Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.32 Billion |

| Market Size (2026) | USD 1.39 Billion |

| Market Size (2031) | USD 1.83 Billion |

| Growth Rate (2026 - 2031) | 5.61% CAGR |

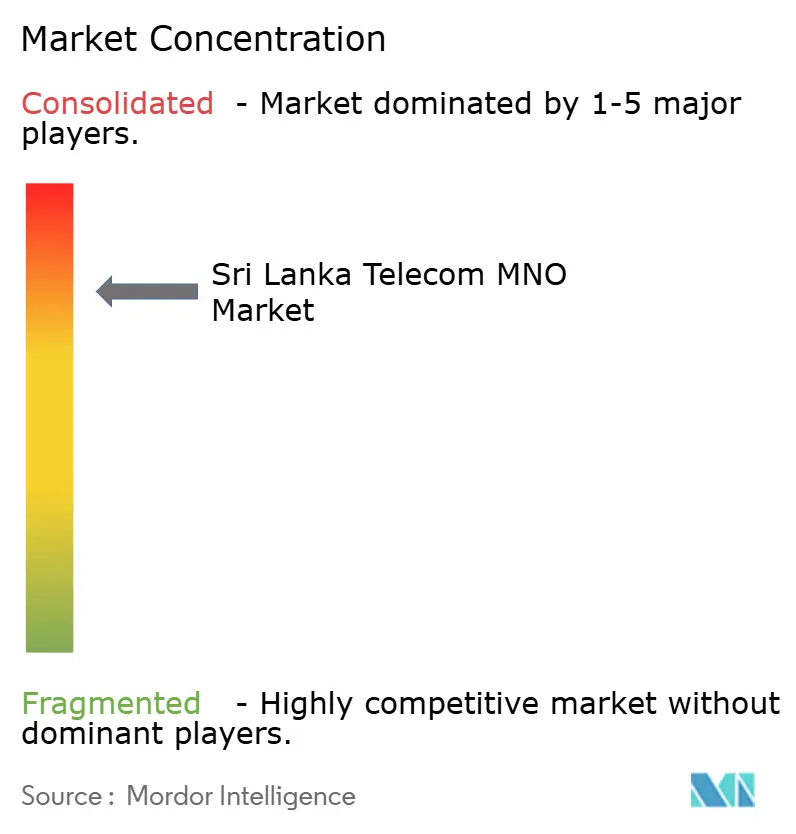

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sri Lanka Telecom MNO Market Analysis by Mordor Intelligence

The Sri Lanka Telecom MNO Market size was valued at USD 1.32 billion in 2025 and estimated to grow from USD 1.39 billion in 2026 to reach USD 1.83 billion by 2031, at a CAGR of 5.61% during the forecast period (2026-2031).

Strong 4G migration, pending 5G launches, and policy-backed digitization programs are lifting service demand even as consumer purchasing power remains constrained by inflation. Post-merger scale efficiencies are freeing cash for rural coverage build-outs, helping operators translate capacity gains into wider market reach. Enterprise cloud-connect deals with free-trade-zone manufacturers are giving the Sri Lanka telecom MNO market an additional high-margin growth lever, while national e-government projects are locking in long-term bandwidth commitments from the public sector. Against this backdrop, operators are prioritizing premium data bundles, satellite back-haul partnerships, and undersea cable resale to diversify revenue and hedge foreign-exchange risk.

Key Report Takeaways

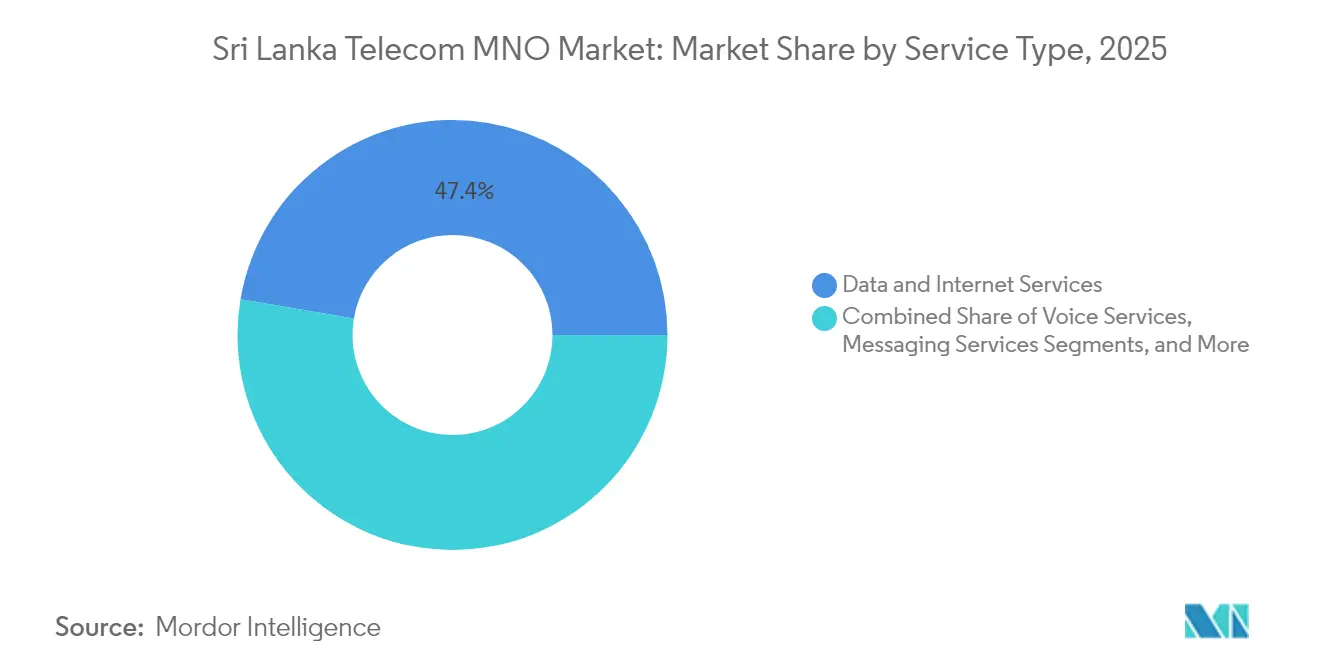

- By service type, data and internet services commanded 47.35% of the Sri Lankan telecom MNO market share in 2025; IoT and M2M services are forecast to expand at a 5.71% CAGR through 2031.

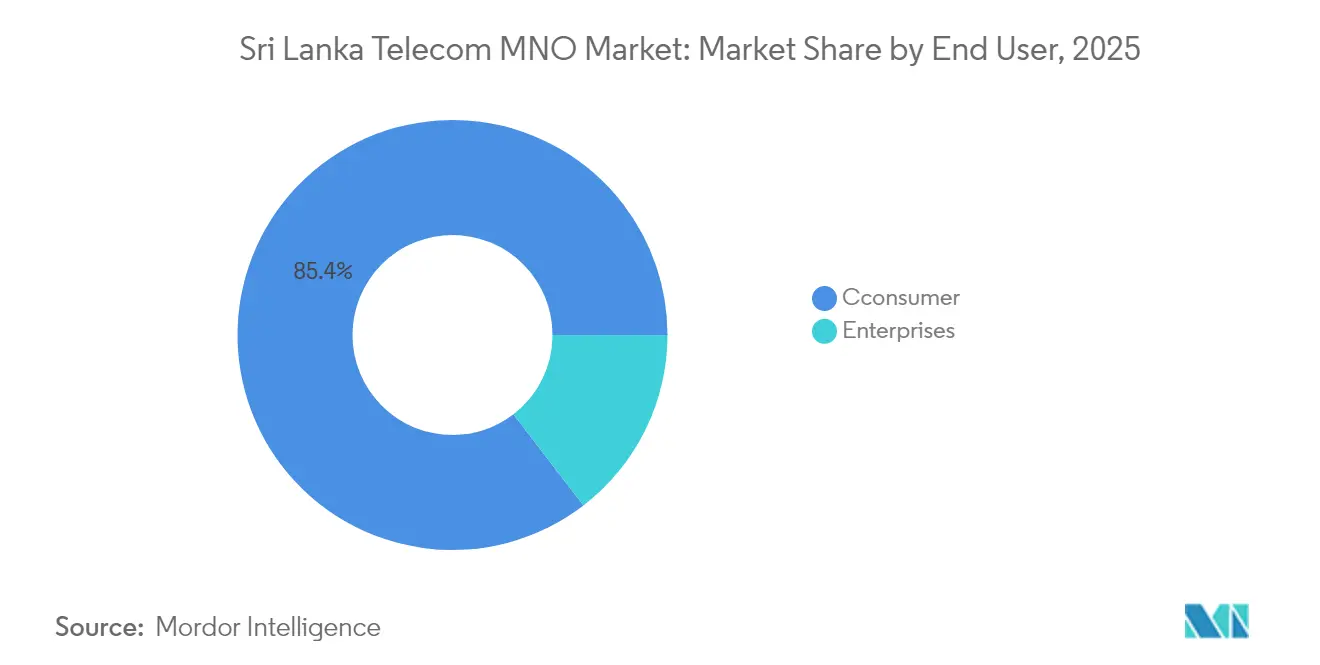

- By end user, the consumer segment retained 85.42% share of the Sri Lankan telecom MNO market size in 2025, while enterprise services are projected to grow at a 6.29% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Sri Lanka Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 4G/5G subscriber migration lifts ARPU | +1.2% | Colombo, Kandy, Galle | Medium term (2-4 years) |

| Post-merger cap-ex synergies freeing rural cash | +0.8% | Island-wide, rural districts first | Long term (≥ 4 years) |

| Government push for digital public services | +1.0% | National; early traction in Western Province | Medium term (2-4 years) |

| Enterprise cloud-connect deals in free-trade zones | +0.6% | Katunayake, Biyagama, Seethawaka | Short term (≤ 2 years) |

| Under-sea cable capacity resale to Maldives and East Africa | +0.3% | Colombo landing stations | Long term (≥ 4 years) |

| Fintech-enabled micro data bundles for informal workers | +0.4% | Urban periphery settlements | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid 4G/5G Subscriber Migration Lifts ARPU

Continued substitution of 3G connections with 4G SIMs is driving a steady rise in average revenue per user as data usage per subscriber scales past 6 GB per month [1]SLT-Mobitel, “SLT-Mobitel Crowned Fastest 4G Network,” mobitel.lk. Dialog’s first-quarter 2025 revenue climbed 20% year-on-year on the back of higher-value 4G bundles, underscoring the elasticity of demand for faster service tiers [2]Dialog Axiata PLC, “Acquisition of Airtel Lanka Completed,” dialog.lk. SLT-Mobitel’s nationally recognized 22.46 Mbps median download speed positions the carrier to convert speed-sensitive users even before full 5G commercialization. Operators have already completed multiple 5G trials topping 1.55 Gbps, signalling a near-term leap in performance that is expected to accelerate premium-tier adoption once commercial spectrum is released. Active public consultations on 5G rules by the Telecommunications Regulatory Commission ensure spectrum road-maps remain aligned with network-investment cycles.

Post-Merger Cap-Ex Synergies Freeing Cash for Rural Coverage

The 2024 amalgamation of Airtel Lanka into Dialog eliminated duplicate towers, core switches, and retail overhead, releasing roughly USD 60 million per year that is being redeployed into green-field coverage for low-population districts. SLT-Mobitel’s co-investment in the “Gamata Sanniwedanaya” rural tower program shows how freed capital is widening service footprints into historically underserved zones. Hutchison Lanka has earmarked USD 200 million through 2027 to lift population coverage to 90%, signaling industry-wide conviction that rural take-rates will be margin-accretive once scale is reached. Reduced network redundancy has also moderated wholesale bandwidth costs, allowing operators to maintain profitability in spite of elevated energy tariffs.

Government Push for Digital Public Services (e-Gov, e-Health)

Mandatory biometric enrolment for the National Digital ID, scheduled for 2026 completion, is creating predictable bandwidth demand from every divisional secretariat in the country. The ICT Agency’s Lanka Government Network refresh is provisioning symmetrical 100 Mbps links to 3,500 public-sector sites, locking operators into multi-year backbone contracts [3]ICT Agency of Sri Lanka, “Lanka Government Network Upgrade,” icta.lk . Ongoing consultations on a national AI policy outline additional data-center capacity requirements, providing revenue upside to carriers with collocated cloud platforms [4]Ministry of Digital Economy, “AI Sri Lanka Consultation Paper,” mode.gov.lk. These programs are lifting enterprise-related revenue faster than legacy consumer voice lines, cushioning operators against cyclical retail spending dips.

Surge in Enterprise Cloud-Connect Deals with Free-Trade-Zone Firms

Multinational garment and electronics exporters clustered in Katunayake and Biyagama are migrating mission-critical workloads to public cloud, triggering a spike in point-to-point data-center links and managed SD-WAN contracts. Dialog’s Tier-III facilities guarantee 99.982% uptime, a specification increasingly stipulated in supplier agreements with European buyers, giving Sri Lankan factories an on-shore alternative to Singapore colocation. Economic normalization after the 2022 crisis has reignited FDI from India, whose investors frequently bundle enterprise connectivity with conditional cloud credits, further propelling uptake. Accelerating export orders means that service-level guarantees translate directly into production continuity, making premium connectivity a non-discretionary spend item.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency-linked device import inflation | -0.9% | Rural and low-income urban communities | Short term (≤ 2 years) |

| High sector-specific taxes | -1.1% | Nationwide, all service categories | Medium term (2-4 years) |

| Delay in 700 MHz refarming | -0.7% | Rural 5G coverage corridors | Long term (≥ 4 years) |

| Chronic grid outages raising tower opex | -0.5% | Remote districts with weak grid reliability | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Currency-Linked Device Import Inflation Squeezing Uptake

Rupee depreciation has inflated CIF values for 4G and 5G smartphones by more than 30% since 2023, pushing entry-level handset prices beyond LKR 45,000 for large-screen models, a level that stalls upgrade cycles among prepaid users. The affordability gap slows migration to data-first bundles and curbs ARPU headroom. Operators have rolled out zero-interest microloans, but delinquency risks compel cautious quota allocation, limiting reach.

High Sector-Specific Taxes Dampening Demand

The combined Telecom Levy and VAT elevate effective usage charges by close to 29%, pricing marginal households out of higher-capacity packs. Dialog alone remitted LKR 14.8 billion in direct and consumption taxes during Q1 2025, diverting funds that could otherwise underwrite network densification. Elevated fiscal pressure dilutes elasticity from promotional discounts, leading operators to defer some discretionary cap-ex until taxation clarity emerges.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Cement Revenue Leadership

Data and internet services captured 47.35% of the Sri Lankan telecom MNO market share in 2025, underpinning revenue leadership as subscriber behavior pivots from voice packages to gigabyte-tiered bundles. The Sri Lanka telecom MNO market size tied to IoT and M2M connectivity is still modest, but its 5.71% CAGR positions it as a structural growth engine, especially for industrial automation and smart logistics applications.

Operators recognize that over-the-top messaging substitutes continue to cannibalize legacy SMS income; consequently, they are bundling zero-rated OTT access with premium data packs to reinforce stickiness among heavy users. Dialog Television’s direct-to-home platform, delivered under the same subscriber identity as mobile accounts, cross-sells high-definition streaming while leveraging single-sign-on convenience. SLT-Mobitel’s NB-IoT offerings, spanning smart metering and asset tracking, are building an annuity-style revenue pool whose margins exceed consumer voice lines by 600 basis points. These product strategies collectively safeguard carrier relevance as global content players intensify competition.

By End User: Enterprises Accelerate Premium Uptake

Although consumers accounted for 85.42% of 2025 revenue, enterprise clients drove a faster 6.29% CAGR, lifting their slice of the Sri Lanka telecom MNO market size by 2031. Hybrid-cloud migrations, Industry 4.0 pilots, and regulatory-mandated cybersecurity upgrades are placing sustained pressure on backbone connectivity needs, favoring operators with end-to-end managed service portfolios.

Dialog Enterprise’s 20-rack colocation expansion in 2025 improves cross-sell opportunities for MPLS, SD-WAN, and unified communications, cushioning churn risk inherent in pure-bandwidth contracts. SLT-Mobitel has responded with tiered enterprise automation bundles that integrate private LTE, IoT, and managed security, enabling single-invoice simplicity for mid-market firms. Consumer growth remains stable but susceptible to handset affordability and tax shocks; loyal-scheme discounts and micro-data bundles mitigate churn but compress per-user margins.

Geography Analysis

Rural districts absorbed 28% of new 4G subscriptions in 2025 as operators extended over 550 base stations under shared-tower models. The Sri Lanka telecom MNO market size linked to rural voice and data spending is projected to climb from USD 406.8 million in 2026 to USD 594.5 million by 2031 on the back of improving coverage reach and subsidized handset finance. Western Province retains the densest traffic volumes and is forecast to grow, supported by early 5G roll-outs and corporate campus demand clusters in Colombo Port City.

Upper-central regions continue to battle grid unreliability, compelling operators to invest in hybrid solar-diesel generator sets that inflate site opex by 14%. TRCSL’s 2025 approval of Starlink tariffs ranging from LKR 9,200 to LKR 1.8 million gives mining and agribusiness operators in isolated valleys a viable redundancy channel. Coastal townships along the Southern Expressway benefit from incremental fiber runs paralleling the highway, enabling low-latency back-haul for tourism SMEs.

Coverage density in Northern Province will hinge on 700 MHz spectrum refarming progress. Operators have requested staggered release to align depreciation schedules of legacy GSM equipment, aiming to contain capital stacks while meeting universal-service mandates.

Competitive Landscape

Following the Airtel amalgamation, the Sri Lankan telecom MNO market has transitioned to an oligopolistic structure, conferring moderate pricing power. Dialog’s 20 million-plus subscription base grants sizable economies in spectrum utilization and handset procurement, underpinning its 45% year-on-year EBITDA jump in Q1 2025. SLT-Mobitel leverages state-backed fixed-line holdings to offer attractively bundled quad-play packs, keeping churn below 2%. Hutchison’s lean cost base allows competitive unlimited-data pricing even as it races to scale 4G coverage.

Technology road-maps converge on 5G non-stand-alone deployments using existing 2100 MHz sites for expedited time-to-market. SLT-Mobitel’s collaboration with Ericsson on a “5G Island of Innovation” secures early-mover advantage in ultra-low-latency enterprise applications. Dialog’s AI-driven personalization engine, which sends dynamic content offers based on real-time usage, has lifted upsell conversion rates by 11%.

Satellite back-haul partnerships and undersea cable swaps are emerging as white-space opportunities. SLT-Mobitel’s equity stake in SEA-ME-WE-6 secures capacity resale rights that can be monetized among African operators seeking lower-latency routes into Asia, diversifying its earnings mix.

Sri Lanka Telecom MNO Industry Leaders

Dialog Axiata PLC

SLT-Mobitel (Sri Lanka Telecom PLC)

Hutchison Telecommunications Lanka (Pvt) Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: TRCSL approved five retail tariff plans for Starlink satellite broadband, launching the first licensed LEO service in Sri Lanka.

- August 2024: Dialog Axiata completed the full amalgamation of Airtel Lanka, finalizing staff integration and transferring 2*5 MHz of 1800 MHz spectrum into its national grid.

- April 2024: Dialog signed a strategic alliance with Telin to secure international voice and A2P SMS termination, reinforcing the quality of service on cross-border traffic.

Sri Lanka Telecom MNO Market Report Scope

Telecom or telecommunication is the long-range transmission of information by electromagnetic means.

Sri Lanka's telecom MNO market is segmented by services (voice services [wired and wireless], data and messaging services (coverage to include internet and handheld data packages, as well as package discounts), and OTT and servicespayTV services. The impact of macroeconomic trends on the market is also covered under the scope of the study. The impact of factors affecting the market's evolution in the near future, such as drivers and constraints, are also covered in the study. The market sizes and forecasts are provided in USD for all the above segments.

Service Type

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

End-user

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

How large is the Sri Lanka telecom MNO market in 2026?

The market’s value stands at USD 1.39 billion in 2026 and is forecast to hit USD 1.83 billion by 2031.

Which service type generates the most revenue?

Data and internet services lead with 47.35% of 2025 revenue and are growing at a 5.55% CAGR to 2031.

What is driving enterprise telecom growth?

Government digital programs and free-trade-zone cloud adoption are pushing enterprise revenue toward a 6.29% CAGR through 2031.

How did Dialog’s Airtel merger affect competition?

It reduced the market to three major players, granting Dialog scale economies that support rural expansion and premium product development.

What challenges limit 5G roll-out?

High device costs, sector-specific taxes, and delayed 700 MHz refarming collectively slow nationwide 5G coverage.

Page last updated on: