Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.70 Billion |

| Market Size (2026) | USD 2.86 Billion |

| Market Size (2031) | USD 3.8 Billion |

| Growth Rate (2026 - 2031) | 5.88% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oman Telecom MNO Market Analysis by Mordor Intelligence

The Oman Telecom MNO Market size was valued at USD 2.70 billion in 2025 and estimated to grow from USD 2.86 billion in 2026 to reach USD 3.80 billion by 2031, at a CAGR of 5.88% during the forecast period (2026-2031).

This uptrend is propelled by nationwide 5G rollouts, Oman's emergence as a Gulf submarine-cable hub, and Vision 2040’s USD 442 million digital-economy program. Enterprise digitalization, a 134% mobile-penetration rate, and licensing of Starlink for rural back-haul further magnify data traffic. Competition within the three-player oligopoly has sharpened since Vodafone’s 2022 launch, raising network-performance benchmarks and service-bundling innovations. Sustained wholesale revenues from more than 20 submarine cables and four terrestrial links provide an added earnings buffer for operators.

Key Report Takeaways

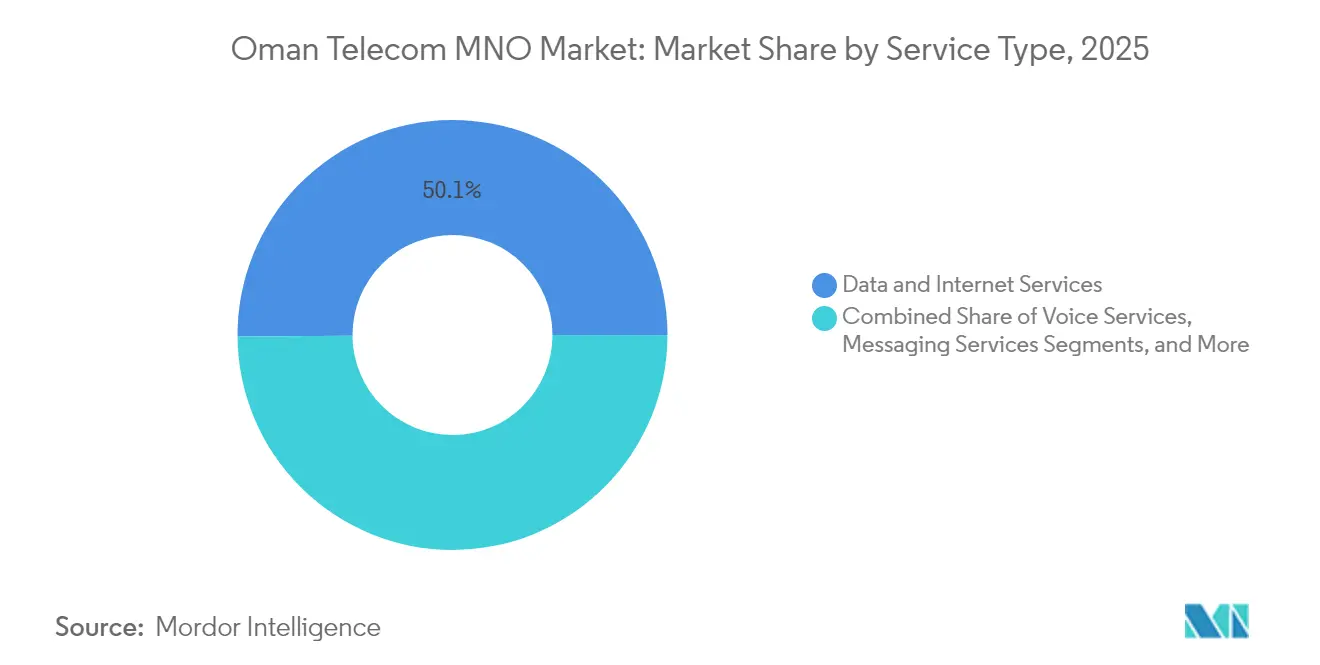

- By service type, data and internet services led with 50.12% of Oman telecom MNO market share in 2025; IoT and M2M services are advancing at a 5.99% CAGR through 2031.

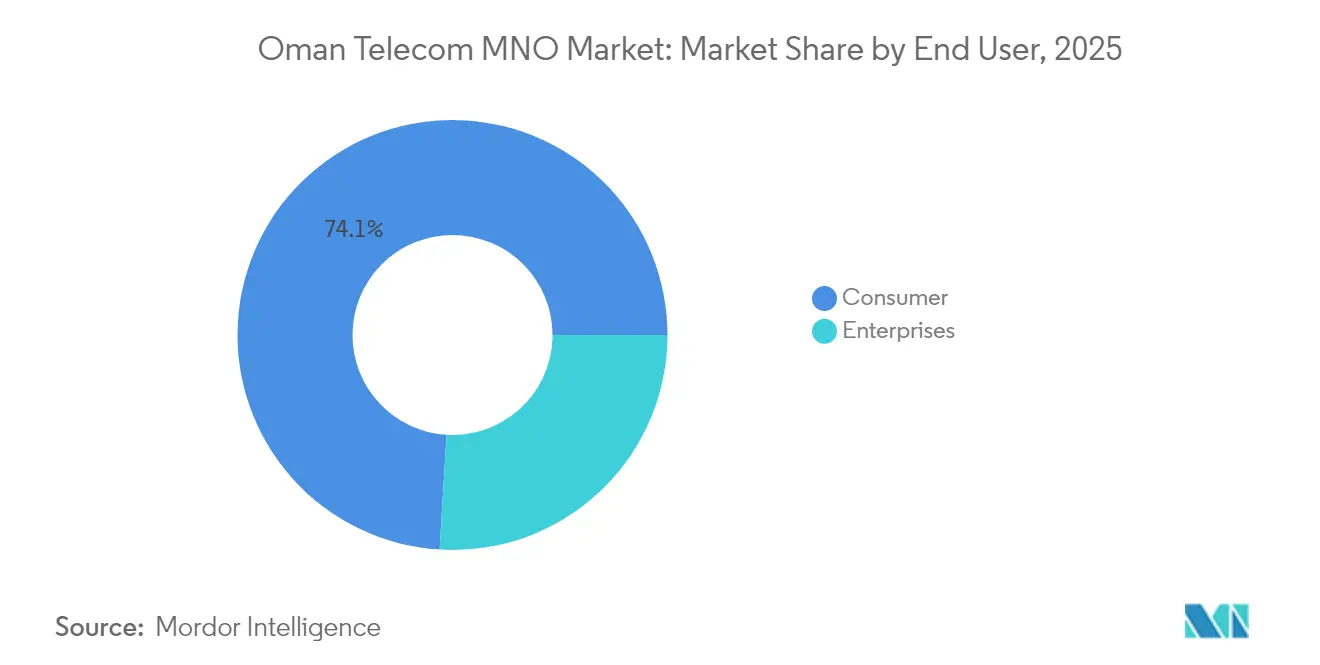

- By end user, the consumer segment held 74.05% of the Oman telecom MNO market size in 2025, while the enterprise segment is forecast to expand at a 6.26% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Oman Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G rollout and surging data traffic | +1.8% | Muscat, Salalah, Sohar | Medium term (2-4 years) |

| Vision 2040 digital-economy investments | +1.2% | SEZs and smart-city zones nationwide | Long term (≥ 4 years) |

| Rising smartphone and internet penetration | +0.9% | Rural uplift through satellite backhaul | Short term (≤ 2 years) |

| Oman as Gulf submarine-cable hub | +0.7% | National with regional spillovers | Long term (≥ 4 years) |

| Starlink license enabling rural backhaul | +0.5% | Mountainous and desert districts | Medium term (2-4 years) |

| Tourism-driven seasonal roaming boost | +0.3% | Muscat, Salalah, Nizwa, coastal resorts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

5G Rollout and Surging Data Traffic

All three operators have launched commercial 5G, lifting down-link speeds to 252.3 Mbps on Omantel’s network and pushing consumers toward higher-value plans. Vodafone’s Ericsson-built greenfield network achieved a 95% Omanization rate, accelerating skills transfer and localized maintenance [1]Ericsson, “Vodafone Oman’s 5G Network Deployment,” ericsson.com. The sunset of 3G networks in 2024 forced subscribers onto 4G and 5G, widening ARPU and opening fixed-wireless-access prospects for logistics hubs in Sohar and Duqm. Enterprise IoT adoption now outpaces consumer uptake, with use cases in smart metering and port automation catalyzing incremental revenue. Data-traffic momentum underpins the projected 1.8-percentage-point uplift in overall CAGR.

Vision 2040 Digital-Economy Investments

The Ministry of Transport, Communications, and Information Technology earmarked USD 442 million for digital transformation, spawning AI pilots and national accessibility standards for apps and websites [2]Ministry of Transport, Communications and Information Technology, “Digital Transformation Programs,” mtcit.gov.om. SEZ developments at Duqm and Sohar require dedicated 5G campus networks, while the government’s goal to elevate logistics to global-top-ten status by 2040 deepens infrastructure demand. The country’s ICT sector is valued at USD 5.47 billion in 2025 and is projected to almost double by 2029, reinforcing the +1.2% CAGR impact.

Rising Smartphone and Internet Penetration

Mobile penetration reached 134% by mid-2024, translating into 5.02 million active internet users and 4.39 million social-media accounts. The e-commerce market is on track to double to USD 1.1 billion by 2028, bolstering demand for mobile payments and digital-banking platforms. Rural coverage is improving through satellite licensing for Starlink and OmanSat, ensuring inclusivity and adding 0.9 percentage points to forecast growth. High smartphone adoption also fuels OTT video, music, and gaming traffic, spurring network-capacity upgrades.

Oman as Gulf Submarine-Cable Hub

Hosting more than 20 subsea systems, including the 2Africa and Al Khaleej cables, Oman enjoys unmatched route diversity and wholesale dominance [3]TelecomTalk, “Ooredoo to Land 2Africa Subsea Cable in Oman,” telecomtalk.info. Omantel maintains 100+ international interconnects, and Equinix’s Salalah data center, launched in November 2024, offers carrier-neutral colocation to hyperscalers. These assets secure stable wholesale margins, lifting the growth forecast by 0.7%. The country’s status attracts regional cloud deployments and deepens roaming-partner ties with 700 networks across 200 countries.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 12% royalty on telecom revenues | -1.4% | Nationwide | Long term (≥ 4 years) |

| Saturated mobile-subscriber base | -0.8% | Urban markets | Medium term (2-4 years) |

| OTT revenue leakage to foreign platforms | -0.6% | Voice and messaging nationwide | Short term (≤ 2 years) |

| Spectrum-refarming delays for 6G | -0.4% | Nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

12% Royalty on Telecom Revenues

A uniform 12% levy on gross telecom income caps reinvestment potential and constrains price flexibility. The burden, higher than neighboring GCC norms, forces cost-rationalization measures such as Omantel’s migration of 200 products to a cloud-native charging platform. Vodafone’s asset-light model and Ooredoo’s operational-efficiency drive partly offset the margin squeeze, yet the royalty still shaves 1.4 percentage points off projected CAGR.

OTT Revenue Leakage to Foreign Platforms

Messaging and voice traffic continues its shift to WhatsApp, Telegram, and similar OTT services, eroding legacy revenue streams. As 5G elevates video-call quality, the cannibalization effect intensifies. Operators respond by bundling content and launching fintech ventures, evidenced by Ooredoo’s B2B marketplace and digital-wallet pilots [4]Telecom Review, “Ooredoo Oman Operational Efficiencies,” telecomreview.com. However, limited regulatory recourse means voice and SMS erosion subtracts 0.6 percentage points from growth forecasts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Dominance Drives IoT Growth

Data and internet services held 50.12% of the Oman telecom MNO market share in 2025, anchoring top-line performance as enterprises shift workloads to cloud platforms. Voice still contributes materially but declines annually, while messaging yields continue to contract under OTT pressure. The Oman telecom MNO market size attributed to IoT and M2M services is projected to grow at a 5.99% CAGR through 2031, propelled by smart-city deployments in Muscat and Duqm and automated-meter-reading rollouts for water utilities. Operators monetize these connections via managed-services contracts and edge-computing bundles.

Fixed-wireless-access offerings deliver fiber-like speeds in challenging terrain, augmenting data revenue and reinforcing the centrality of 5G. OTT and PayTV streams add modest upside as local content partnerships mature, whereas roaming and enterprise-solutions lines benefit from Oman’s status as a logistics and tourism hub. TRA’s certification requirements for IoT reliability support premium pricing and keep churn low, further stabilizing data-service cash flows.

By End User: Enterprise Acceleration Outpaces Consumer Growth

Consumer lines represented 74.05% of the Oman telecom MNO market size in 2025, owing to high device penetration and diversified prepaid and postpaid plans. Yet, enterprise revenues are forecast to expand at a 6.26% CAGR, outpacing mass-market growth as Vision 2040 compels every sector, such as energy, logistics, healthcare, and public administration, to digitize operations. Omantel’s A’amali+ bundles for SMEs and Fiber Pro tiers for corporates illustrate the rising appetite for managed connectivity and cybersecurity packages.

Enterprise ARPU exceeds consumer equivalents by multiples, with contracts often spanning three-year horizons. Private 5G networks for industrial zones and port terminals feature guaranteed latency and slice isolation, commanding premium tariffs. In the consumer arena, unlimited-data plans and content add-ons sustain subscriber loyalty, though margin pressure persists from the royalty regime and OTT substitution. Device-financing offers and embedded-finance features further differentiate operator propositions across both segments.

Geography Analysis

Muscat, housing the largest 5G base-station density and 565 ATMs, remains the prime revenue generator, while Salalah leverages Equinix’s new data center to attract cloud workloads and submarine-cable landings. Sohar and Duqm industrial hubs rely on fixed-wireless-access and fiber back-haul to support petrochemical plants and container terminals. The Oman telecom MNO market size for coastal governorates rises in tandem with port logistics upgrades, while hinterland growth hinges on satellite backhaul.

Terrestrial links connect Oman to every GCC neighbor, reinforcing wholesale income stability and roaming reciprocity with 700 partners worldwide. Fixed-broadband penetration, still 11% in early 2024, offers a runway for fiber builds financed through government-operator co-investment schemes. Tourism centers such as Nizwa and coastal resorts generate seasonal spikes in roaming usage, magnified by 5G’s higher throughput for social-media uploads, video calls, and digital-tourism apps.

Rural districts benefit from March 2025 Starlink licensing and OmanSat’s Category 1 authorization, narrowing the digital divide in mountainous and desert areas. The TRA’s open-access mandates ensure smaller ISPs can lease capacity, stimulating regional service diversity. Transportation megaprojects, including the USD 3 billion railway and 800 miles of new roads, require robust mobile coverage and IoT sensors for smart-infrastructure management. Collectively, these geographic dynamics deepen national connectivity resilience and diversify revenue sources beyond Muscat’s urban core.

Competitive Landscape

Oman’s telecom arena is a concentrated three-player oligopoly: Omantel, Ooredoo, and Vodafone. The top two operators, Omantel and Ooredoo, together held a significant share of subscriptions in 2024, though Vodafone rapidly gained its position in the Oman telecom MNO market within two years through aggressive digital onboarding and loyalty rewards. Competition pivots on 5G speed, coverage, and differentiated enterprise offerings. Omantel leads coverage and wholesale capacity owing to its extensive submarine-cable stakes, while Vodafone tops consistency scores at 74.4% and positions itself as a fully digital-service brand.

Ooredoo pursues vertical diversification, partnering with Shell Oman to deploy IoT solutions for the energy sector and with Oman Data Park for cloud-hosting bundles. Omantel’s equity investment in Byanat enhances data analytics capabilities that feed into AI-driven customer experience platforms. Vodafone’s asset-light strategy includes extensive tower-sharing agreements, compressing capex and expediting rollout timelines.

Regulatory levers such as spectrum allocations, infrastructure-sharing mandates, and quality-of-service audits maintain competitive equilibrium. The 12% royalty regime, shared by all, limits undercutting on tariffs and channels rivalry toward service innovation and customer-experience differentiation. Future battlegrounds include satellite-terrestrial integration, fintech ecosystems, and managed security services tailored to Vision 2040’s cybersecurity framework.

Oman Telecom MNO Industry Leaders

Oman Telecommunications Company (Omantel)

Omani Qatari Telecommunications Company (Ooredoo)

Vodafone Oman

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: The Ministry of Transport, Communications and Information Technology launched the Digital Accessibility Guide to enhance digital inclusion across public and private sectors, mandating accessibility standards for mobile applications and websites serving people with disabilities and elderly users.

- March 2025: TRA granted Starlink Muscat approval to provide satellite internet services in Oman, introducing new competitive dynamics in rural and remote area connectivity while complementing terrestrial network coverage.

- November 2024: Equinix opened its Salalah data center facility, enhancing Oman’s position as a regional digital hub and providing carrier-neutral colocation services for international connectivity and cloud services.

- October 2024: Oman Data Park signed a USD 450 million MoU with INTRO Technology to establish the Kemet Data Center in the Suez Canal Economic Zone, spanning 80,000 sqm and focusing on cloud solutions, IoT, and digital-transformation services for African and Middle-Eastern markets.

- October 2024: Omantel completed a comprehensive digital-transformation project with Optiva, migrating over 200 products and services to a cloud-native charging platform on private-cloud infrastructure, enabling GenAI and 5G service innovations for more than 3 million customers.

Oman Telecom MNO Market Report Scope

Telecom or Telecommunication is the long-range transmission of information by electromagnetic means.

Oman's Telecom MNO Market includes in-depth trend analysis based on connectivity like Fixed Networks, Mobile Networks, and Telecom Towers. The Oman telecom MNO market is segmented by services (voice services (wired and wireless), data and messaging services, and OTT and pay-tv services).

The market sizes and forecasts regarding value (USD) for all the above segments are provided.

Service Type

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

End-user

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

How large is the Oman telecom MNO market in 2026?

The market is valued at USD 2.86 billion in 2026 and is projected to reach USD 3.80 billion by 2031.

What CAGR is expected for Oman’s mobile-network operators through 2031?

Revenue is forecast to rise at a 5.88% CAGR, driven by 5G adoption and enterprise digitalization.

Which service type contributes the most revenue?

Data and internet services account for 50.12% of total 2025 revenue, far outpacing voice and messaging.

Who are the major players and their shares?

Omantel and Ooredoo together held roughly 78% of subscriptions in 2024, while Vodafone secured 12% after its 2022 entry.

What role do submarine cables play in Oman's telecom sector?

Hosting more than 20 subsea systems positions Oman as a wholesale connectivity hub, generating stable international revenue streams, especially through Omantel’s 100+ interconnects.

Page last updated on: