Yemen Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

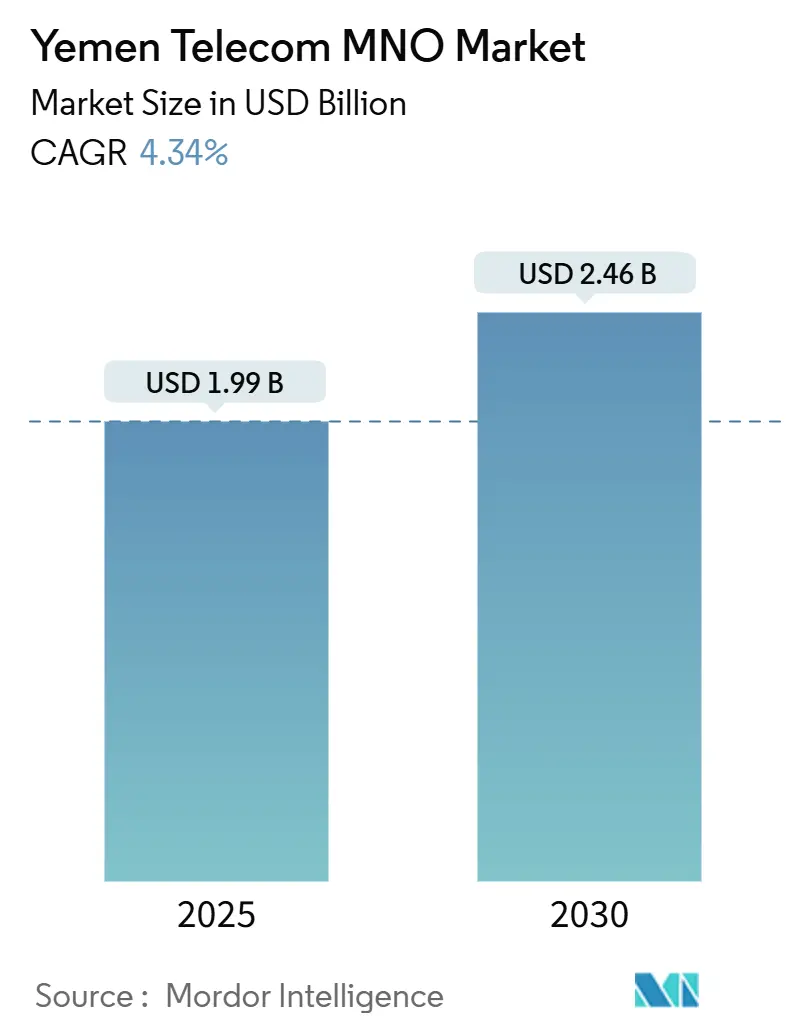

| Market Size (2025) | USD 1.99 Billion |

| Market Size (2030) | USD 2.46 Billion |

| Growth Rate (2025 - 2030) | 4.34% CAGR |

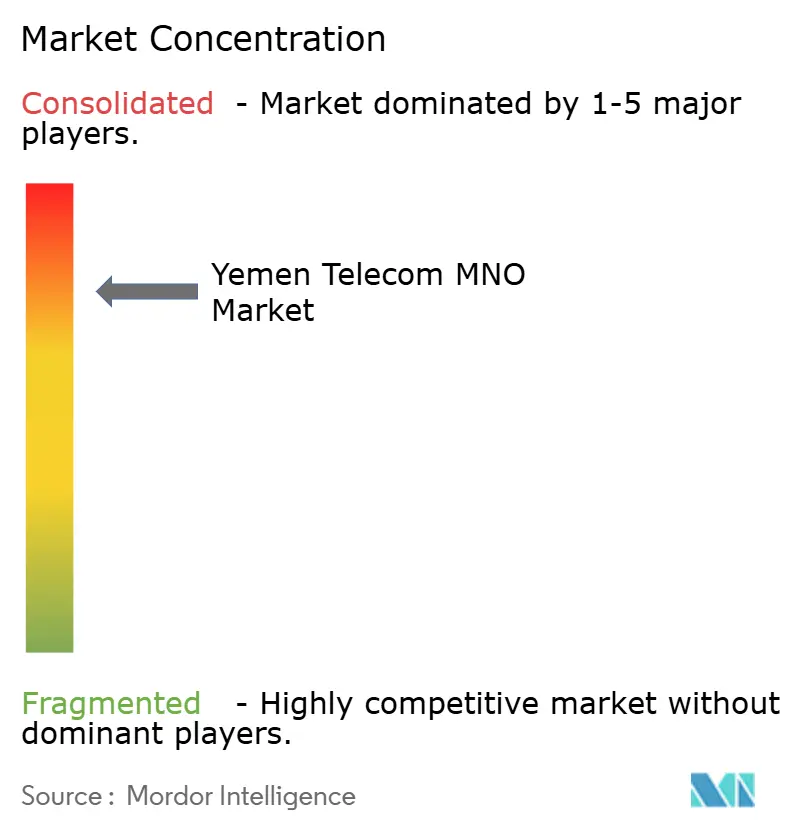

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Yemen Telecom MNO Market Analysis by Mordor Intelligence

The Yemen Telecom MNO Market size is estimated at USD 1.99 billion in 2025, and is expected to reach USD 2.46 billion by 2030, at a CAGR of 4.34% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 20.30 million Subscribers in 2025 to 24.70 million Subscribers by 2030, at a CAGR of 4.30% during the forecast period (2025-2030).

The outlook demonstrates how the Yemen Telecom MNO market continues to expand despite conflict-related infrastructure losses that touched USD 4.1 billion between 2015 and 2019. Sustained growth is fueled by rapid smartphone uptake among the under-25 cohort, humanitarian-funded backbone repairs that restore damaged fiber routes, and aggressive 4G rollouts by AdenNet and YOU in southern governorates. Competitive pressure has intensified after the September 2024 launch of Starlink, which introduced satellite broadband options that bypass terrestrial networks. [1]Arab News, “Starlink rolls out satellite internet in Yemen,” arabnews.comRevenue diversification through mobile money, airtime-based remittances, and data-hungry OTT entertainment further supports the Yemen Telecom MNO market, even as operators navigate forex shortages and a single-cable international bandwidth constraint.

Key Report Takeaways

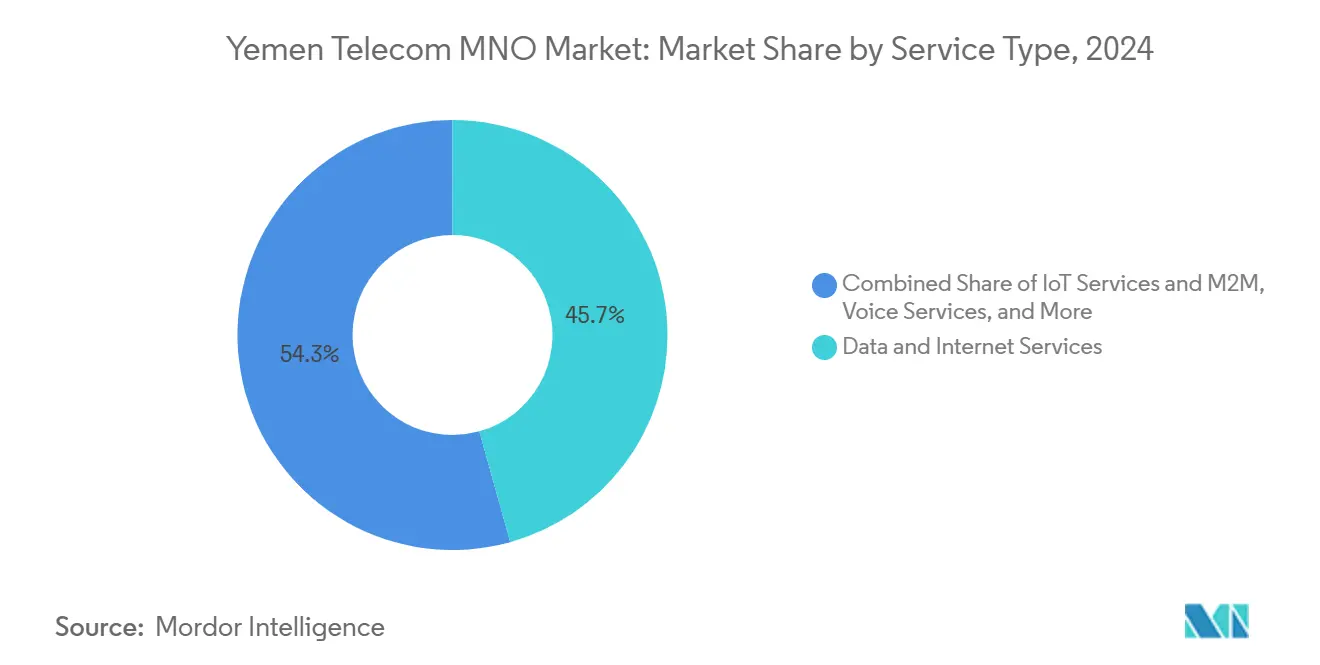

- By service type, data and internet services held 45.68% of the Yemen Telecom MNO market share in 2024, while “other services” led growth with a 4.45% CAGR forecast through 2030.

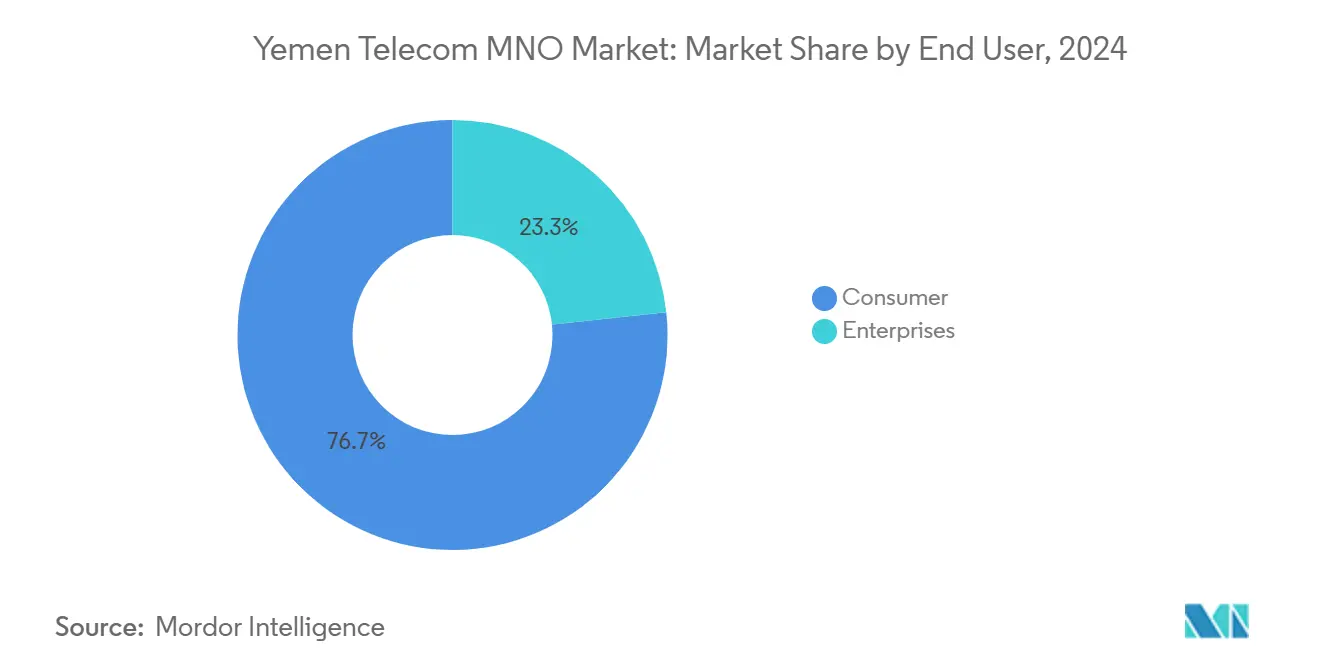

- By end-user, consumer subscriptions accounted for 76.69% of the Yemen Telecom MNO market size in 2024, whereas enterprise connections are projected to expand at a 4.77% CAGR during 2025-2030.

Yemen Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive smartphone adoption among under-25 | +1.2% | Urban centers nationwide | Medium term (2-4 years) |

| Rapid 4G expansion by AdenNet and YOU | +0.8% | Southern governorates | Short term (≤ 2 years) |

| Humanitarian-funded backbone restoration | +0.6% | Conflict-affected regions | Long term (≥ 4 years) |

| Rising demand for mobile money and remittance | +0.9% | Rural and underbanked zones | Medium term (2-4 years) |

| Data-hungry OTT entertainment consumption | +0.7% | Major cities with reliable coverage | Short term (≤ 2 years) |

| Government e-services migration push | +0.5% | Government-controlled territories | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive Smartphone Adoption Among Under-25 Population

Two-thirds of Yemen’s population is below 25, and this demographic now regards smartphones as primary gateways to education, employment, and social life. Operators committed to 4G coverage are rewarded with sustained data traffic that replaces traditional voice calls and SMS. Smartphones also underpin mobile wallet usage because formal banking penetration remains low. The market response underscores how the Yemen Telecom MNO market captures incremental revenue by tailoring affordable data bundles for youth while integrating digital payment features. [2]United Nations Development Programme, “Yemen Human Development Update 2025,” undp.org

Rapid 4G Expansion by AdenNet and YOU in Southern Governorates

The USD 93 million Huawei-built AdenNet system that went live in 2018 triggered a chain reaction of competitor upgrades across Aden, Lahij, and Abyan. Fresh 4G sites reduce the North-South bandwidth gap and let southern subscribers access video streaming and cloud-based work tools. YOU’s concurrent deployments add price competition that pressures Yemen Mobile and Sabafon to modernize their own radio networks. Faster rollouts in government-held territory highlight how geographic stability attracts investment capital to the Yemen Telecom MNO market, even during conflict. [3] Emarat Al Youm, “AdenNet 4G network boosts southern Yemen connectivity,” emaratalyoum.com

Humanitarian-Agency-Funded Backbone Restoration Projects

Since 2015, the Emergency Telecommunications Cluster and allied NGOs have funded fiber repairs and microwave relief links that keep mobile networks live during outages. Restored backbones lower congestion on the country’s only international gateway and create redundancy against sabotage. Such projects prove that social welfare budgets can dovetail with commercial infrastructure goals because repaired routes later handle fee-based traffic once the crisis eases. This model gives the Yemen Telecom MNO market a long-term resilience pathway amid recurring security setbacks.

Rising Demand for Mobile Money and Airtime-Based Remittance

Diaspora transfers increasingly arrive via airtime credits that recipients convert to cash or bill payments. Regulatory latitude that lets non-banks issue e-money accelerates telecom entry into finance services. Humanitarian agencies also disburse allowances through mobile wallets, further monetizing the network. Revenue from fee-based withdrawals and merchant commissions cushions operators against ARPU erosion in voice. The World Bank has cited Yemen as a pilot case for MENA digital payment ecosystems, reinforcing the financial upside for the Yemen Telecom MNO market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Armed-conflict damage to towers and fiber | -1.8% | Nationwide, heavy in northern regions | Long term (≥ 4 years) |

| Dual taxation by Sana'a and Aden regulators | -1.1% | All operating zones | Medium term (2-4 years) |

| Severe forex shortages limiting imports | -0.9% | National | Medium term (2-4 years) |

| Single-cable international bandwidth limit | -0.7% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Armed-Conflict Damage to Towers and Fiber Routes

Repeated shelling and sabotage raise repair bills and keep capex tied to replacement rather than expansion. The USD 4.1 billion loss tally from 2015-2019 equals nearly twice the 2025 market value, a gap that highlights how destructive attacks sharply dilute investment ROI. Submarine cable cuts also stall international traffic, forcing operators to rent costly satellite bandwidth. These headwinds depress the Yemen Telecom MNO market growth outlook.

Dual Taxation by Sana'a and Aden Regulators Inflating OPEX

Operators must honor duplicate licensing, spectrum, and customs fees, effectively paying double the statutory burden. Each authority demands compliance reports, duplicate numbering plans, and localized tariff approvals, fragmenting national operations. The extra overhead squeezes EBITDA margins and delays 5G trials that would otherwise position the Yemen Telecom MNO market for technology parity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Drive Revenue Transformation

Data and internet services delivered 45.68% of the Yemen Telecom MNO market share in 2024, a reflection of consumer pivot from voice to app-based communication. The Yemen Telecom MNO market size for other services, which include value-added offerings, roaming, and IoT connections, is projected to climb at 4.45% CAGR through 2030 as enterprises demand secure VPNs and cloud access. Operators monetize this trend with tiered data packs, zero-rating educational portals, and content bundles that address OTT video demand. Voice and legacy SMS still serve rural pockets where 2G remains dominant, yet their revenue contribution is fading as data prices fall and smartphone penetration climbs. High-margin enterprise connectivity for logistics and oil installations emerges as a stabilizer because these sectors require around-the-clock telemetry and fleet monitoring links, even during security incidents. Bundling mobile money with data offers creates stickiness that lifts average revenue per user and underpins new cross-selling models within the Yemen Telecom MNO market.

Other service lines such as managed security, device insurance, and cloud hosting are set to gain relevance as government portals migrate online. The Yemen Telecom MNO industry records heightened uptake for virtual meeting applications that run on 4G where fiber is scarce. Each new value-added service mitigates churn and supports higher price points compared with plain data streams. Operators that master service orchestration therefore secure more of the Yemen Telecom MNO market size while differentiating on customer experience rather than raw bandwidth alone.

By End-User: Enterprise Growth Accelerates Digital Transformation

Consumer accounts formed 76.69% of revenues in 2024, but enterprise subscriptions will rise at a 4.77% CAGR to 2030, driven by state ministries contracting long-term connectivity and hosting deals. These contracts guarantee predictable traffic, helping operators hedge against prepaid churn in consumer segments. Fleet operators, freight forwarders, and NGOs deploy IoT SIMs for vehicle tracking and cold-chain verification, all of which demand higher SLA-bound ARPU. The Yemen Telecom MNO market size tied to enterprises thus benefits from premium plans in spite of the wider economic slowdown.

Small retailers and health clinics are also adopting mobile point-of-sale solutions to accept digital payments, feeding additional data and SMS traffic. As more ministries digitize permit issuance and records management, enterprises must maintain always-on links to government APIs, reinforcing demand for backup circuits and secure cloud gateways. This convergence lets carriers amortize capex across both retail and corporate bases, achieving a virtuous scale dynamic that supports network modernization across the Yemen Telecom MNO market.

Geography Analysis

Southern governorates led by Aden now account for the fastest subscriber additions thanks to the post-2018 4G grid that serves commerce zones, ports, and free-trade districts. The Yemen Telecom MNO market size linked to this southern corridor benefits from donor funding that underwrites tower hardening and fiber trenching. In contrast, Houthi-held northern regions face sanction-linked equipment shortages that restrict LTE expansion to urban Sana'a corridors. The imbalance forces operators to prioritize southbound investment where import logistics and regulatory approvals move faster. Starlink offers a nationwide satellite overlay that reduces the north-south disparity by letting subscribers in remote Sa'ada or Marib import user terminals and gain 150-250 Mbps downlink speeds without terrestrial hops.

Central highlands and eastern deserts remain underserved because persistent security checkpoints deter fiber crews. Operators respond with microwave trunk links that maintain basic 2G/3G backhaul for voice but limit high-definition video streaming. Yet demand for learn-from-home platforms and tele-health apps surges even in these areas whenever ceasefires allow network uptime. The Yemen Telecom MNO market captures pockets of high ARPU where humanitarian agencies station field offices that need bandwidth for data reporting and biometric distribution systems.

Cross-border initiatives spearheaded by the Saudi-Yemeni Business Council in December 2024 will introduce consortium-funded gateways that blend terrestrial and satellite links. The plan aims to lower transit costs on the Alexandria-Aden-Jeddah route, improving latency for Gulf-bound traffic and strengthening the resilience of the Yemen Telecom MNO market.

Competitive Landscape

Three carriers command more than 95% of subscribers, illustrating how the Yemen Telecom MNO market remains concentrated despite recent entries. Yemen Mobile enjoys first-mover spectrum rights and nationwide CDMA-to-LTE refarm projects that anchor 45% share. Sabafon leverages parent Beyon’s scale to import swap-out kits that lighten OPEX, while YOU positions itself as the data challenger through aggressive southern 4G expansion. All three carriers experience margin compression from dual taxes and forex losses that inflate vendor invoices, yet they seek differentiation through localized content bundles and fintech partnerships.

Starlink’s arrival changes the competitive equation by offering satellite broadband that sidesteps tower sabotage. Initial device requisition averaged 4,000 units in the first quarter of service, mostly to NGOs and SMEs requiring high-throughput back-up links. While satellite ARPU exceeds USD 100 monthly, its value proposition hinges on avoided downtime rather than price competition against 4G. Incumbents respond with fail-over SIM pairs, microwave redundancy, and public commitments to future 5G pilots framed around ITU-2024 spectrum rules.

Vendor alliances also shape rivalry. Huawei remains AdenNet’s turnkey partner, Ericsson supplies Sabafon’s core refresh, and ZTE pilots fixed-wireless terminals for YOU. These arrangements split the Yemen Telecom MNO market into distinct vendor footprints, complicating network interoperability yet allowing each carrier to negotiate supply credits that offset currency volatility. The competitive narrative therefore intertwines geopolitics, vendor diplomacy, and service innovation.

Yemen Telecom MNO Industry Leaders

Sabafon

Yemeni Omani United

Yemen Mobile

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: ITU Radio Regulations 2024 edition entered into force, guiding future 5G spectrum policy.

- December 2024: Saudi-Yemeni Business Council unveiled SAR 6.3 billion projects, including a Starlink-powered communications venture.

- October 2024: SAMENA Council analysis highlighted Yemen’s regulatory hurdles ahead of 5G adoption.

- September 2024: Starlink commenced satellite internet service in Yemen, the first such launch in West Asia.

Yemen Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

How large is the Yemen Telecom MNO market in 2025?

How large is the Yemen Telecom MNO market in 2025? The Yemen Telecom MNO market size is USD 1.99 billion in 2025 and is projected to reach USD 2.46 billion by 2030.

What is the forecast CAGR for Yemen mobile operators?

Aggregate revenue across operators is expected to advance at a 4.34% CAGR between 2025 and 2030.

Which service segment leads revenue today?

Data and internet services held 45.68% of revenue in 2024, the largest slice among all service categories.

Why is enterprise demand growing faster than consumer demand?

Government e-services and business continuity needs push enterprise connections at a 4.77% CAGR, exceeding consumer growth.

How does Starlink affect local competition?

Satellite broadband bypasses terrestrial outages, adding a premium alternative that pressures mobile operators to upgrade redundancy.

What is the main barrier to faster network upgrades?

Dual taxation from competing regulators increases operational expenses and diverts cash from capital investment.

Page last updated on: