNA's ability to detect recurrence earlier, potentially reducing reliance on frequent imaging. NCCN guidelines also emphasize tissue-informed ctDNA testing, integrating biopsy, molecular analysis, and surveillance into a streamlined workflow. This approach drives recurring revenue opportunities, positioning the diagnostic segment for growth.

Chemo-to-Immunotherapy Treatment Shift in Systemic Therapy

The Merkel cell carcinoma market is transitioning from chemotherapy to immunotherapy for advanced cases. A German analysis reported average costs of USD 74,124 over 180 days for immune checkpoint inhibitors, compared to USD 28,236 for chemotherapy. While adoption varies by country due to access and reimbursement challenges, nations like Japan prioritize avelumab as a first-line treatment, reserving chemotherapy for later stages.[2]Journal of the American Academy of Dermatology, “The Epidemiology of Merkel Cell Carcinoma in the United States,” Journal of the American Academy of Dermatology, ovid.com This shift supports higher per-patient value, enabling the market to grow faster than disease incidence.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Tiny incident population and trial recruitment bottlenecks | -1.1% | Global, most acute outside North America and the EU where case volumes are too low for dedicated site infrastructure | Long term (≥ 4 years) |

| High biologic cost and reimbursement scrutiny | -0.8% | EU and the US | Medium term (2-4 years) |

| Post-PD-(L)1 refractory treatment gap with no approved second-line option | -0.6% | Global | Medium term (2-4 years) |

| Immunosuppressed-patient treatment trade-offs limiting eligible population | -0.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tiny Incident Population And Trial Recruitment Bottlenecks

The Merkel cell carcinoma market faces challenges due to a limited patient pool for trials and specialized treatments. A 2025 epidemiology review in the United States reported an average incidence rate of 0.68 per 100,000 person-years since 2013, resulting in consistently low annual case counts. This restricts recruitment, centralizes studies in major cancer centers, and complicates evidence generation compared to common solid tumors.[3]Samuel M. Ehlers and colleagues, “Circulating Tumor DNA Assay Detects Merkel Cell Carcinoma Recurrence, Disease Progression, and Minimal Residual Disease,” Journal of Clinical Oncology via PMC, pmc.ncbi.nlm.nih.gov TuHURA Biosciences’ Phase 3 IFx-2.0 study, targeting 118 patients across 22 to 25 United States sites, highlights the significant infrastructure required for even modest trials. These bottlenecks delay pipeline turnover and concentrate innovation in a few centers, increasing execution risks for smaller companies.

High Biologic Cost And Reimbursement Scrutiny

The Merkel cell carcinoma market is under pressure from high biologic costs and stricter reimbursement reviews. In Q3 2025, Medicare Part B reported pembrolizumab pricing at USD 58.562 per milligram, equating to USD 11,712 for a 200 mg dose, with commercial payer rates exceeding USD 20,000 per infusion in some states.[4]ClinicalTrials.gov, “A Study of Navtemadlin in Advanced Merkel Cell Carcinoma,” ClinicalTrials.gov, clinicaltrials.gov These costs impact prior authorization, step-edit rules, and treatment-site economics, particularly in smaller settings. Hospitals and academic centers, better equipped to manage access logistics, dominate care delivery. Reimbursement scrutiny influences not only pricing but also treatment locations and the adoption rate of new therapies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease Stage: Advanced Staging Anchors Market Revenue and Clinical Trial Investment

Stage III accounted for 44.45% of the Merkel cell carcinoma market size in 2025 and is projected to grow at a 7.28% CAGR through 2031, making it the largest and fastest-growing segment. This stage bridges local disease management and systemic immunotherapy, including patients with clinically positive nodes or nodal disease identified pathologically. NCCN Version 2.2026 recommends sentinel lymph node biopsy for clinically node-negative patients, improving detection and shifting some cases to Stage III. This shift enhances identification at a point where systemic therapy becomes relevant.

Stages I and II constitute the remaining disease-stage split, with revenue focused on surgery, sentinel node biopsy, radiation, and follow-up. These stages could gain value if adjuvant immunotherapy becomes routine. The STAMP pembrolizumab and ADAM avelumab trials, with results expected during the forecast period, may redirect early-stage revenue from radiation-only treatments to checkpoint inhibitors.

By Modality: Treatment Dominates Revenue While Diagnostics Redraw the Care Pathway

Treatment held 68.32% of revenue in 2025, driven by surgery, radiation, and systemic therapies. PD-1 and PD-L1 inhibitors have replaced platinum-based chemotherapy as the primary revenue source in advanced disease, emphasizing durable responses and reimbursement access. Targeted therapy remains niche but is under exploration for specific cases like MCPyV-negative or checkpoint-refractory disease.

Diagnosis is the fastest-growing modality, with a projected 7.96% CAGR through 2031. Growth is fueled by ctDNA testing, increased tissue collection, and sentinel lymph node procedures. Frequent monitoring, such as every three months, ensures consistent revenue generation compared to episodic diagnostic billing.

By End User: Hospital Oncology Departments Lead, Academic Centers Accelerate

Hospital Oncology Departments held 62.34% of the Merkel cell carcinoma market share in 2025, reflecting their ability to integrate dermatology, oncology, pathology, and reimbursement services. Their scale in pharmacy purchasing and administration enhances efficiency in managing costly checkpoint regimens, solidifying their market leadership.

Academic Cancer Centers are projected to grow at an 8.35% CAGR through 2031, driven by their role as trial hubs and early adopters of biomarker-led care. Institutions like Dana-Farber play a key role in advancing new treatment combinations, with programs like STAMP and ADAM relying on academic infrastructure for evidence generation.

Geography Analysis

North America dominates the Merkel cell carcinoma market, driven by high treatment adoption, advanced specialist infrastructure, and widespread guideline-based care. The United States leads this region with greater case visibility, extensive immunotherapy use, and a well-established referral system for rare skin cancers. NCCN guidance has standardized checkpoint inhibitor use for unresectable or metastatic diseases, while the 2025 update emphasized quarterly ctDNA surveillance in routine follow-ups. This combination of treatment access and monitoring depth secures North America's leading position in the market.

Europe ranks as the second-largest region in the Merkel cell carcinoma market, with Germany, the United Kingdom, and France as key revenue contributors. The region benefits from established checkpoint inhibitor use and multidisciplinary care pathways in specialized oncology and dermatology centers. Real-world registry data from German dermatologic oncology centers has strengthened clinical evidence in this rare-disease segment. However, intense reimbursement reviews in some markets may limit uptake outside major centers and affect biologics' pricing power.

Asia-Pacific is the fastest-growing region in the Merkel cell carcinoma market, with Japan, China, and Australia driving growth through diverse demand patterns. Japan prioritizes checkpoint inhibitors in care pathways, with chemotherapy as a secondary option. Regulatory familiarity with retifanlimab in Japan during 2025 highlights the potential for faster adoption of rare-cancer immunotherapies. Aging populations and expanding oncology infrastructure in urban centers further support the region's rapid growth trajectory, despite its smaller current market base compared to North America and Europe.

Competitive Landscape

The Merkel cell carcinoma market demonstrates moderate concentration in approved systemic therapies, with pembrolizumab, avelumab, and retifanlimab dominating the first-line advanced setting across major markets. This creates a stable product structure, though competition persists as companies differentiate through access, dosing strategies, and combination potential. Incyte continues to position retifanlimab within its oncology portfolio, while NCCN guidelines recognize multiple PD-1 and PD-L1 options in the first-line setting.

The clinical pipeline introduces heightened competition and uncertainty in the Merkel cell carcinoma market. TuHURA Biosciences advanced IFx-2.0 into a Phase 3 study under an FDA Special Protocol Assessment, targeting 118 patients and pairing it with pembrolizumab for first-line advanced or metastatic disease. Replimune remains relevant with RP1, which showed activity in the MCC setting, despite receiving a complete response letter in April 2026 for its melanoma biologics license application.

Commercial strategies are expanding beyond drug development. Natera leverages guideline-linked ctDNA adoption to strengthen its role in patient monitoring, enhancing care pathway relevance. MacroGenics and Sagard Healthcare Partners expanded a royalty purchase agreement tied to ZYNYZ in May 2026, showcasing financial strategies to support rare oncology commercialization.

Merkel Cell Carcinoma Industry Leaders

Merck & Co.

Pfizer Inc.

Bristol-Myers Squibb Company

AstraZeneca PLC

TuHURA Biosciences, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Merck presented over 100 abstracts across more than 25 cancer types at the 2026 ASCO Annual Meeting, emphasizing the long-term significance of KEYTRUDA and its oncology pipeline.

- May 2026: Phio Pharmaceuticals' CEO, Robert Bitterman, participated in a fireside chat with Force Family Office CEO Steven Saltzstein and dermatologist Dr. Mary Spellman to discuss advancements in skin cancer prevention and treatment.

- April 2026: Replimune Group received a complete response letter from the FDA for its RP1 biologics license application with nivolumab for advanced melanoma, potentially delaying its MCC program progress after Phase 2 data was shared at ESMO 2025.

- October 2025: TuHURA Biosciences initiated Phase 3 clinical site activation for NCT06947928, enrolling 118 patients across 22 to 25 U.S. sites to compare IFx-2.0 with pembrolizumab against pembrolizumab with a placebo in advanced MCC cases.

Global Merkel Cell Carcinoma Market Report Scope

As per the scope of the report, Merkel cell carcinoma (MCC) is a rare, highly aggressive type of skin cancer that develops in the top layer of the skin, known as the epidermis. Also referred to as neuroendocrine carcinoma of the skin, it is characterized by its tendency to grow rapidly and spread quickly (metastasize) to nearby lymph nodes and other organs.

The Merkel Cell Carcinoma Market is segmented by disease stage, modality, end-user, and geography. By disease stage, the market includes Stage I, Stage II, and Stage III. By modality, the market is segmented into diagnosis (biopsy, imaging, and others) and treatment (surgery, radiation therapy, chemotherapy, targeted therapy, and others). By end-user, the market is categorized into academic cancer centers, hospital oncology departments, office-based oncology and infusion centers, and reference laboratories and molecular diagnostics labs. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Stage I |

| Stage II |

| Stage III |

| Diagnosis | Biopsy |

| Imaging | |

| Others | |

| Treatment | Surgery |

| Radiation Therapy | |

| Chemotherapy | |

| Targeted Therapy | |

| Others |

| Academic Cancer Centers |

| Hospital Oncology Departments |

| Office-Based Oncology and Infusion Centers |

| Reference Laboratories and Molecular Diagnostics Labs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Disease Stage | Stage I | |

| Stage II | ||

| Stage III | ||

| By Modality | Diagnosis | Biopsy |

| Imaging | ||

| Others | ||

| Treatment | Surgery | |

| Radiation Therapy | ||

| Chemotherapy | ||

| Targeted Therapy | ||

| Others | ||

| By End User | Academic Cancer Centers | |

| Hospital Oncology Departments | ||

| Office-Based Oncology and Infusion Centers | ||

| Reference Laboratories and Molecular Diagnostics Labs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the Merkel cell carcinoma market?

The Merkel cell carcinoma market stands at USD 3.47 billion in 2026 and is projected to reach USD 4.70 billion by 2031 at a 6.27% CAGR.

Which treatment approach is driving revenue in Merkel cell carcinoma care?

Systemic treatment is the main revenue driver, with the treatment segment accounting for 68.32% of revenue in 2025, supported by PD-1 and PD-L1 inhibitor use.

Why is Stage III the most important disease stage commercially?

Stage III held 44.45% of revenue in 2025 and is projected to grow at 7.28% CAGR through 2031 because it sits at the point where systemic immunotherapy becomes central.

Why are diagnostics growing faster than treatment in this space?

The diagnosis segment is forecast to grow at 7.96% CAGR through 2031 because ctDNA surveillance, tissue collection, and repeat monitoring are becoming more routine in follow-up care.

Which care settings are gaining the most momentum?

Hospital Oncology Departments led with 62.34% of revenue in 2025, while Academic Cancer Centers are projected to grow fastest at 8.35% CAGR due to their clinical trial role and earlier biomarker adoption.

Which region offers the strongest growth opportunity?

Asia-Pacific is the fastest-growing region, while North America remains the largest current contributor because of deeper immunotherapy penetration, stronger specialist infrastructure, and wider use of guideline-based care.

Page last updated on: