Liver Cancer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

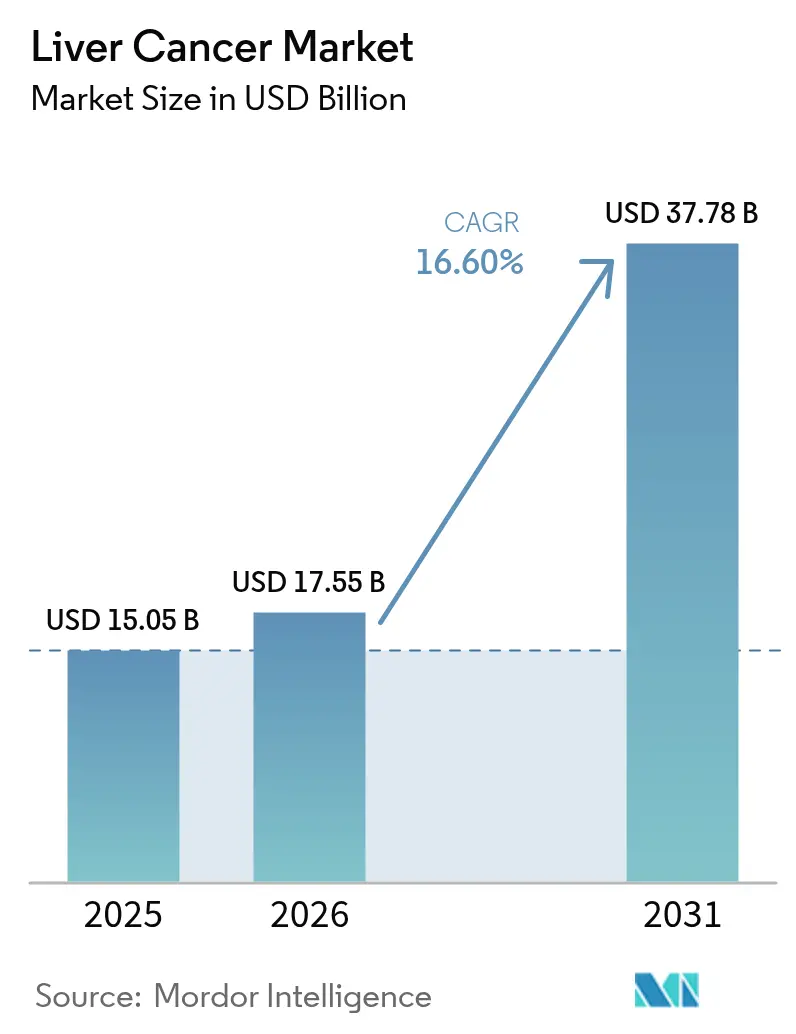

| Market Size (2026) | USD 17.55 Billion |

| Market Size (2031) | USD 37.78 Billion |

| Growth Rate (2026 - 2031) | 16.60% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Liver Cancer Market Analysis by Mordor Intelligence

The liver cancer market size was valued at USD 15.05 billion in 2025 and estimated to grow from USD 17.55 billion in 2026 to reach USD 37.78 billion by 2031, at a CAGR of 16.60% during the forecast period (2026-2031). Strong momentum is arising from dual-checkpoint immunotherapy approvals, the rapid uptake of targeted agents, and broader reimbursement for combination regimens that unite systemic and locoregional modalities. Expanded screening programs, AI-enabled diagnostics, and radiopharmaceutical innovations continue to expand the treatable patient pool, while digital pharmacies are reshaping drug access. Competitive intensity heightens as large pharmaceutical companies acquire radiopharma specialists and partner with manufacturing technology firms to shorten production cycles. The Asia-Pacific’s high hepatitis B prevalence and widening healthcare coverage position the region as the leading growth contributor, whereas North America retains scale advantages through its established clinical trial infrastructure and first-in-class launches.

Key Report Takeaways

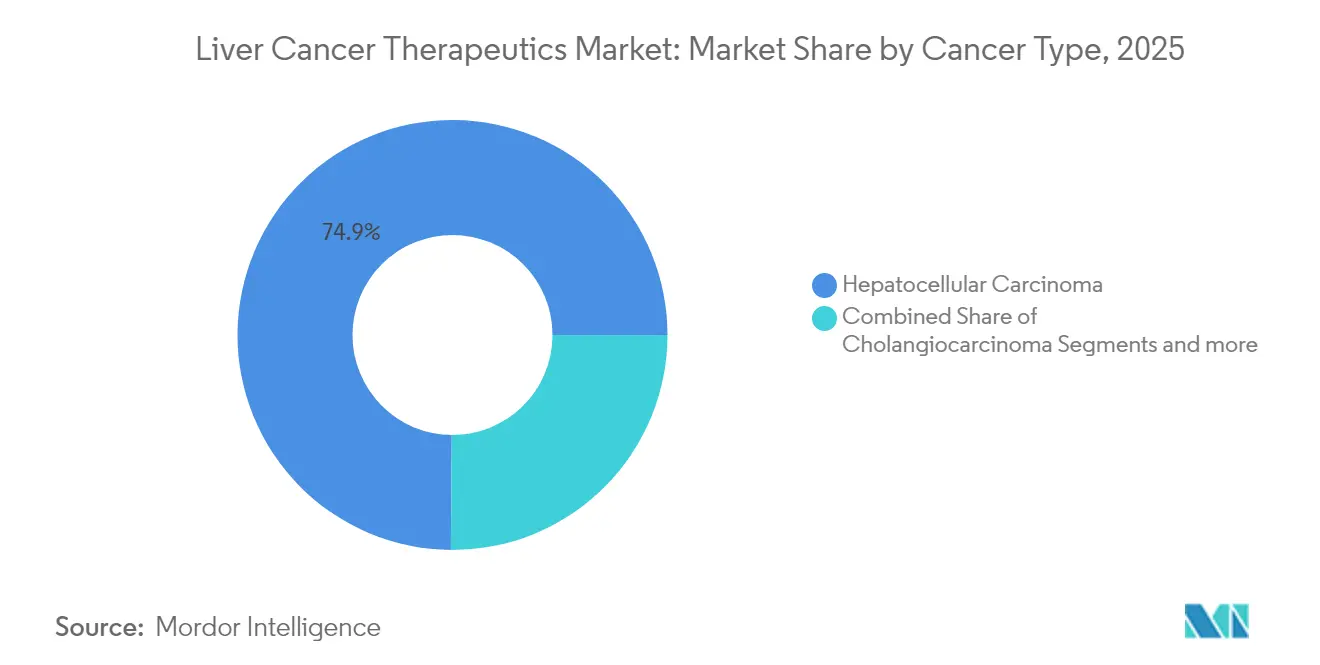

- By cancer type, hepatocellular carcinoma held 74.88% of the liver cancer market share in 2025, while hepatoblastoma is projected to expand at a 19.18% CAGR to 2031.

- By 2025, chemotherapy commanded a 30.72% share of the liver cancer market size; meanwhile, targeted therapy is projected to advance at a 19.25% CAGR through 2031.

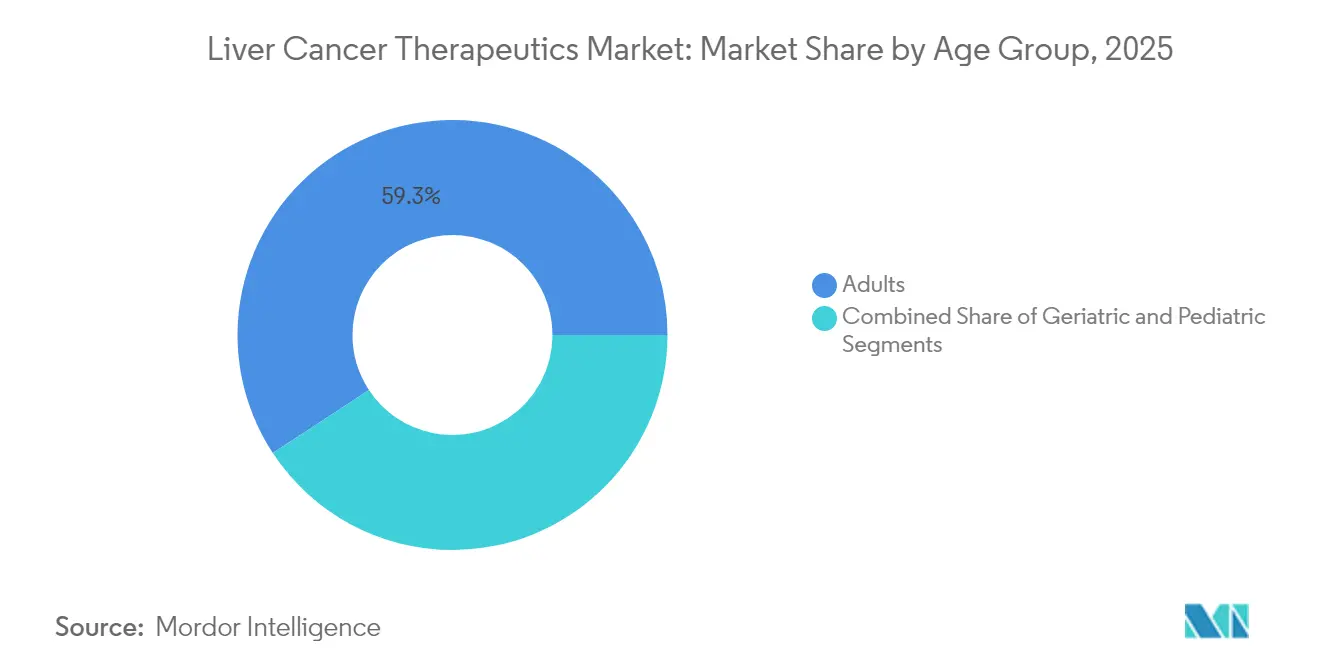

- By age group, adults accounted for 59.25% of the liver cancer market size in 2025, whereas the geriatric segment is projected to grow at a 18.83% CAGR between 2026 and 2031.

- By distribution channel, hospital pharmacies led with a 61.54% revenue share in 2025; online pharmacies are expected to grow at a 19.05% CAGR through 2031.

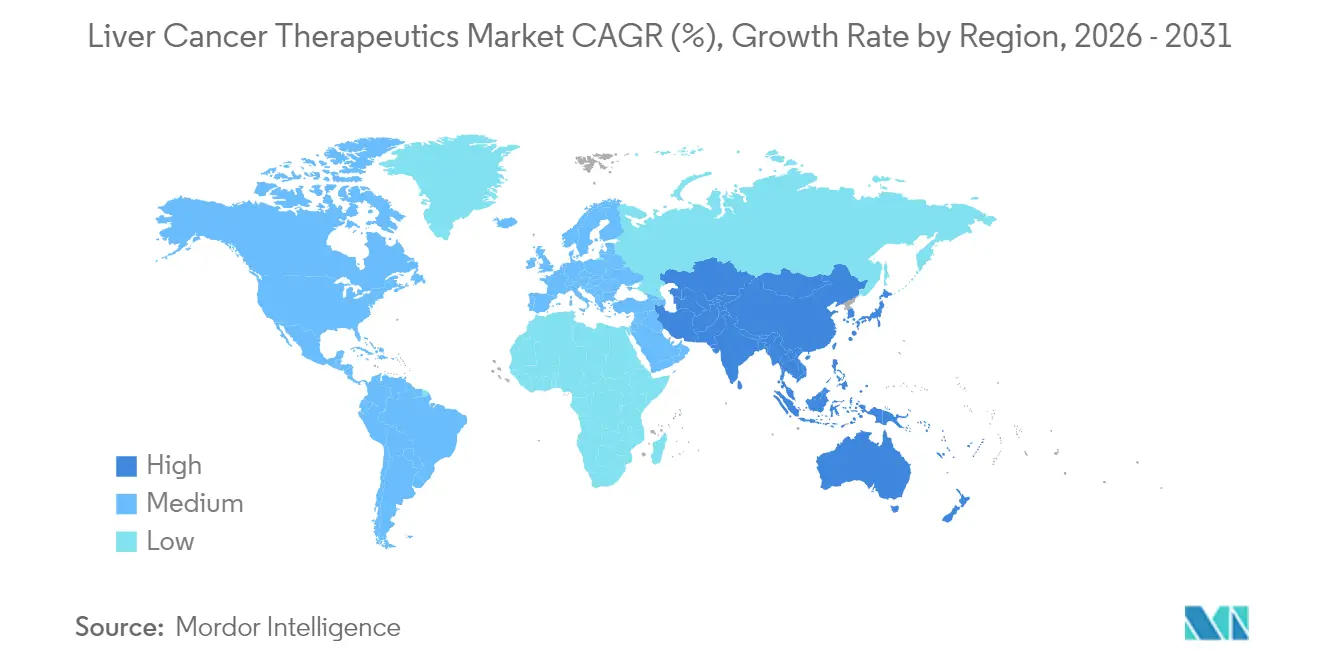

- By geography, North America captured 39.68% of the liver cancer market share in 2025, while the Asia-Pacific region recorded the fastest regional CAGR at 19.02% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Liver Cancer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in incidence of hepatocellular carcinoma | +4.2% | Asia-Pacific, Sub-Saharan Africa | Long term (≥ 4 years) |

| First-line approvals of dual checkpoint combos | +3.8% | North America, EU, spill-over to APAC | Medium term (2-4 years) |

| NAFLD/NASH conversion in obese cohorts | +3.1% | North America, EU, Middle East | Long term (≥ 4 years) |

| Reimbursement for TACE-IO protocols | +2.9% | US, Germany, Japan | Medium term (2-4 years) |

| AI-enabled ultrasound & liquid-biopsy uptake | +2.4% | North America, EU, pilots in APAC | Short term (≤ 2 years) |

| VC-backed radiopharma pipelines | +2.2% | US, Europe manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Incidence of Hepatocellular Carcinoma (HCC)

Global hepatocellular carcinoma cases are projected to increase by 53.8%, from 905,347 in 2020 to 1,392,474 by 2040, underscoring the long-term demand for treatment solutions [1]Qianqian Guo, "Projected epidemiological trends and burden of liver cancer by 2040 based on GBD, CI5plus, and WHO data," Scientific Reports, nature.com. Asia-Pacific shoulders roughly three-quarters of chronic hepatitis B infections, while Mongolia registers the world’s highest age-standardized incidence. Rising metabolic dysfunction-associated steatotic liver disease (MASLD) in high-income economies adds a second growth pillar as obesity-linked HCC cases escalate, especially among younger cohorts in Northern Europe and parts of Asia. These epidemiologic shifts ensure durable expansion of the liver cancer market, reinforced by ageing populations and extended life expectancy in China, Japan, and Western Europe

Expanding First-Line Approvals of Drug Combos

The April 2025 FDA approval of nivolumab plus ipilimumab reset global first-line standards, yielding a 23.7-month median overall survival versus 20.6 months for sorafenib or lenvatinib monotherapy. Europe ratified the regimen two months later, triggering rapid guideline updates across national health systems. Positive EMERALD-1 and LEAP-012 readouts further validated integrating checkpoint inhibitors with anti-VEGF or locoregional treatments, lifting adoption curves and accelerating payer assessments. As reimbursement frameworks adapt, premium-priced combinations enlarge revenue pools and intensify R&D competition.

Rapid NAFLD and NASH Conversion into HCC in Obese Cohorts

NAFLD now affects nearly 30% of adults globally. FDA’s March 2024 clearance of resmetirom, the first NASH therapy, confirms commercial viability for agents that intercept fibrosis and HCC progression. Patients with NASH face a higher liver cancer risk, and diabetes compounds malignant transformation rates. Digital therapeutics such as the NASH App report high disease-activity improvement, suggesting telehealth can complement pharmacologic care.

Wider Reimbursement for Loco-Regional TACE-IO Protocols

Medicare, Japan’s SHI, and Germany’s statutory funds now reimburse TACE combined with immunotherapy after studies showed high durable remission rates in advanced HCC. China’s 2024 NRDL tender reduced prices of innovative oncology drugs by a large margin, widening access for combination regimens. United States CMS policy in 2025 permits separate payment for costly diagnostic radiopharmaceuticals, incentivizing precision imaging and treatment planning.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Severe immune-related adverse events in cirrhotics | -2.8% | Regions with advanced cirrhosis burden | Short term (≤ 2 years) |

| High attrition in late-phase HCC trials | -2.1% | Global, notable in biotech-led programs | Medium term (2-4 years) |

| Sub-optimal surveillance in low-HDI nations | -1.9% | Sub-Saharan Africa, Southeast Asia, Latin America | Long term (≥ 4 years) |

| Price ceilings in China’s NRDL | -1.6% | China, spill-over to other emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Severe Immune-Related Adverse Events (irAEs) in Cirrhotics

Checkpoint inhibitor hepatotoxicity appears in 12.9% of cirrhotic patients, prompting 18% discontinuation in the nivolumab–ipilimumab arm of CheckMate-9DW. Geriatric cohorts show heightened vulnerability, necessitating biomarkers that predict irAE risk to maintain treatment uptake.

High Attrition in Late-Phase Trials

Tumor heterogeneity, underlying liver dysfunction and stringent endpoints contribute to elevated late-stage failure rates. FDA withdrawals of unverified oncology indications underscore the imperative for confirmatory evidence, pressuring biotech financing cycles and dampening near-term pipeline visibility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cancer Type: Dominance of HCC and Rapid Pediatric Gains

Hepatocellular carcinoma secured a 74.88% market share in the liver cancer market in 2025, validating its role as the primary value driver. This dominance reflects both incidence rates and the weight of R&D capital directed toward checkpoint combinations and anti-angiogenic backbones. The April 2025 dual-checkpoint approval intensified competitive differentiation and expanded frontline choices. Cholangiocarcinoma remains a minor but strategically important niche where fast-track designations for tumor-infiltrating lymphocyte products illustrate regulatory appetite for cell-based innovation.

Hepatoblastoma, though rare, is advancing at a 19.18% CAGR, buoyed by improved imaging and molecular profiling that allow early surgical candidacy and enrollment in pediatric immunotherapy trials. Gene-expression studies are propelling precision dosing, and CAR-T exploration for pediatric solid tumors is introducing potentially curative options. This tail-segment acceleration diversifies revenue sources and spurs partnerships with academic centers specializing in pediatric oncology.

By Therapy: Targeted Agents Redefine Clinical Algorithms

Chemotherapy retained 30.72% of the liver cancer market share in 2025, due to its widespread availability and low acquisition cost, especially in resource-constrained regions. Yet, targeted therapy is growing at a 19.25% CAGR as oncologists prioritize precision over cytotoxicity. Atezolizumab–bevacizumab and durvalumab-bevacizumab combinations demonstrate sustained progression-free benefits, supporting expanded indications in guidelines. Radiopharmaceuticals, including actinium-225 constructs from RayzeBio, broaden the targeted spectrum with highly localized alpha-particle lethality.

Immunotherapy’s rise drives the shift toward multimodal regimens that integrate stereotactic radiation and transarterial procedures, enabling deeper responses while sparing healthy parenchyma. Chemotherapy now primarily features in combination schedules or as bridging therapy awaiting the initiation of immuno-targeted therapy.

By Age Group: Geriatric Needs Shape Protocols

Adults accounted for 59.25% of the liver cancer market size in 2025, reflecting their demographic dominance and established screening programs. The geriatric segment, however, grows at 18.83% CAGR owing to rising life expectancy and MASLD prevalence. Clinical data reveal that lenvatinib paired with a hepatic-artery infusion regimen (RALOX-HAIC) extends survival in patients older than 70 years without escalating toxicity.

Geriatric protocols emphasize the management of low-grade immune-related adverse events (irAEs) and telehealth monitoring. Remote platforms reduce hospital visits, which is particularly important for mobility-limited seniors. Pediatric care advances in tandem with the development of tumor-specific antigen targeting and the establishment of institutional networks that facilitate multicenter trials.

By Distribution Channel: Digital Dispensing Accelerates

Hospital pharmacies addressed 61.54% of prescriptions in 2025, maintaining dominance through embedded oncology practices and immediate administration capabilities. Yet online pharmacies are expanding swiftly at a 19.05% CAGR as telemedicine mainstreams follow-up care. Partnerships such as Onco360’s exclusive dispensing of new targeted agents highlight the strategic role of specialty e-pharmacies.

Telepharmacy regulations enacted during the pandemic remain in place, supporting cross-state prescription fulfillment in the United States. AI chatbots handle adherence queries and adverse-event triage, improving outcomes and reducing pharmacist workload.

Geography Analysis

North America commanded 39.68% of global revenue in 2025, buoyed by early checkpoint inhibitor uptake, generous insurance coverage, and leading clinical-trial density. FDA’s Project Orbis fosters simultaneous multinational review, accelerating first-in-class access for United States patients and partners in Canada and Australia. Inflation Reduction Act price-negotiation provisions, however, may curb list-price growth, encouraging companies to optimize launch sequencing.

Asia-Pacific is projected to post a 19.02% CAGR through 2031, the fastest worldwide. China, holding more than 50% of incident cases, blends steep NRDL price reductions with rising urban insurance penetration, which expands volume to offset constrained margins. Japan and South Korea supply robust investigator networks, with roughly half of global HCC trials enrolling at Asia-Pacific sites, reducing development timelines.

Europe maintains consistent uptake supported by centralized health-technology assessments and pathway harmonization. EMA’s endorsement of dual-checkpoint regimens streamlines regional reimbursement. Latin America and the Middle East deliver emerging upside as public–private partnerships expand radiotherapy capacity and viral-hepatitis elimination drives surveillance.

Mordor Intelligence provides coverage of the liver cancer market across other key regional markets, including Asia, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The liver cancer market hosts a balanced mix of multinational incumbents and agile biotechs. Bristol Myers Squibb’s USD 4.1 billion acquisition of RayzeBio anchors its move into actinium-225 radioligand therapy targeting solid tumors, including HCC. Roche and AstraZeneca reinforce leadership through broad immunotherapy portfolios, while Amgen and Tempest Therapeutics pursue bispecific T-cell engagers and small-molecule immune modulators.

AI-powered drug discovery partnerships proliferate; Cellares’ integrated manufacturing platform, joined by Bristol Myers Squibb, aims to industrialize cell therapy production and cut batch variability. Chinese innovators accelerate global competition with checkpoint combinations tailored to HBV-related HCC, gaining rapid NRDL listing after positive pivotal data.

Patent cliffs emerge for first-generation TKIs, stimulating biosimilar entries that could lower barriers in cash-pay markets. White-space opportunities persist in pediatric and ultra-rare hepatic tumors, where fast-track pathways and orphan pricing bolster return prospects.

Liver Cancer Industry Leaders

-

Bristol‑Myers Squibb Company

-

Eisai Co., Ltd.

-

Exelixis Inc

-

Merck & Co. Inc.

-

Bayer AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: FDA approved nivolumab plus ipilimumab for unresectable or metastatic HCC in adults.

- March 2025: European Commission granted centralized authorization for nivolumab–ipilimumab in first-line unresectable HCC, based on CheckMate-9DW data.

- February 2025: Tempest Therapeutics received FDA fast-track designation for amezalpat combination therapy in hepatocellular carcinoma.

- September 2024: Eisai and Merck announced LEAP-012 results showing lenvatinib plus pembrolizumab with TACE improved progression-free survival to 14.6 months versus 10.0 months for TACE alone.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global liver cancer therapeutics market as prescription pharmaceutical agents, small-molecule, biologic, and radiopharmaceutical, used to treat primary hepatic malignancies (chiefly hepatocellular carcinoma and cholangiocarcinoma) as well as approved systemic options for unresectable or metastatic cases.

Scope exclusion: diagnostic imaging, screening, surgical resection devices, and loco-regional embolization tools are not sized in this model.

Segmentation Overview

-

By Cancer Type

- Hepatocellular Carcinoma

- Cholangiocarcinoma

- Hepatoblastoma

- Other Primary Liver Cancers

-

By Product Type

-

Therapy

- Targeted Therapy

- Immunotherapy

- Chemotherapy

- Radiation Therapy

-

Diagnostic

- Ultrasound Scans

- Confirmatory Needle Biopsy

- Endoscopic Ultrasound

- CT Scan

- PET Scan

- Other Diagnostic Types

-

Therapy

-

By Age Group

- Adults

- Geriatric

- Pediatric

-

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with practicing oncologists, hospital pharmacists, payor advisors, and procurement leads across North America, Europe, and key Asia-Pacific markets. These discussions validated regimen mix, real-world dose intensity, typical discount structures, and adoption lags for newly approved therapies, thereby closing data gaps spotted during desk work.

Desk Research

We began with epidemiological baselines from sources such as GLOBOCAN, the WHO Cancer Observatory, and national cancer registries; these outline incident and prevalent patient pools by country. Market access data from FDA, EMA, and NMPA approval portals, tariff filings in UN Comtrade, and reimbursement schedules published by CMS and Japan's MHLW helped us map launch timing and price corridors. Financial disclosures, investor decks, and pipeline updates were scanned through D&B Hoovers and Dow Jones Factiva to gauge commercial uptake and competitive intensity. This list is illustrative, not exhaustive.

A second pass mined clinical-trial libraries, peer-reviewed journals, and trade association notes (e.g., ASCO abstracts) to benchmark emerging checkpoint inhibitor combinations and their expected penetration.

Market-Sizing & Forecasting

We start with a top-down prevalence-to-treated-patient build, adjusting for diagnosis rates, treatment eligibility, line-of-therapy drop-offs, and regional reimbursement caps. Outputs are cross-checked against a bottom-up roll-up of sampled average selling price multiplied by treated volumes reported by leading suppliers and channel audits. Key variables fed into the model include HCC incidence growth, checkpoint inhibitor uptake curves, median therapy duration, weighted ASP erosion, health-insurance coverage expansion, and regional currency movements. Multivariate regression with scenario overlays, augmented by expert consensus, projects values through 2030 while flagging sensitivities. Gap pockets in bottom-up data are bridged using triangulated hospital formulary pulls and tender award values.

Data Validation & Update Cycle

Our team reruns anomaly and variance checks, peers review assumptions, and senior analysts sign off before publication.

Reports are refreshed each year, with interim revisions triggered by material events such as label expansions or major price shifts.

Why Our Liver Cancer Therapeutics Baseline Commands Reliability

Published figures often diverge because firms pick different drug baskets, patient-flow assumptions, and currency years. According to Mordor Intelligence, our disciplined scope and annual refresh help decision-makers rely on one clear baseline.

Key gap drivers versus other publishers revolve around whether loco-regional therapies are counted, the breadth of countries covered, and how off-invoice rebates are factored into ASPs.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.35 B (2025) | Mordor Intelligence | - |

| USD 3.67 B (2024) | Global Consultancy A | Excludes immunotherapy add-on regimens; uses five-country scope |

| USD 3.78 B (2024) | Data Provider B | Uses list prices without rebate normalization |

| USD 2.34 B (2024) | Industry Journal C | Counts only approved TKIs, omits pipeline entrants already commercial in Japan |

In short, our balanced top-down patient approach, corroborated by bottom-up supplier checks and continuous validation, underpins a transparent, reproducible baseline that clients can confidently build plans upon.

Key Questions Answered in the Report

What is the current size of the liver cancer market?

The market is valued at USD 17.55 billion in 2026 and is projected to reach USD 37.78 billion by 2031.

How fast is the liver cancer market growing?

It is expanding at an 16.60% CAGR, positioning it among the fastest-growing oncology categories.

Which therapy class is showing the highest growth?

Targeted therapy is the fastest-growing class, advancing at a 19.25% CAGR through 2031.

Which region offers the greatest growth potential?

Asia-Pacific posts the highest regional CAGR at 19.02%, driven by large hepatitis B populations and improving health-care access.

What recent regulatory milestone changed first-line treatment standards?

The FDA’s April 2025 approval of nivolumab plus ipilimumab established a dual-checkpoint immunotherapy option for treatment-naïve advanced HCC patients.

How are distribution channels evolving for liver cancer drugs?

Online pharmacies are growing at a 19.05% CAGR, supported by telemedicine, while hospital pharmacies remain the largest sales channel.

Page last updated on: