Maldives Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

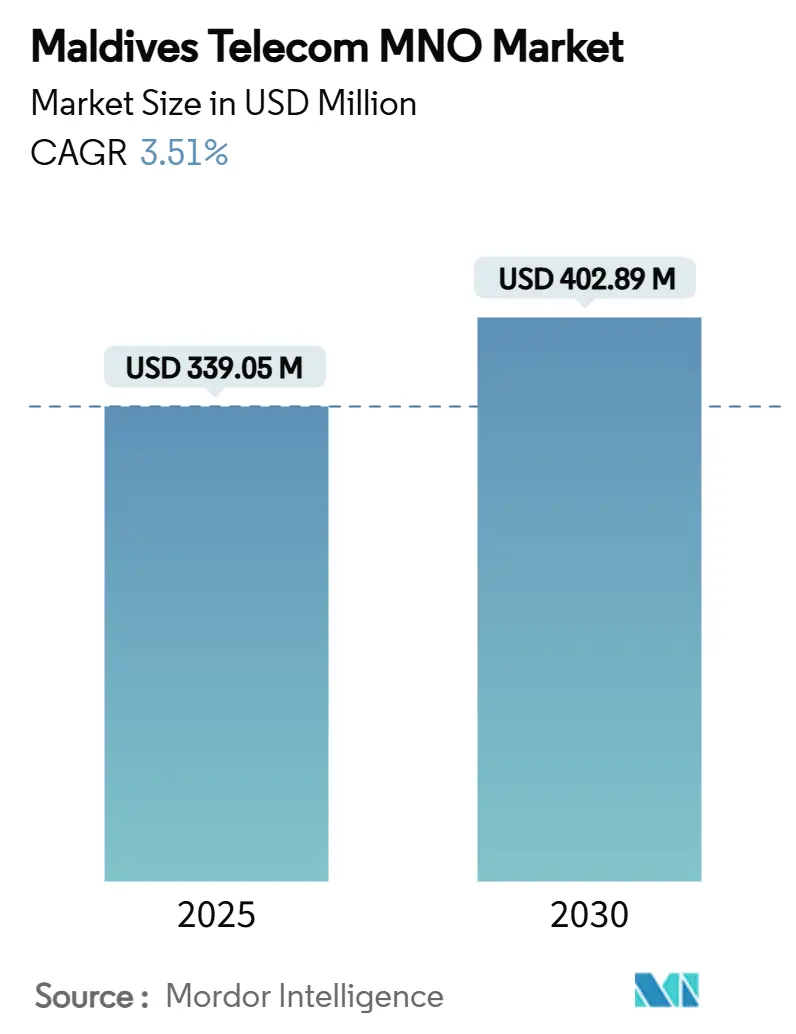

| Market Size (2025) | USD 339.05 Million |

| Market Size (2030) | USD 402.89 Million |

| Growth Rate (2025 - 2030) | 3.51% CAGR |

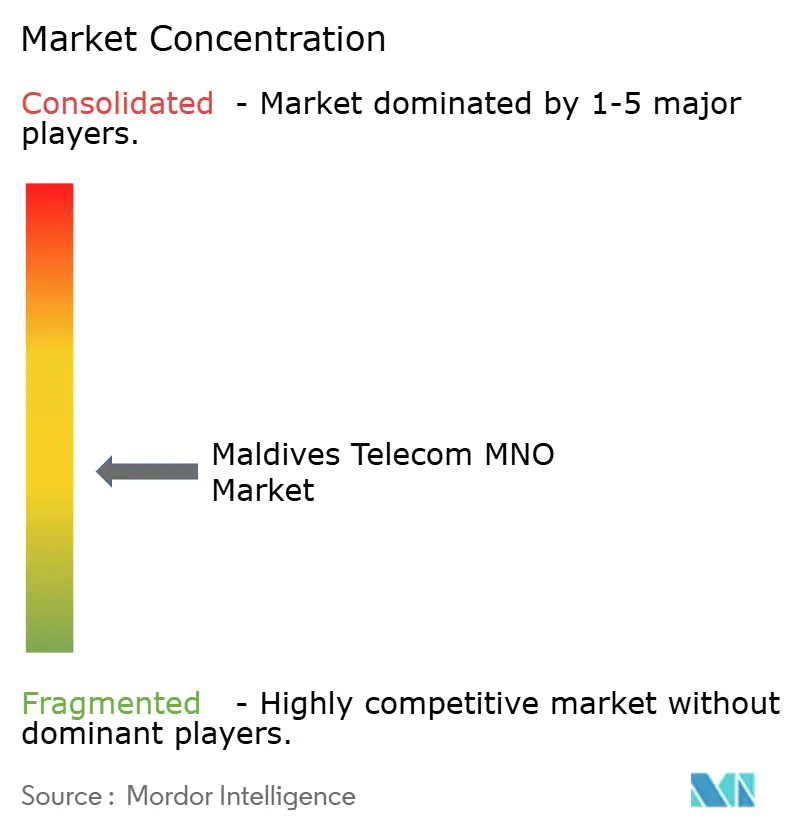

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Maldives Telecom MNO Market Analysis by Mordor Intelligence

The Maldives Telecom MNO Market size is estimated at USD 339.05 million in 2025, and is expected to reach USD 402.89 million by 2030, at a CAGR of 3.51% during the forecast period (2025-2030).

This steady climb is underwritten by tourism-driven data surges, government-backed digitization, and ongoing 5G network investments that together keep average revenue per user resilient despite the archipelago’s small population base. Data services already account for 46.03% of revenue, and SEA-ME-WE 6’s 126 Tbps of new international capacity is expected to further lift network quality and reduce backhaul costs. A tightly regulated duopoly ensures nationwide coverage that now spans 87% of households with fiber, while mobile penetration exceeds 125%, revealing untapped upgrade potential for premium 5G tiers. Operators remain alert to structural risks that stem from high subsea capex and climate-related infrastructure exposure, yet the overriding market opportunity lies in monetizing tourists who top 2 million arrivals annually and routinely demand fast, reliable connectivity.[1]Asian Development Bank, “ADB, Dhiraagu to Expand Internet Access in Maldives Through New Undersea Cable System,” adb.org

Key Report Takeaways

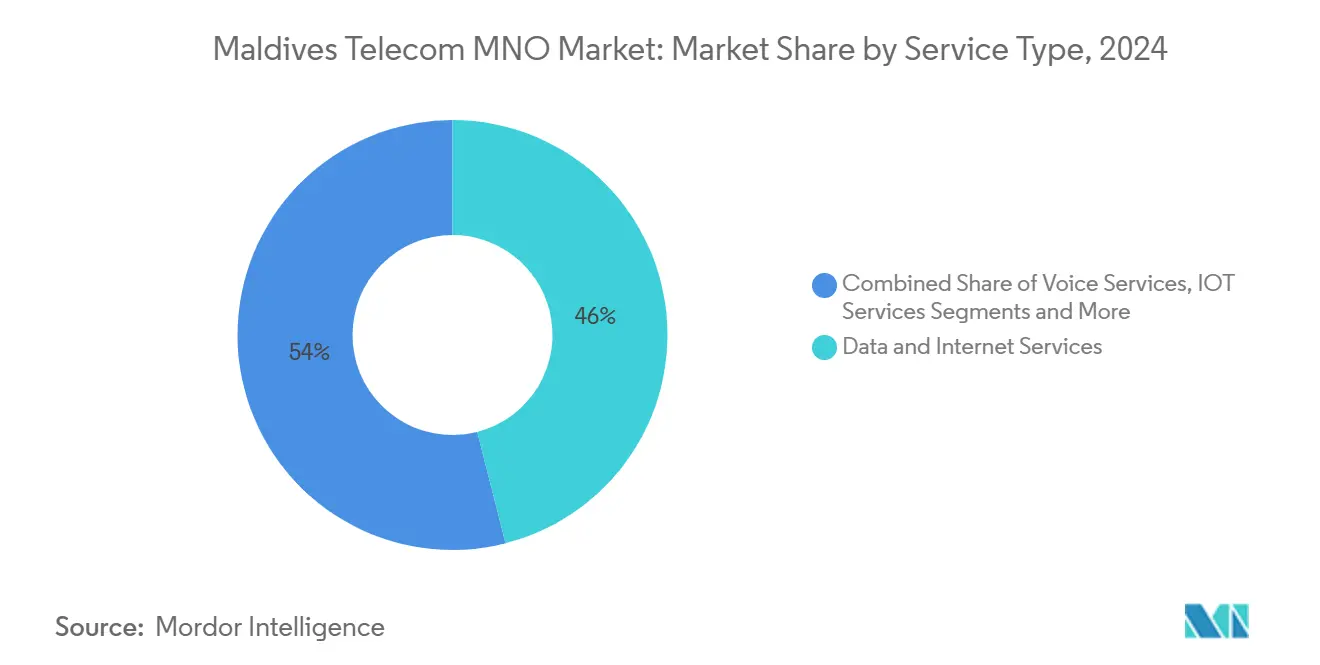

- By service type, data services led with 46.03% of Maldives telecom market share in 2024 and are on track for a 3.57% CAGR through 2030.

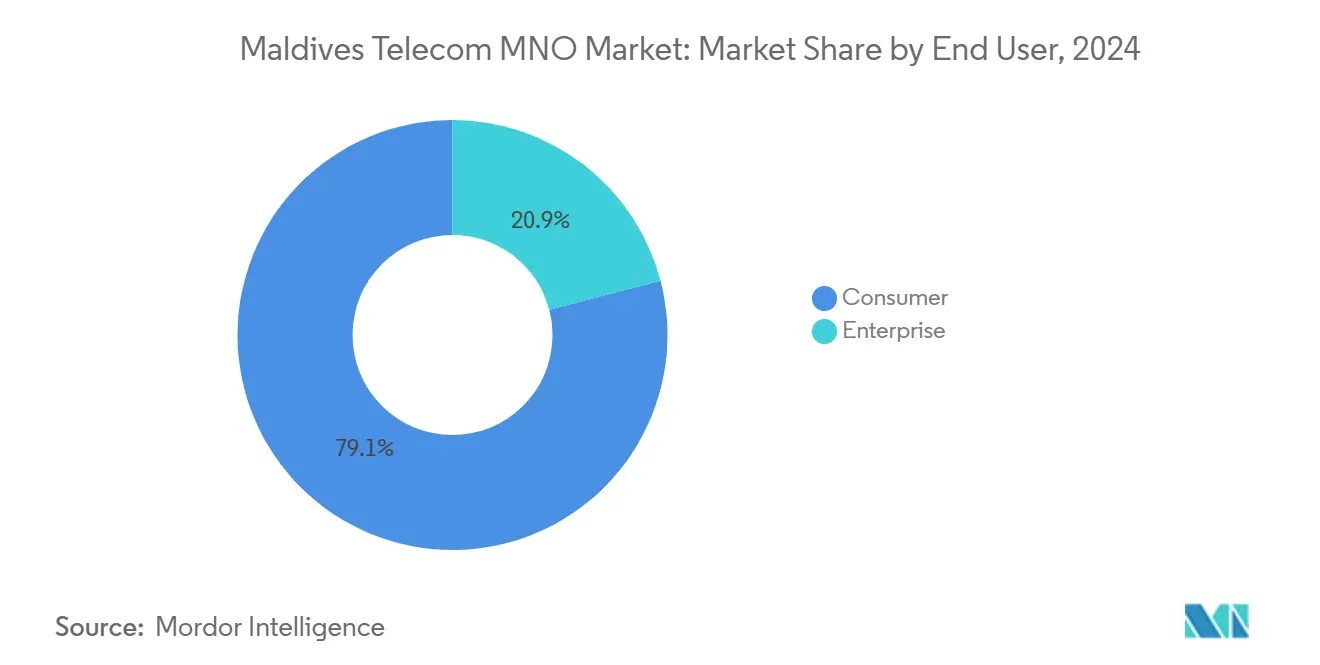

- By end user, consumer services held 79.06% revenue share in 2024; enterprise services are projected to expand at a 4.68% CAGR to 2030.

Maldives Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming tourism-led demand for high-speed mobile data | +0.8% | Resort islands, Male region | Short term (≤ 2 years) |

| Government “Digital Raajje” initiatives & e-Gov uptake | +0.6% | All inhabited atolls | Medium term (2-4 years) |

| Rapid 5G rollout across all inhabited islands | +0.5% | Nationwide | Medium term (2-4 years) |

| ARPU lift from bundled content (OTT & PayTV) | +0.4% | Urban centers | Short term (≤ 2 years) |

| SEA-ME-WE 6 submarine cable landing | +0.3% | Nationwide | Long term (≥ 4 years) |

| Mobile-first fintech and e-money services | +0.2% | Commercial hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Booming Tourism-Led Demand for High-Speed Mobile Data

Tourist arrivals reached 2.05 million in 2024, an 8.9% lift that translated directly into seasonal data peaks up to 60% above baseline traffic. Resort operators now purchase dedicated enterprise circuits to guarantee seamless guest Wi-Fi, while visitors drive prepaid SIM sales that average MVR 100–150 per pack. International eSIM brands such as GigSky add price competition, offering 5G packages that undermine roaming margins yet broaden overall data consumption. Network planners must therefore size capacity for holiday surges, especially in resort-dense atolls where high-revenue tourists congregate.[2]GigSky, “Buy eSIM for Maldives,” gigsky.com The Communications Authority of Maldives enforces quality-of-service rules that protect the country’s hospitality brand, recognizing reliable connectivity as indispensable tourism infrastructure.

Government “Digital Raajje” Initiatives & E-Gov Services Uptake

The Digital Raajje framework pushes every public agency online, eliminating costly inter-island travel for routine paperwork. Fiber-to-the-home now passes 87% of households and underpins digital ID, instant payment, and tax portals that elevate baseline data traffic. DhiraaguPay integrates directly with e-government apps, showcasing how operators monetize public digitization through transaction fees and platform hosting. The Maldives Instant Payment System, built with Finnish vendors, further cements telecom infrastructure at the heart of national modernization.

Rapid 5G Rollout Across All Inhabited Islands

Dhiraagu reached 60% population coverage with 5G by December 2024, extending beyond Greater Male to key resort atolls. Ooredoo prioritizes fixed-wireless 5G to serve homes lacking fiber, packaging allowances up to 525 GB under its Faseyha brand. Although monetization remains modest, 5G enables smart-resort IoT, environmental sensors, and immersive guest services that justify premium pricing. Shared-infrastructure talks are underway to curb capex and accelerate coverage on sparsely populated islands where standalone deployments break scale economics.

ARPU Lift from Bundled Content (OTT & PayTV)

Content tie-ups raise average revenue per user by packaging streaming rights with mobile and broadband plans. Dhiraagu offers Stingray music and Lionsgate Play, while Ooredoo’s Go Play Market—launched with MediaKind and Microsoft—targets both subscribers and over-the-top viewers. Local platform Baiskoafu extends Maldivian cultural content reach, increasing stickiness in a small domestic audience. Bandwidth-intensive video drives demand for higher-tier data plans, though operators must balance license fees against limited per-user spending power. Medianet’s transition to 4K cable TV across 90% of islands underscores continued appetite for premium entertainment even as mobile streaming grows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex for nationwide subsea backhaul | -0.4% | Outer atolls | Long term (≥ 4 years) |

| Limited low-band spectrum constraining rural coverage | -0.3% | Remote islands | Medium term (2-4 years) |

| Small, dispersed population limits economies of scale | -0.2% | Nationwide | Long term (≥ 4 years) |

| Climate-related disruptions to coastal infrastructure | -0.2% | Entire archipelago | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capex for Nationwide Subsea Backhaul

SEA-ME-WE 6 demanded USD 20 million from Dhiraagu alone, a sizable outlay in a USD 321.73 million market.[3]Submarine Networks, “SEA-ME-WE 6,” submarinenetworks.com Every additional inhabited atoll forces kilometer-by-kilometer submarine build-out that yields limited incremental revenue. OMS Group’s USD 300 million regional program highlights the scale needed for economic fiber routes. Operators rely on concessional debt and cross-subsidizing tourist hotspots to fund universal-service mandates. Climate resilience—armoring, deeper burial, hardened landing stations—adds cost layers that extend payback well beyond the industry’s typical five-year horizon.

Limited Low-Band Spectrum Constraining Rural Coverage

Sub-1 GHz spectrum is scarce, compelling reliance on 1800 MHz and 2100 MHz bands that require denser base-station grids. Re-farming proposals face broadcast lobby resistance, mirroring global debates around 700 MHz and 3600 MHz allocation. Remote islands thus experience higher per-subscriber cost, slowing return on 5G rollouts. Until regulators secure wider contiguous blocks, coverage ambitions will trail demand, particularly for emergency and IoT services that depend on lower frequencies for reach.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Drive Market Evolution

Data services controlled 46.03% of Maldives telecom market share in 2024 on the strength of 125% smartphone penetration and 87% fiber reach. The segment is tracking a 3.57% CAGR, paced by tourist demand spikes and the Digital Raajje mandate for online public services. Voice held 36.96%, yet VoLTE migration and messaging apps erode traditional traffic even as legacy circuits persist in remote atolls. IoT captured 5.01% with environmental and smart-resort deployments, while OTT & PayTV climbed fastest at a 3.79% CAGR as operators bundle Disney, Lionsgate Play, and Stingray content. Other value-added offerings rounded out 4.19%, reflecting international bandwidth resale and messaging revenues. Regulatory oversight assures service quality and open number portability, encouraging differentiated data-centric packages that reinforce the Maldives telecom market position.

The interplay of subsea capacity, consumer video appetite, and enterprise digitization keeps data revenue accelerating, while voice ARPU softens. Operators will likely refocus on content-led bundles and IoT verticals to defend profitability as the Maldives telecom market edges toward saturation in core connectivity.

By End User: Enterprise Segment Outpaces Consumer Growth

Consumers generated 79.06% of revenue in 2024, reflecting prepaid tourist SIM uptake and high mobile penetration. Growth in this cohort slows to a 3.19% CAGR as the market matures, shifting operator focus toward ARPU uplift and churn reduction. Enterprises, though smaller at 20.94%, are forecast to grow 4.68% annually on the back of resort digitization, government e-services, and cross-atoll corporate networking. Higher-margin contracts, managed security, and IoT solutions position the enterprise slice as the chief profitability lever for the Maldives telecom market.

Public-sector agencies form a sizable sub-segment, demanding secure inter-island links and uptime guarantees. Operators using network-as-a-service models may capture incremental value in this space, reinforcing enterprise momentum.

Geography Analysis

Nationwide 4G coverage blankets all 187 inhabited islands, yet service experience varies with population density. Greater Male accounts for nearly 40% of total revenue thanks to affluent consumers, administrative offices, and year-round tourist flows. Here, the Maldives telecom market size for 5G alone is projected to cross USD 25 million by 2030, underlining premium-tier appetite.

In central atolls, mixed tourism and fishing economies create moderate demand characterized by prepaid churn and seasonality. Fiber penetration tops 70% in these clusters, enabling OTT uptake that keeps ARPU above the national average. The Maldives telecom market share for Dhiraagu remains higher in this belt given its early fiber lead, while Ooredoo relies on fixed-wireless to close coverage gaps.

Far-flung northern and southern atolls struggle with sparse populations that dilute economies of scale. Operators leverage universal-service funds and concessional loans to finance subsea spurs, yet climate-exposed infrastructure raises opex. Even so, digital ID and instant-payment platforms are lifting baseline data traffic, signaling long-term revenue potential once connectivity costs decline.

Competitive Landscape

Maldives communications remains a duopoly anchored by Dhiraagu and Ooredoo, both vertically integrated across mobile, fixed, and PayTV. Opensignal’s November 2024 report awarded Ooredoo six network-experience prizes—including upload speed and coverage—while Dhiraagu captured five for download speed and gaming quality. These public scorecards feed aggressive marketing and periodic SIM-card price promotions that sustain churn around 2% per quarter despite the MVR 200 porting fee.

Strategic moves center on 5G expansion and content bundling. Dhiraagu completed universal fiber-to-home coverage in August 2024, positioning itself for premium converged packages that integrate Lionsgate Play and Stingray music. Ooredoo counters with Microsoft-backed Go Play Market and wide-area 5G FWA, targeting underserved households and resort operators. Both firms invest in climate-resilient subsea routes, recognizing environmental risk as a shared existential threat.

Supplier partnerships broaden competitive arsenals. Dhiraagu tapped Ericsson for standalone 5G core, while Ooredoo leverages Nokia’s ReefShark radios to optimize power draw in remote sites. Ties with regional cable consortia, IoT platform providers, and fintech ventures illustrate a widening ecosystem approach as the Maldives telecom market transitions from basic connectivity to integrated digital services.

Maldives Telecom MNO Industry Leaders

Dhiraagu (Dhivehi Raajjeygé Gulhun PLC)

Ooredoo Maldives

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: SEA-ME-WE 6 entered service, boosting international capacity to 126 Tbps and lowering wholesale bandwidth costs for both operators. Dhiraagu financed USD 20 million of the landing with Asian Development Bank support.

- November 2024: Opensignal survey saw Ooredoo win six mobile-experience awards and Dhiraagu five, intensifying network-quality messaging in a tight two-player field.

- October 2024: OMS Group signaled USD 300 million in new regional subsea and terrestrial fiber investments, potentially giving Maldivian operators cheaper regional transit paths.

- August 2024: Dhiraagu achieved 100% fiber-to-the-home coverage across inhabited islands, a landmark that elevates broadband performance and cross-sell potential.

Maldives Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise And Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise And Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

How large is the Maldives telecom market in 2025?

The market is valued at USD 321.73 million for 2024 and is tracking a 3.51% CAGR, placing 2025 revenue near USD 333 million.

How extensive is 5G coverage in the Maldives right now?

Dhiraagu’s network covers 60% of the population, while Ooredoo focuses on fixed-wireless 5G for un-fibered homes.

What is the biggest operational challenge for operators?

High subsea backhaul capex across 1,200 islands strains returns and extends payback timelines compared with terrestrial markets.

Who regulates the telecom sector?

The Communications Authority of Maldives oversees licensing, spectrum allocation, and quality-of-service standards.

Page last updated on: