Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 153.83 Billion |

| Market Size (2026) | USD 159.8 Billion |

| Market Size (2031) | USD 193.34 Billion |

| Growth Rate (2026 - 2031) | 3.88% CAGR |

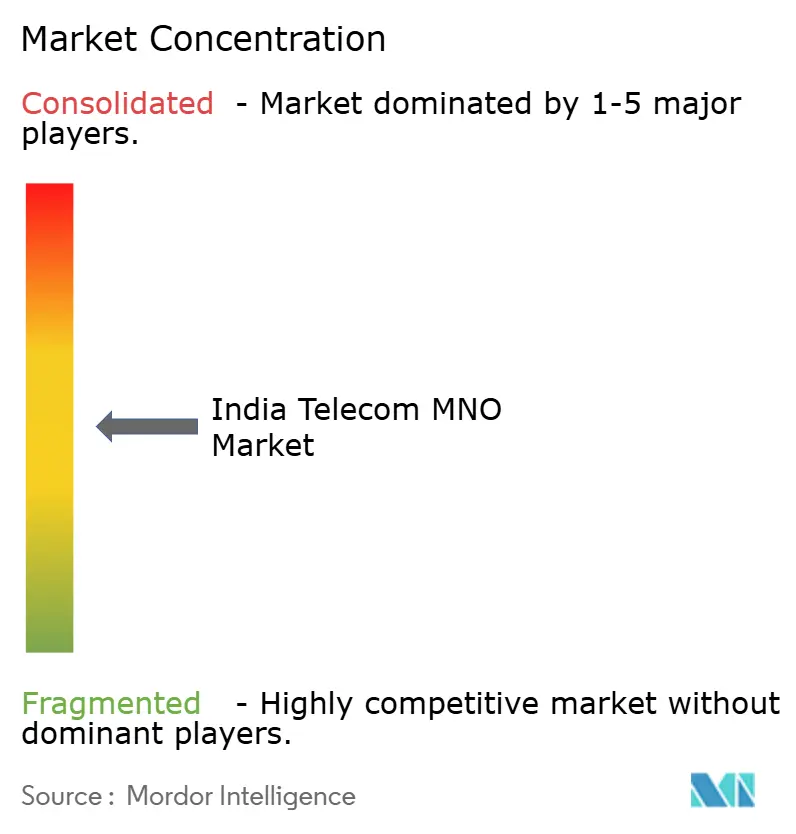

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Telecom MNO Market Analysis by Mordor Intelligence

The India Telecom MNO market size is expected to grow from USD 153.83 billion in 2025 to USD 159.8 billion in 2026 and is forecast to reach USD 193.34 billion by 2031 at 3.88% CAGR over 2026-2031.

This advance is paced by sustained mobile-data consumption, enterprise digital-transformation demand, and the ongoing shift from volume growth to value-focused service innovation. Data and Internet Services already account for 60.11% of revenue, propelled by per-subscriber usage that averages 30 GB each month across 490 million active connections. Voice Services still generate 16.98% of revenue as 2G/3G sunsets accelerate VoLTE adoption, while bundled OTT content and cloud add-ons lift average revenue per user across urban cohorts. Enterprise customers are emerging as the fastest-growing buyer group, with private 5G, edge connectivity, and managed cloud services underpinning a 4.29% CAGR in B2B revenue. Competitive intensity remains high because three operators command more than 90% share, yet differentiation has shifted toward network quality, ecosystem depth, and AI-driven service portfolios.

Key Report Takeaways

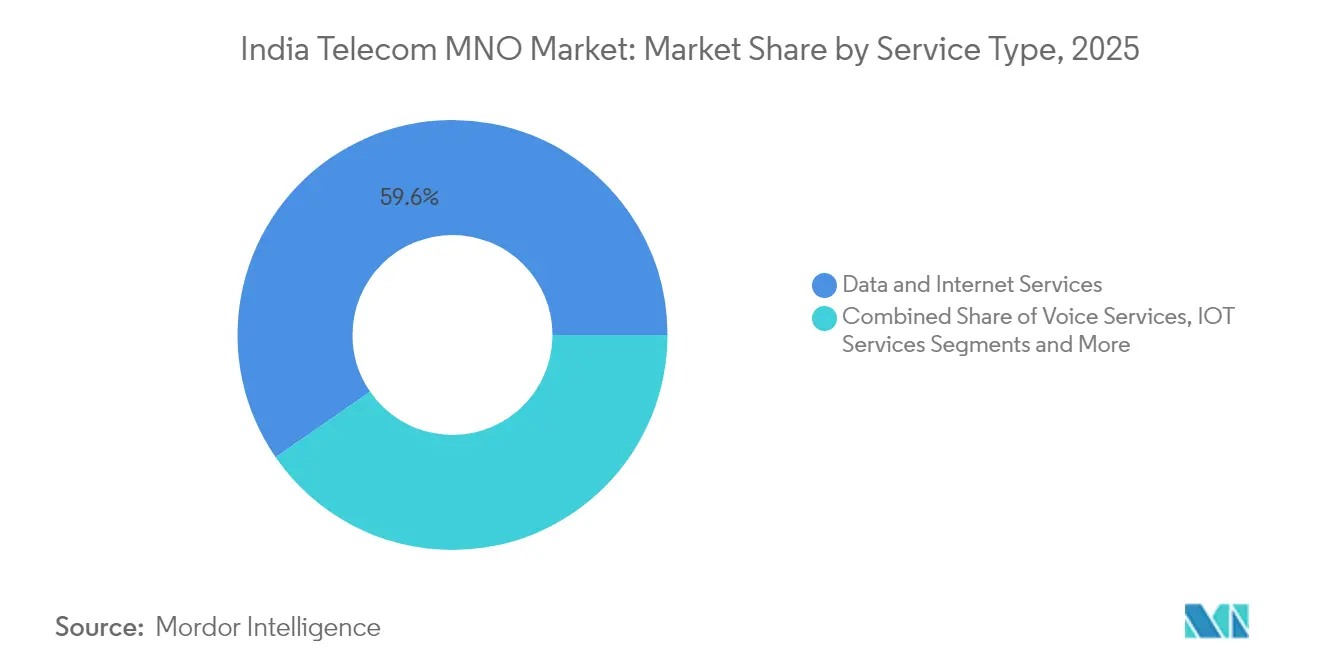

- By service type, Data and Internet Services led with 59.62% of India telecom MNO market share in 2025.

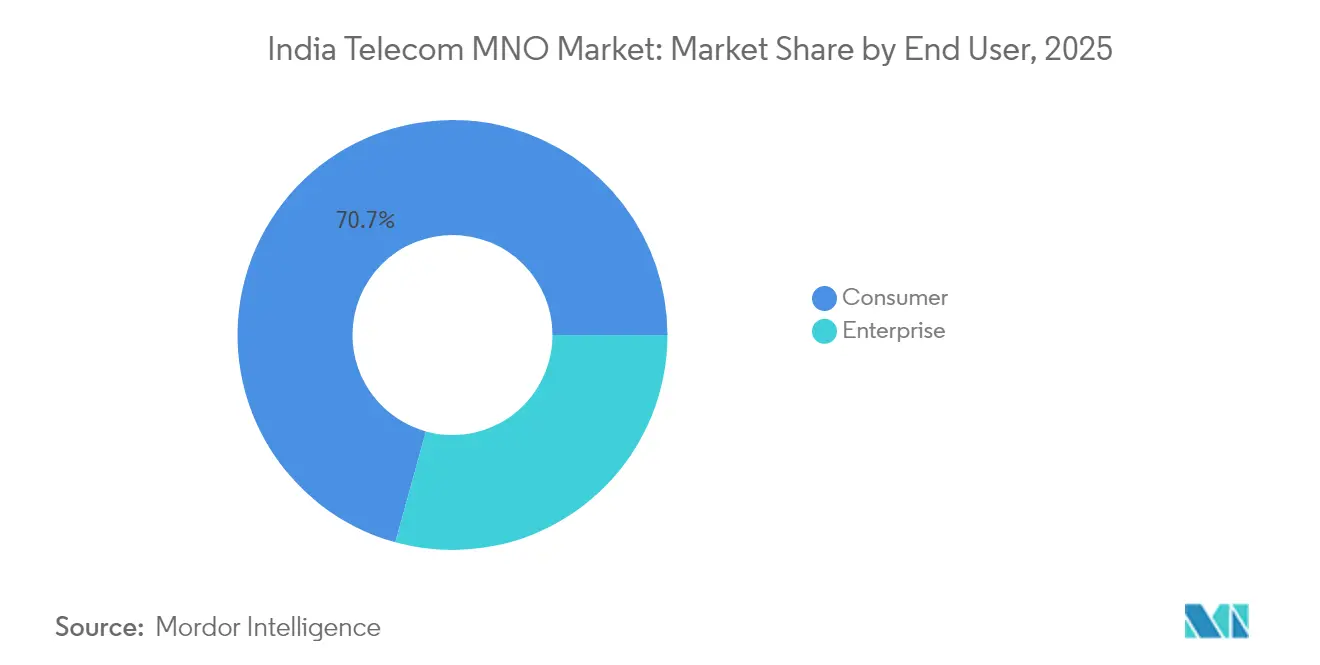

- By end user, the Enterprise segment is projected to expand at a 4.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging mobile-data traffic fueled by low-cost 4G/5G plans | +1.2% | National; strongest in Tier-2 and Tier-3 cities | Medium term (2-4 years) |

| Digital India and BharatNet programs widening broadband reach | +0.8% | Rural and semi-urban districts | Long term (≥ 4 years) |

| Falling smartphone ASPs expanding addressable base | +0.6% | Nationwide, low-income cohorts | Short term (≤ 2 years) |

| Enterprise appetite for private 5G and edge connectivity | +0.9% | Metro clusters and industrial corridors | Medium term (2-4 years) |

| eSIM and multi-IMSI uptake in IoT devices | +0.3% | Smart-city and industrial IoT zones | Long term (≥ 4 years) |

| Bundled OTT content driving ARPU uplift | +0.4% | Urban and semi-urban circles | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging mobile-data traffic fueled by low-cost 4G/5G plans

Average monthly consumption has hit 30 GB per user, and Jio alone carries 8% of global mobile traffic, validating India’s data-centric trajectory. Scale economics now let operators monetize incremental gigabytes through cloud, gaming, and AI-enhanced services while sustaining network reinvestment. Fixed-wireless access (FWA) subscriptions are set to surpass 10 million by end-2025, creating an alternative broadband path in underserved zones. The combination of affordable pricing and dense 5G roll-outs positions the India telecom MNO market to pioneer data-intensive consumer and industrial applications.[1]ET Telecom, “Bharti Airtel's arm launches sovereign cloud for enterprises,” telecom.economictimes.indiatimes.com

Digital India and BharatNet programs widening broadband reach

Public-sector fiber backbones lower the marginal cost of rural roll-outs, letting private carriers extend 4G/5G to villages that were previously uneconomical. BSNL’s state-funded 4G build—targeting 100,000 sites by March 2025—illustrates how government stimulus de-risks private capital while anchoring demand from e-health, agri-tech, and e-learning initiatives. Compliance with India-resident data rules adds parallel demand for locally hosted cloud and connectivity, pulling the India telecom MNO market into new revenue pools.[2]ET Telecom, “Jio Platforms teams up with AMD, Cisco, Nokia,” telecom.economictimes.indiatimes.com

Enterprise appetite for private 5G and edge connectivity

Factory automation pilots show 40–60% efficiency gains, prompting full-scale deployments in automotive, logistics, and healthcare facilities. Operators now package spectrum, MEC, and managed security as turnkey offerings, lifting B2B ARPUs well above consumer levels. BSNL’s network-as-a-service model and Airtel’s sovereign-cloud launch exemplify the pivot toward margin-rich enterprise portfolios that elevate the overall India telecom MNO market.

Bundled OTT content driving ARPU uplift

Operator-content alliances have created sticky bundles that defend market share and justify tariff premiums. The OTT and PayTV category already contributes 6.91% of revenue, and integrated billing plus exclusive sports rights are lifting churn-adjusted ARPU in metro circles. Deeper user-behavior data further supports ad monetization strategies, reinforcing the flywheel effect within the India telecom MNO market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated debt loads limiting operator capex | -0.7% | Nationwide; acute for Vi | Medium term (2-4 years) |

| High spectrum costs and sector-specific levies | -0.5% | National | Long term (≥ 4 years) |

| Municipal right-of-way delays for fiber | -0.3% | Urban civic bodies | Short term (≤ 2 years) |

| Rising data-localization compliance costs | -0.2% | Enterprise hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Elevated debt loads limiting operator capex

Vodafone Idea’s USD 27 billion debt and stalled fund-raise underscore a financing overhang that defers 5G roll-outs and erodes competitiveness. High leverage tightens cash flows, prioritizes short-term ARPU over long-range innovation, and lets better-capitalized peers win premium subscribers—constraining the broader India telecom MNO market.[3]ET Telecom, “Centre, Trai dismiss telecom companies’ revenue fears on satcom,” telecom.economictimes.indiatimes.com

High spectrum costs and sector-specific levies

Licensing fees and auction premiums absorb double-digit shares of operator revenue, curbing reinvestment capacity, particularly for rural 5G coverage where payback periods are longer. While treasury receipts rise, the drag on network modernization shaves potential CAGR points off the India telecom MNO market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Lead Solidifies Digital Dominance

Data and Internet Services delivered 59.62% of 2025 revenue, confirming their primacy in the India telecom MNO market. The segment is tracking a 3.82% CAGR as urban saturation balances rural onboarding. 5G FWA uptake underpins outsized momentum, while robust fiber backhaul accelerates gigabit-class offerings. Voice still holds 16.74% revenue; yet VoLTE lowers cost-per-minute, preserving cash flow. IoT and M2M Services, though only 5.06% of revenue, post a 3.93% CAGR and benefit from 32% YoY cellular-module shipment growth. OTT and PayTV contribute 6.85% with a 3.84% CAGR, boosted by exclusive sports content.

Operators leverage data analytics to curate prepaid bundles, microtarget rural cohorts, and upsell cloud storage. Competitive differentiation pivots on latency, consistent throughput, and platform openness for third-party apps. Regulatory clarity on satellite backhaul encourages hybrid connectivity, expanding addressable households. Altogether, these shifts keep the India telecom MNO market on a steady value-accretion path despite moderating subscriber additions.

By End User: Enterprise Growth Outpaces Consumer Saturation

Enterprises generated 29.28% of 2025 revenue and are on a 4.12% CAGR trajectory, reflecting appetite for private 5G, MEC, and cybersecurity bundles. Telecom APIs for billing, identity, and messaging open incremental monetization lanes, and WhatsApp Business price cuts spur CPaaS adoption. BSNL pursues a 15% enterprise revenue jump next year via network-as-a-service.

The consumer base, still 70.72% of revenue, grows at 3.67% CAGR. Urban users demand seamless content plus cloud backups, while rural cohorts join via low-cost smartphones and BharatNet extensions. Convergence of work-from-anywhere lifestyles blurs segment lines, letting operators remix tariffs, loyalty schemes, and fintech add-ons. That evolution keeps the India telecom MNO market resilient even as net-additions slow.

Geography Analysis

Metro circles contribute the bulk of value, yet incremental growth tilts toward Tier-2 and Tier-3 cities where smartphone adoption curves remain steeper. Northern and Western regions, led by Delhi, Mumbai, and Gujarat, account for more than one-third of India telecom MNO market size. Southern circles post the highest data ARPU because of earlier 5G roll-out and affluent subscriber profiles.

Rural villages gain coverage through shared infrastructure and USOF subsidies. Fiber kilometers per capita rose notably after BharatNet Phase II, enabling small-cell densification that cuts backhaul costs. The east, historically underserved, is catching up as operators bundle FWA with content in Bengali and Odia languages. Jammu & Kashmir and Northeast show limited but strategic deployments that support defense and tourism.

Regulatory incentives such as reduced license fees for remote areas encourage build-outs, while satellite backhaul experiments promise leapfrog gains for islands and high-altitude zones. These moves collectively expand geographic inclusivity, ensuring the India telecom MNO market remains a nationwide growth story rather than an urban-centric opportunity.

Competitive Landscape

Reliance Jio, Bharti Airtel, and Vodafone Idea hold more than 90% combined share, giving the India telecom MNO market a high-concentration profile. Jio leverages scale economics to price aggressively and cross-sell digital apps, while Airtel pursues premium positioning via network quality and B2B cloud depth. Vodafone Idea struggles with capital constraints yet preserves pockets of loyalty through differentiated content bundles.

BSNL’s state-funded 4G and planned 5G roll-out inject a public-sector dynamic; 50,000 indigenous 4G sites were active by late 2024 and a further 50,000 are on track for mid-2025 completion. Strategic partnerships—Jio with AMD/Cisco/Nokia on a Telecom-AI stack, Airtel with Singtel and Google Cloud on sovereign services—underscore technology as a battlefield. Satellite tie-ups with SpaceX position carriers to diversify backhaul and address untapped households.

M&A speculation lingers around fiber holdings and tower portfolios as operators monetize assets to fund 5G densification. Device financing, fintech, and ad-tech spin-offs deepen ecosystem moats. Together, these vectors elevate competition from pure connectivity into integrated digital-platform rivalry, shaping long-term trajectories for the India telecom MNO market.

India Telecom MNO Industry Leaders

Reliance Jio Infocomm

Bharti Airtel

Vodafone Idea Limited

Bharat Sanchar Nigam Limited (BSNL)

Mahanagar Telephone Nigam Ltd. (MTNL)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Bharti Airtel’s Xtelify unit launched an AI-powered cloud platform for enterprises, partnering Singtel, Globe, and Airtel Africa to improve operations across 590 million touchpoints.

- July 2025: BSNL unveiled its 5G network-as-a-service blueprint, planning 19,000 additional sites and a 15% enterprise revenue lift.

- June 2025: Government and TRAI dismissed operator fears of satellite cannibalization, noting Starlink’s small data capacity and higher price points.

India Telecom MNO Market Report Scope

The telecom industry comprises the sales of telecom goods and services by companies (organizations, single proprietorships, and partnerships) that supply communication hardware equipment for transmitting voice, data, text, and video. The telecoms market includes the sales of items by manufacturers like GPS equipment, cellular phones, and switching equipment.

The telecom MNO industry in India is segmented by services (voice services (wired and wireless), data and messaging services, and OTT and pay TV services).

The market sizes and forecasts are provided in value (USD) for all the above segments.

Service Type

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

End-user

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

Why is VoLTE important to operators?

VoLTE frees legacy spectrum, lowers cost per minute, and supports high-definition voice without separate circuit-switched networks.

What challenges limit faster 5G expansion?

High spectrum fees and operator debt loads restrict capital spending, particularly for Vodafone Idea.

How many 5G base stations are active nationwide?

Operators have deployed about 460,000 5G sites, covering 779 districts.

What is driving enterprise demand?

Private 5G networks, edge computing, and managed cloud services are fueling a 4.12% CAGR in enterprise revenue.

Page last updated on: