Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 13.42 Billion |

| Market Size (2026) | USD 13.95 Billion |

| Market Size (2031) | USD 16.95 Billion |

| Growth Rate (2026 - 2031) | 3.98% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Telecom MNO Market Analysis by Mordor Intelligence

The UAE Telecom MNO Market size is expected to grow from USD 13.42 billion in 2025 to USD 13.95 billion in 2026 and is forecast to reach USD 16.95 billion by 2031 at 3.98% CAGR over 2026-2031.

Sustained capital outlays in 5G stand-alone (SA) networks, wholesale fiber, and edge data centers keep the UAE telecom MNO market at the forefront of Middle East digitalization. Regulators encourage infrastructure quality instead of network overcrowding, so operators monetize premium tiers instead of pursuing price wars. Consumer demand for video streaming, mobile gaming, and ultra-reliable connectivity keeps data ARPU resilient even when voice revenues flatten. Enterprise digitization, led by oil-and-gas, logistics, and public-sector smart-city programs, steadily expands the addressable base for private 5G, IoT, and network-slice services that command higher margins.

Key Report Takeaways

- By service type, data and internet services held 46.05% of the UAE telecom MNO market share in 2025. IoT and M2M services are projected to pace the UAE telecom MNO market at a 4.02% CAGR between 2026-2031.

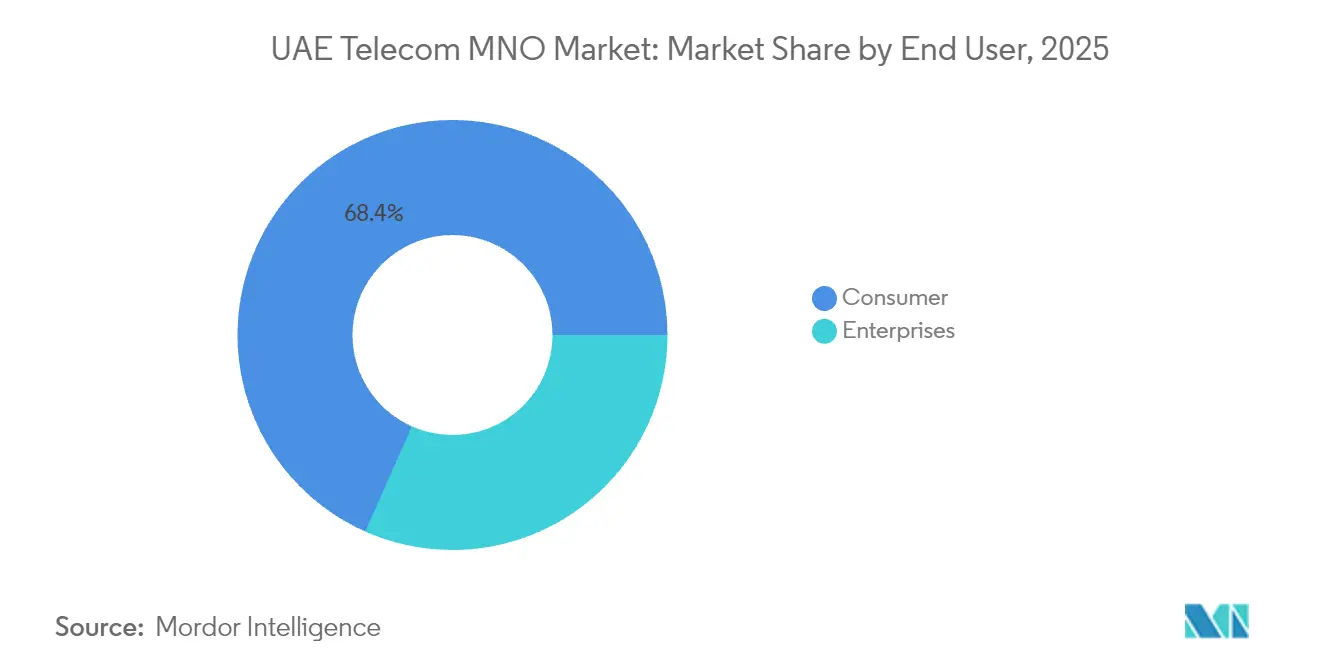

- By end user, the consumer segment accounted for 68.35% of the UAE telecom MNO market size in 2025. The enterprise segment and solutions are set to grow at a 4.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UAE Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)%Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G SA roll-out and premium-tier ARPU uplift | +1.2% | Dubai and Abu Dhabi first, then nationwide | Medium term (2-4 years) |

| Surging video-streaming and mobile-gaming demand | +0.8% | Urban centers across all seven emirates | Short term (≤2 years) |

| Enterprise appetite for private 5G / IoT connectivity | +0.7% | Industrial zones and smart-city corridors | Long term (≥4 years) |

| Fixed–mobile convergence bundles fueling upsell | +0.5% | Residential clusters countrywide | Medium term (2-4 years) |

| Government 6G R&D incentives | +0.4% | Research hubs in Abu Dhabi | Long term (≥4 years) |

| AI-driven network slicing for ultra-low latency | +0.3% | Enterprise and public-sector mission-critical networks | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

5G SA Roll-out and Premium-tier ARPU Uplift

Standalone 5G unlocks network slicing and latency guarantees that cannot be replicated on non-stand-alone deployments. e& UAE hit 30.5 Gbps under trial conditions, proving the headroom for differentiated performance tiers [1]e&, “e& UAE Sets New Record With World’s Fastest 5G Speed,” eand.com. du followed with Voice-over-New-Radio for superior call clarity on 5G radios [2]RCR Wireless News, “du Claims First 5G VoNR Launch in the UAE,” rcrwireless.comas enterprises pay a premium for deterministic latency in smart-factory and remote-operation cases, operators package bronze, silver, and gold slices with escalating SLAs. Early adopters validate the price-elasticity thesis: higher speed and assured performance lift blended mobile ARPU even when subscriber growth slows.

Surging Video-streaming and Mobile-gaming Data Demand

Consumer behavior keeps shifting toward UHD streaming, social video, and cloud gaming. du disclosed that 5G users already generate more than 60% of aggregate mobile traffic, up from a minority base in 2024 [3]Developing Telecoms, “du to Drive Development and Support for 5G-A Innovation,” developingtelecoms.com . Tourist inflows further elevate peak-hour loads; Gulf inbound visitors report consistently high 5G roaming speeds at UAE airports and leisure venues. Data-hungry use cases justify tiered unlimited plans that preserve margins, while partnerships with OTT video platforms capture incremental content revenue.

Enterprise Appetite for Private 5G / IoT Connectivity

The push for Industry 4.0 prompts manufacturers, ports, and utilities to seek dedicated 5G bands that guarantee deterministic performance and on-prem data sovereignty. e& signed with ADNOC to build the world’s largest single-site private 5G network covering upstream, midstream, and downstream assets. The regional IoT market is forecast at USD 42.8 billion in 2028, giving operators a clear runway to bundle connectivity with managed devices and analytics. Long hardware refresh cycles and stringent HSE requirements lock in multiyear revenue corridors that are less exposed to consumer churn cycles.

Fixed-Mobile Convergence Bundles Fueling Upsell

Fiber ubiquity (99.3% FTTH penetration) lets incumbents bundle 1 Gbps home broadband, post-paid mobile, and OTT TV into single-invoice packs. e&’s Neo Home at AED 399 (USD 109) adds Amazon Prime to raise perceived value. du counters with wireless-home broadband at AED 159, leveraging its LTE-5G CPE portfolio to service low-rise zones quickly. Converged bundles reduce churn and tack on incremental margin through content commissions and cloud storage add-ons. As households consolidate telecom spend, the UAE telecom MNO market benefits from higher revenue per addressable unit.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying price competition post-MNP liberalization | -0.6% | Dense urban clusters | Short term (≤2 years) |

| High federal royalty fees on operator revenue | -0.4% | Nationwide | Medium term (2-4 years) |

| Cross-border OTT substitution of legacy voice/SMS | -0.3% | International-calling corridors | Medium term (2-4 years) |

| Data-sovereignty and cybersecurity compliance costs | -0.2% | Enterprise and public-sector workloads | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Intensifying Price Competition Post-MNP Liberalization

Porting a number now completes within two working days free of charge, eliminating historic inertia that kept subscribers loyal to incumbents [4]Gulf News, “How to Switch Mobile Network Providers in the UAE Without Changing Your Number,” gulfnews.com. Promotional cashback, bonus data, and handset-bundle campaigns erode consumer ARPU just when capex intensity peaks for 5G SA. Operators counter with experience-based differentiation, speed, coverage, and digital self-care apps, to defend yields, yet the downward push on entry-level tariffs persists.

Cross-border OTT Substitution of Legacy Voice/SMS

Even though VoIP blocks apply to certain apps inside UAE borders, residents and travelers often circumvent restrictions via roaming SIMs or Wi-Fi calling in adjacent states, reducing paid international minutes. Botim’s relaunch as a GCC “ultra-app” with 90 million users illustrates how OTT ecosystems scale rapidly once a local foothold is granted [5]Khaleej Times, “UAE: VoIP App Botim to Be Relaunched; Free Calls to Continue Working,” khaleejtimes.com . As 5G lowers latency, OTT providers deliver voice and video at near-PSTN quality, pressuring incumbents to shift value toward data, cloud security, and managed collaboration tools.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Drive Market Evolution

Data and internet services captured 46.05% of the UAE telecom MNO market share in 2025, confirming that bandwidth rather than voice forms the revenue core of the UAE telecom MNO market. The UAE telecom MNO market size attributed to data services will keep expanding as 4K video, cloud gaming, and metaverse pilots move from proof-of-concept to mainstream packages. IoT and M2M post the fastest 4.02% CAGR through 2031, fueled by onshore oil facilities, automated ports, and municipality-wide smart-meter rollouts. Operators layer device management, analytics, and cybersecurity over plain connectivity to lift service take rates and margins.

Network usage patterns underscore the shift. More than 60% of du’s traffic already rides on 5G cells, a ratio that is projected to exceed 80% by 2027 as mmWave densification progresses. Voice revenues stay relevant in enterprise PBX and premium international calling, but discretionary voice is increasingly consumed via OTT. Messaging continues to decay as over-the-top chat dominates. Meanwhile, OTT and Pay TV thrive inside converged bundles, allowing carriers to recapture entertainment spend that once leaked to standalone SVOD apps. Other services, roaming packs, financial wallets, and advertising- supplement the revenue mix and smooth seasonal volatility.

By End User: Enterprise Acceleration Reshapes Revenue Mix

Consumer subscriptions still account for 68.35% of the UAE telecom MNO market size in 2025, reflecting high smartphone ownership, dual-SIM habits, and robust tourism flows. Yet enterprise contracts, though smaller in count, bring higher ARPU and are set to climb 4.28% CAGR, the quickest across any segment, through 2031. The UAE telecom MNO market aligns with national AI and industrial automation agendas, so CIOs treat 5G slices and edge compute as mission-critical utilities rather than optional connectivity add-ons.

Operators reposition themselves as transformation partners. e& enterprise bundles Azure Stack, cybersecurity SOC, and private 5G under outcome-based SLAs, locking multi-year annuities that are less sensitive to consumer price promotions. du courts SMEs with “smart office in a box” that combines SD-WAN, UCaaS, and mobile lines. As the share of B2B revenue climbs, cash-flow visibility improves, enabling a virtuous cycle of reinvestment into next-gen networks. Consumer retention tactics pivot toward lifestyle add-ons, streaming, gaming passes, and device care, buffering ARPU against discounting pressures spawned by number portability.

Geography Analysis

Dubai and Abu Dhabi anchor the UAE telecom MNO market because both emirates host dense business districts, free-trade zones, tourist magnets, and pilot corridors for autonomous mobility. They benefit from early 5G SA launches and thorough indoor coverage in malls, airports, and stadiums, pushing blended mobile speeds to 275.9 Mbps on e& and 264.1 Mbps on du according to Opensignal. The two emirates generate the bulk of enterprise contracts in oil, aviation, and financial services, so private 5G nodes, edge data centers, and cloud regions often cluster here first.

Sharjah, Ajman, Fujairah, Ras Al Khaimah, and Umm Al Quwain present different network economics. Population is more dispersed, making fiber ROI challenging; operators therefore rely on FWA-over-5G to hit broadband targets. Pay-TV bundling differentiates offers in these cost-conscious markets, while tourism inflows sustain roaming revenue on coastal resorts. State-backed infrastructure funds co-invest in towers and ducts, shortening payback for extensions into industrial zones that host cement, quarrying, and logistics plants.

Nationally, submarine cable landings at Fujairah create an east-west switch-yard that elevates the UAE telecom MNO market into a regional transit hub. Hyperscale data-center expansions, du’s USD 544 million Azure-anchored campus and G42-e&’s Khazna joint platform, ensure content proximity that reduces latency on local mobile links. Abu Dhabi’s 2025-2027 digital strategy earmarks AED 13 billion for AI-ready infrastructure, providing a guaranteed offtake for 5G slices and government cloud.

Regulatory Landscape

The UAE telecom MNO market operates under the Telecommunications and Digital Government Regulatory Authority (TDRA), with the core legal basis anchored in Federal Law by Decree No. 3 of 2003, which empowers TDRA to license operators, manage frequency spectrum, and enforce sector technical standards. In pricing, TDRA oversight is applied through the Price Control Request (PCR) process, where service providers seek approval for introducing new tariffs or changing existing prices, shaping how MNOs design premium tiers and bundles under a regulated duopoly structure.

On network and device ecosystems, TDRA Type Approval is required for telecom equipment imports and sales, tightening compliance requirements across radios, CPE, and IoT devices before market distribution. For the 2026 to 2031 period, TDRA’s UAE Spectrum Outlook (2026-2031) signals an emphasis on more flexible spectrum planning and exploring spectrum sharing approaches. The same policy direction aligns regulation with the shift from 5G to 5G-Advanced capabilities and longer-run 6G preparation, while TDRA also continues consumer protections such as interventions that curb intrusive marketing SMS practices.

Competitive Landscape

The UAE telecom MNO market remains a regulated duopoly in 2025, with e& UAE and du jointly controlling a significant share of the studied market. e& leverages scale to maintain national best-in-class scores in download speed and video experience, while du outperforms in network availability and gaming latency. Rather than price wars, both pursue technology-led differentiation. e& runs over 400 AI use cases and 160 machine-learning models for predictive maintenance, dynamic spectrum allocation, and real-time customer-experience scoring. du counters with an innovation center focused on 5G-Advanced, open RAN, and network APIs that expose quality-on-demand functions to developers.

Spectrum policy under the Telecommunications and Digital Government Regulatory Authority keeps two players balanced: each was granted mid-band and high-band blocks but pays staggered royalties tied to revenue rather than profit, encouraging efficient capex deployment instead of subscriber-count arms races. Satellite backhaul firms and neutral-host indoor providers add ancillary competition but do not challenge mass-market segments. Vertical-specific entrants, such as energy SCADA integrators, partner instead of compete, fortifying the incumbents’ channel reach.

Strategic moves highlight international diversification. In May 2025 e& took a minority stake in Caribbean operator Digicel to expand wholesale voice capacity across the Americas. Meanwhile, du deepened ties with Microsoft Azure to ensure cloud adjacency to its 5G edge nodes, securing anchor tenant economics for its data-center arm. Both place early bets on 6G testbeds, anticipating commercial readiness near 2029, thus reinforcing the UAE telecom MNO market as the GCC laboratory for next-gen connectivity.

UAE Telecom MNO Industry Leaders

e&UAE (Etisalat)

du (Emirates Integrated Telecommunications Co.)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

5G-Advanced capability upgrades and core capacity scaling create near-term whitespace for monetizable premium connectivity across both consumer and enterprise segments. In 2026, e& UAE publicized multiple step-ups in network capability, including upgrading EMIX with 400G links and enabling 4-carrier aggregation on a live 5.5G network. Operators can translate rising traffic loads into opportunities for higher-tier plans, quality-on-demand packages, and differentiated enterprise SLAs anchored in throughput and latency guarantees.

International connectivity and cloud-adjacent ecosystems also expand the addressable opportunity set beyond traditional mobile access. In 2026, du’s actions around subsea and interconnection, including partnering with Datawave to invest in the Singapore-India-Gulf (SING) submarine cable system and upgrading UAE-IX (powered by DE-CIX) to support higher-capacity interfaces (800 GE access and added 400 GE ports), strengthen the economics for content localization, enterprise connectivity, and edge-enabled services. Alongside this, TDRA’s UAE Spectrum Outlook (2026-2031) provides an enabling backdrop for spectrum planning flexibility and sharing mechanisms, supporting new commercialization models around advanced bands, private networks, and IoT/M2M growth areas already highlighted within the UAE’s enterprise digitization programs.

Recent Industry Developments

- July 2026: e& agreed to sell its entire 16.21% stake in Vodafone Group for USD 5.95 billion, ending the relationship agreement between the two companies. The divestment frees capital and management focus for infrastructure priorities that align more directly with UAE network upgrades, enterprise services, and adjacent digital platforms.

- June 2026: du launched du Ventures, a USD 50 million corporate venture fund in partnership with Shorooq, targeting investments in digital technologies. The venture fund formalizes a pipeline for ecosystem participation beyond connectivity, supporting new product formation in areas such as software, data, and platform services that can be bundled with MNO assets.

- May 2025: du and Microsoft signed an AED 2 billion (USD 544 million) agreement to develop a hyperscale data center in the UAE. The build-out strengthens cloud adjacency for operator networks, enabling lower-latency enterprise offerings and anchoring wholesale and edge use cases tied to 5G and fixed-mobile convergence bundles.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers telecom mobile network operator revenue generated inside the United Arab Emirates from core connectivity and related service categories that are billed to end users.

Scope exclusions: We exclude pure device hardware sales and one time network build EPC style project revenue that is not recorded as telecom service revenue.

Segmentation Overview

- Overall Telecom Revenue and ARPU

- Service Type

- Voice Services

- Data and Internet Services

- Messaging Services

- IoT and M2M Services

- OTT and PayTV Services

- Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.)

- End-user

- Enterprises

- Consumer

Data Sources, Market Sizing, and Validation

Desk Research

Desk research set the baseline for UAE telecom demand and supply conditions, and it also helped us keep assumptions consistent across years. We referenced public UAE sector releases and statistical series such as Telecommunications and Digital Government Regulatory Authority publications, UAE government open data, ITU indicators, World Bank datasets, and GSMA country factsheets, which are useful to anchor penetration, usage, and coverage trends.

To tighten the commercial view, we also used operator annual reports, investor presentations, and audited financial statements, followed by press releases and reputed business media for updates on tariff actions and network milestones. A paid subscription for company financials and intelligence was used to standardize reported line items, and an import export shipment level database was selectively checked to sanity test network equipment cycle timing. These desk sources are not exhaustive, and many other public documents were also reviewed for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on validating what drives service revenue in the UAE, where a few operators and channel ecosystems shape pricing and bundles. We spoke with operator side leaders, enterprise telecom buyers, distributors, and industry advisors across the UAE to confirm ARPU direction, subscriber mix, and the pace of 5G monetization, and then we used those inputs to adjust desk based assumptions where gaps were found.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 12% | |

| Mid tier: 49% | Functional/Unit leaders: 42% | |

| Smaller Players: 19% | Managers: 46% |

Market-Sizing & Forecasting

The market model starts from a top-down reconstruction of the UAE telecom revenue pool, where subscriber base by service type and ARPU patterns are applied to arrive at annual value, and then split checks are applied across voice, data and messaging, and OTT and pay-TV services. Once that total was built, selective bottom-up approximations were used to corroborate it, such as operator reported service revenue roll ups, sampled plan pricing versus active subscriber mix, and channel checks on enterprise contract behavior.

Key inputs used in the model include mobile and fixed subscriber counts, smartphone and broadband penetration, ARPU and bundle mix shifts, data consumption trends per user, and the timing of 5G coverage and adoption milestones. Where a variable was not consistently available in public series for each year, the gap was handled with short run interpolation anchored to operator disclosures, followed by interview led reasonableness checks.

Forecasting was carried out using scenario analysis supported by simple time series smoothing on ARPU and subscriber growth, and then stress tested against primary feedback on price competition, premium plan uptake, and enterprise demand. When the direction of one driver could change the total meaningfully, assumptions were revisited and adjusted until the market path remained explainable and repeatable.

Data Validation & Update Cycle

Outputs were validated through triangulation across demand indicators, operator financial disclosures, and regulatory statistics, so the total does not rely on one data stream. Outliers were flagged when year to year movements did not align with known tariff changes, subscriber shifts, or major network events, and then the underlying drivers were rechecked before sign off.

Reports are refreshed annually, and interim updates are made when a material event occurs such as a large pricing move, a major regulatory change, or a sharp shift in subscriber mix. Before delivery, we run a fresh pass on the key assumptions and recalculate tables so clients receive the most current view available at the time of publication.

Mordor Intelligence's the United Arab Emirates Analysis of the Telecom Sector Market Size Compared Against Other Published Estimates

Published UAE telecom market values often differ because analysts do not always count the same revenue lines, and the service mix can be treated differently across mobile, fixed, and bundled offerings. The year used for currency timing, the handling of promotional pricing, and how forecasts assume ARPU progression also create visible gaps.

The main gap comes from scope, where some estimates fold in a broader national telecom market definition that mixes ISP only revenue and adjacent digital services, while Mordor Intelligence counts the UAE telecom MNO market using operator led service revenue across voice, data and messaging, and OTT and pay-TV services, supported by subscriber and ARPU based build ups. Differences also show up when aggressive cases assume faster 5G monetization or do not reconcile revenue paths with penetration and usage signals that can be cross checked in public UAE statistics.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 13.42 B (2025) | |

| Industry Research Publisher A | USD 11.76 B (2025) | Uses a broader telecom services scope that explicitly spans fixed line, mobile, and broadband connectivity across sectors, which can treat operator and ISP revenue pools differently versus an MNO focused revenue build. |

| Market Platform B | USD 9.67 B (2025) | Provides limited visible inclusion rules on the accessible summary, and the lower value can come from narrower counted service lines and different handling of OTT and pay-TV revenue, along with alternate currency timing assumptions. |

Looking across the three figures, most of the spread is explained by what is counted as telecom revenue in the UAE and how bundle economics are translated into ARPU and service revenue. By keeping the drivers tied to observable subscriber and pricing signals, the estimate stays easier to follow, recheck, and update when the market shifts.

Key Questions Answered in the Report

How big is the UAE telecom MNO market in 2026?

The UAE telecom MNO market size stands at USD 13.95 billion in 2026 and is projected to reach USD 16.95 billion by 2031.

What is the forecast CAGR for UAE telecom through 2031?

Industry revenue is expected to grow at a 3.98% CAGR over the 2026-2031 period.

Which service category holds the largest UAE telecom MNO market share?

Data and internet services lead with 46.05% market share in 2025 thanks to widespread 5G and fiber coverage.

Which segment is growing fastest inside UAE telecom?

IoT and M2M log the highest growth, expanding at a 4.02% CAGR through 2031 as enterprises deploy Industry 4.0 solutions.

Who are the main players in UAE telecom?

E& UAE and du dominate, together capturing 97.5% of sector revenue under a regulated duopoly.

Why is 5G SA important for UAE operators?

5G stand-alone enables network slicing and ultra-low latency that let operators sell premium connectivity tiers to enterprises and consumers.

Page last updated on: